Natural Capital, Domestic Product and Proximate Causes of Economic Growth: Uruguay in the Long Run, 1870–2014

Abstract

1. Introduction

2. Theory and Empirical Approaches

2.1. Theoretical Frameworks

2.1.1. The Blessing of Natural Resource Abundance

2.1.2. Production Structure Approach: The Difficulties of a Primary Sector Specialization

2.1.3. Crowding-Out Approach: Natural Resources Displace Other Types of Capital

2.1.4. Institutional Change and Factor Endowment Approach

2.1.5. Economic History Approaches

2.2. The Empirical Evidence of the Resource Curse

2.2.1. The Impact of Natural Resources on Economic Growth

2.2.2. The Impact of Resources on Factors Linked to Growth

2.2.3. Is This Apparent Paradox a Red Herring?

3. Hypothesis and Empirical Strategy

3.1. Historical Overview and Reasons to Study Uruguay

3.1.1. Duality of the Structural Change

3.1.2. The Relevance of Studying the Non-Mineral Wealth

3.1.3. Natural Capital as a Better Proxy for the Abundance of Natural Resources

3.2. Empirical Strategy

4. Materials and Methods

4.1. Natural Capital Estimation

- considers only expected production, we consider, whenever it is possible, output actually recorded, except from 2015 to 2038, where we had to project productions in order to obtain the present discounted value for 1991 to 2014. When historical data were not available, we use different estimation techniques to complete the series.

- considers fixed production rates of return, we consider rents of natural resources actually received, which are therefore variable over time.

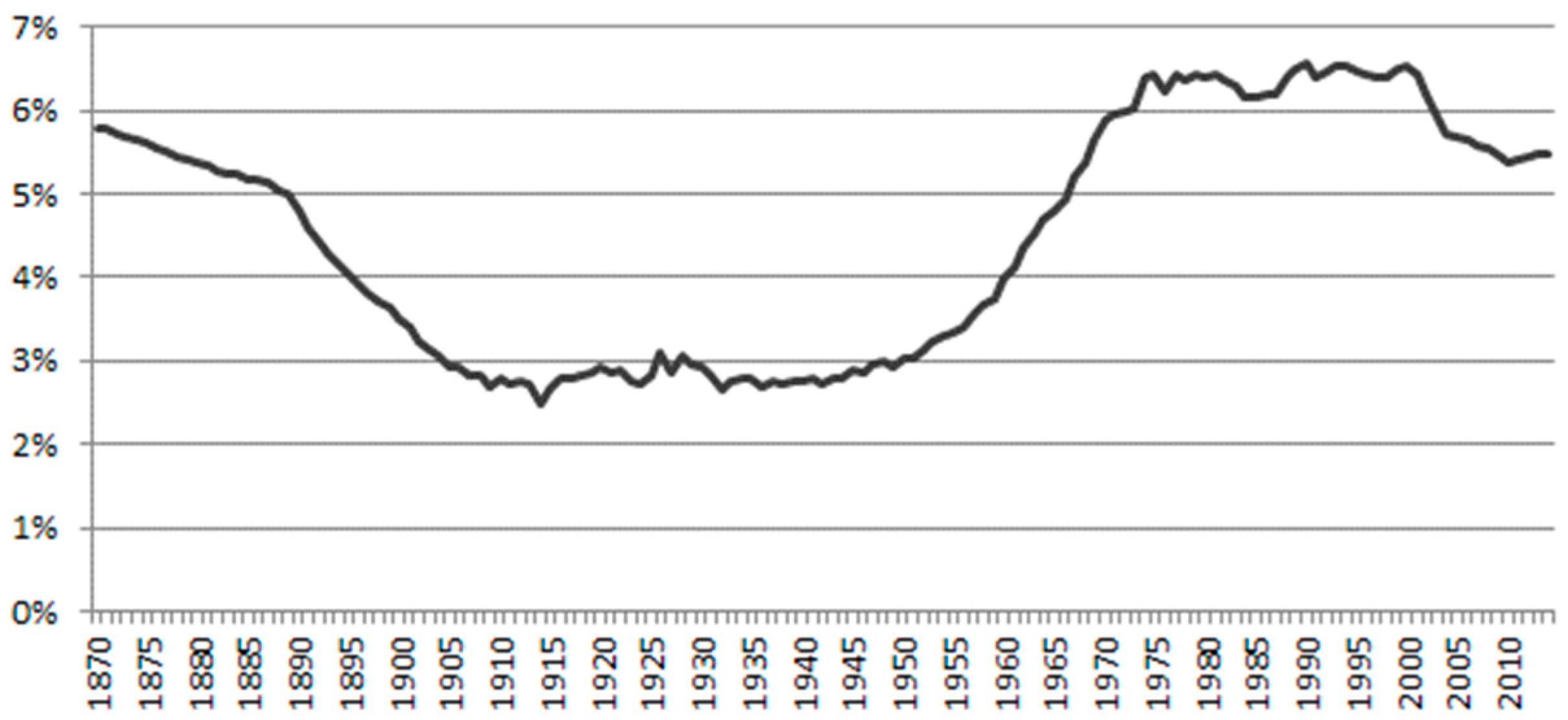

- considers a fixed social discount rate, we consider an annual variable rate which we estimate.

- assumes a fixed growth rate of future incomes, we take advantage of the information constructed and forecast future rents according to past trajectory (144 years) of the rents.

- = pure time preference

- = changing life chance (negative sign)

- = marginal utility of consumption

- = expected consumption growth rate

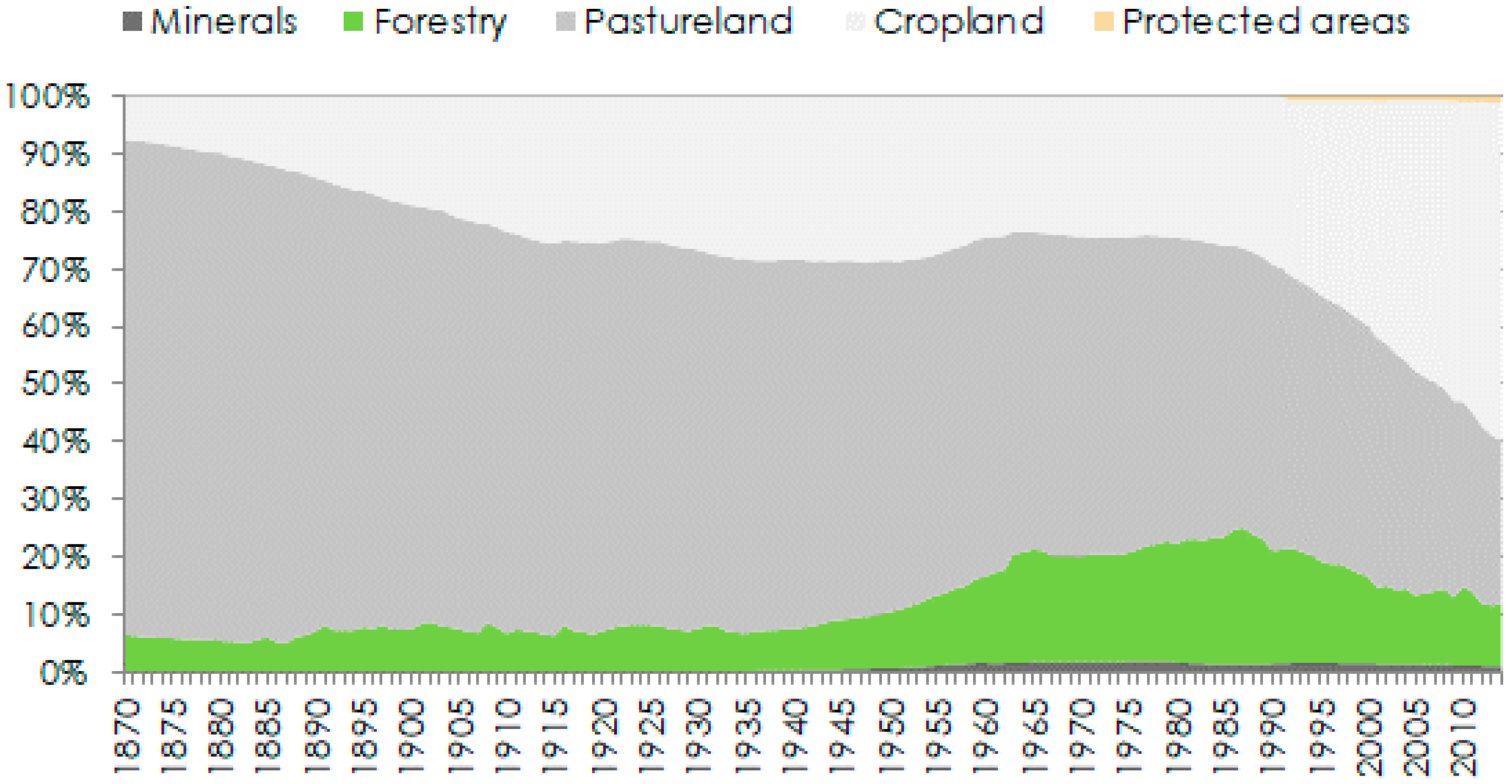

4.2. Natural Capital by Component

4.2.1. Cropland

4.2.2. Pastureland

4.2.3. Mineral Resources

4.2.4. Timber Resources

4.2.5. Non-Timber Forest Resources

4.2.6. Protected Areas

4.3. Comparison with Previous Estimates

4.4. Contrast with Linear Non-Causality

5. Results

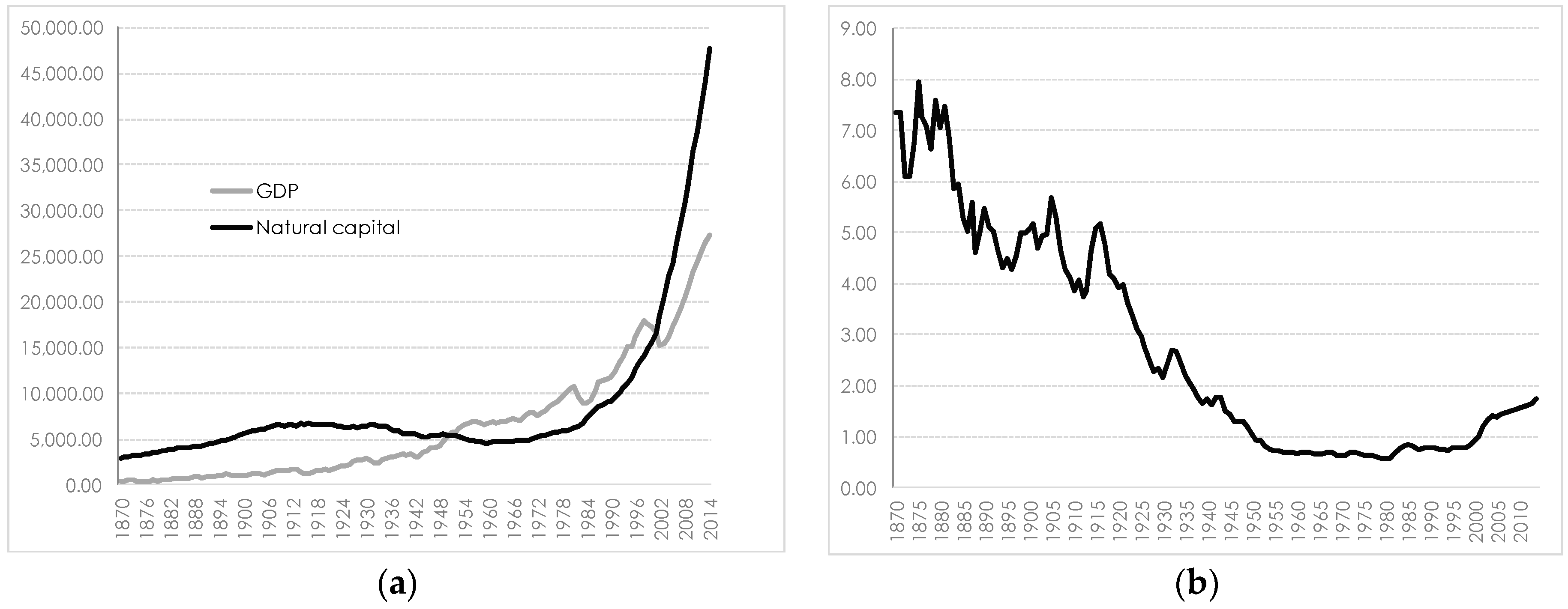

5.1. Some Stylized Facts

5.2. Causality Exercises

6. Discussion

7. Conclusions

Supplementary Materials

Acknowledgments

Author Contributions

Conflicts of Interest

Appendix. Measuring the Consumption Rate of Interest

- = pure time preference.

- = changing life chance (negative sign).

- = marginal utility of consumption.

- = expected growth rate of consumption.

- : investment ratio,

- : expected rate of return on investment,

- : expected growth rate of incomes from work.

References

- Sachs, J. How to handle the macroeconomics of oil wealth. In Escaping the Resource Curse; Humphreys, M., Sachs, J., Stiglitz, J., Eds.; Columbia University Press: New York, NY, USA, 2007; pp. 173–193. [Google Scholar]

- Badeeb, R.; Lean, H.; Clark, J. The evolution of the natural resource curse thesis: A critical literature survey. Resour. Policy 2017, 51, 123–134. [Google Scholar] [CrossRef]

- Auty, R. Sustaining Development in Mineral Economies: The Resource Curse Thesis; Routledge: London, UK, 1993. [Google Scholar]

- Manzano, O.; Rigobon, R. Resource Curse of Debt Overhang? National Bureau of Economic Research: Cambridge, MA, USA, 2001; pp. 1–37. [Google Scholar]

- Leite, C.; Weidmann, J. Does Mother Nature Corrupt? Natural Resources, Corruption and Economic Growth; International Monetary Fund: Washington, DC, USA, 1999. [Google Scholar]

- Van der Ploeg, F. Natural resources: Curse or blessing? J. Econ. Lit. 2011, 49, 366–420. [Google Scholar] [CrossRef]

- Torvik, R. Why do some resource-abundant countries succeed while others do not? Oxf. Rev. Econ. Policy 2009, 25, 241–256. [Google Scholar] [CrossRef]

- Willebald, H.; Badía-Miró, M.; Pinilla, V. Introduction: Natural resources and economic development. What can we learn from history? In Natural Resources and Economic Growth: Learning from History; Badía-Miró, M., Pinilla, V., Willebald, H., Eds.; Routledge Explorations in Economic History; Taylor & Francis Group: London, UK; New York, NY, USA, 2015; pp. 21–45. [Google Scholar]

- Barbier, E. Frontier expansion and economic development. Contemp. Econ. Policy 2005, 23, 165–316. [Google Scholar] [CrossRef]

- David, P.; Wright, G. Increasing returns and the genesis of American resource abundance. Ind. Corp. Chang. 1997, 6, 203–245. [Google Scholar] [CrossRef]

- Wright, G. Resource-based growth then and now. In Patterns of Integration in the Global Economy; World Bank Project, Ed.; World Bank: Washington, DC, USA, 2001. [Google Scholar]

- Cimoli, M.; Porcile, G.; Primi, A.; Vergara, S. Cambio estructural, heterogeneidad productiva y tecnología en América Latina. In Heterogeneidad Estructural, Asimetrías Tecnológicas y Crecimiento en América Latina; Cimoli, M., Ed.; CEPAL-BID: Santiago de Chile, Chile, 2005; pp. 9–39. [Google Scholar]

- Presbich, R. El desarrollo económico de la América Latina y algunos de sus principales problemas. El Trimest. Econ. 1949, 16, 347–431. [Google Scholar]

- Singer, H. The distribution of gains between investing and borrowing countries. Am. Econ. Rev. 1950, 40, 473–485. [Google Scholar]

- Seers, D. A model of comparative rates of growth in the world economy. Econ. J. 1962, 72, 45–78. [Google Scholar] [CrossRef]

- McCombie, J.; Roberts, M. The role of the balance of payments in economic growth. In The Economics of Demand-Led Growth. Challenging the Supply-Side Vision of the Long Run; Setterfield, M., Ed.; Wiley: Hoboken, NJ, USA, 2002; pp. 87–114. [Google Scholar]

- Dosi, G.; Nelson, R. Technical change and industrial dynamics as evolutionary processes. In Handbook of the Economics of Innovation; Hall, B., Rosenberg, N., Eds.; North Holland: Amsterdam, The Netherlands, 2010; pp. 51–127. [Google Scholar]

- Corden, W.; Neary, J. Booming sector and de-industrialization in a small open economy. Econ. J. 1982, 92, 825–848. [Google Scholar] [CrossRef]

- Corden, W. Booming sector and Dutch disease economics: Survey and consolidation. Oxf. Econ. Pap. 1984, 36, 359–380. [Google Scholar] [CrossRef]

- Neary, J.; van Wijnbergen, S. Natural Resources and the Macroeconomy; MIT Press: Cambridge, MA, USA, 1986. [Google Scholar]

- Gylfason, T. Natural resources and economic growth: From dependence to diversification. In Economic Liberalization and Integration Policy: Options for Eastern Europe and Russia; Broadman, H.G., Paas, T., Welfens, P.J.J., Eds.; Springer: Berlín, Germany, 2006. [Google Scholar]

- Sachs, J.; Warner, A. The curse of natural resources. Eur. Econ. Rev. 2001, 45, 827–838. [Google Scholar] [CrossRef]

- Auty, R. Introduction and Overview. In Resource Abundance and Economic Development; Auty, R., Ed.; Oxford University Press: Oxford, UK, 2001; pp. 3–18. [Google Scholar]

- Bulte, E.; Damania, R.; Deacon, R. Resource intensity, institutions, and development. World Dev. 2005, 33, 1029–1044. [Google Scholar] [CrossRef]

- Sala-i-Martin, X.; Subramanian, A. Addressing the natural resource curse: An illustration from Nigeria. J. Afr. Econ. 2013, 22, 570–615. [Google Scholar] [CrossRef]

- Auty, R. The political economy of resource-driven growth. Eur. Econ. Rev. 2001, 45, 839–846. [Google Scholar] [CrossRef]

- Isham, J.; Woolcock, M.; Pritchett, L.; Busby, G. The varieties of resource experience: Natural resource export structures and the political economy of economic growth. World Bank Econ. Rev. 2005, 19, 141–174. [Google Scholar] [CrossRef]

- Woolcock, M.; Prichett, L.; Isham, J. The social foundations of poor economic growth in resource-rich economies. In Resource Abundance and Economic Development; Oxford University Press: New York, NY, USA, 2001. [Google Scholar]

- Boschini, A.; Pettersson, J.; Roine, J. Resource curse or not: A question of appropriability. Scand. J. Econ. 2007, 109, 593–617. [Google Scholar] [CrossRef]

- Birdsall, N.; Pinckney, T.; Sabot, R. Natural Resources, Human Capital, and Growth; Carnegie Endowment for International Peace: Washington, DC, USA, 2000. [Google Scholar]

- Wood, A.; Mayer, J. Africa’s export structure in a comparative perspective. Camb. J. Econ. 2001, 25, 369–394. [Google Scholar] [CrossRef]

- Bravo, C.; De Gregorio, J. The Relative Richness of the Poor? Natural Resources, Human Capital and Economic Growth; The World Bank Policy Research; World Bank: Washington, DC, USA, 2005. [Google Scholar]

- Barbier, E. Scarcity, frontiers and the resource curse: A historical perspective. In Natural Resources and Economic Growth: Learning from History; Badía-Miró, M., Pinilla, V., Willebald, H., Eds.; Routledge Explorations in Economic History; Taylor & Francis Group: London, UK; New York, NY, USA, 2015; pp. 54–76. [Google Scholar]

- Acemoglu, D.; Johnson, S.; Robinson, J. The colonial origins of comparative development: An empirical Investigation. Am. Econ. Rev. 2001, 91, 1369–1401. [Google Scholar] [CrossRef]

- Engerman, S.; Sokoloff, K. Factor endowments, institutions, and differential paths of growth among new world economies. In How Latin America Fell Behind: Essays on the Economic Histories of Brazil and Mexico; Haber, S., Ed.; Stanford University Press: Stanford, CA, USA, 1997; pp. 260–304. [Google Scholar]

- Engerman, S.; Sokoloff, K. Factor Endowments, Inequality, and Paths of Development among New World Economies; National Bureau of Economic Research: Cambridge, MA, USA, 2002. [Google Scholar]

- Gelb, A.H. Oil Windfalls: Blessing or Curse? Cambridge University Press: New York, NY, USA, 1998. [Google Scholar]

- Sachs, J.; Warner, A. Natural Resource Abundance and Economic Growth; National Bureau of Economic Research: Cambridge, MA, USA, 1995. [Google Scholar]

- Neumayer, E. Does the “resource curse” hold for growth in genuine income as well? World Dev. 2004, 32, 1627–1640. [Google Scholar] [CrossRef]

- Arezki, R.; Van der Ploeg, F. Can the Natural Resource Curse be turned into a Blessing? The Role of Trade Policies and Institutions; International Monetary Fund: Washington, DC, USA, 2011. [Google Scholar]

- Beck, T. Finance and Oil: Is There a Resource Curse in Financial Development? Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1769803 (accessed on 20 February 2018).

- Boschini, A.; Pettersson, J.; Roine, J. The resource curse and its potential reversal. World Dev. 2013, 43, 19–41. [Google Scholar] [CrossRef]

- Ross, M. A closer look at oil, diamonds, and civil war. Annu. Rev. Political Sci. 2006, 9, 265–300. [Google Scholar] [CrossRef]

- Auty, R. The resource curse and sustainable development. In Handbook of Sustainable Development; Atkinson, G., Dietz, S., Neumayer, E., Eds.; Edward Elgar: Cheltenham, UK, 2007; pp. 207–219. [Google Scholar]

- Collier, P.; Hoeffler, A. Testing the neocon agenda: Democracy in resource-rich societies. Eur. Econ. Rev. 2009, 53, 293–308. [Google Scholar] [CrossRef]

- Boos, A.; Holm-Müller, K. The relationship between the resource curse and genuine savings: Empirical evidence. J. Sustain. Dev. 2013, 6, 59–72. [Google Scholar] [CrossRef]

- Bhattacharyya, S.; Hodler, R. Do Natural Resource Revenues Hinder Financial Development? The Role of Political Institutions; Oxford Centre for the Analysis of Resource Rich Economies: Oxford, UK, 2014. [Google Scholar]

- Bhattacharyya, S.; Collier, P. Public Capital in Resource Rich Economies: Is there a Curse? Center for the Study of African Economies: Oxford, UK, 2014. [Google Scholar]

- Gylfason, T. Nature, power and growth. Scott. J. Political Econ. 2001, 48, 558–588. [Google Scholar] [CrossRef]

- Dietz, S.; Neumayer, E.; De Soysa, I. Corruption, the resource curse and genuine saving. Environ. Dev. Econ. 2007, 12, 33–53. [Google Scholar] [CrossRef]

- Barajas, M.; Chami, M.; Yousefi, M. The Finance and Growth Nexus Re-Examined: Do All Countries Benefit Equally? International Monetary Fund: Washington, DC, USA, 2013. [Google Scholar]

- Daniele, V. Natural resources and the ‘quality’of economic development. J. Dev. Stud. 2011, 47, 545–573. [Google Scholar] [CrossRef]

- Stijns, J. Natural resource abundance and economic growth revisited. Resour. Policy 2005, 30, 107–130. [Google Scholar] [CrossRef]

- Brunnschweiler, C. Cursing the blessings? Natural resource abundance, institutions, and economic growth. World Dev. 2008, 36, 399–419. [Google Scholar] [CrossRef]

- Brunnschweiler, C.; Bulte, E. The resource curse revisited and revised: A tale of paradoxes and red herrings. J. Environ. Econ. Manag. 2008, 55, 248–264. [Google Scholar] [CrossRef]

- Dartey-Baah, K.; Amponsah-Tawiah, K.; Aratuo, D. Emerging “Dutch disease” in emerging oil economy: Ghana’s perspective. Soc. Bus. Rev. 2012, 7, 185–199. [Google Scholar] [CrossRef]

- Papyrakis, E.; Gerlagh, R. Resource abundance and economic growth in the United States. Eur. Econ. Rev. 2007, 51, 1011–1039. [Google Scholar] [CrossRef]

- Pegg, S. Is there a Dutch disease in Botswana? Resour. Policy 2010, 35, 14–19. [Google Scholar] [CrossRef]

- Fosu, A.; Gyapong, A. Terms of trade and growth of resource economies: Contrasting evidence from two African countries. In Beyond the Curse: Policies to Harness the Power of Natural Resources; Arezki, R., Gylfason, T., Sy, A., Eds.; International Monetary Fund: Washington, DC, USA, 2011; pp. 257–272. [Google Scholar]

- De Gregorio, J.; Labbé, F. Copper, The real exchange rate and macroeconomic fluctuations in Chile. In Beyond the Curse: Policies to Harness the Power of Natural Resources; Arezki, R., Gylfason, T., Sy, A., Eds.; International Monetary Fund: Washington, DC, USA, 2011; pp. 203–233. [Google Scholar]

- Gylfason, T. Natural Resource Endowment: A Mixed Blessing? Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1766385 (accessed on 20 February 2018).

- Loayza, N.; Mier y Teran, A.; Rigolini, J. Poverty, Inequality, and the Local Natural Resource Curse; World Bank, Policy Research Working Paper; World Bank: Washington, DC, USA, 2013. [Google Scholar]

- Liu, Y. Is the natural resource production a blessing or curse for China’s urbanization? Evidence from a space–time panel data model. Econ. Model. 2014, 38, 404–416. [Google Scholar] [CrossRef]

- Hammond, J. The resource curse and oil revenues in Angola and Venezuela. Sci. Soc. 2011, 75, 348–378. [Google Scholar] [CrossRef]

- Rubio, M. Oil illusion and delusion: Mexico and Venezuela over the twentieth century. In Natural Resources and Economic Growth: Learning from History; Badía-Miró, M., Pinilla, V., Willebald, H., Eds.; Routledge Explorations in Economic History; Taylor & Francis Group: London, UK; New York, NY, USA, 2015; pp. 160–183. [Google Scholar]

- Marwah, H. Oil as sweet as honey: Linking natural resources, government institutions and domestic capital investment in Nigeria 1960–2000. In Natural Resources and Economic Growth: Learning from History; Badía-Miró, M., Pinilla, V., Willebald, H., Eds.; Routledge Explorations in Economic History; Taylor & Francis Group: London, UK; New York, NY, USA, 2015; pp. 100–118. [Google Scholar]

- Stijns, J. Natural resource abundance and human capital accumulation. World Dev. 2006, 34, 1060–1083. [Google Scholar] [CrossRef]

- Blanco, L.; Grier, R. Natural resource dependence and the accumulation of physical and human capital in Latin America. Resour. Policy 2012, 37, 281–295. [Google Scholar] [CrossRef]

- Shao, S.; Yang, L. Natural resource dependence, human capital accumulation, and economic growth: A combined explanation for the resource curse and the resource blessing. Energy Policy 2014, 74, 632–642. [Google Scholar] [CrossRef]

- Atkinson, G.; Hamilton, K. Savings, growth and the resource curse hypothesis. World Dev. 2003, 31, 1793–1801. [Google Scholar] [CrossRef]

- Wood, A.; Berge, K. Exporting manufactures: Human resources, Natural Resources, and Trade Policy. J. Dev. Stud. 1997, 34, 35–59. [Google Scholar] [CrossRef]

- Bornhorst, F.; Thornton, J.; Gupta, S. Natural Resource Endowments, Governance, and the Domestic Revenue Effort: Evidence from a Panel of Countries; International Monetary Fund: Washington, DC, USA, 2008. [Google Scholar]

- Mehlum, H.; Moene, K.; Torvik, R. Institutions and the resource curse. Econ. J. 2006, 116, 1–20. [Google Scholar] [CrossRef]

- Alexeev, M.; Conrad, R. The elusive curse of oil. Rev. Econ. Stat. 2009, 91, 586–598. [Google Scholar] [CrossRef]

- Lederman, D.; Maloney, W. Natural Resources: Neither Curse nor Destiny; The World Bank: Washington, DC, USA, 2007. [Google Scholar]

- Boyce, J.; Herbert Emery, J. Is a negative correlation between resource abundance and growth sufficient evidence that there is a “resource curse”? Resour. Policy 2011, 36, 1–13. [Google Scholar] [CrossRef]

- Cavalcanti, T.; Mohaddes, K.; Raissi, M. Growth, development and natural resources: New evidence using a heterogeneous panel analysis. Q. Rev. Econ. Finance 2011, 51, 305–318. [Google Scholar] [CrossRef]

- James, A. The resource curse: A statistical mirage? J. Dev. Econ. 2015, 114, 55–63. [Google Scholar] [CrossRef]

- Auty, R. From resource cruse to rent curse: A theoretical perspective. In Natural Resources and Economic Growth: Learning from History; Badía-Miró, M., Pinilla, V., Willebald, H., Eds.; Routledge Explorations in Economic History; Taylor & Francis Group: London, UK; New York, NY, USA, 2015. [Google Scholar]

- Lewis, W. Crecimiento y Fluctuaciones; Fundación de Cultura Económica: Buenos Aires, Argentina, 1983; p. 209. [Google Scholar]

- Foreman-Peck, J. A History of the World Economy. International Economic Relations since 1850; Harvester Press: Brighton, UK, 1983. [Google Scholar]

- Álvarez, J.; Bilancini, E.; D’Alessandro, S.; Porcile, G. Agricultural institutions, industrialization and growth: The case of New Zealand and Uruguay in 1870–1940. Explor. Econ. Hist. 2011, 48, 151–168. [Google Scholar] [CrossRef]

- Willebald, H.; Bértola, L. Uneven development paths among Settler Societies, 1870–2000. In Settler Economies in World History; Lloyd, C., Metzer, J., Sutch, R., Eds.; Brill: Leiden, The Netherlands, 2013; pp. 105–140. [Google Scholar]

- Wellstead, A. The (post) staples economy and the (post) staples state in historical perspective. Can. Political Sci. Rev. 2007, 1, 8–25. [Google Scholar]

- Bértola, L. Overview of the Economic History of Uruguay Since the 1870s. Available online: http://eh.net/encyclopedia/article/Bertola.Uruguay.final (accessed on 20 February 2018).

- Oddone, G. El Declive. Una Mirada de la Economía de Uruguay en el Siglo XX; Librería Linardi y Risso: Montevideo, Uruguay, 2010. [Google Scholar]

- Bulmer-Thomas, V. The Economic History of Latin America since Independence; Cambridge University Press: Cambridge, UK, 2003. [Google Scholar]

- Bonino, N.; Tena, A.; Willebald, H. Uruguay and the first globalization: On the accuracy of export performance, 1870–1913. Rev. Hist. Econ. 2015, 33, 287–320. [Google Scholar]

- Willebald, H. Desigualdad y especialización en el crecimiento de las economías templadas de nuevo asentamiento, 1870–1940. Rev. Hist. Econ. 2007, 25, 293–348. [Google Scholar] [CrossRef]

- Bonino, N.; Román, C.; Willebald, H. Structural change and long-term patterns. A methodological proposal for Uruguay in the very long run. In Proceedings of the Seminario de Investigación, Programa de Historia Económica y Social, PHES-FCS-UdelaR, Montevideo, Uruguay, 6 September 2012. [Google Scholar]

- Jacob, R. Uruguay 1929–1938: Depresión Ganadera y Desarrollo Fabril; Fundación de Cultura Universitaria: Montevideo, Uruguay, 1981; p. 432. [Google Scholar]

- Bértola, L. La Industria Manufacturera Uruguaya 1913–1961: Un Enfoque Sectorial de su Crecimiento, Fluctuaciones y Crisis; Facultad de Ciencias Sociales de la Universidad de la República y Centro Interdisciplinario de Estudios sobre el Desarrollo Uruguay: Montevideo, Uruguay, 1993. [Google Scholar]

- Arnabal, L.; Bertino, M.; Fleitas, S. Una revisión Del desempeño de la industria en Uruguay entre 1930 y 1959. Rev. Hist. Ind. 2013, 13, 143–173. [Google Scholar]

- Astori, D. Estancamiento, desequilibrios y ruptura. 1955–1972. In El Uruguay Del Siglo XX; Instituto de Economía, Ed.; Ediciones de la Banda Oriental: Montevideo, Uruguay, 2001. [Google Scholar]

- Paolino, C.; Pittaluga, L.; Mondelli, M. Cambios en la Dinámica Agropecuaria y Agroindustrial del Uruguay y Las Políticas Públicas; Serie Estudios y Perspectivas CEPAL; CEPAL: Santiago de Chile, Chile, 2014. [Google Scholar]

- Bértola, L.; Isabella, F.; Saavedra, C. El Ciclo Económico de Uruguay, 1998–2012; Documento de Trabajo Facultad de Ciencias Sociales; Facultad de Ciencias Sociales: Montevideo, Uruguay, 2014. [Google Scholar]

- Reyes Abadie, W. La Banda Oriental: Pradera, Frontera, Puerto; Ediciones de la Banda Oriental: Montevideo, Uruguay, 1966. [Google Scholar]

- Barrán, J.; Nahum, B. Historia Rural del Uruguay Moderno; Ediciones de la Banda Oriental: Montevideo, Uruguay, 1978. [Google Scholar]

- Instituto de Economía. El Proceso Económico del Uruguay; Fondo de Cultura Universitaria: Montevideo, Uruguay, 1969. [Google Scholar]

- World Bank. The Changing Wealth of Nations: Measuring Sustainable Development in the New Millennium; The World Bank: Washington, DC, USA, 2011. [Google Scholar]

- World Bank. Where Is the Wealth of Nations? Measuring Capital for the 21st Century; The World Bank: Washington, DC, USA, 2006. [Google Scholar]

- Ding, N.; Field, B. Natural Resource Abundance and Economic Growth; University of Massachusetts Amherst: Amherst, MA, USA, 2005. [Google Scholar]

- Sandonato, S. Capital Natural en Uruguay. 1990–2010. Propuesta Metodológica, Estimaciones y Ejercicios de Descomposición. Bachelor’s Thesis, Universidad de la República, Montevideo, Uruguay, 2012. [Google Scholar]

- Willebald, H.; Sandonato, S. Indicadores de Capital Natural; Nota Técnica Nº 1, Series Documentos del Reporte Anual 2014; Recursos Naturales y Desarrollo Red Sudamericana de Economía Aplicada: Montevideo, Uruguay.

- Pearce, D.; Ulph, D. A social discount rate for the United Kingdom. In Environmental Economics: Essays in Ecological Economics and Sustainable Development; Pearce, D., Ed.; Edward Elgar Publishing: Cheltenham, UK, 1999; pp. 268–285. [Google Scholar]

- Lindmark, M.; Andersson, L. Where Was the Wealth of the Nation? Measuring Swedish Capital for the 19th and 20th Centuries; Centre for Environmental and Resource Economics: Umea, Suecia, 2016. [Google Scholar]

- De Rosa, M.; Sinisclachi, S.; Vilá, J.; Vigorito, A.; Willebald, H. La Evolución de Las Remuneraciones Laborales y la Distribución del Ingreso en Uruguay; Futuro en Foco, Cuadernos Sobre Desarrollo Humano: Montevideo, Uruguay, 2017. [Google Scholar]

- Román, C.; Bertoni, R. Auge y ocaso Del carbón mineral en Uruguay. Un análisis histórico desde fines del siglo XIX hasta la actualidad. Rev. Hist. Econ. 2013, 31, 459–497. [Google Scholar]

- Lampietti, J.; Dixon, J. To See the Forest for the Trees: A Guide to Non-Timber Forest Benefits; Environment Department Paper; World Bank: Washington, DC, USA, 1995. [Google Scholar]

- Giles, J.; Mirza, S. Some Pretesting Issues on Testing for Granger Non Causality; Econometrics Working Paper; University of Victoria: Victoria, BC, Canada, 1999. [Google Scholar]

- Lingarde, S.; Tylecote, A. Resource-rich countries’ success and failure in technological ascent, 1870–1970: The Nordic countries versus Argentina, Uruguay and Brazil. J. Eur. Econ. Hist. 1999, 28, 77–114. [Google Scholar]

- Bertino, M.; Bertoni, R.; Tajam, H.; Yaffé, J. Historia Económica Del Uruguay. Tomo III: La Economía Del Batllismo y de los Años Veinte; Fin de Siglo: Montevideo, Uruguay, 2005. [Google Scholar]

- Moraes, I. La Pradera Perdida. Historia y Economía Del Agro Uruguayo: Una Visión de Largo Plazo, 1760–1970; Linardi y Risso: Montevideo, Uruguay, 2008. [Google Scholar]

- Martín-Retortillo, M.; Pinilla, V.; Velazco, J.; Willebald, H. The goose that laid the golden eggs? Agricultural development in Latin America in the 20th century. In Agricultural Development in the World Periphery: A Global Economic History Approach; Pinilla, V., Willebald, H., Eds.; Palgrave Studies in Economic History; Palgrave Macmillan: Basingstoke, UK, 2018. [Google Scholar]

- OPYPA-MGAP. El Desarrollo Agropecuario y Agro-Industrial de Uruguay; Reflexiones en el 50 Aniversario de la Oficina de Programación y Política Agropecuaria; MGAP-OPYPA: Montevideo, Uruguay, 2015. [Google Scholar]

- Castro, P. Distribución Regional de la Producción y Geografía Económica. El Caso Del Agro en Uruguay (1870–2008). Master’s Thesis, Universidad de la República, Montevideo, Uruguay, 2017. [Google Scholar]

- Bertoni, R. Energía y Desarrollo. La Restricción Energética en Uruguay Como Problema: 1882–2000; CSIC: Montevideo, Uruguay, 2011. [Google Scholar]

- Maddison, A. Ultimate and proximate growth causality: A critique of Mancur Olson on the rise and decline of nations. Scand. Hist. Rev. 1988, 36, 25–29. [Google Scholar] [CrossRef]

- Abramovitz, M. Thinking about growth. In Thinking about Growth and Other Essays on Economic Growth and Welfare; Abramovitz, M., Ed.; Cambridge University Press: Cambridge, UK, 1989; pp. 3–79. [Google Scholar]

- Rodrik, D. In Search of Prosperity. Analytic Narratives on Economic Growth; Princeton University Press: Princeton, NJ, USA, 2003. [Google Scholar]

- Szirmai, A. Proximate, Intermediate and Ultimate Causality: Theories and Experiences of Growth and Development; Working Paper Series on Institutions and Economic Growth; Maastricht Graduate School of Governance: Maastricht, The Netherlands, 2012. [Google Scholar]

- Román, C.; Willebald, H. Formación de capital en el largo plazo en Uruguay, 1870–2011. Investig. Hist. Econ. 2015, 11, 20–30. [Google Scholar] [CrossRef]

- Fleitas, S.; Rius, A.; Román, C.; Willebald, H. Contract Enforcement, Investment and Growth in Uruguay since 1870; Instituto de Economía: Montevideo, Uruguay, 2013. [Google Scholar]

- Román, C. El PIB Histórico Por el Lado Del Gasto en Uruguay, 1870–2016: Una Primera Aproximación, Unpublished work.

- Williamson, J. Land, labor and globalization in the third world, 1870–1940. J. Econ. Hist. 2002, 62, 55–85. [Google Scholar]

- Bértola, L.; Lorenzo, F. Witches in the south: Kuzntes-like swings in Argentina, Brazil and Uruguay since the 1870. In The Experience of Economic Growth; van Zanden, J., Heikenen, S., Eds.; Amsterdam University Press: Amsterdam, The Netherlands, 2004. [Google Scholar]

- Azar, P.; Bertino, M.; Bertoni, R.; Fleitas, S.; García Repetto, U.; Sanguinetti, C.; Sienra, M.; Torrelli, M. De Quiénes, Para Quiénes y Para Qué. Las Finanzas Públicas en el Uruguay del Siglo XX; Editorial Fin de Siglo: Montevideo, Uruguay, 2009. [Google Scholar]

- Azar, P. Public Education Spending: Efficiency, Productivity and Politics. Ph.D. Thesis, Universtat Autònoma de Barcelona, Barcelona, España, 2017. [Google Scholar]

- Roldós, J. A long-run perspective on trade policy, instability, and growth. In The Effects of Protectionism on a Small Country. The Case of Uruguay; Connolly, M., De Melo, J., Eds.; The World Bank: Washington, DC, USA, 1994. [Google Scholar]

- Willebald, H. Land abundance, frontier expansion and appropriability: Settler economies during the first globalization. In Natural Resources and Economic Growth: Learning from History; Badía-Miró, M., Pinilla, V., Willebald, H., Eds.; Routledge Explorations in Economic History; Taylor & Francis Group: London, UK; New York, NY, USA, 2015; pp. 248–270. [Google Scholar]

- Schrijver, N. Sovereignty over Natural Resources: Balancing Rights and Duties; Cambridge University Press: New York, NY, USA, 2008. [Google Scholar]

- Czelusta, J.; Wright, G. Resource-based growth past and present. In Natural Resources: Neither Curse nor Destiny; Lederman, D., Maloney, W., Eds.; World Bank/Stanford University Press: Stanford, CA, USA, 2007; pp. 183–211. [Google Scholar]

- Angelsen, A. Cost-Benefit Analysis, Discounting, and the Environmental Critique: Overloading of the Discount Rate? Michelsen Institute Report; Chr. Michelsen Institute: Bergen, Norway, 1991. [Google Scholar]

- Lindmark, M.; Acar, S. Sustainability in the making? A Historical estimate of Swedish sustainable and unsustainable development 1850–2000. Ecol. Econ. 2013, 86, 176–187. [Google Scholar] [CrossRef]

- Chua, A.; Choong, W. A review of approaches to construct social discount rate. Sains Humanika 2016, 8, 37–42. [Google Scholar] [CrossRef]

- Sen, A. On optimizing the rate of saving. Econ. J. 1961, 71, 479–496. [Google Scholar] [CrossRef]

- Kay, J. Social discount rates. J. Public Econ. 1972, 1, 359–378. [Google Scholar] [CrossRef]

- Brum, C.; Román, C.; Willebald, H. Un Enfoque Monetario de la Inflación en el Largo Plazo. El Caso de Uruguay (1870–2010); El Trimestre Económico: Montevideo, Uruguay, 2016. [Google Scholar]

- Oddone, G. Restricciones para sostener el crecimiento: Lecciones y desafíos para las políticas públicas. In La Aventura Uruguaya. El País y el Mundo; Arocena, R., Caetano, G., Eds.; Debate: Montevideo, Uruguay, 2011; pp. 67–90. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

| Annual Growth Rates | NK/GDP | ||

|---|---|---|---|

| Natural Capital (NK) | GDP | ||

| 1870–1909 | 2.0% | 3.6% | 527.4% |

| 1910–1959 | −0.7% | 2.8% | 178.6% |

| 1960–2014 | 4.3% | 2.6% | 103.5% |

| 1870–2014 | 1.9% | 3.0% | 133.2% |

| Period | H0: lnNK Does Not Cause lnGDP | H0: lnGDP Does Not Cause lnNK | ||

|---|---|---|---|---|

| Statistic | p-Value | Statistic | p-Value | |

| 1870–1909 | 0.39 | 0.531 | 2.56 | 0.109 |

| 1910–1959 | 0.26 | 0.607 | 0.07 | 0.790 |

| 1960–2014 | 2.13 | 0.346 | 7.95 | 0.047 |

| 1870–2014 | 1.44 | 0.837 | 4.45 | 0.348 |

| 1870–1909 | 1910–1959 | 1960–2014 | ||||

|---|---|---|---|---|---|---|

| Statistic | p-Value | Statistic | p-Value | Statistic | p-Value | |

| Produced capital | 11.13 | 0.004 | 0.36 | 0.947 | 3.51 | 0.173 |

| Human capital | 0.40 | 0.525 | 9.86 | 0.043 | 2.67 | 0.102 |

| Exports | 0.63 | 0.429 | 7.76 | 0.021 | 0.76 | 0.385 |

| Terms of trade | 8.65 | 0.033 | 0.00 | 0.985 | 3.09 | 0.079 |

| 1870–1909 | 1910–1959 | 1960–2014 | ||||

|---|---|---|---|---|---|---|

| Statistic | p-Value | Statistic | p-Value | Statistic | p-Value | |

| Produced capital | 2.6 | 0.273 | 3.35 | 0.340 | 0.62 | 0.733 |

| Human capital | 0.44 | 0.506 | 8.41 | 0.078 | 0.27 | 0.600 |

| Exports | 0.96 | 0.328 | 3.04 | 0.219 | 1.44 | 0.229 |

| Terms of trade | 0.9 | 0.342 | 0.94 | 0.331 | 0.83 | 0.364 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sandonato, S.; Willebald, H. Natural Capital, Domestic Product and Proximate Causes of Economic Growth: Uruguay in the Long Run, 1870–2014. Sustainability 2018, 10, 715. https://doi.org/10.3390/su10030715

Sandonato S, Willebald H. Natural Capital, Domestic Product and Proximate Causes of Economic Growth: Uruguay in the Long Run, 1870–2014. Sustainability. 2018; 10(3):715. https://doi.org/10.3390/su10030715

Chicago/Turabian StyleSandonato, Silvana, and Henry Willebald. 2018. "Natural Capital, Domestic Product and Proximate Causes of Economic Growth: Uruguay in the Long Run, 1870–2014" Sustainability 10, no. 3: 715. https://doi.org/10.3390/su10030715

APA StyleSandonato, S., & Willebald, H. (2018). Natural Capital, Domestic Product and Proximate Causes of Economic Growth: Uruguay in the Long Run, 1870–2014. Sustainability, 10(3), 715. https://doi.org/10.3390/su10030715