1. Introduction

As one of the most critical issues today, climate change is a challenge all humanity shares [

1]. The primary driver of climate change is the extensive release of greenhouse gases (GHGs), with carbon dioxide emissions being the predominant contributor [

2]. To mitigate carbon dioxide emissions, as of April 2025, 152 countries have proposed a range of climate strategies aiming for “zero carbon” or “carbon neutral” goals (including 48 countries with legislation, 52 countries with policy documents, 12 countries with a declaration/pledge, and 40 countries in discussion (Energy & Climate Intelligence Unit:

https://eciu.net/netzerotracker (accessed on 1 April 2025))).

The formulation or adjustment of policies often affects the decisions and behaviors of investors, thus affecting the market [

3]. This effect continues to flow between markets, showing a trend of risk contagion, often called risk spillover [

4]. In general, markets with high turnover rates, strong liquidity, and wide industry coverage are more likely to become risk transmitters. On the contrary, markets with incomplete mechanisms and relatively small scales are more likely to become risk receivers, which means that the market price of these are more likely to be affected by the previous ones. Due to the information transmission and product transactions throughout financial markets, the phrase “risk spillover” was first used in the financial fields. In addition to the traditional stock markets [

5,

6], scholars have focused more on risk spillovers inside the energy system in recent years [

7,

8]. As the main source of emissions, carbon dioxide emissions from energy account for over 80% of the global carbon dioxide emissions. Hence, the proposal of carbon neutrality targets is bound to affect the energy system, leading to risk contagion among energy-related markets [

9].

Through analyzing and summarizing the existing literature, we found that the risk spillover of fossil fuel markets (FMs), represented by coal, oil, and natural gas, has received widespread attention [

10]. Following closely behind is the carbon market (CM), which was first innovatively proposed in the Kyoto Protocol [

11]. With the gradual extension of the coverage of the “energy industry” and related industries, some scholars have also begun to analyze the spillover effects within the electricity (EMs), green bond (GMs), and renewable energy markets (RMs) [

12,

13,

14]. However, the studies above focus more on the risk spillovers between the same type of markets (within subsystems), while ignoring the risk contagion between different types of markets (across subsystems). Liu et al. [

15] used the DY and BK indices to estimate the volatility spillover between FMs and EMs in Europe. Deng et al. [

16] evaluated the asymmetric connectedness between FMs and China’s GM. Yousaf et al. [

17] proposed a QVAR-based model to analyze the quantile connectedness between FMs and RMs in the United States. Similarly, the cross-market spillover effects between energy subsystems (other than FMs) have also been studied by scholars [

18,

19]. However, no thorough investigation has been conducted on all five aforementioned subsystems, which has caused an incomplete analysis of the sources and subjects of risk spillover in the energy system. Given the evolving energy transition trends, the relationship among these subsystems is getting tighter. Through the joint estimation of risk spillover within all the subsystems above, it can help collectively capture the full complexity of energy systems [

20].

Figure 1 summarizes the literature introduced above.

As matter stands, the studies on the same type of market spillover effects typically examine cross-border/regional effects. However, when studying the spillover effects in different types of markets, most studies have only focused on one specific region (China/Europe/US). Thus, the universality of the proposed models cannot be verified, and the absence of external validation may also limit the results.

In terms of risk measurement, the value at risk (VaR) model is used to measure the maximum potential loss at a certain level of confidence, which is widely adopted in financial fields [

21]. However, the VaR model focuses more on measuring risk and cannot model the risk spillovers between multiple systems or markets. Hence, the extended conditional value at risk (CoVaR) model is further introduced to address the aforementioned issues [

22]. According to the calculation methods, it can be further divided into three types: quantile regression-based CoVaR [

23], copula-based CoVaR [

24], and multivariate GARCH-based CoVaR [

25], which are widely applied in different scenarios depending on their applicability. Of these, the GARCH-based models can reflect the time-varying non-linear risk correlation, and the typical models mainly include the constant conditional correlation–GARCH model (CCC-GARCH) [

26] and the BEKK-GARCH model [

27]. However, the former cannot capture the dynamic correlation between multiple markets, and the economic meaning of the latter model parameters is not clear.

To address the aforementioned issues, we constructed a thorough risk spillover research framework for energy-related systems and conducted empirical analysis around some of the world’s largest energy economies. The contribution and innovation of this paper mainly lie in three aspects.

On the basis of the previous studies, the energy system is divided creatively into five subsystems in this paper, which can help collectively capture the full complexity of energy systems, especially given the evolving energy transition trends. Moreover, we examine risk spillovers between markets, not just within the same subsystem but also between markets across different systems.

This paper concentrates on two major carbon emission and energy consumption entities, China and Europe, which can view the issue of risk spillovers in energy systems from a broader global perspective, overcoming the constraints of the existing research scope.

The dynamic conditional correlation–GARCH (DCC-GARCH) and CoVaR approaches were adopted to capture the dynamic correlation and risk contagion among various market segments in the energy system. In the comparison with the traditional quantile regression-based CoVaR, the DCC-GARCH-CoVaR with fewer estimated parameters has better performance.

The remaining sections of this research are organized as follows. Following the introductory section, the methodology is introduced in

Section 2. The empirical analysis is presented in

Section 3, followed by the conclusions and policy implications in

Section 4.

2. Methodology

2.1. Models

The DCC-GARCG-CoVaR model is utilized to characterize the dynamic correlation and risk spillovers between various markets within the energy system. The basic principles and steps of the models are introduced in this section.

2.1.1. DCC-GARCH Technology

The GARCH model was first proposed by Bollerslev in 1986 and is widely used to describe the volatility characteristics of markets. The steps are as follows [

28]:

- ⮚

Step 1: Construct the rate of return (ROR) function

To ensure the stability of the data and model, it is necessary to convert the original unstable price data into stable ROR data. The ROR function is constructed in Formula (1)

where

represents the ROR of the

-th market at time

and

represents the initial price.

- ⮚

Step 2: Construct the variance equation, as shown in Formula (2)

where

represents the conditional variance of

at time

;

represents the constant term;

represents the interference term of mean value equation at time

;

and

, respectively, represent the ARCH and GARCH coefficients of the equation; and

.

So far, the single-variable GARCH model has been constructed. Then, the DCC-GARCH model can be further expressed as follows [

29]

where

represents the dependent variable matrix,

represents the independent variable matrix, and

represents the coefficient matrix. Here,

.

To ensure that the ROR series is the positive definition, use Formula (4)

where

represents the conditional covariance matrix,

represents the diagonal matrix composed of the conditional standard deviations

,

represents the DCC matrix as shown in Formula (5),

represents the conditional variance matrix of the normalized residuals estimated by a single variable as shown in Formula (6), and

represents the diagonal matrix of

.

where

represents the unconditional covariance matrix after normalizing the residuals,

α represents the degree of influence of the standardized residual on the conditional variance of the one-period lag, and

represents the first-order degree of influence of the standardized residuals on the conditional variance. Here,

.

So far, the dynamic correlation coefficient between market

i and market

j can be expressed by Formula (7):

2.1.2. CoVaR Approach

The VaR model was first proposed in 1993 and can give the maximum loss under certain conditions and reflect the risk intuitively. The VaR of a market can be calculated by Formula (8):

Based on VaR, the CoVaR [

22] can be further expressed as follows

where

represents the conditional risk value generated by market

to market

,

represents the risk loss, and

represents the quantile.

Therefore, the degree of systemic risk spillover from market

to financial market

can be expressed as follows:

Combining the DCC-GARCH model with the CoVaR model [

23], the following formula can be obtained

where

represents the mean value of the GARCH model estimation,

represents the standard deviation of the DCC-GARCH model estimation, and

represents the quantile of ROR distribution of market

when the confidence level is

, where

.

To better reflect the degree of risk spillover, the indicator

is used to characterize the risk spillover effect between markets, as shown in Formula (12):

2.2. Data Sources and Descriptive Statistics

2.2.1. Data Sources

To study the risk spillovers of the energy system, we first constructed five subsystems, and two typical representatives were selected for analysis in each subsystem, as shown in

Table 1.

- ⮚

Chinese Energy System

- (1)

Fossil fuel subsystem

According to BP, China’s total primary energy consumption in 2021 reached approximately 157.65 Exajoules (EJ). Of these, the consumption of coal, oil, and natural gas accounted for 54.7%, 19.4%, and 8.7%, respectively. Thus, the two fossil fuels mainly used in China (coal and oil) were selected as representatives in the fossil fuel subsystem. Referring to [

30,

31], we selected the thermal coal trading in Zhengzhou Commodity Exchange (ZCE) and crude oil produced in the Daqing field as the markets for analysis.

- (2)

Electricity subsystem

In the electricity subsystem, the current Chinese power market mainly adopts the spot market trading method and is still in the pilot development stage. Therefore, China has not yet established an electricity futures market that could be used to select research objects in this paper. Referring to [

42], we selected the stock prices of listed power companies to measure the development level of the electricity market. Thus, Huaneng Power International, Inc. and China Yangtze Power Co., Ltd. were selected as the typical representatives of the electricity subsystem.

- (3)

Green bond subsystem

In the green bond subsystem, the China Green Bond Index and China Climate-Aligned Bond Index—the two earliest bond indexes established and issued in China—were mainly selected to reflect the development of the green bond markets.

- (4)

Renewable energy subsystem

The selection method of representative objects in the renewable energy subsystem is similar to that in the electricity subsystem (selecting leading enterprises). However, the renewable energy industry chain is long, and there are a large number of enterprises from upstream research and development manufacturing to downstream terminal applications. Thus, we have selected the most representative renewable energy enterprises from the aspects of market size and company revenue to characterize the subsystem, referring to Ref. [

32]. According to the list of “Top 500 Chinese Energy Enterprises in 2024” released by China’s Academy of Energy Economics, renewable energy-related companies such as Contemporary Amperex Technology Co., Ltd. and EVE Energy Co., Ltd. are both on the list (Neway valve was listed among the “Top 500 Chinese Energy Enterprises in 2024”:

https://www.newayvalve.com/37/178 (accessed on 17 June 2025)). Of these, CATL ranks 14th on the list (which is also a leading position among all renewable energy-related enterprises).

- (5)

Carbon subsystem

In the carbon subsystem, relatively few data are available because of the late official listing and trading time of the national unified carbon emission trading system (ETS). Therefore, the main research object of the carbon subsystem is the ETS in pilot areas. According to the carbon market information disclosure data, the cumulative trading volume in Guangdong’s ETS and Shenzhen’s ETS was CNY 4.130 billion and CNY 1.203 billion, respectively, as of June 2022, which has a better market operation effect than other pilot regions. Therefore, the Guangdong carbon market and Shenzhen’s carbon market were selected as representative research objects for the carbon subsystem.

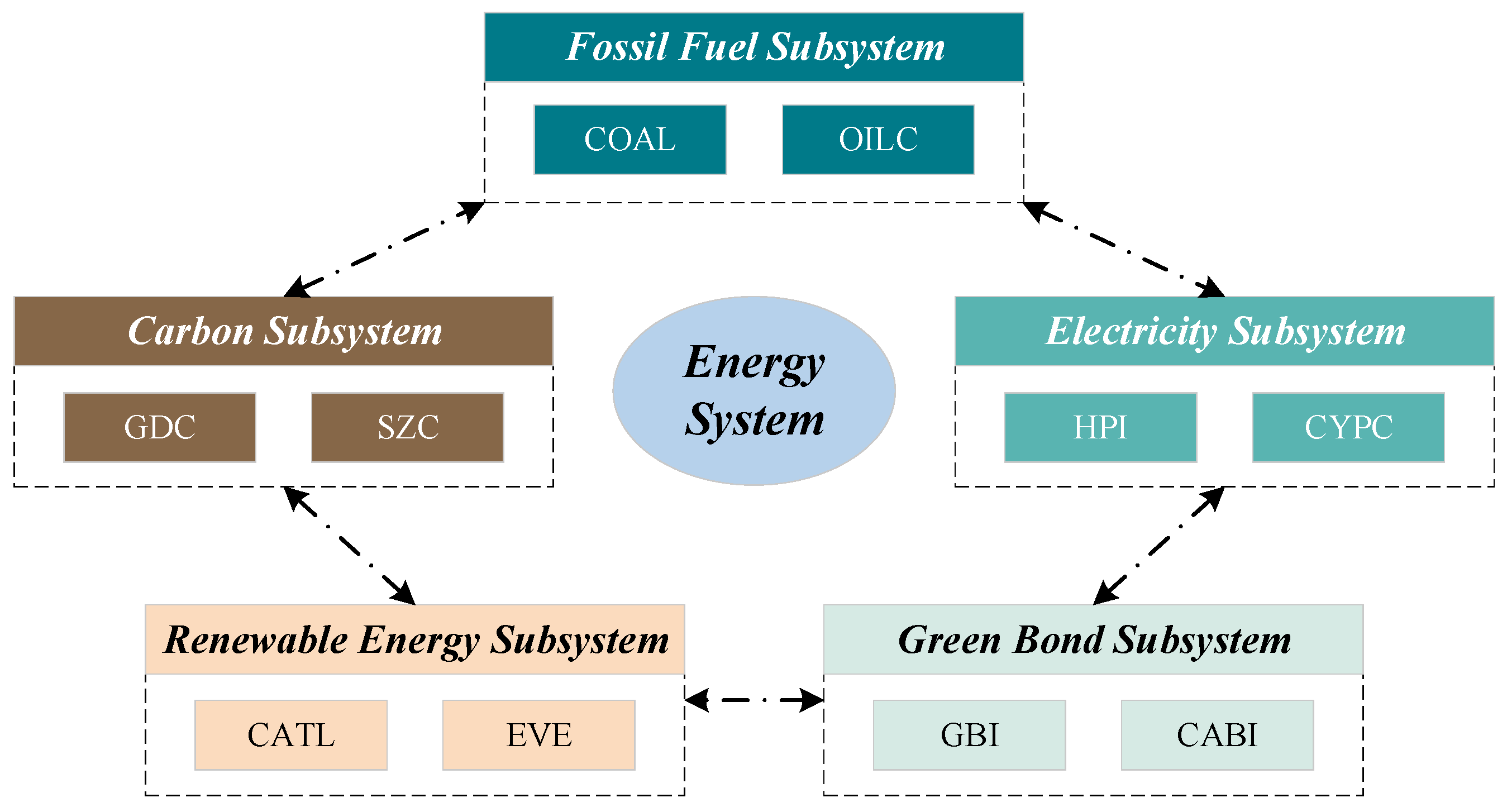

The framework diagram of the Chinese energy system and subsystems is shown in

Figure 2.

As shown in

Figure 2, the Chinese energy system constructed in this paper mainly consists of five subsystems and each subsystem includes two market segments (ten segments in total).

- ⮚

European Energy System

- (1)

Fossil fuel subsystem

In contrast to China’s energy structure, the main energy sources consumed in Europe are oil and natural gas, accounting for 33.5% and 25.0%, respectively, of the total primary energy consumption in 2021. Thus, we selected these two main fossil fuels in Europe (oil and natural gas) as representatives in the fossil fuel subsystem. Referring to [

37,

38], we selected Brent crude oil and NBP natural gas as the represent markets for analysis.

- (2)

Electricity subsystem

As for the electricity subsystem, the French and German electricity markets were mainly selected. On the one hand, these two countries were the largest electricity generation entities in Europe in 2021, reaching 547.2 and 548.5 Terawatt-hours (TWh), respectively. On the other hand, both countries have only one unified electricity market, unlike other regions (such as Norway, which has five segmented electricity markets).

- (3)

Green bond subsystem and renewable energy subsystem

Referring to [

39], we selected the Franklin Euro Green Bond and S&P/TSX Renewable Energy and Clean Technology Index as representatives of the green bond subsystem and renewable energy subsystem (due to data limitations, we were unable to obtain data on two market prices that were similar to other subsystems. Therefore, only one market was chosen as a representative in each of these two subsystems).

- (4)

Carbon subsystem

Furthermore, the selection of representative markets within the European carbon subsystem differs from that of China. The European carbon market is mainly based on the European Union’s emission trading system (EU ETS). Hence, EUA and CER were selected as representatives.

The framework diagram of the European energy system and subsystems is shown in

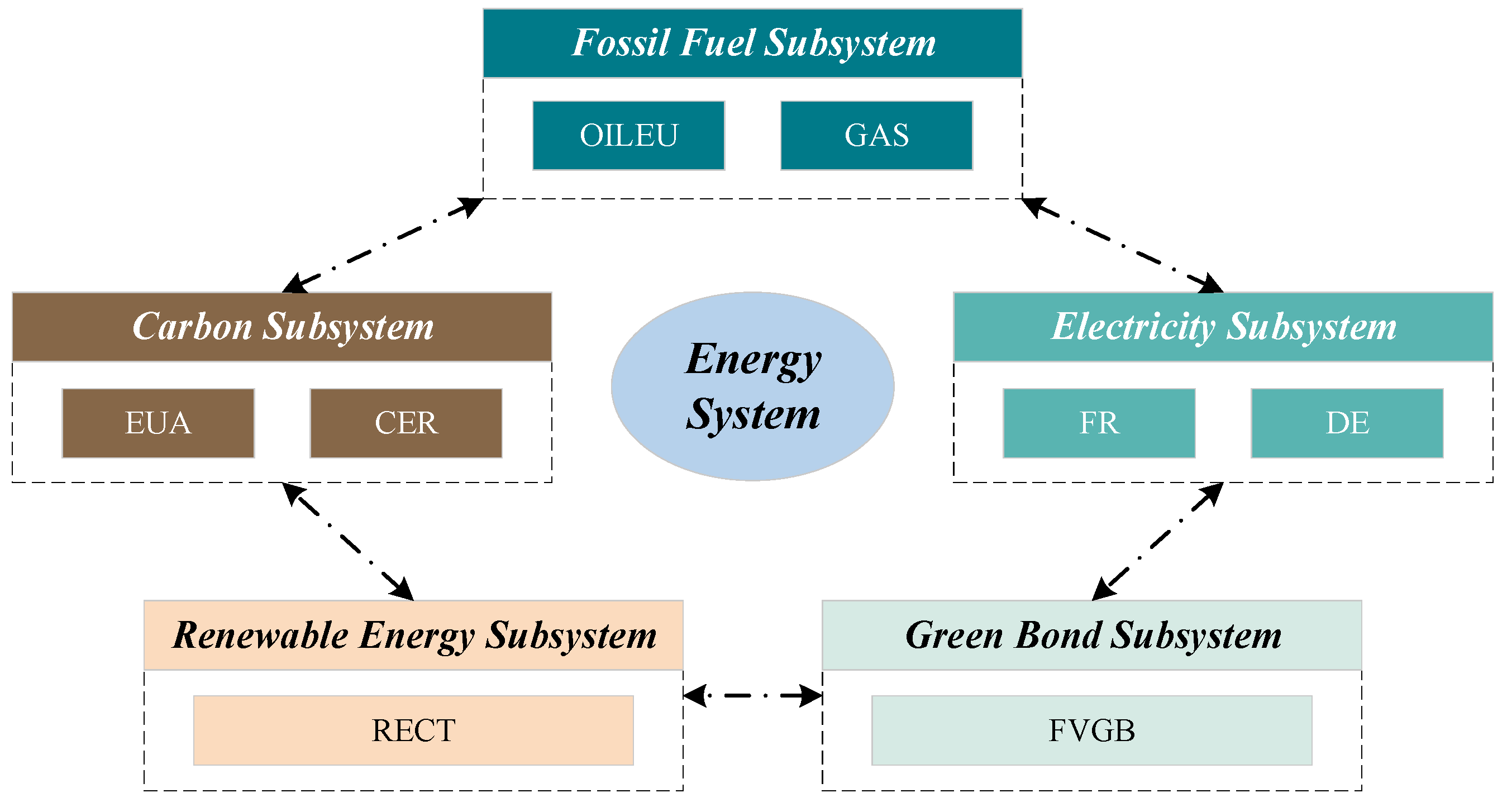

Figure 3.

As shown in

Figure 3, the European energy system constructed in this paper mainly consists of five subsystems. Of these, the fossil fuel/electricity/carbon subsystems mainly include two market segments each, and the green bond/renewable energy subsystems mainly include one market segment (eight segments in total).

2.2.2. Descriptive Statistics

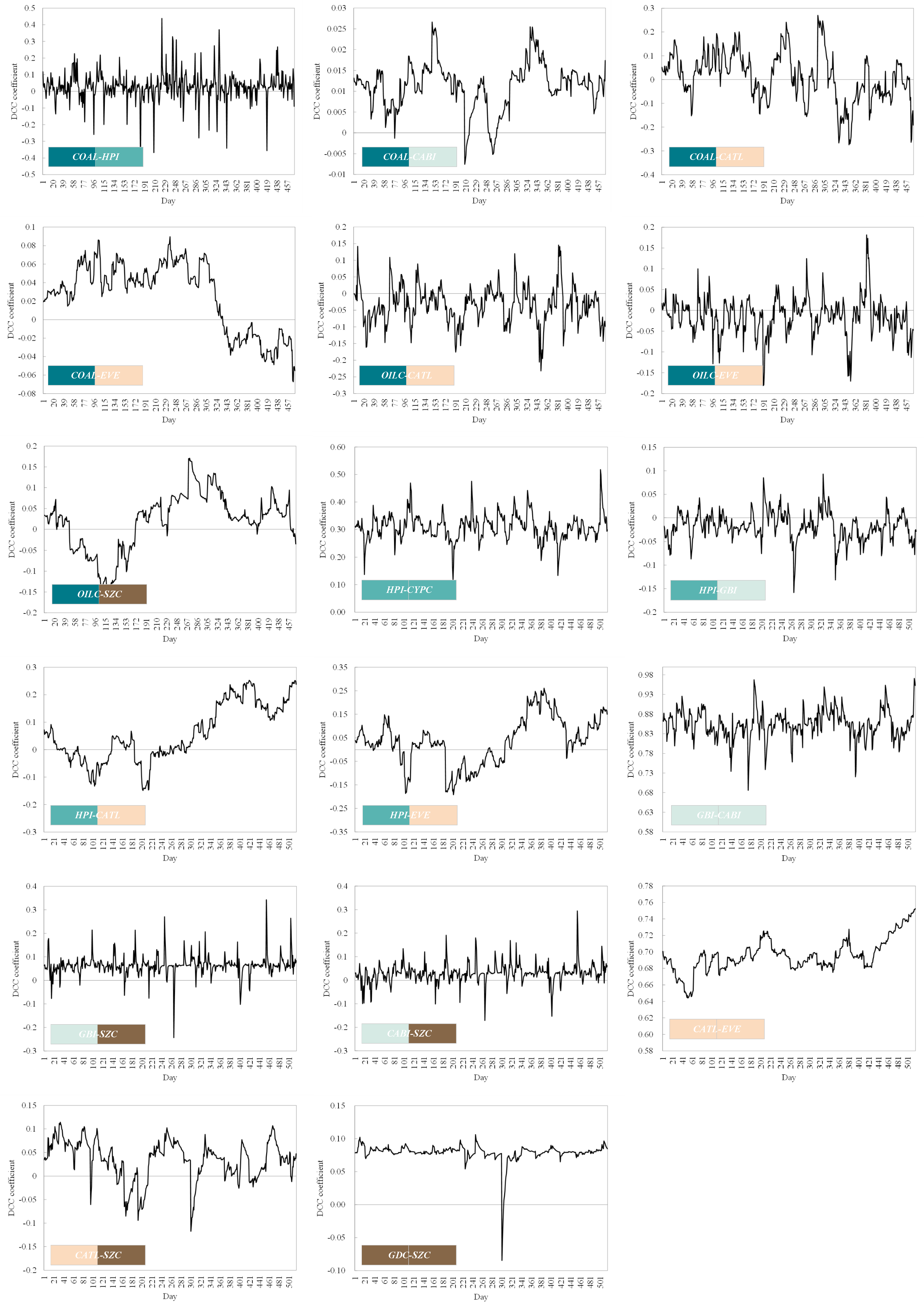

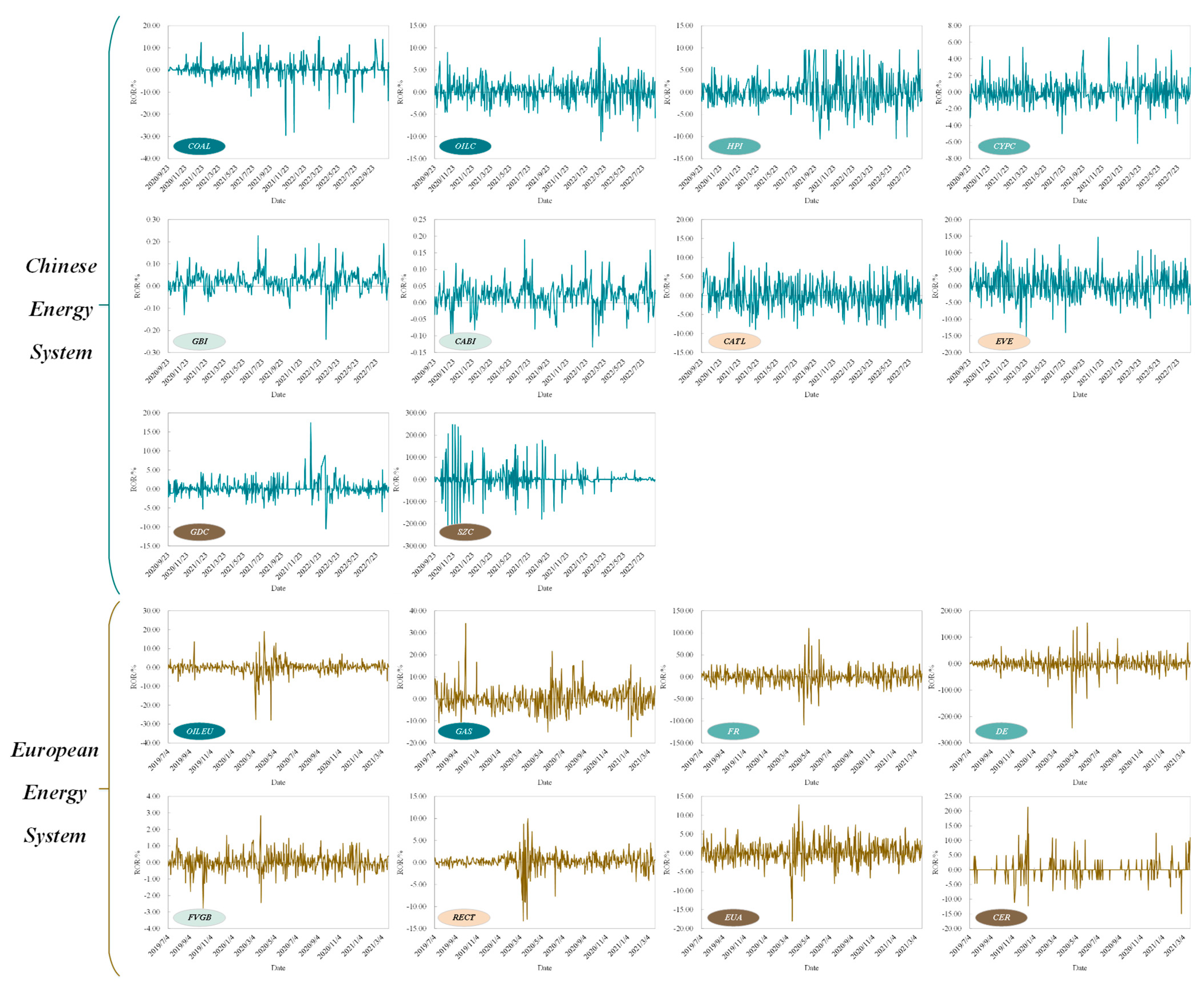

Considering the different timing of proposing carbon neutrality targets, market data on the Chinese energy system span from 22 September 2020 to 31 August 2022 (China proposed the carbon neutral target on 22 September 2020), and market data on the European energy system are from 4 July 2019 to 22 March 2021 (Europe proposed the carbon neutral target on November 2018; moreover, the EU discontinued CER’s operation for carbon offsetting and instead adopted a new international emission reduction mechanism under the Paris Agreement after March 2021). All data are sourced daily from the WIND database. The initial price data are converted into ROR data using Equation (1), as shown in

Figure A1.

All markets exhibited apparent convergence in the ROR data changes, also called volatility clustering (

Figure A1). In other words, the amplitude of price fluctuations tended to be persistent within a certain period. Large price fluctuations in the current period are often accompanied by large price fluctuations in the next period, similar to low volatility. The ROR descriptive statistics on the aforementioned markets are shown in

Table A1.

The following conclusions can be obtained via

Table A1:

(1) During the statistical period, the return of the carbon subsystem is significantly higher than that of other subsystems, for both the Chinese and European energy systems. By contrast, the average ROR of CYPC and DE in the electricity subsystem were the lowest at 0.0113 and −0.1397, respectively, in both energy systems. From the standard deviation, Chinese and European green bond subsystems exhibited gentle fluctuation trends. However, the standard deviation of SZC in the Chinese carbon subsystem reached 48.5808, indicating that the price fluctuation in the market is significant.

(2) In terms of skewness, the skewness of each market in each subsystem was not 0, indicating that the distribution of returns in each market is asymmetric. Furthermore, the kurtosis of each market was greater than 3, and the J-B statistics were significant at the level of 1%, suggesting that the ROR of each market is not a normal distribution but rather a typical leptokurtic distribution characteristic. This finding proves that the energy system has a feedback effect.

(3) All market RORs passed the ADF test and were significant at the 1% level, meaning that all markets are stable. Furthermore, all market RORs passed the ARCH-LM test and were significant at the 10% level. This finding implies an ARCH effect in each market so that GARCH modeling can be conducted for each market.

2.3. Research Framework

The research framework of this paper is shown in

Figure 4.

As shown in

Figure 4, the research framework is mainly divided into the following four steps:

- ⮚

Step 1: Energy system construction and data collection

First of all, it is necessary to clarify the research scope of this paper, that is, the construction of the energy system and subordinate subsystems. Meanwhile, considering the availability and applicability, a certain amount of market price data should be collected.

- ⮚

Step 2: Data preprocessing and descriptive statistical analysis

After collecting the original price data of each research object, it is necessary to convert them into stable ROR data through data preprocessing. Subsequently, descriptive statistics are required for each set of ROR sequence data. In addition to being able to summarize the characteristics of the processed data, it is also able to determine whether the data are stable and have an ARCH effect. The ADF test and ARCH-LM test are also the basis for the subsequent research.

- ⮚

Step 3: Dynamic correlation analysis based on the DCC-GARCH model

The dynamic correlation analysis is a prerequisite for judging the risk spillover effect within the energy system. In this step, it is first necessary to establish a single GARCH model for each research object and determine whether the parameter estimation results meet the conditions. Then, the dynamic correlation between various markets can be calculated using the DCC-GARCH model.

- ⮚

Step 4: Risk spillover effects analysis based on the CoVaR model

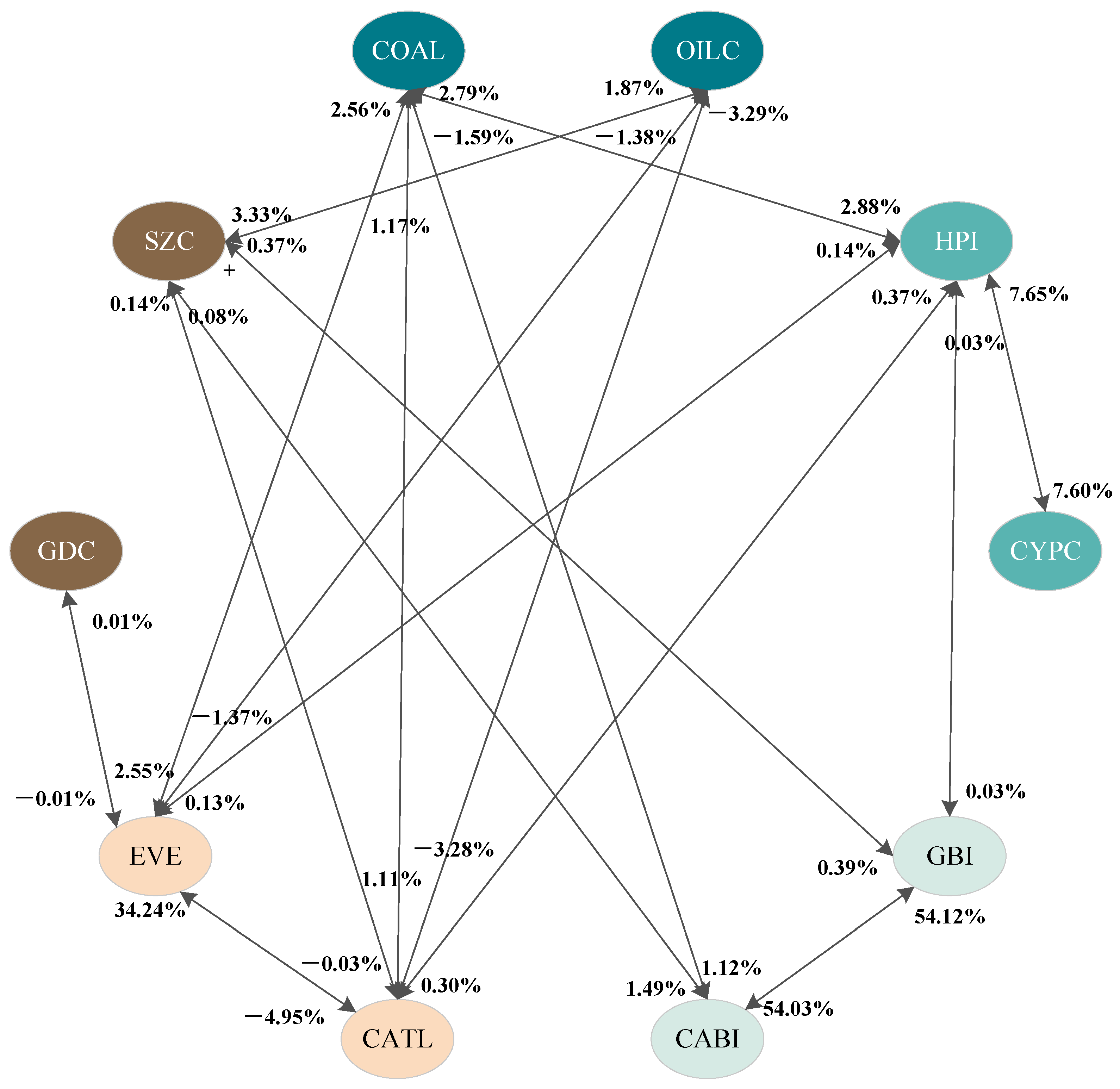

Before establishing the risk spillover model of the energy system, it is necessary to first test the estimated parameters of the DCC-GARCH model. If the research object meets the conditions of the estimated parameters, the risk spillover effect between markets can be further calculated by the CoVaR model. Finally, the risk transmission relationship between various markets is visualized through a risk network diagram, and the risk vulnerability of each subsystem is analyzed.

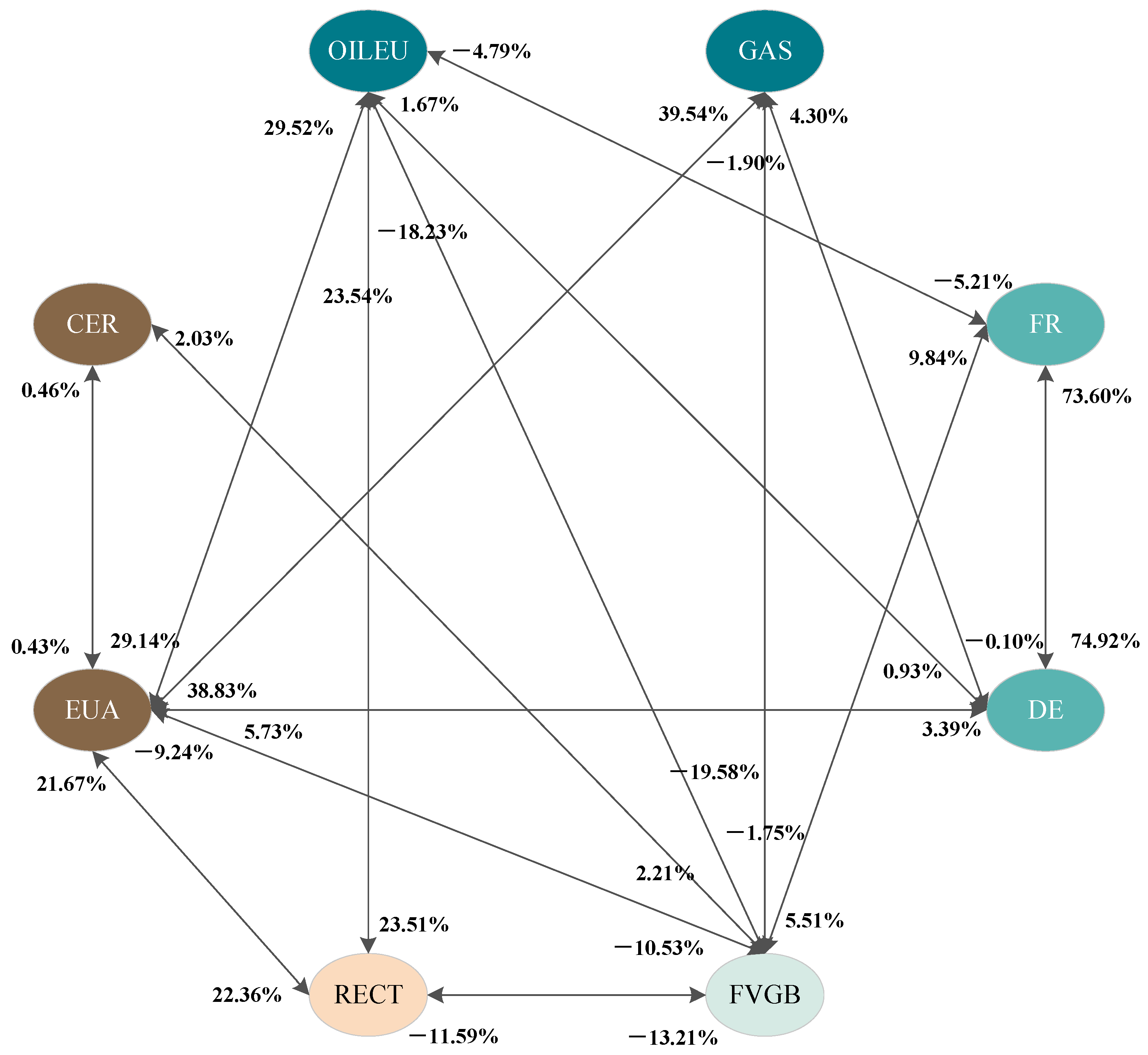

4. Conclusions and Policy Implications

4.1. Conclusions

The proposed “zero carbon” and “carbon neutrality” targets are the key measures for countries to address climate change issues. As a significant emitter, promoting clean pro-duction and environmental protection in the energy sector is essential to achieving carbon emission reduction targets. Conversely, the proposed carbon neutral target will also have an impact on the energy system, so as to bring risk contagion among the energy markets. As significant contributors to global carbon emissions and energy consumption, this risk spillover analysis of the Chinese and European energy markets not only helps to enhance their own energy systems but also provides other emerging economies with a reference and experiences. Thus, in-depth research on the risk spillover effects of multi-energy systems based on the DCC-GARCH-CoVaR model was conducted in this study, which not only identified the risk contagion among subsystems within the energy system but also obtained the risk transmission relationship between the internal markets of each subsystem. The following conclusions and policy implications can be drawn:

(1) Even though there are fewer markets in the European energy system studied in this research than there are in the Chinese energy system, the market linkage within the former system is nevertheless much stronger than that within the latter. Specifically, the dynamic correlation across markets within the same subsystem is more significant in the Chinese energy system. Of these, the relationship between GBI and CABI within the green bond subsystem is the closest. However, the situation in the European energy system is quite different. The linkage between EUA and CER within the carbon subsystem is not close, despite the fact that they are members of the same subsystem. On the contrary, some cross-subsystem markets have closer linkage relationships, such as EUA and GAS/OILEU within the fossil fuel subsystem.

(2) The high correlation between markets also leads to the large-scale diffusion of risks, and the risk spillovers within the European energy system are about 2.6 times that within the Chinese energy system. It appears difficult for the carbon subsystem to suffer risk spillovers with other markets or subsystems within the Chinese energy system due to limited market liquidity and trading activity. The emerging green bond and renewable energy subsystems, however, are more susceptible to risk transmission. With the exception of the sluggish CER market, other markets in the European energy system have maintained a risk spillover impact ranging from 40.68% to 105.80%. It is interesting to note that the EUA market, which also derives from the carbon subsystem, is the largest market for risk spillovers.

4.2. Policy Implications and Future Directions

Based on the aforementioned conclusions, the following policy implications are pro-posed:

(1) For the market regulators and policymakers of the Chinese energy system, it is essential to strengthen supervision of the linkage among the energy markets and form a thorough risk management and monitoring system. On the basis of the research results in this paper, they can make effective risk responses from the following aspects:

- ⮚

Establish a cross-departmental/subsystem collaboration mechanism and release risk warning information (e.g., explore and establish real-time data-sharing platforms).

- ⮚

Strengthen the supervision of false information to avoid the large-scale transmission of risks and crack down on the trading behaviors of manipulating the energy markets. When there is a serious risk of contagion, cross-market circuit breakers can be introduced into the system.

- ⮚

Establish a closed-loop risk prevention and control mechanism of “pre-event, during the event, and post-event”. Of these, it is necessary to strengthen the identification of key risk points in advance, closely track and monitor the changes in risks during the process, and summarize the reasons and prepare for the next risk response afterwards.

The suggestions above also apply to the European energy system. However, the market regulators should concentrate more on the price fluctuations and risk spillovers from the EUA market. In the fourth phase of the EU ETS (2021–2030), stricter carbon emission control and targeted carbon leakage rules have been implemented. The constraints on the allowance amount and the gradual cancellation of free allowance distribution will further affect the EUA market, resulting in wider risk transmission. To this end, European policymakers need to vigorously improve policies related to the carbon market, such as expanding the coverage of entities and steadily promoting non-free allowances.

(2) For investors with information barriers, there is a lag in their perception of macroeconomic policy adjustments and energy market risks, resulting in investment losses caused by difficulty in rapidly altering their investment plans. As a result, investors should improve the information acquisition capabilities and actively follow the latest advancements in energy systems, especially those with high-risk spillover markets and subsystems. Moreover, investors can refer to the conclusions of this paper to diversify and optimize investment strategies centered on energy markets with minimal risk linkages. In addition, investors should undoubtedly improve their understanding of the energy market and develop sound investing ideas.

4.3. Limations and Future Directions

Although this paper has conducted extensive research on the energy systems of China and Europe, data factors still constrain its progress towards broader and more comprehensive results and conclusions. For instance, it is difficult to find suitable alternative/supplementary segments for some subsystems in the European energy system. In the future, we will strive to improve the completeness of data and further carry out analyses of risk spillovers of other major energy consumption and carbon emission entities. Moreover, cross-border energy system risk spillovers may be also a possible future research direction. From the perspective of risk contagion, an in-depth analysis of the major reasons behind this phenomenon would also be noteworthy. In a follow-up study, we will further explore the key policy events and explore the impact and effect of these major events.

From the perspective of the model, the DCC-GARCH-CoVaR model was adopted to solve the risk spillover issue in the energy system presented in this paper. Indeed, the superiority of this method in solving the problems has been demonstrated through previous research and comparative analysis. However, it cannot be denied that no model can be applied to all scenarios and problems simultaneously. Therefore, in the next step of our research, we plan to use a broader range of models for a comparative analysis to enhance the scientific rationality of the study.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}