1. Introduction

Following the growing evidence on the necessity to accomplish environmentally sustainable economic development, the study of the governance and exploitation of natural resources gained prominent role in economics and the social sciences, ever since Elinor Ostrom’s seminal contribution in 1990 [

1,

2,

3,

4,

5,

6]. Common goods are deductible and non-excludable, hence characterized by a high degree of rivalry in consumption and/or utilization and, at the same time, by a low degree of excludability for the whole collection of subjects interested in or allowed to use and/or consume the good. Common goods appear as private goods to outsiders, but are common goods for insiders.

Common-pool natural resources (CPRs) are studied to highlight the necessity to limit exploitation of fringe and flow resources to a level that does not damage the productive potential of the stock, or core resource. Institutional mechanisms identified in rules regulating access and management are needed to enforce appropriation rights and their limits [

7]. This research stream came to concentrate on self-managed common property regimes, which cannot be simply equated either to public or to private ownership, but share some features of both, and have been understood as the most typical way in which natural resources are managed and exploited [

1]. More recent literature concentrated on forms of communitarian ownership generating positive externalities as they concern knowledge/cultural commons [

3], and urban spaces [

8,

9].

Mechanisms governing the use and exploitation of common resources and the resolution of conflict thereof have been studied and devised to overcome tragedy of the commons situations, as in Garret Hardin’s classical statement of the problem [

10], and in Mancur Olson treatment of the breakdown of collective action [

11]. Given the rival and non-excludable nature of such resources, conflict over their appropriation and over-exploitation are to be considered endemic due to collective action failure [

12]. The technology used and the governance structure are functional to adequately regulating appropriation, by limiting the risk of opportunism and conflict and by punishing the violation of rules of appropriation [

12,

13]. Governance, besides limiting the risk of opportunism by the involved parties, is also functional to the coordination of collective action in terms of improved information flows and alignment of expectations [

14]. Adequate coordination can be achieved not only by controlling and punishing defectors, but also through proper involvement and deliberation processes based on membership rights and other consultative and participative practices, through improved information circulation, and the creation of organization specific knowledge, culture, and social capital [

15,

16,

17].

The analysis of the governance of common resources has been applied to the organizational realm to a notably limited extent. Some streams of literature in law and economics did start this field of enquiry, by defining business corporations as a form of “team production” [

18] and by enlarging the concept of corporate governance to include a wide array of mechanisms mitigating risk and uncertainty in contractual relations [

19], and to represent the multi-stakeholder corporate embodiment of the social contract [

20]. Some authors got as far as identifying corporate dimensions that can be likened to common goods, and business enterprises have been explicitly understood as “commons” themselves [

9,

10,

11,

12,

13,

14,

15,

16,

17,

18,

19,

20,

21]. Other authors explicitly consider team production and collective action as founding principles of entrepreneurial action and innovation processes in new business environments, highlighting also the special role of intrinsic and prosocial motivations in innovation and growth processes [

22,

23]. However, to the best of the author’s knowledge, no contribution has systematically analyzed the corporate patrimony within the common property approach, and explicitly discussed, in this line of enquiry, the specific features, sustainability (economic and social) and longevity of “alternative” or “heterodox” enterprise forms, such as co-operative and social enterprises [

24,

25,

26]. Few exceptions of approaches similar to the one followed in this paper are found in some works concerning capital resources in worker co-operatives [

27], and co-operative finance [

28].

This paper concentrates on common or non-divided asset ownership as a common-pool resource. It widens the existing literature, evidencing the analogies between business corporations and their patrimony with common goods, to study the features and economic functions of common property systems in the study of entrepreneurial ventures. Indeed, also the working of other organizational dimensions in co-operative enterprises can be interpreted following the model of common property regimes developed by Ostrom; for example, their governance and distributive patterns. This work, however, concentrates on self-financed accumulation and the use of capital only. Co-operative enterprises are identified as privileged organizational contexts since, both in their historical origin and institutional evolution, they have been characterized in most countries by the presence of capital resources that are non-divided and non-divisible among their members. This work also widens the existing theoretical approaches to co-operative enterprises by spelling out a new institutionalist framework able to study the transactional and productive costs determinants and the optimal level of non-divided asset ownership in co-operative enterprises. Finally, the non-divisibility of capital is connected with the longevity and financial sustainability of cooperative enterprises. As it shall be evidenced, incentive alignment and inter-temporal solidarity between different generations of members in cooperatives are understood as the main drivers of financial stability and sustainability in the medium- to long-term (intergenerational solidarity is implicit in the kind of co-operative ownership rights developed in some countries, such as Italy, and studied in this paper. When a new member is acquired by the organization, he or she is accepting the national legislation and the statutory bylaws on this subject matter).

The strategy of the paper is as follows:

Section 2 deals with the definition, economic relevance, pattern of emergence, and optimal dimension of non-divided capital funds in both investor-owned companies and co-operative enterprises. In

Section 3, the origin and spread of common capital resources in co-operatives is analyzed within a new institutionalist frame by comparing their costs and benefits, both transactional and productive, with the costs and benefits of individually- held capital resources.

Section 4 discusses for better financial sustainability and firm longevity induced by the presence of non-divided capital resources, especially discussing incentive alignment and inter-generational solidarity.

Section 5 concludes the paper.

2. Common Resources in Investor-owned and in Co-Operative Enterprises

One initial key question in this study concerns the reasons why the analysis of common pool capital resources is largely absent in contemporary economics and organization literatures. The proposed answer concerns the dominant system of property rights, whose concentration and exclusivity limits the economic and organizational relevance of communalities in the ownership of enterprises (since priority is given to the analysis of the private sector, only investor-owned companies and cooperative enterprises are considered in this paper. Occasional references to publicly-owned organizations is introduced for the sake of an exemplifying role only).

The accumulation of owned capital is observed in all enterprise forms since it is functional to financing investment programs, buffering the organization against negative unpredicted events, and serving as collateral required as a guarantee of loan repayment. Additionally, capital resources can be characterized by a positive degree of communality in all ownership forms (public, private, and co-operative) when the relevant operative and strategic decisions are taken by a collectivity of controlling patrons (e.g., diffused share-ownership in joint stock companies and publicly-listed corporations), since in this case the use of capital resources may not be easily made excludable and the “exit” option can be costly. The utilization of a limited and rival stock of assets coupled with a low degree of excludability in strategic decision-making can engender a “tragedy of the commons” situation characterized by free riding in contribution (e.g., distribution of dividends is preferred to reinvestment of residuals) and over-exploitation (e.g., resources are used beyond the collectively-optimal point). However, the diversity of organizational forms in terms of control rights and governance can induce important differences in the analysis of the presence and modalities of utilization of common resources. The paper briefly considers investor-owned companies (IOFs, hereafter) first, and then introduces the case of co-operative enterprises.

2.1. Common Capital Resources in Investor-Owned Companies

The strictly private nature of capital resources in IOFs strongly reduces as a norm, and often eliminates the relevance communality, since shares are saleable and, in most cases, ownership is concentrated in a few hands. Decision-making becomes exclusive, and excludability in utilization is perfect after contractual constraints have been fulfilled. This is the standard observed solution in small- to medium-sized firms, and in family businesses, which are dominant in numbers in all contemporary economies.

However, even in the case of IOFs, capital resources can acquire a relevant degree of communality when the firm is constituted as joint stock. More specifically, as the number of stockholders increases, and no stockholder achieves a dominant position (ownership is dispersed), costly exit due to sunkeness of capital resources and investments and to asset specificity can induce a high degree of rivalry in the utilization of resources and in the appropriation of the surplus. In the same situation, non-excludability in decision-making, in the utilization of assets, and in the distribution of value added is likely to be high as well. This argument may be even more valid in widely held joint-stock and in publicly-quoted companies characterized by fragmented shareholdership, in which no dominant position is detected. In spite of dispersed ownership, the emergent dominant role of the management due to separation between ownership and control can reduce the problems related to communality thanks to centralized decision-making (cfr. the classic work by Berle and Means, [

29]). The same result would not be possible in co-operatives since, in their case, managers are appointed by members’ representatives, and need to respond more closely to their preferences [

30]. In this case, communality and the connected behavioral biases such as free-riding can represent a more serious challenge.

As said, a high degree of rivalry and non-excludability is to be considered, in IOFs, as an exception, not as the rule, due to concentrated ownership. Furthermore, even in the presence of a high degree of non-excludability in decision-making and capital utilization, the “exit” option represented by the sale of stocks can allow stockholders to recoup the value of their financial investments. In other words, the sale of owned stocks can be the preferred choice whenever non-excludability in decision-making leads to a “tragedy of the commons” situation in which individual preferences conflict with collectively optimal choices, and organizational costs are inflated by the growth of decision-making costs. Conversely, stockholders may, in many situations, prefer concentrated to dispersed ownership since the former solution allows for the elimination of inefficient and costly collective choices when asset specific and non-recoupable investments make the exit option costly. These remarks can explain the prevalence of concentrated ownership in IOFs in most contemporary economies. At the other extreme of the spectrum, sole-proprietorships or closely-held joint-stocks are found (in an evolutionary interpretation, concentrated ownership can be considered a central autopoietic property of capitalist property rights [

31,

32]).

2.2. Common Capital Resources in Co-Operative Firms

Co-operative enterprises are here understood as mutual benefit organizations characterized by membership rights that are not assigned on the basis of financial investments, but instead to individuals (e.g., in worker co-operatives) or to economic activities (e.g., in producer co-operatives) on the basis of the “one member, one vote” rule [

33,

34]. Indivisible or common reserves of capital in co-operatives, when they are present, are owned by the organization itself and cannot be shared among individual members, who enjoy a form of usufruct of the assets, but cannot appropriate them (unless this is specifically allowed for in the rules of the single co-operative) (in some national systems, however, (e.g., in France) members can appropriate the residual value of the organization upon its dissolution or conversion). The accumulation of indivisible reserves, or asset lock, has the primary function to self-finance investment programs, to create collateral guarantees protecting external financial supporters, and to insure the membership against negative unpredicted events [

27,

35]. Democratic and participative governance (engendering non-excludability from strategic choices), coupled with the presence of non-divisible, but scarce and deductible capital resources, leads to the emergence of social dilemmas that are typical of the utilization of common resources: conflicting objectives in collective decision-making can entail substantial governance costs. Costs depend both on rivalry (alternative uses of assets and appropriation of incomes streams may not be mutually compatible, leading to overexploitation of limited resources and conflict) and on non-excludability (since all members have the legal right to participate on an equal basis, collective decision-making can become complex, lengthy, and contested).

2.3. Ownership Models in Co-Operative Enterprises

There are three main ownership system-models of co-operative enterprise corresponding to three different theoretical streams. The first model corresponds to private co-operatives in which membership rights are saleable [

36,

37,

38,

39]. The second model corresponds to co-operatives in which the assets are publicly-owned, and members have the usufruct of the capital of the organization. This model broadly corresponds to the institutional system of the former Republic of Yugoslavia. Alternatively, the cooperative can be completely externally financed, without any ownership in the assets it uses [

40,

41]. While the Jugoslav system corresponds, in the theory of worker co-operatives, to the so-called Worker Managed Firm (WMF), the externally-financed version corresponds to the model of the Labor Managed Firm (LMF). The theory of both model, the WMF and the LMF, was initially developed by Vanek [

42] and perfected by Jossa [

40,

41,

43]. The third model corresponds to less well-defined typologies of ownership rights, which some authors have identified in communitarian, or co-operative ownership, and are usually categorized as lying in between public and private ownership [

34]. In most variants of this ownership system, which spread especially in continental Europe, the assets of the organization are owned neither publicly, nor by individual members, but by the organization itself, or by the community of reference. The behavioral implications of this their models still await finer definition and enquire (mixes between the salient institutional features of the three models are not excluded. For example, the well-known group of co-operatives based in Mondragon, Basque Region of Spain, can be considered a mix of the second and third model). This paper is set to analyze the problem of accumulation of capital in the third model and in those hybrid systems that include relevant elements of the third model. The main reason is that, among non-state-owned models of co-operative enterprises, only non-privately-owned co-operatives demonstrated to be compatible with non-divided asset ownership.

2.4. Legal Constraints in Western Countries

Institutional models loosely correspond to, but do not coincide with, the three theoretical models presented in the previous section. While public ownership of co-operatives is barred by law and by the International Cooperative Alliance (ICA) seven principles, which refer to voluntary association, member democratic control and economic participation, and autonomy, independence of the co-operative, education and training of co-operative members and care for the community. On the other hand, the market for membership shares, even when not excluded by law like in the US, is rarely implemented or excluded by co-operatives’ bylaws. On the other hand, several national legislation do not set special constraints against the possibility of the sale and demutualization of cooperatives. Finally, a partial non-profit distribution constraint and the asset lock era required in several countries, for example Italy and Finland, to strengthen patrimonial stability. These are the reasons why existing institutional systems are to be prevalently considered hybrids, which mix to different extents different features of the three theoretical models.

In western countries, three main institutional models for the accumulation of capital resources in co-operative enterprises can be singled out. In the first model, which mainly lies within the common law tradition, reserves of capital are, as a norm, divisible among members. Forms of common ownership are not mandated and, in some cases, excluded by law. Common ownership can be allowed when it is spontaneously introduced by individual organizations in their bylaws. If we take the United Kingdom as the most relevant example of this kind of institutional tradition, we notice that, until recent years, bona fide co-operative societies registered under the 1965 Industrial and Provident Act were not allowed to accumulate common or indivisible reserves. The possibility to introduce restrictions to divisibility of capital in companies’ bylaws was introduced in the reformed 2002 Industrial and Provident Act and in the Co-operative and Community Benefit Societies Act in 2003. However, at the present stage of legislative development, the possibility for co-operatives to introduce a fully-blown asset lock is still barred by law, while it has been allowed in community benefit societies since 2006. The asset lock regulation for community benefit industrial and provident societies has been in force and available for use since 2006 (The Community Benefit Societies Restriction on Use of Assets Regulations 2006/264). Bencom regulations implement the provisions of the 2003 Act to “lock in” the value of the assets and resources of a community benefit society. (cfr.:

http://www.thenews.coop/32865/news/banking-and-insurance/uk-co-op-law-2010-summary/) [

44].

The second and the third models are, instead, mainly found within the civil law tradition of continental Europe. In the second model, which includes France and Spain as national cases, law requires the creation of reserves of capital that cannot be shared by members while the organization is active. Such reserves, however, can be appropriated upon dissolution, sale, or conversion of the enterprise. In the third model, which is found mainly in Finland and Italy, compulsory accumulation of net residuals into indivisible reserves is coupled by the prohibition for members to cash in the residual value of the organization also upon its dissolution, sale, or conversion (the Italian law requires that any left-over residual value of the indivisible capital reserves of dissolved or converted (transformed into investor-owned companies) co-operatives has to be transferred to national or regional funds controlled by related associations of co-operatives and used to finance new co-operative start-ups). The two civil law models share similarities, but also important differences. The former is characterized, comparatively, by stronger financial incentives for members, since these can appropriate the residual value of the organization. However, at the same time, the patrimony is less stable since divisibility in the case of dissolution or conversion can represent, by itself, the incentive to stop operation and cash in any residual value of the organization [

45]. Conversely, the latter model can suffer from too weak financial incentives, as evidenced in the undercapitalization hypotheses by Furubotn and Pejovich [

46], and Vanek [

47]. At the same time, this model has been showing a high degree of patrimonial stability since it does not offer incentives to demutualize or sell the organization. In both civil law systems, however, net operating losses can be imputed to indivisible reserves. This possibility can, in principle, weaken patrimonial stability since it is liable to mismanagement and unlawful appropriation (the system of capital accumulation in the former Republic of Yugoslavia can be interpreted a radical version of the third civil law system. Under Yugoslav self-management legislation, all positive net residuals had to be reinvested in invisible reserves, whose function was to absorb operating losses in the presence of a strict capital maintenance requirement (CMR). The CMR prevented any reduction of the net book value of capital [

40,

48]). Finally, in the US context, a similar legal categorization exists, though in this case the main divide is drawn between co-operatives and non-profit organizations. Only the latter are characterized by capital indivisibility, even if legislation does not forbid indivisibility into mutual benefit organizations [

49].

One final question that has crucial bearing on the working of the institutional system for capital accumulation relates to the ownership of net residuals. In the first institutional system, ownership is clearly attributed to the membership, which has to devise proper rules to distribute or to reinvest it, at its will, in shareable reserves of capital. On the other hand, the second and third system are compatible with the idea that the ownership of residuals, both positive and negative, is attributed to the co-operative as an organization. Distribution, which can be limited by law, needs to be deliberated by the elected bodies (the Board of Directors), while the default solution is that residuals are reinvested in the organization in indivisible reserves. While the UK represents an example of the former solution, Italian legislation has instead followed the latter solution, which is more strongly connected with the presence of assets-as-common resources in co-operative enterprises.

3. Divisible and Indivisible Reserves of Capital

This section goes beyond specific institutional constraints and introduces a new-institutionalist account of the economic motivation and process of formation backing non-divided forms of capital ownership in co-operatives. Building on the framework developed by Hansmann [

30,

50,

51,

52], the basic category of transaction costs is sorted into the two sub-categories of the net costs of (i) the governance of common resources; and (ii) individual ownership of the shares of capital by the members of the co-operative. The costs attached to the two sub-categories are compared in order to single out the optimal level of common resources.

Co-operative enterprises can self-finance themselves in two fundamental ways: capital shares individually owned by members; or by resorting to non-divided and non-divisible reserves of capital derived by reinvested positive residuals, which take the form of the asset lock (for the sake of simplicity, such intermediate forms of common ownership, in which indivisible reserves exist, but can be appropriated by members upon dissolution or conversion, are not considered). In the former case, individually-owned financial instruments have, in different national contexts, pronouncedly different regulatory features, since they can be differentiated on the basis of yearly yields, dividend distribution, and reimbursement rights. Reimbursements rights can take different forms, since such instruments can: (i) be perpetual (not redeemable) and not refundable by the enterprise. In this case they pay annuities to incumbent members [

53] and may, under specific circumstances, be sold on the market for membership rights [

35,

36,

37]; (ii) be refunded when the member-owner quits the organization; and (iii) be refunded independently of the position as incumbent member under looser temporal constraints [

36,

37,

54,

55]. Finally, members can finance their organization also by subscribing member loans or bonds.

Members’ individual ownership of capital leads to capital variability whenever: (i) the shares need to be paid back to quitting or incumbent members (a situation common in most national systems of co-operative legislation); (ii) the shares are transformed into debt capital upon quittance of the member; or (iii) members can sell their shares on the market to non-members. In all these cases (refund, sale, or transformation into debt capital of individual shares) the total amount of owned capital is reduced upon quittance. The intensity of capital variability is proportional to the percent of total capital individually held by members, and to the rate of members’ turnover. Insofar as it can reduce and/or make uncertain the total dimension of the patrimony and its availability as a collateral guarantee, variability can represent a limit to investment processes and to the ability of the organization to borrow from financial intermediaries [

35,

45]. By constituting indivisible reserves, locked assets effectively counteract capital variability. In Italy, all typologies of cooperative enterprises (worker, consumer, producer, user, and social cooperatives) are required by law to reinvest at least 30% of their net residual earnings into indivisible reserves of capital, which cannot be shared among members both during the life of the organization, and also upon its dissolution or conversion. This constraint is increased to 70% in the case of cooperative banks. Any residual value is to be transferred to national or regional funds controlled by co-operative associations, which finance the start-up of new co-operative ventures. Empirical evidence shows, however, that a dominant proportion of Italian cooperatives reinvests close to 100% of net residuals into locked assets. That is, legal requirements are not nearly binding. This evidence supports the idea of the existence of an endogenous process of formation of locked assets in cooperatives [

27]. Considering a second example, in the Mondragon group of worker co-operatives, net residuals are partly distributed to incumbent members (about 70%, though this percentage has been varying over the years), who are mandated to reinvest their individual shares in internal capital accounts as long as they are members. The remaining share of net residuals (30%) is reinvested into indivisible reserves [

35,

54,

55]. Due to shares being paid back when members quit or retire, the total amount of the group assets held in indivisible reserves is, to date, about 50% [

56].

A second function of non-divided ownership is found in the necessity to counteract the risk of demutualization, that is the termination of a co-operative venture through the sale of assets, or through conversion into a IOF. When a large share of total capital is individually owned, its variability, as moderated by the intensity of members’ turnover, can lead to undercapitalization: the co-operative would have to refund or transform into bonds or loans substantial shares of owned capital, thus leading to increased dependence on external finance, higher leverage, and lower collateral guarantees [

35,

45]. When this problem becomes severe, the co-operative can be forced to demutualize in order to increase owned capital (equity) and reduce leverage. Furthermore, co-operative members individually owning large shares of capital can also decide to demutualize in order to cash in the value of their individual assets. They can also acquire unusual and undue lobbying power over strategic decision-making processed. This problem is especially severe in best and worst performing co-operatives. In the former case, high value-added co-operatives are characterized by market value of individual shares that can far exceed the nominal value. This difference can represent a powerful incentive to sell out to investors and liquidate the market value of shares (this has been the reason for the disappearance of the well-known group of lumberjack plywood cooperatives in the US pacific North West: the high market value of the members’ financial stakes made the sale of these organizations to external investors more convenient than the sale on the market for membership rights to new incoming co-operators). In the latter case, the risk of economic crisis and demutualization can create financial incentives favoring demutualization itself. When the organization fares negative economic and financial conditions, members may be induced to sell out shares or demutualize to reduce expected financial losses, accelerating the process of the crisis. In this line of enquiry, Jacobson and O’Leary [

57] study the demutualization process of seven out of fifteen of the largest diary co-operatives in Ireland in the 1980ies. The lack of correct application of cooperative principles led to a situation in which members’ shares were not reimbursed, and dormant or inactive members had the same patrimonial and decision-making rights than active members. Such imbalances contributed to strengthen the incentive and the desire of active members to demutualize. These remarks evidence that individual ownership, though it can strengthen financial incentives, is likely to substantially increase patrimonial instability.

Demutualization is more common just in those institutional contexts in which individualized members’ ownership of capital is dominant, especially in common law, Anglo-Saxon countries (cfr. for example Battilani, Balnave, and Patmore [

58], on Australia). The relatively smaller number and diffusion of co-operatives in common law compared to civil law countries is better explained by larger numbers of conversion into IOFs, than by higher failure rates. In more general terms, the small total number of co-operatives, economy-wide, is better explained by small creation numbers than short-lived active existence. Co-operatives’ duration is indeed longer than investor-owned companies’ [

59]. To exemplify, one well-known demutualization wave of co-operatives, mutual insurance companies, building societies and credit unions took place in the United Kingdom during the 1980s and the early 1990s. In continental Europe, instead, where much larger diffusion of (legally mandated) non-divided reserves of capital is recorded, demutualization has less often been observed, and this fact has better supported the sustainability and longevity of co-operatives (in Italy, demutualization is allowed by law only after the demutualizing co-operative renounces the whole value of its asset, which is to be paid out to national funds financing new co-operative start-ups).

3.1. Undercapitalization, Common Ownership, and Diffusion of Co-Operatives

While in civil law countries the accumulation of indivisible reserves is, as a norm, required by law, common law countries, for example, the UK, have witnessed in recent years a new trend favoring the diffusion of non-divided forms of capital ownership. Constraints on divisibility, reimbursement, and sale of individual shares are often introduced in the bylaws of co-operatives, social enterprises, and employee-owned companies by conferring either part or the whole patrimony of the organization into locked assets or trust funds [

8,

60]. The spontaneous emergence of forms of (partial or complete) common ownership in institutional contexts in which they are not mandated, or even favored by law, testifies in favor of their substantive economic relevance and of the potential for wider diffusion.

The legally-imposed accumulation of indivisible reserves showed to be effective in preventing demutualization, but has been repeatedly accused to lead to dynamically inefficient investment choices, implying under-investment and under-capitalization [

40,

45,

46]. Undercapitalization due to suboptimal reinvestment of net residuals into locked assets and limited access to financial markets (due to absence of tradable shares) have been taken as implying the self-selection of co-operatives into low-capital, high-labor intensive sectors [

59,

61,

62,

63]. They have also been taken to explain the low rate of creation of new co-operative ventures due to limited financial support to new start-ups. On the other hand, the (partial) presence of common ownership in some co-operative forms, especially agricultural and producer co-operatives, that survived and prospered in many countries, and some successful co-operative experiments, such as the Mondragon group, speak to the contrary of such an interpretation. This counter-evidence leaves open the possibility to pursue new enquiry on models of co-operative finance that are at least partly based on common ownership [

64] (cfr. also the works by Jossa [

40,

43] on models of externally-financed worker co-operatives under public ownership).

3.2. The Emergence of Common Capital Resources in a New-Institutionalist Perspective

The foregoing arguments can be better systematized by analyzing the economic forces, which favor the emergence of an optimal amount of indivisible capital reserves. These forces need to underpin the stability of accumulated capital and of entrepreneurial processes, without renouncing financial incentives to invest optimally and increase productivity. In this, it should be noted, in the most notable and competitive examples of co-operative enterprises and employee-owned firms, mixed forms of capital ownership are found. Individualized, non-divided, and mixed forms of capital ownership can be singled out in specific cases. In the Mondragon group, non-divisible reserves of capital coexist with large shares of capital held directly by members in internal capital accounts [

54,

55]. In the John Lewis Partnership, one of the largest and oldest employee-owned firms in the UK, employees’ appropriation rights are strictly regulated and limited by the patrimony of the partnership being held in trust funds, which cannot be shared among partners at any time, but which entitle incumbent partners to receive annual dividends. In many employee-owned companies, not all the patrimony is held in trust, and the presence of both individually-owned shares and trust funds is detected [

60]. This evidence suggests that capital in such ownership forms can be decomposed into different parts, which contribute in different ways to the financial health of the organization. The different parts have different functions: while non-divided ownership is mainly geared to guarantee stability to investment processes and collateral guarantees, individual ownership improves financial incentives and performance.

In a new-institutionalist perspective it is necessary to ask what are the costs attached to the transactions involved in each of the two forms of ownership, and their optimal dimension thereof. As already anticipated, individual financial instruments are characterized by high transaction costs connected to members’ turnover, which, in turn, depend on members’ different temporal horizons of permanence as incumbent members and on heterogeneous members’ preferences. When members show homogeneous temporal horizons and preferences, transaction costs connected with membership rights and with individual financial positions are low since homogeneity simplifies and lowers the costs of collective decision-making, this way limiting conflict and turnover. These elements favor the permanence of individual ownership, due to the strong match between individual financial incentives and returns [

65]. The well-known examples of professional partnerships and of the group of worker-owned plywood co-operatives in the US Pacific Northwest in the twentieth century share the features of the presence of a highly homogeneous membership performing similar professional and work tasks, and having similar educational levels and personal features [

36,

37,

50,

51,

66,

67,

68]. In such cases, non-divided ownership may not be observed, since owned capital and organizational processes are stable even in its absence and members would aim at maximizing financial returns by means of individual ownership [

36,

37]. In the framework presented in this paper, members’ homogeneous preferences imply that rivalry in the utilization of capital and non-excludability in collective decision-making are more easily managed. Since the tasks performed by different members are similar, the number of different uses to which capital can be put is limited and rules governing utilization of resources and the equitable sharing of the surplus are more easily devised and monitored. As complexity and dimension increase, homogeneity fades away, members’ objectives become heterogeneous and more difficult to reconcile, this way fostering both organizational and financial instability [

51]. Different preferences concerning investment processes, organizational models and distributive patterns, and different temporal horizons make collective decision-making less straightforward and more costly, this way increasing governance costs, members’ turnover, and the risk of demutualization.

Insofar as it allows the organization to internalize, control, and reduce, by means of administrative procedures, the costs engendered by individual ownership, non-divided ownership represents one possible remedy, which can take back stability to mutualistic financial structures in the presence of complexity and heterogeneity of preferences [

30]. However, non-divided ownership can engender costs and inefficiencies of its own.

As previously anticipated, underinvestment due to members’ truncated temporal horizon, which arises when the median member’s horizon is lower than the optimal duration of investment programs, represents the most classical problem concerning non-divided ownership. This problem may be especially serious in worker co-operatives, due to high member turnover, especially when the median temporal horizon is short and the median age of members is high. It engenders lower than optimal investment schedules and higher then optimal distribution of income and dividends to members, this way leading to under-capitalization and dissolution [

42,

45,

46,

47,

69].

Under-capitalization due to non-divided ownership can be effectively counteracted in at least four cases: (i) when the rate of return on marginal investment programs is sufficiently high, and/or their temporal duration is limited; (ii) when the temporal horizon of the median member is sufficiently long and new younger members are constantly associated to the co-operative; (iii) when ownership is mixed and individual shares of capital are found side by side with common ownership. In this case, individual shares would finance the marginal (short-term) components of capital [

35,

45]; and (iv) when members’ and/or directors’ decisions are informed by social preferences that weigh positively the welfare of future generations of members. In this case, optimal investment schedules are the result of intergenerational reciprocity among different generations of members, since each incumbent generation is favored by the stock of capital bequeathed by previous generations, and favors future generations in a similar way, by bequeathing the existing stock of capital [

34]. One further crucial element that can justify the introduction of non-divided ownership, even in the presence of a truncated temporal horizon, has again to do with stability: by reducing the transaction costs connected with individual ownership, non-divided ownership can end up reducing turnover and prolonging the median temporal horizon, this way weakening the impact of the horizon problem. This result can be modelled in game theoretic terms by the trust game [

70]. In this interpretation, the present generation of members (trustee or second mover) has to decide how much to keep for itself, and how much to give back (transfer to future generations of members) of the amounts invested by previous generations of members (grantor or first mover).

Among the weaknesses of common capital resources, besides the highlighted presence of weak financial incentives and risks of under-investment, the costs and inefficiencies deriving from the spread of conflict over utilization and from opportunistic behaviors, as evidenced in the literature on “the tragedy of the commons”, need to be considered as well [

10,

11]. These costs can be high in the absence of adequate regulation [

1]. Therefore, non-divided ownership can represent an effective institutional device substituting individual ownership only if the new emerging costs of governance are properly controlled through administrative procedures and other working rules, and through managerial decisions.

3.3. The Optimal Amount of Non-Divided Capital Resources

In order to single out the optimal or preferred amount of non-divided resources, the advantages deriving from common ownership need to be compared with their costs, and with the corresponding costs and benefits attached to individual ownership.

The comparison of costs and benefits is complex as it requires analysis of transactional, operational, and welfare-generating or -depleting dimensions. However, this comparison offers a vantage point from which empirical research can depart. The equilibrium between common and individual ownership derives from the balance between two categories of net costs attached to the two different ownership regimes (a detailed comparison of the benefits attached to different ownership forms is outside the scope of this paper, which is limited to the cost side):

- (i)

costs deriving from the governance of common resources (excess of utilization and depletion of assets, monitoring, conflict, and decision-making costs), plus efficiency losses in terms of suboptimal investment decisions (horizon problem) and absence of highly-powered financial incentives. Costs of governance include lengthy and inconsistent decision-making processes, conflict over rules governing, and decisions concerning use of resources and distribution of proceedings, monitoring activities, inefficient choices which privilege the median voter preferences over average preferences, and the costs of lobbying by dominant groups of members;

- (ii)

costs deriving from contractual imperfections attached to individual ownership, which can engender organizational impasse due to absence of agreement on collective choices, high turnover leading to disinvestments processes, and de-mutualization. Absence of agreement can derive from conflict over strategic decisions concerning alternative investment plans and their temporal horizon, resource allocation and utilization, trade-offs between individual appropriation of proceedings, and collective decisions concerning investment plans.

When the balance between these two categories of costs leads to the emergence of a relevant amount of common capital resources, governance becomes the crucial organizational dimension regulating the internalization of contractual costs and control over the emerging governance costs [

71,

72]. It also bears relevant implications on the alignment of members’ preferences with organizational objectives. The non-divisibility and non-salability of common assets, when decision-making and conflict costs are kept under control, can lead to better alignment, and have empowering effects on collective action. Alignment, in this case, is the result of reconstitutive downward effects that tend to modify and refine individual preferences to make them compatible with collective ones (on the concepts of reconstitutive downward causation and reconstitutive downward effects, cfr. Hodgson [

73,

74]). This argument, of course, does not exclude effects running in the opposite direction, since individual members’ preferences in co-operatives can influence organizational objectives through participation in decision-making processes and other organizational patterns.

In an evolutionary interpretation, common ownership represents an emergent feature of collective action by members associated in co-operative ventures. This emerging institutional solution overcomes individual ownership and the attached contractual costs in the presence of complex and heterogeneous members’ preferences. In more general terms, the interpretation of entrepreneurial action as exclusively attached to, and explained by, individual behavior and preferences is not granted and more, but it is instead overcome in favor of new emerging forms of collective entrepreneurial action [

75,

76,

77] (a non-reductionist interpretation of collective action and institutions as emergent social dimensions, which cannot be explained in terms of individual behavior alone, but are, nonetheless, anchored to individual behavior, is found in prominent contributions to institutional and evolutionary economics [

1,

73]).

3.4. Co-Operative Governance and the Problem of Free-Riding

When the amount of non-divided and non-divisible capital becomes relevant, the presence of common-pool capital resources (rival, but not excludable) implies the presence of “tragedy-of-the-commons-like dilemmas”, for example, over-exploitation of resources. Indeed, free-riding has long been identified as one of the fundamental problems haunting collective entrepreneurial action by groups of principals and leading to a break-down of cooperative or mutualistic governance [

1], for example, as concerns the sub-optimal effort contribution in worker co-operatives [

78]. In the subject matter of this paper, when capital is divided or divisible, financial incentives are stronger and, in principle, can be sufficient to guarantee strong member involvement and high productivity, thus eschewing the problem of free riding on effort and resource contribution, and over-utilization of resources. This is especially so in worker and producer co-ops. However, members’ heterogeneity (different preferences and time horizons) can quite easily engender contrasts, whose expected costs are idiosyncratic and cannot be predicted since they are determined by specific personal and contextual factors. Nonetheless, the expected costs of capital variability and the risk of demutualization, as discussed in the paper, can negatively impact on financial performance and patrimonial stability. Furthermore, opportunism can be present also when capital is divisible, if its utilization is subjected to collective action. Different members or groups of members, if they have decision-making or influence power, can take advantage in various ways of the available resources directing benefits and proceedings to their own benefit. The non-divisibility of capital clearly dampens financial incentives, and increases both rivalry and non-excludability in the utilization of resources. These elements imply that free-riding and opportunism are more serious problems in the presence of non-divided than divided ownership. Excessive use of capital by members in the absence of strong incentives to carry out new investment programs and replace worn out or outdated assets can spread hand with economic inefficiency. In terms of effort contribution, in worker co-ops, over exploitation correspond to lower than optimal contribution, which implies excessive effort contribution by other worker-members. An effective solution can be found in the reinterpretation of the eight design principles for the governance of common-pool natural resources proposed by Elinor Orstrom [

1] (the eight design principles are: (i) definition of clear group boundaries; (ii) MATCHING rules governing use of common goods to local needs and conditions; (iii) ensuring that those affected by the rules can participate in modifying the same rules; (iv) outside authorities respect the rule-making rights of community members; (v) developing a system for monitoring members’ behavior, by community members themselves; (vi) implementing graduated sanctions for rule violators; (vii) providing dispute resolution; and (viii) developing nested tiers governance from the lowest level units to the entire system). These principles set the stage for the effective involvement of members in the building up and practice of co-operative governance by favoring involvement and by punishing defection [

7,

79]. Member involvement and participation in decision-making is fundamental, since it favors the expression of not-fully self-interested (intrinsic, social, and other regarding) motivations. However, involvement is not enough. The eight principles can be easily adapted to the governance of co-operative organizations, since in co-operative’s boundaries are clearly defined and rules (statutory bylaws and other regulation) can be fine-tuned to the needs of members and to the specific conditions of individual co-operatives [

79]. Governance rules can be worked out in a participatory way, and can be enforced directly by the co-operative, after legislative provisions are respected. Members can be monitored by peers and supervisors, who are appointed on the basis of delegation of decision-making power from members to directors. Monitoring, sanctions, and dispute resolution can be implemented by the co-operative itself, when lawsuits are not undertaken [

80]. Finally, co-operative governance can be multi-layered in complex, vertically integrated and/or geographically distributed organizations. The potential costs of members’ opportunism are internalized and managed inside organizational boundaries. The eight design principles need adaptation from their application to natural resources to business institutions. However, the initial assessment of their application to the management of non-divided asset ownership in co-operatives appears promising and ripe for fruitful developments.

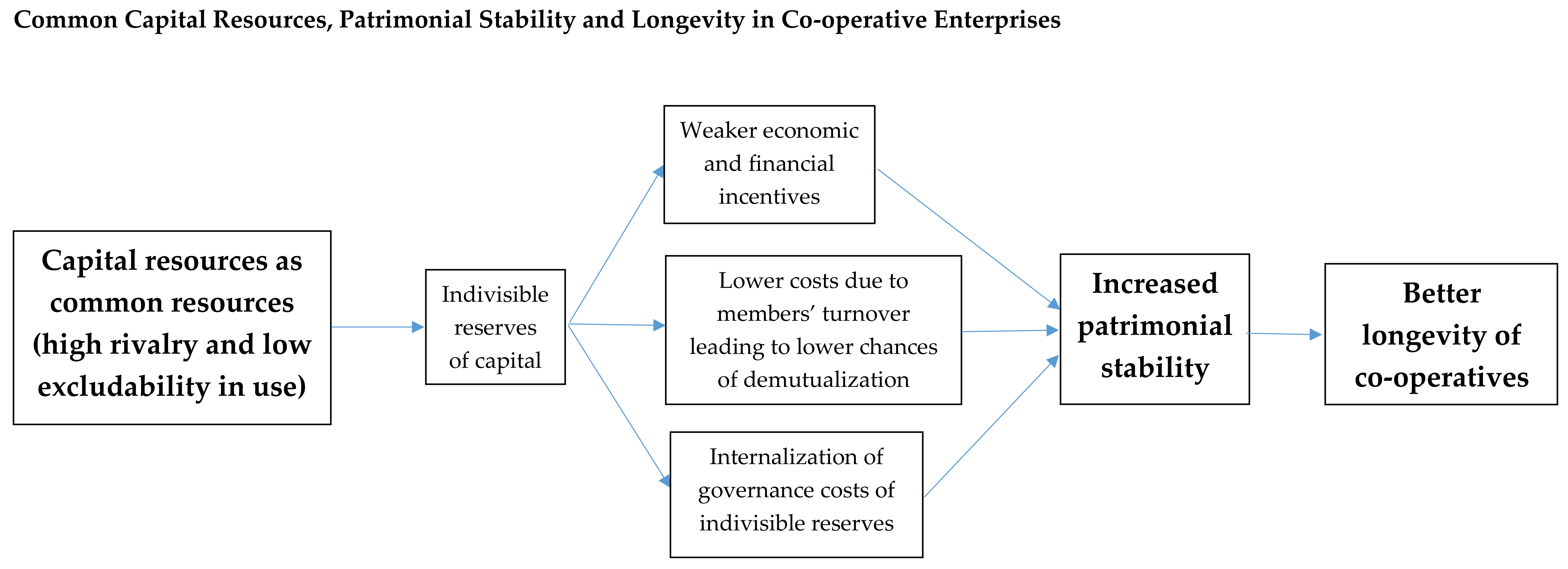

4. Sustainability and Longevity

One of the most salient consequences of the introduction of capital indivisibility is better financial and economic sustainability due to patrimonial stability, and increased longevity of co-operatives. Contrary to the predictions of the best-known models in economic theory [

42,

46], capital indivisibility does not lead to short termism, degeneration, and dissolution. Indeed, co-operatives have been shown to live longer than IOFs [

59]. Instead, and in line with prevalent empirical evidence [

44,

59], the exclusion of the possibility to demutualize and sell the assets of the organization, the internalization of, and control over, costs deriving from contractual imperfections, and the better alignment between individual preferences and organizational objectives appear to favor longer term resilience. Better sustainability and resilience is especially evidenced during periods of crisis since, in the last ten years, in several countries, co-operatives withstood the strong downturn in demand better than IOFs. They also laid-off fewer workers than IOFs, thanks to fluctuating wages and to the insurance function played by the non-divisible component of capital [

27,

44,

81,

82].

The arguments of this paper showed that indivisibility of capital is likely to lead to better stability of the patrimony, since common capital resources cannot be shared by members and are to be considered ownership of the organization itself. The prohibition of members’ appropriation profoundly changes incentives, expectations, and behaviors. When new members enter the cooperatives, they know they cannot appropriate its patrimony. Different institutions cause differential ex-ante selective processes: members desiring to appropriate the economic value of the organization are likely not to join this kind of associative venture in the first stance. Existing members (new and incumbent) accept a fundamental associative pact, a social contract, in which appropriation of the patrimony is excluded. By subscribing the associative pact, they only expect economic (monetary and non-monetary) remuneration deriving from mutual benefit, but not financial remuneration attached to capital shares. The associative pact also implies acceptance of intergenerational solidarity. Incumbent members know that the existing patrimony was accumulated by previous generations of members, and that future generations will enjoy similar benefits after their own quittance. The ex-ante working of the associate pact in cooperatives guarantees static and intertemporal stability, which is closely connected with longevity. Co-operatives that do not undergo economic crisis and financial distress can expect their patrimony to be preserved, virtually without limitation, even in the presence of internal heterogeneity of preferences. In turn, the impossibility to appropriate the patrimony in case of internal dispute lowers the probability of disputes arising in the first stance, since no individual member or group would obtain any monetary advantage from it.

Environmental Sustainability

The work has been focusing on capital as common (rival, but not excludable) resource. The spread of co-operatives, beyond their own financial sustainability dealt with in this paper, can help, if properly regulated, to support environmental sustainability in several ways. First, co-operatives have been reported to be concentrated in high labor-intensive sectors [

63]. This feature, which clearly puts them at a disadvantage in capital-intensive sectors, signals a tendency to avoid resource-intensive production processes and to lower the consumption of resources. Second, co-operatives have limited access to financial markets, given the absence or reduced role of saleable equity shares in most co-operative models [

34]. This feature would, again, push co-operatives to invest less in capital- and resource-intensive production processes. Third, the well-known tendency of co-operatives to under-invest and be undercapitalized when the temporal horizon of permanence of (median) members is too short [

46] can surely lead to some degree of allocative inefficiency (under-investing co-operatives require returns on investment programs to be inefficiently higher than the prevailing market rate). However, this feature can also signal a tendency to save on the utilization of resources, and to optimize the utilization of the existing capital stock. These elements, taken together, imply that the emergence of non-divided capital ownership in co-operatives, and of the related governance mechanisms and rules are, themselves, ways to reproduce in the micro-context of the business organization the environmental benefits derived from the management of common-pool natural resources by the same principals who exploit them, as in the Ostrom framework. Indeed, co-operative enterprises were born, historically, just to give to member-persons the possibility to directly control the production process on which their welfare was dependent. Lower resource exploitation at the micro level implies lower exploitation of resources also at the macro level, and this is seen as one of the most qualifying outcomes of co-operative governance as collective action governance of common-pool resources. Going beyond organizational boundaries, co-operatives can also create networks, consortia, and associations that can be especially effective in managing larger assets [

83,

84]. This is especially true in the context of the exploitation of natural resources, such as in fisheries and in agriculture, in which co-operatives are most common, but also in the case of historical and cultural commons, such as the management and re-utilization of historical buildings, monuments, and cultural heritage. Finally, it is also true in the emerging sector of ecological tourism, which allows co-operatives to manage natural resources without owing them in an economically and environmentally sustainable way. The ability of co-operative enterprises to reduce the strain placed on the carrying capacity of the environment will have to be deeply enquired by future research. Here it is sufficient to evidence that co-operative governance can show that the conflicting interaction between social systems and the environment that hosts them does not need to end up in operational closure, indifference, and damage for the environment [

85].

5. Concluding Remarks

This work represents an attempt to reformulate the problem of the ownership of capital in co-operative enterprises by analyzing it in a new perspective, which looks at how common or non-divided capital resources can, when properly regulated, bear productive and welfare-increasing potential, and not necessarily represent an anomaly in, or obstacle to, the correct development of entrepreneurial organizations. This new viewpoint can allow taking some steps towards overcoming well-known negative results (e.g., concerning under-investment and under-capitalization, demutualization, and dissolution), which did not advise, to date, the spread of this kind of similar institutional solution.

The paper strived to explain, within the new-institutionalist frame of analysis, the pattern of emergence and spread (both spontaneous and legally mandated) of non-divided reserves of capital, interpreted as deductible and non-excludable assets, and to identify the main economic forces defining their optimal level. The answer has been found in the complex comparison between the transactional and operational costs attached to individualized versus common reserves of capital. A strong compatibility and linkage between collective entrepreneurial action in co-operative enterprises, and the emergence of non-divided forms of ownership has been evidenced.

The main implication of this work is that common resources, when tragedy of the commons-like social dilemmas are overcome, can represent a fundamental and empowering tool allowing members to achieve higher welfare, both monetary and non-monetary, and empowerment. As already evidenced in the literature analyzing the collective governance of common-pool natural resources, members (appropriators) and their representatives are in the best position to work out the most effective governance solutions, due to better information, knowledge, and experience concerning the specific circumstances of the resource. The problem of opportunism in terms of free riding has been signaled several times as a major potential flaw of collective action and of co-operative governance. The study of design principles for the management of common-pool natural resources led to the definition of a series of mechanisms derived from eight basic principles and able to make such management effective. Not the same effort was put into researching and defining similar mechanisms guaranteeing the effectiveness of co-operative governance in enterprises. This paper has pointed out that the eight design principles studied in the case of common natural resources can be reinterpreted and quite easily adapted to govern the accumulation and utilization of non-divided asset ownership in co-operatives.

While the paper focuses on the similarities between the governance of CPRs and the governance of non-divided capital in co-operatives, differences should not be forgotten, as well in its implementation, since they can help in identifying critical institutional elements, and welfare-increasing dimensions that are absent in the case of natural resources. The main directions for future research seem to relate to the development of the legal definition and regulation of common property systems in the co-operative form of ownership, including both non-divisible and divisible capital reserves [

56].

Finally, the works also dealt with the impact of common ownership on patrimonial stability and on the financial sustainability of co-operatives. While existing models are not able to explain in a satisfactory way the survival, diffusion, and longevity of organizational forms characterized by common ownership, this paper spells out the theoretical connection between these two elements. The connection is substantiated by the better patrimonial stability of co-operatives characterized by the presence of non-divided and non-divisible capital resources.

{kind=link}