Abstract

In the current context of the ban on fossil fuel vehicles (diesel and petrol) adopted by several European cities, the question arises of the development of the infrastructure for the distribution of alternative energies, namely hydrogen (for fuel cell electric vehicles) and electricity (for battery electric vehicles). First, we compare the main advantages/constraints of the two alternative propulsion modes for the user. The main advantages of hydrogen vehicles are autonomy and fast recharging. The main advantages of battery-powered vehicles are the lower price and the wide availability of the electricity grid. We then review the existing studies on the deployment of new hydrogen distribution networks and compare the deployment costs of hydrogen and electricity distribution networks. Finally, we conclude with some personal conclusions on the benefits of developing both modes and ideas for future studies on the subject.

1. Introduction

Since the diesel scandal (see F. Cuenot [1]), the authorities of several major European cities have decided to phase out diesel and petrol cars from city centres. The city of Paris, for example, has set itself the target of eliminating diesel cars by 2024 and petrol cars by 2030. More recently, the Brussels Region announced its goal of eliminating diesel cars from the European capital by 2030. In 2023, the European Union decided that from 2035, all new cars on the market must not emit CO2. This is to ensure that the transport sector can become carbon neutral by 2050. In the UK, as pointed out by Jenifer Baxter [2], the government has announced a ban on the sale of new passenger cars with conventional diesel and petrol engines by 2040. These two modes, as highlighted by Bicer et al. [3], are known to cause high levels of air pollution and are blamed for contributing to climate change and global warming.

In this context, two alternative propulsion modes can be considered:

- Electric cars using hydrogen to power a fuel cell vehicle (called FCEV for Fuel Cell Electric Vehicles);

- Electric vehicles using electricity from a battery (called BEV for Battery Electric Vehicles).

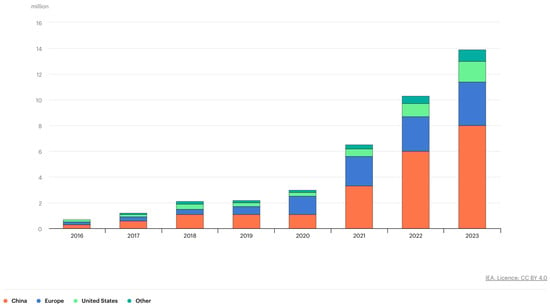

As the International Energy Agency points out in its 2023 report [4], few markets have been as dynamic in recent years as the electric car market. Not only is there exponential growth in sales (see Figure 1), but this increase in sales is also accompanied by a greatly expanded range of vehicles available on the market and improved performance, particularly in terms of significantly increased autonomy. As shown in Figure 1, in 2022, China will again lead the way with around 60% of global electric car sales. This means that more than half of the world’s electric cars are currently on the road in China. Europe is the second largest market: one in five cars sold in 2022 will be electric. The United States is the third largest market: 8% of cars sold will be electric. The IAE estimates that nearly one in five new cars sold in 2023 will be electric.

Figure 1.

World electric car sales 2016–2023 (source: IEA 2023 report [4]).

As these vehicles have a limited range, convenient access to refueling facilities is an important factor for the large-scale adoption of these two modes. In other words, a lack of refueling stations will be a major barrier to the large-scale adoption of these new vehicles. And as the construction of new refueling infrastructure (for FCEV and BEV) is capital intensive, it is important to examine their respective development costs.

In addition, the development of sufficient, high-quality charging infrastructure can reduce users’ fears of running out of battery power. It is, therefore, important to reassure consumers at this level (see Saber [5]).

However, it is not enough to install more terminals, it is also necessary to optimise their location. De Wolf et al. [6] show that it is important to locate new charging stations in a way that is depending on traffic and in a way that minimises the distance a car has to travel between its starting point and a potential charging point. Otherwise, the waiting time at the stations will increase and people will have to travel longer distances to find an available station, which will increase congestion and, therefore, the CO2 emissions of other types of motorisation.

We first summarise (see Section 2) the advantages and limitations of the two alternative propulsion modes in terms of the following criteria:

- The autonomy of the vehicle;

- Refueling time;

- The cost of use;

- The purchase cost;

- The carbon emissions;

- Safety;

- The lifetime.

In Section 3, we present an overview of the main studies on the deployment of new hydrogen transport infrastructures for several European countries. Then, in Section 4, we present the main ideas of a comparison of the costs of new distribution infrastructures made by the Julich Institute [7] for Germany, where most of the electricity surplus comes from green energy (solar cell, wind). In Section 5, we give ideas for new research directions on this topic of comparing the costs of the two alternative modes and finally, in Section 6, we give the main conclusions.

2. Advantages/Constraints of the Two Car Propulsion Modes

Table 1 shows the existing models on the European market with their type (BEV or FCEV), their selling price, their announced autonomy, as well as the full charging time on a normal domestic socket (i.e., not a fast socket).

Table 1.

Existing models on european market.

A first conclusion can be drawn directly from the hydrogen models present on the European electric vehicle market. Although eight developed countries (USA, Canada, UK, Germany, France, Italy, Korea and Japan) took part in a summit in 2009 to promote hydrogen vehicles, only the Japanese (Honda, Nissan and Toyota) have developed and commercialised fuel cell vehicles. They were followed by the Koreans from Hyundai, who also developed fuel cell technologies. In Europe, on the other hand, no commercial model has been developed with fuel cell technology. Only BMW has proposed a prototype, but it is not on the market. So, we can see that at European level, we have so far concentrated on the production of battery electric vehicles.

But this may change in the near future. When the European Commission announced its Green Deal, it announced that it wants to reduce its dependence on fossil fuels, and that hydrogen will play a key role in its future energy systems. This is part of the European Green Deal’s goal to achieve carbon neutrality in the EU by 2050. In this context, the EU Hydrogen Strategy explores the potential of renewable hydrogen to help decarbonise the EU economy in a cost-effective way and sets out a series of actions to support the production, transport and demand creation for this green hydrogen as the share of renewable energy increases. For example, the EU Hydrogen Strategy aims to install at least 6 GW of renewable hydrogen electrolysers in Europe by 2024 and 40 GW by 2030.

Let us begin the comparison of the advantages/disadvantages of the two types of electric drive by presenting two existing models on the European market as an illustration of the advantages/limitations of the two alternative drive modes (see Table 1 for a presentation of other existing models):

- Concerning the BEV, the Nissan Leaf will be offered on the European market at a price of €32,640 including taxes. The manufacturer announces an autonomy of 250 km in the standard cycle, an autonomy in real situation of 140 km. A full charge on a domestic socket takes 13 h. It is also possible to recharge up to 80% of the nominal capacity on a fast charger in 30 min.

- As for the FCEV, the Toyota Mirai will be offered on the European market at a price of €79,200 including taxes. The manufacturer claims an autonomy of 500 km. A full charge takes 3 min.

2.1. The Fuel Cel Electric Cars

Clearly, the advantages (see CNRS [8]) of hydrogen cars are, on the one hand, the charging time (3 min) and the autonomy of the car (up to 600 km), against hours for recharging a BEV at home and a lower autonomy in real traffic conditions. Refueling time and autonomy for FCEVs are, therefore, similar to those of a conventional diesel car.

The main obstacle (see CNRS [8]) for hydrogen cars is clearly the cost—€79,200 for the Toyota Mirai—while the French spend on average €25,000 for a new car. Another major disadvantage is the very limited number of hydrogen refueling stations: there are currently only 22 hydrogen refueling stations throughout France (see AFHYPAC [9]) and 40 in Germany.

Another problem is that hydrogen is currently produced from fossil fuels such as gas, a method of production that is not renewable. As pointed out by Singh et al. [10], hydrogen can be produced in several ways:

- The Steam Methane Reforming (SMR) process, in which natural gas is reacted with steam to produce hydrogen and carbon dioxide. As indicated by Singh et al. [10], about half of the world’s hydrogen supply in 2015 was produced by reforming natural gas (48%). This mode is not suitable for the development of a hydrogen economy for two reasons: reforming natural gas produces as much pollution and CO2 as burning the natural gas directly, and if this mode is used when the hydrogen economy is fully developed, the increased demand for natural gas to produce hydrogen would deplete natural gas reserves. At present, Steam Methane Reforming (SMR) is the cheapest method of producing hydrogen.

- The Partial Oxidation of Oil (POX) is the process where the hydrocarbons are subjected to partial oxidation at a temperature of 1300–1550 °C. This oil gasification process is currently the second most used method to produce hydrogen (30%).

- The Coal Gasification (CG) is the process by which coal is subjected to partial oxidation at a temperature of 1200–1350 °C to produce a mixture of Carbon Monoxide and Hydrogen. This gasification process is currently the third most used method to produce hydrogen (18%).

- The electrolysis of water is the process of splitting water molecules into hydrogen and oxygen using an electrolyzer. Electrolysis is preferred in industry where high purity hydrogen is required, but is more expensive. The great advantage of this method of production, as pointed out by Singh et al. [10], is the fact that hydrogen can be produced by electrolysis of water from electricity produced by solar photovoltaic (PV), wind power, hydroelectric power and thus electrolysis produces only pure oxygen and pure hydrogen. Electrolysis accounts for 4% of current hydrogen production.

As Shukla et al. [11] point out, one of the main advantages of hydrogen is that its only oxidation product is water vapour. In other words, it produces no carbon dioxide if it is produced by electrolysis of the water and if the electricity is produced by wind or solar cells.

What about the safety of hydrogen vehicles? According to Debray et al. [12], hydrogen diffuses in air about 4 and 12 times faster than methane and petrol vapours, respectively. Its auto-ignition temperature in air is 585 °C compared to 537 °C (for methane) and 228 to 501 °C (for petrol vapours). It has a much wider range of flammability in air: 4–75% and 13–65%, compared with 5.3–17% for methane and 1–7.6% for petrol vapours. As the ignition and detonation ranges are particularly high for hydrogen, maximum measures must be taken to prevent leaks, even in the event of a vehicle accident. This is the primary objective of manufacturers in terms of the safety of vehicles using this product. As pointed out by Claus et al. [13], the lightness of hydrogen also helps to disperse it quickly in the open air. The risks are very different in a confined environment. The presence of a roof can create an accumulation of hydrogen which may allow ignition. The most effective countermeasure against the risk of explosion is, therefore, not to install equipment or park vehicles under a roof, but in the open air.

Note also, as mentioned by Jenifer Baxter [2], that hydrogen is a potential solution for heavy goods vehicles, aircraft and shipping—all forms of transport that are currently increasing their use of oil. It should be noted that hydrogen fuel cell buses are already in use in Aberdeen, London (UK) and Dunkerque (France). As mentioned by Jenifer Baxter [2]), these buses have the advantage of producing zero GHG emissions and zero NOx emissions. As demonstrated above for cars, these buses also have a significantly better range than their electric equivalents.

2.2. The Battery Electric Vehicules

The main advantages of BEVs are the lower purchase cost of the vehicle and the wide accessibility of the electrical grid to charge the vehicles. As pointed out by Andwari et al. [14], BEVs have many advantages: they produce no emissions and can be charged overnight using low-cost electricity produced by any type of power station, including renewables.

The two main disadvantages of BEVs are the real autonomy (no more than 260 km in real traffic conditions for the main existing vehicles) and the long time to charge the battery at home (13 h as an average). As pointed out by Andwari et al. [14], electricity storage is still expensive and battery recharging is time-consuming, which explains why the range of these vehicles is limited.

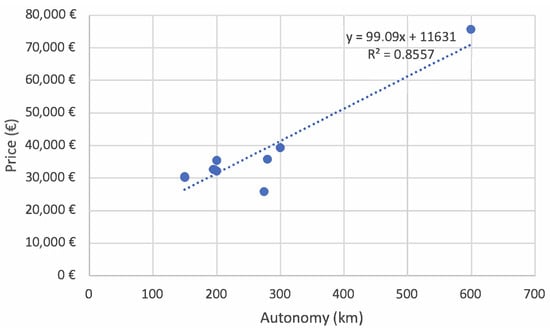

Another disadvantage of battery-powered vehicles is illustrated in Figure 2. Indeed, we see that autonomy and price are positively correlated with a coefficient of 85%. This means that if the user is looking for a high level of autonomy (that of an existing diesel car), the price of the car rises rapidly. In fact, a significant weight of additional batteries is required, which makes the vehicle more expensive to purchase (and heavier).

Figure 2.

Relationship between autonomy and vehicle price.

Note, however, that as Pearre et al. note [15], only 9% of vehicles exceed 160 km in a day. In other words, the autonomy problem only affects a minority of users, as the rest can largely charge at home at night.

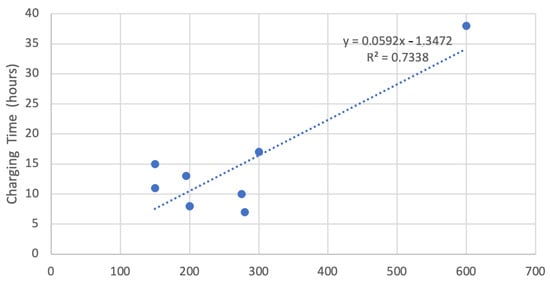

Finally, the same exercise can be carried out between autonomy and charging time, which also shows a positive correlation (see Figure 3).

Figure 3.

Relationship between autonomy and recharge time.

Regarding the social and environmental drawbacks of BEVs, Jenifer Baxter [2] cites two. First, the most commonly used battery is lithium-ion. However, the increase in materials required for battery production has environmental and human costs. Another disadvantage is the lifespan of the lithium-ion battery: only 5% of lithium-ion batteries are currently recycled.

In terms of CO2 emissions, the comparison depends on the mode of production for electricity and hydrogen. As the electricity mix varies from country to country in Europe, a comparison can only be made within a country. For example, for Germany, Robinius et al. [7] consider a high use of excess renewable electricity for hydrogen production and calculate 2.7 g of CO2 per kilometre. They consider direct use of the electricity grid to recharge the BEV and calculate 20.9 g of CO2 per kilometre (see Table 2).

Table 2.

CO2 emissions from use in Germany.

On the other hand, Bicer et al. [3] makes a comparative life cycle assessment of hydrogen and electric vehicles from well to wheel (see Table 3). The lowest GHG emissions are observed in the hydrogen vehicle, corresponding to 57 g CO2 eq/km. The highest global warming potential is obtained for the battery electric vehicle with a value of 170 g CO2 eq/km. This illustrates the fact that the construction of batteries for BEVs is a point that requires a lot of greenhouse gas production.

Table 3.

CO2 emissions for life cycle assessment.

Transport and Environment [16], calculate the life cycle emissions in grams of CO per km for BEVs for different European countries. Table 4 shows the emission reduction compared to a diesel car. This clearly illustrates the influence of the electricity generation mix by country. Indeed, a country like France, with a significant share of carbon-free electricity production, performs much better than Poland, which uses mainly coal.

Table 4.

Life cycle CO2 emissions reduction for BEV in Europe.

Consider the specific safety issues of battery electric vehicles. As noted by Sun et al. [17], current electric vehicles use lithium-ion battery technology. However, the fire risk and hazard associated with this type of high energy battery has become a major safety concern for electric vehicles. This type of battery catches fire easily and is very difficult to extinguish. For example, in 2023, the cargo ship Fremantle Highway, carrying 3000 cars, caught fire off the coast of the Netherlands due to a short circuit in the battery of an electric vehicle it was transporting. The crew were unable to extinguish the fire and all 3000 vehicles went up in smoke. Even though the results of the first statistical studies show that the heat release and hazard of an BEV fire is comparable to that of a fossil-fuelled vehicle fire, once the on-board battery is involved in a fire, it is more difficult to extinguish a BEV fire because the burning battery pack is is inaccessible to externally applied suppressants and can re-ignite without sufficient cooling.

On the other hand, lithium is relatively rare and is only found in a few specific places (Colombia, Chile, China, etc.). As a result, it is becoming increasingly expensive, so in the future, we will have to focus on other types of batteries, possibly using sodium, which is less dangerous, much cheaper and more abundant. Hasa et al. [18] announce that sodium-based batteries will take a share of the dominant position held by lithium-ion batteries in the field of energy storage. As Laurent Gauthier points out [19], the operating principle of sodium-ion batteries is similar to that of lithium-ion batteries: two electrodes, one called positive and the other negative, are made of a material whose atomic structure makes it possible to store positive ions. During charging and discharging, ions are exchanged from one electrode to the other. In lithium-ion batteries, the ion exchanged is the lithium ion Li+, while in sodium-ion batteries, it is the sodium ion Na+. The eighth World Battery and Energy Storage Industry Exhibition (WBE 2023), held from 8 to 10 August in Guangzhou, China, provided an opportunity to launch a new range of sodium-ion batteries with 5–6 times the life of lithium-ion batteries and a charge time of 20 min. The product is not yet on the market and no price has been set. This solution should be cheaper and much more widespread. It could be a solution to the lithium shortage problem.

Finally, we look at the lifespan of fuel cells compared to batteries. It should be noted that lithium batteries have a much shorter life than the fuel cell used in hydrogen vehicles. Batteries, therefore, have to be replaced, whereas the fuel cell does not degrade at the same rate. It continues to produce energy as long as the energy source is present. For example, the Department of Energy estimates that fuel cell stacks are designed to last the lifetime of the vehicle, about 200,000 m. In the US, the battery is only guaranteed for 100,000 m. This is an advantage for hydrogen vehicles, which are also much lighter than battery-powered vehicles.

Note also that recent research is being conducted on optimisation-based energy management strategies that can provide a cost-effective solution to this problem. See, for example, Hu [20], who proposes a cost-optimal, predictive energy management strategy with an explicit awareness of the degradation of both fuel cell and battery systems. This model takes into account the minimisation of hydrogen consumption and fuel cell and battery degradation. As indicated by Kandidayeni [21], the objective of an energy management strategy (EMS) is to minimise hydrogen consumption and maximise the lifetime of the system. Iqbal et al. [22] present an energy management unit (EMU) that optimises the performance of the system under different driving conditions, taking into account hydrogen consumption and the ageing of the battery and fuel cell.

3. Studies on the Development of Hydrogen Distribution Networks

Many countries in Europe expect hydrogen to be part of the solution to achieving the European target of reducing CO2 emissions in the next decade. As emphasised by Shukla et al. [11], the development of an appropriate infrastructure for convenient access to refueling stations is a prerequisite for a large-scale deployment of this new propulsion mode for private vehicles. The authors suggest investing in these new refueling structures in areas where they will have the greatest impact.

To illustrate, we will present the development of hydrogen transport infrastructures in three European countries: the Netherlands, France and Norway. The exercise can be repeated for other countries involved in hydrogen technology.

3.1. Forecast for the Development of Hydrogen Infrastructure in Norway

One of the first studies on this subject was carried out in 2010 by Stiller et al. [23]. The Norwegian project aims to model the hydrogen infrastructure in order to provide decision support for the introduction of hydrogen into the Norwegian energy system. As emphasised by Stiller et al. [23], Norway is an ideal country to introduce renewable hydrogen production, with a large proportion of electricity production from hydropower and a high potential for wind power. In addition, Norway has an extremely high level of taxation on new vehicles and can use tax exemptions to support the introduction of hydrogen vehicles to the market.

The study considers a gradual penetration of hydrogen cars on the Norwegian market, ending with a market share of 70% in 2050. The model assumes that the regional use of hydrogen in Norway will be initiated in population centres such as Olso, Stavanger, Grenland, Bergen and Trondheim. It also considers additional refueling stations along corridors connecting the equipped regions. The model then assumes that hydrogen use will gradually be generalised to the rest of the country. The model considers an increase in the number of refueling stations from 46 in 2020 to 1100 in 2050.

The main findings of the study are as follows:

- The decentralised production, especially electrolysis, will play a central role due to the sparse population in Norway. This shift towards on-site electrolysis is also achieved by considering a high CO2 taxation of €100/t CO2.

- The cost of hydrogen will be competitive with other propulsion modes from a penetration rate of 5% expected in 2025.

- From a penetration of 25%, transport by gaseous hydrogen trucks will be replaced by pipelines.

3.2. Development of a Large-Scale Hydrogen Infrastructure for the Transport Sector in the Netherlands

In 2011, Konda et al. [24] consider a multi-period optimisation model to design the spatial and temporal deployment of large-scale hydrogen infrastructure for the transport sector in the Netherlands.

The H2 demand is spatially estimated using regional population, car density and average daily distance travelled. On the supply side, Konda et al. [24] consider four production modes: Steam Methane Reforming, Coal Gasification, Biomass Gasification and Water Electrolysis. As the authors expect most of the hydrogen to be produced from hydrocarbon resources (natural gas, coal and biomass), they also consider Carbon Capture and Storage to meet the European goal of CO2 emission reduction.

For the transport of hydrogen, the authors consider the two phases: compressed H2 and liquefied H2. As the authors point out, liquefaction is an energy-intensive process, but is cheaper to transport due to its high energy density. Trucks are used to transport the liquid hydrogen or the compressed gaseous hydrogen. In the Dutch case, they do not consider the use of pipelines to transport the hydrogen. The transport capital costs include the purchase cost of the tube trailer (for liquid hydrogen) and the purchase cost of the tanker (for gaseous form). The transport operating costs include labour costs, fuel costs, maintenance costs and general costs.

The main results of the study are as follows:

- The Dutch case study shows that the transition to a large-scale H2-based transport is economically feasible for the three penetration scenarios for HFCV in the Netherlands in 2050 (pessimistic with 12% market share, base case with 25% and optimistic case with 50%).

- The achievable CO2 reduction potential is limited to 30% due to the use of hydrocarbon resources (natural gas, coal and biomass). With the use of carbon capture and storage, 85% of gas emissions can be avoided.

- It can be seen that the Rotterdam area plays a major role and that the H2 supply network is similar to the current Dutch petrol network.

Note that, unlike the Norwegian case, where the population is sparse, the Netherlands is a small and densely populated country.

3.3. Optimal Design and Time Deployment of a New Hydrogen Transmission Network for France

In 2013, André et al. [25] consider the problem of determining the optimal structure for the distribution of hydrogen to refueling stations in France. In the specific case of hydrogen, pipeline networks compete with other hydrogen carriers: compressed gas trucks and liquid cryogenic trucks. They define a local search method that simultaneously searches for the least-cost topology of the network and for the optimal diameter of each pipe. These two problems have generally been solved separately in recent years. The application to the case of the development of a new hydrogen pipeline network in France has been carried out.

Regarding the demand in France, they consider the current urban areas with more than 100,000 inhabitants (78 as in the year 2000). The demand for hydrogen has been estimated on the basis of a complete conversion of car engines from petrol to hydrogen for a horizon beyond 2050.

The main conclusions of this study are the following:

- The two stage approach generally used (which first looks for a topology of minimal length and then optimizes the diameters) is not the best one: increasing the length of the network can help to decrease the network cost by using smaller diameters.

- The network layout follows some natural corridors (Rhone’s valley, Paris-Bordeaux, French riviera, …) and looks like the natural gas network.

- The investment costs in the network are reduced by 18% with respect to the minimal spanning tree (from €2.868 to 2.347 billion) by reducing the average diameter by 30% (from 440 mm to 300 mm) and by increasing the total length by 5% (from 5035 km to 5274 km).

In 2014, André et al. [26] consider the problem of the time evolution of the new network for France. Regarding the time evolution of hydrogen demand, they consider two hydrogen penetration scenarios on the market of cars taken from HyFrance (see [27]):

- A high scenario hydrogen market share for fuels for individual cars ending with 74.5% market share;

- A low scenario for hydrogen market share ending with 20% market share.

As shown in Table 5, the percentage of cars using hydrogen and the year variables are explicitly linked for each demand scenario.

Table 5.

Two scenarios for the hydrogen penetration on the market of individual cars.

This prospective study on increasing the market share of hydrogen vehicles assumes that demand will increase gradually over the years. According to the scenario envisaged, the market share of hydrogen gradually increases from 0.1% to 74.5% of vehicles in circulation (for scenario H for high demand), while this market share increases from 0.05% to 20% in scenario L for low demand. They consider the evolution of demand between 2010 and 2050 with a time step of 5 years. The projected market shares are based on the assumptions made by the HyFRance 2 group [27].

This study shows that:

- For the medium term (before 2025) and low market share (less than 10%), trucks are the most economical options for delivering hydrogen to refueling stations.

- In the long term, the pipeline option is considered an economically viable option once the market share of hydrogen energy for car refueling reaches 10%.

Note also that the authors consider a centralised hydrogen production plant in this study.

4. A Comparison of the Costs of New Distribution Infrastructures

In 2017, Robinius et al. [7] consider the problem of designing the new infrastructure needed to supply battery and fuel cell electric vehicles in Germany. They consider a wide range of demand for these new electric vehicles: from one hundred thousand to several million electric vehicles powered by hydrogen or electricity. They assume that both technologies will use the unavoidable surplus of electricity from renewable sources (wind and solar) that will dominate German energy systems in the near future.

They carry out a comprehensive meta-analysis of existing infrastructure studies. They argue that existing studies have not been extended for high market penetration and develop a new analysis to define the design of new transmission infrastructure.

The main results of this study are as follows:

- They show that at low market penetration levels of a few hundred thousand vehicles, the costs of the two infrastructures (hydrogen refuelling stations and battery charging networks) are essentially the same.

- Hydrogen is then more expensive during the transition period to electricity generation from electrolysis and geological storage, both of which are needed to access renewable hydrogen from surplus electricity.

- If vehicle penetration increases to 20 million vehicles, a battery charging infrastructure would cost around €51 billion, making it more expensive than a hydrogen infrastructure, which would cost around €40 billion.

These results can be explained as follows. In the initial phase, with few electric cars, the most economical way to transport hydrogen (see André et al. [26]) is by road tanker, which requires modest investment. Even if the installation of a hydrogen pump is about 10 times more expensive than a fast electric charging station, given the time of use (3 min to charge a hydrogen vehicle versus 30 min for a battery electric vehicle), we need to invest 10 times less in the number of hydrogen charging stations to supply the same number of electric vehicles.

Second, if the demand for hydrogen is greater, the most economical way (see André et al. [26]) to transport the hydrogen is to build a network of gas pipelines. This involves very high fixed construction costs. This explains why, in the intermediate phase when the network is being built, this very high fixed cost leads to higher hydrogen distribution costs.

Finally, when demand is significantly higher, hydrogen becomes more advantageous as the fixed cost of building the network is amortised over a larger number of vehicles.

It should be noted that the calculations here assume that a new hydrogen transport network has to be built from scratch. However, after the energy crisis of 2022, we observed a 20% decrease in the demand for natural gas in Europe. We will continue to observe this demand with the ban on gas boilers in Europe to achieve carbon neutrality. And, therefore, transport capacity will be available. In fact, it is possible to mix hydrogen and natural gas on the same network and separate them at the outlet.

5. Future Research

As the electricity mix is very different for other countries than Germany, the same analysis as carried out for Germany by Robinus et al. [7] has to be carried out for the other countries to calculate:

- The CO2 emissions per kilometer for the two alternative powertrains: BEV and FCEV;

- The total cost of the two alternative distribution infrastructures.

Note that the cost of the hydrogen distribution infrastructure has already been calculated for France in 2014 by André et al. [26]. This study should be completed to include the cost of the deployment of refuelling stations.

More generally, the production costs of hydrogen and electricity must also be included in the research to compare the total costs (production, transport and distribution) for the two propulsion modes.

Before we come to the conclusions, let us give our personal opinion on the development of the two alternative drive systems for electric vehicles.

First of all, we believe that these two modes will have to be developed, but for different market segments. In fact, as the Belgian Federal Service for Public Transport and Mobility [28] has shown, most private car users travel an average of 35 km per day and, therefore, the current autonomy of battery-powered cars is largely sufficient. On the other hand, for certain categories of users (sales representatives, lorry drivers, coaches, taxis in particular), the need to recharge for a long time every 200 km or so is a significant disadvantage. For these categories, we believe that the hydrogen vehicle is the solution of the future.

Then, as far as distribution networks are concerned, they should follow demand. In fact, if more categories of users use hydrogen (taxis, heavy vehicles, heavy traffic, etc.), the network of hydrogen refuelling stations could be created. As mentioned in Section 4, several national gas transport companies (such as Fluxys in Belgium) are considering the transport of gas through the existing natural gas pipeline network in view of the declining use of gas.

Finally, we believe that hydrogen also has an advantage that batteries do not have. This is the ability to store in gaseous form the energy produced with the excess production of renewable energy (solar and wind). This is a great advantage of load balancing on two scenarios for the hydrogen penetration on the market of individual cars.

6. Conclusions

In the near future, electric charging and hydrogen refueling will provide practical solutions to reduce greenhouse gas emissions from transport activities. As pointed out by Singh et al. [10], the transport sector is a major contributor to global CO emissions and is a sector where the use of fossil fuels is increasing. Battery electric vehicles (BEVs) and fuel cell electric vehicles (FCEVs) have zero emissions (in use and in electricity production if the electricity comes from renewable sources).

Another important advantage of the two modes is the use of renewable energy resources, BEV when charging at night when electricity demand is lower, and hydrogen using the surplus of renewable electricity (solar photovoltaic, wind, hydro) that can be stored in gaseous form.

In fact, as Jenifer Baxter [2] points out, hydrogen can be used to absorb excess renewable electricity, using the gas grid to store this excess. Power to gas is the simple solution when there is a surplus of renewable electricity on the National Grid, in the case of high levels of production from wind turbines or solar panels, or in the case of lower demand. As Jenifer Baxter [2] points out, the excess electricity can be used to produce hydrogen by electrolysis of water. This ensures that no renewable electricity is wasted by using the existing natural gas grid to store the excess hydrogen produced by electrolysis.

A complementary combination of electric charging and hydrogen refuelling infrastructure will thus provide the key to a more sustainable transport system: the BEV will be used for short-distance travel, and hydrogen cars will meet the demand for long-distance and heavy-duty transport through the use of fuel cell electric vehicles.

For Germany, the cost comparison of the two alternatives (BEV and FCEV) shows that at low market penetration levels of a few hundred thousand vehicles, the infrastructure costs are essentially the same. Hydrogen is then more expensive during the transition period to electrolysis-based electricity generation and geological storage, both of which are needed to access renewable hydrogen from surplus electricity. As vehicle penetration increases to 20 million vehicles, a battery charging infrastructure would cost more than the hydrogen infrastructure.

The results of this study depend on the electricity mix. The study should be extended to another important European country with a different electricity mix, namely France, which has many nuclear power plants. The study should also be extended to include the total costs (production costs, transport costs and distribution costs) of the two propulsion modes.

Author Contributions

Conceptualization, D.D.W. and Y.S.; writing, review and editing, D.D.W.; validation, D.D.W. and Y.S. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding. This research was carried out during Daniel De Wolf’s stay at the Center for Operations Research and Econometrics of UClouvain in Louvain-la-Neuve, Belgium.

Acknowledgments

The authors warmly thank the two anonymous referees for the constructive suggestions which made it possible to give more substance to the paper.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Cuenot, F. Do Not Breathe Here: Tackling Air Pollution from Vehicles; Final Report; Transport & Environment: Paris, France, 2015; Available online: https://www.transportenvironment.org/discover/dont-breathe-here-tackling-air-pollution-from-vehicles/ (accessed on 1 September 2023).

- Baxter, J. Energy from Gas: Taking a Whole System Approach; Institution of Mechanical Engineers: London, UK, 2018. [Google Scholar]

- Bicer, Y.; Dincer, I. Comparative life cycle assessment of hydrogen, methanol and electric vehicles from well to wheel. Int. J. Hydrogen Energy 2017, 42, 3767–3777. [Google Scholar] [CrossRef]

- International Energy Agency. Global EV Outlook 2023, Catching up with Climate Ambitions; International Energy Agency: Paris, France, 2023. [Google Scholar]

- Saber, C.; Rouhana, N. Chargeurs de batteries de véhicule électrique. Cult. Sci. L’Ingénieur 2020, 99. Available online: https://eduscol.education.fr/sti/sites/eduscol.education.fr.sti/files/ressources/pedagogiques/12099/12099-chargeurs-de-batteries-pour-ve-ensps.pdf (accessed on 1 September 2023).

- De Wolf, D.; Kilani, M.; Diop, N. Environmental impacts of enlarging electric vehicles market share. Environ. Econ. Policy Stud. 2022, 1–20. [Google Scholar] [CrossRef]

- Robinius, M.; Linsen, J.; Grube, T.; Reus, M.; Stenzel, P.; Syranidis, K.; Kuckertz, P.; Stolten, D. Comparative Analysis of Infrastructures: Hydrogen Fueling and Electric Charging of Vehicles. Energy Environ. 2017, 408, 1–126. [Google Scholar]

- CNRS. Hydrogen Car for All? In Proceedings of the European Fuel Cell Car Workshop, Orléans, France, 1–3 March 2017; Available online: https://news.cnrs.fr/articles/hydrogen-cars-for-all (accessed on 1 September 2023).

- Association Francaise pour l’Hydrogène et les piles à Combustibles, Mobilité hydrogène en France. 2018. Available online: http://www.afhypac.org/mobilite-hydrogene-france/ (accessed on 1 September 2023).

- Singh, S.; Jain, S.; PS, V.; Tiwari, A.K.; Nouni, M.R.; Pandey, J.K.; Goel, S. Hydrogen: A sustainable fuel for future of the transport sector. Renew. Sustain. Energy Rev. 2015, 51, 623–633. [Google Scholar] [CrossRef]

- Shukla, A.; Pekny, J.; Venkatasubramanian, V. An optimization framework for cost effective design of refueling station infrastructure for alternative fuel vehicles. Comput. Chem. Eng. 2011, 35, 1431–1438. [Google Scholar] [CrossRef]

- Debray, B.; Weinberger, B. Guide Pour L’évaluation de la Conformité et la Certification des Systèmes à Hydrogène; ADEME: Angers, France, 2021; pp. 1–192. [Google Scholar]

- Clause, E.; Larrouturou, B.; Rostagnat, M.; Wallard, I. Sécurité du Développement de la Filière Hydrogène; Rapport No. 014277-01; Inspection Générale de l’Environnement et du Développement Durable: Paris, France, 2022; pp. 1–111.

- Andwari, A.M.; Pesiridis, A.; Rajoo, S.; Martinez-Botas, R.; Esfahanian, V. A review of Battery Electric Vehicle technology and readiness levels. Renew. Sustain. Energy Rev. 2017, 78, 414–430. [Google Scholar] [CrossRef]

- Pearre, N.S.; Kempton, W.; Guensler, R.L.; Elango, V.V. Electric vehicles: How much range is required for a day’s driving? Transp. Res. Part Emerg. Technol. 2011, 19, 1171–1184. [Google Scholar] [CrossRef]

- Transport and Environnement. How Clean Are Electric Cars? Transport and Environment Analysis of Electric Car Lifecycle CO2 Emissions. 2020, pp. 1–33. Available online: https://www.transportenvironment.org/wp-content/uploads/2020/04/TEs-EV-life-cycle-analysis-LCA.pdf (accessed on 1 September 2023).

- Sun, P.; Bisschop, R.; Niu, H.; Huang, X. A Review of Battery Fires in Electric Vehicles. Fire Technol. 2020, 56, 1361–1410. [Google Scholar] [CrossRef]

- Hasa, I.; Mariyappan, S.; Saurel, D.; Adelhelm, P.; Koposov, A.Y.; Masquelier, C.; Croguennec, L.; Casas-Cabanas, M. Challenges of today for Na-based batteries of the future: From materials to cell metrics. J. Power Sources 2021, 482, 228872. [Google Scholar] [CrossRef]

- Gauthier, L. La Batterie Sodium-Ion Débarque sur le Marché. Révolution Energétique 2023. Available online: https://www.revolution-energetique.com/la-batterie-sodium-ion-debarque-sur-le-marche/ (accessed on 1 September 2023).

- Hu, X.; Zou, C.; Tang, X.; Liu, T.; Hu, L. Cost-Optimal Energy Management of Hybrid Electric Vehicles Using Fuel Cell/Battery Health-Aware Predictive Control. IEEE Trans. Power Electron. 2020, 35, 382–392. [Google Scholar] [CrossRef]

- Kandidayeni, M.; Trovao, J.P.; Soleymani, M.; Boulon, L. Towards health-aware energy managementstrategies in fuel cell hybrid electric vehicles: A review. Int. J. Hydrogen Energy 2022, 47, 1021–1043. [Google Scholar] [CrossRef]

- Iqbal, M.; Laurent, J.; Benmouna, A.; Becherif, M.; Ramadan, H.S.; Claude, F. Ageing-aware load following control for composite-cost optimal energy management of fuel cell hybrid electric vehicle. Energy 2022, 254, 124233. [Google Scholar] [CrossRef]

- Stiller, C.; Bunger, U.; Moller-Holst, S.; Svensson, A.M.; Espegren, K.A.; Nowak, M. Pathways to a hydrogen fuel insfratstucture in Norway. Int. J. Hydrogen Energy 2010, 35, 2597–2601. [Google Scholar] [CrossRef]

- Konda, M.; Shah, N.; Brandon, N. Optimal transition towards a large-scale hydrogen infrastructure for the transport sector: The case for the Netherlands. Int. J. Hydrogen Energy 2011, 36, 4619–4635. [Google Scholar] [CrossRef]

- André, J.; Auray, S.; Brac, J.; De Wolf, D.; Maisonnier, G.; Ould-Sidi, M.-M. Antoine Simonnet, Design and dimensioning of hydrogen transmission pipeline networks. Eur. J. Oper. Res. 2013, 229, 239–251. [Google Scholar] [CrossRef]

- André, J.; Auray, S.; De Wolf, D.; Sidi, M.O.; Simonnet, A. Time development of new hydrogen transmission pipeline networks for France. Int. J. Hydrogen Energy 2014, 39, 10323–10337. [Google Scholar] [CrossRef]

- HyFrance 2 Project. Final Report: Evaluation Technico-Economique du Développement d’une Filitère Hydrogène en France et de ses Impacts sur le Système Énergétique, L’économie et L’environnement. 2007. Available online: http://ecolo.org/documents/documents_in_french/H2-rapport-_HyFrance_07.pdf (accessed on 1 September 2023).

- Service public fédéral Mobilité et Transports, Enquête sur la mobilité des belges. 2017. Available online: https://mobilit.belgium.be/fr/mobilite-durable/enquetes-et-resultats/enquete-monitor-sur-la-mobilite-des-belges (accessed on 1 September 2023).

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).