Methodology for an Audit of Institutional Projects in the Energy Sector

and

and

Abstract

1. Introduction

- National projects that ensure the achievement of priority areas for accelerated development.

- Federal projects as part of national projects that ensure the achievement of goals, objectives and target indicators of national projects.

- Federal projects outside of national projects, ensurng the achievement of other indicators on behalf of the President, the Government of the Russian Federation.

- Regional projects that ensure the achievement of goals, objectives and target indicators of national projects in the areas of jurisdiction of the constituent entities of the Russian Federation.

- Institutional projects that ensure the achievement of goals, objectives and target indicators of departments.

2. Materials and Methods

- -

- The purpose of the system;

- -

- Responsible participants;

- -

- Responsibilities of each participant;

- -

- The rules, regulations and procedures that will matter;

- -

- Relevant information flows.

- -

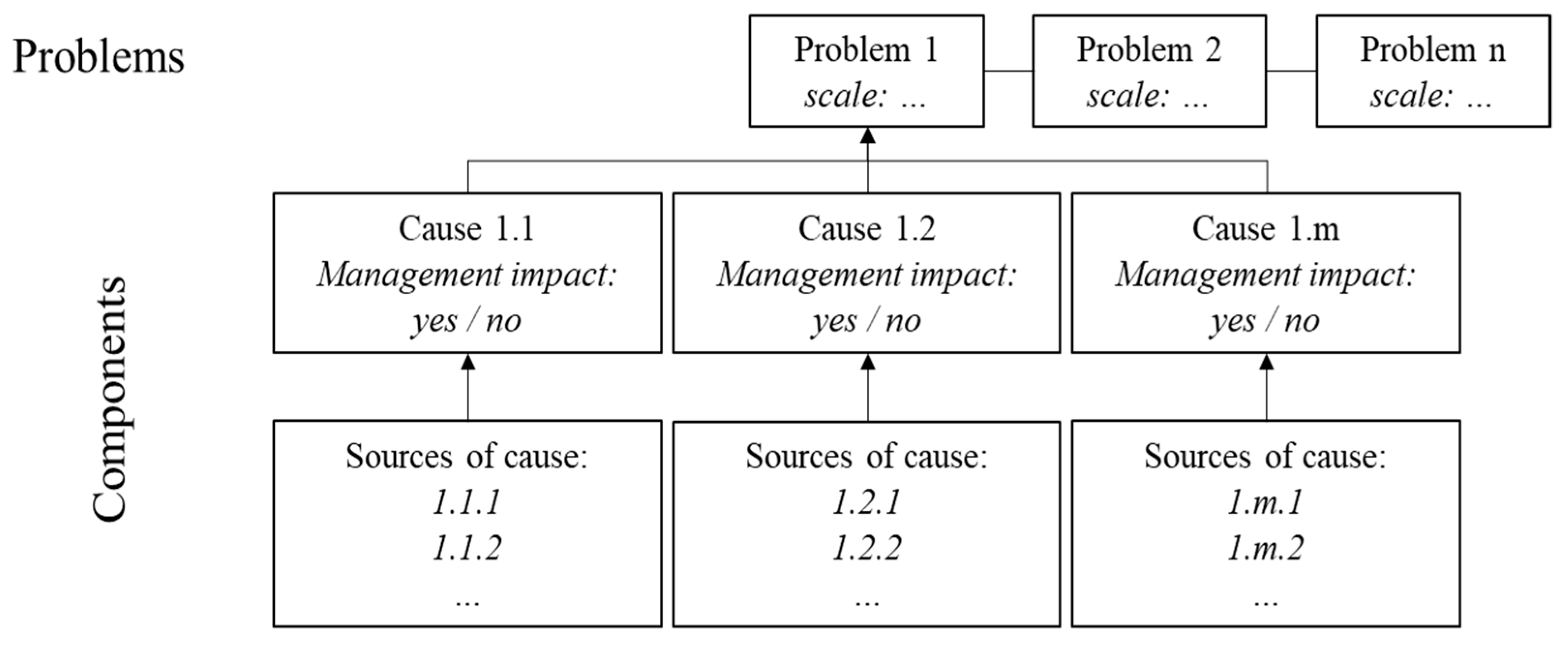

- Identification and analysis of the tasks to be solved by the project;

- -

- Identification of executors and beneficiaries of the project;

- -

- Analysis of the transformational mechanism of the project;

- -

- Assessment of the sufficiency of resource support for the implementation of the project and the validity of the distribution of resources for project activities;

- -

- Analysis of the quality of planning project targets;

- -

- Checking of the compliance of the project passport with the established requirements for the project development procedure;

- -

- Checking of the implementation of project milestones;

- -

- Checking of the implementation of project activities;

- -

- Assessment of the achievement of project targets;

- -

- Analysis of the quality of project implementation;

- -

- Evaluation of the cost effectiveness of the project implementation [22].

- (1)

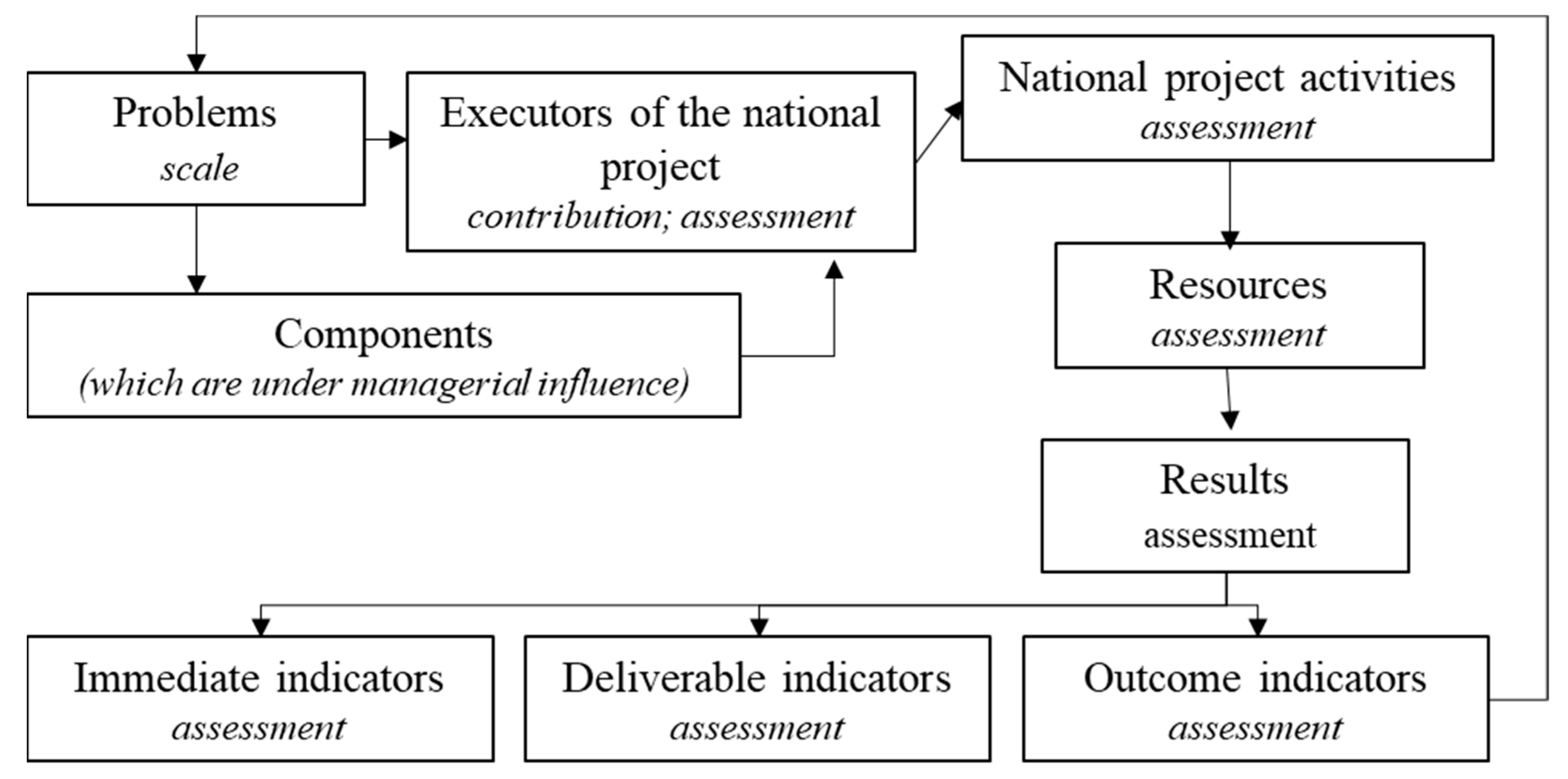

- An audit of the formation of the project (determination of the limit of capital investments and financial performance indicators);

- (2)

- An audit of the project implementation (control of the distribution of resources and work in time).

- (1)

- Analysis of the achievement of the expected results of the project (Table 2);

- (2)

- Evaluation of the effectiveness of the project.

3. Results

- -

- planned contribution of the g-th performer to the solution of the task;

- -

- the potential contribution of the g-th performer to the solution of the tasks set.

- Equal to 1, if it is concluded that the institutional project can meet the needs of all groups of beneficiaries;

- Equal to 0.85, if it is concluded that the institutional project has a limited ability to meet the needs of all groups of beneficiaries;

- Equal to 0.7, if there are doubts about the possibility of an institutional project to sufficiently meet the needs of all groups of beneficiaries.

- ✓

- Coverage of the identified tasks and components by the activities of the institutional project;

- ✓

- Compliance of the expected results of the institutional project with the identified tasks.

- -

- Compliance of target indicators with the goals and objectives of the project (weight 0.25);

- -

- The ability of performers to exert managerial influence on the solution of problems when planning the values of target indicators (weight 0.25);

- -

- Availability of resource limitations of the national project when planning the values of target indicators (weight 0.25);

- -

- Completeness of reflection of the expected results in the context of indicators of immediate results, indicators of final results and indicators of the final effect (weight 0.25).

- -

- Equal to 1, in the absence of significant comments on the content and (or) timely updating of the project passport;

- -

- Equal to 0.5, if there are significant comments on the content and (or) timely updating of the project passport.

- ✓

- Equal to 1, in the absence of significant comments on the content and (or) timely updating of the project passport;

- ✓

- Equal to 0.5, if there are significant comments on the content and (or) timely updating of the project passport.

- -

- Fulfillment of institutional project milestones;

- -

- Achievement of target indicators of the institutional project;

- -

- Cash execution for the costs of the implementation of the institutional project [26].

- -

- “High level” of performance is assigned when the value of the score is more than 0.9;

- -

- “Average level” of performance is assigned when the score value is more than 0.7;

- -

- “Low level” of performance is assigned when the score is 0.7 or less.

- -

- “High level” of performance is assigned when the value of the score is more than 0.9;

- -

- “Average level” of performance is assigned when the score value is more than 0.7;

- -

- “Low level” of performance is assigned when the score is 0.7 or less.

4. Discussion

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Ermolaev, K.A.; Kuzmin, M.S. Problems of modernization and transition to innovative economy. Probl. Mod. Econ. 2017, 4, 85–97. [Google Scholar]

- Sakharov, G.V.; Kvasov, I.A. Evaluation of investment projects in the field of energy. Sci. Work. Free. Econ. Soc. Russ. 2021, 156, 283–298. [Google Scholar]

- Borodin, A.; Mityushina, I.; Harputlu, M.; Kiseleva, N.; Kulikov, A. Factor Analysis of the Efficiency of Russian Oil and Gas Companies. Int. J. Energy Econ. Policy 2023, 13, 172–188. [Google Scholar] [CrossRef]

- Zehir, C.; Zehir, M.; Borodin, A.; Mamedov, Z.F.; Qurbanov, S. Tailored Blockchain Applications for the Natural Gas Industry: The Case Study of SOCAR. Energies 2022, 15, 6010. [Google Scholar] [CrossRef]

- Borodin, A.; Panaedova, G.; Frumina, S.; Kairbekuly, A.; Shchegolevatykh, N. Modeling the Business Environment of an Energy Holding in the Formation of a Financial Strategy. Energies 2021, 14, 8107. [Google Scholar] [CrossRef]

- Mamedov, Z.F.; Qurbanov, S.H.; Streltsova, E.; Borodin, A.; Yakovenko, I.; Aliev, A. Assessment of the potential for sustainable development of electric power enterprises: Approaches, models, technologies. Econ. Oil Gas Ind. 2022, 2, 15–27. [Google Scholar] [CrossRef]

- Degtyareva, V.V.; Kamchatova, E.Y. Development of medium and small business in the sphere of energy: Features of development of highly intelligent projects. Econ. Soc. Mod. Model. Dev. 2018, 8, 57–64. [Google Scholar]

- Guidance GUID 3910 [Electronic Resource]. Available online: https://www.issai.org/wp-content/uploads/2019/08/GUID-3910-Central-Concepts-for-Performance-Auditing.pdf (accessed on 26 February 2023).

- Kerzner, H. Project Management Metrics, KPIs, and Dashboards: A Guide to Measuring and Monitoring Project Performance; John Wiley & Sons: Hoboken, NJ, USA, 2017; Available online: https://www.amazon.com/Project-Management-Metrics-KPIs-Dashboards/dp/1119427282 (accessed on 4 November 2022).

- Samset, K.; Christensen, T. Ex ante project evaluation and the complexity of early decision -making. Public Organ. Rev. 2017, 17, 1–17. [Google Scholar] [CrossRef]

- Matos, S.; Lopes, E. Prince2 or PMBOK—A Question of Choice. Procedia Technol. 2013, 9, 787–794. [Google Scholar] [CrossRef]

- Kahalnikov, M.V. Risks of energy digitalization projects under reducing carbon foorprint. Econ. Entrep. 2021, 1, 230–233. [Google Scholar]

- Dorokhina, E.Y. Benefits and risks of green energy projects. Probl. Sci. Thought 2022, 1, 11–15. [Google Scholar]

- Konnov, I.A. Development of a model of risk management of innovative projects in nuclear energy. Colloq. J. 2020, 11, 20–22. [Google Scholar]

- Kulapin, K.I. Strategic development of the Russian fuel and energy complex in the light of the adoption of the Paris climate agreement. Energy Policy 2019, 3, 18–25. [Google Scholar]

- Famuwagun, O.S. Knowledge in Contemporary Global Projects. 2020, p. 11. Available online: https://www.researchgate.net/publication/345742503_Project_Management_Methodologies_and_Bodies_of_Knowledge_in_Contemporary_Global_Projects (accessed on 15 January 2023).

- Gasik, S. National public projects implementation systems: How to improve public projects delivery from the country level. Procedia—Soc. Behav. Sci. 2016, 226, 351–357. [Google Scholar] [CrossRef]

- Belcher, B.M.; Claus, R.; Davel, R.; Ramirez, L.F. Linking transdisciplinary research characteristics and quality to effectiveness: A comparative analysis of five research-for-development projects. Environ. Sci. Policy 2019, 101, 192–203. [Google Scholar] [CrossRef]

- Abanda, F.H.; Chia, E.L.; Enongene, K.E.; Manjia, M.B.; Fobissie, K.; Pettang, U.J.M.N.; Pettang, C. A systematic review of the application of multi-criteria decision-making in evaluating Nationally Determined Contribution projects. Decis. Anal. J. 2020, 5, 100–140. [Google Scholar] [CrossRef]

- Soloviev, A.I. About the method of system modeling of the stable economic agents (using the example of the rocket and space industry). In The Collection: Economic Security of Russia: Problems and Prospects. Materials of the III International Scientific-Practical Conference; Nizhny Novgorod State Technical University: Nizhny Novgorod, Russia, 2015; pp. 409–415. [Google Scholar]

- Dorzhieva, V.V. Digital transformation of the Russian fuel and energy complex: Priorities and development targets. Kreat. Ekon. 2021, 15, 4079–4094. [Google Scholar] [CrossRef]

- State Audit Standard 104; External State Audit (Control) Standard; Performance Audit, Approved. Resolution of the Collegium of the Accounts Chamber of the Russian Federation: Moscow, Russia, 9 February 2021; No. 2PK.

- State Audit Standard 105; External State Audit (Control) Standard; Strategic Audit, Approved. Resolution of the Board of the Accounts Chamber of the Russian Federation: Moscow, Russia, 10 November 2020; No. 17PK.

- Gryzunova, N.; Vedenyev, K.; Manuylenko, V.; Keri, I.; Bilczak, M. Distributed Energy as a Megatrend of Audit of Investment Processes of the Energy Complex. Energies 2022, 15, 9225. [Google Scholar] [CrossRef]

- No. 11K (1536); Methodology for Assessing the Quality of the Formation and Implementation of the RF GP as Part of the Follow-Up Control over the Execution of the Federal Budget. Board of the Accounts Chamber of the Russian Federation: Moscow, Russia, 9 March 2022.

- Głodzińsk, E. Project assessment framework: Multidimensional efficiency approach applicable for project-driven organizations. Procedia Comput. Sci. 2018, 138, 731–738. [Google Scholar] [CrossRef]

- Velasquez, M.; Patrick, T. An Analysis of Multi-Criteria Decision-Making Methods. Int. J. Oper. Res. 2013, 10, 56–66. [Google Scholar]

- Marnada, P.; Raharjo, T.; Hardian, B.; Prasetyo, A. Agile project management challenge in handling scope and change: A systematic literature review. Procedia Comput. Sci. 2021, 197, 290–300. [Google Scholar] [CrossRef]

- Cordoş, G.S.; Fülöp, M.T. Understanding audit reporting changes: Introduction of Key Audit Matters. Account. Manag. Inf. Syst. Contab. Inform. Gestiune 2015, 14, 128–152. [Google Scholar]

- George-Silviu, C.; Melinda-Timea, F. New audit reporting challenges: Auditing the going concern basis of accounting. Procedia Econ. Financ. 2015, 32, 216–224. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| No | Audit Stages | Content of Audit Procedures |

|---|---|---|

| 1 | Identification and analysis of the tasks of the region, which the project is aimed at solving | An indicator of the distribution of resources between the project executors in terms of their potential contribution to the solution of each task |

| 2 | Identification of performers, investors and beneficiaries | The coefficient of involvement of investors and performers in the solution |

| 3 | Analysis of the transformational mechanism of the project | Distribution of weighting coefficients of tasks between the activities of the institutional project with the assumption that they fully cover each identified task. |

| 4 | Creating a project results map | The works are adjusted in accordance with the coefficients of sufficiency of the resource provision for the implementation of the institutional project and the coefficients of coverage of tasks and components by the activities of the institutional project in the context of activities. |

| 5 | Analysis of the quality of planning indicators | The quality factor of planning the targets of the institutional project. |

| 6 | Checking the compliance of the project passport with the established requirements | The quality coefficient of the project passport compilation. |

| 7 | Summary assessment of the quality of project formation | Summary coefficient of the quality of project formation. |

| Indicator | Formula |

|---|---|

| Assessment of project milestones (Q). | , |

| where Qf—actual number of milestones completed within the established time limit at the end of the reporting period; Qp—number of milestones planned for the reporting period. | |

| Achievement of project target indicators | , |

| where —actual value of the i-th indicator at the end of the reporting period; —planned value of the i-th indicator, set for the corresponding reporting period. | |

| Achievement of immediate target indicators (Pimmediate) | |

| where Pi(immediate)—assessment of the achievement of the i-th target indicator of immediate target indicators; n1—number of immediate target indicators. | |

| Achievement of deliverable target indicators (Pdeliverable). | |

| where Pi(deliverable)—assessment of the achievement of the i-th target indicator of deliverable target indicators; n2—number of deliverable target indicators. | |

| Achievement of outcome target indicators (Poutcome). | |

| where Pi(outcome)—assessment of the achievement of the i-th target indicator of outcome target indicators; n3—number of outcome target indicators. | |

| Final assessment of the achievement of target indicators (P). | , |

| where —full data ratio to assess the achievement of target indicators, calculated as the ratio of the number of target indicators for which actual data on implementation is available to the total number of target indicators set in the national project. | |

| Assessment of national project expenditures | , |

| where —actual volume of expenditures from the j-th source to implement the national project at the end of the reporting period; —planned volume of expenditures from the j-th source to implement the national project at the end of the reporting period; | |

| Final assessment of expenditures from all sources to implement the national project (R). | , |

| where vj—volume of the j-th source; n4—amount of sources. |

| Level of Maturity | Criteria | Value |

|---|---|---|

| Level 0: lack of indicators or baseline data | Achievement of goals is not characterized by indicators or indicators do not have target values, or justification is not provided to achieve target values of indicators. | 0.5 |

| Level 1: explicit assumptions | Assumptions used in justification are clearly stated; Acceptable and reliable statistical data are used; Starting points and inertial scenarios are available only for some indicators. | 0.5 |

| Level 2: realistic assumptions and sound methods | Assumptions used in justification are realistic; Methods used for forecasting are reasonable (in particular, expected changes in indicators are calculated directly or follow national and/or international examples). | 0.75 |

| Level 3: manageable contingencies | There is a plan of action in case of risks; The most significant risks are correctly identified, assessed and managed. | 1 |

| (Q)/(P)/(R) | E1 × k1/E2 × k2/E3 × k3 | |

|---|---|---|

| Less than 0.8 | 0.8 and More | |

| Low level | Efficiency is low, there are significant risks of non-fulfillment of expected results of the departmental project, a revision of the content of the national project is required | Efficiency is low, there are significant risks of non-fulfillment of expected results of the departmental project |

| Average level | Efficiency is average, there are risks of non-fulfillment of expected results of the departmental project, a revision of the project content is required | Efficiency is average, there are risks of non-fulfillment of expected results of the departmental project |

| High level | Efficiency is high, risks of non-fulfillment of expected results of the departmental project are minimal, a revision of the project content is required | Efficiency is high, risks of non-fulfillment of expected results of the departmental project are minimal |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Fedchenko, E.; Gusarova, L.; Timkin, T.; Gryzunova, N.; Bilczak, M.; Frumina, S. Methodology for an Audit of Institutional Projects in the Energy Sector. Energies 2023, 16, 3535. https://doi.org/10.3390/en16083535

Fedchenko E, Gusarova L, Timkin T, Gryzunova N, Bilczak M, Frumina S. Methodology for an Audit of Institutional Projects in the Energy Sector. Energies. 2023; 16(8):3535. https://doi.org/10.3390/en16083535

Chicago/Turabian StyleFedchenko, Elena, Lyubov Gusarova, Timur Timkin, Natalie Gryzunova, Michał Bilczak, and Svetlana Frumina. 2023. "Methodology for an Audit of Institutional Projects in the Energy Sector" Energies 16, no. 8: 3535. https://doi.org/10.3390/en16083535

APA StyleFedchenko, E., Gusarova, L., Timkin, T., Gryzunova, N., Bilczak, M., & Frumina, S. (2023). Methodology for an Audit of Institutional Projects in the Energy Sector. Energies, 16(8), 3535. https://doi.org/10.3390/en16083535