System Dynamics of Polysilicon for Solar Photovoltaics: A Framework for Investigating the Energy Security of Renewable Energy Supply Chains

Abstract

:1. Introduction

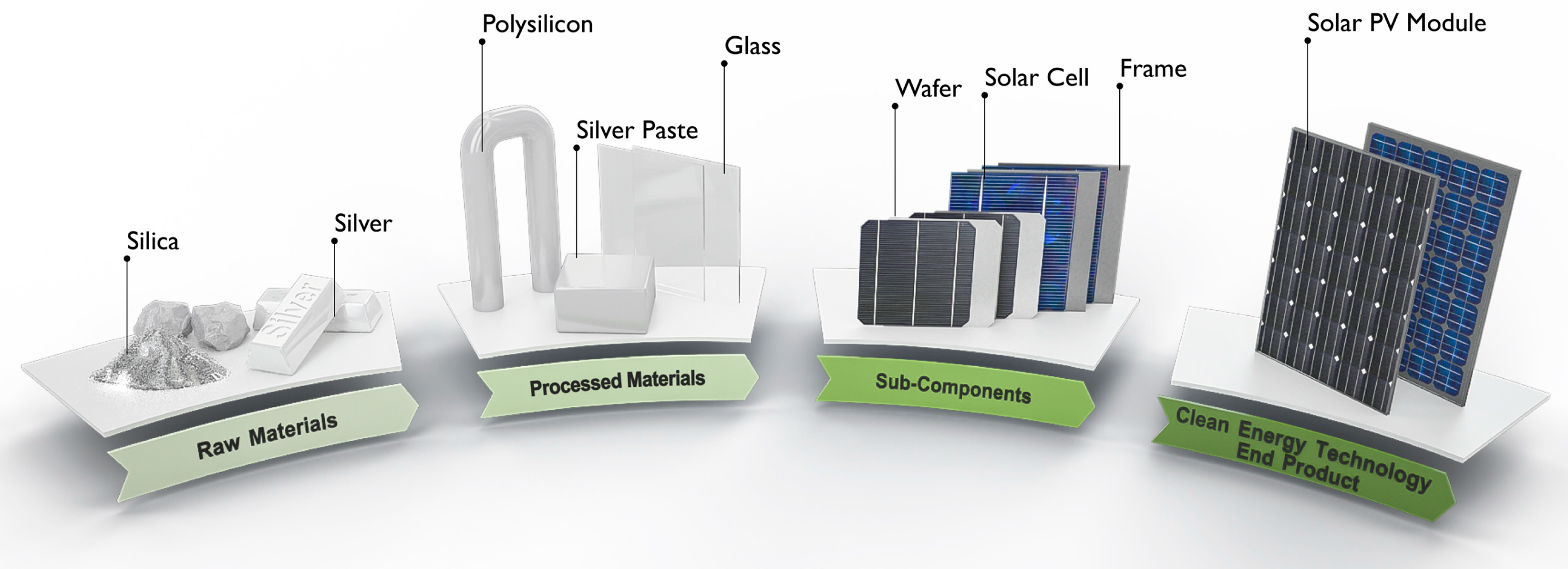

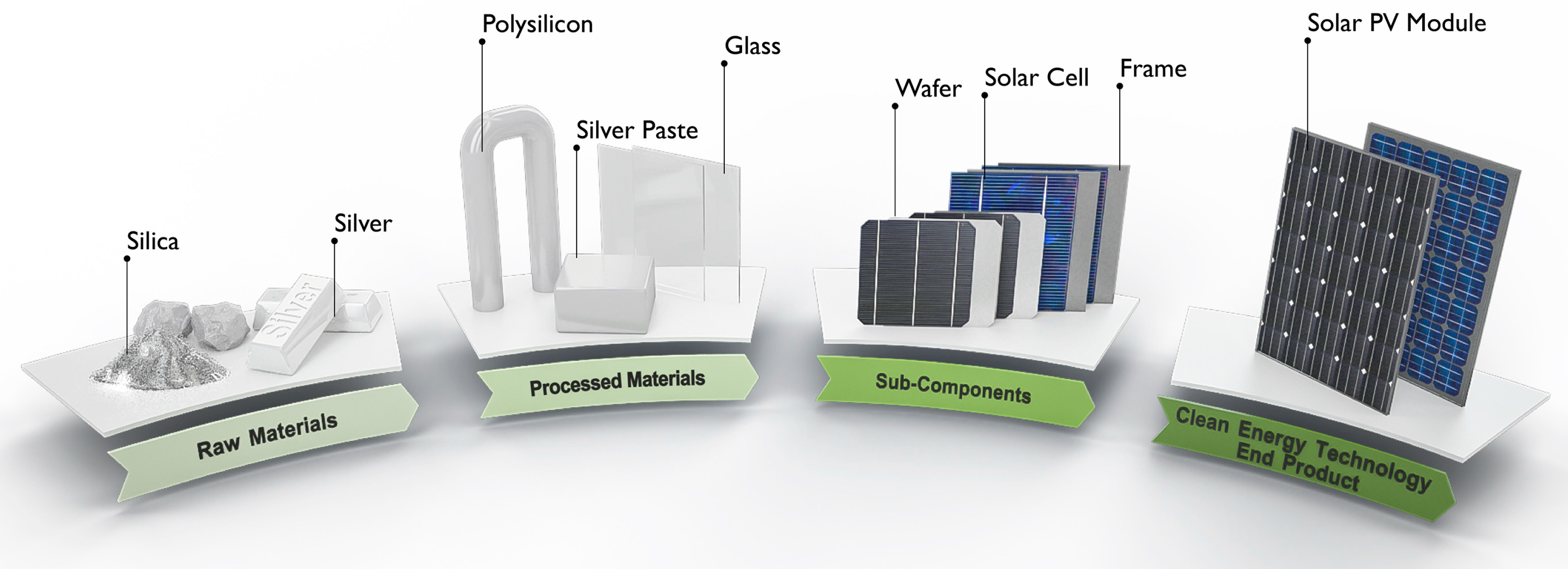

1.1. PV Module Manufacturing Supply Chain

1.2. Polysilicon Manufacturing

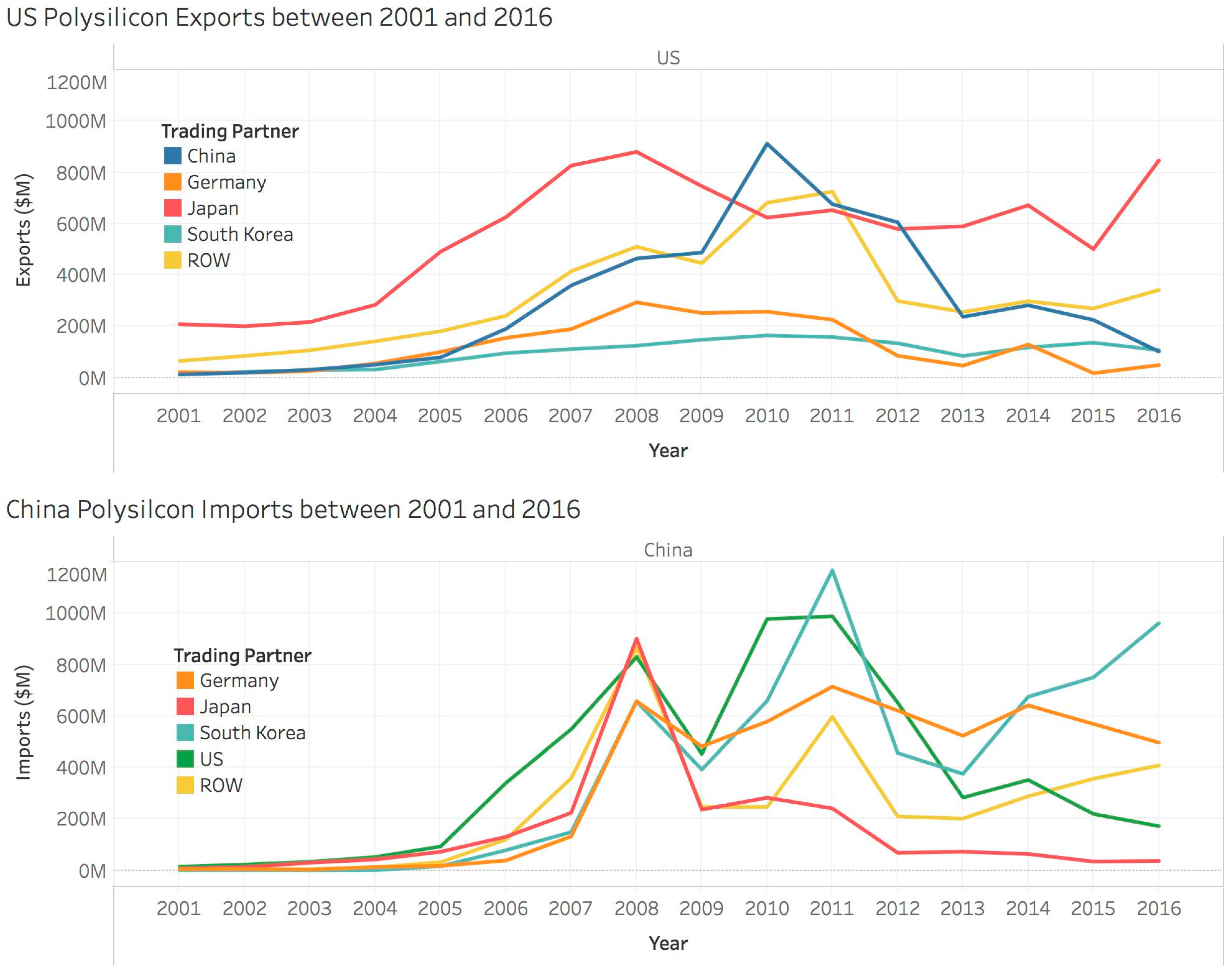

1.3. The Polysilicon Market Today

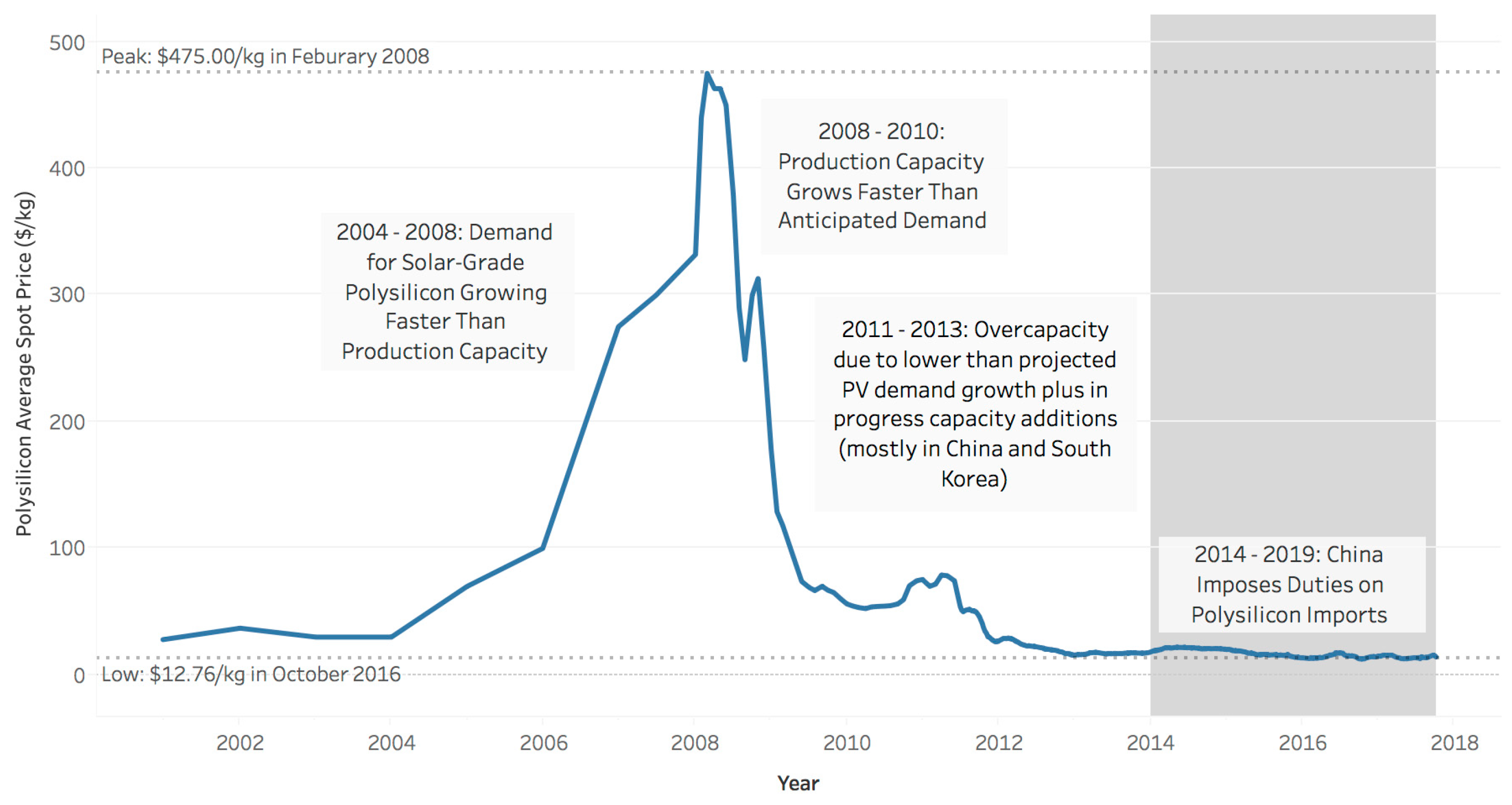

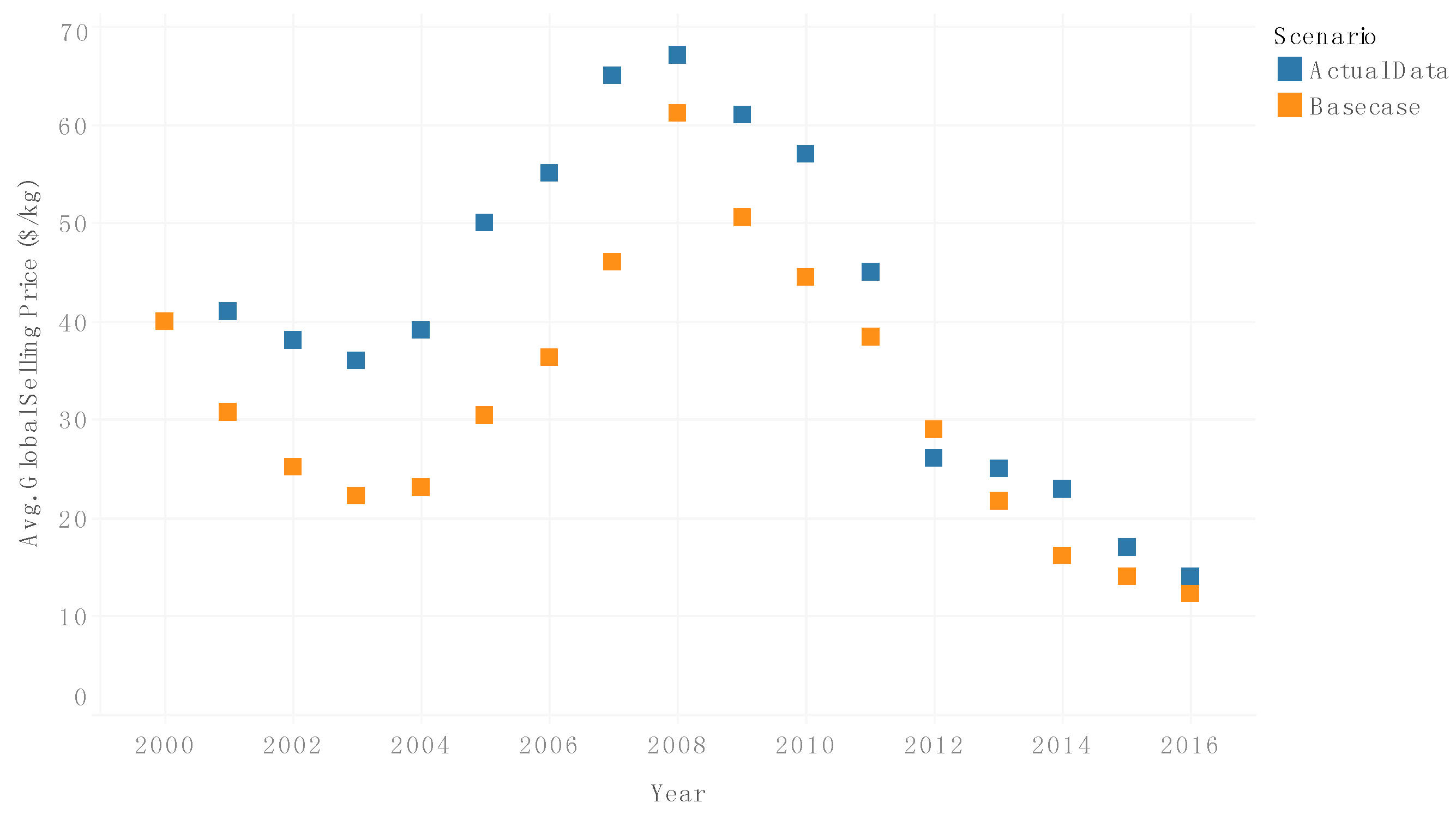

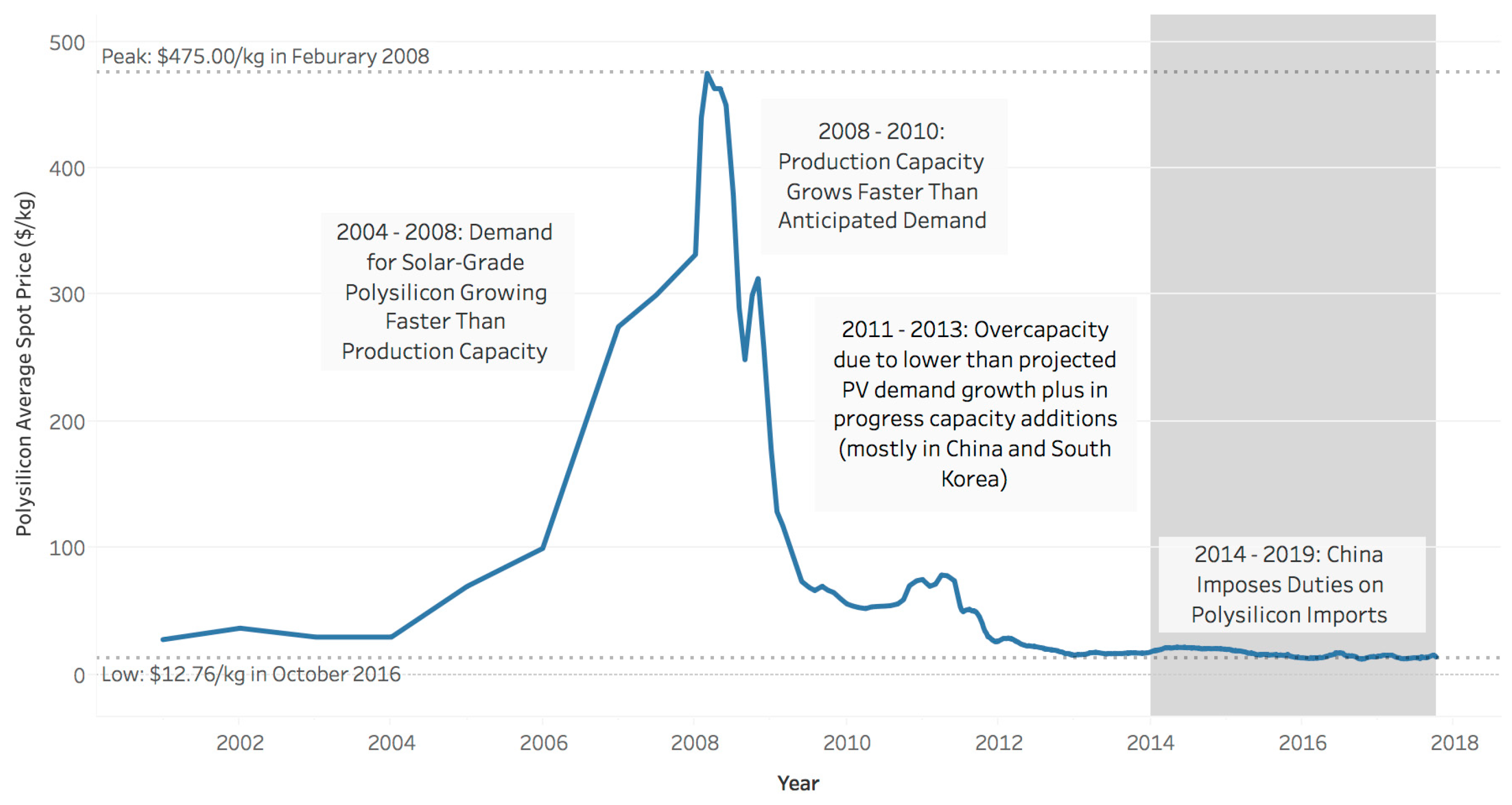

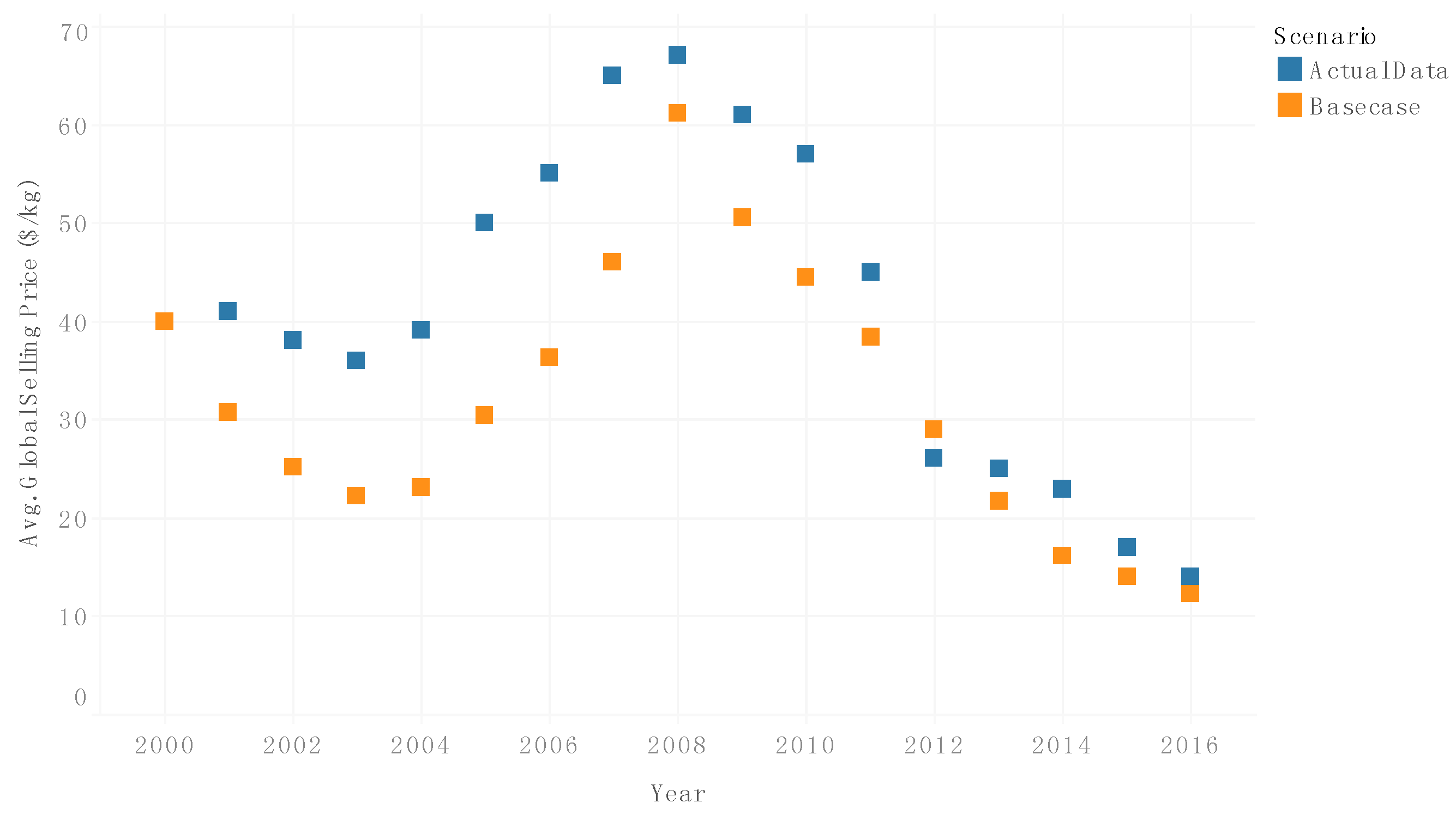

1.4. Polysilicon Market Evolution and Volatility

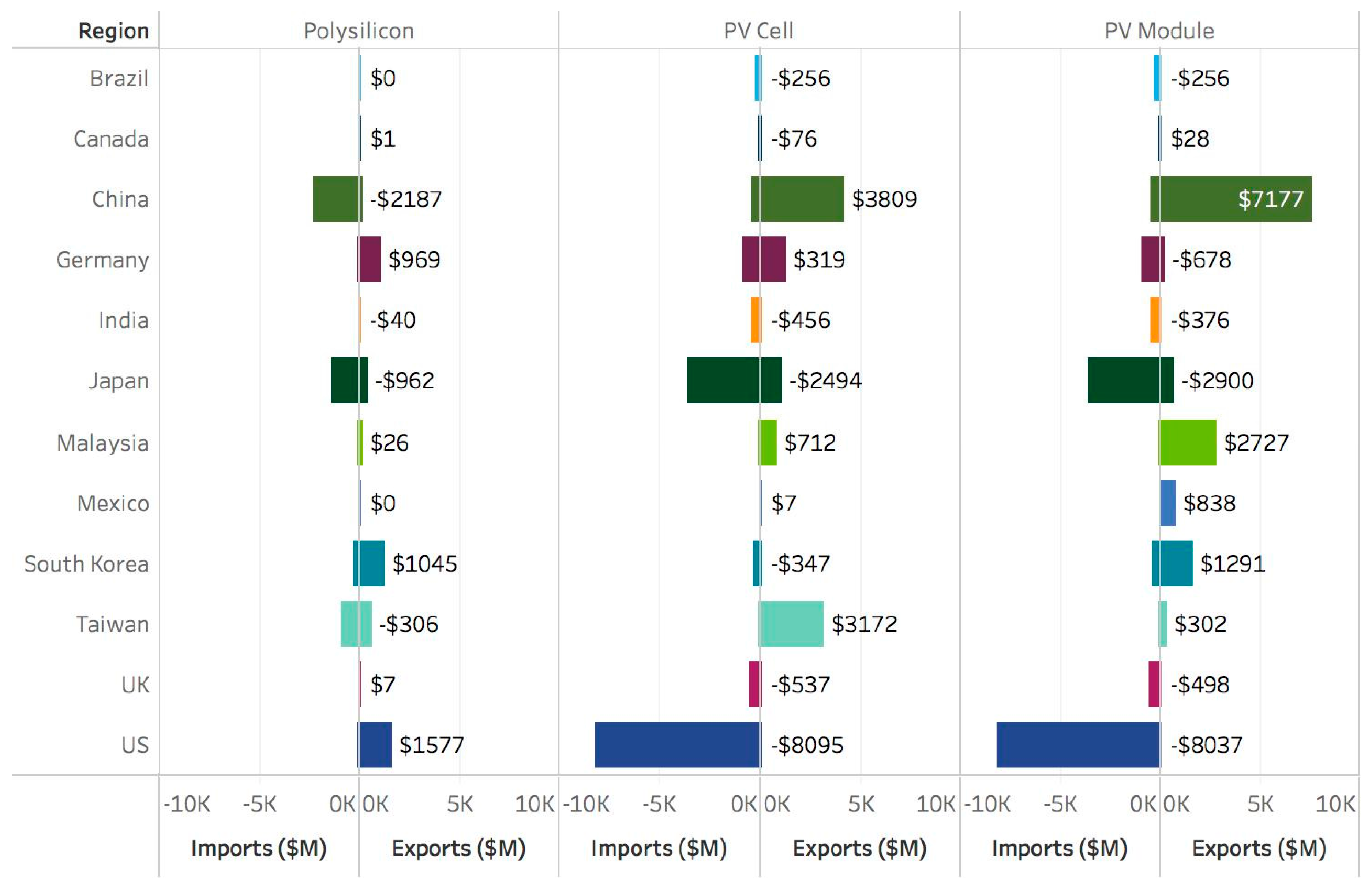

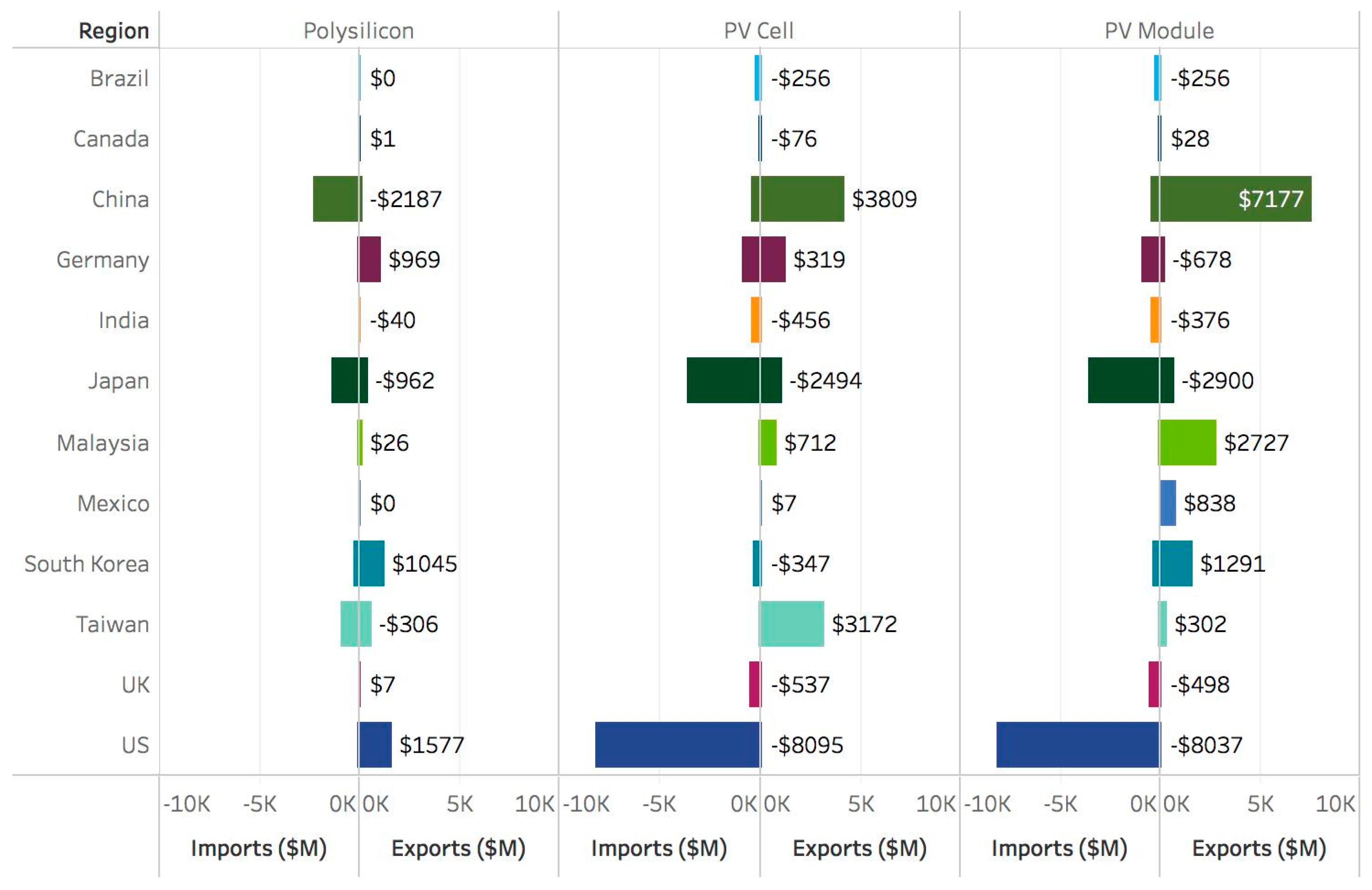

1.5. PV Module Supply Chain Trade Actions

- Trade actions can lead to trade diversion, shifting production, imports and exports.

- From a supply chain perspective, trade actions can increase the costs of inputs for downstream producers by limiting imports of lower cost upstream intermediates.

- Over the longer term, increasing use of trade actions can impact competitiveness and inhibit investment in the solar-PV energy sector.

2. Data and Methods

- Main system elements are broken down into places where items/materials exist at a point in time (“stocks”, in SD parlance) and the rate at which items move between such accumulations (“flows”). This ensures that a proper accounting exists as material moves from one accumulation to the next, sometimes in a series of steps, which is of particular importance in supply chain analysis.

- SD models are generally rich in feedback mechanisms, meaning that changes to one part of the system kick off internally driven responses, which “feedback” and ultimately affect the component that was originally changed. Information feedback assumes a causal connection between model elements (stocks and flows, in particular) [47]. This feedback dynamic is sometimes referred to as a “circular causality” and exists in one of two forms: positive feedback (which tends to accelerate the rate of change in the system) or negative feedback (which counteracts or slows down the rate of change). Combinations of these two types of feedback loops drive the non-linear behavior often seen in dynamic systems.

- Many SD models incorporate logic (including which information is being utilized) about decision rules on the part of decision makers; in aggregate, these actions can be thought of as dynamic response mechanisms. Analysis of system behavior can provide quantitative assessments of the impact of changes to decision rules and response mechanisms, leading to improved future decision making or a more robust understanding of how current system conditions would be different under alternative historical behavior rules.

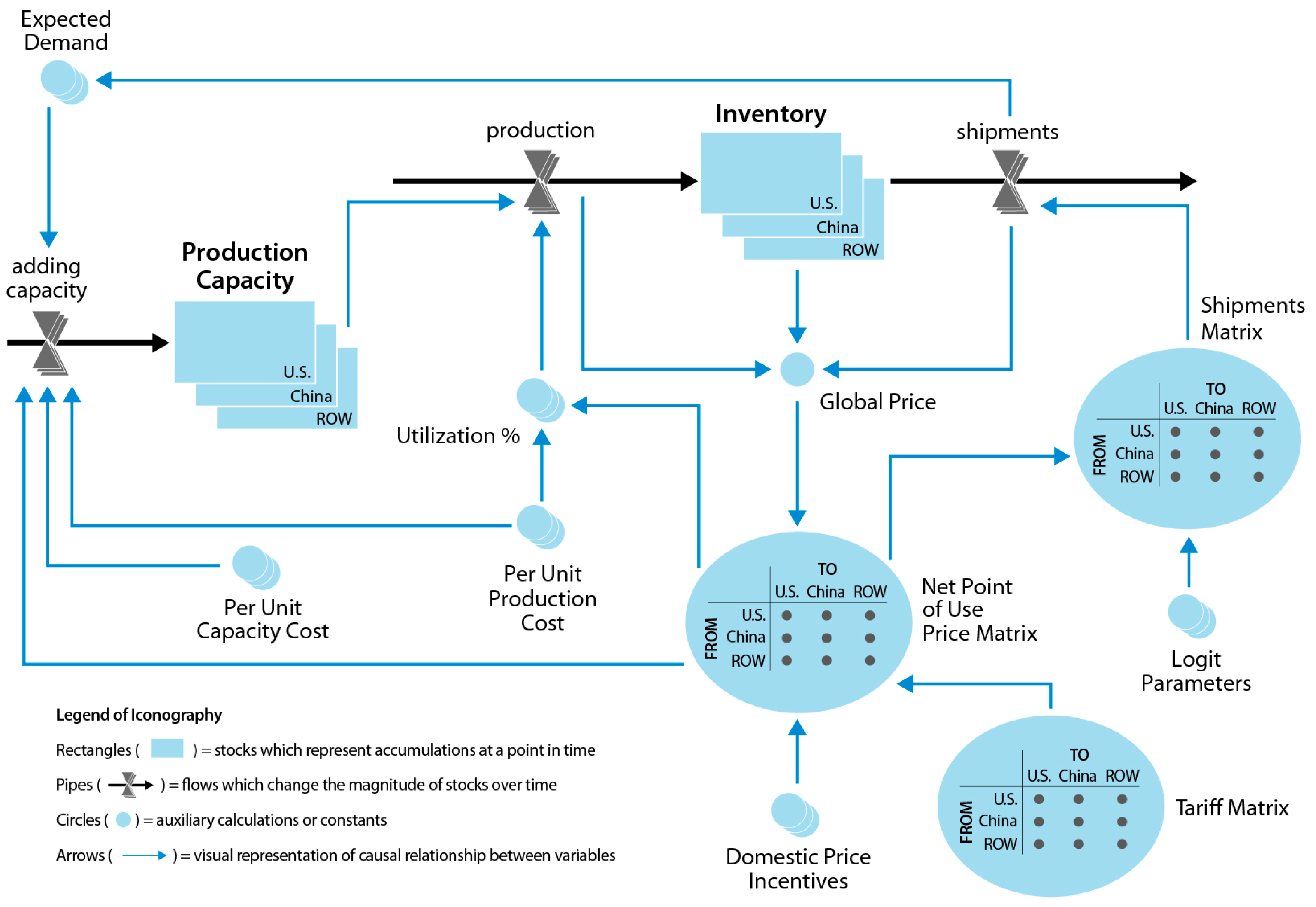

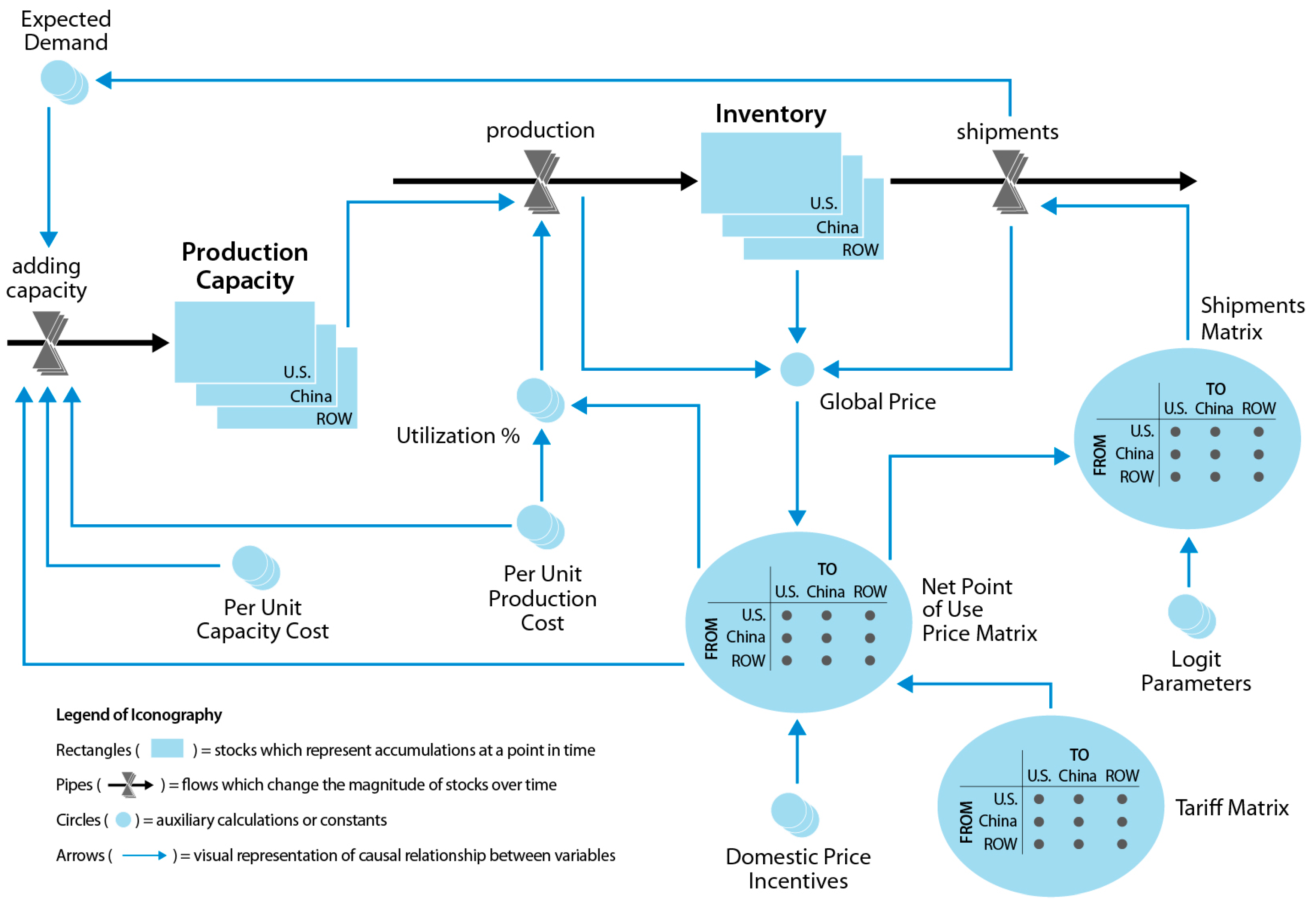

2.1. Polysilicon Manufacturing and Trade (PolyMAT) Model

- P = point-of-use price of polysilicon in region i based on regional origin j

- α = a scaling parameter for polysilicon price (P)

- k = the non-price-driven component of polysilicon attractiveness for any region i based on regional origin j

2.2. Scenario Overview

- The severity of the import duty on the relative volumes of imports and domestic supply

- Retaliatory duties on the relative volumes of imports and domestic supply

- The level of tariff absorbed by a region on global polysilicon flows

- Non-price “attractiveness” drivers on the relative volumes of imports and domestic supply.

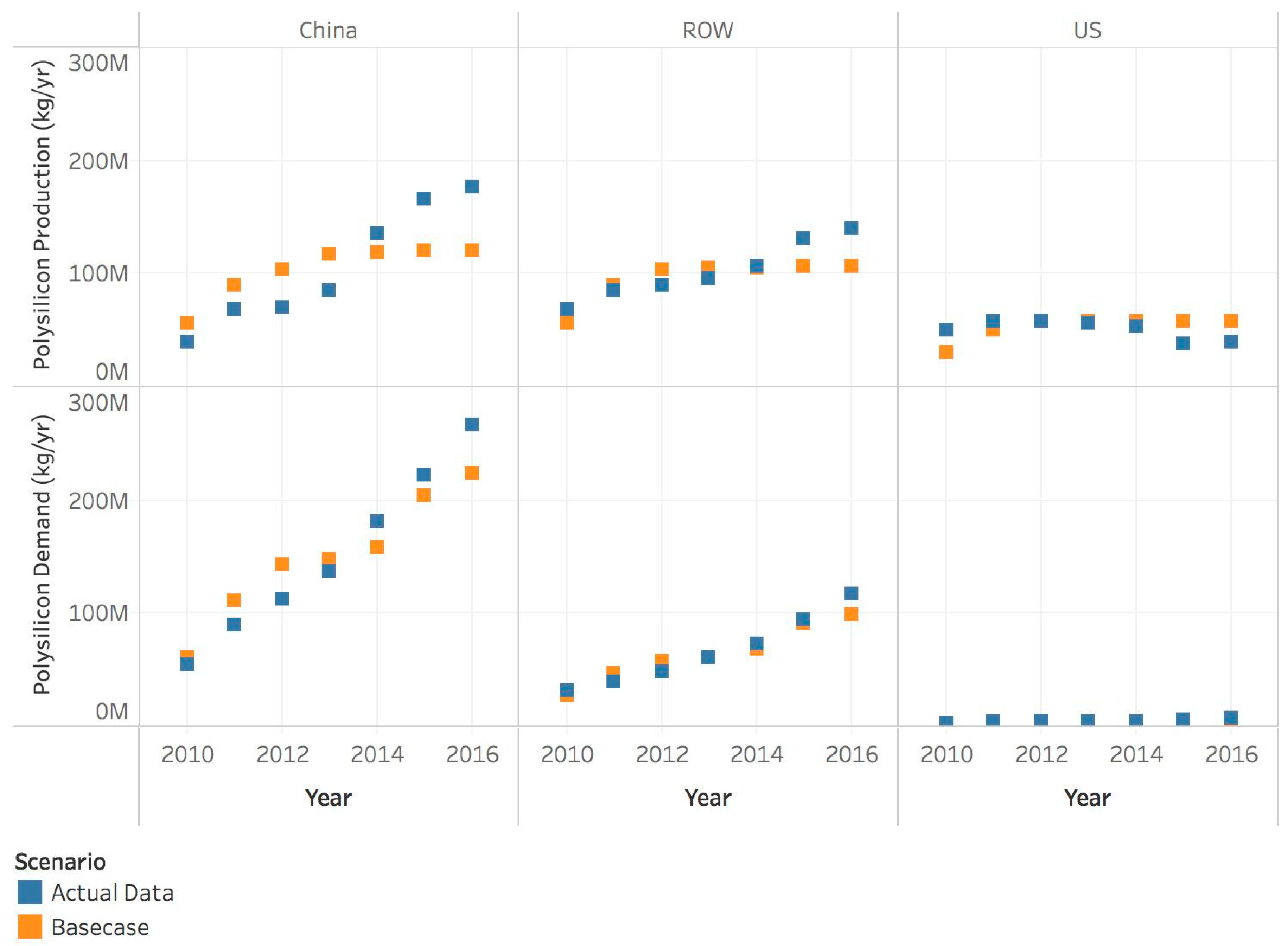

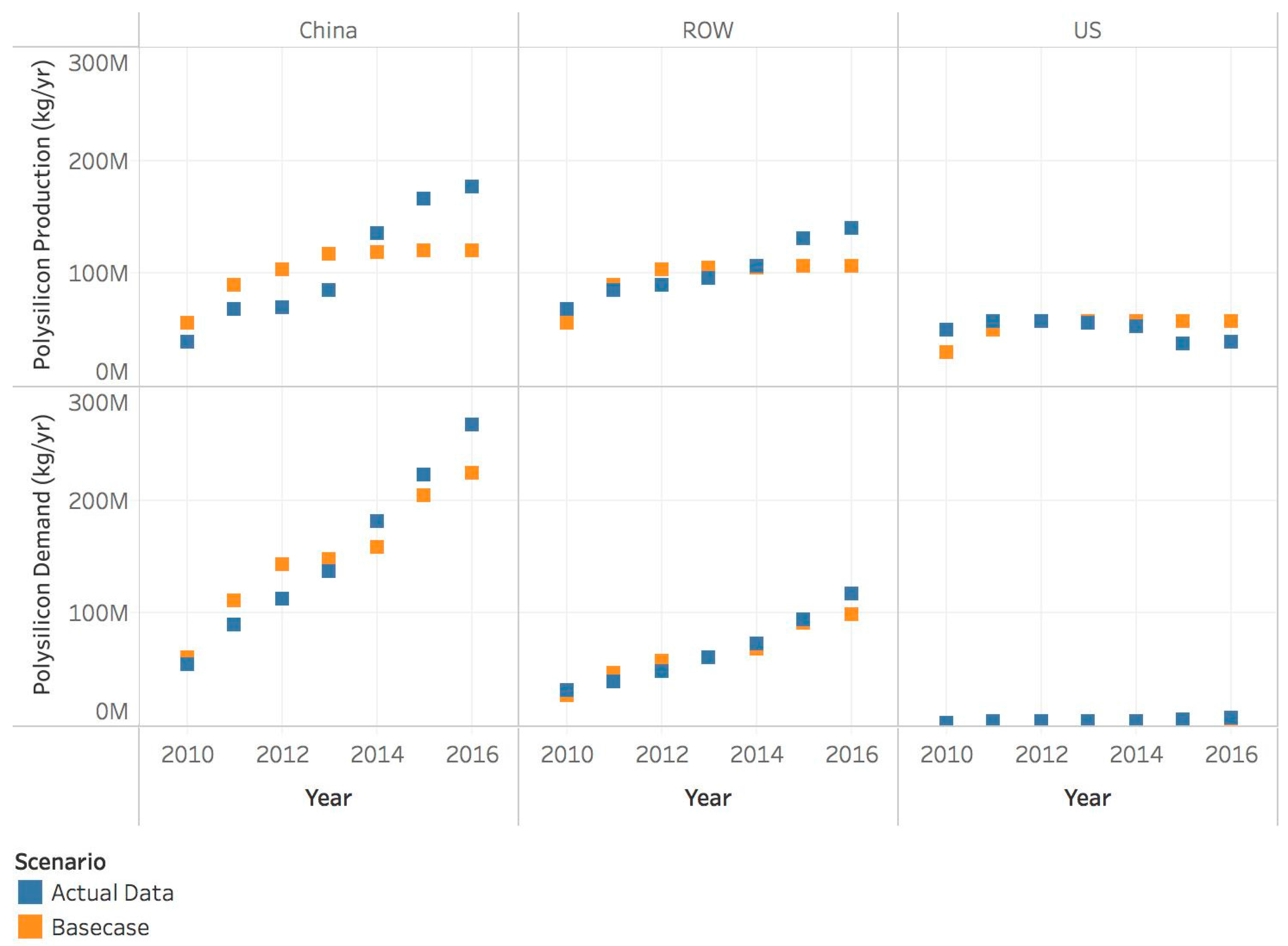

2.3. Base Case

3. Results

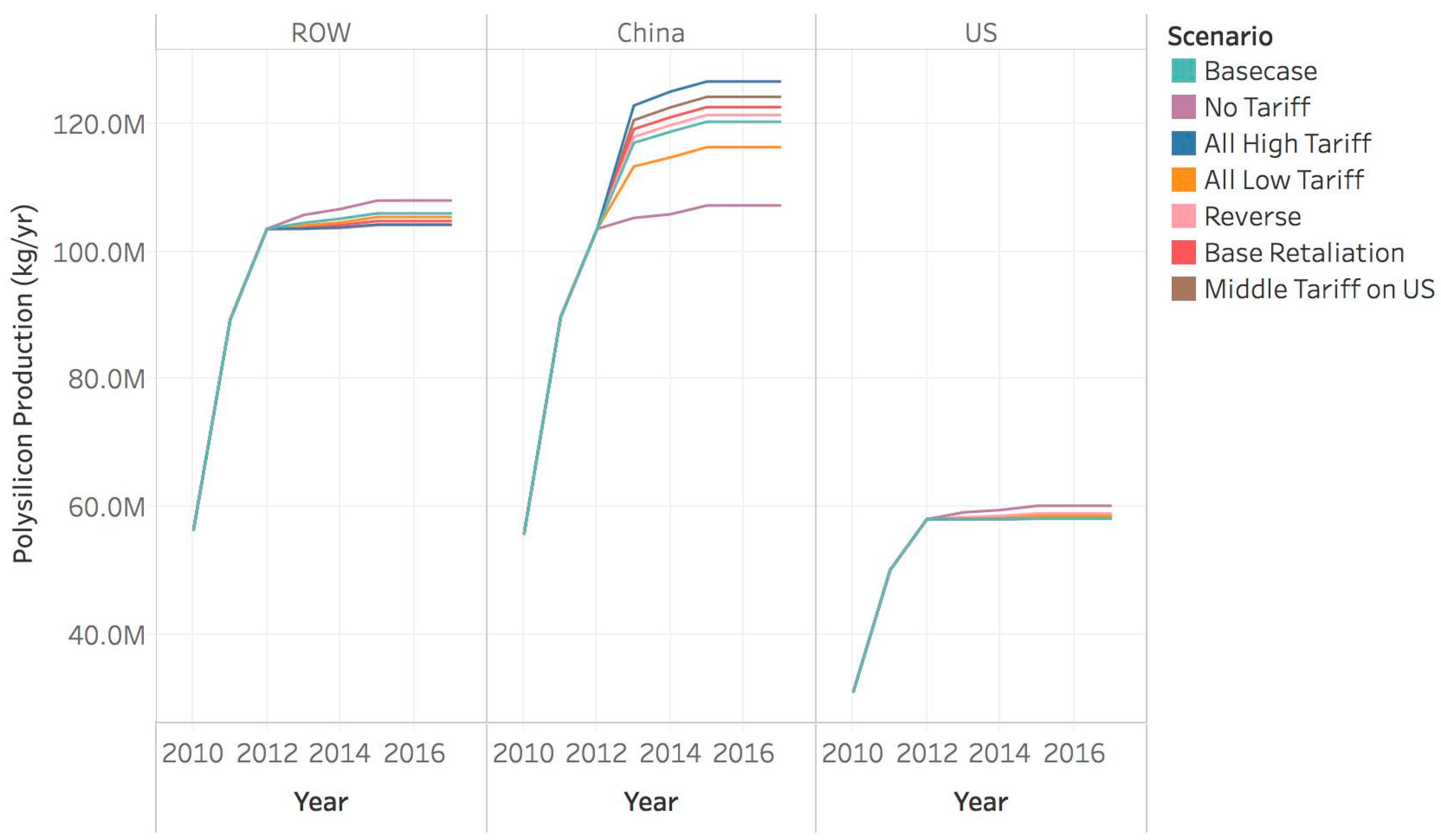

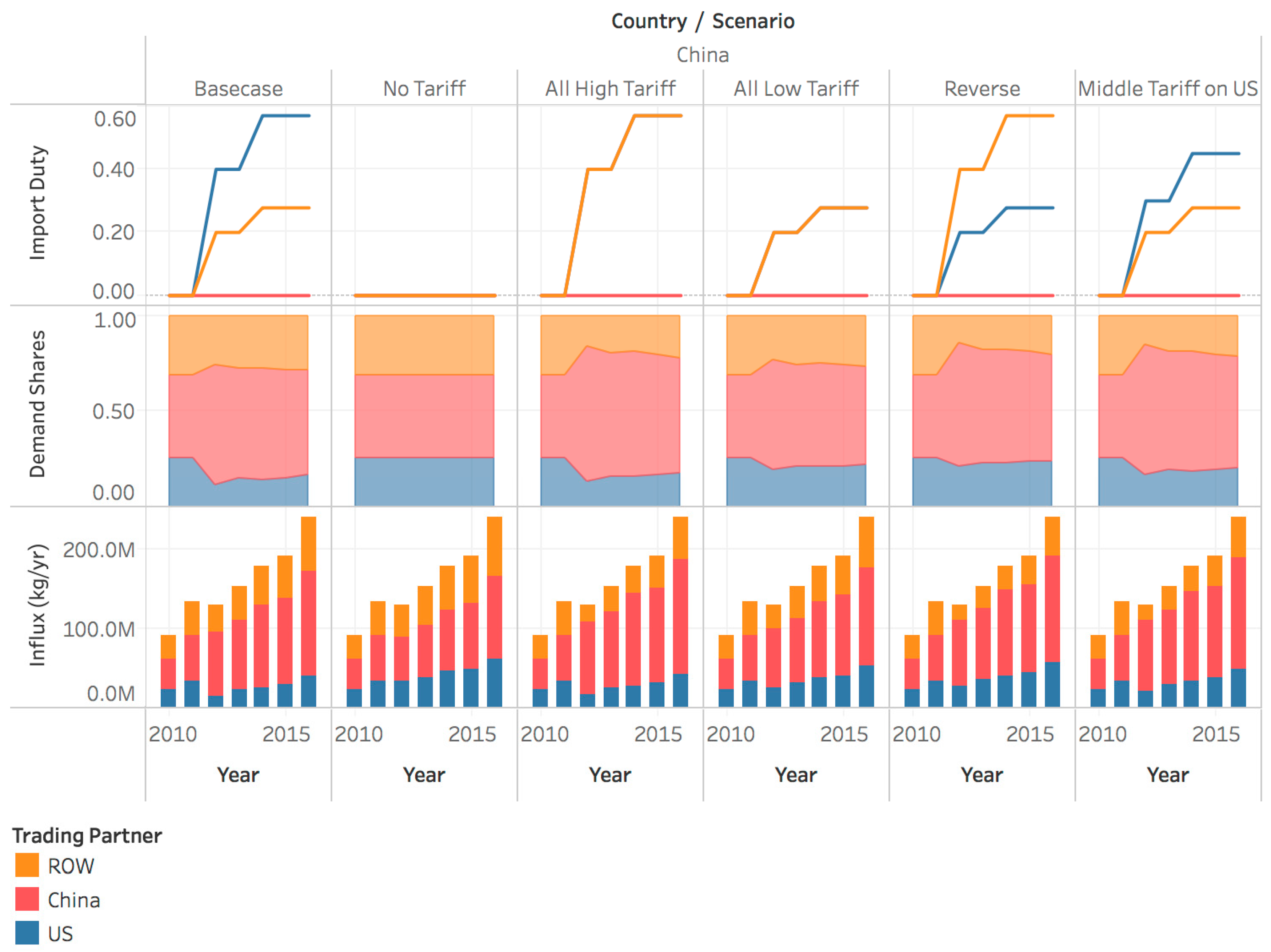

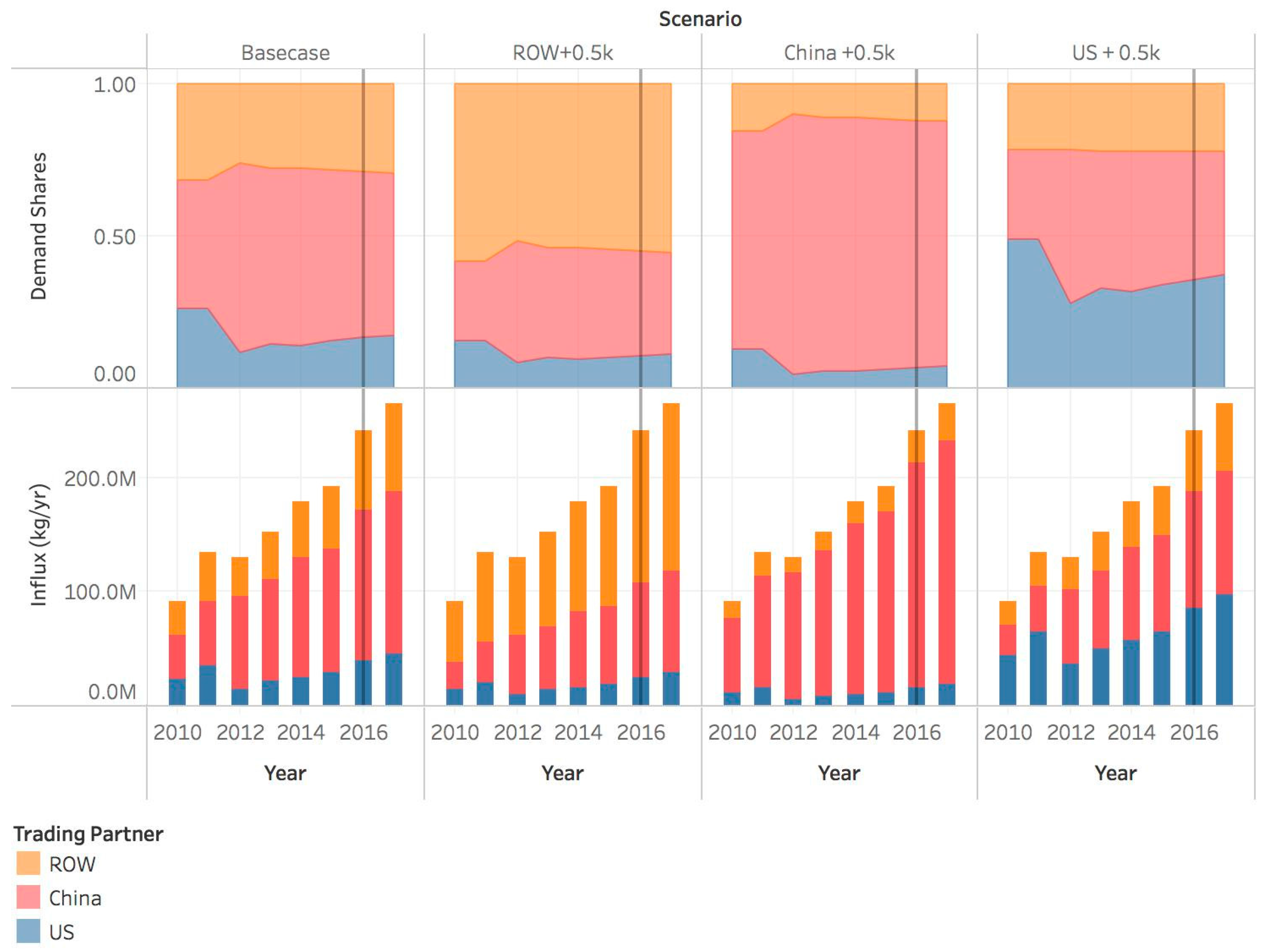

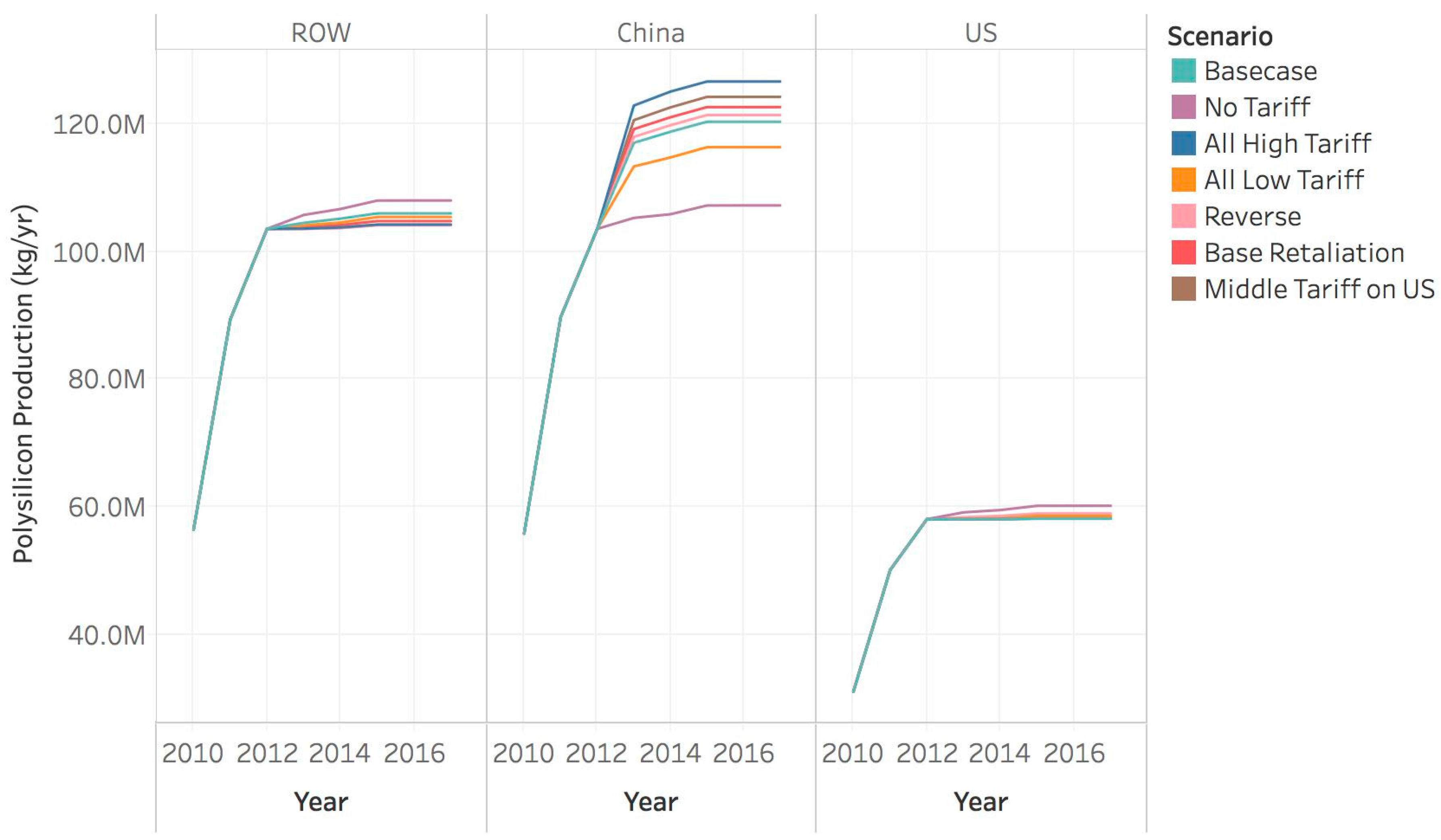

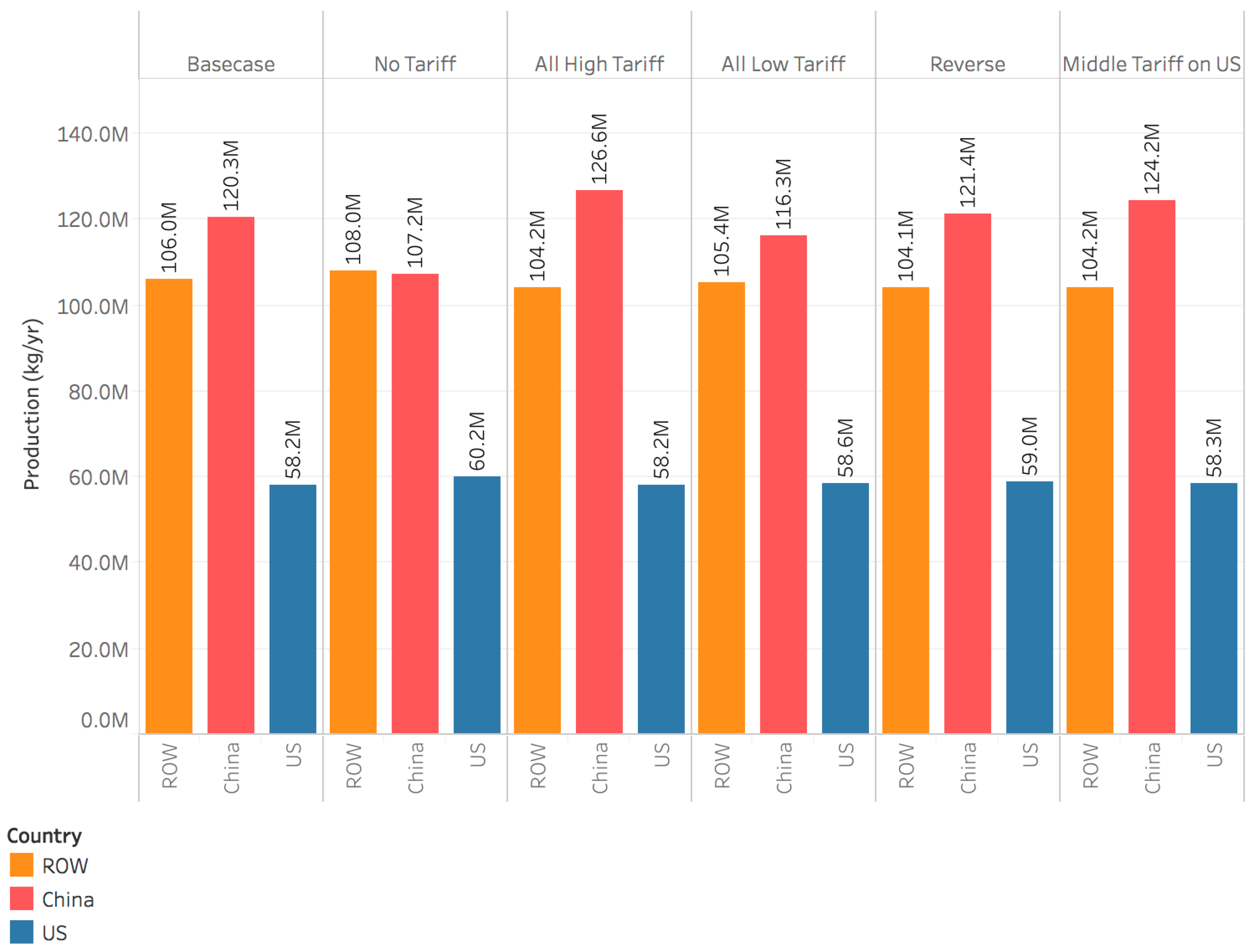

3.1. Trade Action Severity: Impact on Global Polysilicon Flows

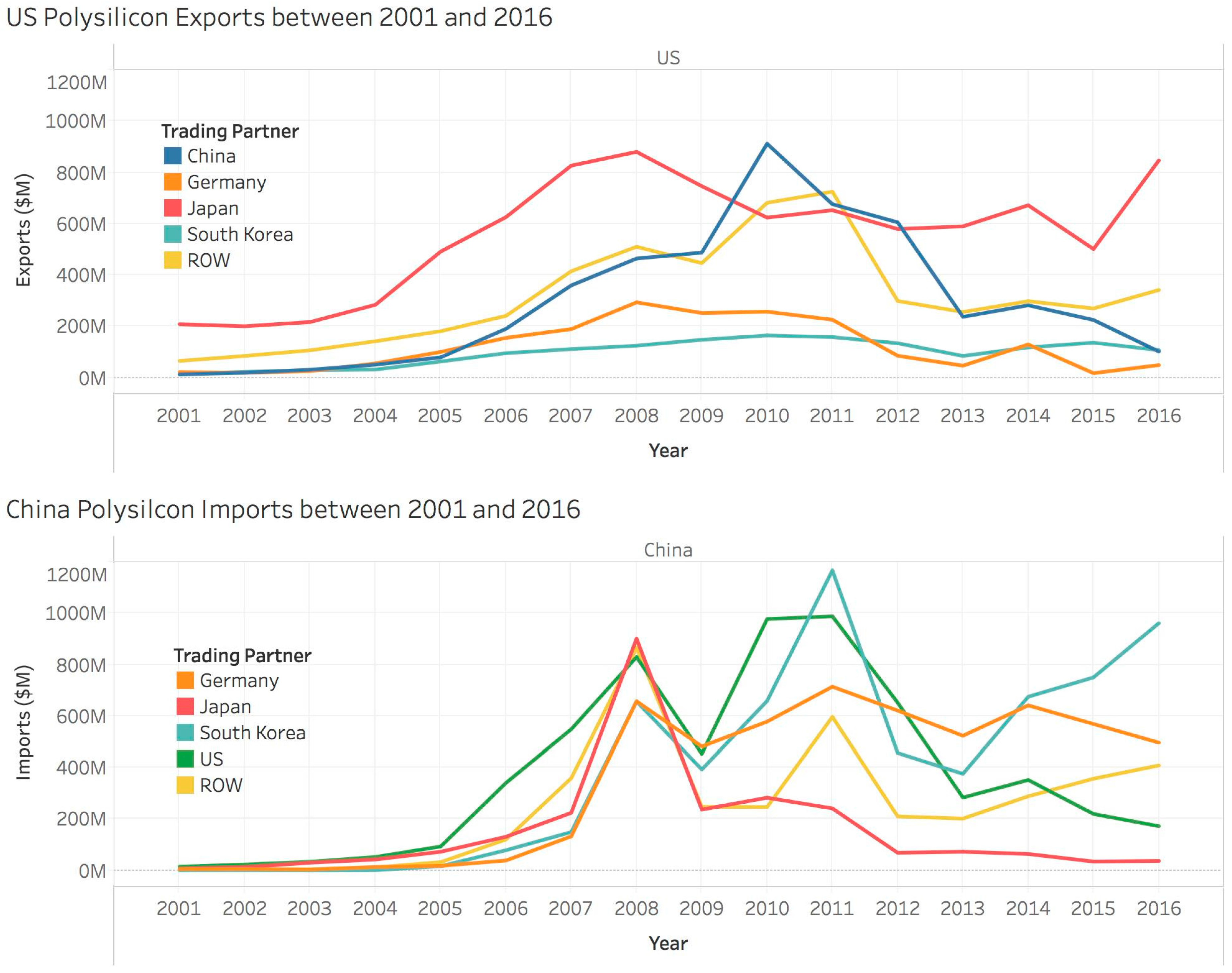

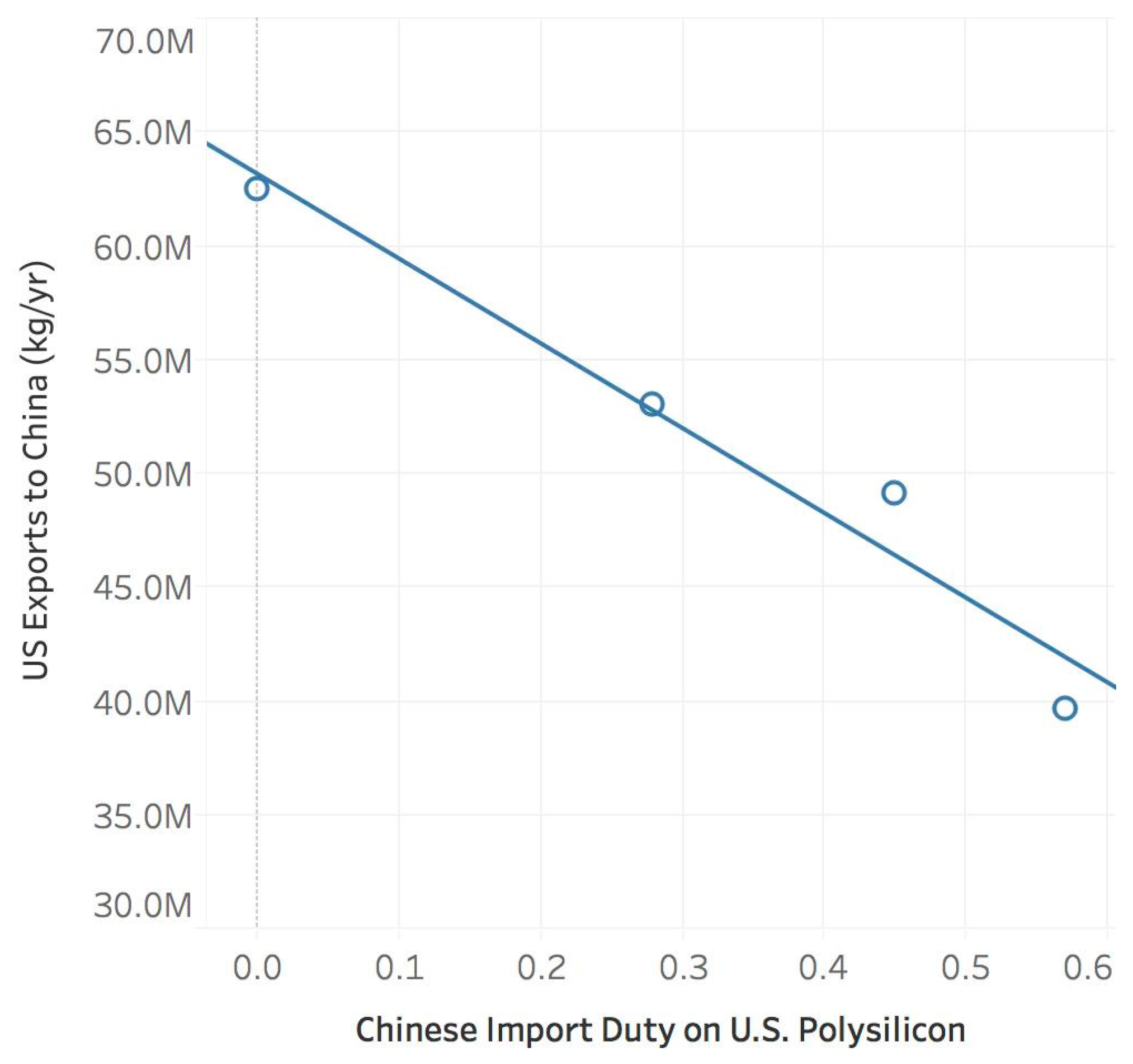

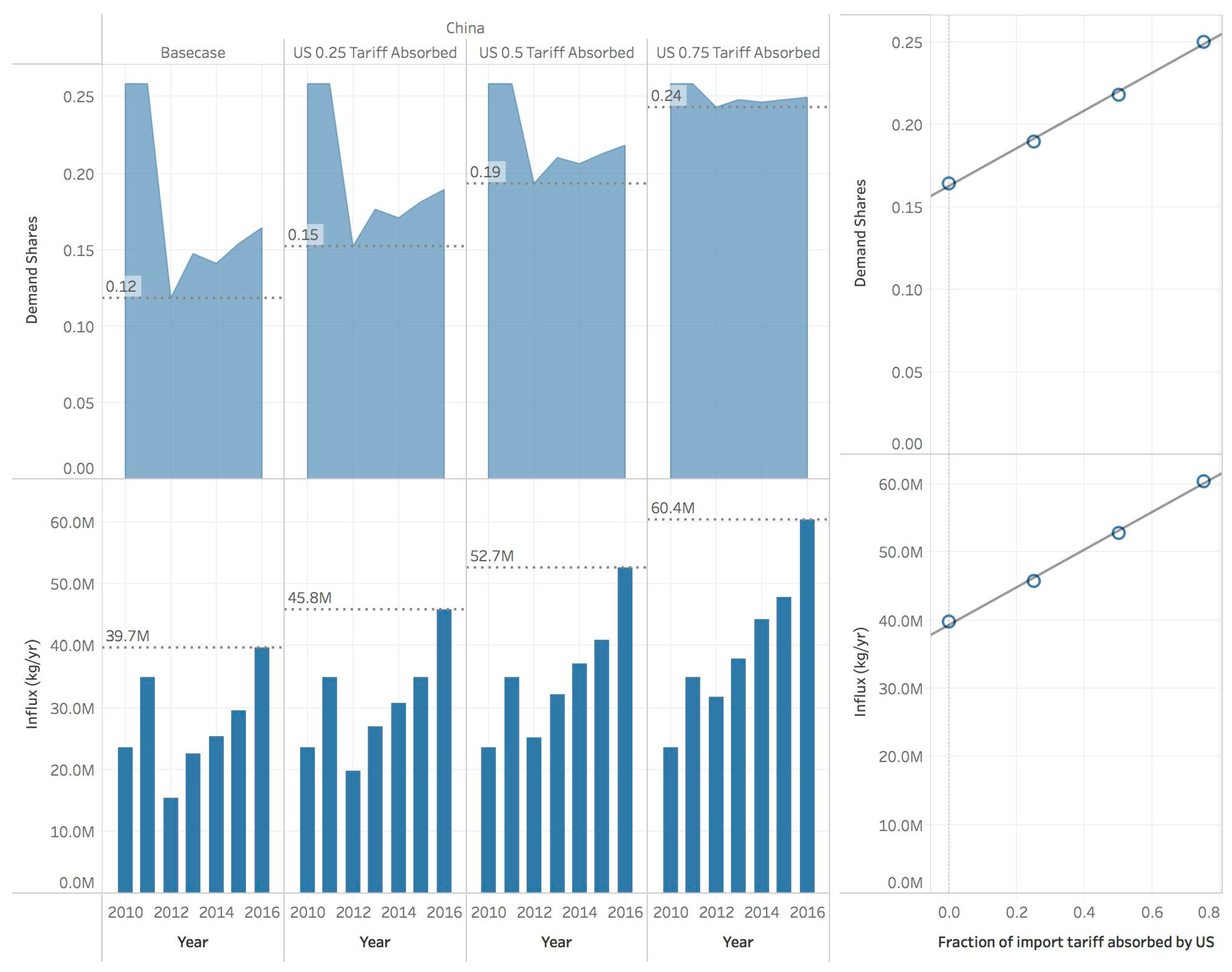

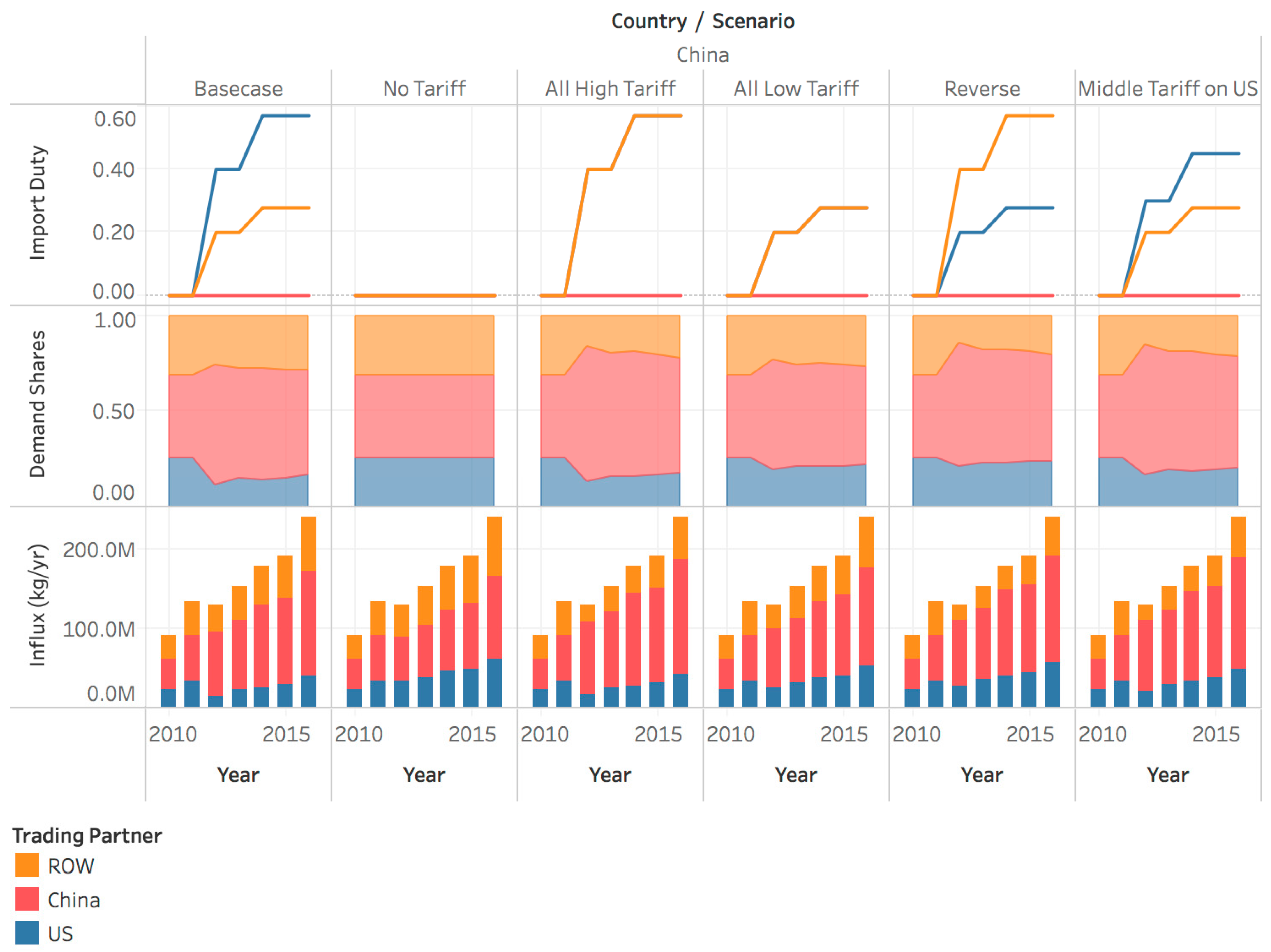

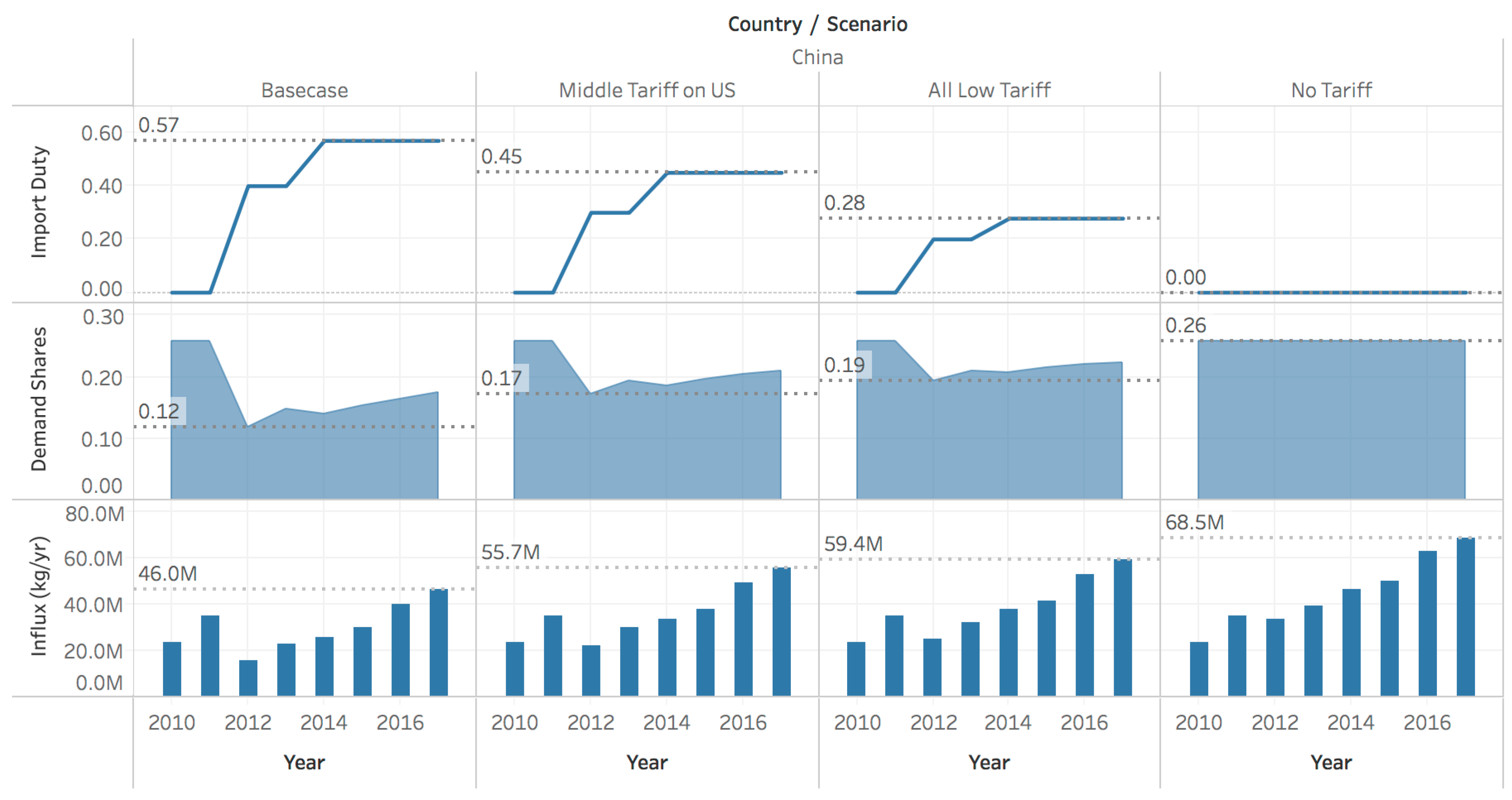

3.2. Impact of Tariff Severity on China and U.S. Flows

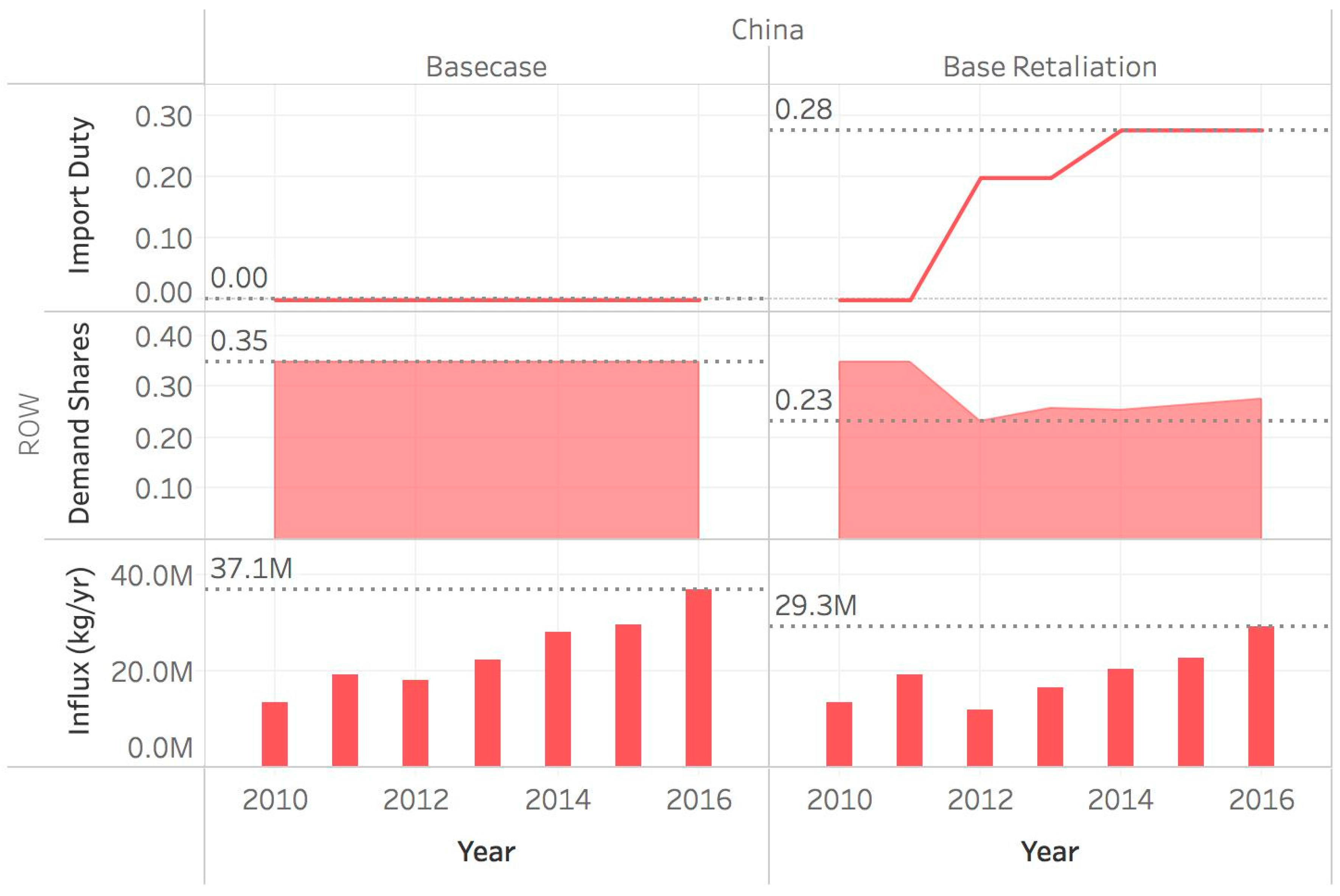

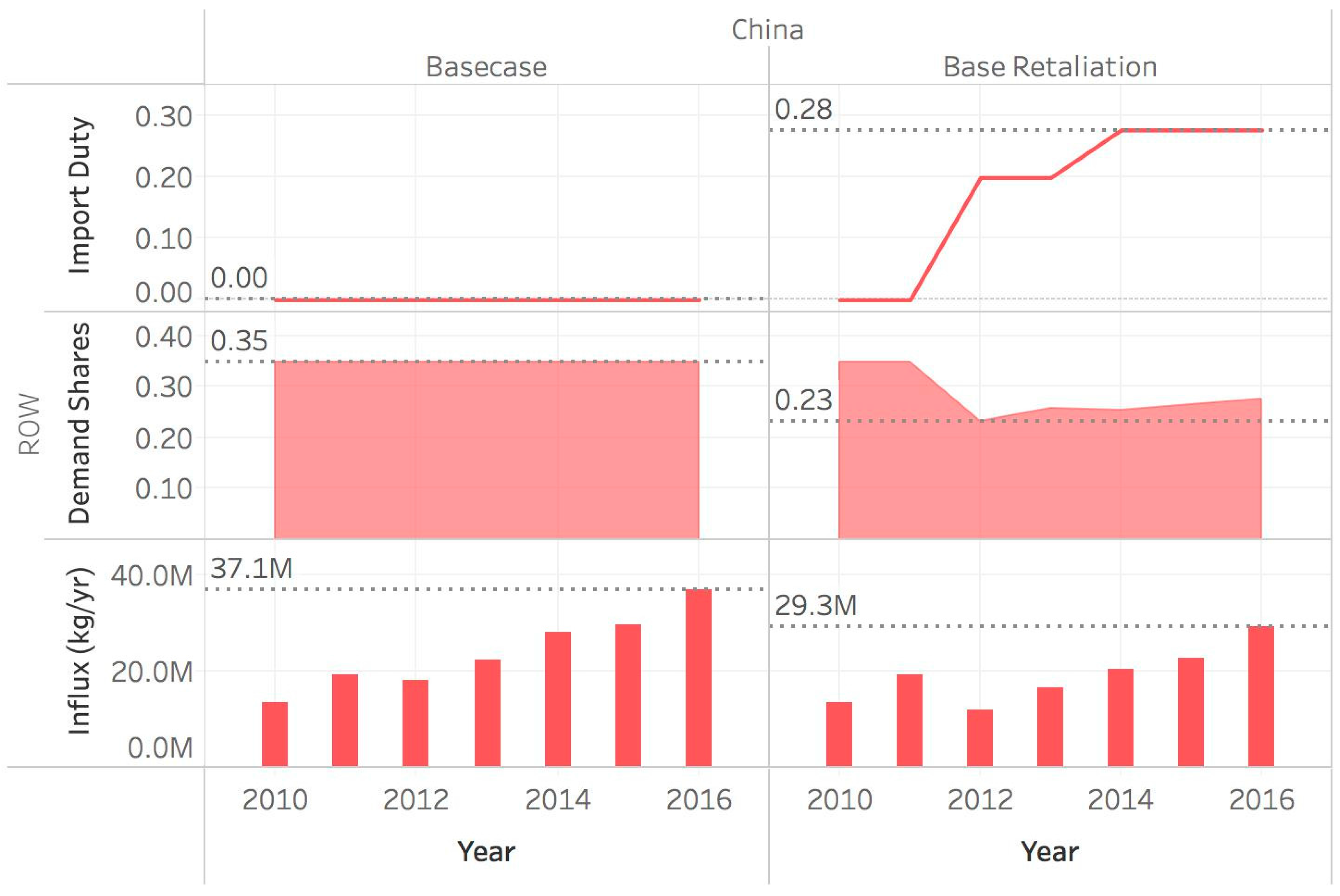

3.3. Retaliation: Impact of U.S. and ROW Tariffs on China Imports

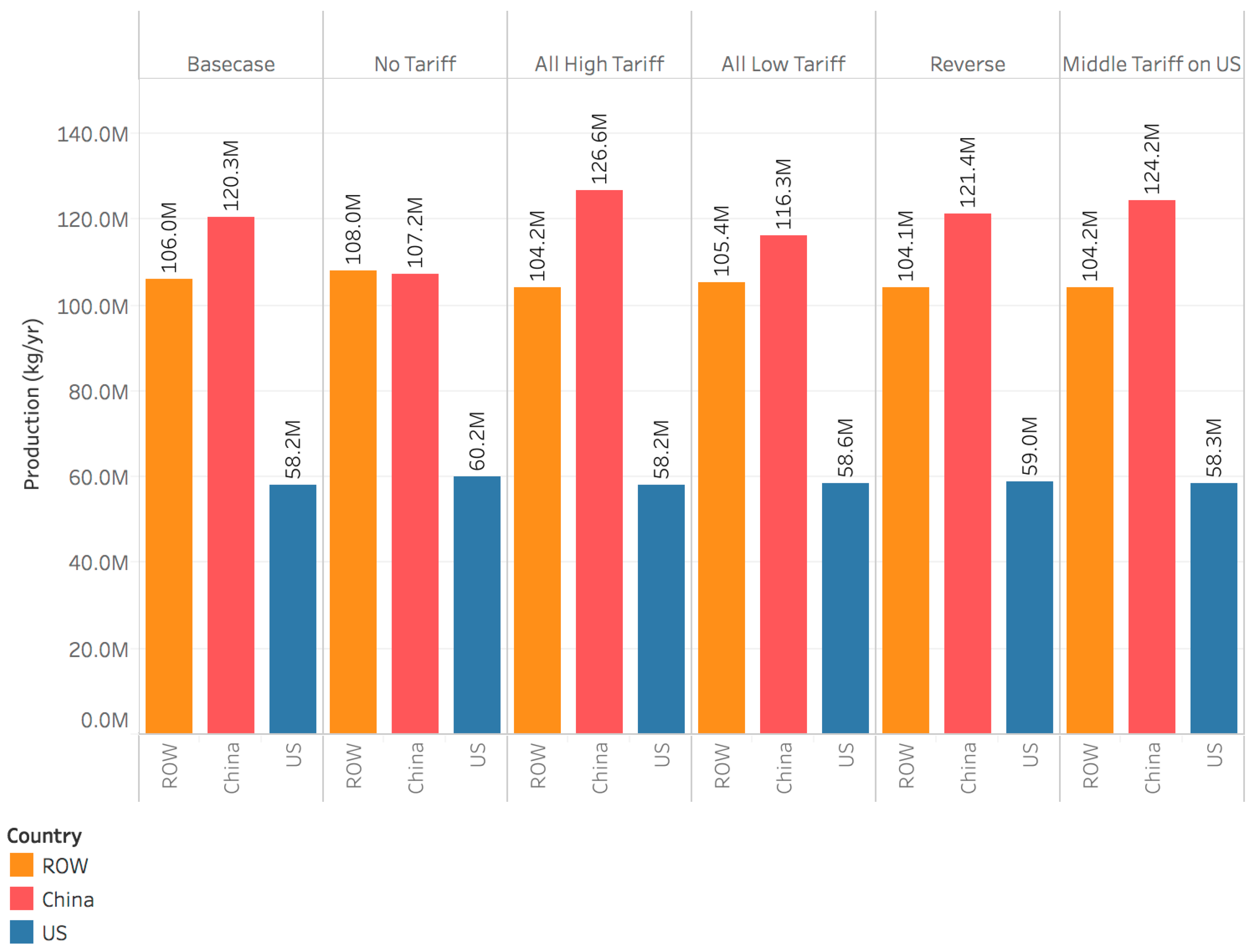

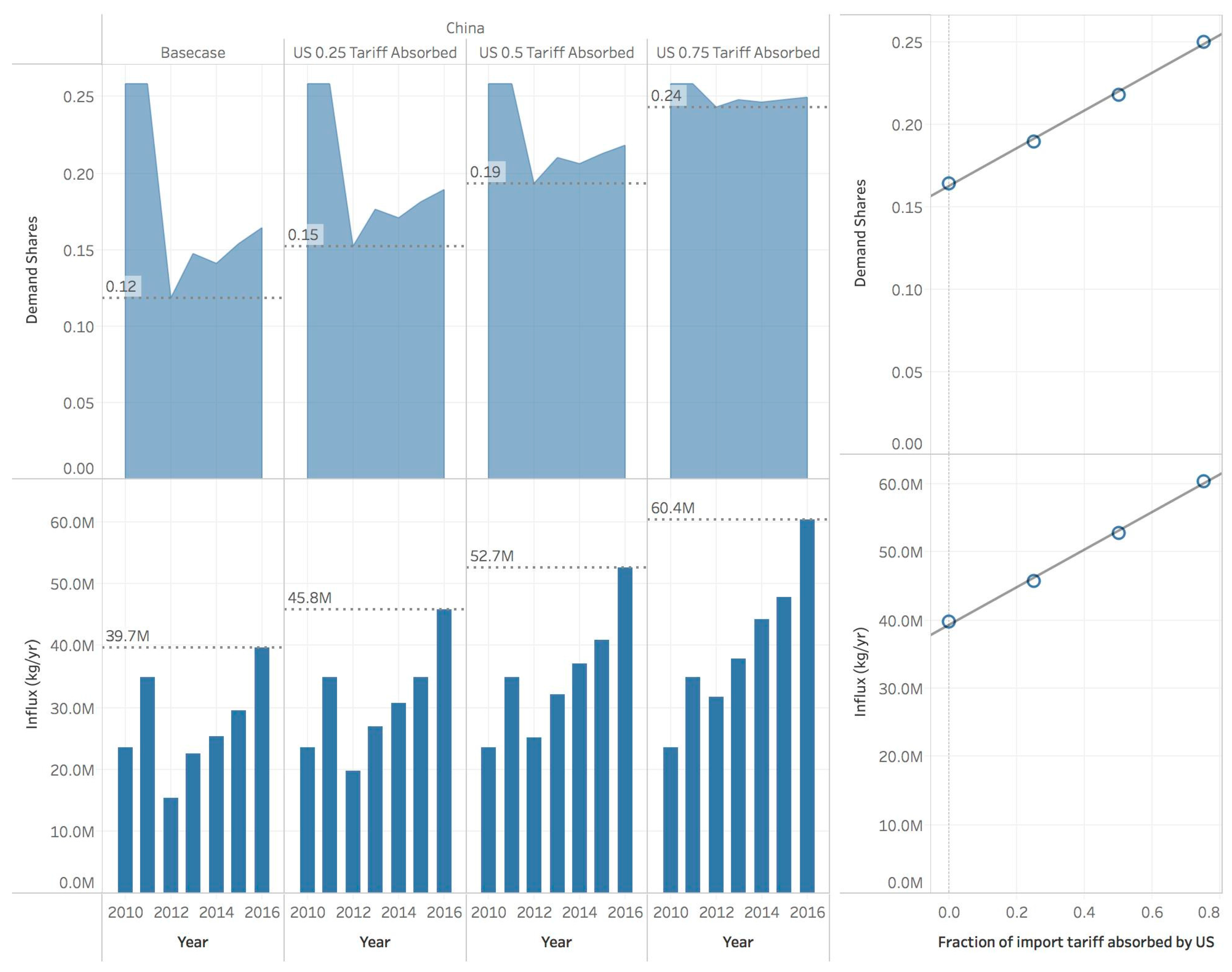

3.4. Impact of Differences in Level of Tariff Absorbed

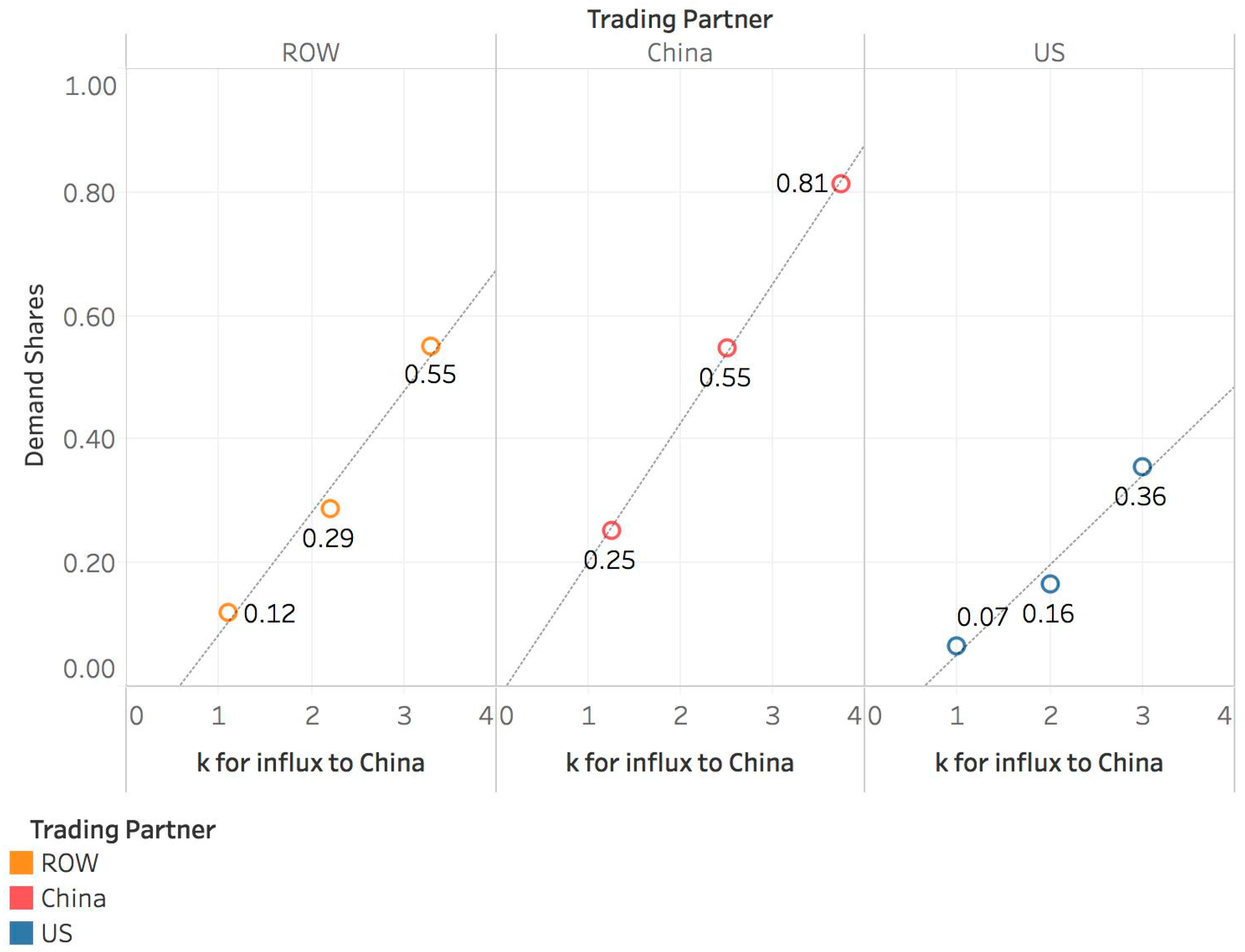

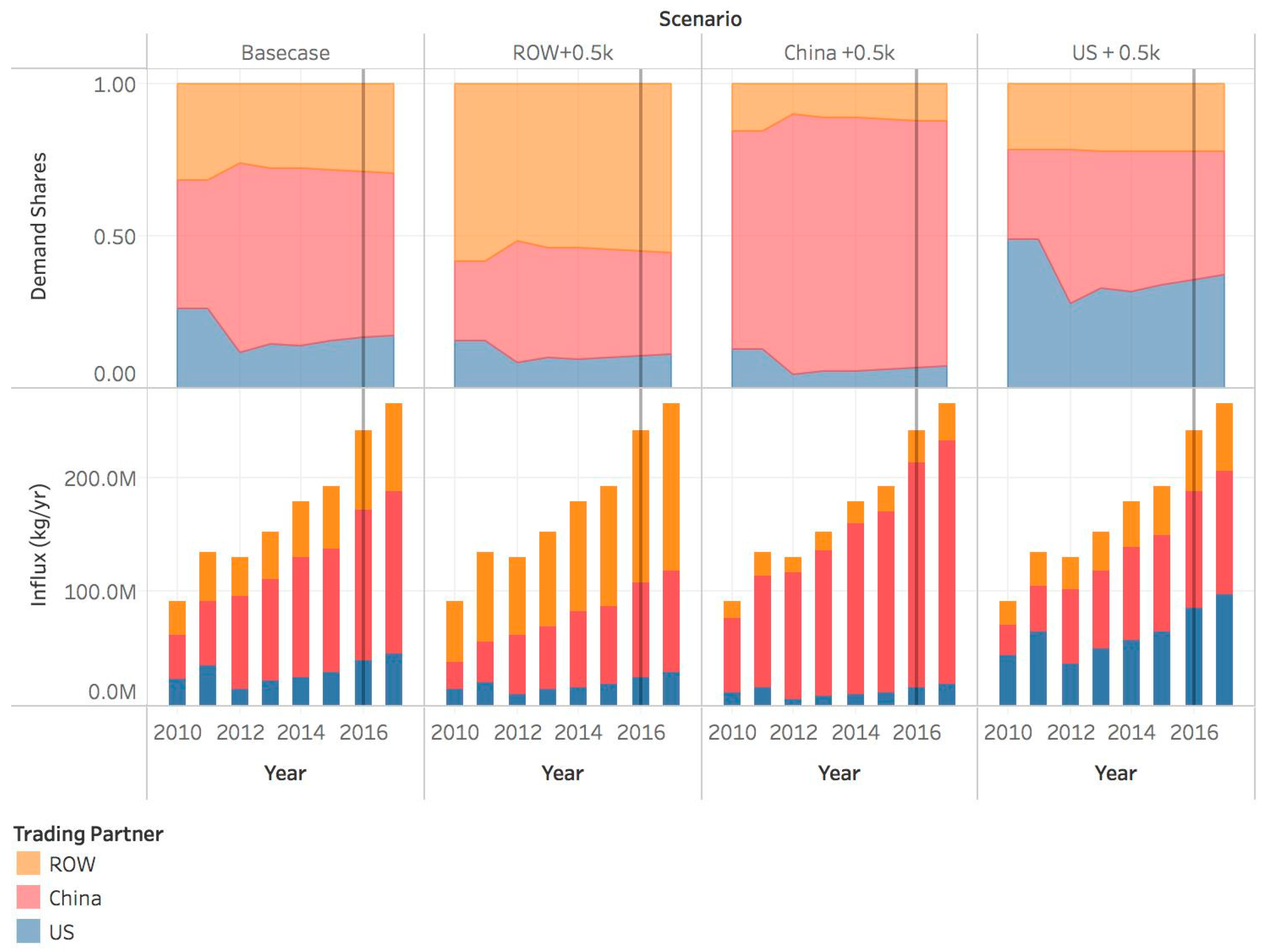

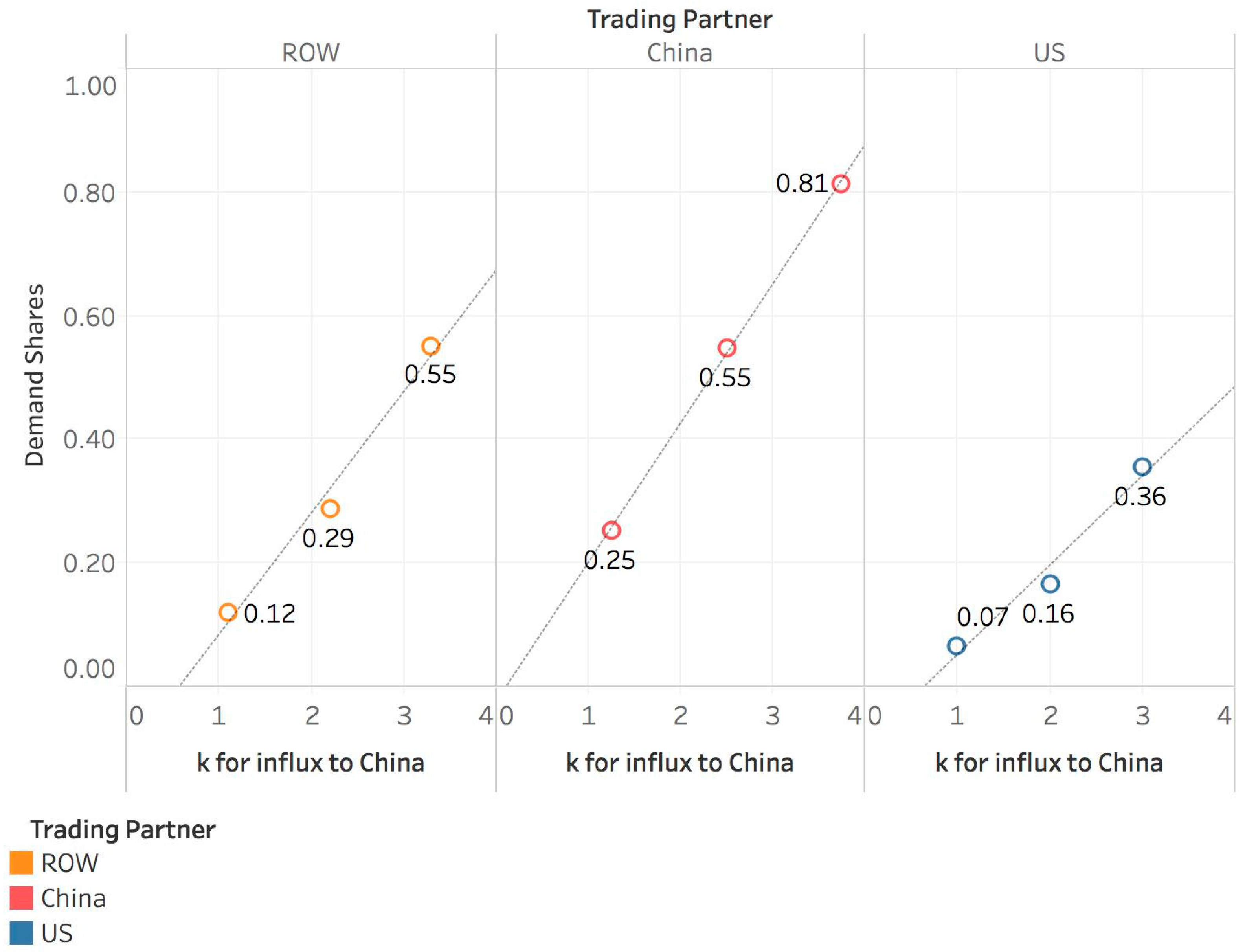

3.5. Impact of Differences in Relative Regional Attractiveness

4. Discussion and Conclusions

- The demand shares and influx from the United States and ROW into China show a steep drop in the year a new duty is assessed, driven by the change in relative polysilicon prices seen as the result of the tariff.

- As the severity of the duty placed on imports from any region increases, the export volumes decrease from that region into the region that levied the tariff. The magnitude of the decrease is influenced by the extent to which other regions are able to meet the tariff levier’s demand (as estimated in the attractiveness, or k, parameter). If, for instance, China levies a tariff on imports from the United States, and the U.S.’s production is clearly more attractive to China than is production from other countries (either because it is the cheapest available or because the United States is a more attractive trading partner for other reasons like trade agreements or political positioning), imports into China from the United States may be reduced but would be further reduced if the same tariff were levied, but China had other available trading partners that were at least as attractive as the United States.

- Once an import tariff has been imposed on a region, the contribution of that region to the duty-imposing region’s demand does not achieve pre-duty levels over the time period and specific scenarios investigated, even as global and regional demands increase. This is to say that, within the current model’s set of specifications, once a region’s exports into a country are hit with a tariff, they were never seen to contribute more total imports into the country than they did prior to the tariff. (Import volumes could, of course, return to or even exceed pre-tariff values, due to increased overall demand, but the presence of an import tariff means that demand share will continue to be less than what it was in a pre-tariff scenario.)

- A region can offset some of the negative trade impacts by absorbing all or part of an export tariff, thereby affecting the ultimate point-of-use price seen by end-users (and hence demand shares) in a tariff-imposing region.

Acknowledgments

Author Contributions

Conflicts of Interest

References

- Valentine, S. Emerging symbiosis: Renewable energy and energy security. Renew. Sustain. Energy Rev. 2011, 15, 4572–4578. [Google Scholar] [CrossRef]

- Winzer, C. Conceptualizing energy security. Energy Policy 2012, 46, 36–48. [Google Scholar] [CrossRef]

- Yergin, D. Ensuring energy security. Foreign Aff. 2006, 85, 69–82. [Google Scholar] [CrossRef]

- Kruyt, B.; van Vuuren, D.P.; de Vries, H.J.M.; Groenenberg, H. Indicators for energy security. Energy Policy 2009, 37, 2166–2181. [Google Scholar] [CrossRef]

- EIA. Real Prices Viewer. U.S. Energy Information Administration. Available online: https://www.eia.gov/outlooks/steo/realprices/ (accessed on 25 August 2017).

- Asif, M.; Muneer, T. Energy supply, its demand and security issues for developed and emerging economies. Renew. Sustain. Energy Rev. 2007, 11, 1388–1413. [Google Scholar] [CrossRef]

- Awerbuch, S. Portfolio-Based Electricity Generation Planning: Policy Implications For Renewables and Energy Security. Mitig. Adapt. Strateg. Glob. Chang. 2006, 11, 693–710. [Google Scholar] [CrossRef]

- Wang, Q.; Martinez-Anido, C.B.; Wu, H.; Florita, A.R.; Hodge, B.M. Quantifying the Economic and Grid Reliability Impacts of Improved Wind Power Forecasting. IEEE Trans. Sustain. Energy 2016, 7, 1525–1537. [Google Scholar] [CrossRef]

- Martinez-Anido, C.B.; Botor, B.; Florita, A.R.; Draxl, C.; Lu, S.; Hamann, H.F.; Hodge, B.M. The value of day-ahead solar power forecasting improvement. Sol. Energy 2016, 129, 192–203. [Google Scholar] [CrossRef]

- NREL (National Renewable Energy Laboratory). Distributed Generation Renewable Energy Estimate of Costs. National Renewable Energy Laboratory. Available online: https://www.nrel.gov/analysis/tech_lcoe_re_cost_est.html (accessed on 25 August 2017).

- Sandor, D.; Chung, D.; Keyser, D.; Mann, M.; Engel-Cox, J. Benchmarks of Global Clean Energy Manufacturing; Clean Energy Manufacturing Analysis Center: Golden, CO, USA, 2017; NREL/TP-6A50-65619.

- The Terminal, Bloomberg Professional Services. (Database: Commodity Price Graph for BNEF Survey Spot Polysilicon Overall Average Price 12/25/00 to 10/2/17). Available online: https://www.bloomberg.com/professional/solution/bloomberg-terminal/?utm_source=bloomberg-menu&utm_medium=terminal&bbgsum=DG-WS-PROF-SOLU-TERMINAL-bbgmenu (accessed on 10 October 2017).

- Hughes, L.; Meckling, J. The politics of renewable energy trade: The U.S.-China solar dispute. Energy Policy 2017, 105, 256–262. [Google Scholar] [CrossRef]

- Cimino, C.; Hufbauer, G. Trade Remedies in Renewable Energy: A Global Survey. In Proceedings of the China, the West, and the Challenge of Alternative Energy Innovation Workshop, Washington, DC, USA, 26 June 2014; Peter, G., Ed.; Peterson Institute for International Economics: Washington, DC, USA, 2014. Available online: http://cedmcenter.org/wp-content/uploads/2014/07/Cimino-trade.pdf (accessed on 15 July 2017).

- OECD (Organization for Economic Cooperation and Development). Overcoming Barriers to International Investment in Clean Energy; OECD Publishing: Paris, France, 2015. [Google Scholar] [CrossRef]

- Mints, P. Photovoltaic Manufacturer Capacity, Shipments, Price & Revenues 2015/2016. In SPV-Supply4; SPV Market Research: San Francisco, CA, USA, 2016. [Google Scholar]

- Mehta, S. Polysilicon 2015–2018: Supply, Demand, Cost and Pricing; GTM Research, Greentech Media: Cambridge, MA, USA, 2014. [Google Scholar]

- CEMAC (Clean Energy Manufacturing Analysis Center). Benchmarks of Global Clean Energy Manufacturing, 2nd ed.; Clean Energy Manufacturing Analysis Center (in Development): Golden, CO, USA, 2018.

- Fu, R.; James, T.L.; Woodhouse, M. Economic Measurements of Polysilicon for the Photovoltaic Industry: Market Competition and Manufacturing Competitiveness. IEEE J. Photovolt. 2015, 5, 515–524. [Google Scholar] [CrossRef]

- Bernreuter, J. The Polysilicon Market Outlook 2020; Bernreuter Research: Wurzburg, Germany, 2016. [Google Scholar]

- REN21 Secretariat. Advancing the Global Renewable Energy Transition: Highlights of the REN21 Renewables 2017 Global Status Report; REN21 Secretariat: Paris, France, 2017; ISBN 978-3-9818107-7-6. [Google Scholar]

- PV Module Intelligence Service, HIS Markit Technology. (Database: PV Suppliers Tracker–Q4 2016). Available online: https://technology.ihs.com/Services/441328/pv-module-intelligence-service (accessed on 3 May 2017).

- Woditsch, P.; Koch, W. Solar grade silicon feedstock supply for PV industry. Sol. Energy Mater. Sol. Cells 2002, 72, 11–26. [Google Scholar] [CrossRef]

- Surplus Supply of Polysilicon Pressures Pricing—But Not All Polysilicon Prices are Equal. 18 April 2012. Available online: https://technology.ihs.com/405979/surplus-supply-of-polysilicon-pressures-pricingbut-not-all-polysilicon-prices-are-equal (accessed on 19 July 2017).

- Lewis, J.I. The Rise of Renewable Energy Protectionism: Emerging Trade Conflicts and Implications for Low Carbon Development. Glob. Environ. Politics 2014, 14, 10–35. [Google Scholar] [CrossRef]

- Crystalline Silicon Photovoltaic Cells, Whether or Not Assembled Into Modules. From the People’s Republic of China: Countervailing Duty Order, 77 Fed. Reg. 236, 73017. 7 December 2012. Available online: https://www.gpo.gov/fdsys/pkg/FR-2012-12-07/html/2012-29669.htm (accessed on 27 September 2017).

- Crystalline Silicon Photovoltaic Cells, Whether or Not Assembled Into Modules. From the People’s Republic of China: Amended Final Determination of Sales at Less Than Fair Value, and Antidumping Duty Order, 77 Fed. Reg. 236, 73018. 7 December 2012. Available online: https://www.gpo.gov/fdsys/pkg/FR-2012-12-07/html/2012-29668.htm (accessed on 27 September 2017).

- European Commission. EU Imposes Definitive Measures on Chinese Solar Panels, Confirms Undertaking with Chinese Solar Panel Exporters, Press Release IP/13/769. 2 December 2013. Available online: http://europa.eu/rapid/press-release_IP-13-1190_en.htm (accessed on 27 September 2017).

- Commission Implementing Decision on Confirming the Acceptance of an Undertaking Offered in Connection with the Anti-Dumping and Anti-Subsidy Proceedings Concerning Imports of Crystalline Silicon Photovoltaic Modules and Key Components (i.e., Cells) Originating in or Consigned from the People’s Republic of China for the Period of Application of Definitive Measures [2013] OJ L325/214. Available online: http://trade.ec.europa.eu/doclib/docs/2013/december/tradoc_151946.UT.en.L325-2013.pdf (accessed on 27 September 2017).

- Commission Implementing Regulation (EU) 2017/367 of 1 March 2017 Imposing a Definitive Anti-Dumping Duty on Imports of Crystalline Silicon Photovoltaic Modules and Key Components (i.e., Cells) Originating in or Consigned from the People’s Republic of China Following an Expiry Review Pursuant to Article 11 of Regulation (EU) 2016/1036 of the European Parliament and of the Council and Terminating the Partial Interim Review Investigation Pursuant to Article 11 of Regulation (EU) 2016/1036 [2017] OJ L56/131. Available online: http://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32017R0367&from=EN (accessed on 27 September 2017).

- Certain Crystalline Silicon Photovoltaic Products from the People’s Republic of China: Antidumping Duty Order; and Amended Final Affirmative Countervailing Duty Determination and Countervailing Duty Order. 80 Fed. Reg. 32, 8592; 18 February 2015. Available online: https://www.gpo.gov/fdsys/pkg/FR-2015-02-18/html/2015-03183.htm (accessed on 28 December 2017).

- Certain Crystalline Silicon Photovoltaic Products from Taiwan: Antidumping Duty Order. 80 Fed. Reg. 32, 8596; 18 February 2015. Available online: https://www.gpo.gov/fdsys/pkg/FR-2015-02-18/html/2015-03179.htm (accessed on 28 December 2017).

- Ministry of Commerce, People’s Republic of China (MOFCOM). Announcement No. 48, 2013, on the Preliminary Ruling of the Anti-Dumping Against Imports of Solar-Grade Polysilicon Originated in the USA and South Korea. 18 July 2013. Available online: http://english.mofcom.gov.cn/article/policyrelease/buwei/201308/20130800224101.shtml (accessed on 27 September 2017).

- Ministry of Commerce, People’s Republic of China (MOFCOM). Announcement No. 63, 2013, on the Preliminary Ruling of the Countervailing Investigation against Imports of Solar-Grade Polysilicon Originated in the U.S. 16 September 2013. Available online: http://english.mofcom.gov.cn/article/policyrelease/buwei/201309/20130900316570.shtml (accessed on 27 September 2017).

- Ministry of Commerce, People’s Republic of China (MOFCOM). Announcement No. 25, 2014, on Final Ruling on Anti-Dumping Investigation against Imports of Solar-Grade Polysilicon Originated in EU. 1 May 2014. Available online: http://english.gov.cn/policies/latest_releases/2014/08/23/content_281474983026898.htm (accessed on 27 September 2017).

- Ministry of Commerce, People’s Republic of China (MOFCOM). Announcement No. 26, 2014, on Final Ruling on the Countervailing Investigation against Imports of Solar-Grade Polysilicon Originated in the EU. 5 May 2014. Available online: http://english.mofcom.gov.cn/article/policyrelease/buwei/201405/20140500585551.shtml (accessed on 27 September 2017).

- Congressional Research Service. U.S. Solar Photovoltaic Manufacturing: Industry Trends, Global Competition, Federal Support; Platzer, M.D., Ed.; R42509; Congressional Research Service: Washington, DC, USA, 2015. Available online: https://fas.org/sgp/crs/misc/R42509.pdf (accessed on 19 July 2017).

- Certain Crystalline Silicon Photovoltaic Products from the People’s Republic of China: Initiation of Countervailing Duty Investigation. 79 Fed. Reg. 4667; 29 January 2014. Available online: https://www.gpo.gov/fdsys/pkg/FR-2014-01-29/html/2014-01743.htm (accessed on 27 September 2017).

- Certain Crystalline Silicon Photovoltaic Products from the People’s Republic of China and Taiwan: Initiation of Antidumping Duty Investigations. 79 Fed. Reg. 4661; 29 January 2014. Available online: https://www.gpo.gov/fdsys/pkg/FR-2014-01-29/html/2014-01738.htm (accessed on 27 September 2017).

- Commission Implementing Regulation (EU) on Imposing Definitive Countervailing Duties on Imports of Solar Glass Originating in the People’s Republic of China [2014] OJ L142/23. Available online: http://trade.ec.europa.eu/doclib/docs/2014/may/tradoc_152501.def.en.L142-2014.pdf (accessed on 27 September 2017).

- Commission Implementing Regulation (EU) 2015/1394 of 13 August 2015 amending Regulation (EU) No 470/2014, as amended by Regulation (EU) 2015/588, on Imposing a Definitive Anti-Dumping Duty and Collecting Definitively the Provisional Duty Imposed on Imports of Solar Glass Originating in the People’s Republic of China Following an Absorption Reinvestigation Pursuant to Article 12 of Council Regulation (EC) No 1225/2009 [2014] OJ L215/42. Available online: http://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32015R1394&from=EN (accessed on 27 September 2017).

- Forrester, J.W. System dynamics—A personal view of the first fifty years. Syst. Dyn. Rev. 2007, 23, 345–358. [Google Scholar] [CrossRef]

- Forrester, J.W. Industrial dynamics. J. Oper. Res. Soc. 1997, 48, 1037–1041. [Google Scholar] [CrossRef]

- Sterman, J.D. Business Dynamics: Systems Thinking and Modeling for a Complex World; Irwin/McGraw-Hill: Boston, MA, USA, 2000; ISBN 978-0-07-231135-8. [Google Scholar]

- Meadows, D.; Randers, J.; Meadows, D. Limits to Growth: The 30-Year Update; Chelsea Green Publishing: White River Junction, VT, USA, 2004. [Google Scholar]

- Millington, J.D.A.; Xiong, H.; Peterson, S.; Woods, J. Integrating Modelling Approaches for Understanding Telecoupling: Global Food Trade and Local Land Use. Land 2017, 6, 56. [Google Scholar] [CrossRef]

- Richardson, G.P. Feedback Thought in Social Science and Systems Theory; Pegasus Communications, Inc.: Encino, CA, USA, 1999. [Google Scholar]

- Luna-Reyes, L.F.; Andersen, D.L. Collecting and analyzing qualitative data for system dynamics: Methods and models. Syst. Dyn. Rev. 2003, 19, 271–296. [Google Scholar] [CrossRef]

- Qudrat-Ullah, H.; Seong, B.S. How to do structural validity of a system dynamics type simulation model: The case of an energy policy model. Energy Policy 2010, 38, 2216–2224. [Google Scholar] [CrossRef]

- Chiung-Wen, H. Using a system dynamics model to assess the effects of capital subsidies and feed-in tariffs on solar PV installations. Appl. Energy 2012, 100, 205–217. [Google Scholar] [CrossRef]

- Vimmerstedt, L.; Bush, B.W.; Hsu, D.D.; Inman, D.; Peterson, S.O. Maturation of biomass-to-biofuels conversion technology pathways for rapid expansion of biofuels production: A system dynamics perspective. Biofuels Bioprod. Biorefin. 2015, 9, 158–176. [Google Scholar] [CrossRef]

- Houari, Y.; Speirs, J.; Candelise, C.; Gross, R. A system dynamics model of tellurium availability for CdTe. Prog. Photovolt. 2014, 22, 129–146. [Google Scholar] [CrossRef]

- Aslani, A.; Helo, P.; Naaranoja, M. Role of renewable energy policies in energy dependency in Finland: System dynamics approach. Appl. Energy 2014, 113, 758–765. [Google Scholar] [CrossRef]

- Al-Sarihia, A.; Contestabileb, M.; Chernia, J.A. Renewable Energy Policy Evaluation Using a System Dynamics Approach: The Case of Oman Paper. In Proceedings of the 33rd International Conference of the System Dynamics Society, Cambridge, MA, USA, 19–23 July 2015; Available online: http://www.systemdynamics.org/conferences/2015/papers/P1003.pdf (accessed on 12 November 2017).

- Osorio, S.; van Ackere, A. Security of Supply in the Swiss Electricity Market: A System Dynamics Approach. In Proceedings of the 32nd International Conference of the System Dynamics Society, Delft, The Netherlands, 20–24 July 2014; Available online: http://www.systemdynamics.org/conferences/2014/proceed/papers/P1201.pdf (accessed on 25 July 2017).

- Happach, R.M.; Größler, A. Modelling the inner-European trade volumes of natural gas. In Proceedings of the 32nd International Conference of the System Dynamics Society, Delft, The Netherlands, 20–24 July 2014; Available online: http://www.systemdynamics.org/conferences/2014/proceed/papers/P1138.pdf (accessed on 25 July 2017).

- Warner, E.; Inman, D.; Kunstman, B.; Bush, B.; Vimmerstedt, L.; Peterson, S.; Macknick, J.; Zhang, Y. Modeling Biofuel Expansion Effects on Land Use Change Dynamics. Environ. Res. Lett. 2013, 8, 10. [Google Scholar] [CrossRef]

- Chung-Shu, L.; Chih-Tung, H.; Dong-Shang, C.; Cheng-Hsing, H. How the European Union’s and the United States’ anti-dumping duties affect Taiwan’s PV industry: A policy simulation. Renew. Sustain. Energy Rev. 2016, 53, 296–305. [Google Scholar] [CrossRef]

- Isee Systems. 2017. Available online: https://www.iseesystems.com/store/products/ (accessed on 9 September 2017).

- Train, K.E. Discrete Choice Methods with Simulation, 1st ed.; Cambridge University Press: Cambridge, UK, 2003. [Google Scholar]

- U.S. Department of Energy. Energy Challenges. In Quadrennial Technology Review; Energy Efficiency and Renewable Energy; U.S. Government Publishing Office: Washington, DC, USA, 2015; pp. 11–32. Available online: https://energy.gov/sites/prod/files/2015/09/f26/QTR2015-01-Challenges.pdf (accessed on 12 November 2017).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Country | Demand | |||

| 2010 | 2016 | |||

| Volume (million kg) | Share (%) | Volume (million kg) | Share (%) | |

| China | 53.8 | 60.9% | 266.4 | 68.0% |

| United States | 2.8 | 3.2% | 7.8 | 2.0% |

| Japan | 6.6 | 7.4% | 10.0 | 2.5% |

| ROW | 25.2 | 28.5% | 107.6 | 27.5% |

| Country | Production | |||

| 2010 | 2016 | |||

| Volume (million kg) | Share (%) | Volume (million kg) | Share (%) | |

| China | 40.0 | 25.2% | 176.5 | 49.5% |

| South Korea | 15.7 | 9.9% | 69.8 | 19.6% |

| Germany | 30.0 | 18.9% | 51.5 | 14.5% |

| United States | 50.6 | 31.9% | 39.4 | 11.1% |

| ROW | 22.3 | 14.1% | 19.1 | 5.4% |

| Complainant Country | Subject Country | Subject Product(s) | Anti-Dumping Duty | Countervailing Duty | Investigation Initiated (Date) | Measure in Force (Date(s)) | Source(s) |

|---|---|---|---|---|---|---|---|

| United States | China | Modules from China made with third country c-Si PV cells | China: 26.71–165.04% | China: 27.64–49.79% | 2014 | 2015 * | [31,32,38,39] |

| China | c-Si PV cells made in China, regardless of where those cells are incorporated into modules. | 18.32–249.96% | 14.78–15.97% | 2011 | 2012 * | [26,27] | |

| European Union | China | Solar glass | 17.5–75.4% on selected firms; 67.1% on all other firms | 3.2–17.1% on selected firms; 17.1% on all other firms | 2013 | 2014–2019 ** | [40,41] |

| China | Solar cells and modules | 27.3–64.9% on selected firms; 53.4% on all other firms | 3.5–11.5% on selected firms; 11.5% on all other firms | 2012 | 2013–2018 | [28,29,30] | |

| China | U.S. | Solar-grade polysilicon | 53.30–57% | 0–2.1% | 2012 | 2014–2019 | [20,33,34] |

| EU | Solar-grade polysilicon | 42% on selected firms; 14.3% on all other firms | 1.2% on all firms | 2012 | 2014–2017 | [20,35,36] | |

| South Korea | Solar-grade polysilicon | 2.4–48.7% on selected firms; 12.3% on all other firms | None | 2012 | 2014–2019 | [20,33] |

| Scenario | Import Duty Level, 2012–2013, 2014–2019 * | k, the Non-Price-Driven Component of Attractiveness | Fraction of Tariff Absorbed (by Exporting Region) | Scenario Goal/Question Addressed | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| China–USA | China–ROW | USA–China | USA–ROW | ROW–USA | ROW–China | China–USA | China–ROW | China–China | |||

| Base Case | 40%, 57% | 20%, 28% | 0% | 0% | 0% | 0% | 2.0 | 2.2 | 2.5 | 0 | To what degree do model results align with historical data? |

| Impact of Duties on Global Polysilicon Flows | |||||||||||

| No Tariff | 0%, 0% | 0%, 0% | 0% | 0% | 0% | 0% | 2.0 | 2.2 | 2.5 | 0 | What if: China had not imposed tariffs? |

| Reverse | 20%, 28% | 40%, 57% | 0% | 0% | 0% | 0% | 2.0 | 2.2 | 2.5 | 0 | What if: China had imposed larger tariffs on the larger source of imports? |

| All High Tariff | 40%, 57% | 40%, 57% | 0% | 0% | 0% | 0% | 2.0 | 2.2 | 2.5 | 0 | What if: China had imposed higher tariff on all imports? |

| All Low Tariff | 20%, 28% | 20%, 28% | 0% | 0% | 0% | 0% | 2.0 | 2.2 | 2.5 | 0 | What if: China had imposed lower tariff on all imports? |

| Middle Tariff on USA | 30%, 45% | 20%, 28% | 0% | 0% | 0% | 0% | 2.0 | 2.2 | 2.5 | 0 | What is the relationship between the severity of China import tariff and U.S. imports? |

| Impact of Responses to Duties on Global Polysilicon Flows | |||||||||||

| Retaliation | 40%, 57% | 20%, 28% | 40%, 57% | 0% | 0% | 20%, 28% | 2.0 | 2.2 | 2.5 | 0 | What if: U.S. and ROW retaliated with tariffs on China imports? |

| Fraction of Tariff Absorbed | 40%, 57% | 20%, 28% | 0% | 0% | 0% | 0% | 2.0 | 2.2 | 2.5 | 0.25, 0.50, 0.75 | What if: U.S. absorbs China’s export tariff rather than passing it on? |

| Impact of Non-price Drivers on Global Polysilicon Flows ** | |||||||||||

| Increased influence of non-price drivers | 40%, 57% | 20%, 28% | 0% | 0% | 0% | 0% | 2.0 | 2.2 | 2.5 ± 50% | 0 | What if: China implements policies to increase use of domestic products (e.g., LCRs, production incentives)? |

| 40%, 57% | 20%, 28% | 0% | 0% | 0% | 0% | 2.0 ± 50% | 2.2 | 2.5 | 0 | What if: China establishes free trade agreement with U.S. or ROW or faces domestic shortage and needs to expand imports? (This is simulated through changes to the parameters in the model logit function.) | |

| 40%, 57% | 20%, 28% | 0% | 0% | 0% | 0% | 2.0 | 2.2 ± 50% | 2.5 | 0 | ||

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sandor, D.; Fulton, S.; Engel-Cox, J.; Peck, C.; Peterson, S. System Dynamics of Polysilicon for Solar Photovoltaics: A Framework for Investigating the Energy Security of Renewable Energy Supply Chains. Sustainability 2018, 10, 160. https://doi.org/10.3390/su10010160

Sandor D, Fulton S, Engel-Cox J, Peck C, Peterson S. System Dynamics of Polysilicon for Solar Photovoltaics: A Framework for Investigating the Energy Security of Renewable Energy Supply Chains. Sustainability. 2018; 10(1):160. https://doi.org/10.3390/su10010160

Chicago/Turabian StyleSandor, Debra, Sadie Fulton, Jill Engel-Cox, Corey Peck, and Steve Peterson. 2018. "System Dynamics of Polysilicon for Solar Photovoltaics: A Framework for Investigating the Energy Security of Renewable Energy Supply Chains" Sustainability 10, no. 1: 160. https://doi.org/10.3390/su10010160

APA StyleSandor, D., Fulton, S., Engel-Cox, J., Peck, C., & Peterson, S. (2018). System Dynamics of Polysilicon for Solar Photovoltaics: A Framework for Investigating the Energy Security of Renewable Energy Supply Chains. Sustainability, 10(1), 160. https://doi.org/10.3390/su10010160