The Significance of the Financial Situation of Local Government Units for Their Energy Transition Activities: The Case of the Podkarpackie Region

Abstract

1. Introduction

2. Literature Review

3. Materials and Methods

- income independence ratio (IIR): share of own income in relation to total income (average for 2019–2022, in %); calculated according to the formula:

- budget result (BR): budget balance in relation to total income (average for 2019–2022, in %); calculated according to the formula:

- debt level (DL): debt in relation to total income realised (as at the end of 2022, in %) calculated according to the formula:

- LGUs with an average level of own income for 2019–2022 in relation to total income above the region average (group 1) and below the region average (group 2);

- LGUs with an average budget balance for 2019–2022 in relation to total income, showing a surplus (group 1) or a deficit (group 2);

- LGUs with an average debt level in relation to total income realised in 2022 below the average for the sample (group 1) and above the average for the sample (group 2).

4. Results

4.1. Characteristics of the Study Sample

4.1.1. Financial Situation of the Surveyed LGUs

4.1.2. Investment Activity of LGUs

4.2. LGUs’ Spending on ET

4.2.1. Level of LGUs’ Investment in ET

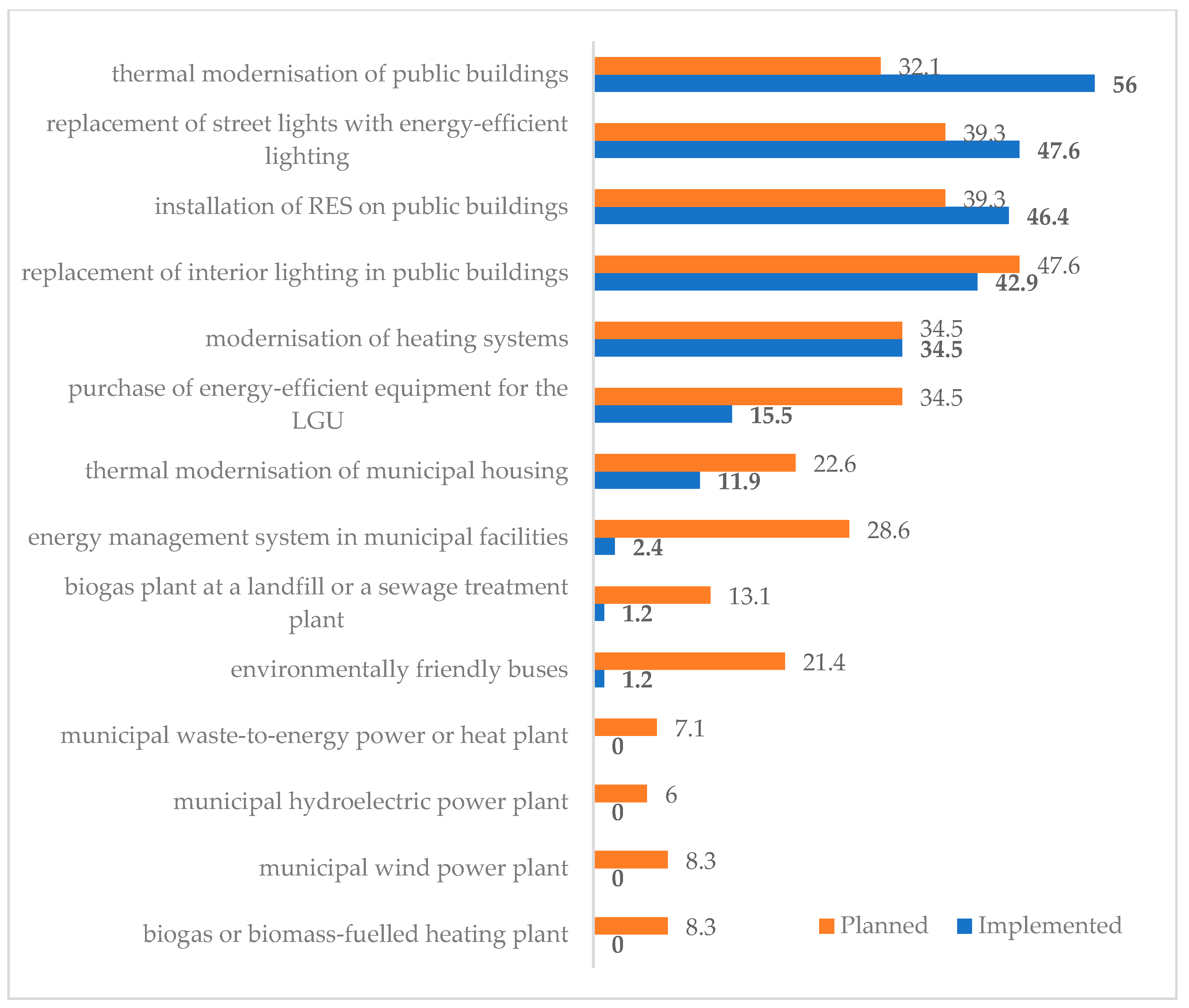

4.2.2. Directions of LGUs’ Investments in ET

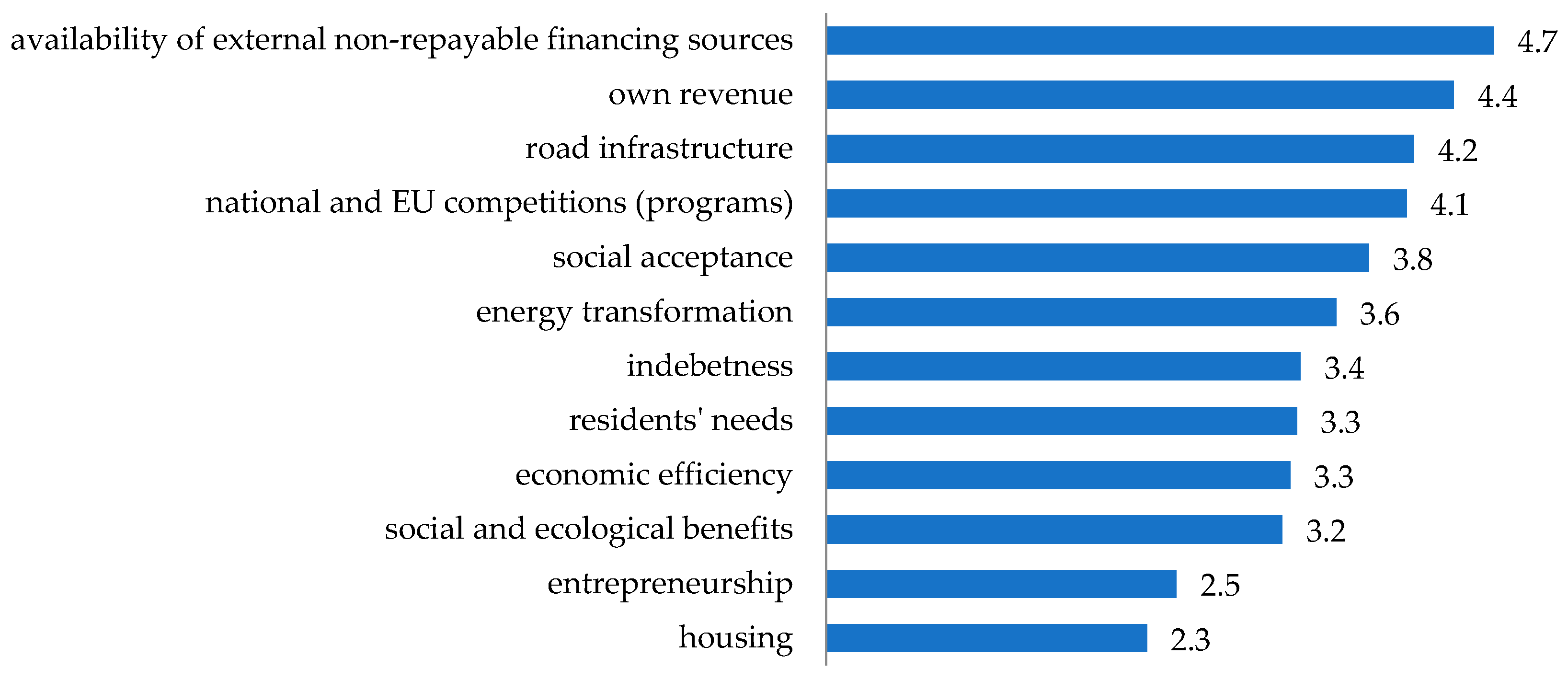

4.2.3. Funding Sources of LGUs’ Investments in ET

5. Discussion

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Resolution Adopted by the General Assembly on 25 September 2015: Transforming Our World: The 2030 Agenda for Sustainable Development; A/RES/70/1; United Nations; General Assembly: New York, NY, USA, 2015.

- Sustainable Development in the European Union. Monitoring Report on Progress towards the SDGs in an EU Context, 2023th ed.; Publications Office of the European Union: Luxembourg, 2023. [Google Scholar]

- Sustainable Development in the European Union. Overview of Progress towards the SDGs in an EU Context, 2022th ed.; Publications Office of the European Union: Luxembourg, 2022. [Google Scholar]

- Tian, J.; Yu, L.; Xue, R.; Zhuang, S.; Shan, Y. Global low-carbon energy transition in the post-COVID-19 era. Appl. Energy 2022, 307, 118205. [Google Scholar] [CrossRef] [PubMed]

- The European Green Deal; COM(2019) 640 Final; European Commission: Brussels, Belgium, 2019.

- European Commission. ‘Fit for 55′: Delivering the EU’s 2030 Climate Target on the Way to Climate Neutrality; Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions; European Commission: Brussels, Belgium, 2021. [Google Scholar]

- EU Clean Energy for all Europeans Package, The Clean Energy Package–CEP. Available online: https://ec.europa.eu/energy/topics/energy-strategy/clean-energy-all-europeans_en (accessed on 15 October 2022).

- Bąk, I.; Tarczyńska-Łuniewska, M.; Barwińska-Małajowicz, A.; Hydzik, P.; Kusz, D. Is Energy Use in the EU Countries Moving toward Sustainable Development? Energies 2022, 15, 6009. [Google Scholar] [CrossRef]

- Polish Energy Policy until 2040 (EPP 2024). Available online: https://www.gov.pl/web/climate/energy-policy-of-poland-until-2040-epp2040 (accessed on 30 March 2024).

- The Energy Market Agency. Available online: https://www.are.waw.pl/badania-statystyczne/prezentacja-wybranych-danych (accessed on 28 April 2024).

- Energy Regulatory Office. Biuletyn Urzędu Regulacji Energetyki. 2023; Volume 1. Available online: https://www.ure.gov.pl/pl/urzad/informacje-ogolne/edukacja-i-komunikacja/publikacje/biuletyn-urzedu-regula/11383,Biuletyn-Urzedu-Regulacji-Energetyki-2023.html (accessed on 28 April 2024).

- Energy Regulatory Office. Energetyka Cieplna w Liczbach—2022 (Thermal Energy in Numbers—2022); URE: Warszawa, Poland, 2023. [Google Scholar]

- Greenhouse Gas Emissions by Country and Sector (Infographic). European Parliament. Available online: https://www.europarl.europa.eu/topics/en/article/20180301STO98928/greenhouse-gas-emissions-by-country-and-sector-infographic (accessed on 16 April 2024).

- Emisje Gazów Cieplarnianych w Polsce—Status quo Według KOBiZE. Available online: https://www.teraz-srodowisko.pl/aktualnosci/KOBiZE-emisja-gazow-cieplarnianych-w-Polsce-Pawel-Mzyk-11271.html (accessed on 20 April 2024).

- Tzeremes, P.; Dogan, E.; Karimi Alavijeh, N. Analyzing the nexus between energy transition, environment and ICT: A step towards COP26 targets. J. Environ. Manag. 2023, 326, 116598. [Google Scholar] [CrossRef] [PubMed]

- Perrin, J.-A.; Bouissete, C. Emerging local public action in renewable energy production. Discussion of the territorial dimension of the energy transition based on the cases of four intermunicipal cooperation entities in France. Energy Policy 2022, 168, 113143. [Google Scholar] [CrossRef]

- Standar, A.; Kozera, A.; Satoła, Ł. The Importance of Local Investments Co-Financed by the European Union in the Field of Renewable Energy Sources in Rural Areas of Poland. Energies 2021, 14, 450. [Google Scholar] [CrossRef]

- Kozera, A.; Standar, A.; Genstwa, N. Are Most Polluted Regions Most Active in Energy Transition Processes? A Case Study of Polish Regions Acquiring EU Funds for Local Investments in Renewable Energy Sources. Energies 2023, 16, 7655. [Google Scholar] [CrossRef]

- Traill, H.; Cumbers, A. The state of municipal energy transitions: Multi-scalar constraints and enablers of Europe’s post-carbon energy ambitions. Eur. Urban Reg. Stud. 2022, 30, 93–106. [Google Scholar] [CrossRef]

- Rankl, F.; Collins, A.; Tyers, R.; Carver, D. The Role of Local Government in Delivering Net Zero, Debate Pack 2 June 2023, Number CDP-2023-0122; House of Commons Library: London, UK, 2023. [Google Scholar]

- Progress in Reducing Emissions. 2022 Report to Parliament; Climate Change Committee: London, UK, 2022. [Google Scholar]

- Rakowska, J.; Ozimek, I. Renewable Energy Attitudes and Behaviour of Local Governments in Poland. Energies 2021, 14, 2765. [Google Scholar] [CrossRef]

- Kozera, A.; Satoła, Ł.; Standar, A.; Dworakowska-Raj, M. Regional diversity of low-carbon investment support from EU funds in the 2014–2020 financial perspective based on the example of Polish municipalities. Renew. Sustain. Energy Rev. 2022, 168, 112863. [Google Scholar] [CrossRef]

- Cheung, G.; Davies, P.J.; Trück, S. Financing alternative energy projects: An examination of challenges and opportunities for local government. Energy Policy 2016, 97, 354–364. [Google Scholar] [CrossRef]

- Hadfield, P.; Cook, N. Financing the Low-Carbon City: Can Local Government Leverage Public Finance to Facilitate Equitable Decarbonisation? Urban Policy Res. 2019, 37, 13–29. [Google Scholar] [CrossRef]

- Tingey, M.; Webb, J. Net Zero Localities: Ambition & Value in UK Local Authority Investment; Edinburgh Research Explorer; The University of Edinburgh, University of Strathclyde Publishing: Glasgow, UK, 2020. [Google Scholar]

- Kuzemko, C.; Britton, J. Policy, politics and materiality across scales: A framework for understanding local government sustainable energy capacity applied in England. Energy Res. Soc. Sci. 2020, 62, 101367. [Google Scholar] [CrossRef]

- Klepacki, B.; Kusto, B.; Bórawski, P.; Bełdycka-Bórawska, A.; Michalski, K.; Perkowska, A.; Rokicki, T. Investments in Renewable Energy Sources in Basic Units of Local Government in Rural Areas. Energies 2021, 14, 3170. [Google Scholar] [CrossRef]

- Kata, R.; Pitera, R. Local Authority Investments in the Field of Energy Transition and Their Determinants (on the Example of South-Eastern Poland). Energies 2023, 16, 819. [Google Scholar] [CrossRef]

- Mey, F.; Diesendorf, M.; MacGill, I. Can local government play a greater role for community renewable energy? A case study from Australia. Energy Res. Soc. Sci. 2016, 21, 33–43. [Google Scholar] [CrossRef]

- Yaqoot, M.; Diwan, P.; Kandpal, T.C. Review of barriers to the dissemination of decentralized renewable energy systems. Renew. Sustain. Energy Rev. 2016, 58, 477–490. [Google Scholar] [CrossRef]

- Cohen, J.J.; Azarova, V.; Kollmann, A.; Reichl, J. Preferences for community renewable energy investments in Europe. Energy Econ. 2021, 100, 105386. [Google Scholar] [CrossRef]

- Kata, R.; Lechwar, M.; Dybka, S.; Cyran, K.; Pitera, R. Kredytowanie Inwestycji Związanych z Energetyką Odnawialną Realizowanych Przez LGU Oraz Podmioty ze Sfery Mieszkalnictwa; Raport Programu Analityczno-Badawczego Fundacji Warszawski Instytut Bankowości, SYGN. WIB PAB 24/2020: Warszawa, Poland, 2020. [Google Scholar]

- Graczyk, A.M.; Graczyk, A.; Żołyniak, T. System for Financing Investments in Renewable Energy Sources in Poland. In Finance and Sustainability; Springer Proceedings in Business and Economics; Daszyńska-Żygadło, K., Bem, A., Ryszawska, B., Jáki, E., Hajdíková, T., Eds.; Springer: Cham, Switzerland, 2020; pp. 153–166. [Google Scholar] [CrossRef]

- Stokes, L.C.; Breetz, H. Politics in the U.S. energy transition: Case studies of solar, wind, biofuels and electric vehicles policy. Energy Policy 2018, 113, 76–86. [Google Scholar] [CrossRef]

- Eurostat Database: Gross Domestic Product (GDP) at Current Market Prices by NUTS 2 Regions. nama_10r_2gdp. Available online: https://ec.europa.eu/eurostat/databrowser/view/nama_10r_2gdp/default/table?lang=en&category=na10.nama10.nama_10reg.nama_10r_gdp (accessed on 22 February 2024). [CrossRef]

- Energy Poverty—Indicators. 2022. Available online: https://dane.gov.pl/pl/dataset/2160/resource/48573/table?page=1&per_page=20&q=&sort= (accessed on 4 March 2024).

- Biernat-Jarka, A.; Trębska, P.; Jarka, S. The Role of Renewable Energy Sources in Alleviating Energy Poverty in Households in Poland. Energies 2021, 14, 2957. [Google Scholar] [CrossRef]

- Przegląd Regionalny. Województwo Podkarpackie 2022; Urząd Marszałkowski Województwa Podkarpackiego, Uniwersytet Rzeszowski: Rzeszów, Poland, 2023. [Google Scholar]

- Sprawozdanie z Działalności Regionalnych izb Obrachunkowych i Wykonania Budżetu Przez Jednostki Samorządu Terytorialnego w 2022 Roku; Krajowa Rada Regionalnych Izb Obrachunkowych: Warszawa, Poland, 2023.

- List of Projects Implemented from European Funds in Poland in 2014–2020. Available online: https://www.funduszeeuropejskie.gov.pl/strony/o-funduszach/projekty/lista-projektow/lista-projektow-realizowanych-z-funduszyeuropejskich-w-polsce-w-latach-2014-2020/ (accessed on 20 September 2023).

- Feng, Y.; Zhang, J.; Geng, Y.; Jin, S.; Zhu, Z.; Liang, Z. Explaining and modeling the reduction effect of low-carbon energy transition on energy intensity: Empirical evidence from global data. Energy 2023, 281, 128276. [Google Scholar] [CrossRef]

- Panwar, N.L.; Kaushik, S.C.; Kothari, S. Role of renewable energy sources in environmental protection: A review. Renew. Sustain. Energy Rev. 2011, 15, 1513–1524. [Google Scholar] [CrossRef]

- Skwierz, S.; Lewarski, M.; Krupin, V.; Gorzałczyński, A.; Jeszke, R.; Pyrka, M.; Rosłaniec, M.; Rabiega, W.; Boratyński, J.; Tatarewicz, I.; et al. POLSKA NET-ZERO 2050: Podręcznik Transformacji Energetycznej dla Samorządów; Instytut Ochrony Środowiska—Państwowy Instytut Badawczy/Krajowy Ośrodek Bilansowania i Zarządzania Emisjami/Centrum Analiz Klimatyczno-Energetycznych: Warszawa, Poland, 2021. [Google Scholar]

- Feng, Y.; Shoaib, M.; Akram, R.; Alnafrah, I.; Ai, F.; Irfan, M. Assessing and prioritizing biogas energy barriers: A sustainable roadmap for energy security. Renew. Energy 2024, 223, 120053. [Google Scholar] [CrossRef]

- Kosiński, E.; Trupkiewicz, M. Gmina jako podmiot systemu wspierania wytwarzania energii elektrycznej z odnawialnych źródeł energii (A municipality (gmina) as part of the support system for generation of electricity from renewable energy sources). Ruch Praw. Ekon. Socjol. 2016, 78, 93–107. [Google Scholar] [CrossRef]

- Kata, R.; Cyran, K.; Dybka, S.; Lechwar, M.; Pitera, R. The Role of Local Government in Implementing Renewable Energy Sources in Households (Podkarpacie Case Study). Energies 2022, 15, 3163. [Google Scholar] [CrossRef]

- Haraldsvik, M.; Hopland, A.O.; Kvamsdal, S.F. Determinants of municipal investments. Appl. Econ. 2023, 1–14. [Google Scholar] [CrossRef]

- Hoppe, T.; van den Berg, M.M.; Coenen, F.H. Reflections on the uptake of climate change policies by local governments: Facing the challenges of mitigation and adaptation. Energy Sustain. Soc. 2014, 4, 8. [Google Scholar] [CrossRef]

- Bąk, I.; Budzeń, D.; Kryk, B.; Sobczyk, A. Financial involvement of local government units in achieving environmental objectives of sustainable development in Poland. Econ. Environ. 2023, 86, 288–311. [Google Scholar] [CrossRef]

- Lackowska, M.; Swianiewicz, P. Czynniki warunkujące preferencje i działania samorządów gminnych w Polsce w zakresie łagodzenia i adaptacji do zmian klimatycznych (Factors influencing preferences and actions of Polish municipal authorities regarding mitigation and adaptation to climate change). Przegląd Geogr. 2017, 149, 55–80. [Google Scholar] [CrossRef]

- Budzeń, D.; Marchewka-Bartkowiak, K. Wydatki zrównoważone środowiskowo w budżetach lokalnych (Environmentally sustainable expenditure in local budgets). Optimum. Econ. Stud. 2022, 3, 41–54. [Google Scholar] [CrossRef]

- Sala, K. Energetyka słoneczna jako czynnik rozwoju regionów i gmin w Polsce (Solar Power as a Factor in the Development of Regions and Communes in Poland). Przedsiębiorczość Eduk. 2018, 14, 125–136. [Google Scholar] [CrossRef]

- Martins, R.D.A.; Ferreira, L.d.C. Opportunities and constraints for local and subnational climate change policy in urban areas: Insight from diverse contexts. Int. J. Glob. Environ. Issues 2011, 11, 37–53. [Google Scholar] [CrossRef]

- Szlufik, M.; Sasinowski, M. Odnawialne źródła energii jako szansa na stworzenie proekologicznego wizerunku jednostki samorządu terytorialnego (Renewable sources of energy as a chance of creating pro-ecological image of local self-government). Młody Jurysta 2018, 4, 67–78. [Google Scholar]

- Kasztelan, A. On the Road to a Green Economy: How Do European Union Countries ‘Do Their Homework’? Energies 2021, 14, 5941. [Google Scholar] [CrossRef]

- Śleszyński, P.; Nowak, M.; Brelik, A.; Mickiewicz, B.; Oleszczyk, N. Planning and Settlement Conditions for the Development of Renewable Energy Sources in Poland: Conclusions for Local and Regional Policy. Energies 2021, 14, 1935. [Google Scholar] [CrossRef]

- Islam, T.; Meade, N. The impact of attribute preferences on adoption timing: The case of photo-voltaic (PV) solar cells for household electricity generation. Energy Policy 2013, 55, 521–530. [Google Scholar] [CrossRef]

- Wójcik, A.; Byrka, K. Raport z Badań Opinii Społecznej Dotyczącej Energetyki w Polsce; Projekt Energia odNowa; WWF Polska: Warszawa, Poland, 2018. [Google Scholar]

- IBRiS. Zielony potencjał społeczny. Polska i Europa Środkowo-Wschodnia; IBRiS: Warszawa, Poland, 2020. [Google Scholar]

- OECD/IEA. Cities, Towns & Renewable Energy, Yes in My Front Yard; OECD/IEA: Paris, France, 2009. [Google Scholar]

- Karanasios, K.; Parker, P. Explaining the Diffusion of Renewable Electricity Technologies in Canadian Remote Indigenous Communities through the Technological Innovation System Approach. Sustainability 2018, 10, 3871. [Google Scholar] [CrossRef]

- Michalena, E.; Angeon, V. Local challenges in the promotion of renewable energy sources: The case of Crete. Energy Policy 2009, 37, 2018–2026. [Google Scholar] [CrossRef]

- Kerr, S.; Johnson, K.; Weir, S. Understanding community benefit payments from renewable energy development. Energy Policy 2017, 105, 202–211. [Google Scholar] [CrossRef]

- Malinowska-Misiąg, E. Fiscal rules versus the financial condition of EU local government units. Pr. Nauk. Uniw. Ekon. We Wrocławiu 2023, 67, 71–80. [Google Scholar] [CrossRef]

- Jastrzębska, M. Zdrowie fiskalne jednostek samorządu terytorialnego. Optimum. Econ. Stud. 2023, 3, 7–23. [Google Scholar] [CrossRef]

- Malinowski, M. Wielowymiarowe zależności między kondycją finansową gmin wiejskich a poziomem życia mieszkańców. Wieś Rol. 2023, 2, 67–89. [Google Scholar] [CrossRef] [PubMed]

- Kita, R.; Łukomska-Szarek, J. Zarządzanie finansami gmin miejskich województwa śląskiego w latach 2019-2021 z wykorzystaniem metody TOPSIS. Akad. Zarządzania 2023, 7, 206–227. [Google Scholar] [CrossRef]

- Ładysz, I.M. Wybrane współczesne problemy jednostek samorządu terytorialnego w Polsce w latach 2018–2022. Rocz. Bezpieczeństwa Międzynarodowego 2023, 17, 123–143. [Google Scholar] [CrossRef]

- Grzebyk, M.; Musiał-Malago, M. Sytuacja finansowa gmin województwa podkarpackiego w latach 1999–2002. Zeszyty Naukowe Akademii Ekonomicznej w Krakowie 2006, 693, 143–155. [Google Scholar]

- Young, J.; Macura, A. Forging Local Energy Transition in the Most Carbon-Intensive European Region of the Western Balkans. Energies 2023, 16, 2077. [Google Scholar] [CrossRef]

- Patel, S.; Parkins, J.R. Assessing motivations and barriers to renewable energy development: Insights from a survey of municipal decision-makers in Alberta, Canada. Energy Rep. 2023, 9, 5788–5798. [Google Scholar] [CrossRef]

- Central Statistical Office, Local Data Bank. Available online: https://bdl.stat.gov.pl/BDL/start (accessed on 11 March 2024).

- Kotlińska, J.; Żukowska, H.; Zuba-Ciszewska, M.; Mizak, A.; Krawczyk-Sawicka, A. Kondycja finansowa jednostek samorządu terytorialnego i jej miary (Financial condition of local government units and its measures). Ekonomista 2022, 3, 367–390. [Google Scholar] [CrossRef]

- Filipiak, B.Z. Indywidualny wskaźnik zadłużenia jako determinanta oceny kondycji finansowej jednostki samorządu terytorialnego (Individual debt ratio as a determinant of the assessment of the financial condition of a local government unit). Soc. Inequalities Econ. Growth 2018, 56, 73–86. [Google Scholar] [CrossRef]

- Dylewski, M.; Filipiak, B.; Gorzałczyńska-Koczkodaj, M. Analiza Finansowa w Jednostkach Samorządu Terytorialnego; Municipium: Warszawa, Poland, 2004. [Google Scholar]

- Jóźwiak, J.; Podgórski, J. Statystyka od Podstaw; PWE: Warszawa, Poland, 2012. [Google Scholar]

- Aczel, A.D. Statystyka w Zarządzaniu; PWN: Warszawa, Poland, 2005. [Google Scholar]

- Stanisz, A. Przystępny Kurs Statystyki z Zastosowaniem STATISTICA PL na Przykładach z Medycyny, t. 1: Statystyki Podstawowe; StatSoft Polska: Kraków, Poland, 2006. [Google Scholar]

- Conover, W.J. Practical Non-Parametric Statistics, 2nd ed.; John Wiley and Sons: New York, NY, USA, 1980. [Google Scholar]

- Podsiad, A.; Piłat, A.; Walewski, M. Kondycja Samorządów Terytorialnych w 2022 r. Raport BGK, Warszawa. 2023. Available online: https://www.prawo.pl/samorzad/kondycja-samorzadow-terytorialnych-w-2022-r-raport-bkg,521410.html (accessed on 20 April 2024).

- Veiga, L.G.; Veiga, F.J. Determinants of Portuguese Local Governments’ Indebtedness; NIPE Work. Papers 16; NIPE—Universidade do Minho: Braga, Portugal, 2014. [Google Scholar]

- Kopańska, A.; Asinski, R. Fiscal and political determinants of local government involvement in public-private partnership (PPP). Local Gov. Stud. 2019, 45, 957–976. [Google Scholar] [CrossRef]

- Heinemann, F. Factor mobility, government debt and the decline in public investment. Int. Econ. Econ. Policy 2006, 3, 11–26. [Google Scholar] [CrossRef]

- Banaszewska, M. The determinants of local public investments in Poland. Equilibrium. Q. J. Econ. Econ. Policy 2018, 13, 105–121. [Google Scholar] [CrossRef]

- Bröthaler, J.; Getzner, M.; Haber, G. Sustainability of local government debt: A case study of Austrian municipalities. Empirica 2015, 42, 521–546. [Google Scholar] [CrossRef]

- Traill, H.; Cumbers, A.; Gray, N. The State of European Municipal Energy Transition: An Overview of Current Trends; University of Glasgow: Glasgow, UK, 2021. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Specification | LGU Total | Poviats | Communes Total | Urban Communes 1 | Rural Communes | Urban-Rural Communes |

|---|---|---|---|---|---|---|

Podkarpackie region

| 181 | 21 | 160 | 16 | 108 | 36 |

Research sample

| 84 | 14 | 70 | 5 | 48 | 17 |

| 46.4 | 66.7 | 43.8 | 31.3 | 44.4 | 47.2 |

| Local Units | IIR | BR | DL | ||||

|---|---|---|---|---|---|---|---|

| Region (N = 181) | Sample (n = 84) | Region (N = 181) | Sample (n = 84) | Region (N = 181) | Sample (n = 79) | ||

| LGU—total | a * | 33.4 | 32.0 | 3.1 | 3.1 | 22.5 | 15.9 |

| b | 26.5 | 22.6 | 82.3 | 79.8 | - | 58.2 | |

| Poviats | a | 33.6 | 31.6 | 4.7 | 4.3 | 12.0 | 12.2 |

| b | 38.1 | 28.6 | 95.2 | 92.9 | - | 78.6 | |

| Communes: | |||||||

| a | 33.4 | 32.1 | 2.9 | 2.9 | 18.4 | 16.6 |

| b | 25.0 | 21.4 | 80.6 | 77.1 | - | 53.8 | |

| a | 48.1 | 45.2 | −0.3 | −0.6 | 30.1 | 31.5 |

| b | 87.5 | 60.0 | 50.0 | 40.0 | - | 20.2 | |

| a | 31.4 | 29.6 | 3.6 | 3.7 | 12.5 | 12.4 |

| b | 16.7 | 12.5 | 88.9 | 85.4 | - | 69.8 | |

| a | 33.1 | 35.1 | 2.1 | 1.6 | 21.4 | 23.0 |

| b | 22.2 | 35.3 | 69.4 | 64.7 | - | 23.5 | |

| Local Units | Region (N = 181) | Sample (n = 84) | ||||||

|---|---|---|---|---|---|---|---|---|

| 2019 | 2020 | 2021 | 2022 | 2019 | 2020 | 2021 | 2022 | |

| LGU—total | 17.4 | 15.2 | 14.9 | 19.1 | 15.4 | 14.5 | 15.0 | 18.7 |

| Poviats | 18.2 | 15.9 | 16.0 | 23.8 | 17.0 | 13.3 | 15.3 | 20.2 |

| Communes—total | 17.9 | 15.3 | 14.8 | 17.3 | 15.0 | 14.7 | 14.9 | 18.4 |

| 15.5 | 15.5 | 14.5 | 16.2 | 13.5 | 14.1 | 14.3 | 16.5 |

| 17.2 | 15.1 | 14.9 | 19.2 | 14.9 | 14.7 | 15.7 | 18.8 |

| 18.7 | 14.7 | 13.7 | 17.2 | 15.9 | 15.0 | 12.7 | 17.9 |

| Local Units | Total | IIR | BR | DL | |||

|---|---|---|---|---|---|---|---|

| Group 1 | Group 2 | Group 1 | Group 2 | Group 1 | Group 2 | ||

| LGU total | 12.2 | 12.4 | 12.2 | 11.7 | 14.6 | 15.6 | 5.9 |

| Poviats | 6.8 | 7.9 | 6.4 | 6.6 | 10.0 | 7.2 | 5.3 |

| Communes—total | 13.5 | 13.8 | 13.4 | 13.1 | 14.9 | 18.8 | 5.9 |

| 4.9 | 7.3 | 0.0 | 0.0 | 7.3 | 0.0 | 4.9 |

| 16.1 | 22.7 | 15.1 | 15.1 | 22.8 | 19.5 | 6.7 |

| 7.0 | 5.8 | 7.7 | 6.1 | 8.5 | 13.0 | 5.3 |

| Correlation between Scale of ET Investment with: | Total | IIR | BR | DL | |||

|---|---|---|---|---|---|---|---|

| Group 1 | Group 2 | Group 1 | Group 2 | Group 1 | Group 2 | ||

| Own income to total income (%) | 0.03 | 0.059 | −0.04 | 0.017 | −0.24 | 0.12 | 0.05 |

| Budget result to total income (%) | 0.033 | 0.15 | 0.05 | 0.171 * | 0.01 | 0.15 | −0.28 * |

| Debt level to total income (%) | −0.13 | 0.03 | −0.18 * | −0.21 * | −0.07 | −0.1 | 0.19 |

| Investments | Implemented Investments | Planned Investments | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Total | LGU Type | IIR | BR | DL | Total | LGU Type | IIR | BR | DL | |||||||||

| Poviats | Communes | Group 1 | Group 2 | Group 1 | Group 2 | Group 1 | Group 2 | Poviats | Communes | Group 1 | Group 2 | Group 1 | Group 2 | Group 1 | Group 2 | |||

| A | 56.0 | 57.1 | 55.7 | 57.9 | 55.4 | 53.7 | 64.7 | 58.7 | 57.6 | 32.1 | 35.7 | 31.4 | 31.6 | 32.3 | 32.8 | 29.4 | 30.4 | 30.3 |

| B | 11.9 | 0.0 | 14.3 | 15.8 | 10.8 | 10.4 | 17.6 | 8.7 | 18.2 | 22.6 | 0.0 | 27.1 | 21.1 | 23.1 | 19.4 | 35.3 | 21.7 | 21.2 |

| C | 34.5 | 28.6 | 35.7 | 21.1 | 38.5 | 34.3 | 35.3 | 34.8 | 39.4 | 34.5 | 35.7 | 34.3 | 52.6 | 29.2 | 31.3 | 47.1 | 37.0 | 27.3 |

| D | 47.6 | 14.3 | 54.3 | 36.8 | 50.8 | 44.8 | 58.8 | 43.5 | 54.5 | 39.3 | 7.1 | 45.7 | 52.6 | 35.4 | 38.8 | 41.2 | 37.0 | 39.4 |

| E | 46.4 | 50.0 | 47.1 | 42.1 | 47.7 | 46.3 | 47.1 | 41.3 | 57.6 | 39.3 | 28.6 | 41.4 | 47.4 | 36.9 | 37.3 | 47.1 | 50.0 | 24.2 |

| F | 42.9 | 35.7 | 44.3 | 36.8 | 44.6 | 43.3 | 41.2 | 45.7 | 42.4 | 47.6 | 42.9 | 48.6 | 47.4 | 47.7 | 46.3 | 52.9 | 45.7 | 45.5 |

| G | 2.4 | 7.1 | 1.4 | 5.3 | 1.5 | 1.5 | 5.9 | 2.2 | 3.0 | 28.6 | 14.3 | 31.4 | 31.6 | 27.7 | 26.9 | 35.3 | 26.1 | 30.3 |

| H | 15.5 | 28.6 | 12.9 | 21.1 | 13.8 | 13.4 | 23.5 | 15.2 | 15.2 | 34.5 | 28.6 | 35.7 | 31.6 | 35.4 | 35.8 | 29.4 | 37.0 | 27.3 |

| I | 1.2 | 0.0 | 1.4 | 5.3 | 0.0 | 0.0 | 5.9 | 0.0 | 3.0 | 21.4 | 7.1 | 24.3 | 21.1 | 21.5 | 19.4 | 29.4 | 15.2 | 27.3 |

| J | 1.2 | 0.0 | 1.4 | 0.0 | 1.5 | 0.0 | 5.9 | 2.2 | 0.0 | 13.1 | 0.0 | 15.7 | 5.3 | 15.4 | 13.4 | 11.8 | 13.0 | 12.1 |

| K | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 8.3 | 0.0 | 10.0 | 5.3 | 9.2 | 9.0 | 5.9 | 6.5 | 9.1 |

| L | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 8.3 | 0.0 | 10.0 | 5.3 | 9.2 | 9.0 | 5.9 | 6.5 | 9.1 |

| M | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 6.0 | 0.0 | 7.1 | 5.3 | 6.2 | 7.5 | 0.0 | 6.5 | 3.0 |

| N | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 7.1 | 0.0 | 8.6 | 5.3 | 7.7 | 9.0 | 0.0 | 6.5 | 6.1 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kata, R.; Cyrek, M.; Wosiek, M. The Significance of the Financial Situation of Local Government Units for Their Energy Transition Activities: The Case of the Podkarpackie Region. Energies 2024, 17, 2761. https://doi.org/10.3390/en17112761

Kata R, Cyrek M, Wosiek M. The Significance of the Financial Situation of Local Government Units for Their Energy Transition Activities: The Case of the Podkarpackie Region. Energies. 2024; 17(11):2761. https://doi.org/10.3390/en17112761

Chicago/Turabian StyleKata, Ryszard, Magdalena Cyrek, and Małgorzata Wosiek. 2024. "The Significance of the Financial Situation of Local Government Units for Their Energy Transition Activities: The Case of the Podkarpackie Region" Energies 17, no. 11: 2761. https://doi.org/10.3390/en17112761

APA StyleKata, R., Cyrek, M., & Wosiek, M. (2024). The Significance of the Financial Situation of Local Government Units for Their Energy Transition Activities: The Case of the Podkarpackie Region. Energies, 17(11), 2761. https://doi.org/10.3390/en17112761