Economic Impacts and Land Use Change from Increasing Demand for Forest Products in the European Bioeconomy: A General Equilibrium Based Sensitivity Analysis †

Abstract

1. Introduction

1.1. Forestry in the EU Bioeconomy: Opportunities and Challenges

1.2. Economic Modelling for Bioeconomy Assessments: A General Overview

2. Materials and Methods

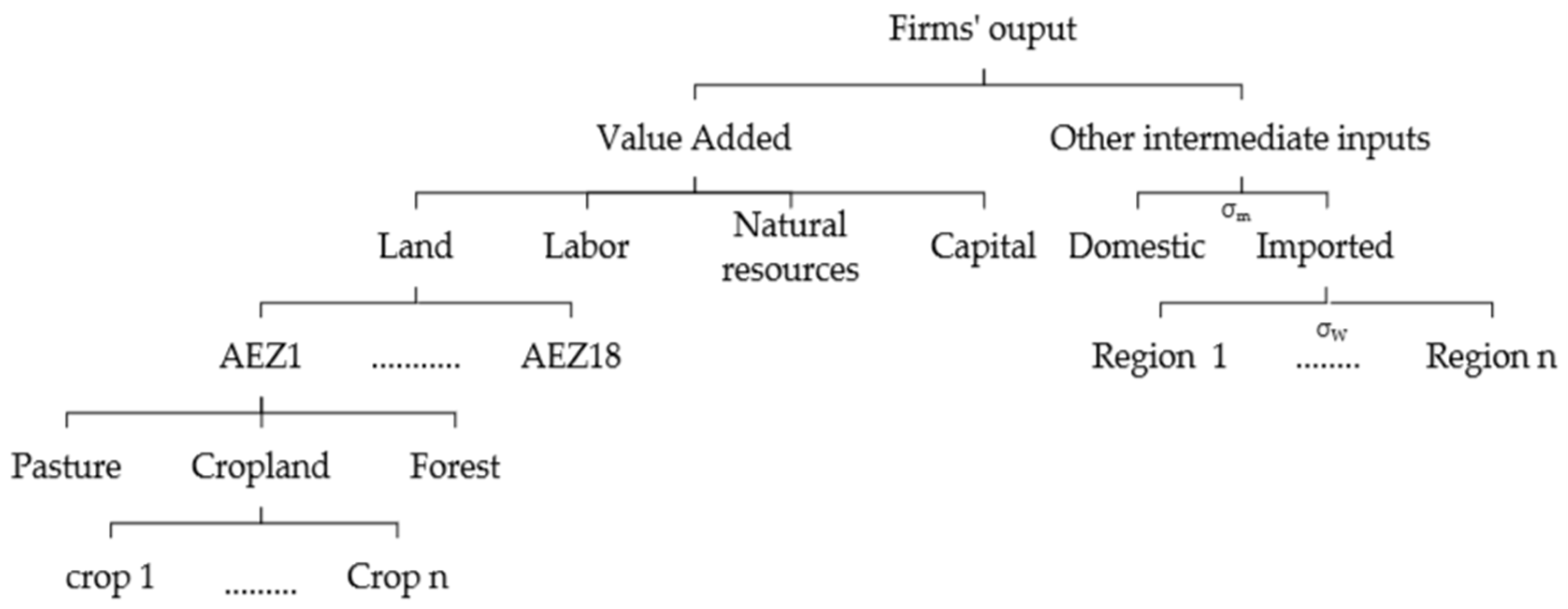

2.1. Model and Data

- -

- GTAP is a global multi-sector and multi-region comparative static Computable General Equilibrium (CGE) model [41].

- -

- Drawing on microeconomic theory of demand and supply, consumers maximize utility subject to their budget constraint while producers minimize production cost subject to a given constant returns to scale production technology [41].

- -

- The production technology is represented via nested Constant-Elasticity-of-Substitution (CES) functions that combine primary factors (labor, land, skilled labor, un-skilled labor and natural resources) and intermediate inputs [41].

- -

- GTAP adopts the Armington assumption in order to differentiate between commodities based on their region of origin [41].

- -

- It assumes perfect competition, i.e. consumer and producer are price takers, and depict a simultaneous global equilibrium in all regional commodity and factor markets based on endogenous prices [41].

- -

- A model experiment (shock) perturbs the initial equilibrium and the model is resolved for new market prices for commodities and factors and related supply and demand quantities to clear all markets [41].

- -

- -

- The globally consistent GTAP database [42] is constructed based on national accounts and other economic statistics.

- -

- It represents the world economy in a specific year including complete bilateral trade information and transport margins [42].

- -

- Its latest version 9 depicts the global economy in 2011 by 140 regions and 57 sectors of which 20 are agri-food sectors [42].

- -

2.2. Scenario Design

3. Results

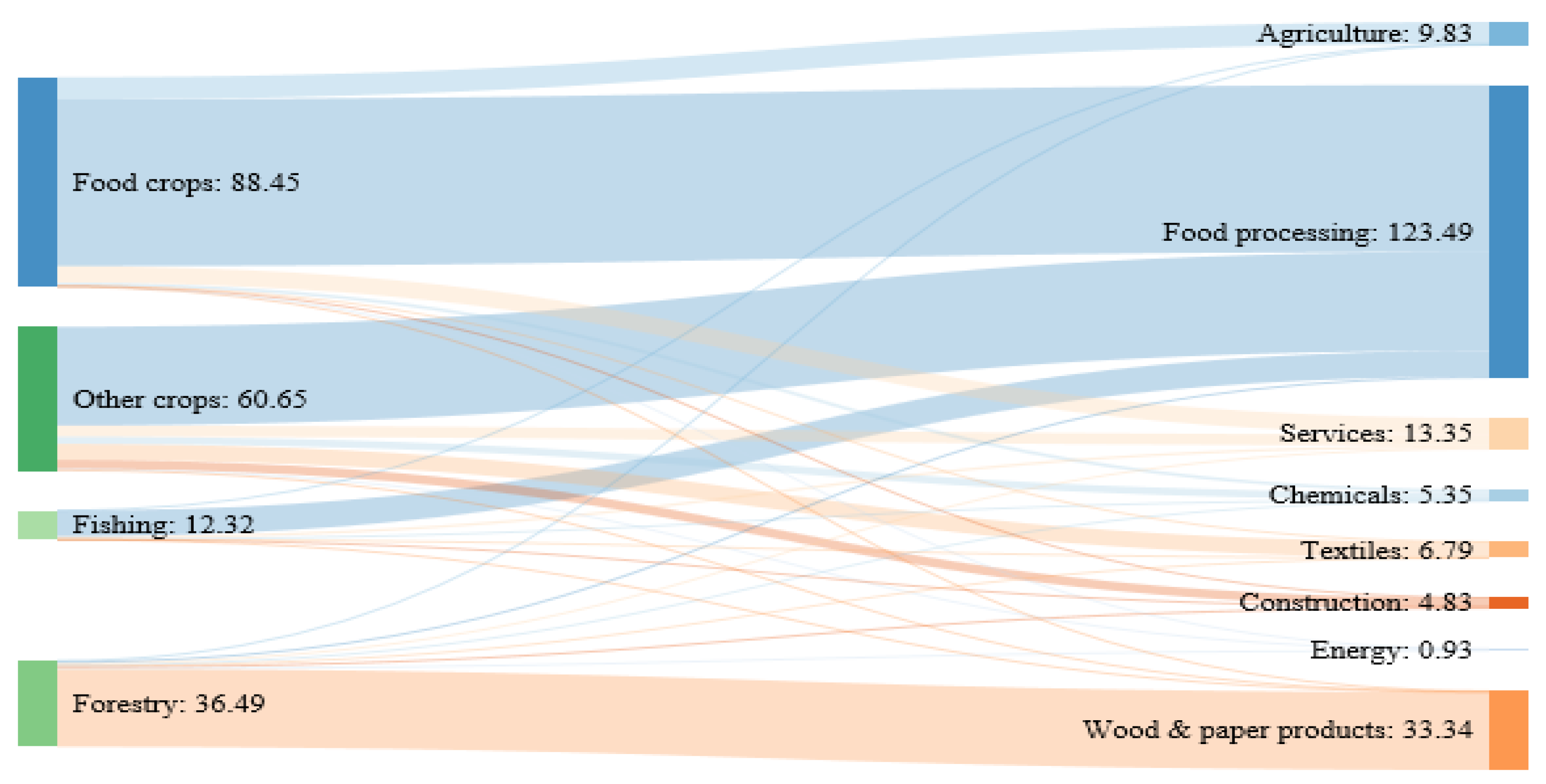

3.1. Effects on Sectoral Output and Prices

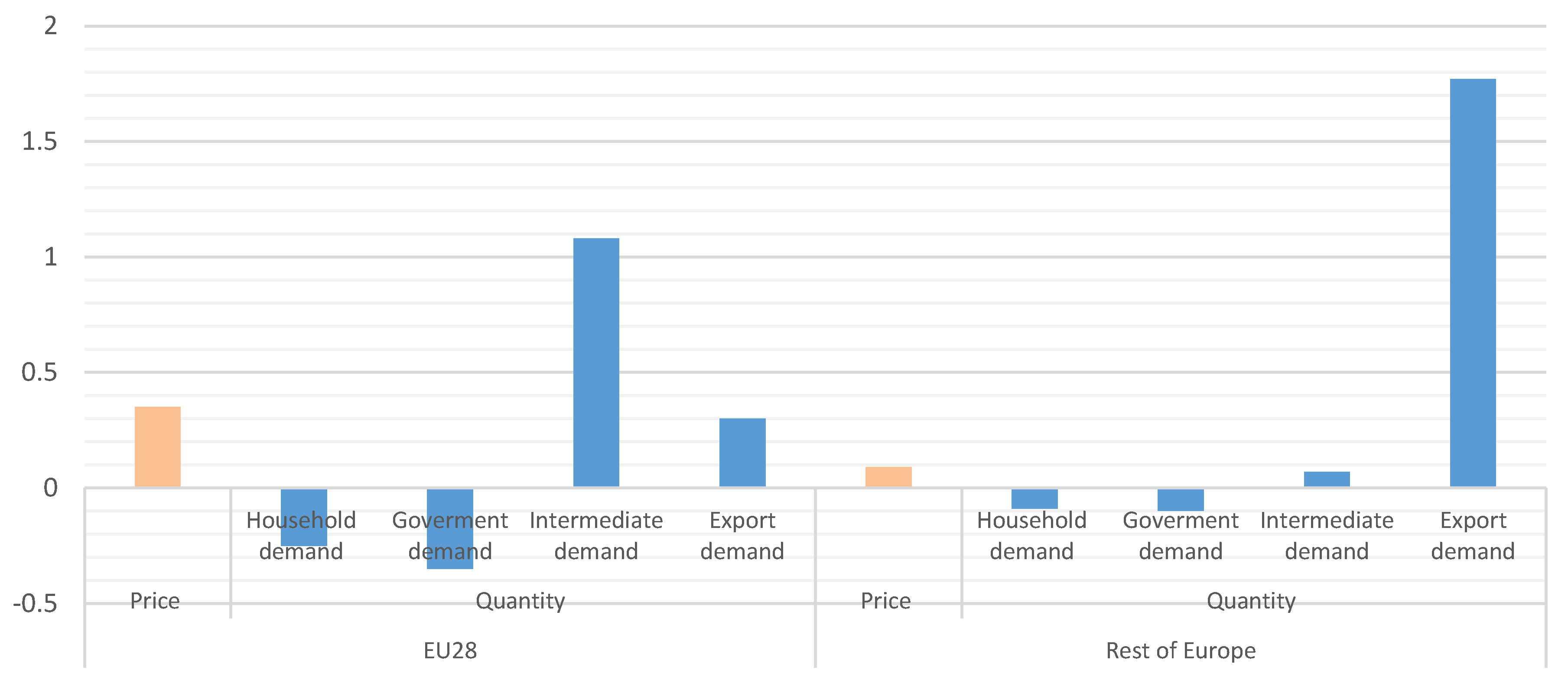

3.2. Effects on Final Demand

3.3. Effects on Trade Patterns of Forest Products

3.4. Effects on LULC Changes

3.5. Sensitivity of Results

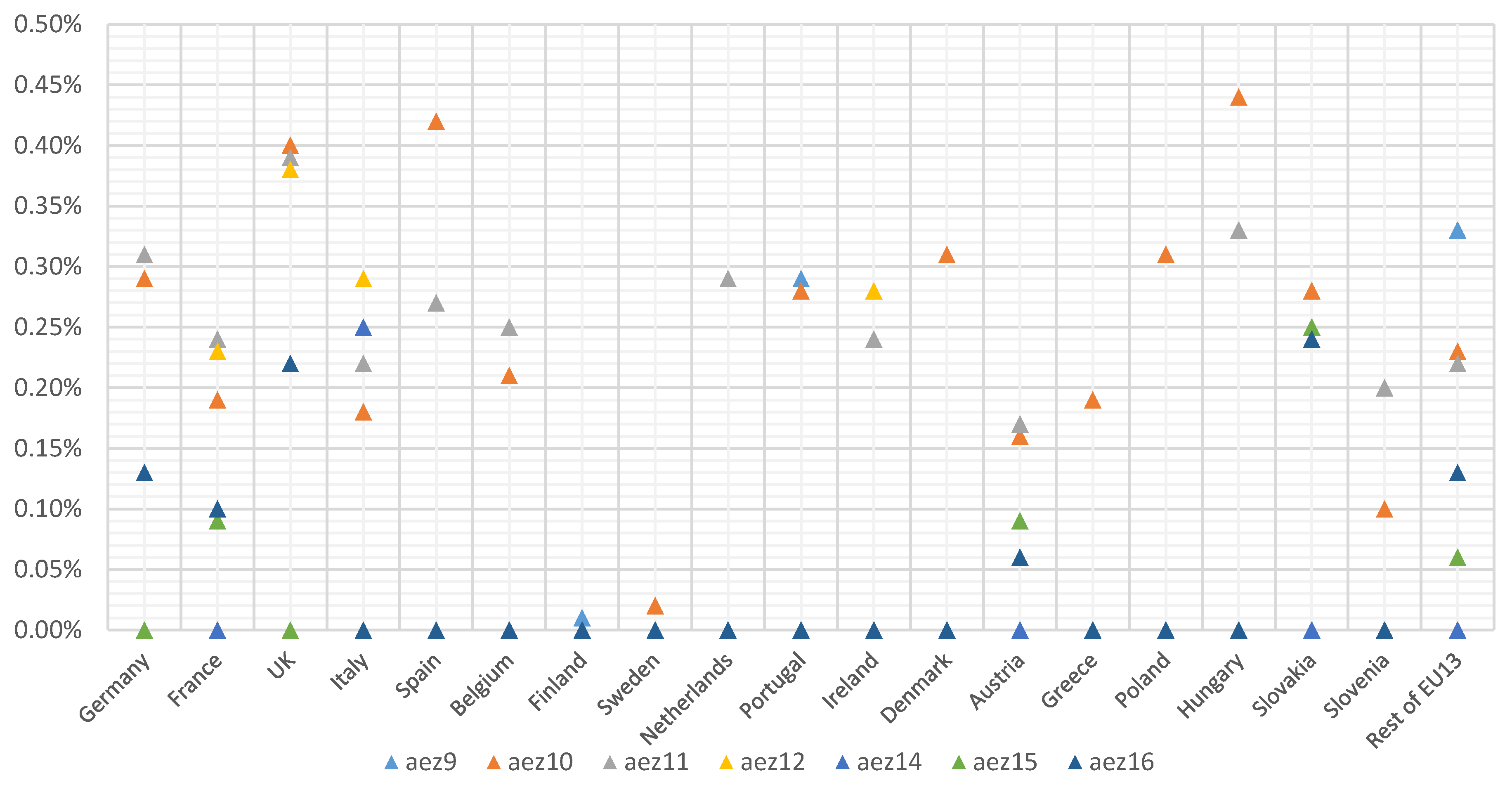

3.5.1. Structural Sensitivity Analysis: GTAP-AEZ-E-AGR Model

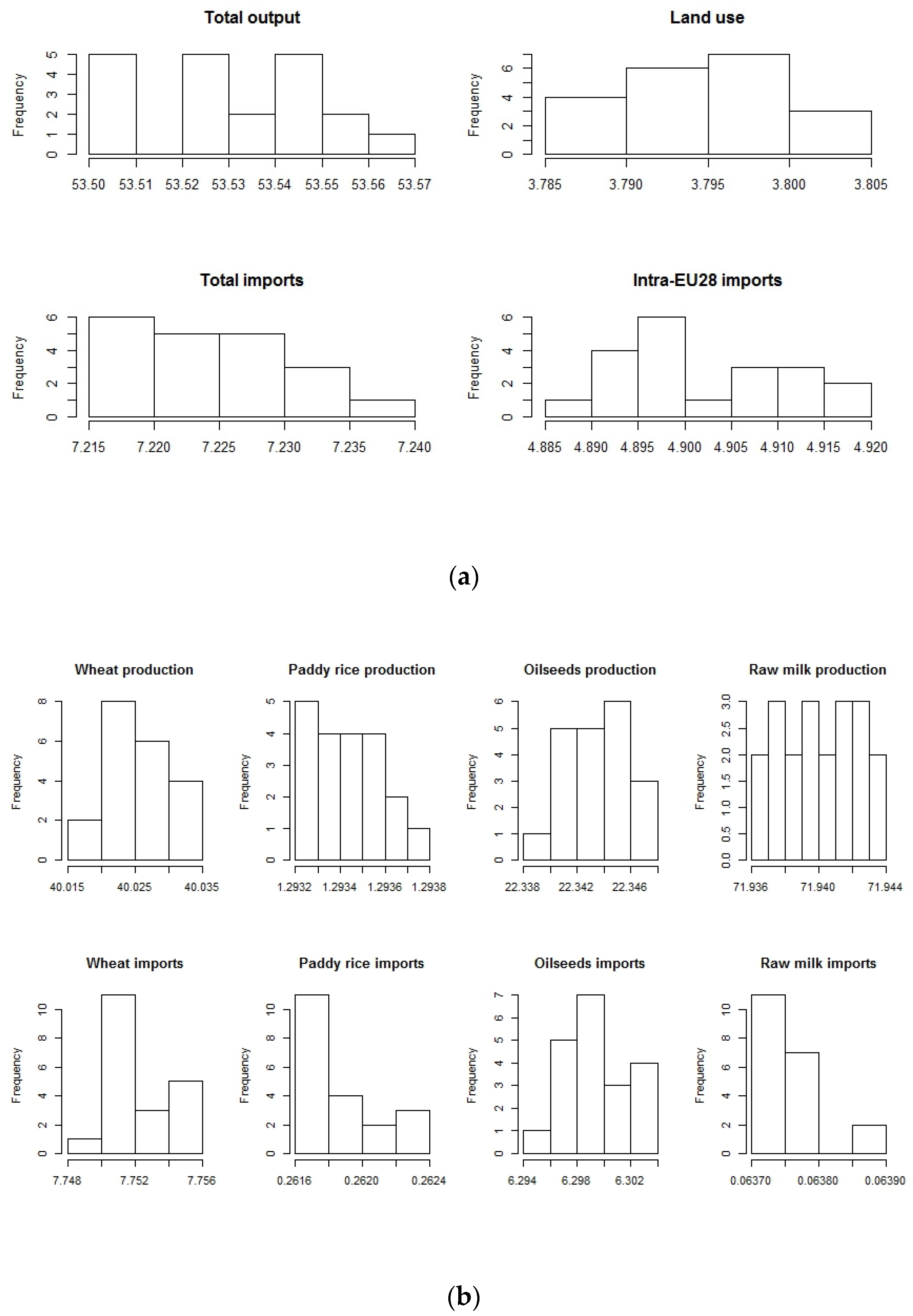

3.5.2. Systematic Sensitivity Analysis

4. Discussion

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| AEZ | Climate Type | LGP 1 in Days | Humidity Level |

|---|---|---|---|

| AEZ 1 | Tropical | 0–59 | Arid |

| AEZ 2 | 60–119 | Dry semi-arid | |

| AEZ 3 | 120–179 | Moist semi-arid | |

| AEZ 4 | 180–239 | Sub-humid | |

| AEZ 5 | 240–299 | Humid | |

| AEZ 6 | >300 days | Humid; year-round growing season | |

| AEZ 7 | Temperate | 0–59 | Arid |

| AEZ 8 | 60–119 | Dry semi-arid | |

| AEZ 9 | 120–179 | Moist semi-arid | |

| AEZ 10 | 180–239 | Sub-humid | |

| AEZ 11 | 240–299 | Humid | |

| AZE 12 | >300 days | Humid; year-round growing season | |

| AEZ 13 | Boreal | 0–59 | Arid |

| AEZ 14 | 60–119 | Dry semi-arid | |

| AEZ 15 | 120–179 | Moist semi-arid | |

| AEZ 16 | 180–239 | Sub-humid | |

| AEZ 17 | 240–299 | Humid | |

| AEZ 18 | >300 days | Humid; year-round growing season |

| GTAP Region | Description | GTAP Region | Description |

|---|---|---|---|

| Israel | Israel | Argentina | Argentina |

| Australia | Australia | Brazil | Brazil |

| New Zealand | New Zealand | Rest of Latin America | Dominican Republic, Bolivia, Chile, Colombia, Ecuador, Paraguay, Peru, Uruguay, Venezuela, Rest of South America, Costa Rica, Guatemala, Honduras, Nicaragua, Panama, El Salvador, Rest of Central America, Jamaica, Puerto Rico, Trinidad and Tobago, Carib |

| Rest of Oceania | Rest of Oceania | EU28 | Austria, Belgium, Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Ireland, Italy, Latvia, Lithuania, Luxembourg, Malta, Netherlands, Poland, Portugal, Slovakia, Slovenia, Spain, Sweden, United Kingdom, Bulgaria, Croatia, Romania |

| China | China | Rest of Europe | Switzerland, Norway, Rest of EFTA, Rest of Europe |

| Rest of East Asia | Hong Kong, Mongolia, Taiwan, Rest of East Asia | Belarus | Belarus |

| Rest of South East Asia | Brunei Darussalam, Cambodia, Lao People’s Democratic Republic, Singapore, Thailand, Viet Nam, Rest of Southeast Asia | Former Russian Federation | Albania, Russian Federation, Rest of Eastern Europe, Kazakhstan, Kyrgyzstan, Rest of Former Soviet Union, Armenia, Azerbaijan, Georgia |

| Rest of South Asia | Bangladesh, Nepal, Pakistan, Sri Lanka, Rest of South Asia | Ukraine | Ukraine |

| Japan | Japan | other Middle East | Oman, Bahrain, Jordan, Kuwait, Qatar, Saudi Arabia, United Arab Emirates |

| Korea | Korea | Islamic Republic of Iran | Islamic Republic of Iran |

| Indonesia | Indonesia | Turkey | Turkey |

| Malaysia | Malaysia | Rest of Western Asia | Rest of Western Asia |

| Philippines | Philippines | Mediterranean Africa | Egypt, Morocco, Tunisia, Rest of North Africa |

| India | India | Nigeria | Nigeria |

| Canada | Canada | South Africa | South Africa |

| USA | USA | Rest of Africa | Rest of Africa- |

| Mexico | Mexico | Rest of the World | Benin, Burkina Faso, Cameroon, Cote d’Ivoire, Ghana, Guinea, Senegal, Togo, Rest of Western Africa, Central Africa, South Central Africa, Ethiopia, Kenya, Madagascar, Malawi, Mauritius, Mozambique, Rwanda, Tanzania, Uganda, Zambia, Zimbabwe, Rest of Eastern Africa, Botswana, Namibia, Rest of South African Customs |

| Rest of North America | Rest of North America | ||

| GTAP Region | Description | GTAP Region | Description |

|---|---|---|---|

| Israel | Israel | Belgium | Belgium |

| Australia | Australia | Finland | Finland |

| New Zealand | New Zealand | Sweden | Sweden |

| Rest of Oceania | Rest of Oceania | Netherlands | Netherlands |

| China | China | Portugal | Portugal |

| Taiwan | Taiwan | Ireland | Ireland |

| Rest of East Asia | Hong Kong, Mongolia, Rest of East Asia, Brunei Darussalam | Denmark | Denmark |

| Rest of South East Asia | Cambodia, Lao People’s Democratic Republic, Singapore, Rest of Southeast Asia | Austria | Austria |

| Rest of South Asia | Nepal, Sri Lanka, Rest of South Asia | Greece | Greece |

| Thailand | Thailand | Luxembourg | Luxembourg |

| Viet Nam | Viet Nam | Poland | Poland |

| Pakistan | Pakistan | Hungary | Hungary |

| Bangladesh | Bangladesh | Slovakia | Slovakia |

| Japan | Japan | Slovenia | Slovenia |

| Korea | Korea | Rest of EU 13 | Cyprus, Czech Republic, Estonia, Latvia, Lithuania, Malta, Bulgaria, Croatia, Romania |

| Indonesia | Indonesia | Rest of Europe | Switzerland, Norway, Rest of EFTA, Rest of Europe |

| Malaysia | Malaysia | Belarus | Belarus |

| Philippines | Philippines | Former Russia | Albania, Russian Federation, Rest of Eastern Europe, Kazakhstan, Kyrgyzstan, Rest of Former Soviet Union, Armenia, Azerbaijan, Georgia |

| India | India | Ukraine | Ukraine |

| Canada | Canada | Gulf | Oman, Bahrain, Jordan, Kuwait, Qatar, United Arab Emirates |

| USA | USA | Saudi Arabia | Saudi Arabia |

| Mexico | Mexico | Islamic Republic of Iran | Islamic Republic of Iran |

| Rest of North America | Rest of North America | Turkey | Turkey |

| Argentina | Argentina | Rest of Western Asia | Rest of Western Asia |

| Venezuela | Venezuela | Egypt | Egypt |

| Peru | Peru | Morocco | Morocco |

| Colombia | Colombia | Other Mediterranean Africa | Tunisia, Rest of North Africa |

| Brazil | Brazil | Tanzania | Tanzania |

| Chile | Chile | Uganda | Uganda |

| Rest of Latin America | Dominican Republic, Bolivia, Ecuador, Paraguay, Uruguay, Rest of South America, Costa Rica, Guatemala, Honduras, Nicaragua, Panama, El Salvador, Rest of Central America, Jamaica, Puerto Rico, Trinidad and Tobago, Caribbean | Ethiopia | Ethiopia |

| Germany | Germany | Kenia | Kenia |

| France | France | Nigeria | Nigeria |

| UK | UK | South Africa | South Africa |

| Italy | Italy | Rest of Africa | Benin, Burkina Faso, Cameroon, Cote d’Ivoire, Ghana, Guinea, Senegal, Togo, Rest of Western Africa, Central Africa, South Central Africa, Madagascar, Malawi, Mauritius, Mozambique, Rwanda, Zambia, Zimbabwe, Rest of Eastern Africa, Botswana, Namibia, Rest of South African Customs |

| Spain | Spain | Rest of the World | Rest of the World |

Appendix B

| Forest | Paddy Rice | Wheat | Cereal Grains nec 1 | Vegetables, Fruit, Nuts | Oil Seeds | Sugar Crops | Plant-Based Fibers | Crops nec | Animal Products nec | Raw Milk | Meat | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Germany | 0.83 | −0.04 | −0.05 | −0.03 | −0.06 | −0.07 | −0.02 | −0.05 | −0.07 | −0.05 | −0.04 | −0.02 |

| France | 0.64 | −0.06 | −0.01 | 0.01 | −0.02 | −0.03 | −0.00 | −0.06 | −0.02 | −0.00 | −0.00 | 0.00 |

| UK | 0.80 | 0.00 | 0.01 | 0.00 | −0.01 | −0.01 | −0.00 | −0.06 | 0.01 | −0.01 | −0.00 | −0.02 |

| Italy | 0.78 | −0.10 | −0.09 | −0.02 | −0.07 | −0.06 | −0.00 | −0.00 | −0.06 | −0.01 | −0.01 | −0.01 |

| Spain | 0.87 | −0.02 | 0.01 | 0.00 | 0.01 | −0.01 | −0.00 | −0.04 | −0.00 | 0.00 | 0.00 | −0.00 |

| Belgium | 0.74 | 0.12 | −0.01 | 0.00 | −0.04 | −0.06 | −0.00 | −0.09 | −0.04 | 0.02 | 0.01 | 0.00 |

| Finland | 0.06 | 0.04 | 0.08 | 0.03 | 0.01 | 0.04 | 0.01 | −0.01 | 0.02 | 0.02 | 0.00 | 0.00 |

| Sweden | 0.11 | 0.05 | 0.06 | 0.02 | 0.03 | 0.02 | 0.00 | −0.00 | 0.01 | 0.01 | 0.00 | 0.01 |

| Netherlands | 0.77 | −0.00 | 0.00 | −0.00 | −0.02 | −0.05 | −0.01 | −0.05 | −0.02 | −0.00 | −0.02 | −0.03 |

| Portugal | 0.68 | −0.01 | 0.03 | 0.01 | 0.01 | 0.00 | 0.02 | −0.00 | 0.01 | 0.01 | 0.00 | 0.00 |

| Ireland | 0.75 | −0.03 | −0.04 | −0.02 | −0.04 | −0.09 | −0.01 | −0.02 | −0.01 | −0.02 | −0.04 | −0.03 |

| Denmark | 0.74 | −0.01 | 0.02 | −0.00 | −0.01 | −0.02 | 0.00 | −0.05 | −0.01 | −0.01 | −0.01 | 0.00 |

| Austria | 0.54 | 0.06 | −0.03 | 0.02 | −0.01 | −0.03 | 0.03 | −0.08 | −0.00 | −0.03 | −0.01 | −0.01 |

| Greece | 0.57 | −0.02 | 0.02 | −0.00 | −0.01 | −0.01 | 0.00 | −0.08 | 0.01 | −0.02 | −0.01 | −0.03 |

| Luxembourg | 1.05 | 0.09 | 0.05 | 0.03 | 0.04 | 0.06 | −0.05 | 0.01 | 0.06 | 0.05 | 0.04 | 0.00 |

| Poland | 0.87 | −0.12 | −0.10 | −0.06 | −0.08 | −0.11 | −0.02 | −0.18 | −0.15 | −0.10 | −0.03 | −0.04 |

| Hungary | 0.90 | −0.07 | −0.05 | −0.03 | 0.02 | −0.07 | 0.01 | −0.12 | −0.06 | −0.02 | −0.01 | −0.05 |

| Slovakia | 0.87 | −0.10 | −0.13 | −0.11 | −0.14 | −0.15 | −0.02 | −0.22 | −0.17 | −0.07 | −0.03 | −0.02 |

| Slovenia | 0.73 | −0.12 | −0.26 | −0.18 | −0.25 | −0.37 | −0.02 | −0.19 | −0.28 | −0.11 | −0.04 | −0.01 |

| Rest of EU 13 | 0.72 | −0.13 | −0.14 | −0.08 | −0.09 | −0.08 | −0.03 | −0.09 | −0.09 | −0.06 | −0.04 | −0.01 |

Appendix C

| σm | σw | |

|---|---|---|

| Forestry | 2.5 | 5 |

| Wheat | 4.45 | 8.90 |

| Sugar | 2.70 | 5.40 |

| Oil seeds | 2.45 | 4.90 |

| Paddy rice | 5.05 | 10.10 |

| Animal products nec | 1.30 | 2.60 |

| Vegetables, fruit, nuts | 1.85 | 3.70 |

References

- Dietz, T.; Börner, J.; Förster, J.; von Braun, J. Governance of the bioeconomy: A global comparative study of national bioeconomy strategies. Sustainability 2018, 10, 3190. [Google Scholar] [CrossRef]

- De Besi, M.; McCormick, K. Towards a Bioeconomy in Europe: National, Regional and Industrial Strategies. Sustainability 2015, 7, 10461–10478. [Google Scholar] [CrossRef]

- Staffas, L.; Gustavsson, M.; McCormick, K. Strategies and policies for the bioeconomy and bio-based economy: An analysis of official national approaches. Sustainability 2013, 5, 2751–2769. [Google Scholar] [CrossRef]

- McCormick, K.; Kautto, N. The Bioeconomy in Europe: An Overview. Sustainability 2013, 5, 2589–2608. [Google Scholar] [CrossRef]

- Wield, D. Bioeconomy and the global economy: Industrial policies and bio-innovation. Technol. Anal. Strateg. Manag. 2013, 25, 1209–1221. [Google Scholar] [CrossRef]

- Philippidis, G.; M’barek, R.; Ferrari, E. Drivers of the Bioeconomy in Europe towards 2030: Short Overview of an Exploratory, Model-Based Assessment; European Commission, JRC-IPTS: Seville, Spain, 2015. [Google Scholar]

- European Commission. Life Sciences and Biotechnology: A Strategy for Europe; European Commission: Seville, Spain, 2002. [Google Scholar]

- European Commission. Taking Sustainable Use of Resources Forward: A Thematic Strategy on the Prevention and Recycling of Waste; European Commission: Seville, Spain, 2005. [Google Scholar]

- European Commission. Directive 2009/28/EC on the Promotion of the Use of Energy from Renewable Sources and Amending and Subsequently Repealing Directives 2001/77/EC and 2003/30/EC; European Commission: Seville, Spain, 2009. [Google Scholar]

- European Commission. A Sustainable Bioeconomy for Europe: Strengthening the Connection between Economy, Society and the Environment—Updated Bioeconomy Strategy; European Commission: Seville, Spain, 2018. [Google Scholar]

- Scarlat, N.; Dallemand, J.-F.; Monforti-Ferrario, F.; Nita, V. The role of biomass and bioenergy in a future bioeconomy: Policies and facts. Environ. Dev. 2015, 15, 3–34. [Google Scholar] [CrossRef]

- SAT-BBE. Design of a Systems Analysis Tools Framework for a EU Bioeconomy Strategy; Wageningen University & Research: The Hague, The Netherlands, 2015. [Google Scholar]

- European Commission. Outcome Report on the 2017 Bioeconomy Policy Day; European Commission: Seville, Spain, 2018. [Google Scholar]

- European Commission. A New EU Forest Strategy: For Forests and the Forest-Based Sector; COM (2013) 659 Final; European Commission: Seville, Spain, 2013. [Google Scholar]

- Hetemäki, L.; Hanewinkel, M.; Muys, B.; Aho, E. Leading the Way to a European Circular Bioeconomy Strategy; European Forest Institute: Joensuu, Finland, 2017. [Google Scholar]

- Ollikainen, M. Forestry in bioeconomy—Smart green growth for the humankind. Scand. J. For. Res. 2014, 29, 360–366. [Google Scholar] [CrossRef]

- Hetemäki, L. Future of the European Forest-Based Sector. Structural Changes towards Bioeconomy; European Forest Institute: Joensuu, Finland, 2014. [Google Scholar]

- EUSTAFOR. European State Forests Boost the Bioeconomy; Eustafor: Brussels, Belgium, 2017. [Google Scholar]

- van Leeuwen, M.G.A.; van Meijl, J.C.M.; Smeets, E.M.W. Toolkit for a Systems Analysis Framework of the EU: Overview of WP2 in the EU FP 7 SAT-BBE Project: Systems Analysis Tools Framework for the EU Bio-Based Economy Strategy. Available online: http://edepot.wur.nl/318439 (accessed on 23 January 2017).

- Philippidis, G.; M’barek, R.; Ferrari, E. Is ‘Bio-Based’ Activity a Panacea for Sustainable Competitive Growth? Energies 2016, 9, 806. [Google Scholar] [CrossRef]

- European Commission. Forest-Based Industries—Growth—European Commission. Available online: https://ec.europa.eu/growth/sectors/raw-materials/industries/forest-based_en (accessed on 15 October 2018).

- Forti, R. Agriculture, Forestry and Fishery Statistics; Eurostat: Luxembourg, 2017. [Google Scholar]

- Hetemäki, L.; Hurmekoski, E. Forest Products Markets under Change: Review and Research Implications. Curr. For. Rep. 2016, 2, 177–188. [Google Scholar] [CrossRef]

- Wolfslehner, B.; Linser, S.; Pülzl, H. Forest Bioeconomy. A New Scope for Sustainability Indicators; EFI: Joensuu, Spain, 2016. [Google Scholar]

- Sikkema, R.; Dallemand, J.F.; Matos, C.T.; van der Velde, M.; San-Miguel-Ayanz, J. How can the ambitious goals for the EU’s future bioeconomy be supported by sustainable and efficient wood sourcing practices? Scand. J. For. Res. 2017, 32, 551–558. [Google Scholar] [CrossRef]

- Hodge, D.; Brukas, V.; Giurca, A. Forests in a bioeconomy: Bridge, boundary or divide? Scand. J. For. Res. 2017, 32, 582–587. [Google Scholar] [CrossRef]

- Mantau, U.; Saal, U.; Prins, K.; Steierer, F.; Lindner, M.; Yerkerk, H.; Eggers, J.; Leek, N.; Oldenburger, J.; Asikainen, A.; et al. EU Wood: Real Potential for Changes in Growth and Use of EU Forests; Final Report; European Union: Brussels, Belgium, 2010. [Google Scholar]

- Angenendt, E.; Poganietz, W.-R.; Bos, U.; Wagner, S.; Schippl, J. Modelling and Tools Supporting the Transition to a Bioeconomy. In Bioeconomy: Shaping the Transition to a Sustainable, Biobased Economy; Lewandowski, I., Ed.; Springer: Cham, Switzerland, 2018; pp. 289–316. [Google Scholar]

- Wicke, B.; van der Hilst, F.; Daioglou, V.; Banse, M.; Beringer, T.; Gerssen-Gondelach, S.; Heijnen, S.; Karssenberg, D.; Laborde, D.; Lippe, M.; et al. Model collaboration for the improved assessment of biomass supply, demand, and impacts. GCB Bioenergy 2015, 7, 422–437. [Google Scholar] [CrossRef]

- Burfisher, M.E. Introduction to Computable General Equilibrium Models. Available online: https://www.cambridge.org/core/books/introduction-to-computable-general-equilibrium-models/8CE618F19C97979CFC20B3038F2B28F0 (accessed on 15 October 2016).

- Krey, V.; Havlik, P.; Fricko, O.; Zilliacus, J.; Gidden, M.; Strubegger, M.; Kartasasmita, I.; Ermolieva, T.; Forsell, N.; Gusti, M. Message-Globiom 1.0 Documentation; International Institute for Applied Systems Analysis: Laxenburg, Austria, 2016. [Google Scholar]

- Banse, M.; van Meijl, H.; Tabeau, A.; Woltjer, G.; Hellmann, F.; Verburg, P.H. Impact of EU biofuel policies on world agricultural production and land use. Biomass Bioenergy 2011, 35, 2385–2390. [Google Scholar] [CrossRef]

- Smeets, E.; Tabeau, A.; van Berkum, S.; Moorad, J.; van Meijl, H.; Woltjer, G. The impact of the rebound effect of the use of first generation biofuels in the EU on greenhouse gas emissions: A critical review. Renew. Sustain. Energy Rev. 2014, 38, 393–403. [Google Scholar] [CrossRef]

- Laborde, D. Assessing the Land Use Change Consequences of European Biofuel Policies and Its Uncertainties; Final Report; Prepared by the International Food Policy Institute (IFPRI) for the European Commission: Washington, DC, USA, 2011. [Google Scholar]

- Britz, W.; Delzeit, R. The impact of German biogas production on European and global agricultural markets, land use and the environment. Energy Policy 2013, 62, 1268–1275. [Google Scholar] [CrossRef]

- Rosegrant, M.W.; Zhu, T.; Msangi, S.; Sulser, T. Global Scenarios for Biofuels: Impacts and Implications. Available online: https://academic.oup.com/aepp/article/30/3/495/8084 (accessed on 22 January 2017).

- Havlík, P.; Schneider, U.A.; Schmid, E.; Böttcher, H.; Fritz, S.; Skalský, R.; Aoki, K.; Cara, S.D.; Kindermann, G.; Kraxner, F.; et al. Global land-use implications of first and second generation biofuel targets. Energy Policy 2011, 39, 5690–5702. [Google Scholar] [CrossRef]

- Wetterlund, E.; Leduc, S.; Dotzauer, E.; Kindermann, G. Optimal use of forest residues in Europe under different policies—Second generation biofuels versus combined heat and power. Biomass Convers. Bioref. 2013, 3, 3–16. [Google Scholar] [CrossRef]

- Rudi, A.; Müller, A.-K.; Fröhling, M.; Schultmann, F. Biomass Value Chain Design: A Case Study of the Upper Rhine Region. Waste Biomass Valor 2017, 8, 2313–2327. [Google Scholar] [CrossRef]

- Raumer, H.-G.S.V.; Angenendt, E.; Billen, N.; Jooß, R. Economic and ecological impacts of bioenergy crop production—A modeling approach applied in Southwestern Germany. AIMS Agric. Food 2017, 2, 75–100. [Google Scholar] [CrossRef]

- Hertel, T.W. Global Trade Analysis: Modeling and Applications; Purdue University: West Lafayette, IN, USA, 1997. [Google Scholar]

- Aguiar, A.; Narayanan, B.; McDougall, R. An Overview of the GTAP 9 Data Base. J. Glob. Econ. Anal. 2016, 1, 181–208. [Google Scholar] [CrossRef]

- Britz, W. CGEBox: A Flexible and Modular Toolkit for CGE Modelling with a GUI; University of Bonn: Bonn, Germany, 2018. [Google Scholar]

- Britz, W.; van der Mensbrugghe, D. CGEBox: A flexible, modular and extendable framework for CGE analysis in GAMS. J. Glob. Econ. Anal. 2018, 3, 106–177. [Google Scholar] [CrossRef]

- Darwin, R.; Tsigas, M.; Lewandrowski, J.; Raneses, A. World Agriculture and Climate Change Economic Adaptations; Agrcultural Economic Report No. 703; Natural Resource and Environment Division, Economic Research Service, US Department of Agriculture: Washington, DC, USA, 1995.

- Lee, H.-L.; Hertel, T.; Sohngen, B.; and Ramankutty, N. Towards an Integrated Land Use Data Base for Assessing the Potential for Greenhouse Gas Mitigation; Purdue University: West Lafayette, IN, USA, 2005. [Google Scholar]

- Keeney, R.; Hertel, T. GTAP-AGR: A Framework for Assessing the Implications of Multilateral Changes in Agricultural Policies; GTAP Technical Papers. Paper 25; Purdue University: West Lafayette, IN, USA, 2005. [Google Scholar]

- Burniaux, J.-M.; Truong, T.P. GTAP-E: An Energy-Environmental Version of the GTAP Model; GTAP Technical Paper No. 16; Purdue University: West Lafayette, IN, USA, 2002. [Google Scholar]

- Rose, S.K.; Lee, H.-L. Non-CO2 Greenhouse Gas Emissions Data for Climate Change Economic Analysis; GTAP Working Paper No. 43; Purdue University: West Lafayette, IN, USA, 2008. [Google Scholar]

- Gibbs, H.; Yui, S.; Plevin, R. New Estimates of Soil and Biomass Carbon Stocks for Global Economic Models; GTAP Technical Paper No. 33; Purdue University: West Lafayette, IN, USA, 2014. [Google Scholar]

- Britz, W.; van der Mensbrugghe, D. Reducing unwanted consequences of aggregation in large-scale economic models—A systematic empirical evaluation with the GTAP model. Econ. Model. 2016, 59, 463–472. [Google Scholar] [CrossRef]

- European Commission. Forest Law Enforcement, Governance and Trade (Flegt).com; 251 Final: Proposal for an EU Action Plan; European Commission: Seville, Spain, 2003. [Google Scholar]

- Plevin, R.J.; Gibbs, H.K.; Duffy, J.; Yui, S.; Yeh, S. Agro-Ecological Zone Emission Factor (AEZ-EF) Model; California Air Resources Board: Sacramento, CA, USA, 2014. [Google Scholar]

- Schürenberg-Frosch, H. We Could Not Care Less About Armington Elasticities But Should We?: A Meta-Sensitivity Analysis of the Influence of Armington Elasticity Misspecification On Simulation Results. SSRN J. 2015. [Google Scholar] [CrossRef]

- Britz, W.; Hertel, T.W. Impacts of EU biofuels directives on global markets and EU environmental quality: An integrated PE, global CGE analysis. Agric. Ecosyst. Environ. 2011, 142, 102–109. [Google Scholar] [CrossRef]

- Domínguez, I.P.; Fellmann, T.; Weiss, F.; Witzke, P.; Barreiro-Hurlé, J.; Himics, M.; Jansson, T.; Salputra, G.; Leip, A. An Economic Assessment of GHG Mitigation Policy Options for EU Agriculture: (EcAMPA 2); JRC Science for Policy Report, EUR 27973 EN, 10.2791/843461; European Commission: Seville, Spain, 2016. [Google Scholar]

- Hildebrandt, J.; Hagemann, N.; Thrän, D. The contribution of wood-based construction materials for leveraging a low carbon building sector in Europe. Sustain. Cities Soc. 2017, 34, 405–418. [Google Scholar] [CrossRef]

- Golub, A.; Hertel, T.W.; Brent, S. Land Use Modeling in Recursively-Dynamic GTAP Framework; GTAP Working Paper No. 48; Purdue University: West Lafayette, IN, USA, 2008. [Google Scholar]

- European Commission. Deforestation: Forests and the Planet’s Biodiversity Are Disappearing. Available online: http://ec.europa.eu/environment/forests/deforestation.htm (accessed on 15 November 2018).

| Models | Literature | Purpose | Spatial Coverage |

|---|---|---|---|

| CGE 1 Models | |||

| GTAP | [32] | Assess the impacts of increased demand for biofuel crops under the EU biofuel directive | Global |

| MAGNE | [33] | Analyze the rebound effect of biofuel use in the context of the EU RED 2 | Global |

| MIRAG | [34] | Assess the implications of the EU biofuel policies on LUC 3 | Global |

| PE 4 Models | |||

| CAPRI | [35] | Address the impact of the German biogas production on European and global agricultural markets and land use | Global with focus on EU |

| IMPACT | [36] | Analyze the effects of increasing demand for biofuels on global food prices | Global |

| GLOBIOM | [37] | Determine the impacts of first- and second-generation biofuels on deforestation | Global |

| Bottom-up Models | |||

| BeWhere | [38] | Determine the optimal use of forest residues for different applications under different economic policy instruments | EU |

| BiOLoCaTe | [39] | Assess a biomass value chain for bioenergy | Farm/regional |

| EFEM | [40] | Analyze the economic and ecological impacts of bioenergy crop production | Farm/regional |

| Sectors | World | EU28 | Rest of Europe | USA | Former Russia | Brazil | Malaysia | Indonesia |

|---|---|---|---|---|---|---|---|---|

| Forestry | 0.182 | 0.820 | 0.210 | 0.033 | 0.068 | 0.010 | 0.036 | 0.018 |

| Paddy rice | −0.001 | −0.103 | −0.052 | 0.006 | −0.001 | 0.003 | −0.004 | −0.001 |

| Wheat | −0.001 | −0.065 | −0.041 | 0.023 | 0.019 | 0.030 | 0.066 | - |

| Cereal grains | −0.002 | −0.030 | −0.030 | 0.003 | 0.006 | 0.006 | −0.008 | −0.001 |

| Oil seeds | −0.002 | −0.074 | −0.042 | 0.001 | 0.008 | 0.011 | −0.006 | 0.002 |

| Plant-based fibers | −0.003 | −0.103 | −0.046 | 0.007 | −0.003 | −0.004 | −0.010 | −0.003 |

| Sugar crops | −0.001 | −0.008 | −0.031 | - | −0.002 | −0.002 | −0.010 | −0.001 |

| Raw milk | −0.001 | −0.017 | −0.011 | 0.001 | −0.003 | - | 0.001 | 0.001 |

| Animal products nec 1 | −0.003 | −0.027 | −0.021 | 0.005 | - | 0.005 | −0.002 | - |

| Member States | Price 1 | Quantity | |||

|---|---|---|---|---|---|

| Household Demand | Government Demand | Intermediate Demand | Export Demand | ||

| Germany | 0.39 | −0.33 | −0.42 | 1.16 | −0.13 |

| France | 0.38 | −0.31 | −0.39 | 1.05 | −0.5 |

| UK | 0.2 | −0.16 | −0.21 | 1.06 | 0.2 |

| Italy | 0.22 | −0.18 | −0.22 | 1.03 | 0.66 |

| Spain | 0.19 | −0.14 | −0.19 | 0.97 | 0.6 |

| Belgium | 0.21 | −0.19 | −0.2 | 1.01 | 0.59 |

| Finland | 0.04 | −0.03 | −0.03 | 0.02 | 0.74 |

| Sweden | 0.06 | −0.06 | −0.05 | 0.02 | 1.01 |

| Netherlands | 0.15 | −0.11 | −0.19 | 1.02 | 0.84 |

| Portugal | 0.16 | −0.11 | −0.17 | 0.71 | 0.82 |

| Ireland | 0.27 | −0.24 | −0.3 | 1.08 | 0.25 |

| Denmark | 0.23 | −0.21 | −0.23 | 1.21 | 0.79 |

| Austria | 0.5 | −0.44 | −0.57 | 1.01 | −0.63 |

| Greece | 0.15 | −0.11 | −0.15 | 1 | 0.46 |

| Luxembourg | 0.24 | −0.24 | −0.23 | 0.89 | 1.24 |

| Poland | 0.39 | −0.23 | −0.4 | 1.15 | 0.34 |

| Hungary | 0.27 | −0.16 | −0.27 | 1.15 | 1.08 |

| Slovakia | 0.39 | −0.25 | −0.39 | 1.08 | 0.52 |

| Slovenia | 0.26 | −0.18 | −0.26 | 1.12 | 1.13 |

| Rest of EU 13 | 0.32 | −0.19 | −0.32 | 0.98 | 0.12 |

| Imports by Country of Origin | Exports by Destination | ||||

|---|---|---|---|---|---|

| Sourcing Regions | Baseline ($US Billion) | Scenario (% Change) | Destination Regions | Baseline ($US Billion) | Scenario (% Change) |

| EU28 | 4.85 | 1.02 | EU28 | 5.21 | 1.00 |

| Indonesia | 0.03 | 2.29 | China | 0.41 | −1.14 |

| Brazil | 0.02 | 2.27 | Rest of Europe | 0.29 | −0.28 |

| Rest of Europe | 0.29 | 1.97 | Nigeria | 0.23 | −0.43 |

| USA | 0.24 | 2.04 | Japan | 0.02 | −1.19 |

| Former Russia | 0.37 | 2.23 | India | 0.04 | −1.17 |

| Ukraine | 0.18 | 1.88 | USA | 0.10 | −1.01 |

| Belarus | 0.13 | 1.89 | Former Russia | 0.04 | −0.84 |

| Total | 7.22 | 1.39 | Total | 6.62 | 0.61 |

| Regions | Paddy Rice | Wheat | Vegetables, Fruit, Nuts | Oil Seeds | Sugar Crops | Plant-Based Fibers | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Area | Price | Area | Price | Area | Price | Area | Price | Area | Price | Area | Price | |

| EU28 | −0.21 | 0.47 | −0.20 | 0.62 | −0.19 | 0.64 | −0.20 | 0.60 | −0.18 | 0.77 | −0.22 | 0.51 |

| Rest of Europe | −0.09 | 0.23 | −0.09 | 0.26 | −0.08 | 0.31 | −0.09 | 0.23 | −0.08 | 0.26 | −0.10 | 0.26 |

| Former Russia | −0.01 | 0.07 | −0.01 | 0.11 | −0.01 | 0.07 | −0.01 | 0.08 | −0.01 | 0.06 | −0.01 | 0.04 |

| Ukraine | −0.02 | 0.09 | −0.06 | 0.18 | −0.06 | 0.25 | −0.04 | 0.14 | −0.06 | 0.28 | −0.07 | 0.15 |

| Malaysia | −0.01 | 0.04 | 0.03 | 0.26 | −0.01 | 0.04 | −0.01 | 0.04 | −0.01 | 0.03 | −0.01 | 0.02 |

| USA | −0.01 | 0.07 | 0.01 | 0.09 | −0.01 | 0.06 | −0.01 | 0.06 | −0.01 | 0.05 | −0.01 | 0.04 |

| Nigeria | −0.01 | 0.03 | - | 0.04 | −0.01 | 0.03 | −0.01 | 0.03 | - | 0.01 | - | - |

| South Africa | 0.01 | 0.10 | 0.01 | 0.10 | 0.01 | 0.11 | - | 0.05 | - | 0.03 | - | 0.05 |

| World | −0.01 | 0.03 | −0.03 | 0.14 | −0.02 | 0.07 | −0.02 | 0.07 | −0.01 | 0.06 | −0.02 | 0.04 |

| GHG Emissions | Baseline | Scenario | |

|---|---|---|---|

| CO2 | 3689.21 | 3678.67 | |

| Non-CO2 | N2O | 317.01 | 317.01 |

| CH4 | 716.44 | 716.43 | |

| F GAS 1 | 158.46 | 158.47 |

| Selected Indicators | World | EU28 | Rest of Europe | ||||||

| Original | Mean | Variance | Original | Mean | Variance | Original | Mean | Variance | |

| Sectoral output | 284.9731 | 284.9731 | 2.67 × 10−6 | 53.5304 | 53.5311 | 3.32 × 10−4 | 4.4753 | 4.4753 | 1.15 × 10−6 |

| Exports | - | - | - | 6.1983 | 6.1987 | 1.39 × 10−4 | 0.3372 | 0.3372 | 2.15 × 10−7 |

| Imports | - | - | - | 7.2243 | 7.2244 | 3.2 × 10−5 | 0.3040 | 0.3040 | 1.22 × 10−7 |

| Land use | 20.0058 | 20.0058 | 1.81 × 10−7 | 3.7951 | 3.7953 | 1.83 × 10−5 | 0.3120 | 0.3120 | 6.47 × 10−8 |

| Selected Indicators | Former Russia | US | Brazil | ||||||

| Original | Mean | Variance | Original | Mean | Variance | Original | Mean | Variance | |

| Sectoral output | 15.3685 | 15.3685 | 3.58 × 10−6 | 22.2379 | 22.2379 | 2.67 × 10−6 | 10.4253 | 10.4253 | 5.12 × 10−8 |

| Exports | 2.3780 | 2.3781 | 2.13 × 10−6 | 2.6766 | 2.6766 | 2.01 × 10−6 | 0.0522 | 0.0522 | 8.84 × 10−9 |

| Imports | 0.1112 | 0.1112 | 8 × 10−9 | 0.5318 | 0.5318 | 1.85 × 10−8 | 0.0201 | 0.0201 | 1.27 × 10−35 |

| Land use | 1.0411 | 1.0411 | 2.11 × 10−7 | 1.4913 | 1.4913 | 1.46 × 10−7 | 0.7256 | 0.7256 | 5.16 × 10−9 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Haddad, S.; Britz, W.; Börner, J. Economic Impacts and Land Use Change from Increasing Demand for Forest Products in the European Bioeconomy: A General Equilibrium Based Sensitivity Analysis. Forests 2019, 10, 52. https://doi.org/10.3390/f10010052

Haddad S, Britz W, Börner J. Economic Impacts and Land Use Change from Increasing Demand for Forest Products in the European Bioeconomy: A General Equilibrium Based Sensitivity Analysis. Forests. 2019; 10(1):52. https://doi.org/10.3390/f10010052

Chicago/Turabian StyleHaddad, Salwa, Wolfgang Britz, and Jan Börner. 2019. "Economic Impacts and Land Use Change from Increasing Demand for Forest Products in the European Bioeconomy: A General Equilibrium Based Sensitivity Analysis" Forests 10, no. 1: 52. https://doi.org/10.3390/f10010052

APA StyleHaddad, S., Britz, W., & Börner, J. (2019). Economic Impacts and Land Use Change from Increasing Demand for Forest Products in the European Bioeconomy: A General Equilibrium Based Sensitivity Analysis. Forests, 10(1), 52. https://doi.org/10.3390/f10010052