1. Introduction

Chile is one of the fastest-growing economies in South America. From 1990 until 2014, Chile’s GDP has more than tripled, which has led to reductions in the poverty levels from 38.6% in 1990 to 7.8% in 2013, reaching an energy access rate of 99% [

1]. However, this ongoing dynamism in the economy and the significant well-being improvement in the population has resulted in a steep increase in energy demand, dragging the power sector into a critical situation due to a lag in the energy supply. Currently, Chile urgently requires dealing with large energy needs for its growing economy in a continuous and secure manner. The projection of the National Energy Commission (CNE) of Chile shows that with energy consumption increasing at the current average annual growth rate of 6%, implying that the country needs to double its energy capacity by adding an approximately 15,000 MW additional installed capacity by 2030 [

2], making it more dependent on external sources. In addition, even though Chile is a minor contributor to global CO

2 emissions (0.2%), the existing upward trend in the CO

2 growth rate—a 110% increases between years 1990 and 2011—has raised environmental concerns [

1].

As a result, the government has increasingly recognized the importance of deploying the potential of Renewable Energy Sources (RESs) and now identifies them as an opportunity to address energy security and fulfill environmental goals. Due to several geographic characteristics, Chile has highly favorable conditions for the deployment of renewable energy generating plants, which was critical in the decision of the Chilean government to include renewables as part of the solution to meet its energy needs. At a glance, the country appears as the promised land for renewable energy developers: large amounts of primary resources and a growing demand with high-energy prices. In addition, it is worth mentioning that Chile has very low tariffs for imported technology, reaching zero in most cases due to free trade agreements, and prides itself on having an open and transparent economy. However, despite the favorable conditions and the government goals, several obstacles still exist preventing the implementation of renewable projects on even more significant numbers. As a matter of fact, renewable energy projects with environmental approval reached 20,780 MW in 2014, but less than 10% of the capacity of these projects (2050 MW) has materialized to date [

3]. It is then difficult to clearly understand why renewables do not seem to take off in the country as planned and there must be some barriers slowing and stopping the advancement of renewables. The focus of this paper is to contribute to the identification and description of the barriers to the development of renewable energy projects in Chile.

The discussion of barriers to RES deployment is certainly an important issue given the fact that most nations now strive to achieve higher shares of RES generation. While much has been said in this respect about existing barriers in the context of various countries, mostly developed ones, no related studies have been done about Chile. Even though barriers for the development and deployment of renewable energies might be quite situation specific in any given region or country, we believe that the identification of barriers from investors’ perspectives in Chile and the discussion of their specific characteristics compared to other international experiences could provide valuable contributions to the literature and to other emerging economies. One reason for this is that there are some potential barriers that are specific to Chile and have not discussed in the literature. For example, the role of mining concessions on land where there is a significant potential for some renewable energies and the type of regulation for grid connection.

The methodology utilized in our study is based on a questionnaire survey (comprising quantitative and qualitative data collection) and a series of semi-structured interviews (qualitative data collection only). Personal interviews were conducted with various renewable energy developers to find out their perspective on the barriers to the diffusion of Renewable Energy Technologies (RETs). The rest of the paper is organized as follows:

Section 2 provides a literature review on barriers to RES deployment.

Section 3 describes RETs in Chile and their status;

Section 4 outlines the research methodology;

Section 5 presents results and discussions; and finally,

Section 6 concludes the paper.

3. Renewables—Potential and Status in Chile

Historically, until the 1990s, electricity generation in Chile was 70%–80% based on hydro sources [

29]. However, in the first decade of the century, recurring and severe droughts and growing demand obliged the Chilean government to search for external foreign fossil energy sources. The discovery of cheap natural gas resources in the neighboring country of Argentina during the late 90s, allowed the Chilean government to reach a long-term supply agreement with the Argentinean Government and direct almost all energy investments in building new gas infrastructure networks with Argentina [

30]. The low cost of imported natural gas made combined-cycle plants more attractive compared to large hydro plants and coal. Consequently, traditional energy sources such as hydro and coal plants decreased their investments in the energy matrix and were replaced by combined-cycle gas plants. From 1995 to 2001, natural gas consumption from Argentina increased fourfold accounting for nearly 80% of Chile’s total natural gas consumption [

31]. However, since 2004, due to the introduction of price regulations that created significant domestic gas shortages in Argentina, gas exports to Chile were practically halted, forcing generators to replace gas-fired electricity plants with more expensive diesel and LNG sources.

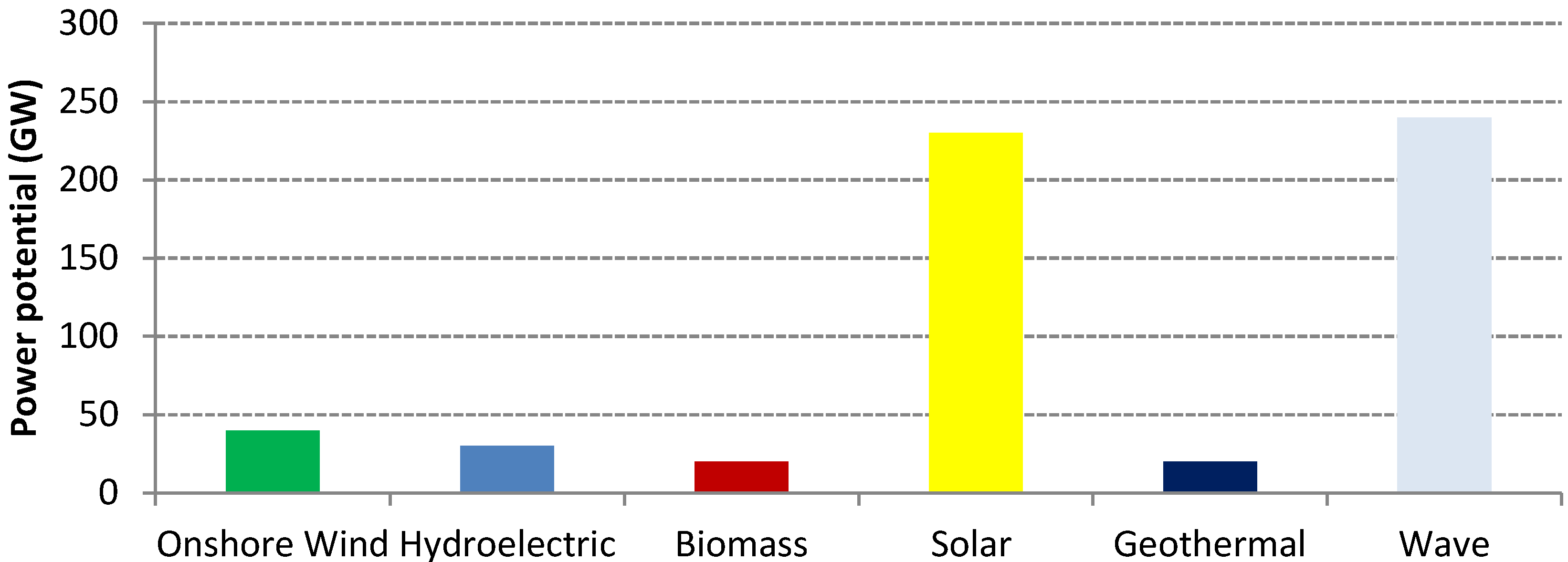

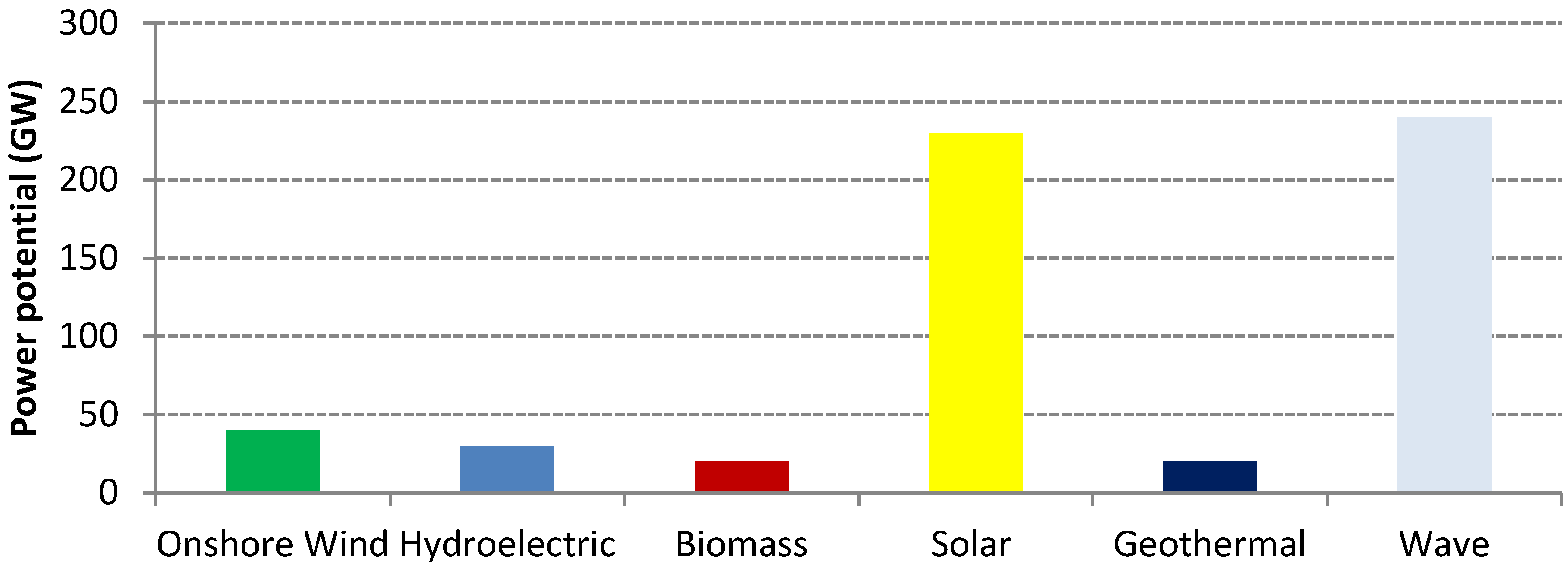

As a result of an increasing energy demand, the rising costs of fossil fuel prices, the reductions in the available capacity of hydro-plants, and some environmental concerns, the government started slowly considering renewable energy sources. Chile is considered one of the most attractive countries for the development of RES, mostly because its geographic location and diversity provides abundant renewable energy resources. Particularly, a significant potential in biomass, hydropower, geothermal, solar, wave and wind have not been exploited yet [

32]. There are over 4000 km of coast exposed to consistent and high Pacific swells which might boost wave energy, Southern Chile has significant areas of wind potential, and the Atacama Desert in northern Chile has excellent conditions for solar energy. The estimated potential of renewables in Chile is summarized in

Figure 1.

The formulation of an explicit renewable energy policy in Chile only occurred a few years ago. The separation of RES from conventional sources and technologies in the Chilean energy matrix was introduced for the first time with the approval of Law No. 20257 in 2008 [

33]. The law aimed to promote the generation of electricity from RES, considering for this purpose the following main renewable energy sources: biomass, small hydraulic energy (capacity is less than 20 MW), geothermal energy, solar energy, wind power and marine energy. The original design of the electricity system during the 80s together with the liberal economic tradition in the country, were the major factors considered by the Chilean government to establish a quota-based obligation (Renewable Portfolio Standard or RPS). According to the RPS, generators located in systems with more than 200 MW, need to incorporate a total of 10% of electricity from RES into their energy mix by 2024 [

34]. As a transition period, between 2010 and 2014, generators need to start supplying at least 5% of their production from RES, then this percentage rises gradually by 0.5% each year, to reach 10% in 2024. This obligation is enforced as of January, 2010 for electricity generation by renewable installations. The law also establishes a fine to be paid by generators when their obligations are not met. The fine is approximately 28 US$/MWh and if the incompliance is repeated within the following three years, it raises to 42 US$/MWh [

33]. However, the opinion of several experts is that, although the fine may seem significant compared to the marginal costs in the market, it is still cheaper for some generation companies not to comply with the quota and pay the fine instead of investing in RES [

35]. In a recent modification to the Law No. 20257 [

34], the government increased the promotion of electricity generation by RES in the energy matrix by doubling its renewable-energy target from the previous goal of 10% by 2024 to 20% by 2025. This new target obviously provides an even stronger incentive for the development of the renewable energy industry. To achieve the 20/25 target, a total of around 6500 MW of new renewable capacity should enter to the grid in the next 10 years, which means an average of around 650 MW every year.

Figure 1.

Estimated Potential of RES in Chile. Source: [

34] and the authors’ own elaboration.

Figure 1.

Estimated Potential of RES in Chile. Source: [

34] and the authors’ own elaboration.

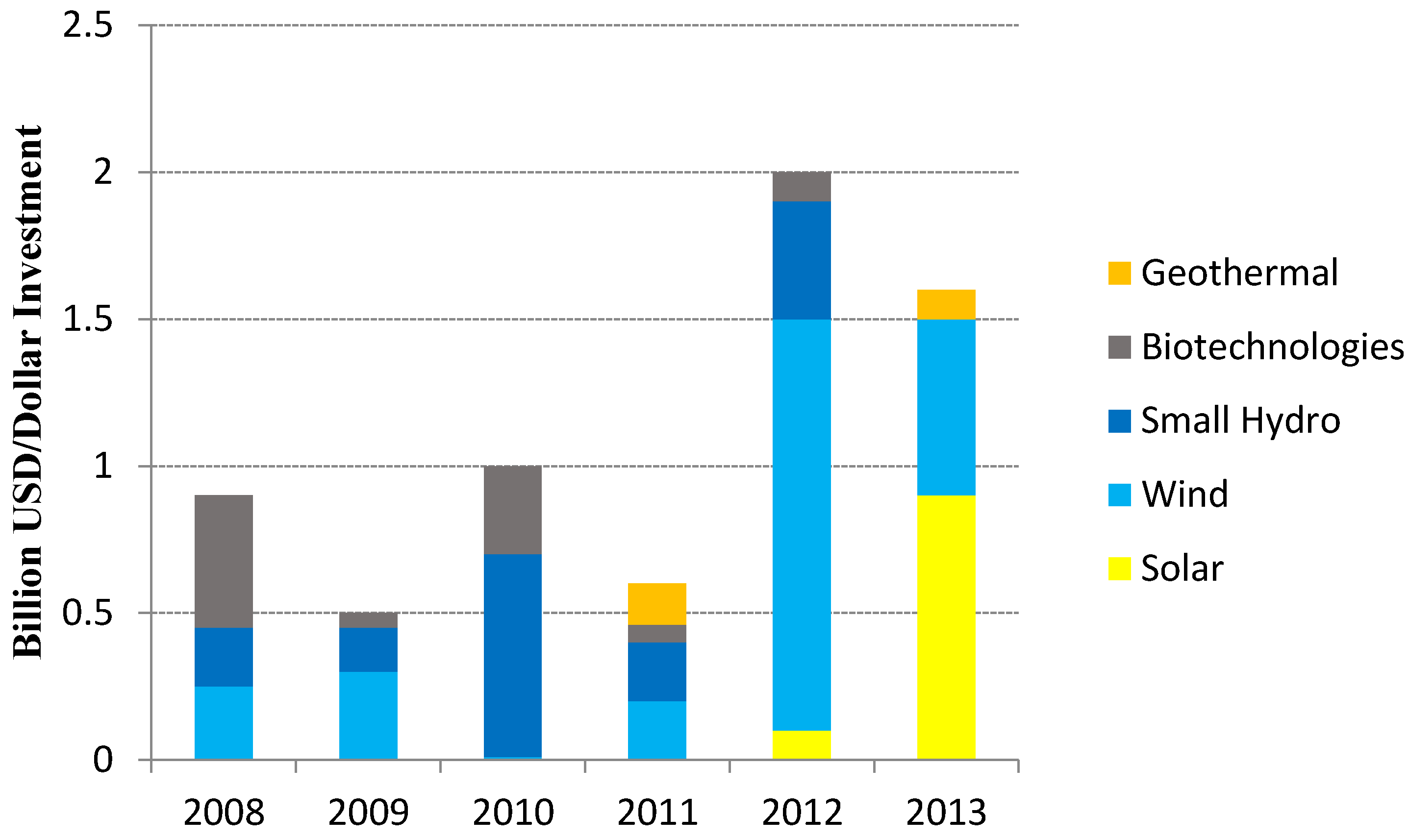

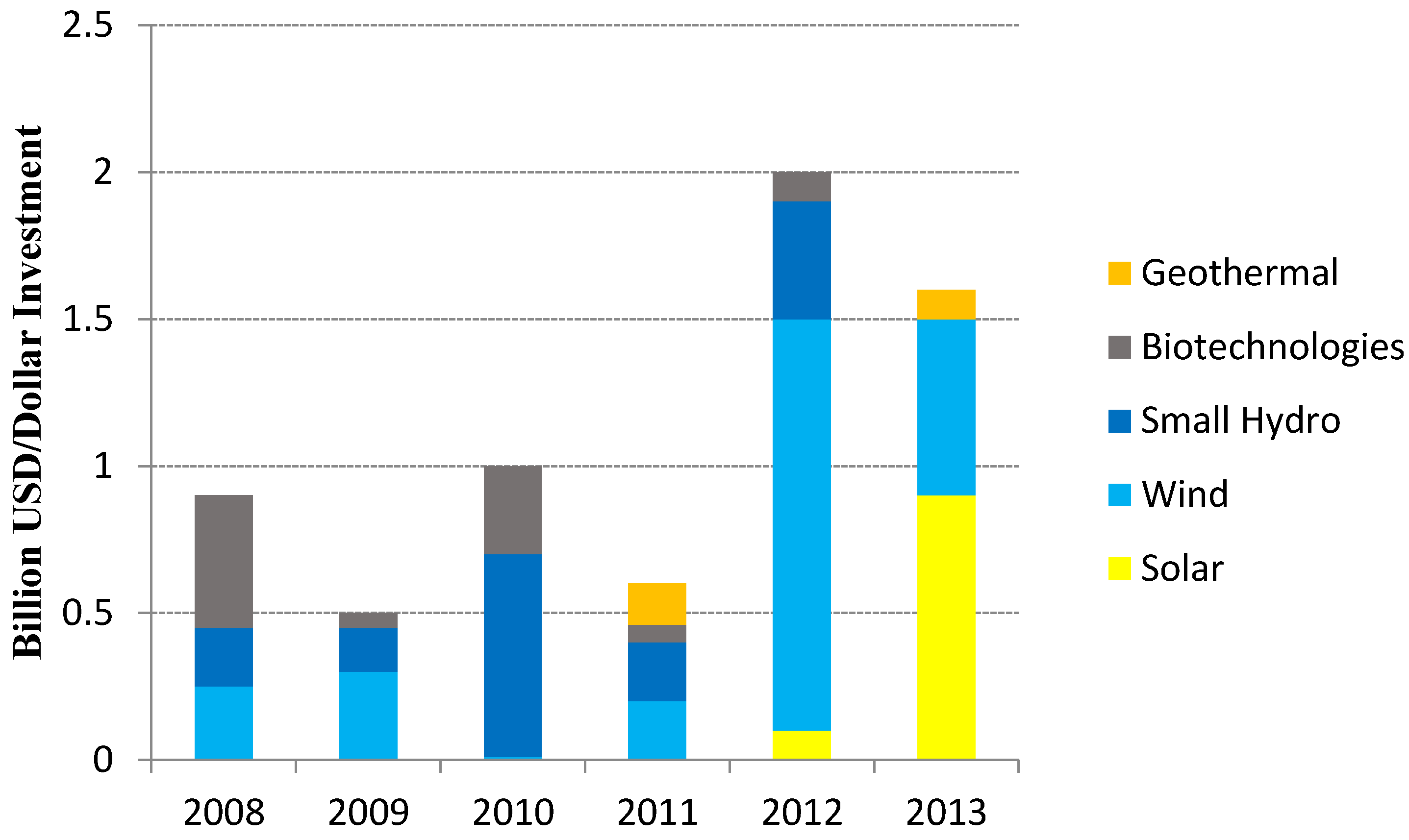

Over the last few years Chile has witnessed significant interest from renewable energy developers looking to expand and diversify their operations in Chile. From the first time with the approval of the Renewable Law, Chile’s renewable sector received an accumulated investment of around $6.7 bn between 2008 and 2013 (See

Figure 2). Most of this investment has been made in wind, small hydro and solar resources.

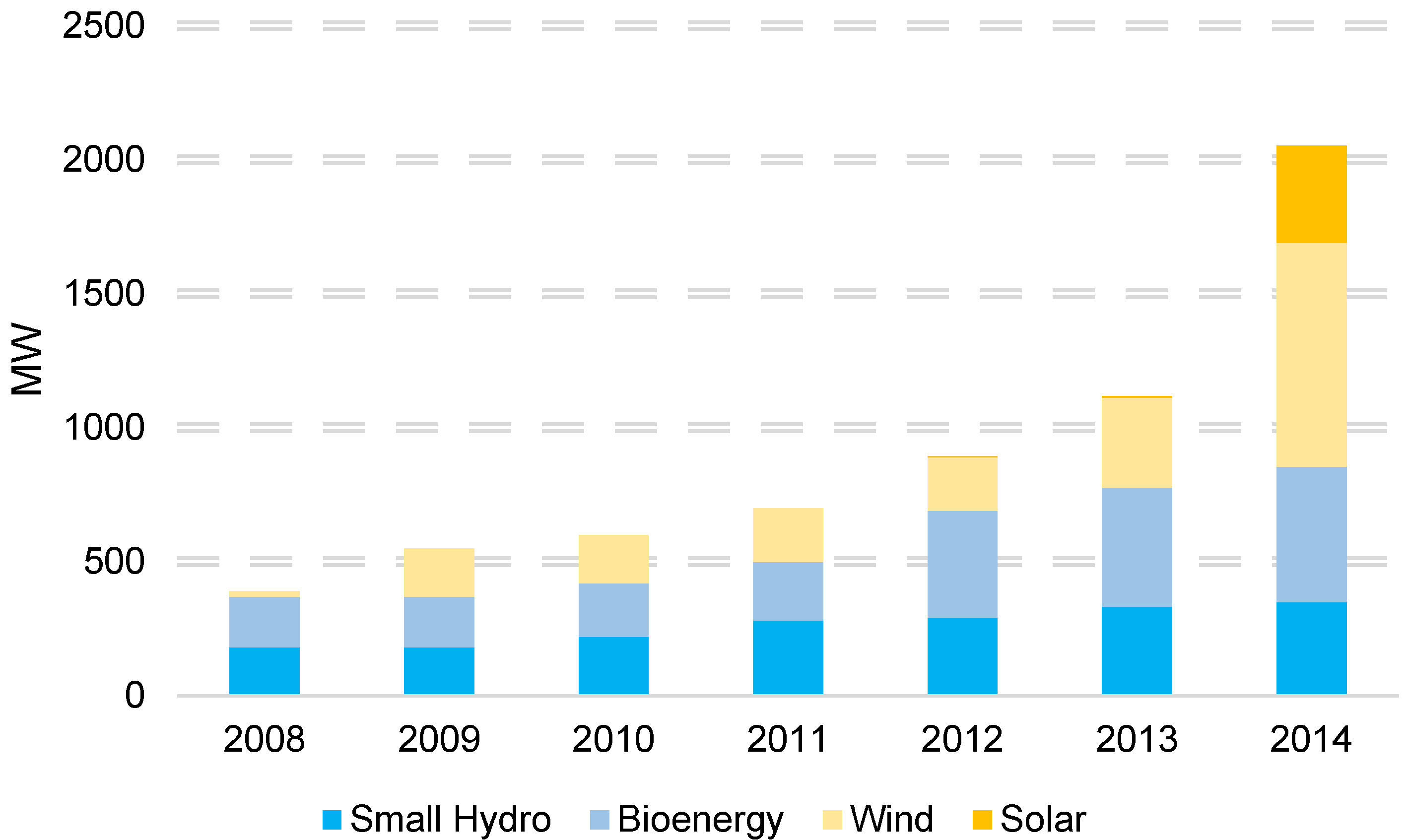

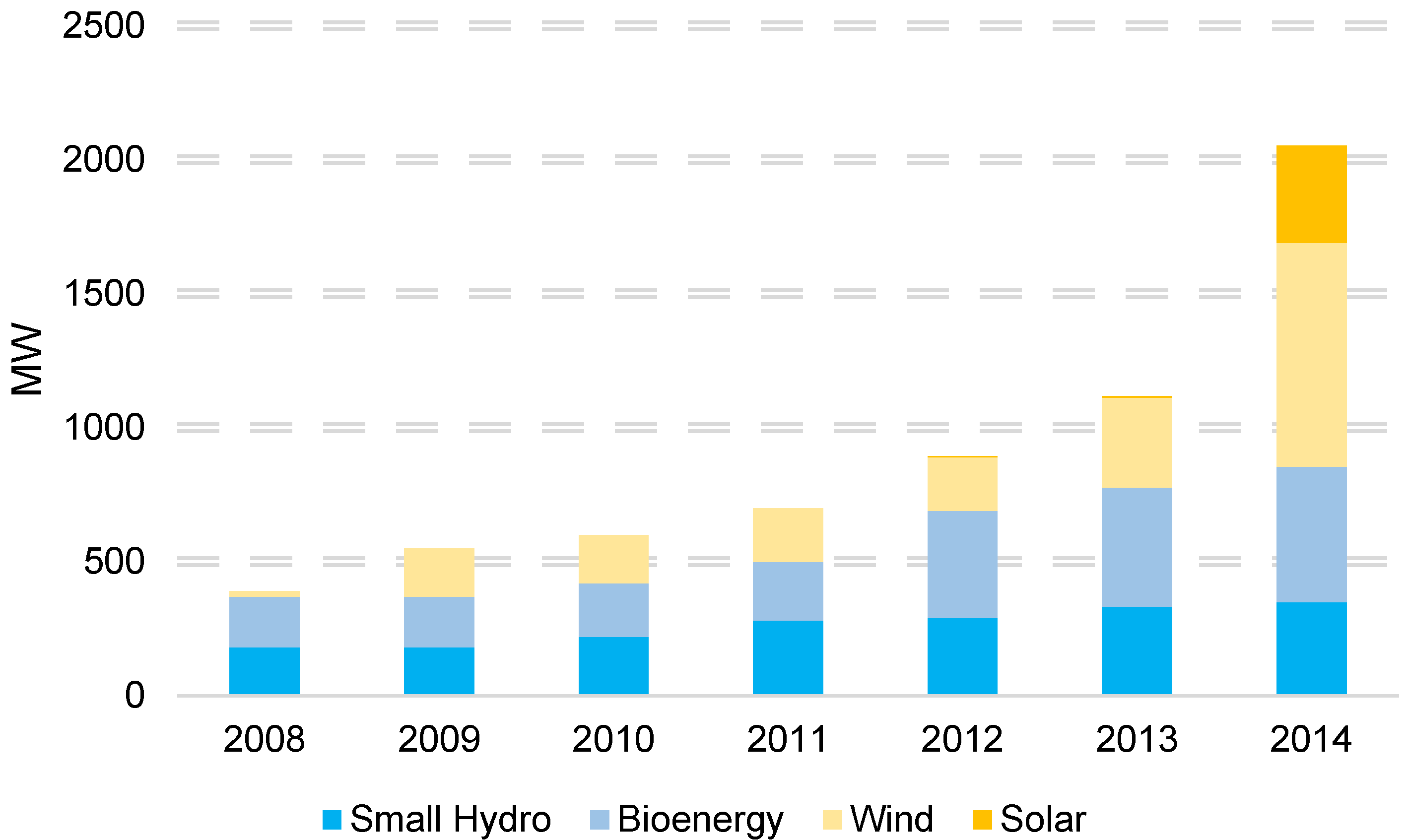

The installed power capacity in renewable energy has also increased greatly from 470 MW in 2008 reaching to 2050 MW in 2014 (see

Figure 3). As of 2014, installed energy capacity from RES has met and even surpassed the defined target. Moreover, renewable installed capacity added 940 MW in 2014 compared to 2013. RES is equivalent to 10% of the total capacity in the whole power system. Wind power leads the RES installed capacity with 840 MW, representing 40% of the share of renewables in the country. The rest of renewable technologies under operation are distributed in 25% biotechnologies (500 MW), 17% small hydro (350 MW) and 18% solar (60 MW).

Figure 2.

Annual renewable energy investments in Chile between 2008 and 2013. Source: [

36].

Figure 2.

Annual renewable energy investments in Chile between 2008 and 2013. Source: [

36].

Figure 3.

Evaluation of RES installed capacity in Chile between 2008 and 2014. Sources: [

34] and the authors’ own elaboration.

Figure 3.

Evaluation of RES installed capacity in Chile between 2008 and 2014. Sources: [

34] and the authors’ own elaboration.

Even though the role and investments in renewable energy projects has increased in Chile over the last few years, its magnitude is small given the large potential the country has. Despite some improvements in the Chilean renewable industry, a serious number of projects under RES are still waiting to enter the market. In particular, renewable energy projects with environmental approval reached 14,500 MW in 2014. However, as can be seen in

Table 1, only 1282 MW are under construction, which raises the question about what the barriers are that prevent the deployment of renewable energy projects in Chile and trying to answer that question is the goal of this paper.

Table 1.

The status of Renewable energy projects in Chile in 2014.

Table 1.

The status of Renewable energy projects in Chile in 2014.

| Technology SIC + SING | Under Construction (MW) | Approved SEIA (MW) |

|---|

| Small Hydro | 134 | 322 |

| Solar PV | 873 | 8,064 |

| Solar CSP | 110 | 760 |

| Biomass | 0 | 96 |

| Biogas | 0 | 1 |

| Wind | 165 | 5,195 |

| Geothermal | 0 | 120 |

| TOTAL: | 1,282 | 14,555 |

4. Research Methodology

The methodology utilized in the paper consists of two complementary methods: a questionnaire survey (comprising quantitative and qualitative data collection) and a series of semi-structured interviews (qualitative data collection only) with renewable project developers in Chile. The methodologies used by Zhang

et al. [

37] and Reddy and Painuly [

38] provided the basis for our survey design. Eleftheriadis and Anagnostopoulou [

39] identified the major barriers faced by solar and wind projects in Greece using a methodology similar to the one used in this paper.

The methodology for a questionnaire survey was split into two phases, which are described in the following subsection. The questionnaire was developed for conducting an online survey of investors’ opinions concerning the barriers to the RETs in Chile. For this purpose, a selection of barriers and market actors were completed first. Then, a preliminary list of barriers was tested in a small pilot study to establish the extent to which the barriers found in the literature are applicable in Chile. This was followed by the implementation of questionnaire survey. Finally, the data collection from the online survey was complemented afterwards by five face-to-face interviews selected from survey. The purpose of these interviews is to provide important insights based on investors` extended opinions and experiences over the barriers they have faced in the marketplace.

4.1. Selection of List of Applicable Barriers in Chile

The findings from the previous section provide very useful insights about observed barriers in various countries. However, it is important to underline that the reported barriers in the literature may be very specific to a country or a region. In other to identify the barriers that are relevant for Chile, we initially considered the most common barriers identified in the international literature and a preliminary list of barriers was tested by a small pilot study to establish the extent to which the barriers found in other countries were applicable in Chile. Opinions and experiences were collected from experts with the goal of characterizing the most critical barriers, whom identified 18 barriers that were all included in the survey (see

Table 2).

Table 2.

Selected barriers to the advancement of renewable energy in Chile.

Table 2.

Selected barriers to the advancement of renewable energy in Chile.

| Category | Number | Barrier |

|---|

| Economic and Financial Barriers | 1 | Market design problems, that obstruct the integration of renewables |

| 2 | High market concentration |

| 3 | Difficulty in Power Purchase Agreement (PPA) negotiations |

| 4 | Unstable prices in the spot market |

| 5 | Longer economic recovery periods |

| 6 | Lack of modeling of externalities |

| 7 | Limited access to financing |

| 8 | High initial investment costs |

| Technological and Infrastructure Barriers | 9 | Grid connection constraints and lack of grid capacity |

| 10 | Inadequate infrastructure to accommodate renewables |

| 11 | Longer processing times for large number of permits |

| 12 | Lack of regulatory framework for land securement |

| 13 | High risk of land speculation due to mining concessions |

| 14 | Lack of coordination among relevant institutions |

| Institutional and Regulatory Barriers | 15 | Lack of political stability |

| Public Awareness and Information barriers | 16 | Local opposition to the development of projects |

| 17 | Lack of dissemination and public awareness |

| 18 | Lack of necessary scientific and technical skills in the workforce |

In particular, the barrier dealing with “unstable prices in the spot market” is a common barrier as there is no dedicated mechanism to place the renewable energy production other than the local spot market. Chile also has significant barriers related to its infrastructure (especially, the transmission infrastructure) because the centralized planning has a limited reach, leaving on private hands the type, amount, and timing of the investment. The lack of maturity of the financial markets regarding renewable technologies creates economic and financial barriers that take a special relevance in the Chilean market. Something similar can be observed regarding the Institutional and Regulatory Barriers as the regulatory energy institutions and the local regulation have not been modernized to accommodate a variety of new technologies. In particular, Chile, as a mining country, has a direct conflict between mining concessions and energy infrastructure deployment. According to the literature review, this barrier is not present in other countries, probably because mining activity only thrives in a handful of countries and where the geographic areas with potential for renewable energies do not coincide with mining areas. Finally, the barriers regarding public awareness and information are rather common with new technologies in countries with an empowered population.

4.2. Identification and Selection of Market Actors

The targeted population for the survey was primarily the group of renewable energy project developers in Chile. A primary reason for this focus was the relatively small number of RET projects that have been deployed to date in Chile, which makes it relevant to perform a robust analysis of investors’ perspectives on barriers to investing.

All respondents were directly involved in the development process of one or more renewable energy projects and were highly familiar with the barriers hindering the adoption in the country of these new technologies. A range of methods was utilized to identify the potential participants for the research. These included:

Utilizing personal networks in industry

Targeting attendees of relevant investment forums and conferences

Approaching specific industry representatives directly

As a result, a total of 128 project representatives were invited to take part in the survey. The representatives were categorized based on the different technologies they were involved with (See

Table 3). The possible technologies include: small hydro, wind, solar, biomass and geothermal. In order to obtain meaningful results, with a confidence interval of 90% and a margin of error of 0.1 [

40], at least 46 responses were required. In the end, a total of 60 project representatives responded the survey.

Table 3 provides a summary of the total invited respondents, required responses to be representative and achieved responses for each technology.

Table 3.

Summary of respondents at the various renewable technologies.

Table 3.

Summary of respondents at the various renewable technologies.

| Technology | Total Actors | Required Minimum Responses | Responses Achieved |

|---|

| Small Hydro | 53 | 18.8 | 23 |

| Wind | 29 | 10.5 | 13 |

| Solar | 29 | 10.5 | 14 |

| Biotechnologies | 13 | 4.6 | 7 |

| Geothermal | 4 | 2.0 | 3 |

| TOTAL: | 128 | 46.4 | 60 |

4.3. Structure of the Questionnaire

The Quota Sampling Method (QSM) was utilized to carry out the descriptive analyses of the survey data. QSM is one of the more rigorous non-probability sampling methods that ensures representativeness by sampling individuals and guarantees to collect necessary information from targeted groups. Essentially it aims to obtain a representative sampling from a not necessarily random selection of individuals, where sampling continues until the quotas are achieved. In our study, individuals correspond to renewable energy investors and developers [

21,

38,

41,

42] who were targeted in the survey as the specific relevant groups [

43]. One of the advantages of using a QSM is that it is considered to be one of the most effective methods to receive a significant rate of responses [

4,

44], given the particular difficulty that involves engaging the investment community for this purpose [

45]. Another advantage of using quota sampling is that, it typically provides sufficient statistical power to detect group differences or to investigate trait or characteristics of a certain subgroup [

46]. Although, QSM has been widely used in a range of research fields, there are several statistical problems inherent in the QSM [

47]. Since QSM draws nonprobability samples from each group under investigation, it does not provide generalizable estimates of the target population or of subgroup differences within the target population and potentially creates complications for statistical inference [

48]. Another problem with the quota method is that it uses proximity selection of subsequent respondent, presenting problems to estimate sampling errors because of the absence of randomness. QSM is the common practice of skipping eligible but absent respondents. This may potentially induce bias, which would be especially problematic if the bias is amplified rather than reduced by a larger sample size.

The questionnaire structure of our study is based on respondents’ opinions on the significance of the different barriers to development of renewables in Chile. At the beginning of the survey, respondents were provided with background information about the aim of the research, the structure of the survey, and the list of the potential barriers. Next, the respondents were requested to rate the relative significance of each barrier on a five-point scale [

4,

37]. In addition, they also had an option to write down their comments and opinions regarding any rated barrier. The rates were from “5”, meaning “extremely important” to them (indicating maximum impact on the development of the technology if the barrier is mitigated), to “1”, meaning “least important” (least impact on the technology). A no-response received a “0” score indicating that the respondent does not consider the given barrier as an obstacle to the development of the renewable project.

Let,

denote the rate given by respondent

to barrier

(as described before, a score from 1 to 5 and

the total number of responders for barrier

. Scores were added across all respondents for a given barrier to calculate its average score:

5. Results and Policy Discussion

The answers to the questionnaire provide useful information about the relative significance of each of the 18 barriers considered, which might guide the priorities in the policies considered by the government to promote the implementation of RES projects.

The mean scores, variance and standard deviation for each of the barriers are summarized in

Table 4. The average score ranges from 4.35 to 2.45, with an overall mean of 3.47, implying that all of these barriers are somehow relevant. The most significant barriers include “Grid connection constraints and lack of grid capacity”, with the highest mean value of 4.35, followed by “Longer processing times for large number of permits” (4.16), “Land and/or water lease securement (3.90), and “Limited access to financing” (3.71). These top-critical barriers will be discussed further in the following sub-sections. The detail discussion of the most critical barriers comes from face-to-face interviews with investors where we gathered data on their extended opinions and experiences over the barriers they have faced. The discussion is complemented by a literature review on identified barriers in other countries, which allows us to compare our results to these studies.

5.1. Grid Connection Constraints and Lack of Grid Capacity

In Chile, the current connection system presents significant limitations, resulting in a complex scenario and long delays for those who wish to invest in renewable generation. The connection procedure to the distribution systems does not make a distinction between renewable and conventional technologies.

Table 4.

Mean scores variance and standard deviation of the barriers in the RES in Chile.

Table 4.

Mean scores variance and standard deviation of the barriers in the RES in Chile.

| Barriers | Number of Responses | Average Score | Ranking | Variance Standard deviation |

|---|

| 1 | 2 | 3 | 4 | 5 |

|---|

| | 1 | 2 | 5 | 13 | 30 | 4.35 | 1 | 0.91 | 0.96 |

- 2.

Longer processing times for large number of permits

| 2 | 0 | 8 | 19 | 22 | 4.16 | 2 | 0.93 | 0.97 |

- 3.

Land and/or Water Lease Securement

| 2 | 6 | 6 | 17 | 19 | 3.90 | 3 | 1.36 | 1.16 |

- 4.

Limited access to financing

| 2 | 4 | 12 | 18 | 12 | 3.71 | 4 | 1.15 | 1.07 |

- 5.

Difficulty in Power Purchase Agreements—PPAs negotiations

| 2 | 4 | 14 | 16 | 12 | 3.67 | 5 | 1.16 | 1.08 |

- 6.

Market design problems in the integration of renewables

| 6 | 0 | 16 | 10 | 15 | 3.60 | 6 | 1.68 | 1.30 |

- 7.

High concentration in the generation market

| 7 | 5 | 7 | 12 | 15 | 3.50 | 7 | 2.08 | 1.44 |

- 8.

High initial investment costs

| 4 | 7 | 12 | 14 | 11 | 3.44 | 8 | 1.53 | 1.24 |

- 9.

Lack of regulatory framework for land securement

| 4 | 7 | 13 | 11 | 12 | 3.43 | 9 | 1.60 | 1.26 |

- 10.

Local opposition to the development of projects

| 2 | 11 | 15 | 12 | 12 | 3.40 | 10 | 1.38 | 1.18 |

- 11.

Unstable prices in the spot market

| 4 | 6 | 16 | 11 | 10 | 3.36 | 11 | 1.45 | 1.21 |

- 12.

Lack of modeling of externalities

| 5 | 10 | 11 | 15 | 11 | 3.33 | 12 | 1.64 | 1.28 |

- 13.

Inadequate infrastructure to accommodate renewables

| 8 | 7 | 7 | 8 | 14 | 3.30 | 13 | 2.31 | 1.52 |

- 14.

Lack of coordination among relevant institutions

| 5 | 10 | 14 | 11 | 12 | 3.29 | 14 | 1.66 | 1.29 |

- 15.

Lack of dissemination and public awareness

| 8 | 4 | 9 | 8 | 9 | 3.16 | 15 | 2.14 | 1.46 |

- 16.

Longer economic recovery periods

| 5 | 9 | 17 | 14 | 6 | 3.14 | 16 | 1.32 | 1.15 |

- 17.

Lack of political stability

| 5 | 8 | 18 | 14 | 4 | 3.08 | 17 | 1.20 | 1.10 |

- 18.

Lack of necessary scientific and technical skills in the workforce

| 12 | 9 | 11 | 5 | 3 | 2.45 | 18 | 1.59 | 1.26 |

Besides, the misalignment between planning and connection timescales is a critical issue experienced by many generators wishing to connect to the distribution systems in the country. In the opinion of interviewees, planning approvals go through long negotiations and can take an unpredictable period of time. The evaluation of the feasibility and profitability of the renewable projects then, depends critically on the distributors and there is little transparency and long delays in the process. All these uncertainties have an impact on the cost and complexity of the connection process and might prevent the implementation of a project, even if it is privately and socially profitable to do it.

Regulation in Chile mandates renewable generators to have a partial exemption for using the trunk transmission system. This exemption is calculated based on the generator size: plants producing less than 9 MW obtain full payment exemption and plants producing between 9 MW and 20 MW are subject to a partial exemption [

31]. However, although the legal framework for the energy sector guaranties open access to any generator, in practice, access requests usually result in significant complications and delays, especially for new entrants. The complications include delays in the application process and excessive procedural requirements. This is mainly explained by a high concentration in the generation market, which creates market power than can be used to prevent entry, and also with vertical integration between some generators and transmission companies in Chile, which creates clear incentives to block the entry of new market participants. In addition, the absence of clarity on how the costs of connecting projects to the grid are shared between developers and grid owners generates additional uncertainty and further delays.

Depending on the wide variety of regulatory designs, electricity system requirements and norms, the grid connectivity concerns vary from country to country and in many cases even from utility to utility. For instance, the UK adopted a regulatory support mechanism (the renewable portfolio standard or RPS) that mandates grid operators to decide independently the optimal transmission capacity needed to economically and effectively distribute electricity generated from RETs [

49]. Since developers do not obtain a special priority grid access, grid connectivity always remained a challenge and it was the cause of delays during several rounds of tenders. However, unlike in Germany, developers are not confronted with the rules and risks like observed in the UK and Chile. This is because under the feed-in tariff regime, the transmission operators have been mandated to provide grid connectivity to the nearest substation. The costs transmission are borne by the transmission system operators and charged to the federal grid agency of Germany [

50].

5.2. Longer Processing Times for Large Number of Permits

Long and complicated bureaucratic procedures to obtain a large number of required permits have also been a major obstacle to the development of RETs in Chile. The process of obtaining permits and their requirements in Chile has a limited legal basis and it is not clearly reflected in any law or official administrative requirement. Although project developers are aware in advance of the required permits for a project, they lack the access to comprehensive information on how to obtain such permits. The existing high level of bureaucracy in the governmental bodies also makes the overall process excessively long and complicated, adding a significant risk to the project during the development phase. Several authorities and different administrative levels within each authority are usually involved in the process. As a result, in most cases, delays may exceed 700 days on average. Among required permits, obtaining the environmental approval by the

Environmental Impact Evaluation System (SEIA) is the most critical one for renewable project developers in Chile. This is related to the structural problems of

SEIA and the uncertainty about the required time needed to obtain them. According to opinions of interviewees, this timespan may vary between 90 and 210 days, depending on the nature of the projects. An extensive and time intensive set of application processes for renewable projects have been widely covered in international literature, such as Mizuno [

51] presented similar experiences in Japan and relative different experiences in the state and municipal level from Australia were studied by Byrnes

et al. [

9]. In comparison to Chile, this procedure alone in various phases of the SEIA takes 570 days in Japan [

51].

5.3. Land and/or Water Lease Securement

The major source of unsolved difficulties comes from the fact that many of the renewable projects (mainly hydro sources) have been submitted for approval to the SEIA in areas that are legally owned or claimed by indigenous communities in Chile, in particular by the Mapuche community. Historically, relations between indigenous communities and the Chilean government have been marked by conflict, primarily because of the expansion of industrial projects on lands that are part of their indigenous territory. Today, a common source of failure in the development of renewable projects, in particular hydroelectric projects in Latin America, is the lack of legal frameworks and adequate consultation with the directly impacted communities. Due to these reasons, various large hydro projects such as Garabí in 2011 in Argentina, Belo Monte project in 2012 in Brazil, and Hidro Aysen in 2014 in Chile, were all suspended [

28]. The absence of compensation mechanisms to the communities, indigenous or not, for the impact of the projects and the lack of basis to ensure that surrounding communities can somehow explicitly benefit from the exploitation of these resources (a lower electricity bill for example), are among the critical reasons for the failure of some projects.

A multitude of barriers related to obtain land securement have also caused the market to move slowly. Major obstacles to obtain the use of land belonging to the state comes from the lack of a land inventory, including a geo referenced map, showing the current status and rights over all territories. Even for this purpose, submitting a request to the Ministry of National Assets can delay a project approximately six months. In the case of private land, the main complications arise if the land has numerous owners and the developer has to separately negotiate with each one of them. The risk of leasing land from third parties for the development of the renewable projects remains also a serious concern as an alternative. This is mainly because obtaining a mining concession for extensive territories is a very simple and fast process in a mining country such as Chile. Given this fact, speculators can request a mining concession with the sole purpose of trying to sell them to developers of energy projects later on. Mining concessions give property rights only to the underground land, which is not required for the installation of an energy project, but in the case of open-pit mines both projects are incompatible. This problem has been also identified in Mexico, which reports similar experiences as in Chile [

52]. Many project developers have had the experience of purchasing land from the legal owner and later discovering that people are living illegally on the land but claim it as their own. Relocating these people has been difficult, expensive and time-consuming.

5.4. Limited Access to Project Financing

Due to the high levels of initial investment required by renewable technologies, access to financing is crucial to the development of projects using such technologies. Financing of renewable projects in Chile is new, developers have to spend a significant amount of time and effort in convincing the local financial institutions that are not familiar with the technologies and find them too risky. Therefore, considering a high risk premium associated to renewable energy in the domestic financial market, project developers face the problem of not being able to obtain funding from financiers or getting more expensive options that might make the project unprofitable. In practice, the financing options for renewable projects in Chile, particularly the role of microfinance sector, is very limited. Financial institutions in Chile are still very immature in the renewable industry and they are unwilling to finance large scale RE projects. To date, only a few projects have been able to obtain loans from local banks.

One of the major obstacles for obtaining local financing is associated with the particular characteristics of Chilean banks, including their conservative culture and a regulation that focus on bank solvency after the 1982 economic crisis, the lack of experience in the evaluation of renewable technologies, and the utilization of the “Project Finance” funding scheme [

53]. High structuring costs of “Project Finance” create an additional obstacle to access to funding. The fixed cost is applied to all projects, independently of their investment requirements, which makes small-scale projects relatively more expensive. Finally, respondents also emphasized the lack of suitable longer-term financial incentives, as government subsidies or tax credits, as a major obstacle for the development of renewable energy sources. Although the Chilean government has introduced several low-interest loans, and also new instruments as guaranties through a government agency CORFO, which is in charge of promoting economic development and innovation, especially in small and medium firms, the respondents agreed that these measures are not sufficient to resolve the problem.

6. Conclusions and Policy Recommendations

Over the last years, a mix of high energy prices resulting from a severe multi-year drought, rising costs of fossil fuels and a steadily increasing energy demand, have put significant pressure on the Chilean economy to start looking into other sources of energy. On other hand, the country is endowed with resources that create an enormous potential for the use of renewable energy. As a result, the government has taken the first steps to significantly increase the role played by renewables in the energy matrix. For this purpose a new law provided an attractive incentive by establishing a renewable-energy target of 20% by 2025. However, the last trends in the development of renewable projects in the country have shown that renewables did not take off as well as planned. The evidence provided from a survey to developers shows that there are a series of barriers slowing and stopping the advancement of renewables.

The paper presents the most important barriers identified from the survey and follow up interviews conducted among the renewable energy developers and investors in Chile. The analysis of the results showed that the top five barriers ranked by the degree of importance given by the interviewees are “grid connection barriers”, “administrative hurdles”, “land and/or water securement problems” and “limited access to project financing”. The analysis of each of these barriers provides valuable references to the Chilean government, contractors and other investors. Mitigating the identified barriers and creating further incentives remains a key challenge for the development of a major renewable energy sector. In this regard, it is clear that the Chilean government should play a key role in establishing additional incentive mechanisms and have a prioritized strategy to eliminate the main barriers that slow or even stop the development of renewable energies in the country.

As far as the need to reach the renewable-energy target of 20% by 2025, electricity grids will have to be upgraded and expanded. In the case of Chile, connecting the two major electric systems (SING in the north and SIC in the central region) that are currently separated would greatly enhance diffusion of RETs. The reason is that the north of Chile possesses excellent renewable power potential, especially for solar energy, and the largest part of the electricity demand—around 75%—is concentrated in the central region. Therefore, the connection between both systems would allow the solar energy sources to reach the demand centers. Australia faces a similar problem due to the remoteness of the solar energy sources and large initial investments are required in transmission to exploit solar energy [

9], but in the case of Chile this can be solved at a much lower cost.

In theory, the construction of transmission lines has significant economies of scale and investments in constructing new transmission lines are considered to be very risky. To address this constraint, establishing coordinated common transmission lines for renewable projects may solve the problem and make the projects feasible. In addition, establishing a comprehensive national transmission planning process, creating standard interconnection procedures, regulating open access to transmission networks, strengthening pricing for transmission, are the most urgent measures to be taken.

With respect to the need for more financial resources and access to funding, the Chilean government must increase the accessible volume of public funding to the sector through different channels. Although the state development agency CORFO’s role in offering financial incentives improves the situation, it is very unlikely that the different programs offered by CORFO become a sufficient mechanism to completely solve the problem in Chile as the resources provided are very limited and mostly target small firms. More capital injection through CORFO could play an active role in addressing these financing gaps through new operational mechanisms and adapted instruments. Besides, the government’s engagements in offering loan guarantees or issuing “green bonds” for local and foreign commercial banks may help to mobilize long-term funding for promotion of renewable sources. Furthermore, as a part of a government policy, it is important to encourage energy-intensive industries in the country, especially the mining industry, to allocate funds for the promotion of technological innovation and renewable pilot projects. As an alternative option, in the initial phase of development, international financial institutions potentially may have also an important role to play in financing clean energy projects and particularly in accelerating market linkages. The investment flow from institutional investors may transmit a good sign of investor confidence and experience to the local banks, which should facilitate the awarding of loans for further projects. Additionally, monetizing positive and negative externalities and ensuring that they are included in energy prices would encourage renewable projects to have a fair competition with conventional sources in the market. This particularly important in the case of diesel, which is taxed at a very low rate given the negative externalities caused by its use [

54], and coal, which is not taxed at all. Given that Chile does not have abundant coal reserves enact the corrective tax could be easier than in countries which face the same barrier but are coal producers like South Africa [

55].

Regarding the streamlining of bureaucratic processes for permits and land and/or water lease securement issues, which is crucial to the deployment of RES systems, there is a compelling need to implement a sound legislation to contribute considerably to the simplification of the processes. Furthermore, a clear and effective assessment methodology for SEIA studies should be established and standardization of all procedures should be implemented such that all licensing authorities would follow the same practices. This would avoid discretionary decisions for approving concessions and would reduce uncertainty for investors. The experience of many countries shows that a key factor in the successful development of a renewable project on territories where communities are against to the project development lies in the direct consultation and negotiations with these communities. In particularly, members of affected communities and the public in general should be given more of a chance to participate throughout the assessment process. It is important to mention however, that in the case of solar energy in Chile this might be a minor barrier compare to other countries, as the solar potential is in large areas of desert where almost nobody lives.

When looking at different options to mitigate the barriers, Chile can benefit from international experiences in implementing, policies that successfully reduce the barriers for renewable energies deployment in many aspects. There are relevant lessons related to technical advances and cost reductions resulting from large-scale market deployments of commercially mature RETs in first-mover countries. In solving some of the problems of grid connectivity, Germany is a good example of a country showing success with its strong and predictable policies and incentives that have spurred similar policy initiatives in many countries [

50]. Moreover, regulatory incentives implemented in Australia have proved to be very effective and also an efficient way of eliminating administrative hurdles [

9]. Finally, well-designed financial support to develop RETs has been fundamental in the success of market leaders, such as Spain, Germany and Japan [

13,

51]. Nevertheless, the application of successfully proven policies in other countries should be carefully adapted to the Chilean market conditions and complemented by rigorous actions to develop and improve the capacity of all local participants involved, including producers, regulators, the public, and the finance community.

Regarding the limitations of this research, it is important to note that the barriers to the implementation of renewables may vary across technologies and, therefore, some further analysis is needed to identify, understand and mitigate the barriers by considering the nature of each technology. It would also be relevant to further explore the role of the main barriers identified in this study, but from the perspective of the government and the financial institutions. Finally, in the case of financial institutions, it would be important to understand the role played in assessing the risk of each renewable project by the type technology, the existing regulation in the electric sector, and the administrative procedures required to implement a project.

{kind=link}

{kind=link}

{kind=link}