Improving Eco-Efficiency through Waste Reduction beyond the Boundaries of a Firm: Evidence from a Multiplant Case in the Ceramic Industry

Abstract

1. Introduction

2. Research Background

- Material efficiency, that is, whether the assessment of water, raw, indirect and other materials is included;

- Energy efficiency, that is, whether the assessment of direct and indirect energy efficiency is included;

- Eco-efficiency perspective, that is, whether the resource usage and the related economic implications are assessed jointly;

- Cost allocation, that is, whether the cost allocation is considered and if it is accurately performed;

- System perspective, that is, whether the assessment is performed at a plant, company, multiplant or supply chain level;

- Results as absolute values, that is, whether the application provides absolute values useful for internal analysis, instead of relative values, useful only for comparative analysis.

- Eight approaches out of 17 do not take an eco-efficiency perspective. They can be called “Resource use-driven methods”, whereas the others approaches are “Resource cost-driven methods” as they intended to assess resource usage (in terms of physical units) and its economic implications.

- Among contributions that take an eco-efficiency perspective, almost all the approaches provide a limited accuracy of cost allocation.

- Most approaches do not consider a holistic perspective. In the most of cases, the resource usage and therefore the identification of the sources of inefficiencies of a production system is at single plant or company level.

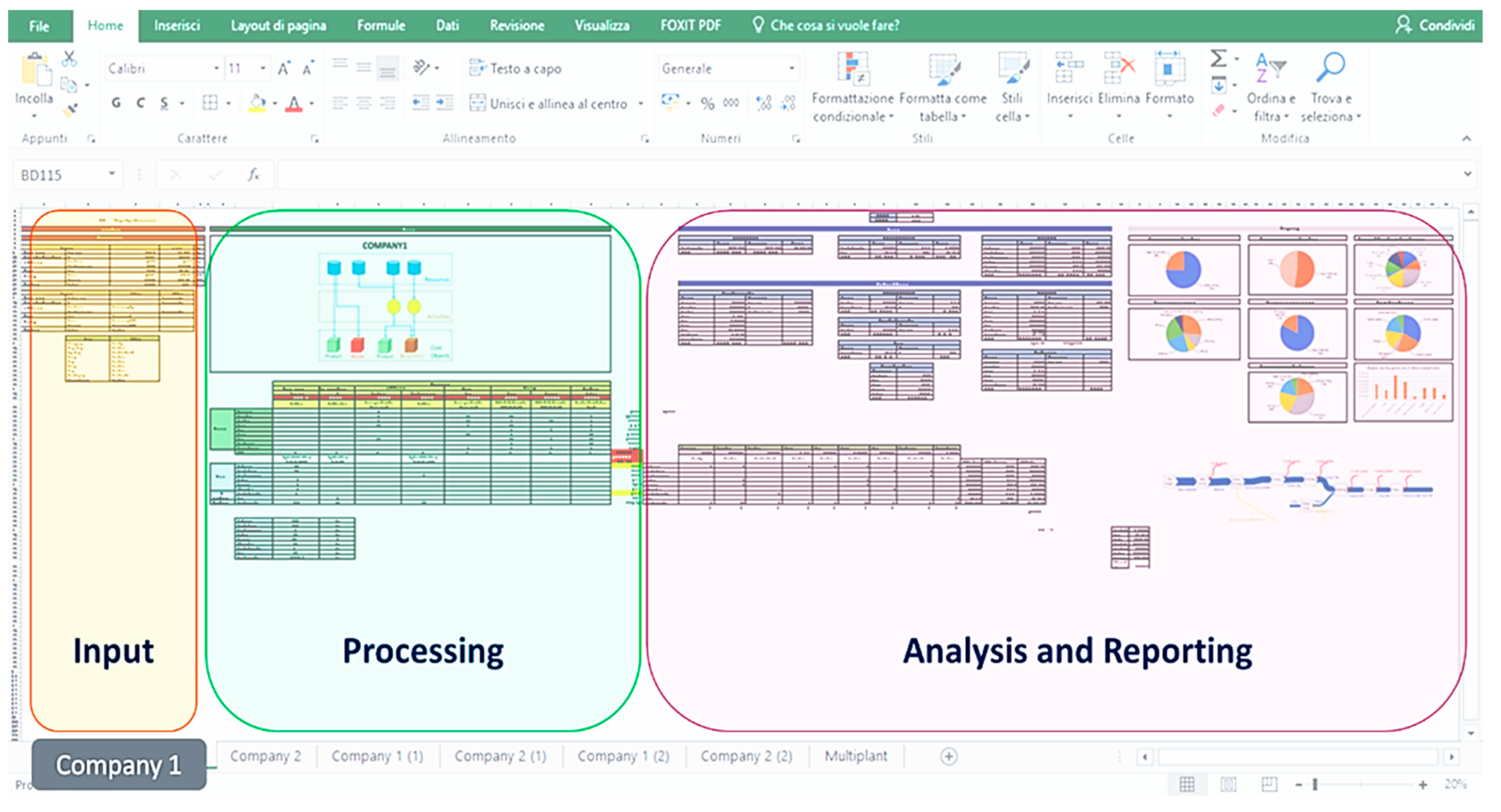

3. A DSS for Waste Reduction in Multiplant Production Systems

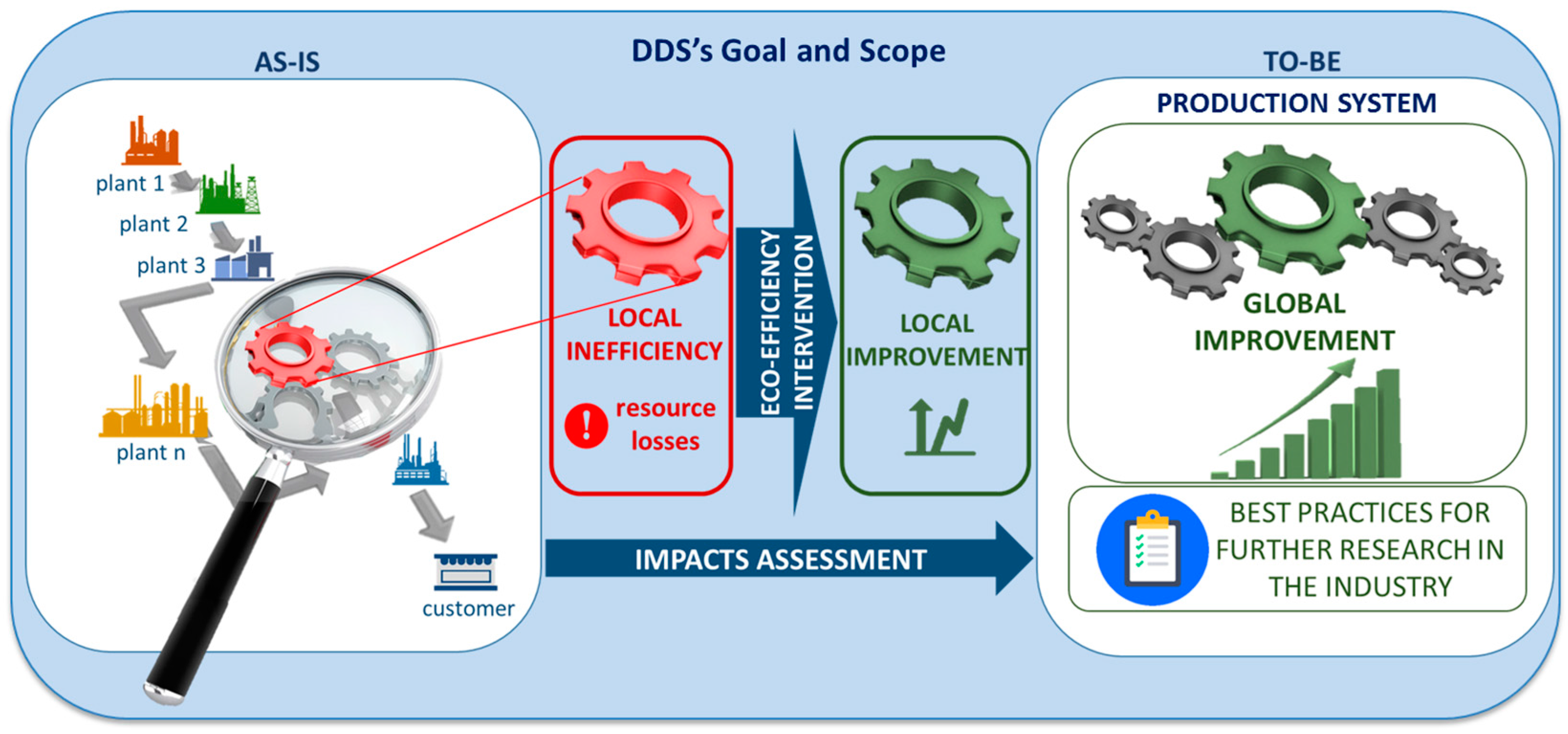

3.1. Goal and Scope

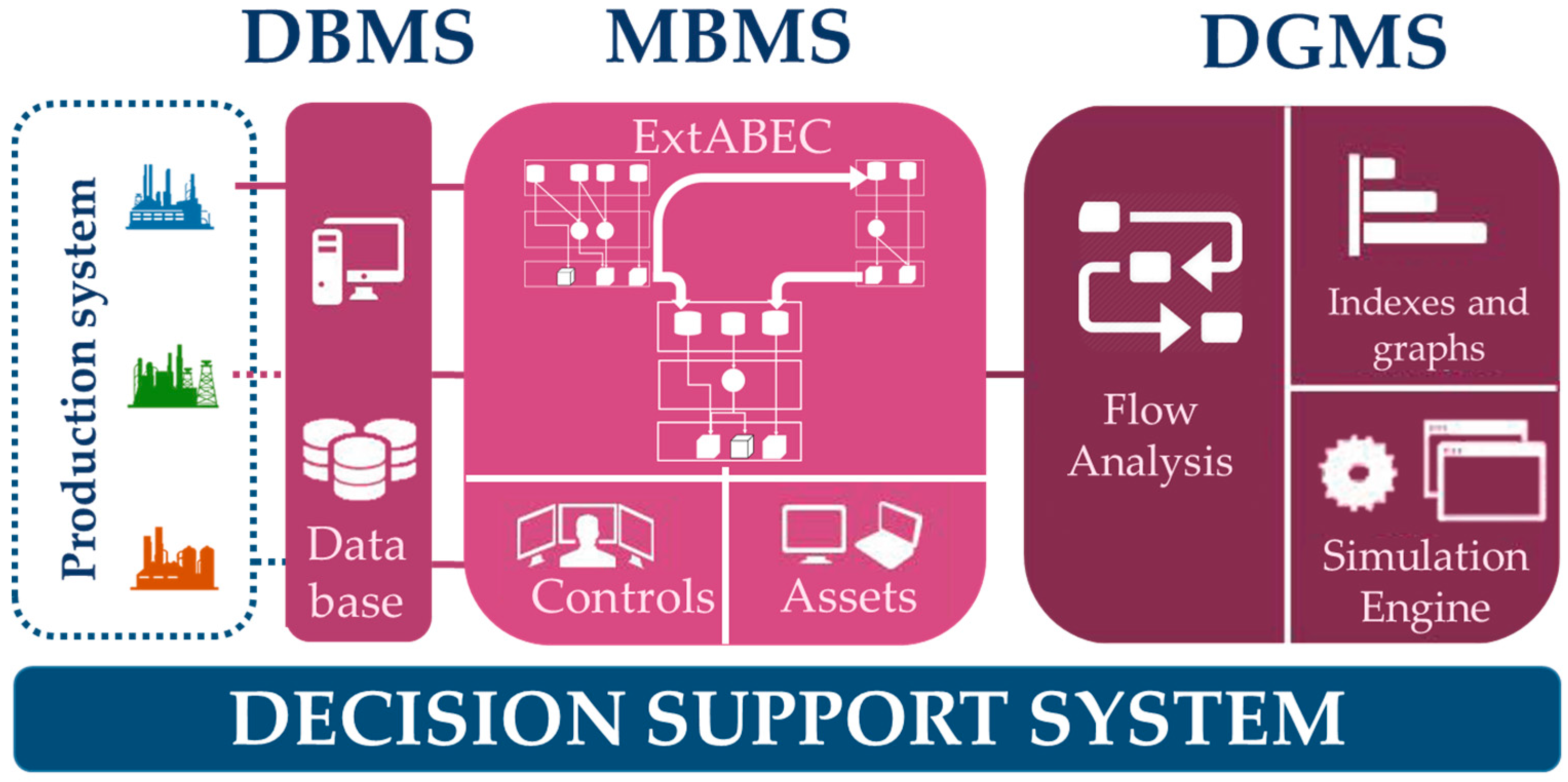

3.2. DSS’s Description

- It considers both material and energy efficiency;

- It takes into account not only the operational and environmental perspective, but also the economic one;

- The cost allocation is based on Activity-Based Costing and therefore it is accurately performed;

- It assesses both the local and global impact of alternative interventions to improve eco-efficiency, in order to implement the more suitable interventions for a whole eco-efficient improvement of a production system, without worsening the performance of the single units;

- It provides the absolute physical and monetary values of the products, wastes and by-products of a production system.

3.3. Steps

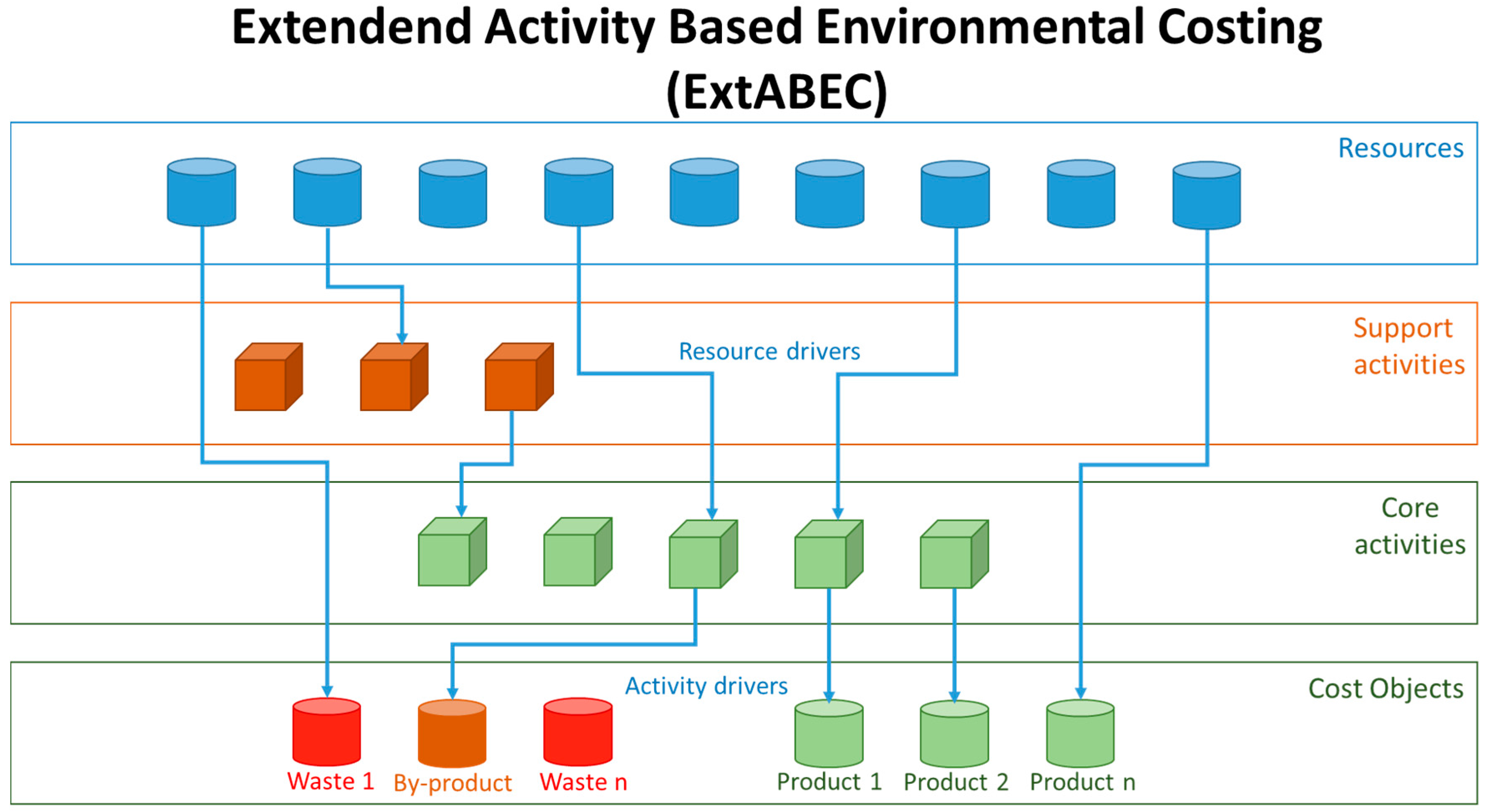

- Boundaries and process modelling. The boundaries of the production system to be analysed are identified. Then, among all the possible set of processes of the production system under examination, users identify the most critical to be assessed and improved. The analysis then identifies the major functions performed by each member involved in the process.

- ExtABEC implementation. This step implies the following activities:

- 2.1

- Identification of the cost objects: products, by-products and wastes are selected.

- 2.2

- Identification and quantification of the resources: all the resources used all along the process under analysis are identified and quantified. Resources include, for example, energy, raw materials, water, labour, and indirect materials.

- 2.3

- Identification of the core activities: the way that activities consume resources is identified. The process must be broken down into the specific activities performed by each component of the production system. The analysis involves determining what activities are done within the production system, how many people, resources and time are required to perform each activity, and what operational data best reflect the performance of the activities.

- 2.4

- Identification of the support activities: the activities that do not have a direct influence on products but are necessary for the process, because they support other primary activities, are identified.

- 2.5

- Identification and quantification of the drivers describing the correlation between activities and support activities.

- 2.6

- Identification of the resource drivers and quantification of their intensities: the way that activities adsorb resources is identified.

- 2.7

- Assignment of the resources to cost objects: when possible, resources can be accounted directly to the cost objects.

- 2.8

- Assignment of the resources to activities: otherwise, resources can be accounted, by means of the resource drivers, to the activities they are used by. The activity cost represents the total cost of resources used to perform a specific unit of work.

- 2.9

- Identification of the activity drivers and quantification of their intensities: the way that cost objects absorb resources by means of activities is identified.

- 2.10

- Assignment of the activities: by means of the activity drivers, the value of the activities is accounted to the cost objects.

- 2.11

- Calculation of the cost of the products/wastes/by-products: for every cost object, the share of resources directly accounted and the share indirectly accounted through the activities is summed up.

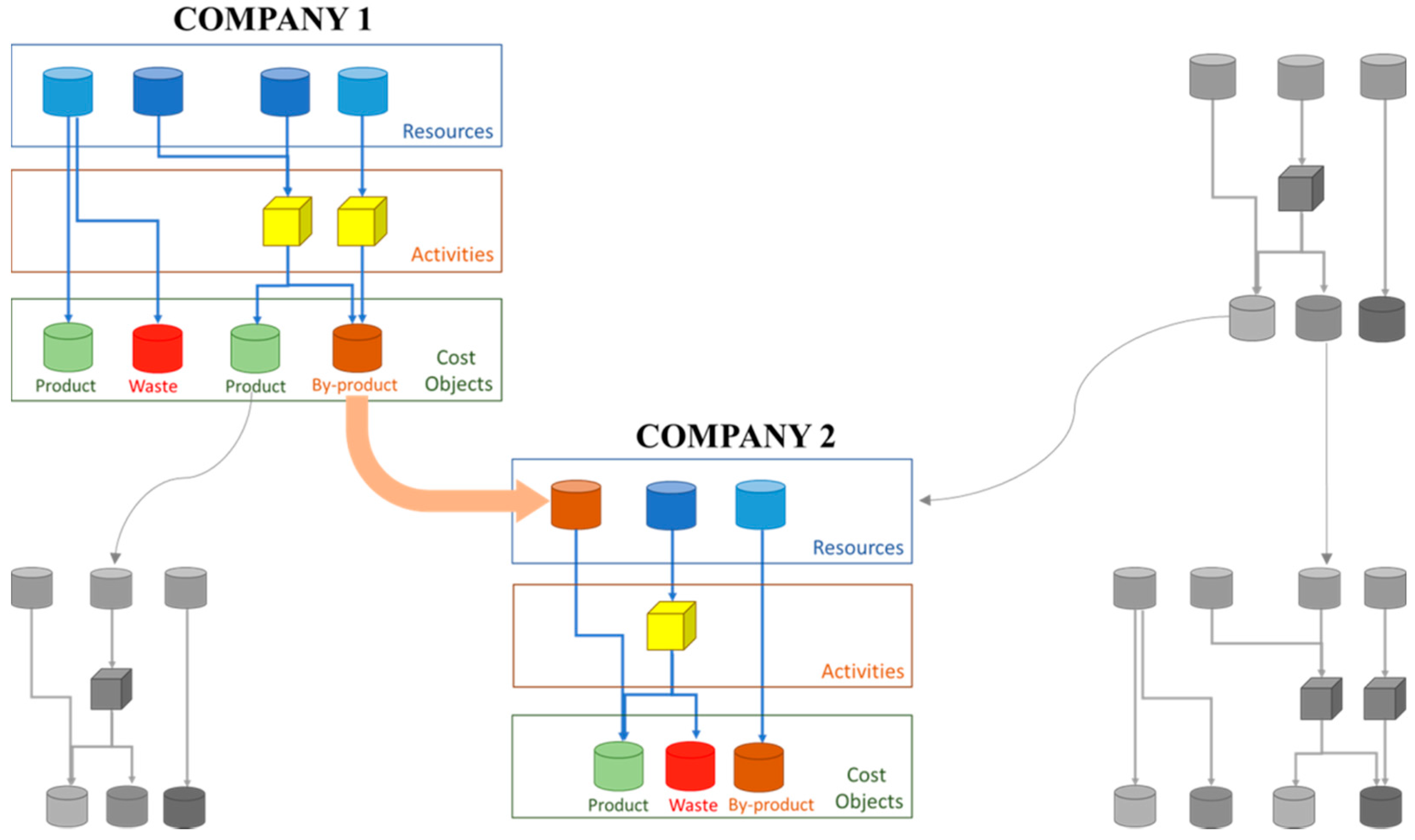

- Resource efficiency analysis. Thanks to flow and cost allocation carried out through ExtABEC implementation, it is possible to identify inefficiencies all along the production route (inefficiencies that are related to resources and activities value lost in the production of wastes instead of saleable products). In this way, players involved in the production route can effectively analyse resource consumption and waste generation of the system, by assessing not only single company performance but also the overall eco-efficiency of the production system analysed.

- Interventions evaluation. To support decision-making, the potential impacts of the individual actions on the examined process are evaluated at different levels (single unit and system-wide), in order to choose improvement interventions that do not worsen the overall eco-efficiency of the production system examined. Considering that the DSS is based on technical input-output format and on coefficients (the cost drivers of ExtABEC), it effectively allows to develop and compare alternative scenarios. With this regard, the adoption of different technologies, the use of different materials, the selection of different suppliers can be evaluated to adopt the best local decision leading to a whole improvement of the eco-efficiency of the production system. The resulting changes in resource and activity costs can be traced to specific product to determine the effect on different players and therefore quantify the eco-efficiency improvement at both local and global level. Therefore, DSS effectively allows the user to develop and compare alternative scenarios to adopt the best local decision leading to a whole improvement of the eco-efficiency of the production system analysed.

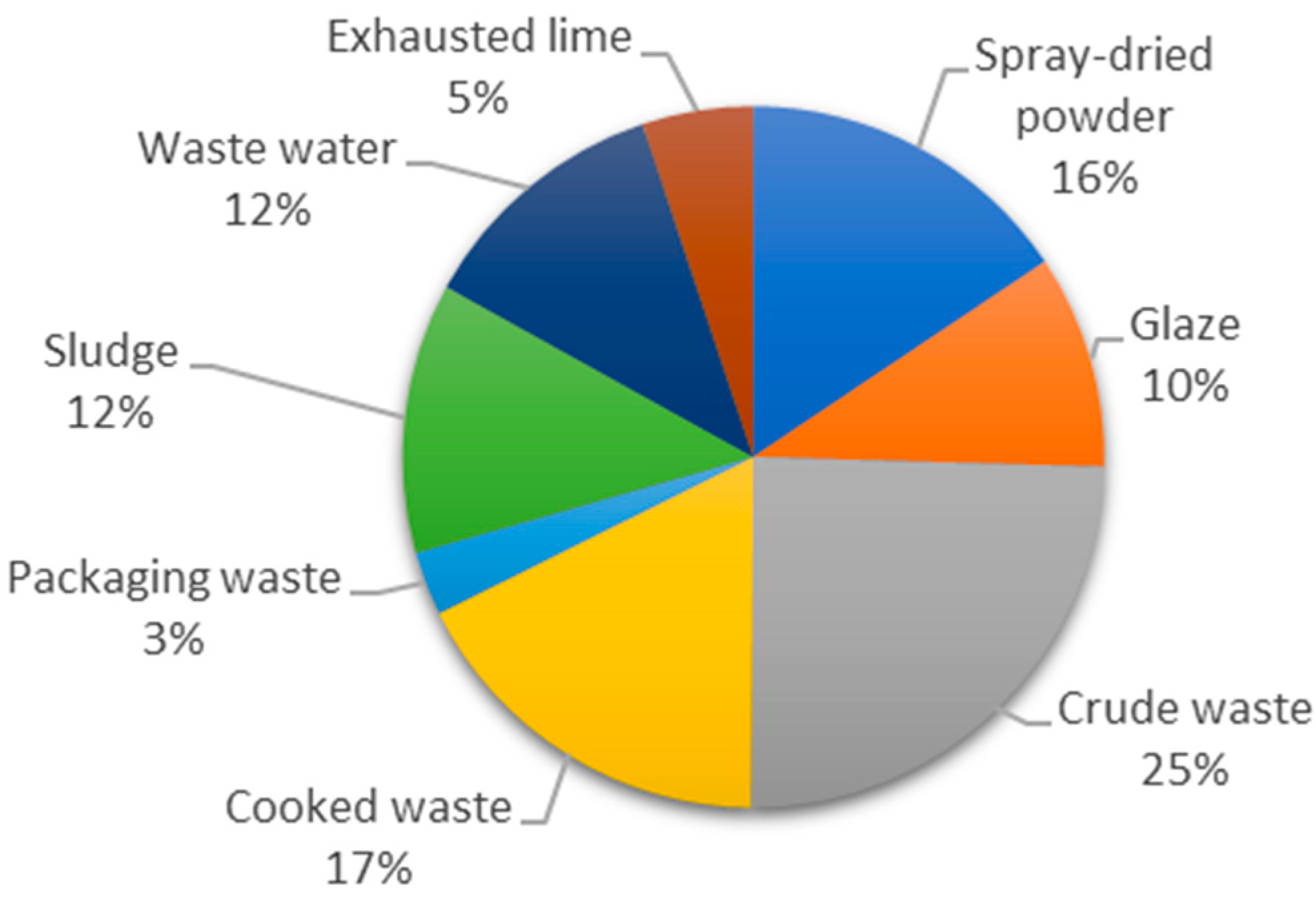

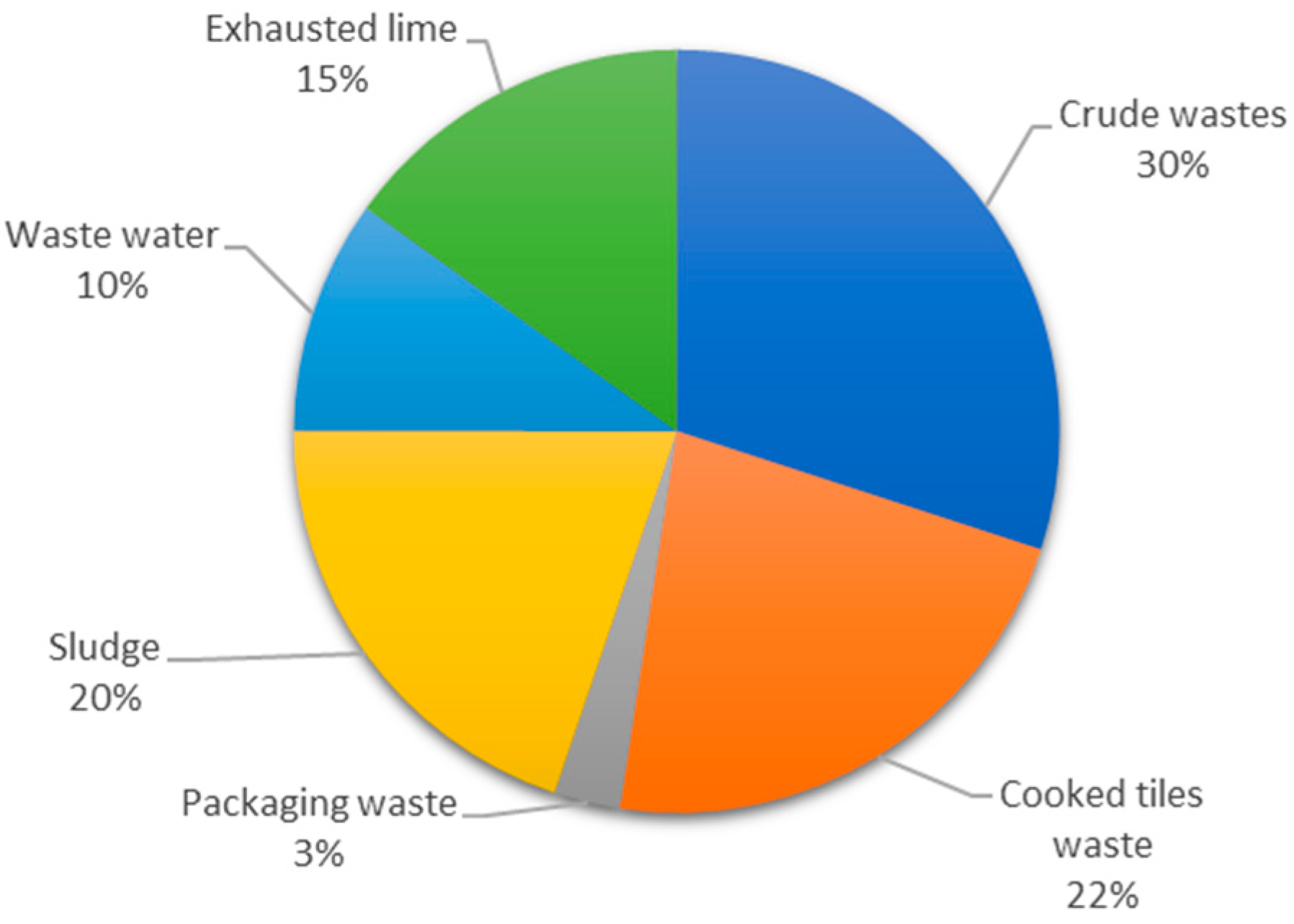

4. Description of the Multiplant Case Study

- Crude waste. This is formed by unfired materials.

- Cooked waste. This is the fired materials generated in the firing.

- Sludge. This consists of the sludge obtained in the cleaning of the glaze mills.

- Waste water. It is mainly generated from cleaning water in preparation and casting units, and in various processing activities.

- Exhausted lime. It is generated in the glaze production stage and during the firing process.

5. Results and Discussion

6. Conclusions

6.1. Theoretical Application of the DSS in Supply Chain Contexts

6.2. Scientific Contribution and Industrial Relevance

Acknowledgments

Author Contributions

Conflicts of Interest

References

- CEC, A. Resource-Efficient Europe—Flagship Initiative under the Europe 2020 Strategy; European Commission: Brussels, Belgium, 2011. [Google Scholar]

- Despeisse, M.; Ball, P.; Evans, S.; Levers, A. Industrial Ecology at Factory Level: A Conceptual Model. J. Clean. Prod. 2012, 31, 30–39. [Google Scholar] [CrossRef]

- Kunz, N.C.; Moran, C.J.; Kastelle, T. Conceptualising ‘Coupling’ for Sustainability Implementation in the Industrial Sector: A Review of the Field and Projection of Future Research Opportunities. J. Clean. Prod. 2013, 53, 69–80. [Google Scholar] [CrossRef]

- Baptista, A.J.; Lourenço, E.J.; Cunha, F.; Marques, B.; Silva, E.J.; Peças, P. Eco-efficiency Framework as a Decision Support Tool to Enhance Economic and Environmental Performance of Production Systems. In Proceedings of the 3rd International Colloquium of the Cluster of Excellence “eniPROD” (Energy-Efficient Product and Process Innovations in Production Engineering), Chemnitz, Germany, 8–9 April 2014. [Google Scholar]

- Lehni, M.; Schmidheiny, S.; Stigson, B. Eco-Efficiency: Creating More Value with Less Impact; World Business Council for Sustainable Development (WBCSD): Geneva, Switzerland, 2000. [Google Scholar]

- Cagno, E.; Micheli, G.J.L.; Trucco, P. Eco-efficiency for sustainable manufacturing: An extended environmental costing method. Prod. Plan. Control 2012, 23, 34–144. [Google Scholar] [CrossRef]

- Europe Innova Eco-Innovation REMake. Guide to Resource Efficiency in Manufacturing. 2012. Available online: http://www.greenovate-europe.eu/ (accessed on 30 November 2017).

- Ribeiro, I.; Peças, P.; Silva, A.; Henriques, E. Life Cycle Engineering Methodology Applied to Material Selection, A Fender Case Study. J. Clean. Prod. 2008, 16, 1887–1899. [Google Scholar] [CrossRef]

- Kabongo, J.; Boiral, O. Creating Value with Wastes: A Model and Typology of Sustainability within Firms. Bus. Strateg. Environ. 2011, 20, 441–455. [Google Scholar] [CrossRef]

- Kuhlang, P.; Edtmayr, T.; Sihn, W. Methodical Approach to Increase Productivity and Reduce Lead Time in Assembly and Production-Logistic Processes. CIRP J. Manuf. Sci. Technol. 2011, 4, 24–32. [Google Scholar] [CrossRef]

- Benoy, A.M.; Owen, L. Link to Link: Driving Resource Efficiency across Supply Chains; Policy Connect CAN Mezzanine: London, UK, 2016. [Google Scholar]

- An, Q.; Yan, H.; Wu, J.; Liang, L. Internal resource waste and centralization degree in two-stage systems: An efficiency analysis. Omega 2015, 61, 89–99. [Google Scholar] [CrossRef]

- Askarany, D.; Yazdifar, H.; Askary, S. Supply chain management, activity-based costing and organisational factors. Int. J. Prod. Econ. 2009, 127, 238–248. [Google Scholar] [CrossRef]

- Schulze, M.; Seuring, S.; Ewering, C. Applying Activity-Based Costing in a Supply Chain Environment. Int. J. Prod. Econ. 2011, 135, 716–725. [Google Scholar] [CrossRef]

- Jørgensen, T.H. Towards more sustainable management systems: Through life cycle management and integration. J. Clean. Prod. 2008, 16, 1071–1080. [Google Scholar] [CrossRef]

- Perotti, S.; Zorzini, M.; Cagno, E.; Micheli, G.J. Green supply chain practices and company performance: The case of 3PLs in Italy. Int. J. Phys. Distrib. Logist. Manag. 2012, 42, 640–672. [Google Scholar] [CrossRef]

- Hur, T.; Yamamoto, R. Measurement of Green Productivity and its Improvement. J. Clean. Prod. 2004, 12, 673–683. [Google Scholar] [CrossRef]

- Suh, S. Theory of Materials and Energy Flow Analysis in Ecology and Economics. Ecol. Model. 2005, 189, 251–269. [Google Scholar] [CrossRef]

- Schmidt, M.; Nakajima, M. Material Flow Cost Accounting as an Approach to Improve Resource Efficiency in Manufacturing Companies. Resources 2013, 2, 358–369. [Google Scholar] [CrossRef]

- Matopoulos, A.; Barros, A.C.; van der Vorst, J.G.A.J. Resource-Efficient Supply Chains: A Research Framework, Literature Review and Research Agenda. Supply Chain Manag. 2015, 20, 218–236. [Google Scholar] [CrossRef]

- Baptista, A.J.; Lourenço, E.J.; Pereira, J.P.; Cunha, F.; Silva, E.J.; Peças, P. EcoPROSYS: An eco-efficiency framework applied to a medium density fibreboard finishing line. In Proceedings of the 23rd CIRP Conference on Life Cycle Engineering, Berlin, Germany, 22–24 May 2016. [Google Scholar]

- Schliephake, K.; Stevens, G.; Clay, S. Making Resources Work More Efficiently—The Importance of Supply Chain Partnerships. J. Clean. Prod. 2009, 17, 1257–1263. [Google Scholar] [CrossRef]

- De Soete, W. Towards a Multidisciplinary Approach on Creating Value: Sustainability through the Supply Chain and ERP Systems. Systems 2016, 1, 16. [Google Scholar] [CrossRef]

- Style. Available online: https://www.spire2030.eu/style (accessed on 30 November 2017).

- Measure. Available online: www.spire2030.eu/measure (accessed on 30 November 2017).

- Marchet, G.; Melacini, M.; Sassi, C.; Tappia, E. Assessing efficiency and innovation in the 3PL industry: An empirical analysis. Int. J. Logist. Res. Appl. 2017, 20, 53–72. [Google Scholar] [CrossRef]

- Zhang, B.; Bi, J.; Fan, Z.; Yuan, Z.; Ge, J. Eco-efficiency analysis of industrial system in China: A data envelopment analysis approach. Ecol. Econ. 2008, 68, 306–316. [Google Scholar] [CrossRef]

- Bribiàn, I.Z.; Capilla, A.V.; Usòn, A.A. Life Cycle Assessment of Building Materials: Comparative Analysis of Energy and Environmental Impacts and Evaluation of the Eco-Efficiency Improvement Potential. Build. Environ. 2010, 46, 1133–1140. [Google Scholar] [CrossRef]

- Saurat, M.; Ritthoff, M. Calculating MIPS 2.0. Resources 2013, 2, 581–607. [Google Scholar] [CrossRef]

- Puig, R.; Fullana-i-Palmer, P.; Baquero, G.; Riba, J.R.; Bala, A. A Cumulative Energy Demand Indicator (CED), Life Cycle Based, for Industrial Waste Management Decision Making. Waste Manag. 2013, 33, 2789–2797. [Google Scholar] [CrossRef] [PubMed]

- De Meester, B.; Dewulf, J.; Verbeke, S.; Janseens, A.; Van Langenhove, H. Exergetic Life-Cycle Assessment (ELCA) for Resource Consumption Evaluation in the Built Environment. Build. Environ. 2009, 44, 11–17. [Google Scholar] [CrossRef]

- Brunner, P.H.; Rechberger, H. Practical Handbook of Material Flow Analysis: Advanced Methods in Resource and Waste Management. Int. J. Life Cycle Assess. 2004, 9, 337–338. [Google Scholar] [CrossRef]

- Ayres, R.U.; Ayres, L.W.; Martinás, K. Exergy, Waste Accounting, and Life-Cycle Analysis. Energy 1998, 23, 355–363. [Google Scholar] [CrossRef]

- Liedtke, C.; Lettenmeier, M.; Baedeker, C. Resource Intensity in Global Food Chains: The Hot Spot Analysis. Br. Food J. 2010, 112, 1138–1159. [Google Scholar] [CrossRef]

- Feire, F.; Thore, S.; Ferrao, P. Life Cycle Activity Analysis: Logistics and Environmental Policies for Bottled Water in Portugal. OR Spektr. 2001, 23, 159–182. [Google Scholar] [CrossRef]

- Gluch, P.; Baumann, H. The life Cycle Costing (LCC) Approach: A Conceptual Discussion of its Usefulness for Environmental Decision-Making. Build. Environ. 2003, 39, 571–580. [Google Scholar] [CrossRef]

- Kumaran, D.S.; Ong, S.K.; Tan, R.B.H.; Nee, A.Y.C. Environmental Life Cycle Cost Analysis of Products. Environ. Manag. Health 2001, 12, 260–276. [Google Scholar] [CrossRef]

- Herbohn, K.A. Full Cost Environmental Accounting Experiment. Account. Org. Soc. 2005, 30, 519–536. [Google Scholar] [CrossRef]

- Shonnard, D.R.; Kicherer, A.; Saling, P. Industrial Applications Using BASF Eco-Efficiency Analysis: Perspectives on Green Engineering Principles. Environ. Sci. Technol. 2003, 37, 5340–5348. [Google Scholar] [CrossRef] [PubMed]

- Bach, V.; Berger, M.; Henßler, M.; Kirchner, M.; Leiser, S.; Mohr, L.; Rother, E.; Ruhland, K.; Schneider, L.; Tikana, L.; et al. Integrated Method to Assess Resource Efficiency—ESSENZ. J. Clean. Prod. 2016, 137, 118–130. [Google Scholar] [CrossRef]

- Emblemsvag, J.; Bras, B. Activity-Based Cost and Environmental Management: A Different Approach to the ISO 14000 Compliance, 1st ed.; Springer Science & Business Media: Berlin, Germany, 2012; ISBN 0-7923-7247-6. [Google Scholar]

- Finnveden, G.; Bjorklund, A.; Ekvall, T.; Moberg, A. Environmental and Economic Assessment Methods for Waste Management Decision-Support: Possibilities and Limitations. Waste Manag. Res. 2007, 25, 263–269. [Google Scholar] [CrossRef] [PubMed]

- Nicoletti, G.M.; Notarnicola, B.; Tassielli, G. Comparative Life Cycle Assessment of Flooring Materials: Ceramic versus Marble Tiles. J. Clean. Prod. 2010, 10, 283–296. [Google Scholar] [CrossRef]

- Bovea, M.D.; Dìaz-Albo, E.; Gallardo, A.; Colomer, F.J.; Serrano, J. Environmental performance of ceramic tiles: Improvement proposals. Mater. Des. 2009, 31, 35–41. [Google Scholar] [CrossRef]

- Barros, M.C.; Bello, P.; Roca, E.; Casares, J.J. Integrated pollution prevention and control for heavy ceramic industry in Galicia (NW Spain). J. Hazard. Mater. 2006, 141, 680–692. [Google Scholar] [CrossRef] [PubMed]

- Juan, A.; Medina, C.; Guerra, M.I.; Moràn, J.M.; Aguado, P.J.; Sánchez de Rojas, M.I.; Frías, M.; Rodríguez, O. Re-Use of Ceramic Wastes in Construction. In Ceramic Materials; Wilfried Wunderlich; InTech Europe: Rijeka, Croatia, 2010; pp. 197–214. ISBN 978-953-307-145-9. Available online: https://cdn.intechopen.com/pdfs-wm/11637.pdf (accessed on 30 November 2017).

- Picazo-Tadeo, A.J.; Prior, D. Environmental externalities and efficiency measurement. J. Environ. Manag. 2009, 90, 3332–3339. [Google Scholar] [CrossRef] [PubMed]

- Gibbs, D.; Deutz, P. Trust and networking in inter-firm relations: The case of eco-industrial development. Local Econ. 2003, 18, 222–236. [Google Scholar] [CrossRef]

- LaLonde, B.J.; Pohlen, T.L. Issues in Supply Chain Costing. Int. J. Logist. Manag. 1996, 7, 1–12. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Approach | Material Efficiency | Energy Efficiency | Eco-Efficiency Perspective | Cost Allocation | System Perspective | Results as Absolute Values |

|---|---|---|---|---|---|---|

| Life Cycle Assessment (LCA) [28] | F | F | / | / | P | F |

| Material Input Per Service (MIPS) [29] | P | / | / | / | P | F |

| Cumulative Energy Demand (CED) [30] | / | F | / | / | P | F |

| Exergetic Life Cycle Assessment (ELCA) [31] | F | F | / | / | F | F |

| Material Flow Analysis (MFA) [32] | F | / | / | / | F | F |

| Material and Energy Flow Analysis (MEFA) [18] | F | F | / | / | F | F |

| Exergy Analysis [33] | F | F | / | / | F | F |

| Hot-Spot Analysis [34] | F | F | / | / | F | / |

| Life Cycle Activity Analysis (LCAA) [35] | P | P | F | F | P | F |

| Life Cycle Costing (LCC) [36] | P | P | F | P | P | F |

| Environmental Life Cycle Costing (E-LCC) [37] | F | F | F | P | P | P |

| Environmental Full Cost Accounting (EFCA) [38] | P | P | F | P | P | F |

| BASF’s Eco-Efficiency Analysis [39] | F | P | P | / | F | / |

| ESSENZ [40] | P | P | P | / | P | F |

| Material Flow Cost Accounting (MFCA) [19] | F | F | F | P | F | F |

| Activity-Based Costing & Environmental Management (ABC&EM) [41] | F | F | F | P | F | F |

| Extended Activity-Based Environmental Costing (ExtABEC at company level) [6] | F | F | F | F | P | F |

| Waste and by-Product | From Resources (€) | From Activities (€) | Full Industrial Cost (€) |

|---|---|---|---|

| Crude waste | 5452 | 27,318 | 32,770 |

| Cooked waste | 5352 | 17,812 | 23,164 |

| Spray-dried powder | 10,904 | 9827 | 20,731 |

| Sludge | 1090 | 15,491 | 16,581 |

| Waste water | 218 | 15,591 | 15,809 |

| Glaze | 9860 | 3209 | 13,069 |

| Exhausted lime | 1090 | 5699 | 6789 |

| Packaging waste | 2784 | 1128 | 3912 |

| TOTAL | 36,750 | 96,075 | 132,825 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Micheli, G.J.L.; Cagno, E.; Tappia, E. Improving Eco-Efficiency through Waste Reduction beyond the Boundaries of a Firm: Evidence from a Multiplant Case in the Ceramic Industry. Sustainability 2018, 10, 167. https://doi.org/10.3390/su10010167

Micheli GJL, Cagno E, Tappia E. Improving Eco-Efficiency through Waste Reduction beyond the Boundaries of a Firm: Evidence from a Multiplant Case in the Ceramic Industry. Sustainability. 2018; 10(1):167. https://doi.org/10.3390/su10010167

Chicago/Turabian StyleMicheli, Guido J. L., Enrico Cagno, and Elena Tappia. 2018. "Improving Eco-Efficiency through Waste Reduction beyond the Boundaries of a Firm: Evidence from a Multiplant Case in the Ceramic Industry" Sustainability 10, no. 1: 167. https://doi.org/10.3390/su10010167

APA StyleMicheli, G. J. L., Cagno, E., & Tappia, E. (2018). Improving Eco-Efficiency through Waste Reduction beyond the Boundaries of a Firm: Evidence from a Multiplant Case in the Ceramic Industry. Sustainability, 10(1), 167. https://doi.org/10.3390/su10010167