Intensity and Direction of Volatility Spillover Effect in Carbon–Energy Markets: A Regime-Switching Approach

Abstract

:1. Introduction

2. Literature Review and Research Question Development

2.1. Studies on Carbon–Energy Correlations

2.2. Research Question Development

3. Research Models

3.1. Bivariate GARCH Model

3.2. DCC Model

3.3. Bivariate SWARCH Model

4. Data and Estimation Results

4.1. Data

4.2. Unit Root Tests

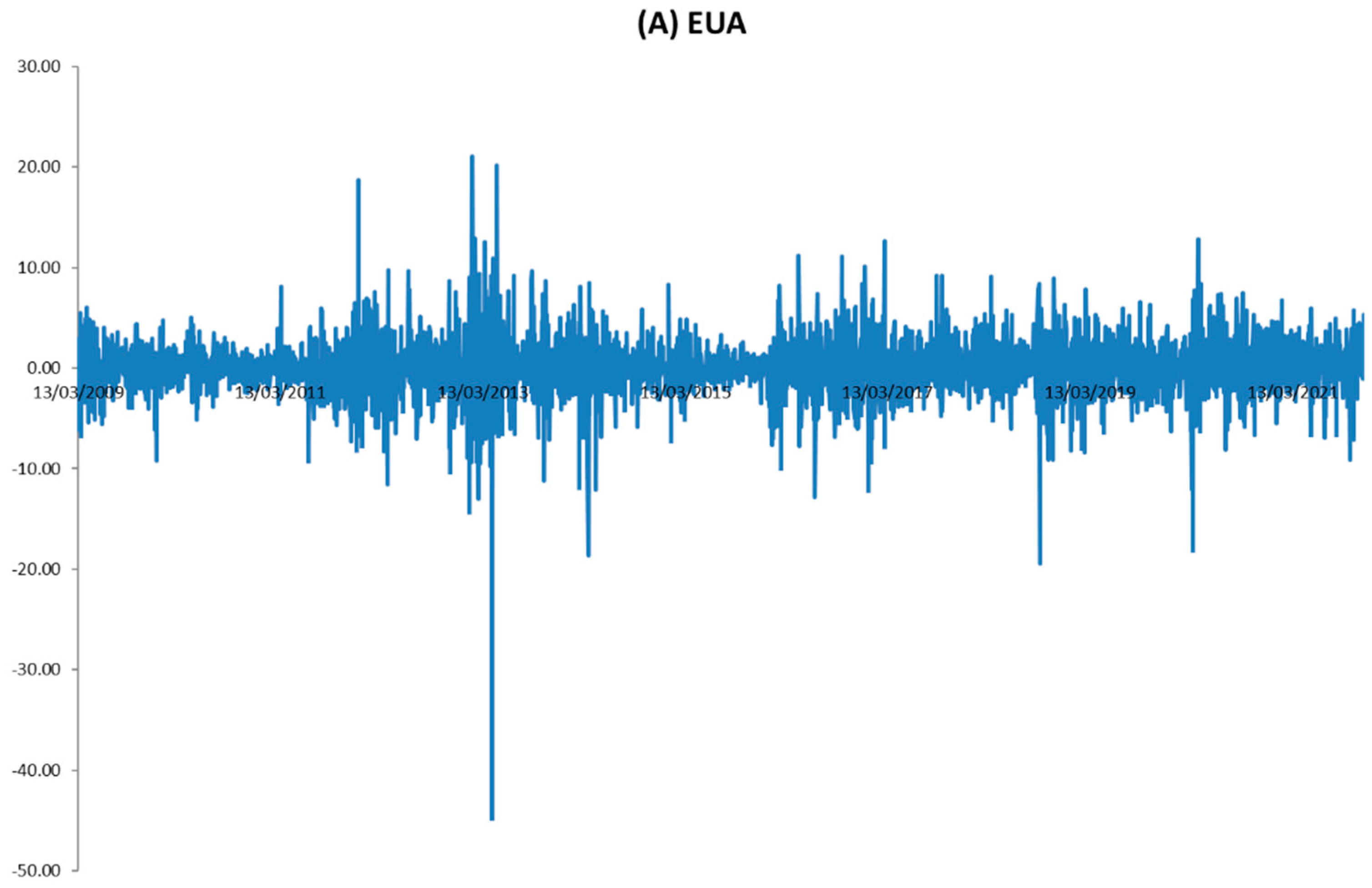

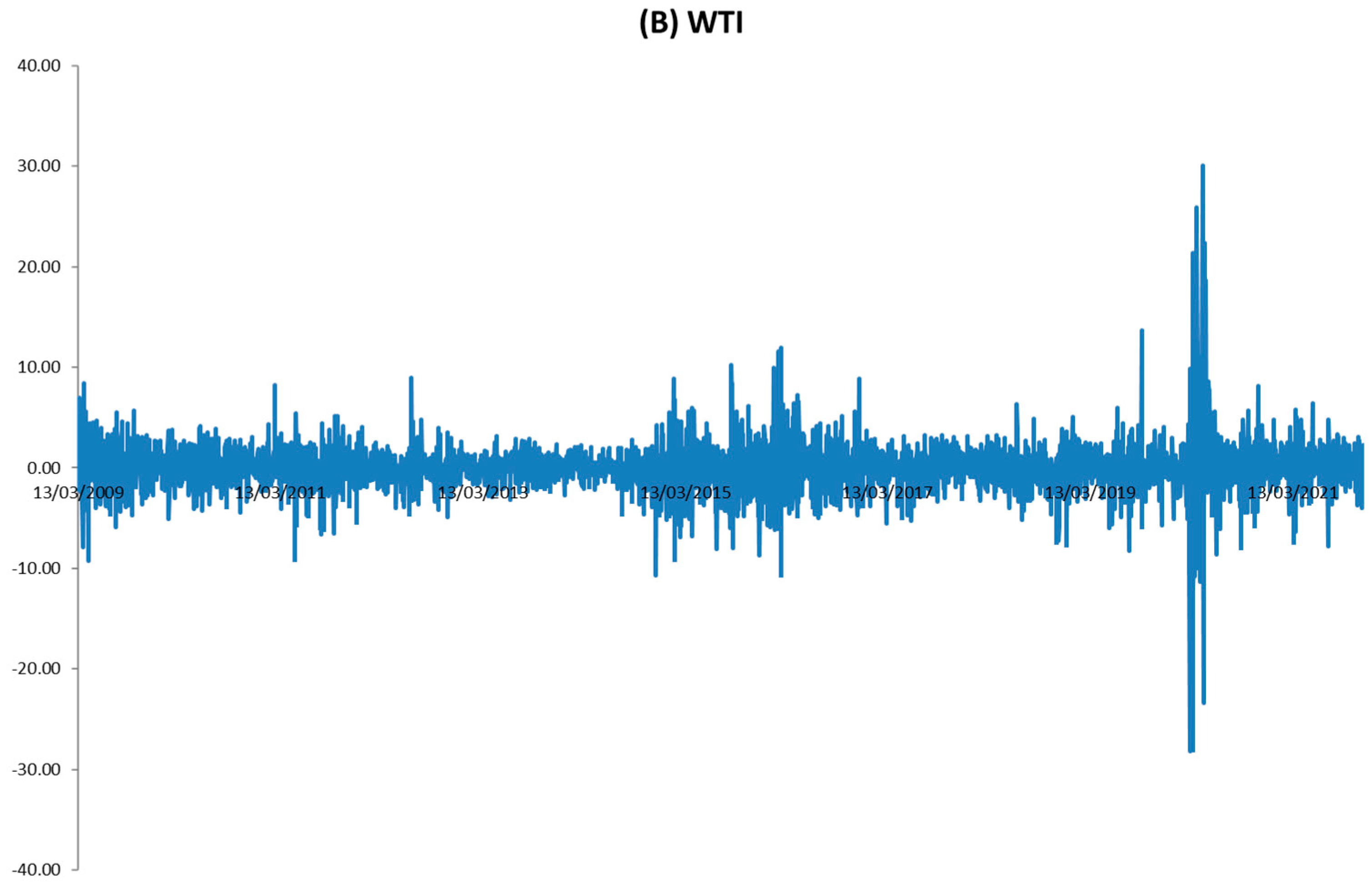

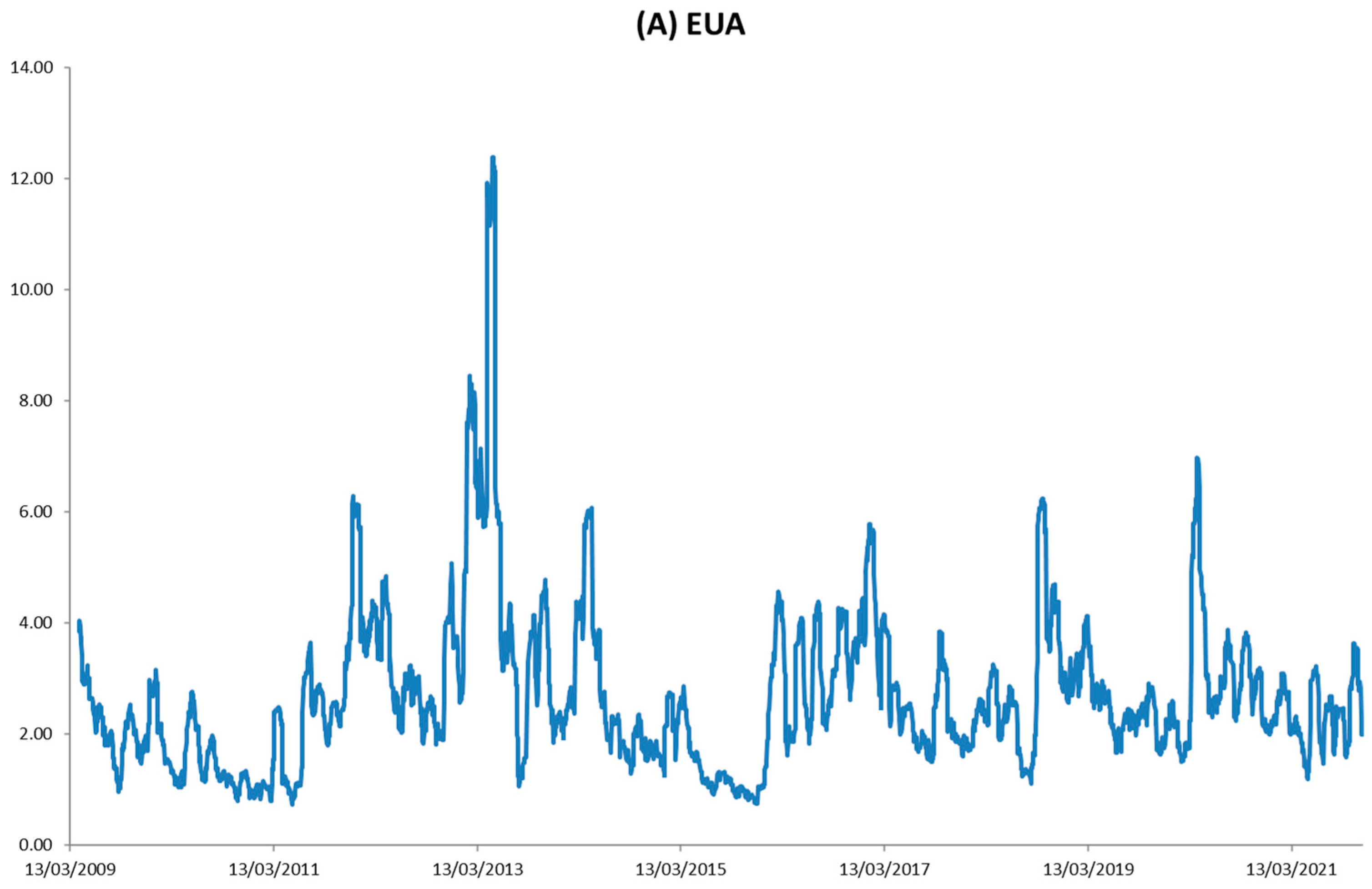

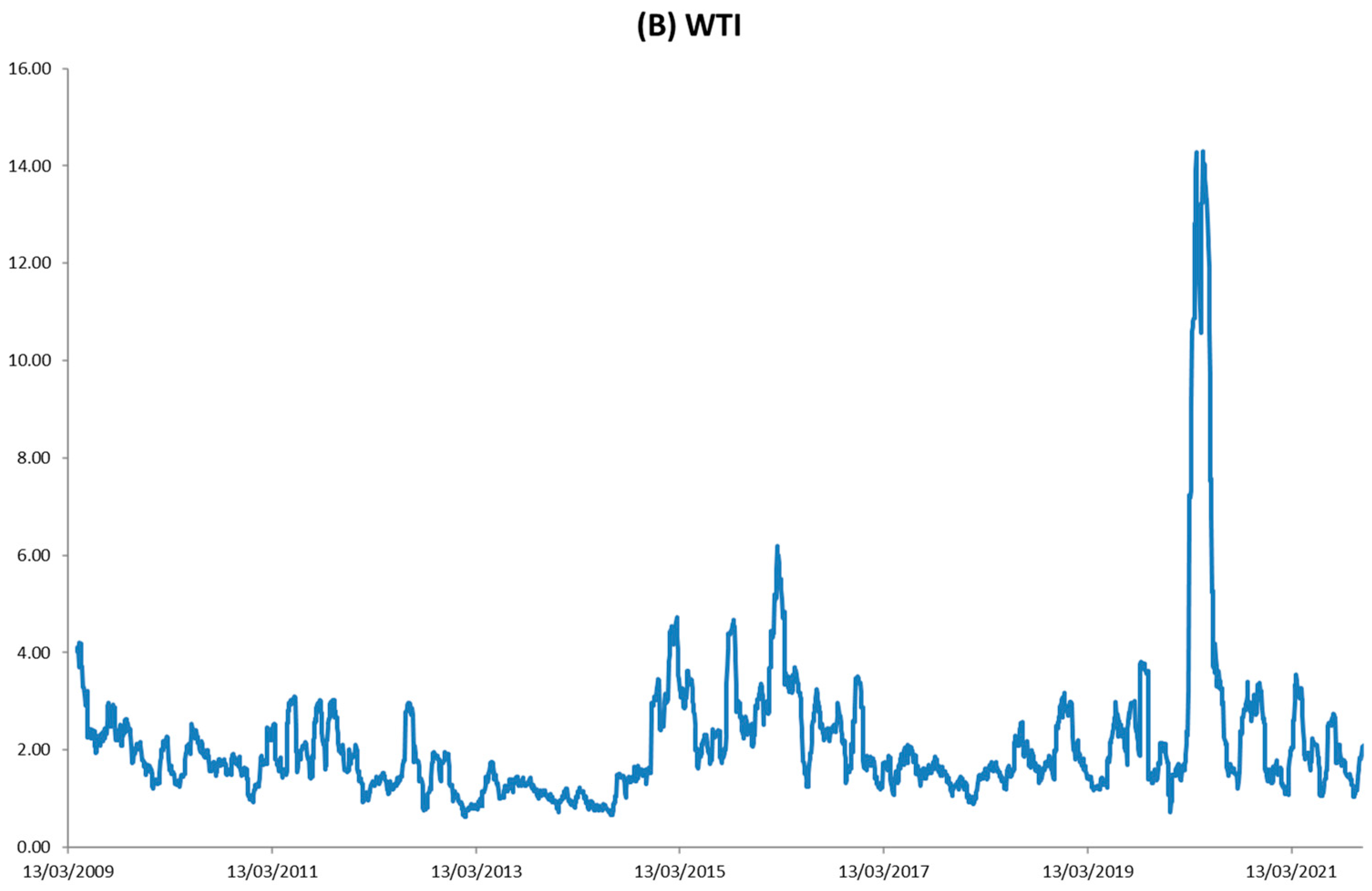

4.3. Illustration of Volatility Jumps

4.4. Bivariate GARCH Model

4.5. DCC Model

4.6. Bivariate SWARCH Model

5. Discussion and Practical Tests

5.1. Volatility Spillover Effect: Intensity and Direction

5.2. Portfolio Risk Forecasting

5.3. Portfolio Construction

5.4. Issue of COVID-19 Pandemic

6. Conclusions and Future Research Directions

Funding

Data Availability Statement

Conflicts of Interest

References

- Michaelowa, A.; Michaelowa, K.; Shishlov, I.; Brescia, D. Catalysing private and public action for climate change mitigation: The World Bank’s role in international carbon markets. Clim. Policy 2021, 21, 120–132. [Google Scholar] [CrossRef]

- Gong, X.; Shi, R.; Xu, J.; Lin, B. Analyzing spillover effects between carbon and fossil energy markets from a time-varying perspective. Appl. Energy 2021, 285, 116384. [Google Scholar] [CrossRef]

- Chevallier, J. Time-varying correlations in oil, gas and CO2 prices: An application using BEKK, CCC and DCC-MGARCH models. Appl. Econ. 2012, 44, 4257–4274. [Google Scholar] [CrossRef] [Green Version]

- Zhang, Y.J.; Sun, Y.F. The dynamic volatility spillover between European carbon trading market and fossil energy market. J. Clean. Prod. 2016, 112, 2654–2663. [Google Scholar] [CrossRef]

- Lin, B.; Chen, Y. Dynamic linkages and spillover effects between CET market, coal market and stock market of new energy companies: A case of Beijing CET market in China. Energy 2019, 172, 1198–1210. [Google Scholar] [CrossRef]

- Li, L. The dynamic interrelations of oil-equity implied volatility indexes under low and high volatility-of-volatility risk. Energy Econ. 2022, 105, 105756. [Google Scholar] [CrossRef]

- Li, L.; Scrimgeour, F. The co-integration of CDS and bonds in time-varying volatility dynamics: Do credit risk swaps lower bond risks? Stud. Nonlinear Dyn. Econom. 2022, 26, 475–497. [Google Scholar] [CrossRef]

- Heckman, J. Sample selection bias as a specification error. Econometrica 1979, 47, 153–161. [Google Scholar] [CrossRef]

- Tan, X.; Sirichand, K.; Vivian, A.; Wang, X. How connected is the carbon market to energy and financial markets? A systematic analysis of spillovers and dynamics. Energy Econ. 2020, 90, 104870. [Google Scholar] [CrossRef]

- Chevallier, J. A model of carbon price interactions with macroeconomic and energy dynamics. Energy Econ. 2011, 33, 1295–1312. [Google Scholar] [CrossRef]

- Tan, X.; Wang, X. Dependence changes between the carbon price and its fundamentals: A quantile regression approach. Appl. Energy 2017, 190, 306–325. [Google Scholar] [CrossRef]

- Zhao, X.; Han, M.; Ding, L.L.; Kang, W.L. Usefulness of economic and energy data at different frequencies for carbon price forecasting in the EU ETS. Appl. Energy 2018, 216, 132–141. [Google Scholar] [CrossRef]

- Lin, B.; Jia, Z. Impacts of carbon price level in carbon emission trading market. Appl. Energy 2019, 239, 157–170. [Google Scholar] [CrossRef]

- Liu, H.; Chen, Y. A study on the volatility spillovers, long memory effects and interactions between carbon and energy markets: The impacts of extreme weather. Econ. Model. 2013, 35, 840–855. [Google Scholar] [CrossRef]

- Koch, N. Dynamic linkages among carbon, energy and financial markets: A smooth transition approach. Appl. Econ. 2014, 46, 715–729. [Google Scholar] [CrossRef]

- Balcılar, M.; Demirer, R.; Hammoudeh, S.; Nguyen, D.K. Risk spillovers across the energy and carbon markets and hedging strategies for carbon risk. Energy Econ. 2016, 54, 159–172. [Google Scholar] [CrossRef] [Green Version]

- Byun, S.J.; Cho, H. Forecasting carbon futures volatility using GARCH models with energy volatilities. Energy Econ. 2013, 40, 207–221. [Google Scholar] [CrossRef]

- Wei, C.C.; Lin, Y.G. Carbon future price return, oil future price return and stock index future Price return in the US. Int. J. Energy Econ. Policy 2016, 6, 655–662. [Google Scholar]

- Lin, B.; Li, J. The spillover effects across natural gas and oil markets: Based on the VEC-MGARCH framework. Appl. Energy 2015, 155, 229–241. [Google Scholar] [CrossRef]

- Wang, Y.; Guo, Z. The dynamic spillover between carbon and energy markets: New evidence. Energy 2018, 149, 24–33. [Google Scholar] [CrossRef]

- Diebold, F.X.; Yilmaz, K. Better to give than to receive: Predictive directional measurement of volatility spillovers. Int. J. Forecast. 2012, 28, 57–66. [Google Scholar] [CrossRef] [Green Version]

- Ji, Q.; Zhang, D.; Geng, J. Information linkage, dynamic spillovers in prices and volatility between the carbon and energy markets. J. Clean. Prod. 2018, 198, 972–978. [Google Scholar] [CrossRef]

- Diebold, F.X. Modeling the persistence of conditional variance: A comment. Econom. Rev. 1986, 5, 51–56. [Google Scholar] [CrossRef]

- Lamoureux, C.G.; Lastrapes, W.D. Persistence in variance, structural change and the GARCH model. J. Bus. Econ. Stat. 1990, 8, 225–234. [Google Scholar]

- Aielli, G.P. Dynamic conditional correlation: On properties and estimation. J. Bus. Econ. Stat. 2013, 31, 282–299. [Google Scholar] [CrossRef]

- Kodres, L.; Pritsker, M. A rational expectations model of financial contagion. J. Financ. 2002, 57, 769–800. [Google Scholar] [CrossRef] [Green Version]

- Trevino, I. Informational channels of financial contagion. Econometrica 2020, 88, 297–335. [Google Scholar] [CrossRef]

- Engle, R.; Ghysels, E.; Sohn, B. Stock market volatility and macroeconomic fundamentals. Rev. Econ. Stat. 2013, 95, 776–797. [Google Scholar] [CrossRef]

- Baker, S.R.; Bloom, N.; Davis, S.J. Measuring economic policy uncertainty. Q. J. Econ. 2016, 131, 1593–1636. [Google Scholar] [CrossRef]

- Gulen, H.; Ion, M. Policy uncertainty and corporate investment. Rev. Financ. Stud. 2016, 29, 523–564. [Google Scholar] [CrossRef]

- Danielsson, J.; Valenzuela, M.; Zer, I. Learning from history: Volatility and financial crises. Rev. Financ. Stud. 2018, 31, 2774–2805. [Google Scholar] [CrossRef]

- Li, L. Dynamic correlations and domestic-global diversification. Res. Int. Bus. Financ. 2017, 39, 280–290. [Google Scholar] [CrossRef]

- Li, L. Testing and comparing the performance of dynamic variance and correlation models in value-at-risk estimation. N. Am. J. Econ. Financ. 2017, 40, 116–135. [Google Scholar] [CrossRef]

- Engle, R.F. Dynamic conditional correlation: A simple class of multivariate generalized autoregressive conditional heteroskedasticity models. J. Bus. Econ. Stat. 2002, 20, 339–350. [Google Scholar] [CrossRef]

- Gray, S.F. Modeling the conditional distribution of interest rates as a regime-switching process. J. Financ. Econ. 1996, 42, 27–62. [Google Scholar] [CrossRef]

- Dueker, M.J. Markov switching in GARCH processes and mean-reverting stock-market volatility. J. Bus. Econ. Stat. 1997, 15, 26–35. [Google Scholar]

- Klaassen, F. Improving GARCH volatility forecasts with regime-switching GARCH. Empir. Econ. 2002, 27, 363–394. [Google Scholar] [CrossRef] [Green Version]

- Smith, D.R. Markov-switching and stochastic volatility diffusion models of short-term interest rates. J. Bus. Econ. Stat. 2002, 20, 183–197. [Google Scholar] [CrossRef]

- Augustyniak, M. Maximum likelihood estimation of the Markov-switching GARCH model. Comput. Stat. Data Anal. 2014, 76, 61–75. [Google Scholar] [CrossRef]

- Ramchand, L.; Susmel, R. Volatility and cross-correlation across major stock markets. J. Empir. Financ. 1998, 5, 397–416. [Google Scholar] [CrossRef]

- Edwards, S.; Susmel, R. Interest-rate volatility in emerging markets. Rev. Econ. Stat. 2003, 85, 328–348. [Google Scholar] [CrossRef]

- Dickey, D.A.; Fuller, W.A. Likelihood ratio statistics for autoregressive time series with a unit root. Econometrica 1981, 49, 1057–1072. [Google Scholar] [CrossRef]

- Phillips, P.C.B.; Perron, P. Testing for a unit root in a time series regression. Biometrika 1988, 75, 335–346. [Google Scholar] [CrossRef]

- Elliott, G.; Rothenberg, T.J.; Stock, J.H. Efficient tests for an autoregressive unit root. Econometrica 1996, 64, 813–836. [Google Scholar] [CrossRef] [Green Version]

- Ng, S.; Perron, P. Lag length selection and the construction of unit root tests with good size and power. Econometrica 2001, 69, 1519–1554. [Google Scholar] [CrossRef] [Green Version]

- French, K.R.; Poterba, J.M. Investor diversification and international equity markets. Am. Econ. Rev. 1991, 81, 222–226. [Google Scholar]

- Tesar, L.L.; Werner, I. Home Bias and the Globalization of Securities Markets; National Bureau of Economic Research: Cambridge, UK, 1992. [Google Scholar]

- Deng, X.; Yao, J. On the property of multivariate generalized hyperbolic distribution and the Stein-type inequality. Commun. Stat. Theory Methods 2018, 47, 5346–5356. [Google Scholar] [CrossRef]

- Li, L.; Lin, W. Examining the volatility of Taiwan stock index returns via a three-volatility-regime Markov-switching ARCH model. Rev. Quant. Financ. Account. 2003, 21, 123–139. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| EUA | WTI | |

|---|---|---|

| Panel A: Natural log level | ||

| Mean | 2.4113 | 4.1823 |

| Q1 | 1.8213 | 3.9300 |

| Median (Q2) | 2.9143 | 4.4894 |

| Q3 | 2.3116 | 4.2015 |

| S.D. | 0.7081 | 0.3417 |

| Skewness | 0.4987 | −0.6036 |

| Kurtosis | 2.4039 | 3.4786 |

| Correlation | −0.1626 | |

| Panel B: Return rate (Logarithmic change) | ||

| Mean | 0.0574 | 0.0376 |

| Q1 | −1.3462 | −1.0658 |

| Median (Q2) | 1.5629 | 1.1675 |

| Q3 | 0.0000 | 0.0000 |

| S.D. | 3.0350 | 2.6399 |

| Skewness | −0.9978 | 0.6581 |

| Kurtosis | 21.3959 | 29.6411 |

| Correlation | 0.1791 | |

| EUA | WTI | |

|---|---|---|

| Panel A: Price level (Natural logarithm) | ||

| ADF | 0.1902 | −2.4291 |

| Phillips–Perron | 0.2785 | −2.3620 |

| ADF-GLS | 0.0606 | −1.6053 |

| NGP | 0.1487 | −5.7049 |

| Panel B: Return rate (Logarithmic change) | ||

| ADF | −42.9309 *** | −19.1259 *** |

| Phillips–Perron | −56.9186 *** | −57.7969 *** |

| ADF-GLS | −2.5954 *** | −2.7100 *** |

| NGP | −4.4264 | −7.3027 * |

| Coefficient | S.D. | t-Statistic | p-Value | |

|---|---|---|---|---|

| EUA Equation | ||||

| µEUA | 0.1290 | 0.0358 | 3.6034 | 0.0002 |

| φEUA | −0.0037 | 0.0032 | −1.1563 | 0.1238 |

| ωEUA | 0.1047 | 0.0241 | 4.3444 | 0.0000 |

| αEUA | 0.1226 | 0.0110 | 11.1455 | 0.0000 |

| βEUA | 0.8777 | 0.0102 | 86.0490 | 0.0000 |

| WTI Equation | ||||

| µWTI | 0.0937 | 0.0268 | 3.4963 | 0.0002 |

| φWTI | 0.0036 | 0.0131 | 0.2748 | 0.3917 |

| ωWTI | 0.1687 | 0.0327 | 5.1590 | 0.0000 |

| αWTI | 0.1370 | 0.0120 | 11.4167 | 0.0000 |

| βWTI | 0.8393 | 0.0143 | 58.6923 | 0.0000 |

| Correlation | ||||

| ρ | 0.1716 | 0.0167 | 10.2754 | 0.0000 |

| Log-likelihood function | −14,890.8106 | |||

| Coefficient | S.D. | t-Statistic | p-Value | |

|---|---|---|---|---|

| EUA Equation | ||||

| µEUA | 0.1122 | 0.0383 | 2.9295 | 0.0017 |

| φEUA | −0.0159 | 0.0085 | −1.8706 | 0.0307 |

| ωEUA | 0.0840 | 0.0221 | 3.8009 | 0.0001 |

| αEUA | 0.1037 | 0.0107 | 9.6916 | 0.0000 |

| βEUA | 0.8949 | 0.0103 | 86.8835 | 0.0000 |

| WTI Equation | ||||

| µWTI | 0.0607 | 0.0348 | 1.7443 | 0.0406 |

| φWTI | −0.0196 | 0.0105 | −1.8667 | 0.0310 |

| ωWTI | 0.1033 | 0.0232 | 4.4526 | 0.0000 |

| αWTI | 0.0991 | 0.0100 | 9.9100 | 0.0000 |

| βWTI | 0.8838 | 0.0118 | 74.8983 | 0.0000 |

| Time-varying correlation | ||||

| τ | 0.0026 | 0.0016 | 1.6250 | 0.0521 |

| π | 0.9751 | 0.0102 | 95.5980 | 0.0000 |

| λ | 0.0110 | 0.0035 | 3.1429 | 0.0008 |

| Log-likelihood function | −14,834.1637 | |||

| Coefficient | S.D. | t-Statistic | p-Value | |

|---|---|---|---|---|

| EUA Equation | ||||

| p11EUA | 0.9729 | 0.0055 | 176.8909 | 0.0000 |

| p22EUA | 0.9316 | 0.0141 | 66.0709 | 0.0000 |

| µEUA | 0.1138 | 0.0413 | 2.7554 | 0.0029 |

| φEUA | −0.0139 | 0.0093 | −1.4946 | 0.0675 |

| ωEUA | 3.4121 | 0.1807 | 18.8827 | 0.0000 |

| αEUA | 0.0242 | 0.0172 | 1.4070 | 0.0797 |

| g2EUA | 6.7405 | 0.4385 | 15.3717 | 0.0000 |

| WTI Equation | ||||

| p11WTI | 0.9841 | 0.0039 | 252.3333 | 0.0000 |

| p22WTI | 0.9309 | 0.0164 | 56.7622 | 0.0000 |

| µWTI | 0.0434 | 0.0361 | 1.2022 | 0.1146 |

| φWTI | −0.0262 | 0.0153 | −1.7124 | 0.0434 |

| ωWTI | 2.2234 | 0.1218 | 18.2545 | 0.0000 |

| αWTI | 0.1704 | 0.0286 | 5.9580 | 0.0000 |

| g2WTI | 8.1736 | 0.8642 | 9.4580 | 0.0000 |

| State-varying correlations | ||||

| ρ1,1 | 0.1751 | 0.0255 | 6.8667 | 0.0000 |

| ρ2,1 | 0.1109 | 0.0391 | 2.8363 | 0.0023 |

| ρ1,2 | 0.2977 | 0.0556 | 5.3543 | 0.0000 |

| ρ2,2 | 0.3609 | 0.0637 | 5.6656 | 0.0000 |

| LRstatisticforρ1,1 = ρ2,1 = ρ1,2 = ρ2,2 | 15.0222 *** | |||

| Log-likelihood function | −14,890.1349 | |||

| Observation Percentage | |

|---|---|

| EUA = LV and WTI = LV | 64.54% |

| EUA = HV and WTI = LV | 19.98% |

| EUA = LV and WTI = HV | 11.00% |

| EUA = HV and WTI = HV | 4.50% |

| Total | 100% |

| MAE | |

|---|---|

| Panel A: MAE (Mean Absolute Error) | |

| Bivariate GARCH-CCC model | 2.3185 |

| Bivariate GARCH-DCC model | 2.3143 (−1.0906) |

| Bivariate SWARCH model with state-varying correlations | 2.1470 (−8.9225) *** |

| Panel B: MAE (Mean Square Error) | |

| Bivariate GARCH-CCC model | 9.9811 |

| Bivariate GARCH-DCC model | 9.9981 (0.3579) |

| Bivariate SWARCH model with state-varying correlations | 8.5664 (−5.5544) *** |

| Panel A: Portfolio mean return | |

| Mean return | |

| Bivariate GARCH-CCC model | 0.0436 |

| Bivariate GARCH-DCC model | 0.0427 (−0.3524) |

| Bivariate SWARCH model with state-varying correlations | 0.0452 (0.1611) |

| Panel B: Portfolio return volatility | |

| Return volatility | |

| Bivariate GARCH-CCC model | 1.7981 |

| Bivariate GARCH-DCC model | 1.7840 (−1.5996) |

| Bivariate SWARCH model with state-varying correlations | 1.6392 (−7.2752) *** |

| Panel C: Sharpe ratios | |

| Sharpe ratio | |

| Bivariate GARCH-CCC model | 0.0242 |

| Bivariate GARCH-DCC model | 0.0239 |

| Bivariate SWARCH model with state-varying correlations | 0.0276 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Li, L. Intensity and Direction of Volatility Spillover Effect in Carbon–Energy Markets: A Regime-Switching Approach. Algorithms 2022, 15, 264. https://doi.org/10.3390/a15080264

Li L. Intensity and Direction of Volatility Spillover Effect in Carbon–Energy Markets: A Regime-Switching Approach. Algorithms. 2022; 15(8):264. https://doi.org/10.3390/a15080264

Chicago/Turabian StyleLi, Leon. 2022. "Intensity and Direction of Volatility Spillover Effect in Carbon–Energy Markets: A Regime-Switching Approach" Algorithms 15, no. 8: 264. https://doi.org/10.3390/a15080264

APA StyleLi, L. (2022). Intensity and Direction of Volatility Spillover Effect in Carbon–Energy Markets: A Regime-Switching Approach. Algorithms, 15(8), 264. https://doi.org/10.3390/a15080264