1. Introduction

Nuclear waste is generally considered as the most important issue to address in the development of the nuclear energy. Its safe management in the long-term is a challenge for all states, irrespective of their stance on nuclear power use.

As concerns about the sustainability of energy strategies has grown, the European Union took a decisive step by adopting the Radioactive Waste and Spent Fuel Management Directive [

1], that creates a strong EU framework with obligations imposed on all Member States. In practice, however, while solutions to take care of low and medium level radioactive waste are increasingly being implemented, the management of high level waste and used nuclear fuel is still a subject of debate both among the scientific community and the nuclear power states.

The options currently available and operating at an industrial scale are the following two: the “once-through” fuel cycle consists in the storage and disposal of used nuclear fuel elements, considered as high level waste (HLW), in a deep geological repository (DGR). On the other hand, in the “closed cycle”, the used Uranium Oxide (UOx) elements are reprocessed in order to obtain fresh Enriched Reprocessed Uranium (ERU) and mixed oxide (MOX) fuel, which are then recycled in the reactors, while the final waste is stored and disposed of. Regardless of the specific strategy adopted, the final disposal of HLW or used fuel is the ultimate stage of the fuel cycle. While once-through is considered as a “pure” used fuel and waste management strategy, closed cycle has a strong impact on the resources management and “cannot be considered to be exclusively a question of waste management, but more, and depending on the quantity to be reprocessed, as a policy issue of energy supply” [

2].

As a matter of fact, the main advantage of reprocessing used fuel relies in recovering plutonium and uranium, to use them in the fabrication of new fuel elements, which reduces the need for fresh UOx and represents savings on costs at the front end. On the other hand, the opponents to the “closed fuel cycle” claim that the recovery of plutonium involves a risk of proliferation. Even though this article does not aim at discussing this issue but addresses specifically the economics of the fuel cycle in Spain, it is worth saying that on the contrary, in the last decades, recycling has helped reducing the global plutonium inventory in the world, through the burning of MOX fuel in civilian reactors and thanks to programs such as MOX for Peace.

1.1. State of the Art

Several assessments have been carried out in order to compare the two main used fuel strategies both in individual countries and at an international level. The main issue addressed by these studies is the economics of the management of the used fuel. Although Högselius [

3] explains that the nuclear power states decide on a long-term strategy based on five main factors (military ambitions and non-proliferation, technological culture, political culture and civil society, geological conditions and energy policy), most of the studies focus on the economical aspects, trying to figure out the influence of the back-end strategy on the costs of the fuel cycle and of the produced electricity.

In the United States, where the closed cycle was abandoned during the Cold War to avoid the proliferation risks, various studies [

4,

5,

6,

7,

8,

9] have since compared the fuel cycle options to assess this risk, but also sustainability, commercial viability, waste disposal and energy security, in order to evaluate the best option for the future of nuclear power. Among them, the assessment published by the Massachusetts Institute of Technology (MIT) [

6] in 2003 concluded that due to the cost of the disposal of MOX used fuel in the DGR and of new reprocessing facilities required in the closed cycle, in the U.S., the costs of the reprocessing are radically higher than the costs of the once-through cycle. Recktenwald and Deinert [

6] analyzed with a probabilistic approach the costs to build, operate and decommission the facilities that would be required to reprocess and recycle the used fuel produced in one hundred year, showing discounting results in life-cycle costs decreasing as recycling is delayed.

On the other hand, the assessment of the costs carried out by the Koreans Ko and Gao shows that the difference in the fuel cycle costs between recycling strategy and “once-through” strategy is negligible “considering the uncertainty associated with the unit cost of the fuel cycle components. Therefore, other factors such as technological and political risks, environmental effects, public acceptability, and nonsproliferation, could play important roles in determining the future nuclear fuel cycle options.” [

9,

10].

In 2011, an Oxford study analyzed the long-term strategy for the UK’s current and future nuclear fuel and waste stockpiles, comparing storage, disposal and reprocessing, concluding that this last option would maximize the U.K.’s existing assets [

11]. Suchitra and Ramana [

12] assessed the economics of reprocessing in India and the cost of producing plutonium for the fast breeder reactor program. In the case of China, which opted the most recently for reprocessing and is currently building a reprocessing facility, Zhou concludes that recycling can and should be maintained in order to keep up China’s R&D activities from the perspective of the future operation of fast reactors [

13,

14].

Apart from these national approaches, some studies try to determine the cost of both strategies, independently from a specific national situation. One of the most thorough transnational analyses on the subject was carried out by the Nuclear Energy Agency (NEA) for the Organization for Economic Co-operation and Development (OECD) in 1985 (subsequently updated several times, with the last version being issued in 2013) [

15]. The back-end policy of the nuclear countries members of the OCDE was taken in account and compared. In its latest actualization, it shows that “the total fuel cycle costs calculated are lower for the open fuel cycle option, but differences between the options considered are relatively small and within the uncertainty bands. In the recycling options, additional costs from reprocessing are being offset by the savings on fuel costs at the front end”.

In a previous article [

16] published in 2012, the Chair of New Energetic Technologies of the ICAI of Madrid has compared the results obtained from the studies conducted by the OECD, by the MIT, by the Boston Consulting Group (BCG) [

17] in 2006, by De Roo and Parsons [

18] in 2011 and by the Electric Power Research Institute (EPRI) [

19] in 2010.

The methodology followed to evaluate the values presented in the analyzed reports consisted of the comparison of three concepts: the cost of uranium ore, the storage costs in DGR and the cost of reprocessing the spent nuclear fuel.

When it comes to comparing global costs for the back-end, the studies face considerable uncertainties due to the fact that some estimates are made on processes that have yet to be fully developed and implemented, over a period of time in which costs could change and/or be influenced by many factors that are not currently known or quantifiable. Therefore, the results depend considerably on the hypothesis chosen by the authors. However, the Chair has determined that in all the studies, two factors decisively impact the overall cost of each option: the estimated cost of the DGR in the open cycle and the reprocessing costs in the closed cycle.

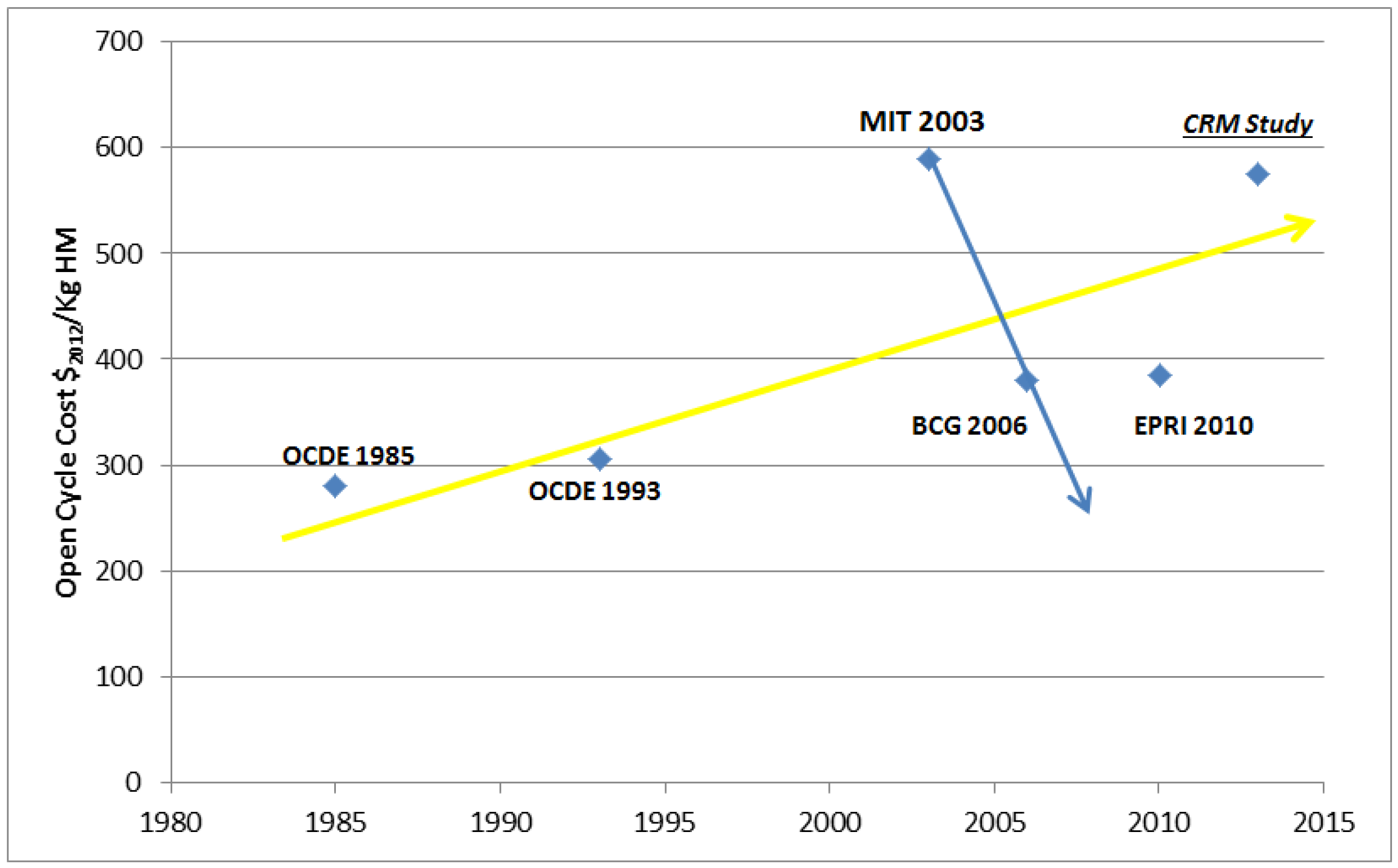

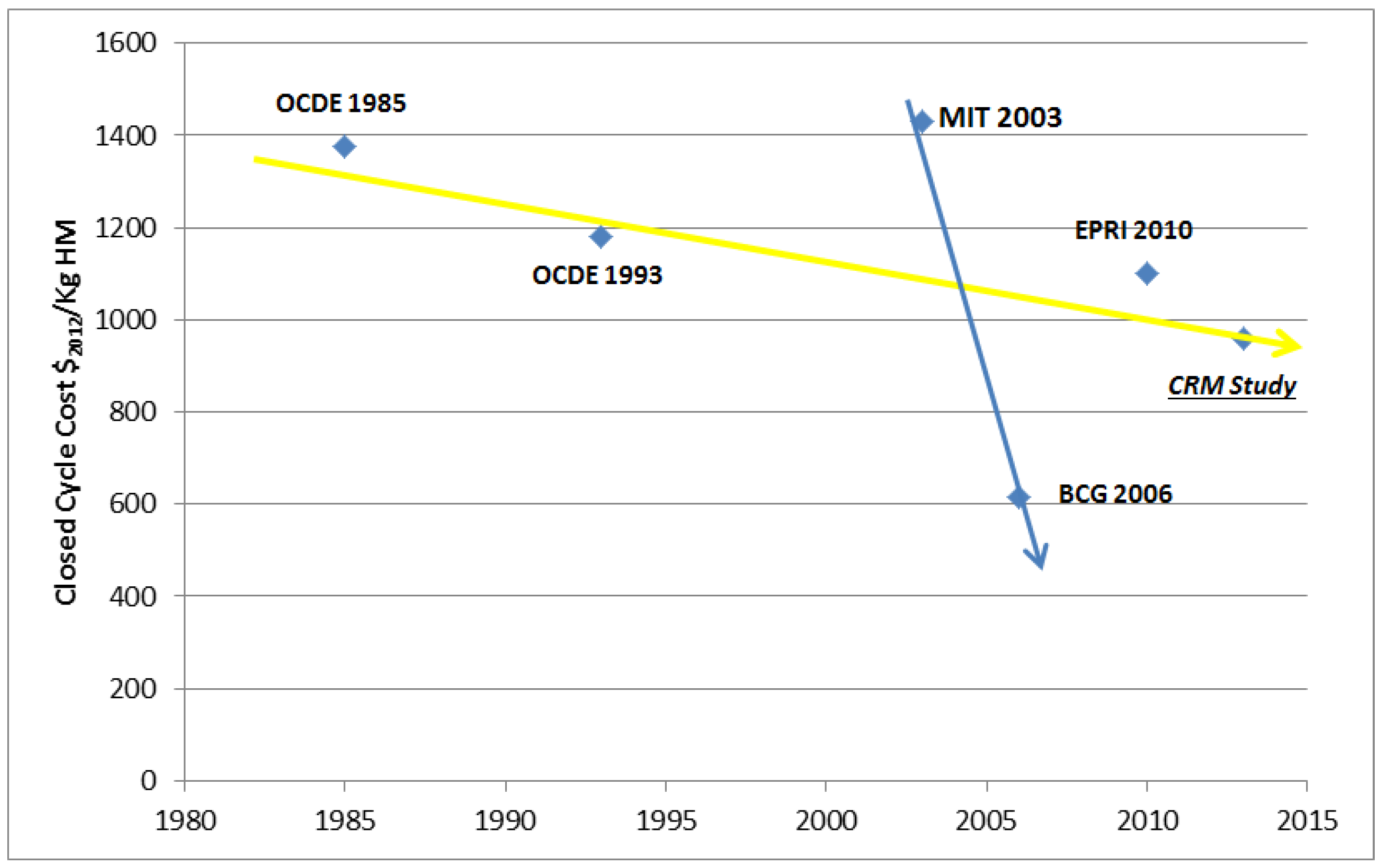

According to the information gathered from all of the reports compared, it is noteworthy that while the costs associated with the DGR increase with time, as shown in

Figure 1, the ones related to the use of reprocessing show a decreasing trend since 1985, except in the MIT and De Roo study (

Figure 2). This may be explained by the fact that whereas reprocessing is a mature technology that is being improved constantly, with experience and R&D resulting in lower prices, to this day there is no DGR operating in the world, and the cost estimates of the most advanced projects (Yucca Mountain in the US, Bure in France, Okiluoto in Finland) are constantly growing, mainly due to difficulties linked with geological, technical, economic and social current and long-term problems.

Figure 1.

Trend analysis of the cost evolution in the open cycle.

Figure 1.

Trend analysis of the cost evolution in the open cycle.

Figure 2.

Trend analysis of the cost evolution in the closed cycle.

Figure 2.

Trend analysis of the cost evolution in the closed cycle.

1.2. The Spanish Situation and New Taxes on Nuclear Used Fuel

Spain is among the large majority of countries that have delayed a decision regarding a fuel management strategy: In the 70s and early 80s some of the used fuel of the Santa Maria de Garoña, José Cabrera and Vandellós-I plants was sent to the United Kingdom and France for reprocessing. Nevertheless, according to the Spanish Radioactive Waste Management Plan in force, Spain’s current strategy consists in a temporary storage of the used fuel, awaiting its final destination, with deposit of the waste in a deep geological repository. Although reprocessing is not excluded, it is nowadays considered as “potential alternative scenario that cannot be considered to be exclusively a question of waste management, but more, and depending on the quantity to be reprocessed, as a policy issue of energy supply” [

2].

Spain is currently building a Centralized Temporary Storage (CTS) or “Almacén Temporal Centralizado” in Spanish, a single facility designed to store, for the next 60 years, all the used fuel generated by the eight operating nuclear power plants during their 40 years of operation.

In 2012 and 2013, the Conservative government created a set of tax measures for an environmental and sustainable energy, including a new tax on the production of used nuclear fuel and a second one on the centralized storage of the used fuel and radioactive waste [

20]:

The tax on the production of used fuel affects the nuclear fuel when it’s extracted from the reactor. It is due per kilogram of heavy metal (HM) generated, at a rate of 2.190 €/kg HM. Each year, it is calculated on the used fuel extracted definitively at each of the Spanish power plants.

The second one [

20], on the centralized storage of used fuel and high level waste, distinguishes between used fuel, and HLW:

- -

Used fuel is taxed per kilogram of heavy metal stored, at a rate of 70 €/kg HM.

- -

HLW will be taxed per cubic meter, at a rate of 30.000 €/m3.

This tax will be applied once, when the fuel or HLW enter the Spanish CTS, independently from its origin, whether it comes from a Spanish power plant or a reprocessing facility. Each year, it is calculated on the difference between the inventory of fuel and HLW in the CTS at the beginning and at the end of the period.

These new taxes will have consequences on the cost of the back-end management. They would affect differently the current open-cycle scenario more than the eventual closed-cycle option, taking into account the fact that in the case of reprocessing the used fuel, the tax on centralized storage would no longer be applied to the content of heavy metal in the stored fuel elements, but rather to vitrified and compacted waste resulting from reprocessed fuel returned to Spain, changing the taxable base and the applicable rate.

Therefore, the Chair of New Energetic Technologies of the ETSI-ICAI of Madrid decided to assess the impact of the new taxes on the economics of the back-end in Spain and to determine if this could have an influence on the choice of one or the other strategy.

2. Methodology

The total cost has been calculated as the combination of management costs and the corresponding tax, according to the new law “Ley de Medidas Fiscales en Materia Medioambiental y Sostenibilidad Energética” (Law of Fiscal Measure on Environmental Material and Sustainable Energy). Both aspects depend on the cycle type, the final waste, and the by-products produced.

The management cost is determined using the method developed by MIT [

7] with the Levelized Cost of Electricity (LCOE) tool. LCOE represents the cost of electricity production in millions of $ per KWh.

The LCOE is determined by analyzing the different phases through which a unit of fuel passes during the entire cycle, considering all the associated costs. In the open cycle, once the fuel is used, it is stored and disposed of, so it is considered as waste. In the closed cycle, the used fuel is sent to be reprocessed. In this case, it is assumed that it would be sent to France, where the reprocessing facility is currently operating.

The economic study has been done using the Discounted Cash Flow Method. The cash flow projections of both, open cycle and closed cycle, should be updated to the same time period to obtain a homogenized and comparable cost.

For the formulation of the normalized cost of electricity generation of both cycles a time frame [

A,

B] that represents the lifetime of the reactor is assumed. The total costs of that period of time, “

t”, are denoted by

Ct and the profile of electricity produced by

Qt, with t ϵ [

A,

B]. The discount rate using continuous compounding is represented by R. Therefore, the levelized cost of electricity is:

The costs taken into account for calculating the management cost of the fuel cycle are divided into “Front-End” and “Back-End” costs. On the one hand, “Front-End” includes the purchase cost of natural uranium, the conversion and mineral enrichment processes, and the fabrication of UOx fuel. On the other hand, the “Back-End” option incorporates the costs in between the removal of the UOx fuel from the reactor’s cooling pool and the final disposal. The costs associated with the operation and maintenance of the reactors have been excluded in all the calculations because we are only interested in the costs that are directly related to the management of nuclear fuel.

In both cases, the study was conducted with a time frame ranging from 2014 to 2028. Furthermore, it should be noted that Spain itself would not carry out either the recycling process or MOx fabrication.

The “Front-End” cost is the same for both alternatives; the difference lies in the “Back-End.” In the case of the open-cycle use consistent style—this or open cycle the costs of transporting and storing the UOx fuel extracted from the reactor are considered, while the closed cycle takes into account the costs of shipping the used UOx fuel to France for reprocessing and the costs of storing the high-level waste from reprocessing.

In the closed cycle, it is assumed that all the UOx fuel stored up until December 2013 and generated annually during the study period will be reprocessed. The same amount of UOx fuel will be sent to France each year between 2018, the first year of fuel shipments, and 2028, the last year of the reference period. The HLW will begin to return to Spain in 2023, five years after the reprocessing of the first used fuel shipment.

In the closed cycle, the management cost has first been calculated under the assumption that Spain will not receive any credit for the sale of reprocessed materials. This assumption constitutes the worst-case scenario. This could be different, as the reprocessed materials can be used in the fabrication of fresh MOX and ERU fuel, so a parametric study on how cost would vary if Spain receives different percentages of the sale price of reprocessed uranium and plutonium was carried out.

The end of the considered period is 2028, because most of the Spanish reactors began operation in 1988, and it has been assumed that they would shut down after 40 years of operation, according to the current practice and the schedule fixed by ENRESA (Empresa Nacional de Residuos Radioactivos), the public Spanish company in charge of used fuel and waste management.

The annual fiscal taxes, standing alone are fixed by the law “Ley de Medidas Fiscales en Materia Medioambiental y Sostenibilidad Energética” [

3] as previously mentioned. The period of analysis is the same as the one considered in the study of management cost (2014–2028). The fuel stored until December 2013 and the prediction of fuel generated by the Spanish nuclear power plants during the period of analysis are included in the cost calculations. The tax rates are shown on

Table 1 and

Table 2.

Table 1.

Taxes rates for open cycle.

Table 1.

Taxes rates for open cycle.

| Rates of different types of taxes for open cycle |

|---|

| Annual discount Rate (%) | 7.6 |

| Used UOx fuel production (k€/tHM) | 2.19 |

| Used UOx fuel storage (k€/tHM) | 0.07 |

Table 2.

Taxes rates for closed cycle.

Table 2.

Taxes rates for closed cycle.

| Rates of different types of taxes for closed cycle |

|---|

| Annual discount Rate (%) | 7.6 |

| Used UOx fuel production (M€/tHM) | 2.19 |

| HLW storage (M€/m3) | 0.03 |

The tax rate for the HLW storage is applied from the year 2023 onward in this study, as it is assumed that the return of the residues to Spain will be delayed until five years after the fuel-reprocessing phase ends due to temporary storage. The total cost is just the sum of management cost and fiscal taxes. Furthermore, to understand the magnitude of this cost and to obtain a more realistic perception of it, the annuity cost is finally calculated using the formula below:

where

CN represents the standard cost,

CRF the control of financial risks, and

CTN the total cycle cost in millions of euros per ton of nuclear fuel.

The CRF is calculated using the following formula:

where

i represents the discount rate, and

N the period of study in years.

3. Results and Discussion

A comparative analysis of the total fuel management cost is carried out for the entire period of study between both alternatives (open and closed cycle). The total cost is calculated for both cases as the product between the unit management cost and the used fuel kilograms each year of this period.

In the base case, which implies not receiving any credit for the reprocessed material sale, the closed cycle is 12% more expensive than the open cycle. The BCG study [

17], after several calculations, concluded that the difference between open and closed cycle costs was around 10%, which is consistent with the results obtained in this study.

Front-end cost is exactly the same in both alternatives. The difference between both cycles resides, in the present economic study, in the back-end cost, because both cycles deal with fuel waste differently through either storage or reprocessing. The high cost of the reprocessing stage is the main cause of the management cost increase in the closed cycle.

As previously noted, these results were obtained assuming no profit in the reprocessed raw materials, which is consistent with the current international plutonium market situation, where the countries that have considered reprocessing, sell reprocessed material at zero profit.

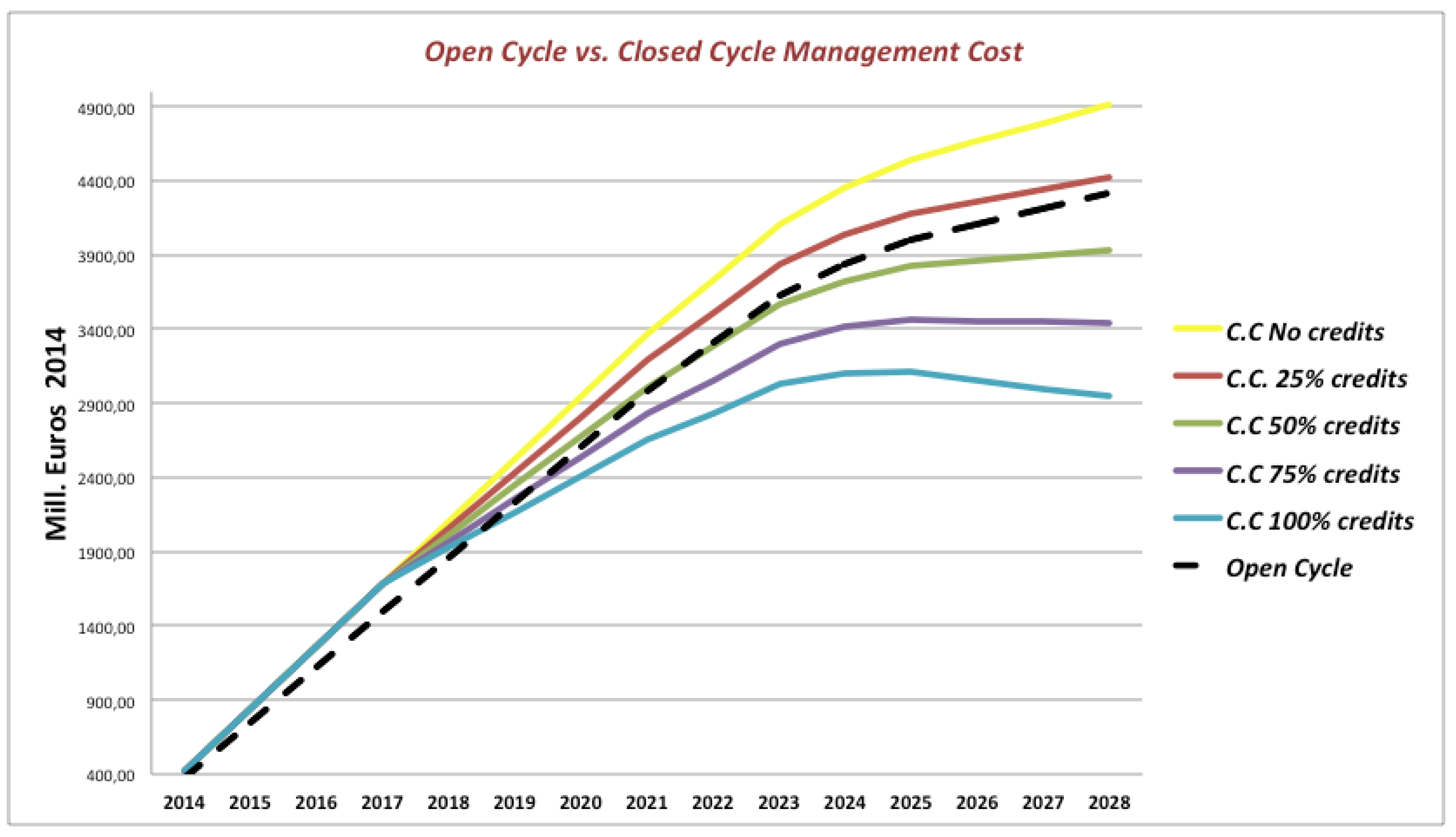

For further analysis, a comparison of the management cost variation in the closed cycle, if Spain received different reprocessed uranium and plutonium selling price percentages (or credits) has been carried out. These different percentages have been estimated in this study and have been finally parameterized at 25%, 50%, 75%, and 100% of the reprocessed materials selling price.

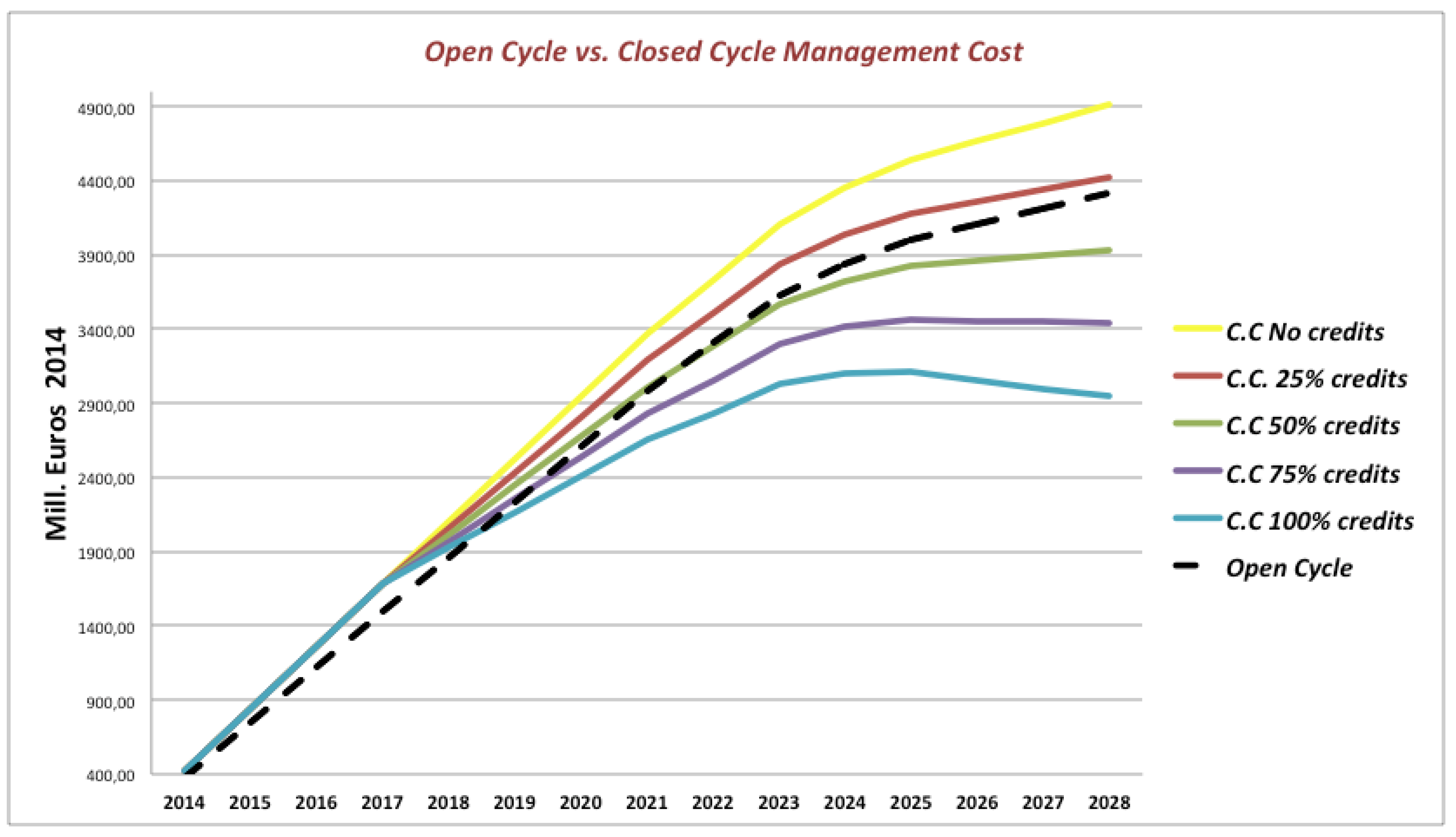

A comparison of management costs between open and closed cycle is presented below. The figure includes the management costs for the closed cycle at the various returned credit percentages stated above (

Figure 3). As observed in the graph, management cost in the closed cycle when no credits are received from the sale of reprocessed materials (yellow line) is higher, specifically 12%, than the open cycle cost (dotted line). If 25% of the credits of the selling price were received (red line), both cycle costs would be practically the same. The closed cycle becomes more economic as the received credit percentage increases, up until the most favorable case, in which all the corresponding credits from the real estimated price of reprocessed materials sale are received. This case would be substantially more economic than the open cycle.

Figure 3.

Comparative economic analysis of the management cost between open cycle and the different hypothesis of the closed cycle for all period of study.

Figure 3.

Comparative economic analysis of the management cost between open cycle and the different hypothesis of the closed cycle for all period of study.

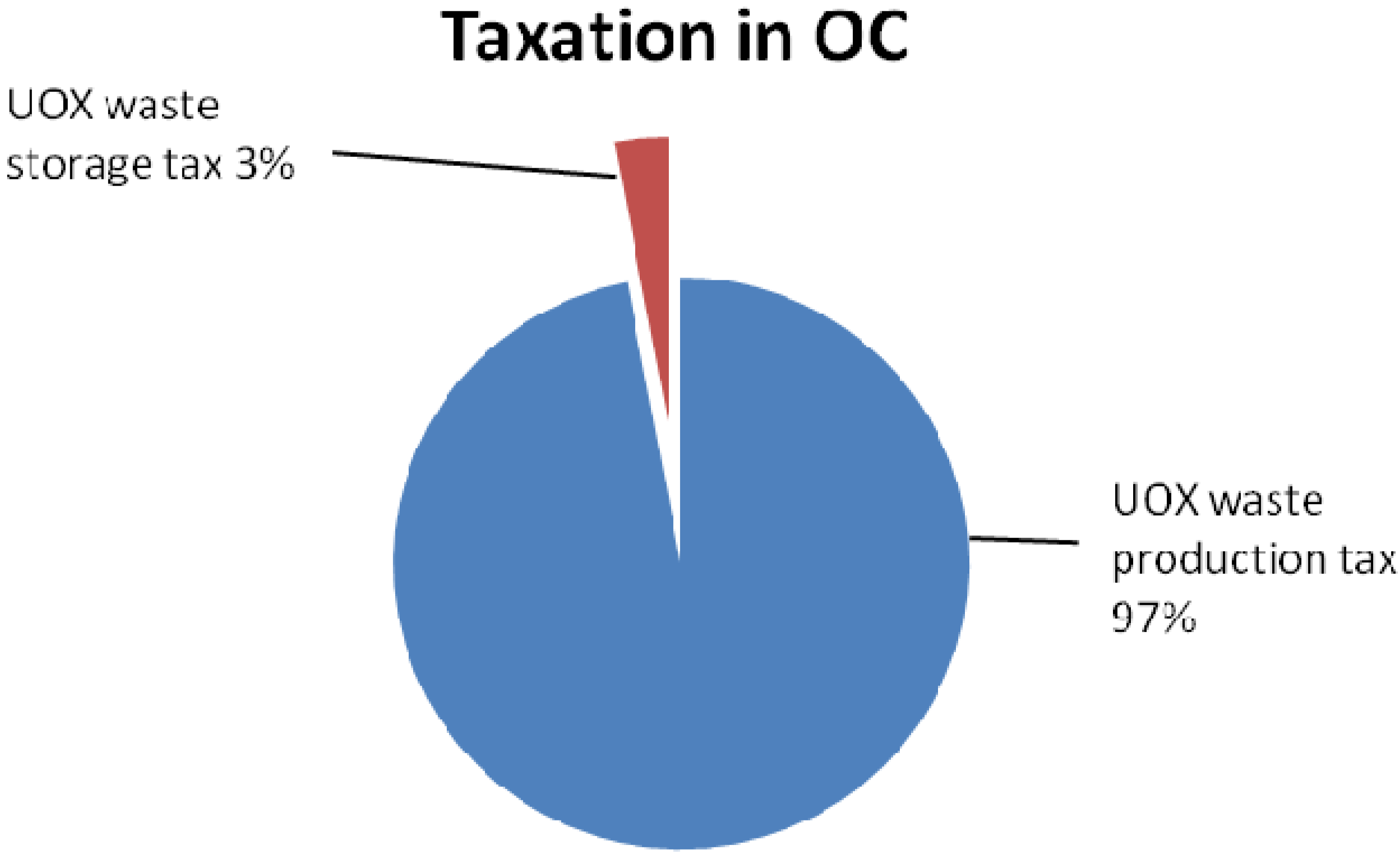

There are two tax rates for the open cycle—one for the fuel waste production at 2190 €

2014/kg

UOx and another for the storage of this fuel waste at 70 €

2014/kg

UOx. For this period of study, the total imposed taxation for production and storage for the open cycle amounts to 3661.2 million € updated to 2014.

Table 3 shows a total cost breakdown for each type of taxation

Table 3.

Taxation in open cycle for all period of study.

Table 3.

Taxation in open cycle for all period of study.

| Taxation in open cycle (M€2014) |

|---|

| UOx waste production tax | 2890.5 M€2014 |

| UOx waste storage tax | 92.39 M€2014 |

| Total | 2982.9 M€2014 |

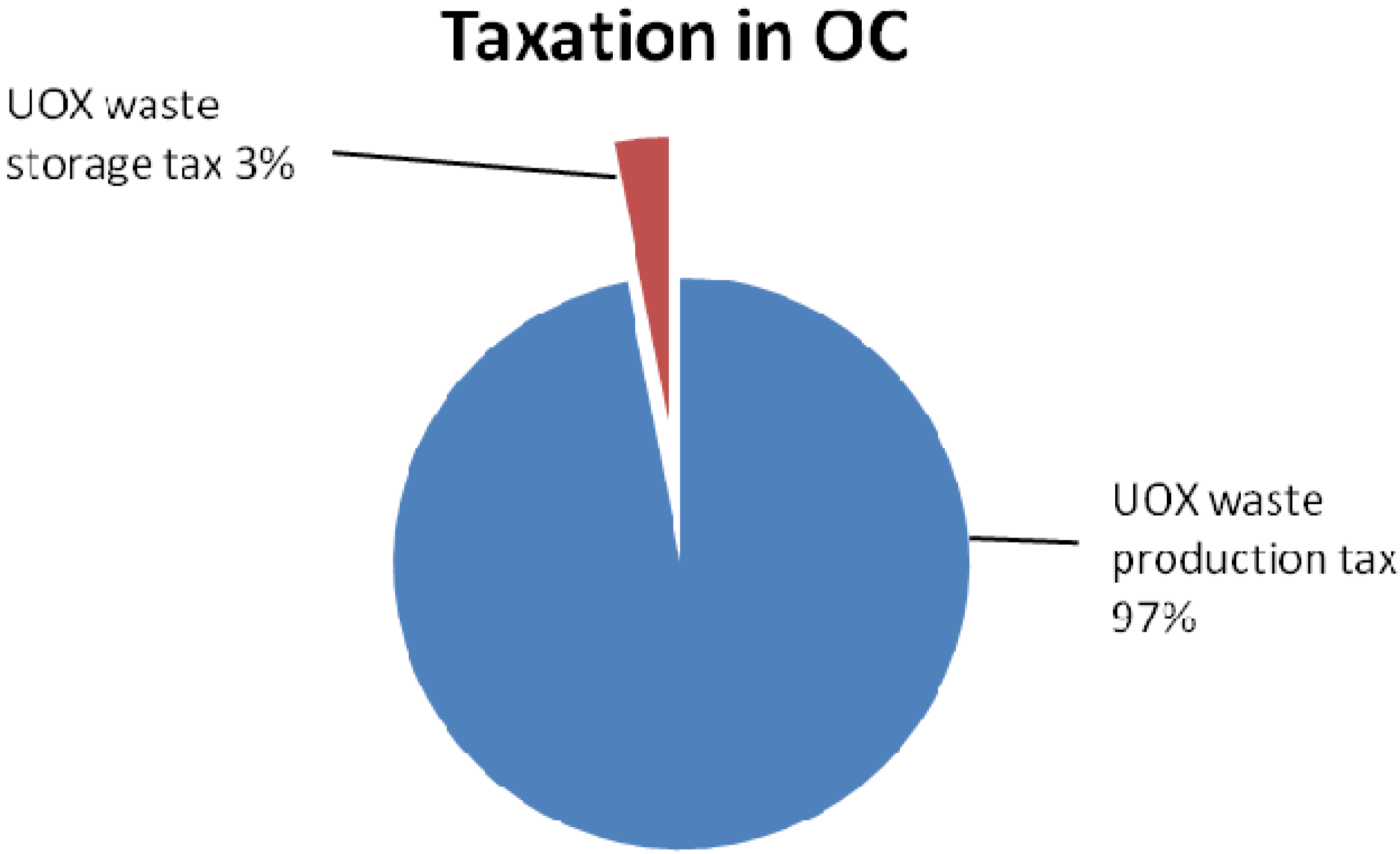

In

Figure 4 each tax distribution with respect to the total taxation is represented.

Figure 4.

Each tax contribution to the total taxation in the open cycle.

Figure 4.

Each tax contribution to the total taxation in the open cycle.

As shown in

Figure 4, the total taxation cost for open cycle is due, almost exclusively, to the nuclear fuel waste production tax for all the period of study.

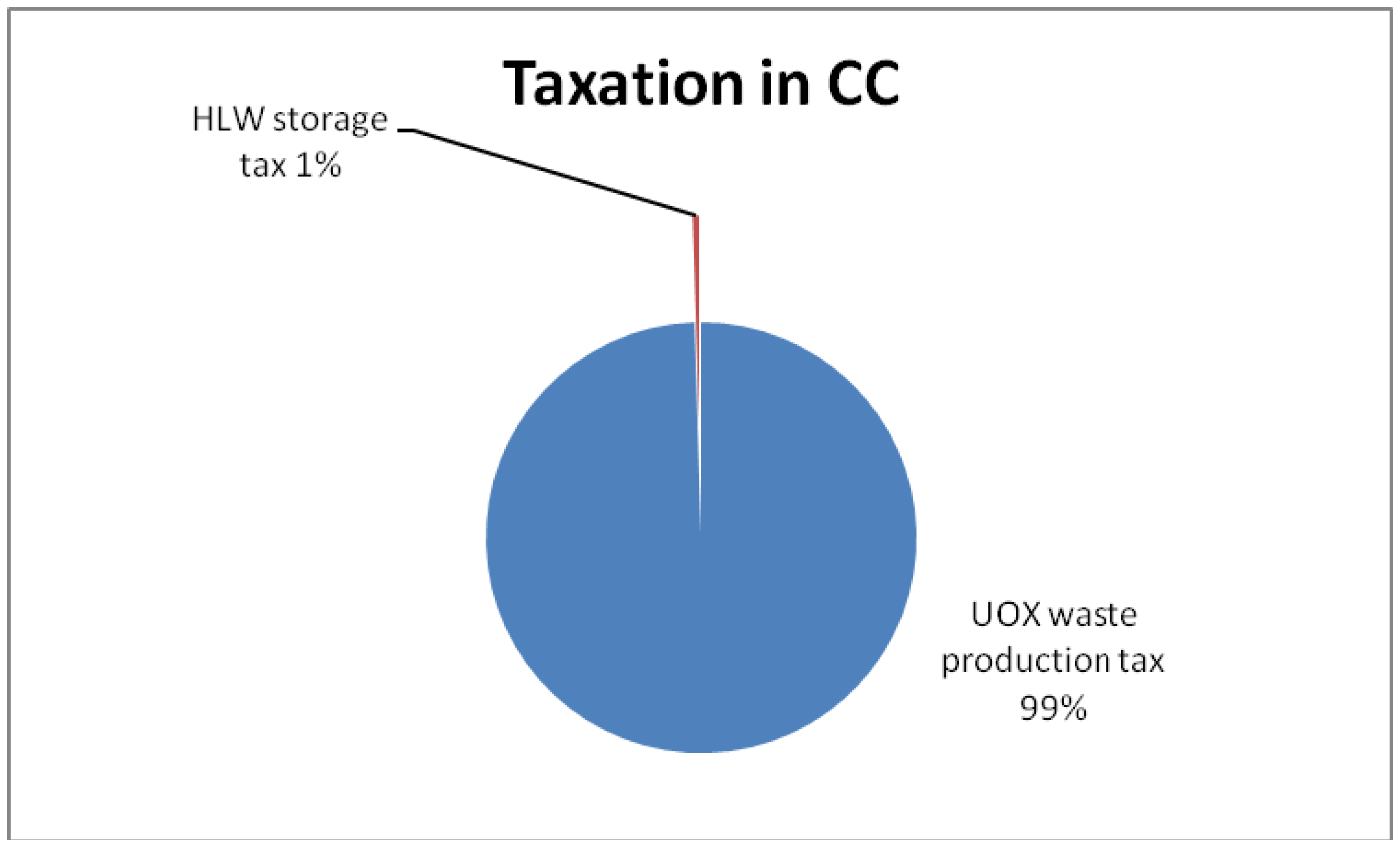

In the case of the closed cycle, two tax rates are also applied. One is a tax on the fuel waste production at a rate of 2190 €

2014/kg

UOx the same as the open cycle. The other is a tax on the high activity vitrified waste from the reprocessing stage, with a total amount of 30,000 €

2014/m

3. In this period of study, from 2014 to 2028, the total imposed taxation cost for production and storage for the closed cycle amounts to 3571.1 million in €

2014. A cost breakdown for each type of taxation is shown in

Table 4.

Table 4.

Taxation in closed cycle for all period of study.

Table 4.

Taxation in closed cycle for all period of study.

| Taxation in Closed Cycle (M€2014) |

|---|

| UOx waste production tax | 2890.5 M€2014 |

| UOx waste storage tax | 14.93 M€2014 |

| Total | 2905.4 M€2014 |

In the closed cycle case, unlike the open cycle case, the fuel legacy up until December 2013 must be taken into account. The assumption made is that the total used fuel accumulated is reprocessed together with the new generated fuel in the period of study. The storage taxation applied to the closed cycle starts being taken into account from year 2023, which is the moment that has been estimated as the one when the vitrified nuclear waste starts to come back to Spain after reprocessing in France, in a constant and equal amount each year.

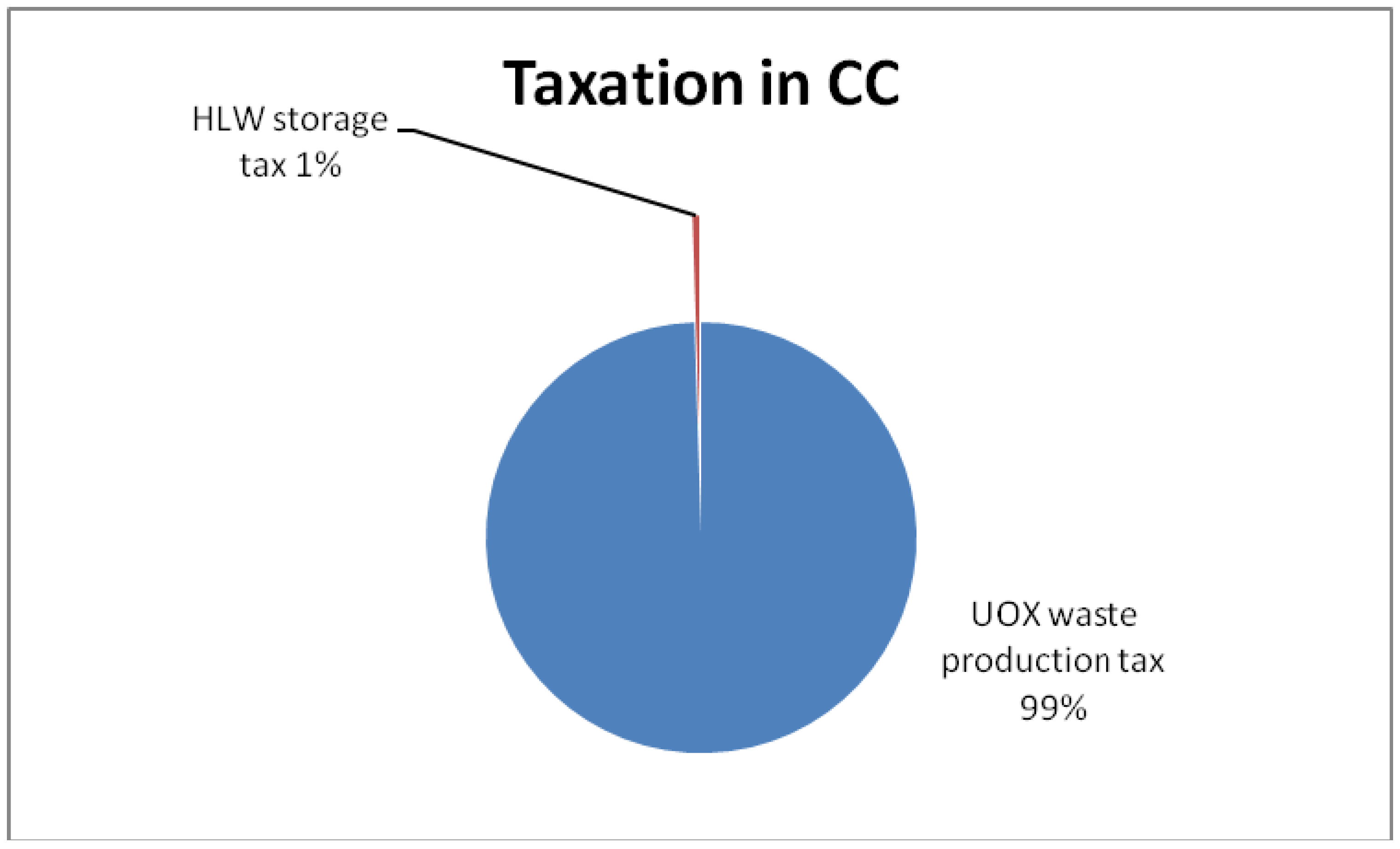

Figure 5 represents the contribution of each tax mentioned to the total taxation.

Figure 5.

Each tax contribution to the total taxation in the closed cycle.

Figure 5.

Each tax contribution to the total taxation in the closed cycle.

For the closed cycle, the storage taxation with respect to the production taxation is further reduced, with storage taxation constituting only 1% of the total taxation of the closed cycle in Spain. The storage tax is clearly insignificant compared to the fuel waste production tax in the closed cycle.

The total cost is defined as the sum of the management cost and the taxes imposed for each type of fuel cycle.

Table 5 collects these results and shows the total cost for each cycle.

Table 5.

Total costs for each alternative through all period of study 2014–2028.

Table 5.

Total costs for each alternative through all period of study 2014–2028.

| Cost | Open cycle | Closed cycle |

|---|

| Management cost (M€2014) | 4320.86 | 4911.16 |

| Total taxes (M€2014) | 2982.89 | 2905.43 |

| Total cost (M€2014) | 7303.75 | 7816.59 |

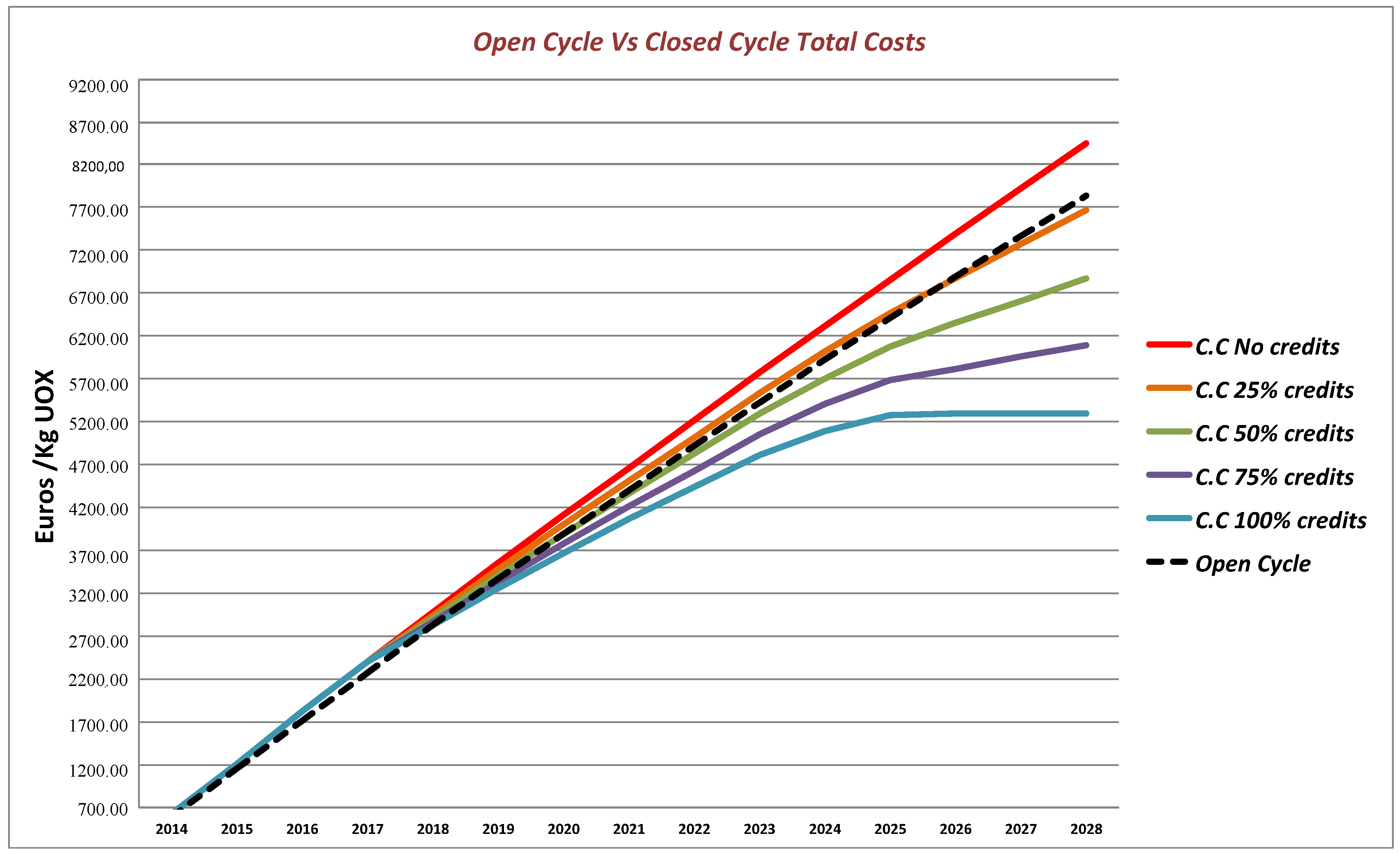

This cost, as explained before, has been calculated assuming that Spain will not receive any credits of the reprocessed material sale, because it is the worst-case scenario and the object of this study. Nevertheless, a parametric analysis of the variation of the total cost, if the material selling price was 25%, 50%, 75% and 100% of the real selling price estimated in this study, has been carried out. A comparison of the open cycle and various selling price percentages of the reprocessed material of the closed cycle is shown in

Figure 6.

The figure shows that the open cycle alternative is more economic than the closed cycle alternative in Spain for the worst-case scenario, in which there are no profits from the reprocessed uranium and plutonium sales. However, the closed cycle becomes more profitable as the credits from the reprocessed uranium and plutonium sales increase toward the most favorable scenario, in which Spain obtains 100% of these credits.

Figure 6.

Comparative analysis of total cost for each alternative for the whole period of study.

Figure 6.

Comparative analysis of total cost for each alternative for the whole period of study.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}