Advancements and Policy Implications of Green Hydrogen Production from Renewable Sources

Abstract

1. Introduction

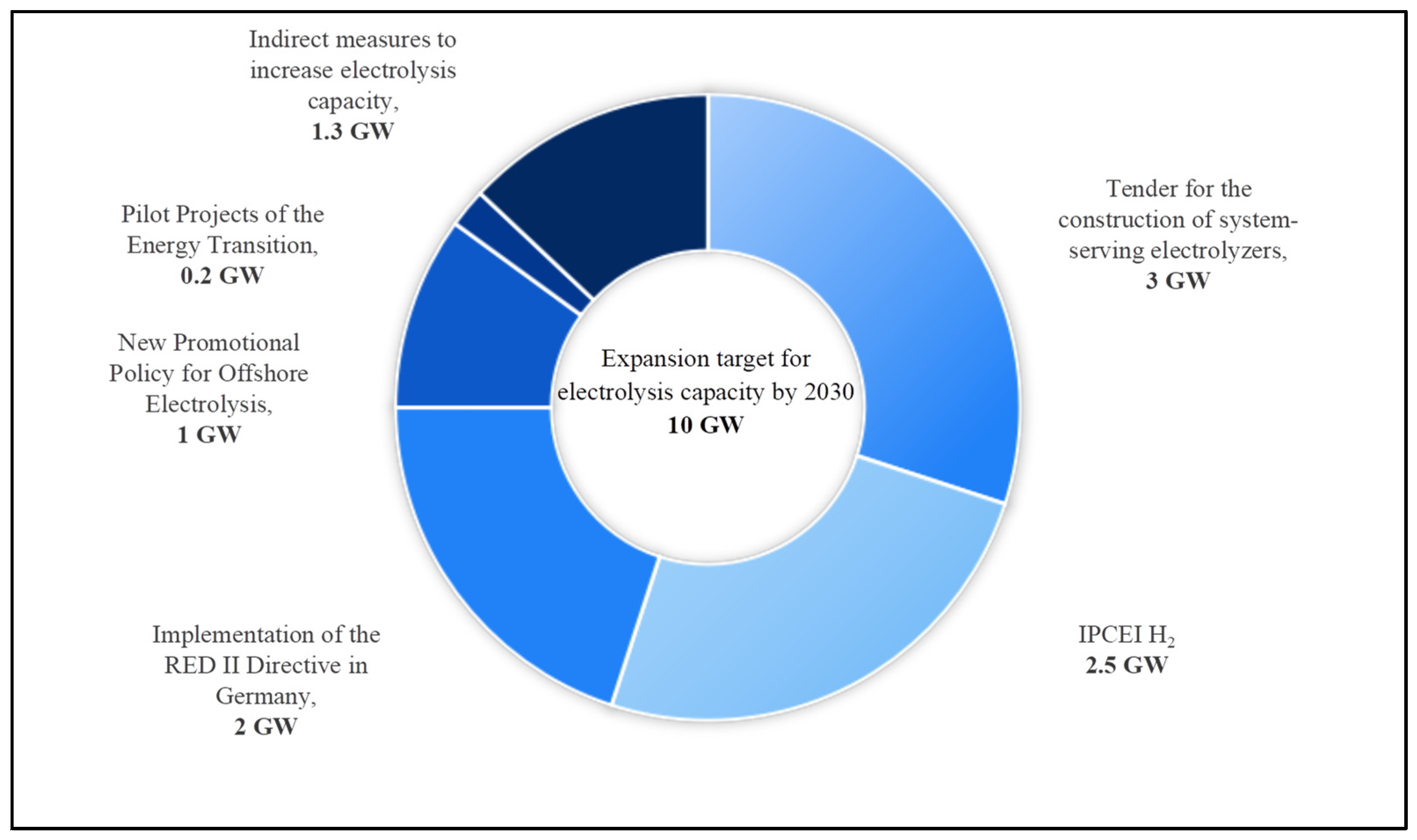

2. Policy Advances

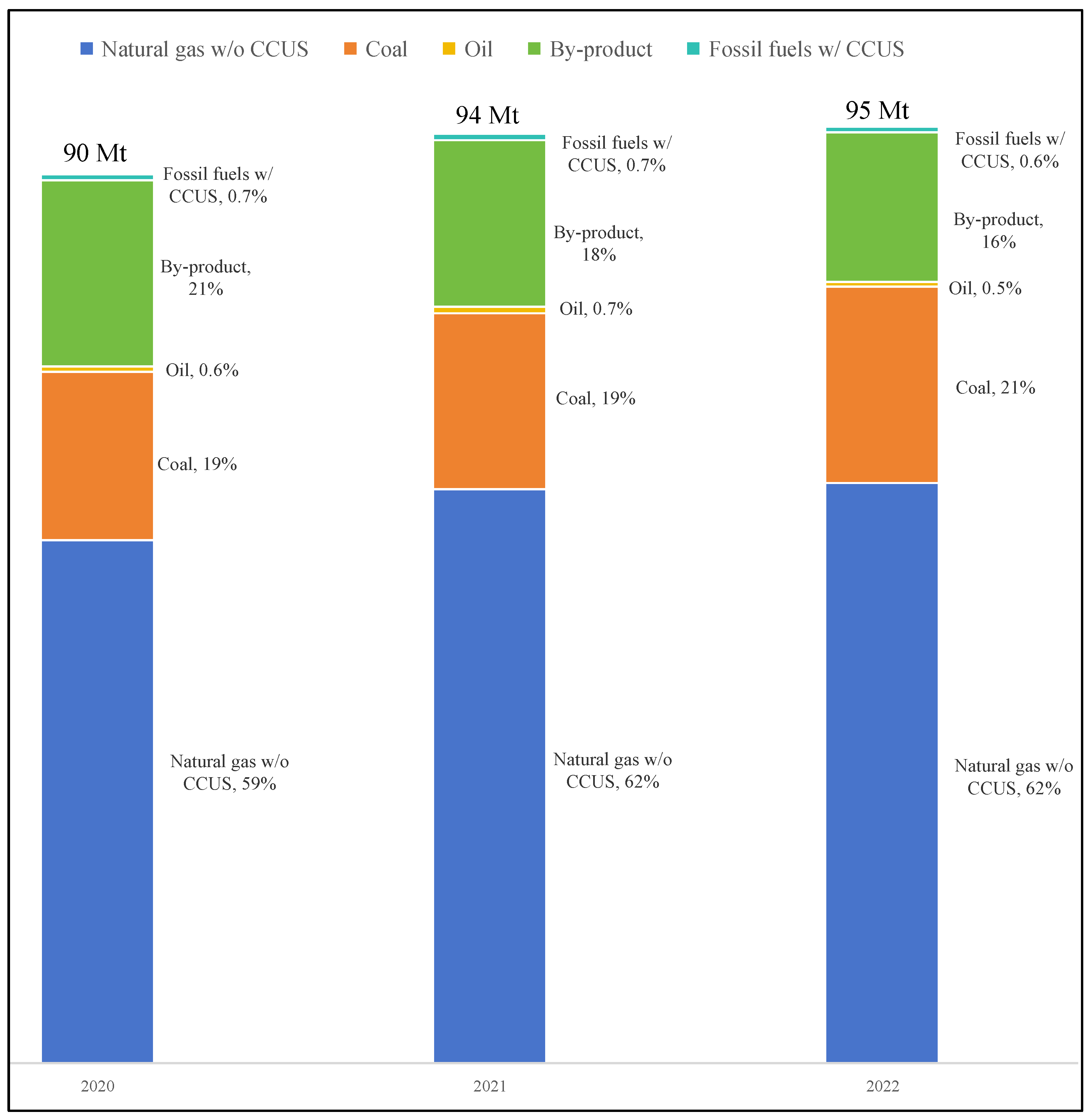

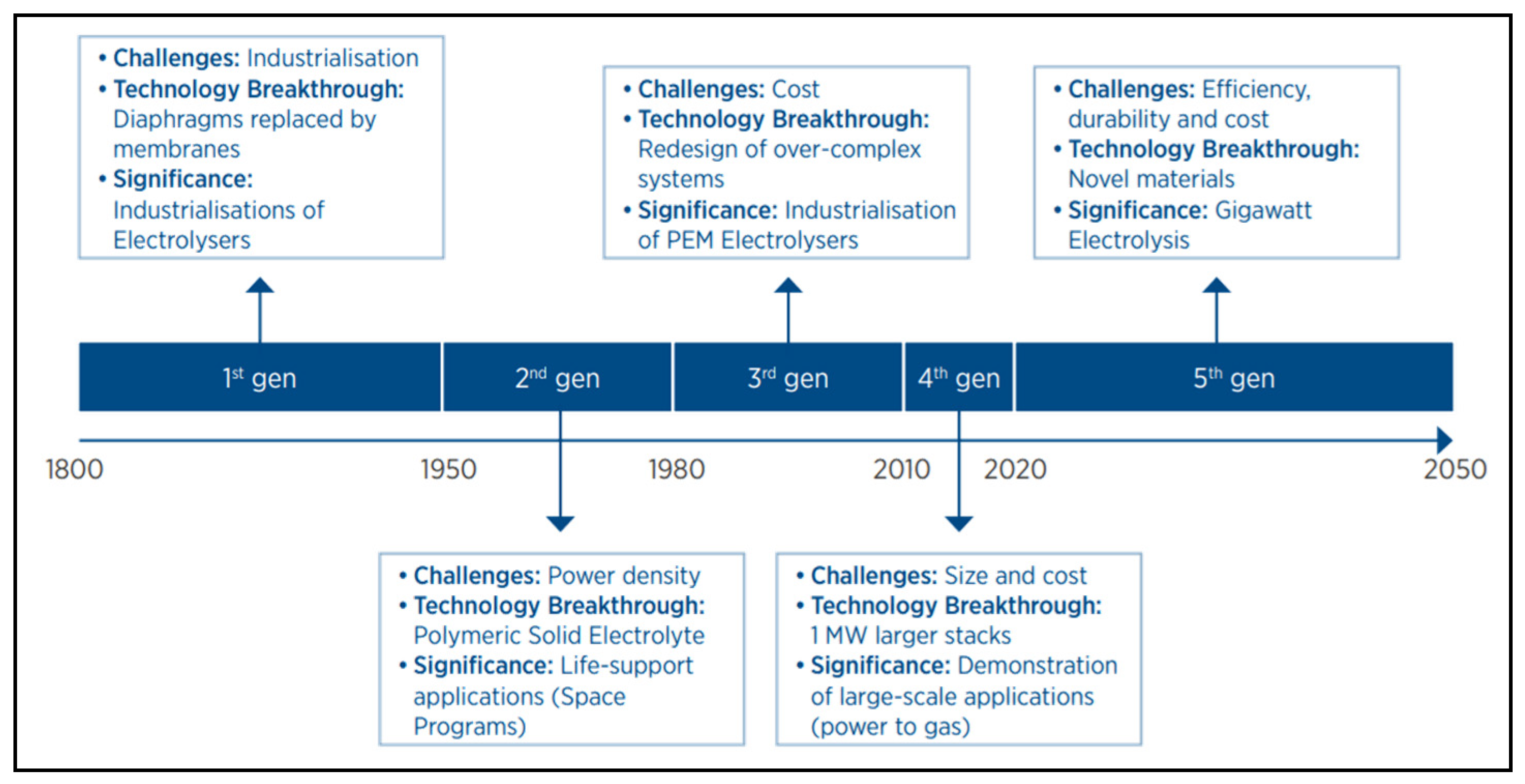

3. Technological Progress

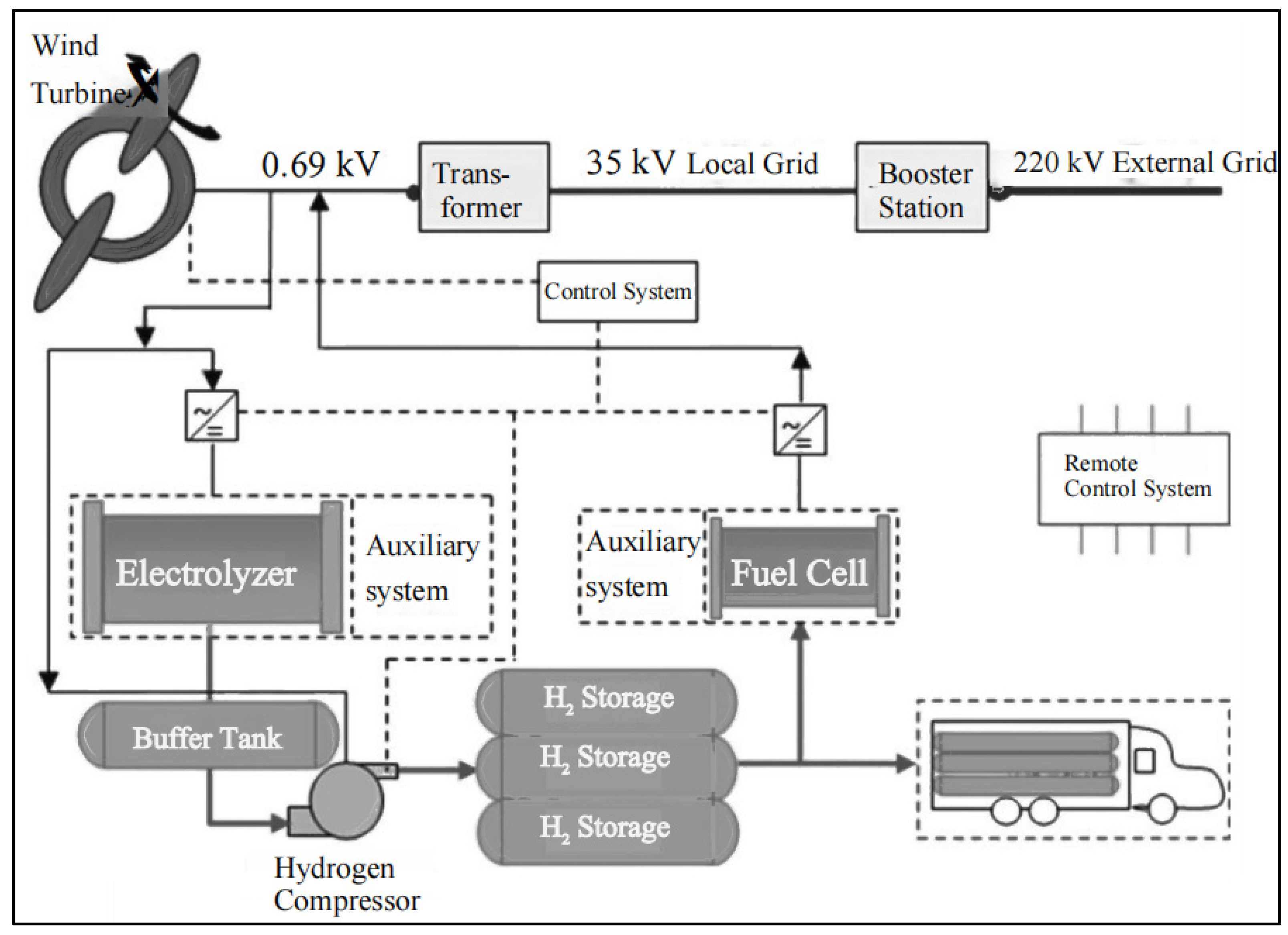

3.1. Wind Power Generation for Hydrogen Production

3.2. Photovoltaic Hydrogen Production

4. Comprehensive Assessment

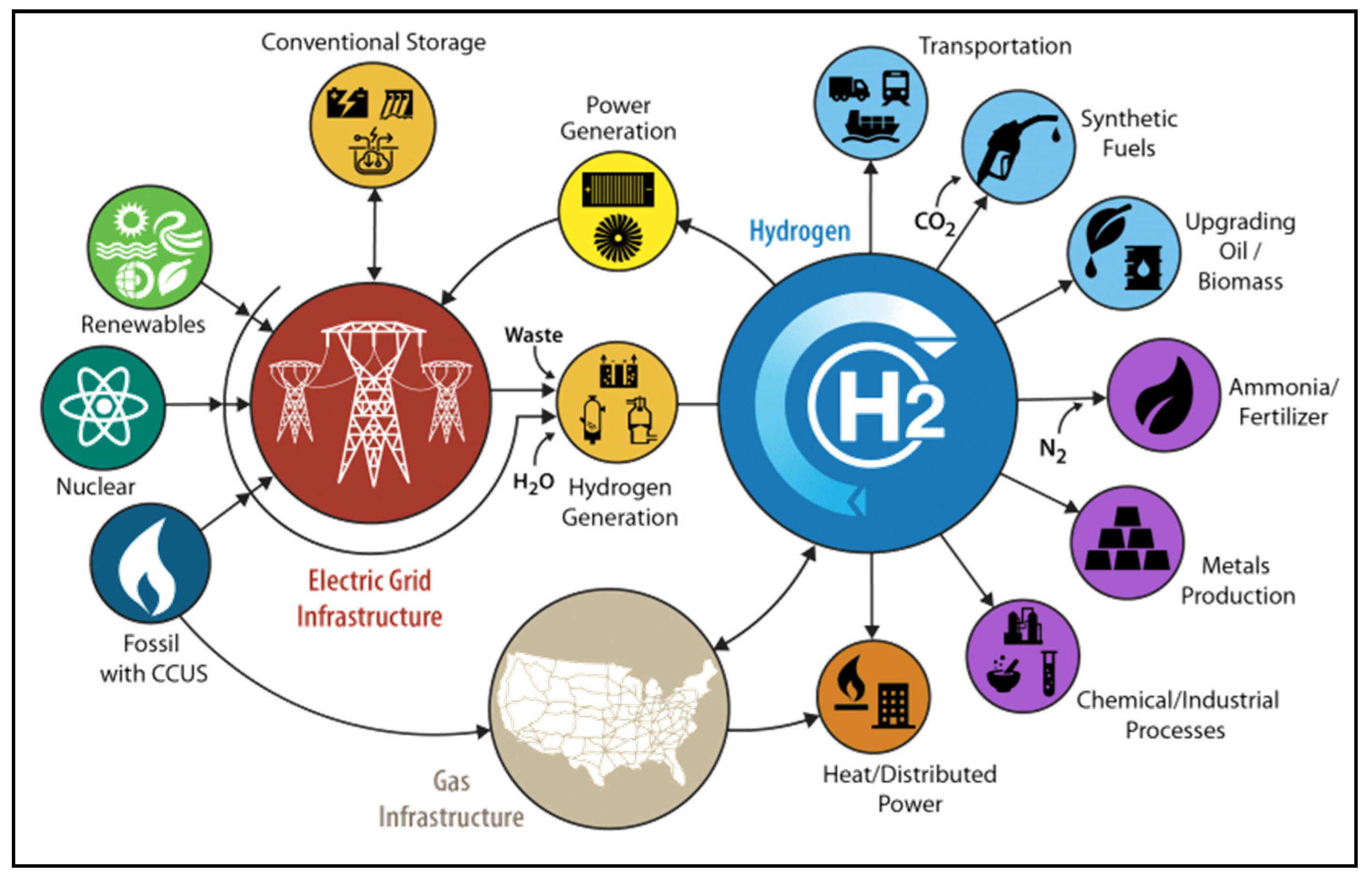

5. Prospects for Water Electrolysis Based on Renewable Energy

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- International Energy Agency. Global Hydrogen Review 2023; International Energy Agency: Paris, France, 2023.

- Hydrogen Council. Hydrogen, Scaling Up; Hydrogen Council: Bonn, Germany, 2017. [Google Scholar]

- Cao, J.W.; Zhang, W.Q.; Li, Y.F.; Zhao, C.H.; Zheng, Y.; Yu, B. Current status of hydrogen production in China. Prog. Chem. 2021, 33, 2215–2244. [Google Scholar]

- Xu, S.; Yu, B.Y. Current development and prospect of hydrogen energy technology in China. J. Beijing Inst. Technol. 2021, 23, 1–12. [Google Scholar]

- U.S. Department of Energy. U.S. National Clean Hydrogen Strategy and Roadmap; U.S. Department of Energy: Washington, DC, USA, 2023.

- Fu, G.Y.; Xiong, H.W. Hydrogen energy development models and their implications in Japan, Germany, and United States. Macroecon. Manag. 2020, 84–90. [Google Scholar] [CrossRef]

- Wei, F.; Ren, X.B.; Gao, L.; Gao, G.Q.; Zhou, C.F. Analysis on transformation and characteristics of American hydrogen energy strategy under carbon neutralization goal. Bull. Chin. Acad. Sci. 2021, 36, 1049–1057. [Google Scholar]

- European Commission. A Hydrogen Strategy for a Climate-Neutral Europe; European Commission: Brussels, Belgium, 2020. [Google Scholar]

- European Commission. REPowerEU: Joint European Action for More Affordable, Secure and Sustainable Energy; European Commission: Brussels, Belgium, 2020. [Google Scholar]

- German Federal Government. National Hydrogen Strategy (Revision); German Federal Government: Berlin, Germany, 2023.

- Ministry of Economy, Trade and Industry. The Fourth Strategic Energy Plan; Ministry of Economy, Trade and Industry: Tokyo, Japan, 2014.

- Ministry of Economy, Trade and Industry. Basic Hydrogen Strategy; Ministry of Economy, Trade and Industry: Tokyo, Japan, 2023.

- National Development and Reform Commission; National Energy Administration. Medium and Long Term Plan for the Development of Hydrogen Energy Industry (2021–2035); National Development and Reform Commission: Beijing, China, 2022.

- National Energy Administration. 2022 National Renewable Energy Power Development Monitoring and Evaluation Report; National Energy Administration: Beijing, China, 2023.

- China Hydrogen Alliance Research Institute. Report on the Development of China’s Hydrogen Energy and Fuel Cell Industry in 2022; China Hydrogen Alliance Research Institute: Beijing, China, 2023. [Google Scholar]

- Asghhari, E.; Abdullah, M.I.; Foroughi, F.; Lamb, J.J. Advance, opportunities, and challenges of hydrogen and oxygen production from seawater electrolysis: An electrocatalysis perspective. Curr. Opin. Electrochem. 2022, 31, 100879. [Google Scholar] [CrossRef]

- Zhang, W.Q.; Yu, B. Development status and prospects of hydrogen production by high temperature solid oxide electrolysis. J. Electrochem. 2020, 26, 212–229. [Google Scholar]

- Shirvanian, P.; Loh, A.; Sluijter, S.; Li, X.H. Novel components in anion exchange membrane water electrolyzers (AEMWE’s): Status, challenges and future needs. A mini review. Electrochem. Commun. 2021, 132, 107140. [Google Scholar] [CrossRef]

- Yu, H.M.; Shao, Z.G.; Hou, M.; Yi, B.L.; Duan, F.W.; Yang, Y.X. Hydrogen production by water electrolysis: Progress and suggestions. Strateg. Study CAE 2021, 23, 146–152. [Google Scholar] [CrossRef]

- El-Eman, R.S.; Özcan, H. Comprehensive review on the techno-economics of sustainable large-scale clean hydrogen production. J. Clean. Prod. 2019, 220, 593–609. [Google Scholar] [CrossRef]

- Hu, S.; Guo, B.; Ding, S.L.; Yang, F.Y.; Dang, J.; Liu, B.; Gu, J.J.; Ma, J.G.; Ouyang, M.G. Acomprehensive review of alkaline water electrolysis mathematical modeling. Appl. Energy 2022, 327, 120099. [Google Scholar] [CrossRef]

- Wu, X.T.; Tan, L.; Zheng, Y.Y.; Lin, C.; Xiao, Q.; Li, X.P. Outlook on hydrogen economy and techno-economic assessment of water electrolysis-based hydrogen production. Chem. Ind. Eng. 2024, 41, 131–140. [Google Scholar]

- Hydrogen Council. Hydrogen Insights 2023; Hydrogen Council: Brussels, Belgium, 2023. [Google Scholar]

- TrendBank. Annual Blue Book of China’s Hydrogen and Fuel Cell Industry (2022); TrendBank: Ningbo, China, 2022. [Google Scholar]

- Yan, Z.Y.; Kong, X.W. Research on non-grid-connected wind power water-electrolytic hydrogen production system and its applications. Strateg. Study CAE 2015, 17, 30–34. [Google Scholar]

- Jorgensen, C.; Ropenus, S. Production price of hydrogen from grid connected electrolysis in a power market with high wind penetration. Int. J. Hydrogen Energy 2008, 33, 5335–5344. [Google Scholar] [CrossRef]

- Zhang, G.T.; Wan, X.H. A wind-hydrogen energy storage system model for massive wind energy curtailment. Int. J. Hydrogen Energy 2014, 39, 1243–1252. [Google Scholar] [CrossRef]

- Yi, W.; Xu, J.Y.; Wu, G.N.; Jiang, Y.Y.; Teng, Y.L. Improvement of wind abandoned consumption capacity in a region of northeast region China by wind power hydrogen storage energy system. Power Capacit. React. Power Compens 2018, 39, 190–197. [Google Scholar]

- Shao, Z.F.; Wu, J.L.; Zhao, Q.; Zhang, Y.J. Cost effectiveness analysis model for wind power produce hydrogen system and simulation. Technol. Econ. 2018, 37, 69–75. [Google Scholar]

- Mirzaei, M.A.; Yazdankhah, A.S.; Mohammadi-Ivatloo, B. Stochastic security-constrained operation of wind and hydrogen energy storage systems integrated with price-based demand response. Int. J. Hydrogen Energy 2019, 44, 14217–14227. [Google Scholar] [CrossRef]

- Lin, H.Y.; Wu, Q.W.; Chen, X.Y.; Yang, X.; Guo, X.Y.; Lv, J.J.; Lu, T.G.; Song, S.J.; McElroy, M. Economic and technological feasibility of using power-to-hydrogen technology under higher wind penetration in China. Renew. Energy 2021, 173, 569–580. [Google Scholar] [CrossRef]

- Kaldellis, J.K.; Apostolou, D.; Kapsali, M.; Kondili, E. Environmental and social footprint of offshore wind energy comparison with onshore counterpart. Renew. Energy 2016, 92, 543–556. [Google Scholar] [CrossRef]

- Crivellari, A.; Cozzani, V. Offshore renewable energy exploitation strategies in remote areas by power-to-gas and power-to-liquid conversion. Renew. Energy 2020, 45, 2936–2953. [Google Scholar] [CrossRef]

- D’Amore-Domenech, R.; Santiago, O.; Leo, T.J. Multicriteria analysis of seawater electrolysis technologies for green hydrogen production at sea. Renew. Sustain. Energy Rev. 2020, 133, 110166. [Google Scholar] [CrossRef]

- Tian, T.; Li, Y.X.; Huang, L.; Shu, J. Comparative analysis of the economy of hydrogen production technology for offshore wind power consumption. Electr. Power. Constr. 2021, 42, 136–144. [Google Scholar]

- Zhou, K.; Ferreira, J.A.; Haan, S. Optimal energy management strategy and system sizing method for stand-alone photovoltaic-hydrogen systems. Int. J. Hydrogen Energy 2008, 33, 477–489. [Google Scholar] [CrossRef]

- Liu, J.Y.; Zhang, H.; Lei, M.J.; Xue, Y.Z. Experimental study on solar photovoltaic electrolysis of water for hydrogen production. Renew. Energy 2014, 32, 1603–1608. [Google Scholar]

- Zini, G.; Rosa, A.D. Hydrogen systems for large-scale photovoltaic plants: Simulation with forecast and real production data. Int. J. Hydrogen Energy 2014, 39, 107–118. [Google Scholar] [CrossRef]

- Homayouni, F.; Roshandel, R.; Hamidi, A. Techno-economic and environmental analysis of an integrated standalone hybrid solar hydrogen system to supply CCHP loads of a greenhouse in Iran. Int. J. Green. Energy 2017, 14, 295–309. [Google Scholar] [CrossRef]

- Mokhtara, C.; Negrou, B.; Settou, N.; Bouferrouk, A.; Yao, Y.F. Design optimization of grid-connected PV-Hydrogen for energy prosumers considering sector-coupling paradigm: Case study of a university building in Algeria. Int. J. Hydrogen Energy 2021, 46, 37564–37582. [Google Scholar] [CrossRef]

- Song, Y.J.; Mu, H.L.; Li, N.; Shi, X.P.; Zhao, X.W.; Chen, C.N.; Wang, H.Y. Techno-economic analysis of a hybrid energy system for CCHP and hydrogen production based on solar energy. Int. J. Hydrogen Energy 2022, 47, 24533–24547. [Google Scholar] [CrossRef]

- Zhou, W.; Lou, C.Z.; Li, Z.S.; Lu, L.; Yang, H.X. Current status of research on optimum sizing of stand-alone hybrid solar-wind power generation systems. Appl. Energy 2010, 87, 380–389. [Google Scholar] [CrossRef]

- Bajpai, P.; Dash, V. Hybrid renewable energy systems for power generation in stand-alone applications: A review. Renew. Sustain. Energy Rev. 2012, 16, 2926–2939. [Google Scholar] [CrossRef]

- Fathima, A.H.; Palanisamy, K. Optimization in microgrids with hybrid energy systems—A review. Renew. Sustain. Energy Rev. 2015, 45, 431–446. [Google Scholar] [CrossRef]

- Vivas, F.J.; Heras, A.D.; Segura, F.; Andújar, J.M. A review of energy management strategies for renewable hybrid energy systems with hydrogen backup. Renew. Sust. Energy Rev. 2018, 82, 126–155. [Google Scholar] [CrossRef]

- Shi, X.F.; Qian, Y.; Yang, S.Y. Fluctuation analysis of a complementary wind-solar energy system and integration for large scale hydrogen production. ACS. Sustain. Chem. Eng. 2020, 8, 7097–7110. [Google Scholar] [CrossRef]

- Apostolou, D. Optimisation of a hydrogen production-storage-re-powering system participating in electricity and transportation markets. A case study for Denmark. Appl. Energy 2020, 265, 114800. [Google Scholar] [CrossRef]

- Zheng, B.; Bai, Z.; Yuan, Y.; Hu, W.X. Hydrogen production system and capacity optimization based on synergistic operation with multi-type electrolyzers under wind-solar power. Proc. CSEE 2022, 42, 8486–8496. [Google Scholar]

- International Energy Agency. Tracking Clean Energy Progress 2023; International Energy Agency: Paris, France, 2023.

- International Energy Agency. Global Hydrogen Review2021; International Energy Agency: Paris, France, 2021.

- International Energy Agency. ETP Clean Energy Technology Guide; International Energy Agency: Paris, France, 2023.

- International Energy Agency. Hydrogen Production and Storage; International Energy Agency: Paris, France, 2006.

- Acar, C.; Dincer, I. Comparative assessment of hydrogen production methods from renewable and non-renewable sources. Int. J. Hydrogen Energy 2014, 39, 1–12. [Google Scholar] [CrossRef]

- Xie, X.S.; Yang, W.J.; Shi, W.; Zhang, S.S.; Wang, Z.H.; Zhou, J.H. Life cycle assessment of technologies for hydrogen production—A review. Chem. Ind. Eng. Prog. 2018, 37, 2147–2158. [Google Scholar]

- Koroneos, C.J.; Dompros, A.; Roumbas, G.; Moussiopoulos, N. Life cycle assessment of hydrogen fuel production processes. Int. J. Hydrogen Energy 2004, 29, 1443–1450. [Google Scholar] [CrossRef]

- Granovskii, M.; Dincer, I.; Rosen, M.A. Exergetic life cycle assessment of hydrogen production from renewables. J. Power Sources 2007, 167, 461–471. [Google Scholar] [CrossRef]

- Cetinkaya, E.; Dincer, I.; Naterer, G.F. Life cycle assessment of various hydrogen production methods. Int. J. Hydrogen Energy 2012, 37, 2071–2080. [Google Scholar] [CrossRef]

- Ozbilen, A.; Dincer, I.; Rosen, M.A. Comparative environmental impact and efficiency assessment of selected hydrogen production methods. Environ. Impact Assess. Rev. 2013, 42, 1–9. [Google Scholar] [CrossRef]

- Bhandari, R.; Trudewind, C.A.; Zapp, P. Life cycle assessment of hydrogen production via electrolysis—A review. J. Clean. Prod. 2014, 85, 151–163. [Google Scholar] [CrossRef]

- Suleman, F.; Dincer, I.; Agelin-Chaab, M. Environmental impact assessment and comparison of some hydrogen production options. Int. J. Hydrogen Energy 2015, 40, 6976–6987. [Google Scholar] [CrossRef]

- Bartels, J.R.; Pate, M.B.; Olson, N.K. An economic survey of hydrogen production from conventional and alternative energy sources. Int. J. Hydrogen Energy 2010, 35, 8371–8384. [Google Scholar] [CrossRef]

- Li, Y.Y. Research on Evaluating the Several Methods of Hydrogen Production Technology by Life Cycle Assessment; Xi’an University of Architecture and Technology: Xi’an, China, 2010. [Google Scholar]

- Olateju, B.; Kumar, A.; Secanell, M. A techno-economic assessment of large scale wind-hydrogen production with energy storage in Western Canada. Int. J. Hydrogen Energy 2016, 41, 8755–8776. [Google Scholar] [CrossRef]

- Nikolaidis, P.; Poullikkas, A. A comparative overview of hydrogen production processes. Renew. Sustain. Energy Rev. 2017, 67, 597–611. [Google Scholar] [CrossRef]

- Milani, D.; Kiani, A.; McNaughton, R. Renewable-powered hydrogen economy from Australia’s perspective. Int. J. Hydrogen Energy 2020, 45, 24125–24145. [Google Scholar] [CrossRef]

- Wang, Y.Z.; Zhou, S.; Zhou, X.W.; Ou, X.M. Cost analysis of different hydrogen production methods in China. Energy China 2021, 43, 29–37. [Google Scholar]

- Chi, J.; Yu, H.M. Water electrolysis based on renewable energy for hydrogen production. Chin. J. Catal. 2018, 39, 390–394. [Google Scholar] [CrossRef]

- Sigal, A.; Leiva, E.P.M.; Rodrıguez, C.R. Assessment of the potential for hydrogen production from renewable resources in Argentina. Int. J. Hydrogen Energy 2014, 39, 8204–8214. [Google Scholar] [CrossRef]

- CIECC; EnerScen. Global Hydrogen Energy Industry Outlook Report; CIECC: Beijing, China, 2024. [Google Scholar]

- Maggio, G.; Nicita, A.; Squadrito, G. How the hydrogen production from RES could change energy and fuel markets: A review of recent literature. Int. J. Hydrogen Energy 2019, 44, 11371–11384. [Google Scholar] [CrossRef]

- Pudukudy, M.; Yaakob, Z.; Mohammad, M.; Narayanan, B.; Sopian, K. Renewable hydrogen economy in Asia-Opportunities and challenges: An overview. Renew. Sustain. Energy Rev. 2014, 30, 743–757. [Google Scholar] [CrossRef]

- Ding, F.; Li, X.G.; Liang, Z.Q.; Wu, M.; Zhu, Y.H.; Feng, D.H.; Zhou, Y. Review of Foreign Experience in Promoting Renewable Energy Development and Inspiration to China. Electr. Power Constr. 2022, 43, 1–11. [Google Scholar]

- International Renewable Energy Agency. Green Hydrogen Cost Reduction: Scaling up Electrolysers to Meet the 1.5 °C Climate Goal; International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2020. [Google Scholar]

- Ju, L.W.; Liu, L. Explore the Greater Potential of Wind and Solar Power; Economic Daily Press: Beijing, China, 2021. [Google Scholar]

- Wang, H.X.; Xu, W.Y.; Zhang, Z.J. Development status and suggestions for green hydrogen energy produced by water electrolysis from renewable energy. Chem. Ind. Eng. Prog. 2022, 41, 118–131. [Google Scholar]

- Guo, B.W.; Luo, D.; Zhou, H.J. Recent advances in renewable energy electrolysis hydrogen production technology and related electrocatalysts. Chem. Ind. Eng. Prog. 2021, 40, 2933–2951. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Utilization Ratio of Photovoltaic | Utilization Ratio of Wind Power | |

|---|---|---|

| National average | 98.3% | 96.8% |

| Western Inner Mongolia | 97.4% | 92.9% |

| Eastern Inner Mongolia | 98.6% | 90.0% |

| Chongqing | 100.0% | 100.0% |

| Sichuan | 100.0% | 100.0% |

| Shaanxi | 97.8% | 95.8% |

| Gansu | 98.2% | 93.8% |

| Qinghai | 91.1% | 92.7% |

| Ningxia | 97.4% | 98.5% |

| Xinjiang | 97.2% | 95.4% |

| Tibet | 80.0% | 100.0% |

| Guangxi | 100.0% | 100.0% |

| Guizhou | 99.4% | 99.7% |

| Yunnan | 99.5% | 99.9% |

| AWE | PEM | SOEC | AEM | |

|---|---|---|---|---|

| Electrolyte | NaOH/KOH | proton exchange membrane | solid oxide | anion exchange membrane |

| Anode catalyst | Ni | Pt, Ir, Ru | CaTiO3 | Ni/NiFeCo alloy |

| Cathode catalyst | Nickel alloy | Pt, Pt/C | Ni/ZrO2 | Ni |

| Temperature/°C | 60–90 | 50–90 | 700–900 | 40–60 |

| Pressure/MPa | 0.1–3.0 | <7.0 | 0.1 | <3.5 |

| Current density/(A·cm−2) | 0.2–0.4 | 1.0–3.0 | 0.3–2.0 | 0.8–2.5 |

| Electrolytic efficiency/% | 60–75 | 70–90 | 85–100 | - |

| Energy consumption /[(kW·h)·cm−3] | 4.5–5.5 | 3.8–5.0 | 2.6–3.6 | - |

| Fixed cost/(USD·kW−1) | 880–1650 | 1540–2550 | >2000 | - |

| Life span/kh | 60–120 | 60–100 | 8–20 | 10–30 |

| Industrialization degree | full industrialization | preliminary commercialization | initial demonstration | laboratory stage |

| Advantages | mature technology low cost | adapt to fluctuating power, pollution-free | high efficiency, low energy consumption | adapt to fluctuating power, low cost |

| Disadvantages | low efficiency pollution | high cost | high temperature | immature technology |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wang, L.; Liu, W.; Sun, H.; Yang, L.; Huang, L. Advancements and Policy Implications of Green Hydrogen Production from Renewable Sources. Energies 2024, 17, 3548. https://doi.org/10.3390/en17143548

Wang L, Liu W, Sun H, Yang L, Huang L. Advancements and Policy Implications of Green Hydrogen Production from Renewable Sources. Energies. 2024; 17(14):3548. https://doi.org/10.3390/en17143548

Chicago/Turabian StyleWang, Leiming, Wei Liu, Haipeng Sun, Li Yang, and Liang Huang. 2024. "Advancements and Policy Implications of Green Hydrogen Production from Renewable Sources" Energies 17, no. 14: 3548. https://doi.org/10.3390/en17143548

APA StyleWang, L., Liu, W., Sun, H., Yang, L., & Huang, L. (2024). Advancements and Policy Implications of Green Hydrogen Production from Renewable Sources. Energies, 17(14), 3548. https://doi.org/10.3390/en17143548