1. Introduction

Power-to-Hydrogen is one of the Power-to-Gas technologies, jointly with Power-to-Synthetic Methane, Power-to-Liquid, Power-to-Chemicals and Power-to-Materials.

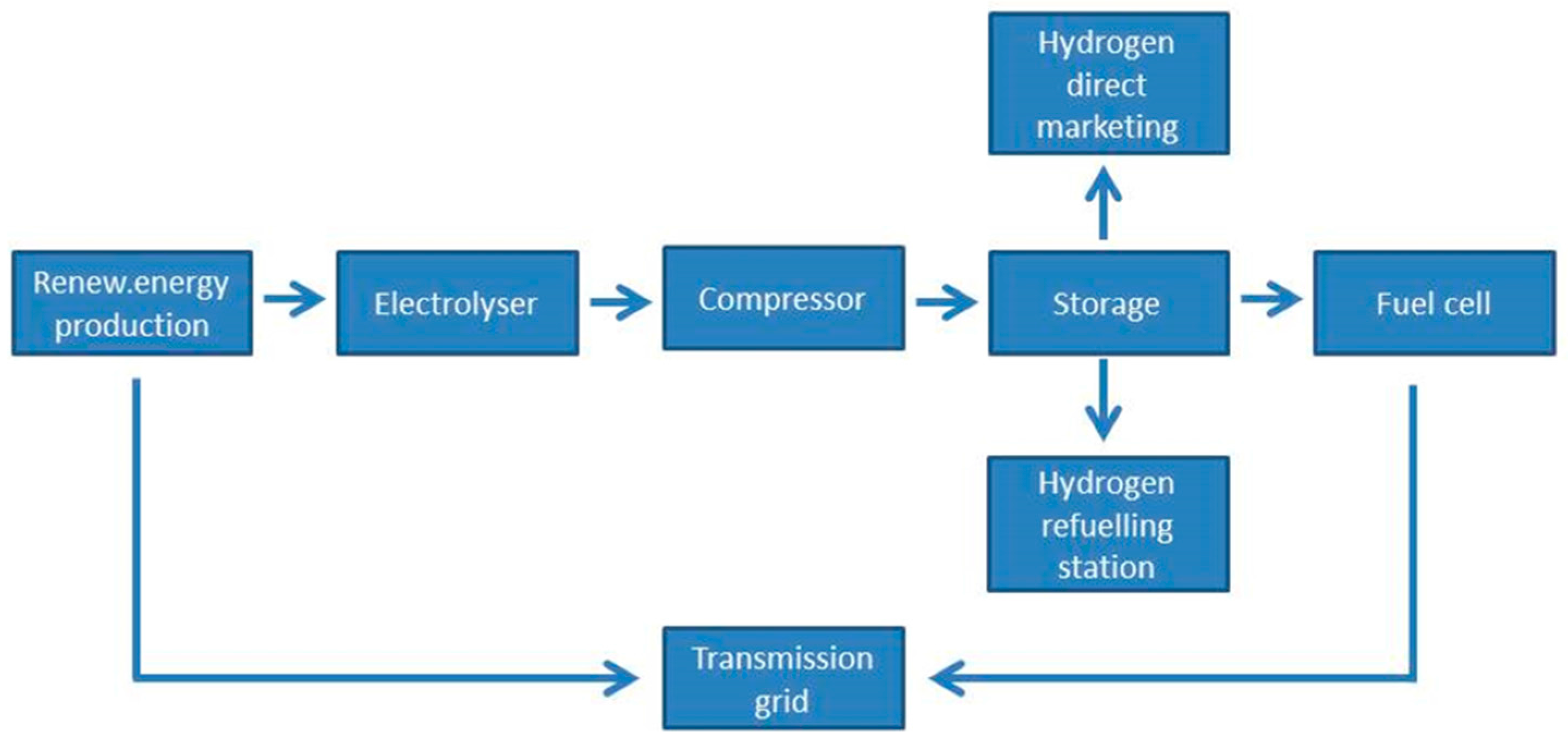

A hydrogen value chain technology foresees production, supply/storage (CGH2, LH2 or CcH2 storage systems), onsite SMR (steam methane reforming) or electrolysis, compression/transfer, and dispenser at 350 or 700 bar.

The produced hydrogen is stored in compressed form and can be directly marketed as a commodity or re-electrified on demand using a fuel cell. As regards the production from variable renewable energies (VRE), the systems basically include one or more wind turbine or another renewable energy system such as PV (photovoltaic) arrays to produce decarbonised electricity that could on demand be supplied directly to the transmission grid or to an electrolyser to produce renewable hydrogen [

1]. Additionally, the systems include a compressor, to densify hydrogen for an efficient storage in a high pressure storage device, and then different possible solutions for a flexible and effective use of renewable energy: hydrogen refuelling stations for Fuel Cell Electric Vehicles (FCEVs), directly market the hydrogen or use it in a local fuel cell for producing electricity that can be fed back into the grid on demand at the appropriate times (

Figure 1).

For instance, renewable hydrogen storage systems could be built in warehouses, and distribution and logistics centres using the refuelling station for fuel cell forklifts.

Considering energy production, previous experiences highlighted that, for stand-alone systems, it is better to include more than one renewable energy source, integrating wind plants with photovoltaics and/or bioenergy plants.

The appropriate storage capacity should be sized depending on the main purpose of the system. To date, around 8 GW of electrolysis capacity are installed worldwide [

2]. Main technologies for electrolysis are: alkaline electrolysis, Proton Exchange Membrane (PEM) electrolysis and solid oxide electrolysis cells (SOEC) [

3].

The older and more mature technology is alkaline electrolysis used since the 1920s and scaled up to multi-megawatt plants [

4]. Alkaline electrolysers performance varies between 50 and 80 kWh

el/kg

H2, which means an efficiency from 62%

LHV to 69%

LHV. Efficiencies of PEM cells electrolysis are similar to alkaline ones [

5] and many commercial suppliers produce kilowatt-scale systems (to hundreds of kilowatts as a maximum). PEM electrolysis allows high pressure hydrogen production but the cell life time is limited. Estimated energy consumptions of PEM electrolysers vary between 50 and 85 kWh

el/kg

H2, that means an efficiency from 59%

LHV to 70%

LHV.

Although high temperature SOEC is the less mature one since it is at an early stage of development, according to [

6], it could reach high efficiency and it may become cheap cause it does not involve noble metals. SOEC systems operate at high temperature (700–1000 °C), with efficiencies of 90%–95%; however, a considerably larger proportion of the heat input energy is required than for the others electrolysis techniques. This could mean lower running costs if a source of high grade heat is readily available, such as from industrial waste heat or a catalytic methanation process [

7].

Generally, the efficiency of the water to hydrogen conversion mainly depends on the used technology and the scale of the system. The electrolyser efficiency could reach up to 80%, while, considering the whole electrolysis system, the higher efficiencies reach up to 60%–65% using alkaline electrolysers [

8].

Using distilled water, electrolysers generically produce hydrogen with purity percentages between 99.5% and 99.99%, which means it could be used in FCEVs without a successive purification phase. Hydrogen is produced using electrolysers at about 30 bar, while FCEVs need a hydrogen pressure of 350 or 700 bar, so a compression system is required.

In this framework, the objective of this research is to identify potential uses of H

2 storage systems in Europe, considering the main regulatory and economic aspects, summarizing opinions and considerations of the managing boards of the main national and European associations dealing with hydrogen and fuel cells, as well as the main industries of the sector and the coordinators of relevant research projects about renewable hydrogen storage systems. To assess the validity of the expert opinion survey, many aspects reported in the paper results have been compared or related to previous studies and references, as done in [

9,

10] that highlighted expert opinion survey as an effective method to produce realistic results.

2. Methods: Experts Opinion Survey

In the above-described framework, the present study has been carried out integrating the information obtained by a survey with the support of the EHA (European hydrogen and fuel cell association) national members, academics, selective industrial experts and DSO (Distribution system operator) specialists, with the aim of pinpointing the potential uses of H2 storage systems in Europe, consistently with the main regulatory and economic aspects.

The survey covered the main technical, regulatory and economic issues regarding the installation and operation of renewable hydrogen storage systems in European countries, calling for specific indications of current and potential use of the storage system, a brief analysis of the main maintenance requirements as well as an overview of current economic aspects and regulatory issues connected to its installation and operation.

The elaborated survey was carried out by means of in-depth interviews and distributions of written questionnaires to the managing boards of the main national and European associations dealing with hydrogen and fuel cells as well as the main industries of the sector. Specific focus was on the opinions of the coordinators of research projects about renewable hydrogen storage systems.

Below, the questions of the written questionnaires distributed to the experts classified for each one of the analysed main topics:

Potential use of the storage system

What are the current locations in your country of renewable hydrogen storage systems?

What are the potential locations in your country of renewable hydrogen storage systems?

Describe the main characteristics of preferred locations and territorial contexts for a renewable hydrogen storage system.

Maintenance requirements

Describe the maintenance requirements of a renewable hydrogen storage plant highlighting timelines and required expertise

Regulatory issue

Describe the regulatory framework regarding the installation and operation of a hydrogen storage plant will be presented considering EU Directives and your country rules.

Economic aspects

Describe main economic issues of renewable hydrogen storage systems considering possible end users and underlying critical aspects and possible solutions in your country. In addition, specify hydrogen and renewable energy prices for a feasible market in your country.

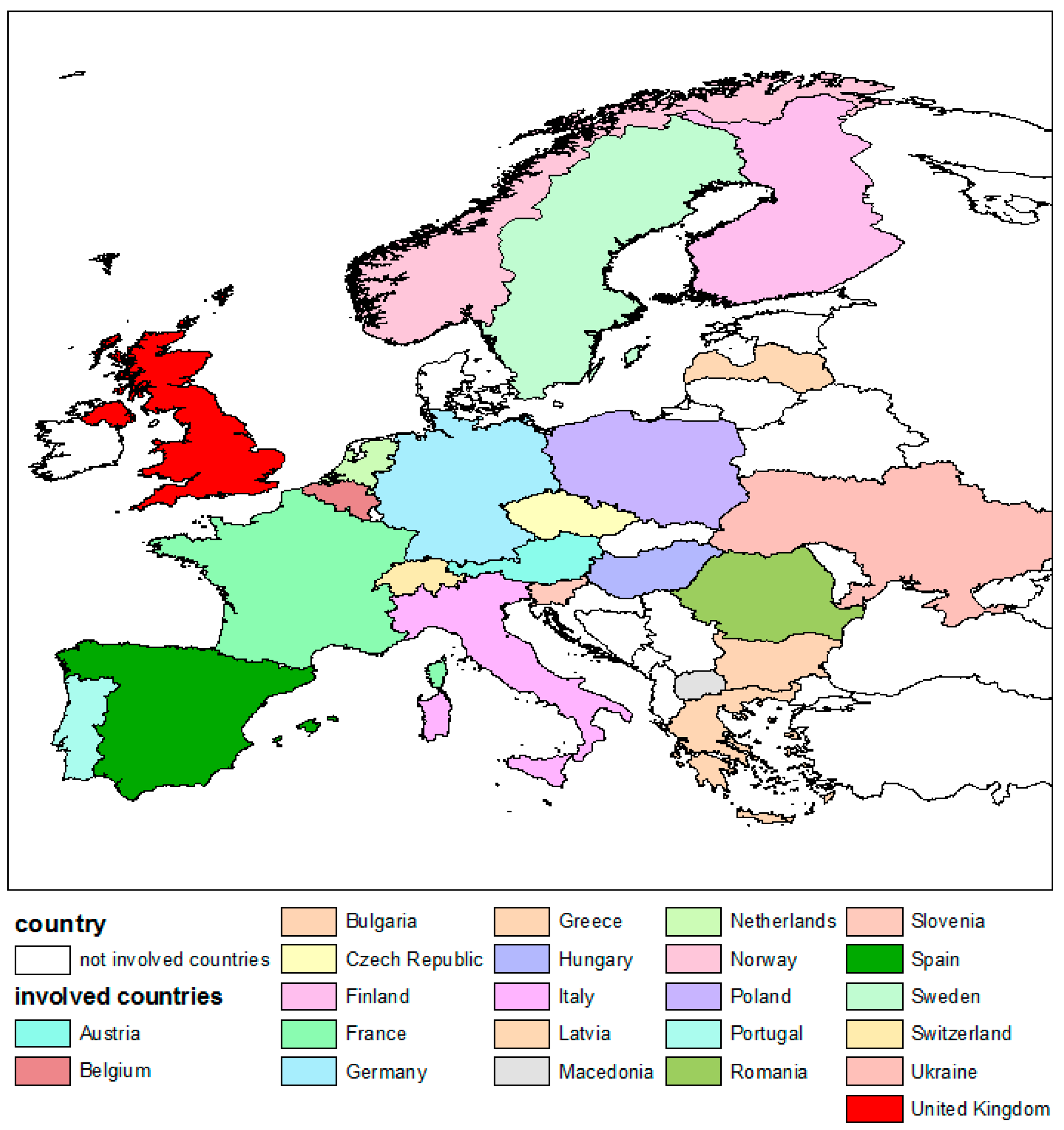

As shown in

Figure 2, the surveys involved most of the European countries, while the remaining countries did not include national associations dealing with hydrogen and fuel cells or did not answer the above listed questions. Additionally,

Table 1 reports for each country the list of the organizations that actively contributed to the survey.

As aforementioned, the expert opinions would be an effective tool to produce realistic results used in many research articles, on energy [

10,

11,

12], storage [

13] and other different topics [

9,

14,

15,

16], in order to have an updated and integrated view of the aspects related to the analysed topic. In this way, the involvement of main stakeholders in the analysis helps researchers and readers to understand local issues within a complete overview of related pros and cons.

3. Expert Opinion Results

The following paragraphs summarize the outcomes obtained by the above described survey shared through in-depth interviews and written questionnaires with the identified experts.

3.1. Main Current Locations of Renewable Hydrogen Storage Systems

3.1.1. North and Central Europe

The first full-scale combined wind power and hydrogen plant was realized in Utsira, a small island of Norway. This off-grid test site aimed at making it self-sufficient with renewable energy. It was an autonomous and remote-operated energy system dismantled years ago, which pilot project was carried out in 2004 supplying electricity to ten private households. This first wind/hydrogen demonstration system in Utsira, which served as the main power system for real users, worked for years without problems, keeping the customers satisfied and getting a public acceptance of hydrogen [

17]. This plant included two 600 kW wind turbines, one connected to the external grid and the other to a stand-alone system, a 5 kW flywheel and a 100 kVA master synchronous machine to balance voltage and frequency, as well as a 10 Nm

3/h electrolyser with a peak load of 48 kW. Hydrogen is compressed by a 5 kW compressor and storage at a 200 bar pressure in a 2400 Nm

3 pressure vessel. Moreover, a 55 kW hydrogen internal combustion engine and a 10 kW fuel cell were installed.

In Norway, there is a small-scale demonstration of hydrogen storage system being tested in Herøya, Porsgrunn, where the first hydrogen refuelling station was built by Norsk Hydro in 2006. In Sweden, only one private house outside Gothenburg has been mentioned during the survey. Currently, there are 20 power to gas projects running in Germany and about two third of which focus on energy storage (mostly injection of renewable hydrogen into the natural gas grid). Within the National Innovation Programme Hydrogen and Fuel Cell Technology (NIP), there are two large projects focus on energy storage both of which are located in the north of Germany. The first is KompElSys Project coordinated by WindGas Hamburg and funded with €13.7 million, while the second one is Wind Hydrogen Project RH2-WKA funded with €6.7 million. In particular, five hydrogen retail stations with onsite electrolysers were built and funded by NIP to provide fuel for FCEVs, and a further wind-to-hydrogen-system provides both stationary storage capacity and fuel. Both those latter projects involve some hydrogen storage facilities and their sites are spread across Germany.

Moreover, one of the main renewable hydrogen storage systems is a wind–hydrogen hybrid power plant, with a 6 MW wind power plant located in Prenzlau (Germany) and opened on 25 October 2011. ENERTRAG AG has partnered with DB Energie GmbH, Vattenfall and TOTAL Germany on the project with DB Energie seeking to use the electricity to contribute to decarbonising the railway network. The rail network needs a predictable and reliable source of power and it is encouraging to see DB Energie recognising the solution that a combination of hydrogen and renewables can offer. In 2010, DB Energie reported that renewables contributed 19.8% of its traction energy mix; however, the minimum goal foreseen by 2020 is a contribution of 35%. When more wind power is available at the site than the amount that can be acceptable by the Grid, a series of electrolysers are used to generate and store hydrogen on site. This stored energy, effectively acting as renewable base-load energy, is used in different ways:

- -

The hydrogen can be mixed with biogas and fed into cogeneration plants which produce electricity and heat. The electricity can then be fed back into the grid at times when there is no wind or other VRE dispatch; the heat is fed into a district heating network, increasing the overall efficiency of the hybrid power plant.

- -

The hydrogen is also used as a fuel by TOTAL hydrogen refuelling stations in Berlin and Hamburg, which support fleets of fuel cell vehicles.

- -

Berlin Brandenburg Airport (BER) is also interested in using hydrogen from this project to fuel its vehicle fleet, which is planned to be in operation soon.

In Austria, two main locations include FCH (Fuel Cells and Hydrogen) R&D (Research and Development) projects: in Pilsbach (upper Austria), there is a test facility for investigating underground storage of wind and solar energy converting electricity into a mixture of methane and hydrogen, whereas, in Auersthal (lower Austria), a power to gas pilot plant has been built with an innovative, flexible and unique in Europe high-pressure PEM electrolyser that uses wind-generated electricity.

Currently, in the UK, more than 30 large caverns spread over several locations are in use. Moreover, large caverns are used as reference scenario. Therefore, it is remarkable that the Teesside shallowest salt bed has about 20 stores considered as a location for storing hydrogen for a large power installation. In Scotland, there are a respectable number of innovative renewable H

2 energy system projects underway, with involvement from many of the key stakeholders in each of these projects. In addition to Orkney “BIG HIT” project, built on the foundations of earlier projects and announced 11 May 2016 using community wind turbine and 1 MW electrolyser in Shapinsay (11 million Euro with FCH-JU (Fuel Cells and Hydrogen Joint Undertaking) support), the three most relevant projects in Scotland are:

- -

Aberdeen Hydrogen Bus project, linking renewable energy with sustainable transport (€22 million with FCH-JU support).

- -

Orkney Surf ‘n’ Turf project linking EMEC renewables with Kirkwall using hydrogen (£4 million, funded by the Scottish Government and Highlands & Islands Enterprise).

- -

Levenmouth project in Methil, optimise local renewable energy use and transport with hydrogen (£4 M with Scottish Government LECF support).

In Czech Republic, 10 km from Prague, there is a pilot plant for photovoltaic electricity storage to hydrogen with a 4 kW Fuel Cell and a 7 kW electrolyser, while, in Hungary and in Poland, there are no renewable hydrogen storage systems

3.1.2. Mediterranean Europe

Considering Italian renewable hydrogen storage systems, the INGRID project integrates Smart Grids innovations with hydrogen-based energy storage to match energy supply and demand optimizing the management of electricity generated by VRE. A 39 MWh energy storage facility using hydrogen-based solid state storage, electrolysis technology and fuel cell power systems is under construction in Puglia (Troia municipality) where over 3500 MW of solar, wind, and biomass electric energy power are already installed. This hydrogen energy storage installation, with more than 1 ton of safely stored hydrogen is controlled by advanced smart grid solutions and provide effective and smart balancing support for the local grid managed by Enel Distribuzione.

The system, which includes a novel fast responding 1.2 MW hydrogen generator, is object of several investigations on potential value streams for the generated carbon-neutral hydrogen. INGRID expected outcomes foresee increasing the round-trip efficiency and the Energy Density up to 600 kWh/m3, almost double that achievable by storing H2 in large caverns.

The platform of HYRREG project, funded by the Program of Cooperation of Southwest Europe (SUDOE), has been mentioned by many experts coming from Southwest Europe, as a real platform to generate hydrogen-related projects and a roadmap to improve regional competitiveness and industrial development in the SUDOE region: Spain, France, Portugal and Gibraltar that occupy about 18% of the surface and 12% of the population of the EU. The platform established by HYRREG has proven to be highly successful according to the number of projects promoted: 40 projects were promoted in 2013, 18 of those with a European dimension, and more than 50 companies have benefitted from the existence of this project [

18].

Jointly with Prenzlau plant, another main renewable hydrogen storage system is located on the French island of Corsica, in the Mediterranean Sea, and combines solar power with electrolysers, hydrogen storage and fuel cells. Known as MYRTE (a French acronym for Renewable Hydrogen Mission for Integration into the Electric Grid), the project is a partnership between CEA (the French Nuclear and Alternative Energies Commission), the energy company AREVA and the University of Corsica. MYRTE contains a 560kW PV power plant that has been connected to the Corsican electricity grid since December 2011. The system can provide electricity during the day and, using the electrolysers and AREVA’s hydrogen energy storage system, excess electricity can be stored and returned when required using fuel cells. The initial aim of the project was to prove the concept, but, since 2013, the plans have been elaborated to further develop the system with a second phase that foresees the inclusion of AREVA’s Greenergy Box, an integrated, containerised hydrogen energy system housing electrolysers, fuel cells, fuel storage and heat management systems.

Moreover, several demonstrator projects on H2 uses for marine and fluvial applications have been launched in the French Region Pays de la Loire by the initiative Mission Hydrogéne. Furthermore, Engie (formerly GDF Suez) is conducting experiments alongside the Dunkerque Urban Community to inject hydrogen into the natural gas supply networks of a new residential neighbourhood within GRHYD demonstration project supported by the French government.

In Greece, there is an autonomous building running on PV, small wind turbines and hydrogen on the National Technical University of Athens campus constructed under the H2SuSBuild FP 7 project aimed at developing clean and energy self-sustained building in the vision of integrating H2 economy with renewable energy sources.

In Slovenia, there is a hydrogen filling station of 350 bar in Bled-Lesce, and a container mobile laboratory of co-generation system in Stegne (Ljubljana).

Generally, European Power to Gas Platform created an online queried map with an overall view of the power-to-gas demonstration projects that are currently operational or planned.

Lastly, considering hydrogen refuelling stations, in 2014, there were 36 stations in Europe with another 80 planned for 2015 and 430 by 2020 [

19]. For a more detailed current situation, H2stations.org, supported by Lindle, published online queried maps of all the planned and in operation hydrogen filling stations worldwide.

3.2. Potential Locations of Renewable Hydrogen Storage Systems

Interesting locations might be linked to current and future EU Projects of Common Interest looking at reinforcing electricity networks linked to VRE. Commission Delegated Regulation (EU) 2016/89 of 18 November 2015 amending Regulation (EU) No 347/2013 of the European Parliament and of the Council highlighted the Union list of projects of common interest in European Countries.

According to the survey’s findings, islands are commonly mentioned among preferred locations for the installation of renewable hydrogen storage systems. In this context, STORIES project is aimed to facilitate VRE penetration in islands, through modifications in the legislative and regulatory framework that will help adopt energy storage technologies such as hydrogen. In particular, STORIES findings stated that hydrogen storage is an interesting solution for small-medium islands when VRE penetration has to be increased. It foresees an increase of the number of islands where hydrogen can be exploited when hydrogen technology becomes more affordable.

Furthermore, PRISMI (Promoting RES Integration for Smart Mediterranean Islands) is a recently approved European project, where this paper authors are involved as applicant, aimed at supporting the transition of Mediterranean islands to an autonomous, cleaner, secure, low-carbon energy system—in line with the overall EU Energy Union package and EU2020 Strategy—through the development of an integrated trans-national approach to assess and exploit renewable energy sources including the use of hydrogen for storing energy.

According to Ulleberg study’s conclusions [

17], the autonomous wind/hydrogen system at the island of Utsira demonstrated that it is possible to supply remote area communities with wind power using hydrogen as the energy storage medium. At the same time, he underlined the need of further technical improvements and cost reductions in order compete with existing commercial solutions, such us wind/diesel hybrid power systems.

3.2.1. North—Central Europe

In UK, islands have been selected as preferred locations, especially in west Scotland with a VRE penetration of 40%–50% even if wind power is more valued for power, and has low utilization of electrolyser. In this context, according to experts’ answers, tidal power seems more attractive than wind power to serve island energy storage, as demonstrated in [

20,

21]. The Orkney Islands in Scotland, recently chosen by the EU BIG HIT project for the development of a new European wide hydrogen research, have over 50 MW of installed wind, wave and tidal capacity that produces over 46 GWh per year of renewable power, and has been a net exporter of electricity since 2013. Energy used to produce the hydrogen for BIG HIT will be provided by the community-owned wind turbines on the islands of Shapinsay and Eday, two of the islands in the Orkney archipelago. At present, the Shapinsay and Eday turbines are often “curtailed”, losing on average more than 30% of their annual output, with their electricity output limited by grid capacity restrictions in Orkney. The otherwise curtailed capacity from the locally owned Shapinsay wind turbine will be used to split the component elements of water, by the process of electrolysis, to produce low carbon “green” hydrogen and oxygen using a 1 MW PEM electrolyser. Moreover, in Scotland, close links between intermittent renewable energy generation such as wind, and hydrogen/fuel cell technologies have been established including technology demonstrators in Shetland Islands, Western Isles, and the establishment of the Hydrogen Office at Methil.

According to the elaborated survey, the north of Germany is most relevant for storage of wind hydrogen due to large and growing volumes of “excess” wind power, though the integration of fluctuating renewable energies via hydrogen in the wider energy system is an issue for the whole of Germany, with “excess” solar power being the main form of energy to be dealt with in the south.

The potential locations of renewable hydrogen storage systems in Finland are: Pori, using offshore wind power and LNG systems; Tampere, using bio and renewable energy systems in Eco-Industrial Park; Oulu, using offshore wind power and considering chlor alkali industries in the area; and Helsinki, using renewable energy systems and Cleantech. In Norway, there is a large potential for widespread micro-grid, particularly small-scale hydro power plants with H2 production and storage. Many small-scale hydro power projects initiated by local entrepreneurs are in planning in areas where given certain conditions H2 distribution provides an effective business model, preferred to selling electricity to the grid. However, they are dependent on a clear energy storage and transport fuel policy through incentives from the government’s new energy framework in planning.

In Ukraine, no operating renewable hydrogen storage systems exist, but there are 28 wind farms, 10 of which located on temporarily occupied territories of Crimea and Donbas. Among these areas, according to the survey, the most promising locations from remaining sites are situated near large cities Odessa and Mykolaiv. These preferred locations should be situated close to end-users of hydrogen gas, such as large delivery companies with large fleet of cars, or close to gas pipelines for injecting, or large ports to refuel ships.

In Sweden, according to survey answers, preferred locations on larger scale are close to the wind farms located in the north of the country, which is less densely populated and, consequentially, most of the energy is used in the south but produced in the north. On smaller scale, off-grid places in the mountains or in the archipelagos that currently have diesel-generators could be selected.

In The Netherlands, as reported in the survey with particular regards to a recent study about new form of sustainable use of platforms at sea, more and more oil and gas installations in the North Sea are out-dated and sometimes not at all productive. The dismantling of these platforms would be a costly action, and therefore TNO, in cooperation with Energie Beheer Netherlands, Shell and Siemens, has developed a vision to use the platforms for delivering innovative applications in the offshore industry. Such vision includes working together with the oil and gas companies, the offshore wind sector and other stakeholders to the ambition to reuse the unused infrastructure platforms at sea. This employment could be maintained and sustainable energy would be accelerated. The idea is to make a connection between the oil and gas industry in the North Sea and offshore wind farms. Old platforms and gas fields can be used in innovative ways to save energy.

While the sea extraction of oil and gas is slowing down, the construction of large offshore wind farms will actually increase. Drilling platforms, pipelines and empty gas fields in the North Sea could be redeveloped for sustainable energy supply. One possible solution is to make a connection between the wind farms and the still-producing platforms at sea. The energy of those platforms is now generated by gas turbines, which cause emissions of CO2, nitrogen and sulphur oxides. Therefore, these pollutants and GHG concentrations will be reduced by making use of the renewable energy of the wind turbines at sea. The empty gas fields can be used for the storage of electricity generated by the wind farms. The electricity can be saved by this to be converted into H2 and mixed into the gas lines. Nearly empty gas fields can also generate electricity directly on the platforms, such as gas-to-wire, when there is no wind and some power is required. This allows a reduction of the cost of the electrical networks at sea.

Potential locations emerged from the survey in Poland are along West–East transport corridor as well as the North seashore; in particular, West–East transport corridor is feasible location of transport-related hydrogen storage systems, along already operating regular transport routes, while the North of Poland seems feasible for hybrid systems along with wind farms and batteries.

In Czech Republic, hydrogen regions are planned to be developed in Prague region: Ústecký kraj and near Trutnov (Krkonoše mountains). Additionally, considering hydrogen energy storage from wind farms, preferred locations could be north and west zones, close to the Germany boundaries.

3.2.2. Mediterranean Europe

In Italy, a renewable hydrogen storage system has been built on a small island in the Maddalena National Park called Spargi in a bilateral project between France and Italy called PMIBB. A disused military facility has been requalified, assembling a 7.5 kW PV plant with a micro wind turbine of 1 KW and an electrolyser to store hydrogen when the produced renewable energy is not required in the island. On the other hand, when the electricity demand is higher than the produced energy, a fuel cell will use the storage hydrogen, reconverting it into electricity.

In Greece, all the islands in general, especially the non-interconnected ones, jointly with other isolated areas with no access to the main electricity grid, could host renewable hydrogen storage systems. In particular, “Green Island Ai Stratis” project pinpointed the island of Ai Stratis in Northern Aegean Sea for stationary power applications through hydrogen Internal Combustion Engines.

In Portugal, although no operating renewable hydrogen storage systems currently exist, the survey findings highlighted many potential locations starting from those areas were wind turbines are largely installed: Mainland, Azores, Madeira and Offshore sites.

Lastly, in Slovenia, potential locations are: Velenje and Bled Municipalities, Luka Koper coastal region, Ljubljana Municipality, and Alpine huts.

3.3. Main Characteristics of Preferred Locations and Territorial Contexts

Blending hydrogen into HENG (Hydrogen Enriched Natural gas) and using it into the existing Natural Gas T&D (Transmission and Distribution) networks in Europe offer an important opportunity of storage. As example, according to [

22], the European natural gas grid accounts for more than 2.2 million km of pipelines and about 100,000 million m

3 of natural gas, which corresponds to about 1100 TWh. The International Energy Agency (IEA), assuming a volumetric blend share of 5% hydrogen in the natural gas (NG), estimated a theoretical storage potential of about 15 TWh of hydrogen, i.e., about 9 TWh of electricity output.

Additionally, hydrogen could be produced from building integrated photovoltaics and added to the NG based CHP (combined heat and power) to meet building energy demand [

23,

24], and to increase building environmental friendliness mainly due to the decrease of carbon dioxide specific emissions for NG hydrogen enrichment [

25,

26].

As regards the use of hydrogen for transport sector applications, its low volumetric energy density should be considered; indeed, hydrogen should be compressed to 350–700 bar to achieve a range of 500 Km. This compression needs about 10%–15% of the energy content in the hydrogen [

27]. Higher energy densities could be attained by liquefying it, but, according to [

27], the energy amount required for this process rises to about 30% of its energy content. Further researches dealt with alternative hydrogen storage solutions, such as storage in solid metal hydrides, liquid carbazole and liquid formic acid [

28,

29].

Among the European TEN-T programme, established to support the construction and the upgrade of transport infrastructure across the continent, there is a specific part for hydrogen called HIT (Hydrogen Infrastructure for Transport) that aims at establishing a basic network of European hydrogen refuelling facilities to allow the use of FCEVs across Europe. Since large scale hydrogen transport necessitates appropriate infrastructures provided with specific pipeline materials and safety procedures [

30], and road transportation is disadvantaged for hydrogen low energy density, in some cases, hydrogen is stored by a conversion into chemicals easier to handle and characterized by a higher energy density.

3.3.1. North and Central Europe

Potential use of the storage system in each European country is related to VRE (mainly wind) grid overloads. As example, Stolten et al. [

31] estimated in Germany a 34% of energy oversupply in a future scenario where the 85% of the total energy production will come from VRE. Converting this energy amount into hydrogen means an availability of 5.4 million tons of H

2, which could fuel about 60% of the total vehicles: 28 million passenger vehicles, two million commercial vehicles and 47,000 buses. Storing fluctuating renewable energies via hydrogen and using the energy carrier in the transport sector is economically most attractive, so the provision of hydrogen as fuel for fuel cell vehicles is regarded as the most advantageous application. Industry plans aim at the build-up of 400 hydrogen retail stations across Germany by 2023, many of which will require hydrogen produced with renewable energies.

Norway has a relatively strong central electricity grid, and a growing surplus of renewable energy production, typically between 5 and 15 TWh per year. Apart from small-scale hydro power, there are also about 50 wind power projects in planning throughout the country; most have been granted, but some need Grid improvements before project fulfilment. In those cases, sometimes the grid upgrade and connection costs can be prohibitive and a H2 storage solution seems attractive. Therefore, a new policy scheme is needed to make sure that H2 renewable energy storage solutions will be feasible.

In Sweden, territorial contexts for a renewable hydrogen storage system are where connection to the grid is too expensive, or where the grid cannot be reinforced for other reasons. From a tax perspective, it could be favourable to install energy storage in buildings that have PV systems today, but the prices need to be an order of magnitude less to make this economically feasible.

Additionally, many experts answered this question quoting HyUnder project, which is aimed at assessing the potential, actors and business models of large-scale underground hydrogen storage in Europe starting from electricity produced by VRE plants. According to this project’s findings, salt caverns are the major storage option for hydrogen underground storage, mainly due to the positive experience with full scale storage caverns, their flexibility when operated on a highly cyclical basis, and the low proportion of cushion gas.

The project developed hydrogen underground storage case studies in France, Germany, Romania, Spain, The Netherlands, and the UK. Among these projects, the potential hydrogen supply for different applications and the potential number of caverns, installed electrolyser capacity and related investments have been assessed for five European countries starting from annual surplus electricity, and assuming a 100% conversion to hydrogen (

Table 2).

These findings show that, converting entirely to hydrogen the estimated amount of electricity surplus from VRE, it is possible to fuel a significant number of FCEVs replacing a large share of industrial hydrogen currently produced mainly from natural gas. In any case, as reported in

Table 2, this scenario needs significant multi-billion Euro investments, with installed electrolyser capacities of several GWs.

Equivalent H2 quantity has been estimated assuming 100% conversion to hydrogen, at 66% efficiency, while the number of FCEVs was based on 0.54 kgH2/100 km and 15,000 km per year. The number of caverns have been assessed assuming a mature-market cavern size of 500,000 m3 with a hydrogen net storage capacity of 4 kt; based on simulations of charging/discharging patterns and the hydrogen inventory of the cavern, the required total storage capacity is about 20% of the total amount of hydrogen produced from surplus; cavern construction costs for brown field sites of 60 €/m3, resulting in some 30 million of euros; and, lastly, electrolyser capacity has been estimated based on 2000 full load hours while investment in electrolysis has been assessed assuming 700 €/kWel for electrolysis in 2025 and 500 €/kWel in 2050.

HyUnder project assessed the potential of large-scale underground hydrogen storage starting from an analysis of salt deposit in Europe, investigating and benchmarking the suitability of all potential feasible geologic storage options for high pressure hydrogen storage.

The obtained results highlighted salt caverns as the primary option for underground hydrogen storage, followed by depleted gas fields and then aquifer formations.

Taking into account non-geological location factors such as the access to nearby brine processing facilities for salt or chlorine production, or brine disposal options like the sea, as well as the availability of cheap electricity (e.g., by eliminating grid fees) and access to potential future hydrogen markets, Hyunder findings pinpointed Germany, the Netherlands and the UK as the most suitable countries for hydrogen storage in salt deposits among the six analysed ones.

In particular, six candidate regions were shortlisted in France, while, in Germany, out of 25 caverns scrutinized, six single sites in three regions have been identified as suitable. In The Netherlands, eight locations out of 27 have been identified as potentially suitable for underground hydrogen storage plants assessing that those eight sites offer ample capacity for potential future needs for buffering and storage VRE as hydrogen.

As previously analysed by [

32], four main potential locations for hydrogen underground storage in salt caverns in Romania have been identified by the survey: Ocna Mures, Targu Ocna, Ocnele Mari and Cacica.

Lastly, in the UK, three regions that are currently used for underground gas storage have been pinpointed for addressing early hydrogen markets, underlying that also almost all salt-bearing locations offer potential for hydrogen storage to meet future demand.

3.3.2. Mediterranean Europe

In Italy, according to the national TSO data (Terna), wind energy not supplied for grid overload from 2009 to 2013 reach 1818 GWh in total, which means on average 363 GWh/year. Considering an efficiency of 70%LHV, this amount could be converted in 7620 tons of H2, corresponding to about 0.03%LHV NG (38.1 MJ/Sm3), which means about 51,300 tons of GHG avoided emissions each year (202 KgCO2/MWhNG).

Generally, locations with connections to gas grid, with hydrogen fuel stations or which favour autarkical solutions or industrial processes should be considered. In any case, before installing a renewable hydrogen storage system, climatic conditions of the potential areas have to be monitored in order to have accurate data for estimating the amount of renewable energy producible onsite (mainly solar radiation for photovoltaic, and annual average wind speed and hours of production per year for wind turbines). Then, by uploading accurate data, many software packages can be used for estimating annual electric energy production according to the system typology.

3.4. Maintenance Requirements of a Renewable Hydrogen Storage Plant

Maintenance requirements are similar to Natural Gas storage and require clean up, as stated by UK experts. Developing experience in deployment is just an effort to teach the maintainers and users, recognizing that this is a high energy gas.

From the survey, it emerged that maintenance requirements are not a critical issue for deployment of hydrogen technologies. Indeed, low maintenance is required: essentially change of membranes and filters in PEM electrolyser and fuel cells, which, for small systems, means around 2000 €/year.

Due to the substantial differences between plants, maintenance requirements need to be established with operators of individual plants. For instance, there are differences between maintenance regimes of PEM and alkaline electrolysers (as core components of hydrogen storage plants), with the literature only giving very broad indications on annual maintenance costs. However, Stolzenburg et al. [

33] provided an exemplary discussion of a large wind-hydrogen-system design.

According to Italian experiences, if distilled water is used generically, an electrolyser could work full time without maintenance for at least five years or 40,000 h, while all the maintenance requirements for hydrogen refuelling stations installed in Slovenia are defined by the manufacturer.

Swedish experts underlined that water filters/membranes need to be changed, and regular maintenance of auxiliary pumps and water management. In addition, required maintenance of the high pressure system and, if a compressor is present, it would require maintenance too.

Lastly, many experts did not answer this question, underlying that there was no example of installation of hydrogen storage unit in their countries (i.e., Finland, Portugal, Romania, and Ukraine).

3.5. Regulatory Framework and Governments Outlooks for the Installation and Operation of a Hydrogen Storage Plant

As regards regulatory issues, according to IEA [

34], new approaches to policy and regulation are essential for achieving the full potential of low carbon, demand–response and storage technologies, increasing system flexibility to integrate VRE (variable renewable energy) and improve electricity security. In particular, Nastasi and Lo Basso [

35] have recently investigated storing renewable excess electricity by means of electrolysers to produce hydrogen for contemporary heating and electricity purposes, performing simulations of twenty energy scenarios with changes in renewable energy share and typology of integrated hydrogen technologies.

European Directives and national regulation frameworks should guide technological development and private investments in the deployment of infrastructure for producing hydrogen by renewables, and promoting their reliability to consumers. Indeed, a consistent and clear EU regulatory framework should ensure a substantial cost saving and support a gradual increase in the use of H2 in its different intended uses, as part of the Roadmap to H2 economy.

At European level, the oldest document mentioned by the experts interviewed is the Commission’s White Paper of 28 March 2011 (Roadmap to a Single European Transport Area—Towards a Competitive and Resource Efficient Transport System) called for a reduction in the dependence of transport on oil aims to the development of a sustainable alternative fuels strategy as well as of the appropriate infrastructure. Its general objective is the reduction of 60% in greenhouse gas emissions from transport by 2050, as measured against the 1990 levels.

Currently, hydrogen together with electricity, biofuels, natural gas, and liquefied petroleum gas (LPG) was identified as the principal alternative fuel with a potential for long-term oil substitution, based on the consultation of stakeholders and national experts, as well as the expertise reflected in the Communication from the Commission of 24 January 2013 entitled “Clean Power for Transport: A European alternative fuels strategy”.

Directive 2014/94/EU on the deployment of alternative fuels aims to establish a coherent policy framework that meets the long-term energy needs of all transport modes by building on a comprehensive mix of alternative fuels including hydrogen as well as to support the market development of alternative fuels in a technologically neutral way by removing technical and regulatory barriers.

This Directive requires Member States to adopt national policy frameworks and notify them to the Commission by 18 November 2016, two years after its entry into force.

The elaborated National policy frameworks of each member state should include an assessment of the state and future development of the alternative fuels market, including hydrogen, in the transport sector, as well as national targets, objectives, and supporting measures for the their deployment, including a minimum level of infrastructure to be put in place.

In particular, considering Hydrogen supply for transport (Article 5), those Member States which decide to include hydrogen refueling points accessible to the public in their National policy frameworks shall ensure that an appropriate number of such points are available to guarantee the circulation of hydrogen powered motor vehicles, including fuel cell vehicles, within networks determined by those Member States, by 31 December 2025 at the latest.

In addition, EU Member States should submit to the European Commission by 2019 and every three years, thereafter, a progress report about the implementation of their national frameworks.

As regards the particular situation in EU member states, here below some considerations emerged from the survey:

In Scotland, there is a very favourable government policy for renewable energy and use of hydrogen as part of “whole energy system” approach to energy policy. The Scottish Government has consistently prioritized renewable energies and innovative technologies such storage systems to broadening the challenge of community energy, as reported in the document “Community Energy Policy Statement” published in 2014. In particular, starting from April 2015, it has established a Local Energy Challenge Fund (LECF) of up to £20 million, which offers grant and loan funding for major demonstrator projects providing transformative innovative local energy solutions. In this context, the Scottish Hydrogen and Fuel Cell Association (SHFCA) have strong links with other government policy teams for transport and environment, the enterprise development agencies, the environment agency, local authorities, cities, universities, utilities, and companies involved in hydrogen and fuel cell sector.

As regards safety rules, in UK COMAH (Control of Major Accident Hazards) provided rules about safety of stored energy that should be considered. Moreover, in Sweden, permission to store “dangerous goods” as hydrogen with regard to pressure and other installations are required. To obtain this, a HAZOP (HAZard and Operability) and a What-if analysis needs to be performed. Other regulations are on electricity production and the buying/selling to the grid.

In Ukraine, as there is no example of installation of hydrogen storage unit, the exact procedure related with it is not known. In any case, such installation should be required to conform to rules of exploitation of gas storage systems and all equipment should be certified. EU certification should work in Ukraine as well according to acceptance of EU regulations envisaged by the Association agreement between the EU and Ukraine. According to expert opinions, the Hungarian government is focused on nuclear power and completely neglects all forms of renewable energy and consequentially the use of hydrogen is not included in government strategies.

In Poland, there is an Act of Parliament dated 20 February 2015 concerning renewable energy however there is no direct information/regulation regarding hydrogen storage system included.

In addition, in Greece, Portugal and Romania no regulatory framework regarding the installation and operation of a hydrogen storage plant exists, so it is necessary to obtain a particular permission. In Greece, hydrogen systems fall into the general category of hybrid power systems, for which the Greek current law has been designed mainly for wind-pump hydro power stations. Lastly, considering Austrian regulations, Energie Institut summarized in its website national rules.

3.6. Main Economic Issues of Renewable Hydrogen Storage Systems

With reference to economic aspects, according to IEA [

36], hydrogen from renewable electricity is cost effective if low-cost, surplus electricity is used. In EU4 (France, Italy, Germany and UK) IEA estimated that low-cost, surplus renewable power would be sufficient to supply 30% of the hydrogen used in transport by 2050, assuming that between 3% and 7% of annual renewable power generation is available at prices of around 20 to 30 €/MWh, in a timespan ranging from 1370 to 2140 h of the year, depending on the region.

Experts interviewed generally stated that energy storage plants not only enable a better match of the fluctuating supply of electricity produced by wind or other renewables to the flexible energy demand avoiding grid overloads, but they are also considered as an economic optimization in the electricity market.

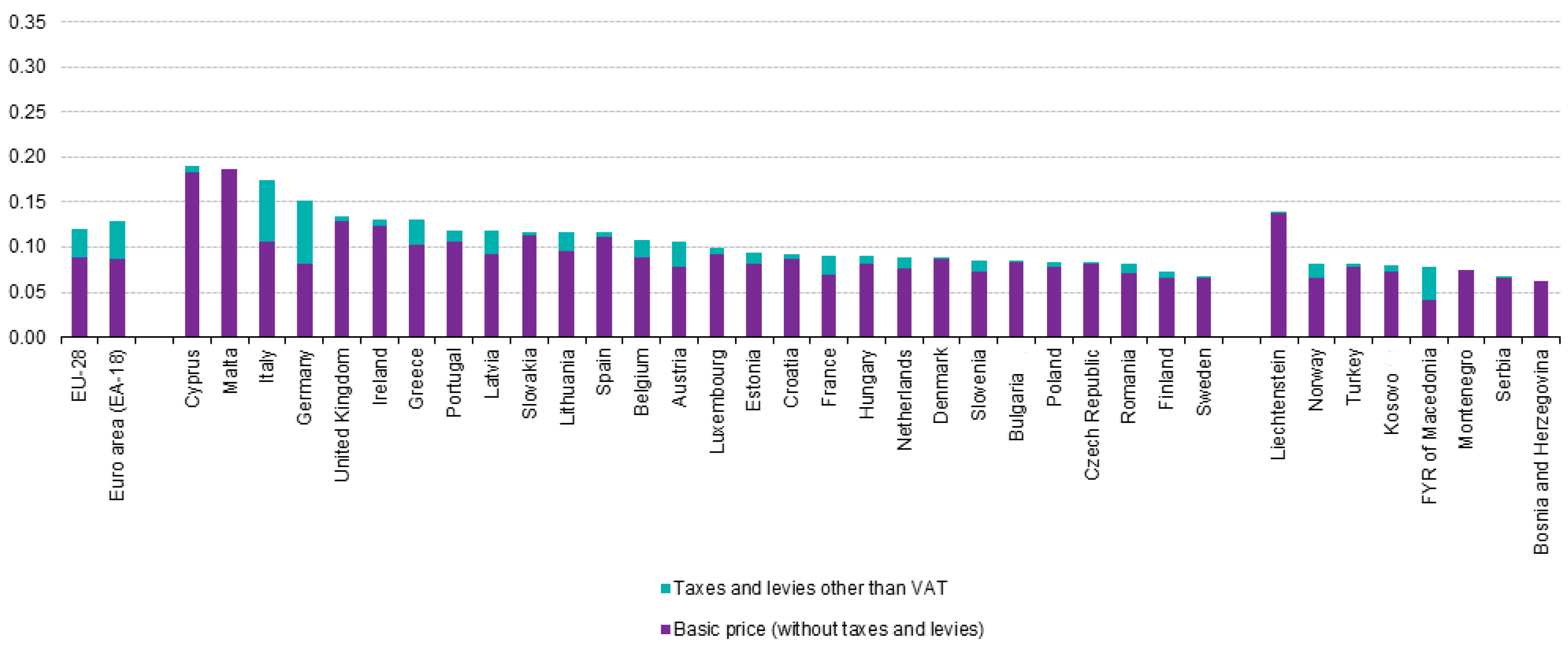

Considering a current natural gas price in Europe of 27 €/MWh, the cost of hydrogen produced from SMR is about 1.6 €/Kg. On the other hand, the cost of hydrogen produced from electrolysis is from two to five times higher [

37], due to the electrolysers costs, as reported in

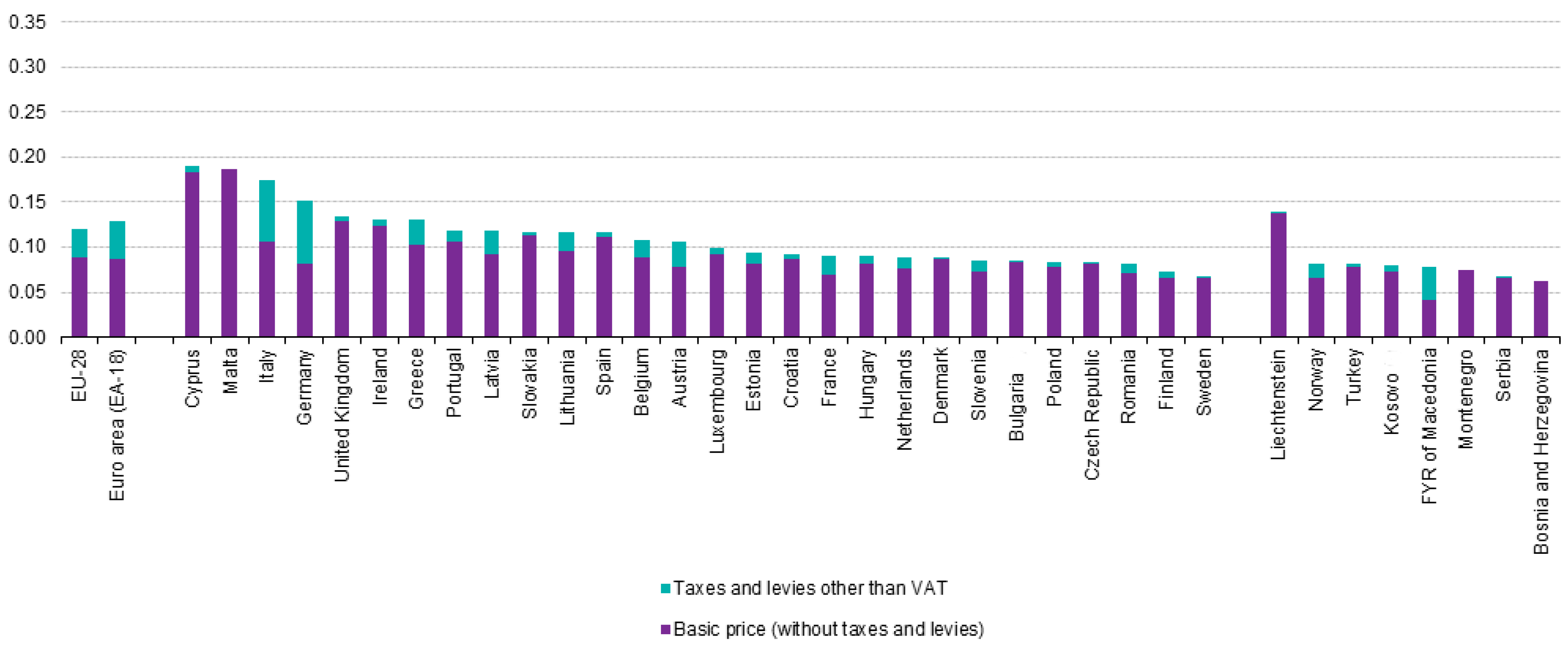

Table 3, as well as for the electric energy prices in European countries for industrial uses assuming a range of consumption among 500 and 2000 MWh/year (

Figure 3).

Actually, current feed in tariffs for renewable energy production guarantee a fixed remuneration per kWh over a defined period. Therefore, the economic balance of hydrogen produced by renewables is one of the crucial aspects that should be overcome using renewable energy when electricity prices are cheaper for overproduction.

Indeed, since the spot market price is related to energy supply and demand, in case of an oversupply of electricity, negative spot market electricity prices occur in many European Countries.

The energy efficiency for hydrogen production is essential to estimate the amount of the renewable energy that could be used by consumers; consequentially, it is a crucial factor for elaborating a business plan to assess economic aspects of the process.

Since electrolysis dominates the total costs and electricity prices, considering hydrogen production by renewables,

Table 3 reports initial investment costs, efficiency lifetime and maturity of alkaline, PEM and SOEC electrolysers starting from IEA data [

22].

Investment costs of

Table 3 do not include H

2 purification and compression systems, but a strong decrease of investments costs due to technological developments and a larger scale production is expected. Investment costs of all electrolysers typology will decrease in the following years: alkaline electrolysis should reach 600 €/kW and PEM electrolysers should reach 800 €/kW [

39]. Previously, in 2007, Zoulias and Lymberopoulos affirmed that the electrolyser cost should be reduced by 40% to increase economic competitiveness of a stand-alone storage system. Operating costs for alkaline electrolysers range from 15 to 50 €/kW per year depending on the plant size, while PEM electrolysers operating costs vary from 30 to 70 €/kW per year.

Considering electricity to electricity conversion, the high investment cost of fuel cells, together with the low efficiency (about 30%) of the technology to produce hydrogen and then re-electrify it on demand, lowers its application.

From an economic analysis of a stand-alone hydrogen energy storage system, Khan and Iqbal stated in 2009 that this kind of system was not favourable for mass deployment but there was the possibility to improve the cost-competitiveness of such a system.

3.6.1. North and Central Europe

Renewable hydrogen in Germany is considered economically more attractive in the transport sector, where it also yields the greatest environmental benefits. Renewable hydrogen can be used both as fuel for fuel cell vehicles and in refinery processes, with remaining legal issues being addressed by regulators. The use of hydrogen in industry and for stationary energy storage is economically less attractive. This is further argued in [

40]. Additionally, Kroniger and Madlener [

41] investigated the economic viability of hydrogen storage for excess electricity produced in wind power plants, analysing two scenarios of a 50 MW wind system in Germany with and without re-electrification unit.

Economic benefits emerged by the experts survey are: load factor increase of the wind farm, producing energy also when the wind farm is disconnected from the grid; temporal arbitrage, producing hydrogen in times of low spot market prices that will be re-electrified in times of high spot market prices; and supply of energy services to the Grid operator in the form of reserve capacity. An economic evaluation was conducted for the first time with real option analysis (ROA) considering the irreversible character of the investment, the risk of fluctuating wind speed, fluctuating spot market price and fluctuating call of minute reserve capacity. Kroniger and Madlener results [

41], elaborated under the 2014 prevailing technical and political boundary conditions in Germany, underlined a higher economic competitiveness in the case of direct marketing of the produced hydrogen from the 50 MW wind energy park under examination. As stated by [

38], hydrogen transportation costs varies between 2 and 3 €/Kg depending on the travel distance.

Additionally, FCEVs, zero-emission cars that run on hydrogen, are at the top of the World Economic Forum (WEF) rankings about the top 10 emerging technologies in 2015. To compile this list, the WEF, with a panel of 18 experts, draws on the collective expertise of the Forum’s communities to identify the most important recent technological trends. By doing so, WEF aims to raise awareness of their potential and contribute to closing the gaps in investment, regulation and public understanding that so often prevent progress. Indeed, the aim is to increase the number of hydrogen distribution infrastructure considering mass-market fuel cell vehicles as an attractive prospect. According to Apak et al. [

42], even if nowadays hydrogen is more expensive than conventional fuels, in the near future its cost per kilometre driven could be more competitive compared to taxed gasoline and diesel fuel in the EU. In Germany, Hydrogen mobility is promoted with the German National Innovation Programme (NIP). A fiscal commitment of €1.4 billion from 2006 to 2016, half provided by the government, and half by the industry.

Hydrogen storage at large scale in UK is a result of cost minimization of capital asset investment. The high mismatch between user demand profiles and wind turbine production means there is no economic case for renewable hydrogen storage systems. In Ukraine, in agreement with the survey results, to be competitive as a vehicle fuel, the cost of hydrogen should not exceed 5.8 €/kg (taking as a reference the price of gasoline in Ukraine 0.83 €/L for 21 April 2016, average fuel economy 7 L/100 km for gasoline cars and 1 kg H2/100 km for FCEVs). The price for electricity from wind farms guaranteed by the government is 0.09 €/kWh. Taking into account that to produce 1 kg of hydrogen by electrolysis it is required 48 kWh, it will cost 4.32 €/kg H2 (capital costs not included). If they can be kept low, the production of renewable hydrogen could be profitable. On the contrary, in Finland, hydrogen energy price is about 8–12 €/kg.

In Finland, Oy Woikoski Ab company is the main significant operator in the hydrogen field and it is active also in the hydrogen infrastructure area.

Given the abundance of easily storable renewable energy in Norway with 98% renewable energy production (hydropower dams throughout the country with over 50 TWh of magazine storage capacity), it is out of the question to store (excess) renewable energy as H2 for further re-electrification back to the grid. Magazine capacity can be regulated to such a precision that electric energy production is optimally managed by the help of the Norwegian Water Resources and Energy Directorate and the state-owned central grid operator Statnett. However, with new environmental policies for the transportation sector under development, it is proposed to demand 100% zero emission vehicle car and vehicle sales from 2025. A complete electrification of the road transport sector is estimated to demand 7 TWh for battery electric vehicles (BEVs), and 20 TWh of hydrogen production for FCEVs. The electric energy prices in Norway have been very low in the last years due to the growing surplus of electric energy, typically 5–6 €-cents per KWh (taxes included). It has newly been proposed by the Norwegian parliament to remove electricity tax for H2 production, to stimulate H2 production for transport fuel. It has been suggested from NEL Hydrogen that given economies of scale, H2 can be sold from large scale production facilities for 4 to 5€ per kg, produced from alkaline electrolysis from hydro power.

In Sweden the prices for fuel cells are still at a level that makes economically feasible installations impossible. Since Sweden has much hydropower, regulating power is abundant. Therefore, when considering energy storage in Sweden, grid reinforcement can always be considered as an option, which is usually cheaper. In addition, pumped hydro could be developed, since it is not used at all in Sweden today and the potential is very large.

3.6.2. Mediterranean Europe

As emerged in the survey, in Italy, Mobilità H2 has recently developed a national plan for hydrogen mobility pinpointing short and mid-term economic and feasibility scenarios that will be published by the end of 2016 with the aim of be adopted by the national policy framework to be presented according to the 2014/94/EU Directive on the deployment of alternative fuels.

Main economic issues highlighted by Austrian experts are: taxes and tariffs on electricity and gas; development of learning curves and economies of scale of investment costs of electrolysis units; and development of power balancing market and development of general electricity price on electricity exchange in Leipzig, the largest city in the federal state of Saxony, Germany.

In Portugal, conforming to the elaborated survey, when wind farm has excess of production, national energy management can send energy to pumping hydro storage in some appropriate dams or export excess energy to Spain. Pumping hydro storage depends on levels of water in dams, but the overall efficiency would be below 50%. In case of exportation the price depends on energy spot MIBEL market. In this context, if a power-to-gas could be available efficiencies between sending and returning energy from energy storage should be tested/calculated.

Greek experts pinpointed that the cost of electrolysers is too high and is not reducing, underlying that it is the main critical factor to integrate VRE and hydrogen storage systems.

Lastly, in Slovenia, VRE in general are sophisticated and expensive technologies that nowadays cannot be successfully implemented without subsidy policies. Therefore, since Slovenia currently has no subsidy policies supporting hydrogen technologies, the deployment slows down.

3.7. Potential Renewable Energy Amount and Hydrogen Storage Benefits

The European energy system is undergoing profound changes following a decarbonisation path towards an increasing growth of renewable energy percentages, starting from 2020 climate and energy package and continuing with 2030 climate and energy framework until the 2050 energy roadmap aimed to reduce GHG emissions by up to 95%. The main aim of those EU strategic plans is a decarbonisation of the energy system avoiding GHG emissions increasing of world’s temperature of 2 °C, as stated during the 21st Conference of Parties held in Paris at the end of 2015. As examples, in May 2016, Portugal ran for four days straight on renewable energy alone and [

8] reported the expected installed wind capacity as a proportion of minimum demand in summer 2020 according to 2015 data (

Figure 4).

Therefore, the increasing renewable power installed in Europe simultaneously needs strategies and actions to face varying electricity demand throughout the day and generation-driven fluctuations. These actions should include a revolution in the energy conversion, storage and distribution technologies. Indeed, the increasing VRE share in EU energy mixes negatively affects the grid and the energy price in peak hours, considering that reinforcement of transmission lines and ancillary services are not sufficiently fast or effective [

43].

The use of excess electricity for producing hydrogen is currently an effective way to facilitate the penetration of huge portions of intermittent renewable sources into the electrical grid reducing VRE curtailment. Only in UK experts assessed that energy curtailment could reach 2.8 TWh per year by 2020 and approximately between 50 and 100 TWh per year by 2050, estimating that storage systems monetary value for this excess energy could be around £10 billion per year by 2050.

Hydrogen from renewable electricity can be used in many applications, such as industrial, mobility, heat supply and electricity generation, absorbing otherwise curtailed wind/solar electricity and operating on a time base that meets load levelling and balancing services aims. In fact, many countries have already put hydrogen and fuel cells among the drivers of their economy for the near future.

Hyunder project estimates energy storage needs assuming a 100% renewable energy power system detailed with 1300 GW from wind and 830 GW from photovoltaic and a 50% “excess” generation assumed, corresponding to 400–480 TWh per year (60% wind, and 40% PV), which means about 10%–15% of annual EU electricity consumption of the last years. That means an H2 storage need of 50 TWh (220 GW) of energy capacity, beyond EU capacity of pumped hydro and compressed air energy storage.

In this context, a flexible energy storage medium like hydrogen can be used for both short- and long-term storage applications as a adaptable intermediate that can be converted to electricity, heat and transport fuel, dealing with the mismatch between energy demands and the intermittent supply.

In particular, the added flexibility of the electrolysis can play a crucial role in the European energy market. The following describes the upside of this type of consumption flexibility:

It should be possible to deliver fast reserve, such as primary and secondary control reserve, from the electrolysis process. These reserve products are the most profitable markets making them interesting for the business case of electrolysis driven hydrogen production.

The fossil fuelled power plants, which currently deliver these reserves, are being phased out, creating a need for new providers of reserve.

The majority of European countries expects the demand for reserves will increase as the share of renewables increases. This again calls for new providers of reserve, and electrolysis could play a role.

Solutions for enhanced frequency control capability are required in many countries. As an example, UK has launched a new tender for enhanced frequency reserve, which is a place where electrolysis can play a role.

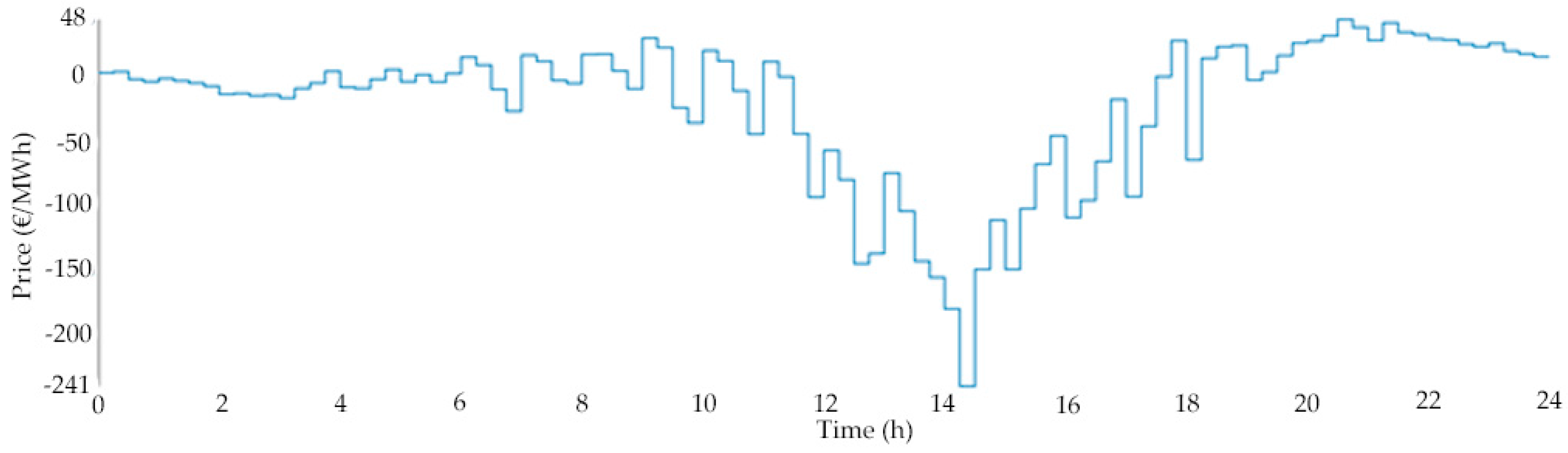

The electricity intraday markets are growing in liquidity. As the share of renewables increase, the electricity prices will lower and the intraday prices might become more volatile. A recent example is 8 May in Germany where the intraday prices dropped to lower than −100 €/MWh for several hours. Such situations are interesting for electricity consumers such as electrolysis as it is possible to receive money for consuming energy.

Figure 5 shows the volume weighted average price in the quarterly continuous intraday spot market on 8 May 2016 in Germany; the lowest price was 241 €/MWh and a total of 12 quarter-hours were below −100 €/MWh.

4. Conclusions

This survey has constructed a comprehensive picture of expert opinion on the current status of renewable hydrogen storage systems in Europe. The results obtained integrating all the information received by the interviewed European experts and stakeholders during the surveys have been used to provide some preliminary strategies for improving the exploitation of hydrogen as an effective energy carrier for storing and more efficiently using renewable energy produced in Europe.

The obtained results show how, and in which particular aspects, regulatory frameworks and economic issues still need to be improved and better detailed in a mid-long-term view in order to facilitate hydrogen investments, projects and markets in European countries, providing an overall view of the European situation as well as country-specific information. The overall results highlighted that, in almost all countries, there is an increasing energy oversupply that could be converted into hydrogen reducing grid overloads.

In particular, the results in this paper provide an overall view of current and potential locations for renewable H2 storage in Europe, giving some specific hints and main characteristics of most countries. Additionally, key maintenance requirements and current regulatory frameworks and government outlooks have been highlighted.

Moreover, the obtained results include an economic analysis and a presentation of economic benefits with feasibility scenarios, underlying that hydrogen storage plants could be considered as an economic optimization in the electricity market. Other emerged economic benefits are a load factor increase of VRE plants, producing hydrogen in times of low spot market prices, as well as a supply of energy service to the grid operator in the form of reserve capacity.

Considering the potential use of H2 storage systems, the infrastructures to generate, store and distribute hydrogen play a key role in creating hydrogen demand markets in the short term. Among these, building renewable hydrogen storage systems is essential since they are built on the use of low carbon hydrogen and the need to store energy.

As regards potential locations of renewable hydrogen storage systems, the survey results pinpointed small islands as preferred locations to facilitate VRE penetration into their energy systems, both in the North Sea and Mediterranean Sea, enabling a better match of the fluctuating supply of electricity locally produced.

Concluding, the overall framework emerged by the research survey highlights that renewable H2 storage systems have different potentialities in terms of end uses and locations in Europe, defining different plans of intervention for each analysed country.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}