Mapping ICT Use along the Citrus (Kinnow) Value Chain in Sargodha District, Pakistan

Abstract

:1. Introduction

2. The Citrus Industry in Pakistan

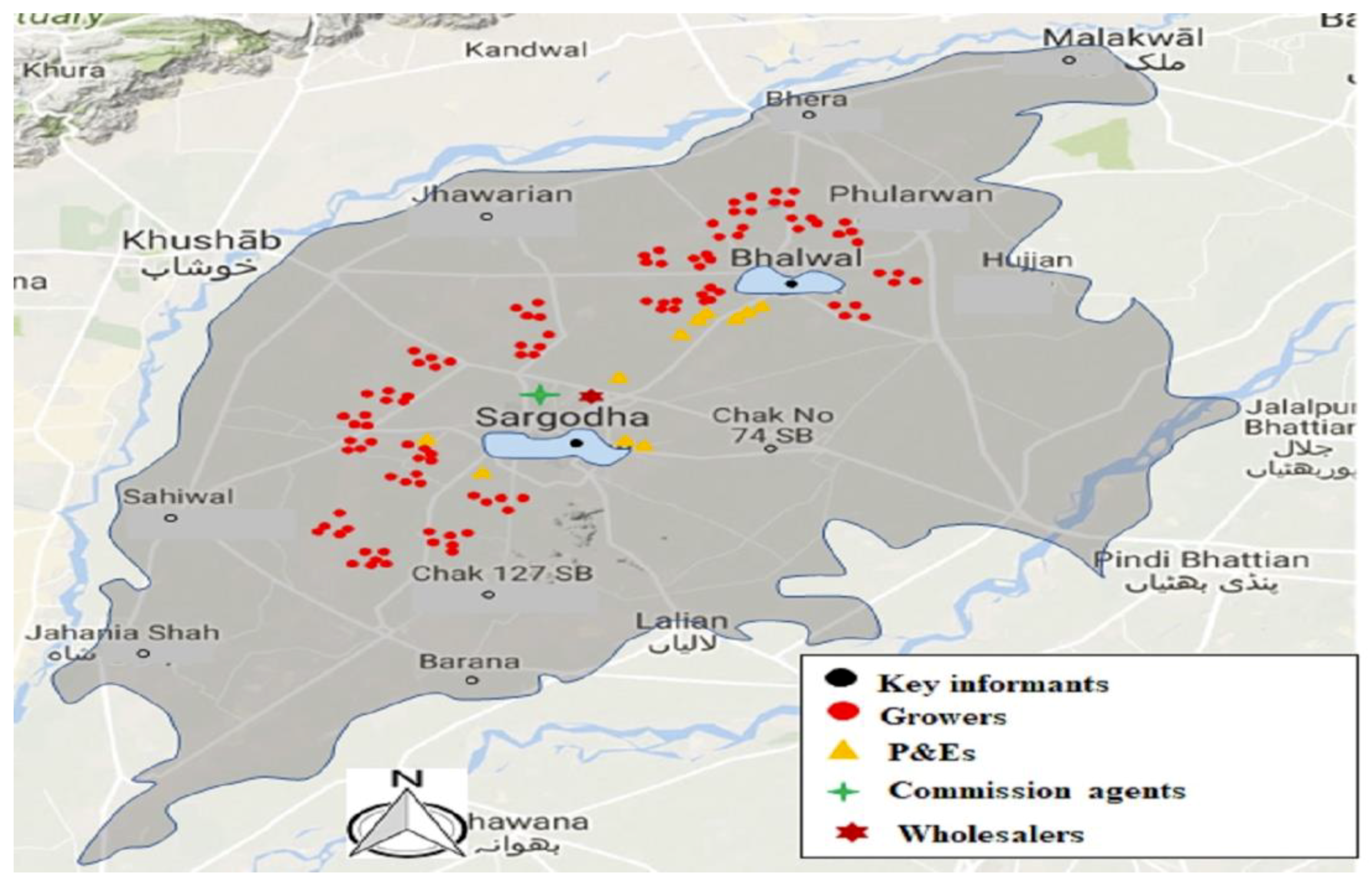

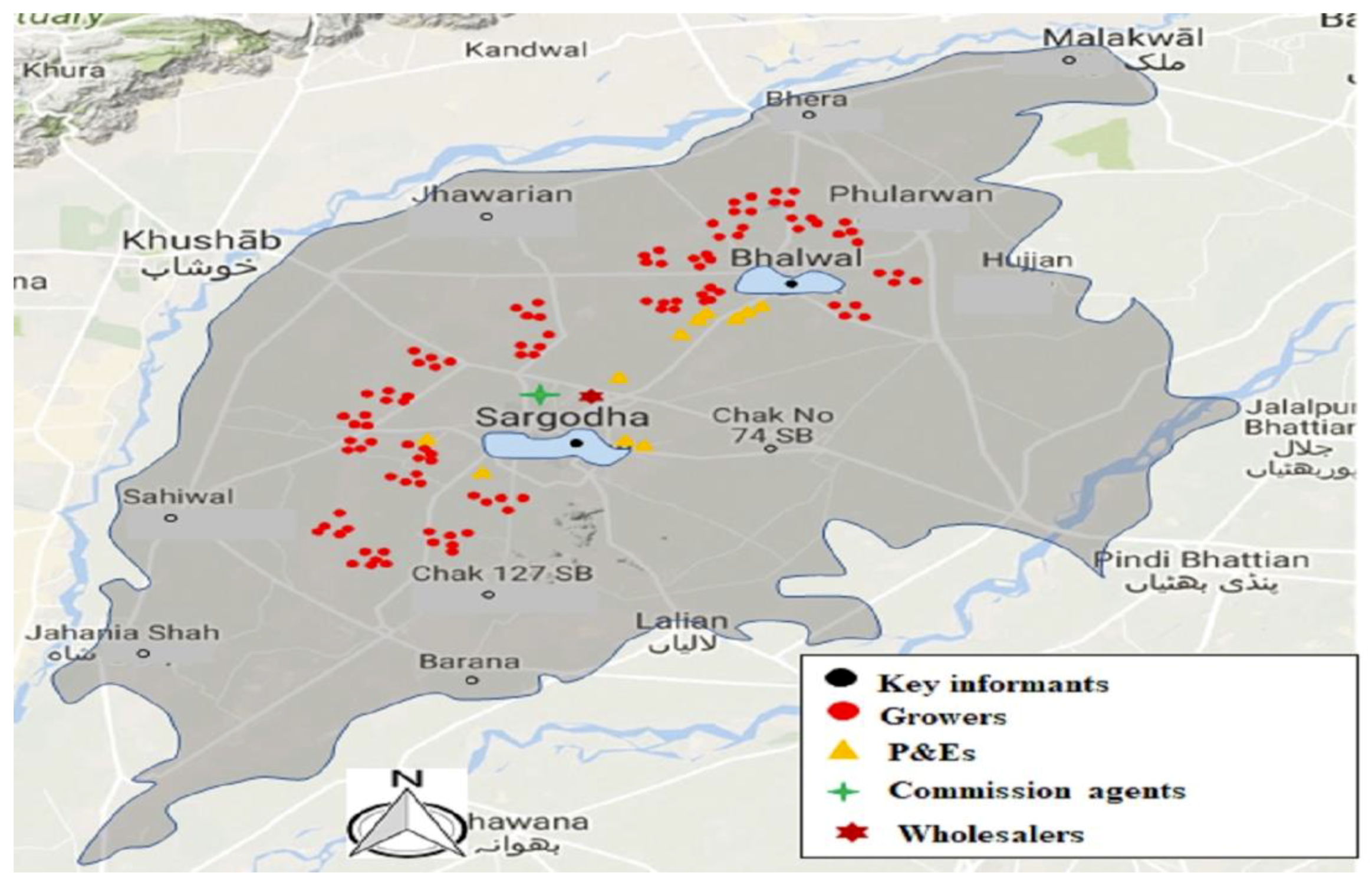

3. Methodology

- p = the probability that y = 1 if the respondent use ICT,

- 1 − p = the probability that y = 0 if the respondent does not use ICT,

- x = vector, the explanatory variables,

- β = vector, the coefficients of the explanatory variables, usually estimated by the maximum likelihood procedure,

- the log odds ratio of the probability that a grower use ICT.

4. Results and Discussion

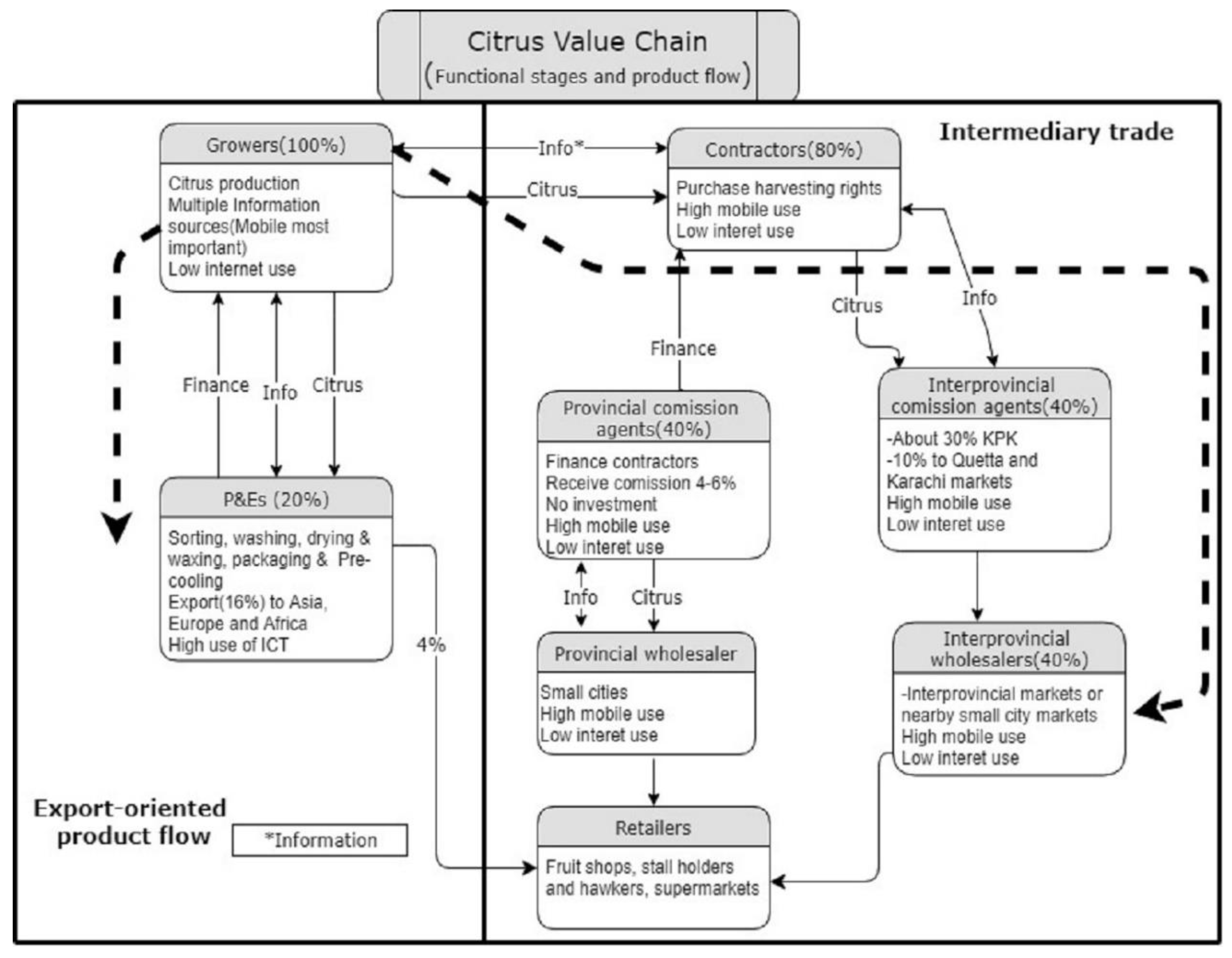

4.1. Citrus Production Stage

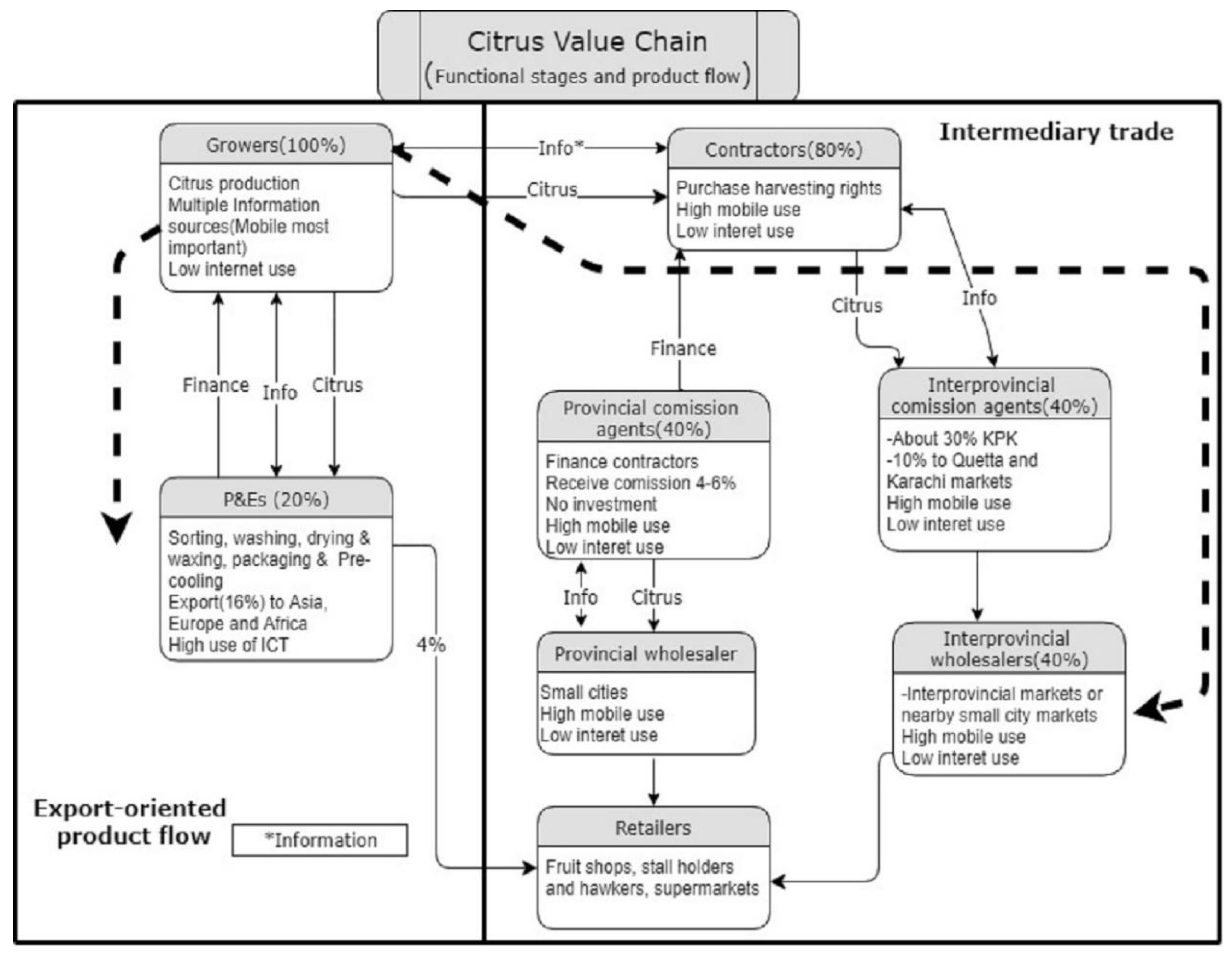

4.2. Citrus Intermediary Trade

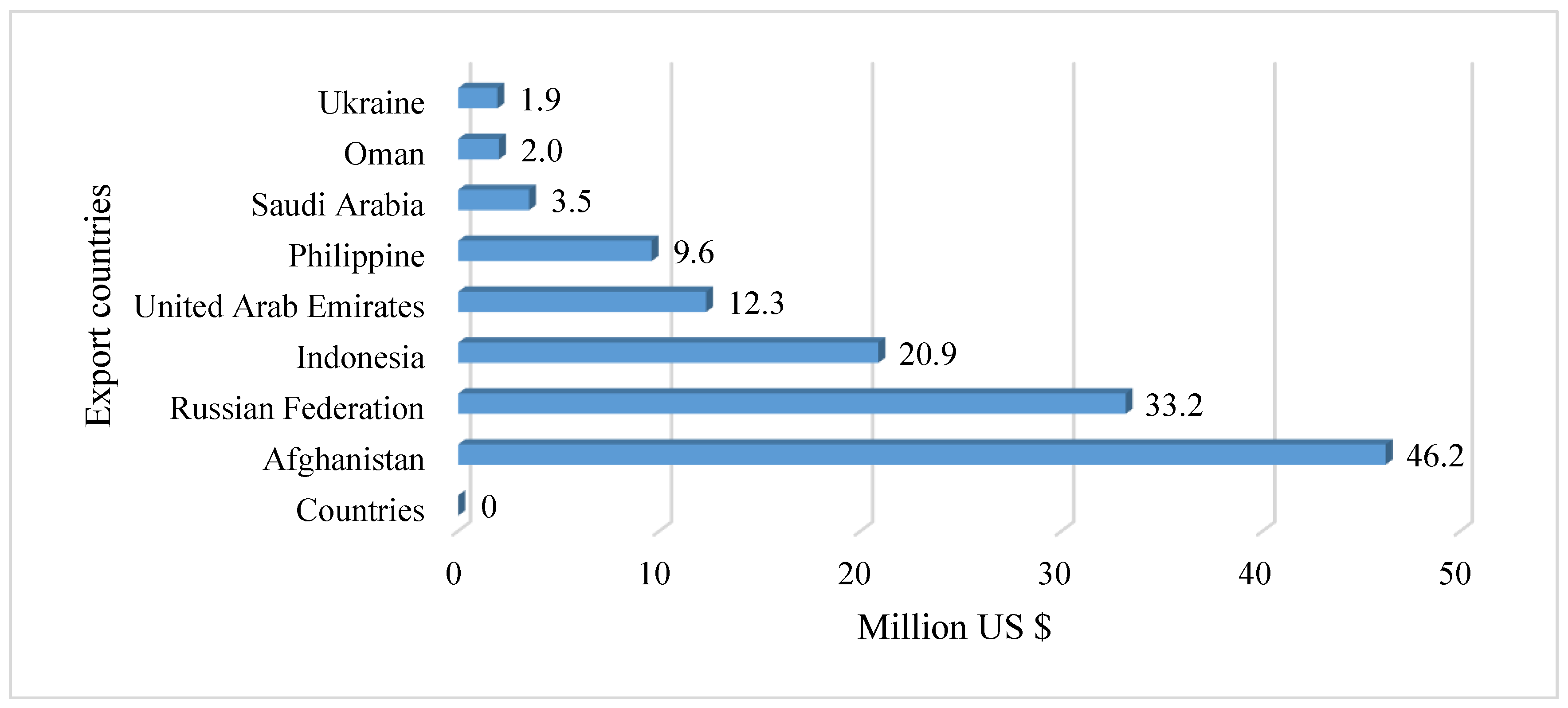

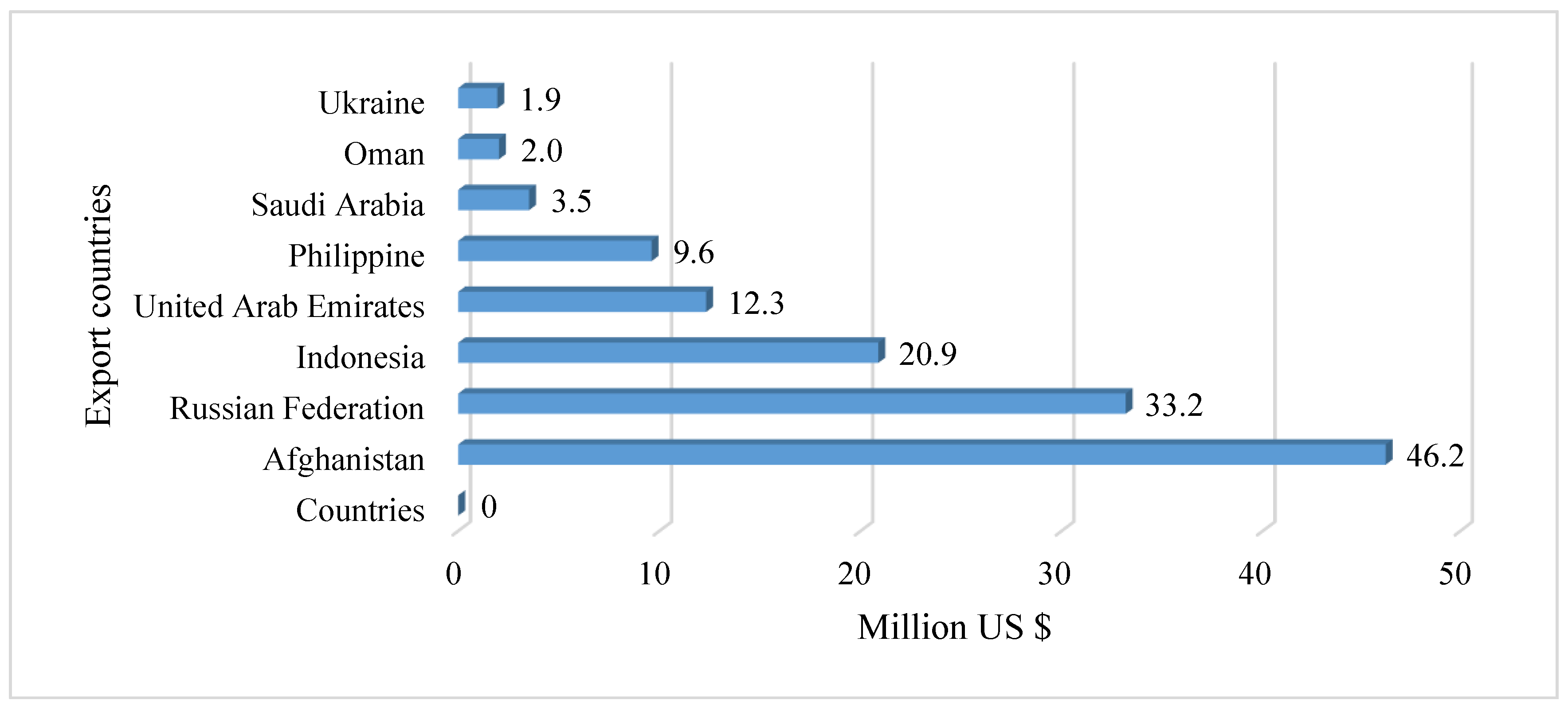

4.3. Citrus Processing and Export Stage

4.4. Discussion

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Sturgeon, T.; Zylberberg, E. The Global Information and Communications Technology Industry: Where Vietnam Fits in Global Value Chains; The World Bank: Washington, DC, USA, 2016. [Google Scholar]

- Group of Twenty. Towards Food and Water Security: Fostering Sustainability, Advancing Innovation Berlin, Germany; G-20: Berlin, Germany, 2017; Available online: http://www.g20.utoronto.ca/2017/170122-agriculture-en.pdf (accessed on 11 December 2018).

- Svenfelt, Å.; Zapico, J.L. Sustainable food systems with ICT? In Proceedings of the 4th International Conference ICT for Sustainability, ‘Smart and Sustainable’ (ICT4S 2016), Amsterdam, The Netherlands, 29 August–1 September 2016; pp. 194–201. [Google Scholar]

- Krmac, E.V. Intelligent value chain networks: business intelligence and other ICT tools and technologies in supply/demand chains. In Supply Chain Management-New Perspectives; InTechOpen: London, UK, 2011. [Google Scholar]

- Chopra, S.; Meindl, P. Supply chain management. Strategy, planning & operation. In Das Summa Summarum des Management; Springer: Berlin, Germany, 2007; pp. 265–275. [Google Scholar]

- Maqbool, S.; Rafiq, M.; Imran, M.; Qadeer, A.; Abbas, T. Role of Information and Communication Technology in supply chain management to create competitive advantage: A literature base study. Int. J. Res. Commer. IT Manag. 2014. Available online: https://www.researchgate.net/publication/261793707_CREATING_COMPETITIVE_ADVANTAGE_THROUGH_SUPPLY_CHAIN_MANAGEMENT (accessed on 11 December 2018).

- Chisita, C.T. Knotting and networking agricultural information services through Web 2.0 to create an informed farming community: A case of Zimbabwe. In Proceedings of the World Library and Information Congress: 78th IFLA General Conference and Assembly, Helsinki, Finland, 11–17 August 2012; pp. 11–17. [Google Scholar]

- De Silva, H.; Ratnadiwakara, D. Using ICT to Reduce Transaction Costs in Agriculture through Better Communication: A Case-Study from Sri Lanka; LIRNEasia: Colombo, Sri Lanka, 2008. [Google Scholar]

- Zylberberg, E. Redefining Brazil’s Role in Information and Communication Technology Global Value Chains. MIT-IPC Work. Pap. 2016. Available online: https://ipc.mit.edu/sites/default/files/documents/16-003.pdf (accessed on 11 December 2018 ).

- Townsend, J.H. Digital Taxonomy for Sustainability; University of Southampton: Southampton, UK, 2015. [Google Scholar]

- Chung, K.C.; Fleming, P.; Fleming, E. The impact of information and communication technology on international trade in fruit and vegetables in APEC. Asian-Pac. Econ. Lit. 2013, 27, 117–130. [Google Scholar] [CrossRef]

- Ebner, H.; Manouselis, N.; Palmér, M.; Enoksson, F.; Palavitsinis, N.; Kastrantas, K.; Naeve, A. Learning object annotation for agricultural learning repositories. In Proceedings of the 2009 Ninth IEEE International Conference on Advanced Learning Technologies, Riga, Latvia, 15–17 July 2009; pp. 438–442. [Google Scholar]

- Qingfeng, Z. E-commerce key to modernized farming. China Daily Europe, 29 January 2018. [Google Scholar]

- Siraj, M. Kinnow Value Chain Knowledge Gaps and ICT Prevalence in the Chain; CABI, South Asia: Rawalpindi, Pakistan, 2008. [Google Scholar]

- International Telecommunication Union. Measuring the Information Society Report; International Telecommunication Union: Geneva, Switzerland, 2016. [Google Scholar]

- Pakistan Bureau of Statistics. Pakistan Statistical Year Book; Pakistan Bureau of Statistics: Islamabad, Pakistan, 2016.

- Broad Band Commission. The State of Broadband: Broadband Catalyzing Sustainable Development; United Nations: Geneva, Switzerland, 2016. [Google Scholar]

- Hanif, U. Pakistan can improve ranking by adopting ICT. The Express Tribune, 25 March 2018. [Google Scholar]

- Taylor, N.; Rushton, J. A Value Chain Approach to Animal Diseases Risk Management: Technical Foundations and Practical Framework for Field Application; FAO: Rome, Italy, 2011; Volume 4. [Google Scholar]

- World Trade Organization. Pakistan Trade Profile; World Trade Organization: Geneva, Switzerland, 2016. [Google Scholar]

- Naseer, M. Report on export of Kinnow; Trade Development Authority of Pakistan: Islamabad, Pakistan, 2010.

- Sharif, M.; Farooq, U.; Malik, W.; Bashir, M. Citrus Marketing in Punjab: Constraints and Potential for Improvement [with Comments]. Pak. Dev. Rev. 2005, 44, 673–694. [Google Scholar] [CrossRef]

- Siddique, M.I.; Garnevska, E. Citrus Value Chain(s): A Survey of Pakistan Citrus Industry; IntechOpen: London, UK, 2018. [Google Scholar]

- Abbas, G. Pakistan exported record 370,000 tons of Kinnow in 2017–18. Pakistan Today, 6 June 2018. [Google Scholar]

- Singh, M.; Marchis, A.; Capri, E. Greening, new frontiers for research and employment in the agro-food sector. Sci. Total Environ. 2014, 472, 437–443. [Google Scholar] [CrossRef] [PubMed]

- Reardon, T.; Chen, K.; Minten, B.; Adriano, L. The Quiet Revolution in Staple Food Value Chains: Enter the Dragon, the Elephant, and the Tiger; Asian Development Bank: Mandaluyong, Philippines, 2012. [Google Scholar]

- Metro. Fruits and Vegetables. Available online: https://www.metro.pk/product-worlds/fruits-vegetables (accessed on 11 December 2018).

- Jan, I.; Ullah, S.; Akram, W.; Khan, N.P.; Asim, S.M.; Mahmood, Z.; Ahmad, M.N.; Ahmad, S.S. Adoption of improved cookstoves in Pakistan: A logit analysis. Biomass Bioenergy 2017, 103, 55–62. [Google Scholar] [CrossRef]

- Ouedraogo, B. Household energy preferences for cooking in urban Ouagadougou, Burkina Faso. Energy Policy 2006, 34, 3787–3795. [Google Scholar] [CrossRef]

- Ahsanuzzaman, A. Three Essays on Adoption and Impact of Agricultural Technology in Bangladesh; Virginia Tech: Blacksburg, VA, USA, 2015. [Google Scholar]

- Pandey, M.; Sikka, B.; Panthari, S. ICT system for increasing efficiency of apple-value chain. In Proceedings of the National Seminar, Arunachal Pradesh, India, 9–11 April 2011. [Google Scholar]

- Alarcon, P.; Fèvre, E.M.; Murungi, M.K.; Muinde, P.; Akoko, J.; Dominguez-Salas, P.; Kiambi, S.; Ahmed, S.; Häsler, B.; Rushton, J. Mapping of beef, sheep and goat food systems in Nairobi—A framework for policy making and the identification of structural vulnerabilities and deficiencies. Agric. Syst. 2017, 152, 1–17. [Google Scholar] [CrossRef] [PubMed]

- Makokha, S.; Witwer, M.; Monroy, L. Analysis of Incentives and Disincentives for Live Cattle in Kenya; Technical Notes Series, MAFAP, FAO, Rome (e Monitoring African Food and Agricultural Policies project-MAFAP); FAO: Rome, Italy, February 2013. [Google Scholar]

- UNCTAD. Information Economy Report 2006; United Nations: New York, NY, USA; Geneva, Switzerland, 2006. [Google Scholar]

- Mago, B.; Trivedi, P. Evidence of customers’ perceptions toward the usage of social networking sites as e-business mechanism in UAE. Eur. Sci. J. ESJ 2014, 10. [Google Scholar] [CrossRef]

- Liu, L.; Nath, H.K. Information and communications technology and trade in emerging market economies. Emerg. Mark. Financ. Trade 2013, 49, 67–87. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Data Collection Tools | Stakeholders | Data Collected |

|---|---|---|

| Structured Interviews (Questionnaires) | 121 growers, 25 contractors, 27 commission agents, 39 wholesalers, 10 processors and exporters (P&Es) | Demographic characteristics, information channels, level of information and communication technologies (ICT) use, membership of online discussion forums, role and activities at particular stage, value addition, production, contracting, marketing and export system |

| Semi-structured Interviews (Group interviews) | 3 P&Es managers, 5 progressive growers, 2 commission agents, 2 contractors, key informants (1 extension officer, 1 transporter, 1 social worker, 1 village leader, 1 fruit market president) | Their roles in the citrus value chain, impact of ICT on business operation, weaknesses and challenges they faced, suggestions to improve value chain (VC) efficiency through ICT use |

| Variables | Different Tools to Obtain Agricultural Information | Willingness to Invest in ICT | Online Network Membership | ICT’s Role in Price Determination | ||

|---|---|---|---|---|---|---|

| Mobile | Internet | Apps | ||||

| Age | - | - | - | - | - | + |

| Education | + | + | + | + | + | + |

| Farming experience | - | - | - | - | - | - |

| Land holding | + | + | + | + | + | + |

| Distance from local market | + | + | + | + | + | + |

| Distance from extension office | - | - | - | - | - | - |

| Distance from road | + | + | + | + | + | + |

| Parameters | Percentage |

|---|---|

| Sell orchard to contractors | 84.3% |

| Sell orchard to P&Es | 13.2% |

| Sell orchards at fruiting stage | 82.2% |

| Sell orchard at ripening stage | 15.7% |

| Orchard management by both contractors and growers | 91.7% |

| Lack of knowledge of destination of product | 71.9% |

| International quality-oriented growers | 14.9% |

| Characteristics | Mean | Minimum | Maximum | Std. Deviation |

|---|---|---|---|---|

| Age (years) | 45.17 | 24 | 73 | 12.797 |

| Education (years) | 11.83 | 0 | 22 | 4.435 |

| Farming experience (years) | 16.84 | 2 | 50 | 11.939 |

| Landholding (acre) | 29.19 | 3 | 200 | 37.474 |

| Distance from local market (km) | 15.58 | 1 | 50 | 11.267 |

| Distance from extension office (km) | 15.02 | 1 | 45 | 10.848 |

| Distance from metal road (km) | 1.52 | 0 | 7 | 1.844 |

| Use of mobile phone | 0.85 | 0 | 1 | 0.357 |

| Use of internet | 0.44 | 0 | 1 | 0.498 |

| Use of apps | 0.34 | 0 | 1 | 0.475 |

| ICT’s role in price determination | 0.79 | 0 | 1 | 0.407 |

| Willingness to invest in ICT | 0.82 | 0 | 1 | 0.387 |

| Membership of the online network | 0.29 | 0 | 1 | 0.455 |

| Variables | ICT Tools to Obtain Agriculture Information | Willingness to Invest in ICT | Membership of Online Network | ICT’s Role in Orchard Price Determination | ||

|---|---|---|---|---|---|---|

| Mobile | Internet | Apps | ||||

| Age | 0.031 | −0.064 *** | −0.067 *** | 0.075 ** | −0.069 *** | 0.049 * |

| (1.032) | (0.938) | (0.93) | (1.078) | (0.933) | (1.051) | |

| Education | 0.162 ** | 0.300 *** | 0.322 *** | 0.017 | 0.169 *** | 0.132 * |

| (1.176) | (1.350) | (1.38) | (1.017) | (1.185) | (1.141) | |

| Farming experience | −0.013 | −0.018 | −0.001 | −0.096 *** | 0.001 | 0.025 |

| (0.987) | (0.982) | (0.99) | (0.909) | (1.001) | (1.025) | |

| Landholding | 0.014 | −0.004 | −0.006 | 0.024 * | −0.012 | 0.011 |

| (1.015) | (0.996) | (0.99) | (1.024) | (0.988) | (1.012) | |

| Farm distance from local market | 0.274 *** | 0.029 | 0.061 | 0.047 | 0.062 | 0.181 ** |

| (1.315) | (1.030) | (1.06) | (1.048) | (1.064) | (1.198) | |

| Farm distance from extension office | −0.070 | −0.045 | −0.072 | −0.008 | −0.087 ** | −0.132 * |

| (0.932) | (0.956) | (0.93) | (0.992) | (0.917) | (0.876) | |

| Farm distance from metal road | −0.809 *** | −0.120 | −0.115 | −0.163 | −0.260 | −0.627 *** |

| (0.445) | (0.887) | (0.89) | (0.849) | (0.771) | (0.534) | |

| Intermediary Trade | ||||

|---|---|---|---|---|

| Contractors % N = 25 | Commission Agents N = 27 | Wholesalers % N = 39 | ||

| Demographic characteristics | ||||

| Age | below 25 | 0 | 3.7 | 17.5 |

| 26–35 | 16.0 | 66.7 | 37.5 | |

| 36–45 | 40.0 | 18.5 | 22.5 | |

| 46–55 | 20.0 | 7.4 | 12.5 | |

| 56–65 | 24.0 | 0.0 | 2.5 | |

| 65 or above | 0 | 3.7 | 5.0 | |

| Education | Illiterate | 36.0 | 0.0 | 43.6 |

| Primary | 16.0 | 0.0 | 20.5 | |

| Middle | 8.0 | 11.1 | 17.9 | |

| High School | 28.0 | 11.1 | 2.6 | |

| College | 4.0 | 33.3 | 15.4 | |

| University | 8.0 | 44.4 | 0.0 | |

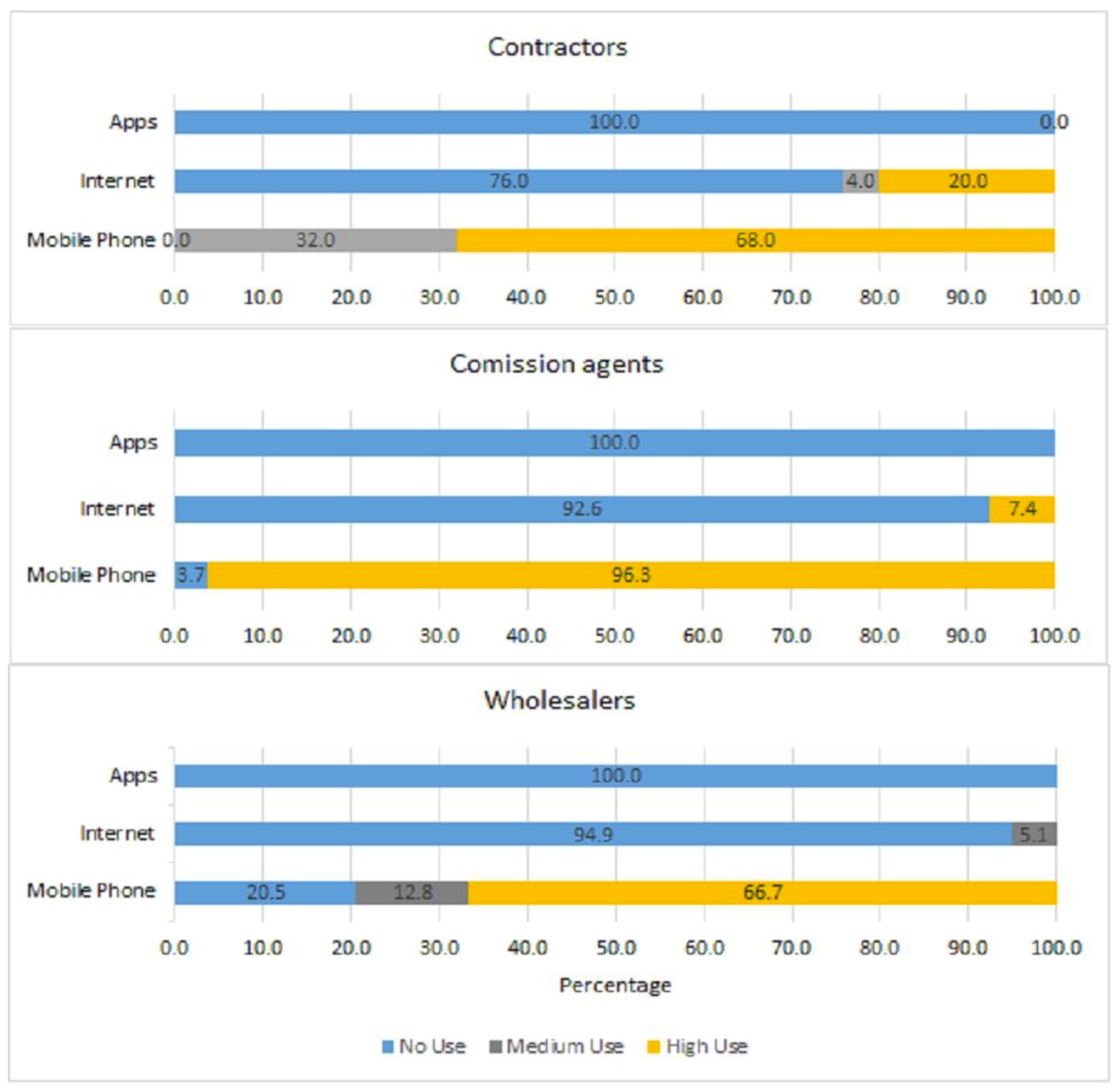

| Sources of Information | ||||

| Mobile | 100 | 100 | 89.7 | |

| Internet | 32 | 7.4 | 10.3 | |

| TV | 24 | 25.9 | 0 | |

| Extension Department | 16 | 0 | 0 | |

| Newspaper | 0 | 0 | 5.1 | |

| Magazine | 0 | 7.2 | 5.1 | |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Waqar, M.; Gu, R.; Nie, F. Mapping ICT Use along the Citrus (Kinnow) Value Chain in Sargodha District, Pakistan. Sustainability 2018, 10, 4743. https://doi.org/10.3390/su10124743

Waqar M, Gu R, Nie F. Mapping ICT Use along the Citrus (Kinnow) Value Chain in Sargodha District, Pakistan. Sustainability. 2018; 10(12):4743. https://doi.org/10.3390/su10124743

Chicago/Turabian StyleWaqar, Muhammad, Rui Gu, and Fengying Nie. 2018. "Mapping ICT Use along the Citrus (Kinnow) Value Chain in Sargodha District, Pakistan" Sustainability 10, no. 12: 4743. https://doi.org/10.3390/su10124743

APA StyleWaqar, M., Gu, R., & Nie, F. (2018). Mapping ICT Use along the Citrus (Kinnow) Value Chain in Sargodha District, Pakistan. Sustainability, 10(12), 4743. https://doi.org/10.3390/su10124743