Impact of Renewable and Non-Renewable Energy Consumption and CO2 Emissions on Economic Growth in the Visegrad Countries

Abstract

:1. Introduction

2. Literature Review

3. Materials and Methods

3.1. Date

3.2. Methodology and Econometric Framework

- -

- Δ represents the first difference value of the variable;

- -

- represents the long-term rate;

- -

- ε(t) represents the residual component.

4. Empirical Results and Discussion

4.1. Results for Unit Root Test

4.2. Co-Integration Results

4.3. Results of Evaluations of Short- and Long-Term Models

4.4. Causality Results

4.5. Diagnostics Results

5. Discussion

6. Conclusions

7. Limitations and Future Research

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

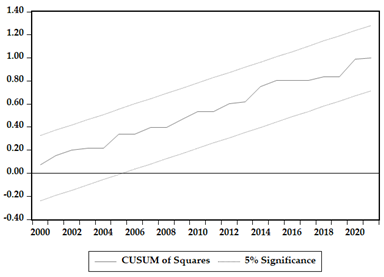

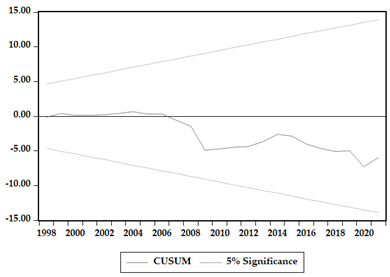

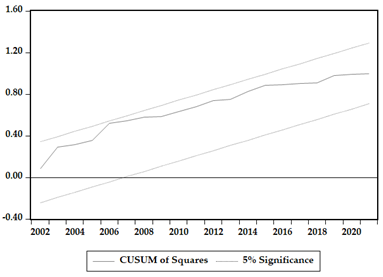

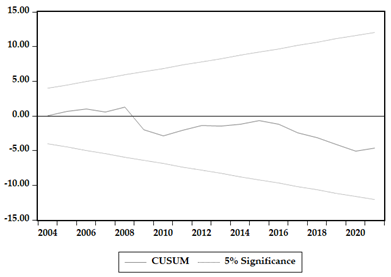

Appendix A. CUSUM and CUSUMSQ Result for the Estimated Models

| Czech Republic | |

|  |

| Poland | |

|  |

| Hungary | |

|  |

| Slovak Republic | |

|  |

References

- Bhuiyan, M.A.; Zhang, Q.; Khare, V.; Mikhaylov, A.; Pinter, G.; Huang, X. Renewable Energy Consumption and Economic Growth Nexus—A Systematic Literature Review. Front. Environ. Sci. 2022, 10, 878394. [Google Scholar] [CrossRef]

- Menegaki, A.N.; Tsani, S. Chapter 5—Critical Issues to Be Answered in the Energy-Growth Nexus (EGN) Research Field. In The Economics and Econometrics of the Energy-Growth Nexus; Menegaki, A.N., Ed.; Academic Press: Cambridge, MA, USA, 2018; pp. 141–184. ISBN 978-0-12-812746-9. [Google Scholar]

- Bhat, J.A. Renewable and non-renewable energy consumption—Impact on economic growth and CO2 emissions in five emerging market economies. Environ. Sci. Pollut. Res. 2018, 25, 35515–35530. [Google Scholar] [CrossRef]

- Ito, K. CO2 emissions, renewable and non-renewable energy consumption, and economic growth: Evidence from panel data for developing countries. Int. Econ. 2017, 151, 1–6. [Google Scholar] [CrossRef]

- Marques, L.; Fuinhas, J.; Marques, A. On the Dynamics of Energy-Growth Nexus: Evidence from a World Divided into Four Regions. Int. J. Energy Econ. Policy 2017, 7, 208–215. [Google Scholar]

- Huang, B.-N.; Hwang, M.; Yang, C. Causal relationship between energy consumption and GDP growth revisited: A dynamic panel data approach. Ecol. Econ. 2008, 67, 41–54. [Google Scholar] [CrossRef]

- Alper, A.; Oguz, O. The role of renewable energy consumption in economic growth: Evidence from asymmetric causality. Renew. Sustain. Energy Rev. 2016, 60, 953–959. [Google Scholar] [CrossRef]

- Esso, J.L. The Energy Consumption-Growth Nexus in Seven Sub-Saharan African Countries. Econ. Bull. 2010, 30, 1191–1209. [Google Scholar]

- Fang, Y. Economic welfare impacts from renewable energy consumption: The China experience. Renew. Sustain. Energy Rev. 2011, 15, 5120–5128. [Google Scholar] [CrossRef]

- Inglesi-Lotz, R. The impact of renewable energy consumption to economic growth: A panel data application. Energy Econ. 2016, 53, 58–63. [Google Scholar] [CrossRef]

- Sebri, M. Use renewables to be cleaner: Meta-analysis of the renewable energy consumption–economic growth nexus. Renew. Sustain. Energy Rev. 2015, 42, 657–665. [Google Scholar] [CrossRef]

- Bhattacharya, M.; Paramati, S.R.; Ozturk, I.; Bhattacharya, S. The effect of renewable energy consumption on economic growth: Evidence from top 38 countries. Appl. Energy 2016, 162, 733–741. [Google Scholar] [CrossRef]

- Rajaguru, G.; Khan, S.U. Causality between Energy Consumption and Economic Growth in the Presence of Growth Volatility: Multi-Country Evidence. J. Risk Financ. Manag. 2021, 14, 471. [Google Scholar] [CrossRef]

- Myszczyszyn, J.; Suproń, B. Relationship among Economic Growth (GDP), Energy Consumption and Carbon Dioxide Emission: Evidence from V4 Countries. Energies 2021, 14, 7734. [Google Scholar] [CrossRef]

- Topcu, E.; Altinoz, B.; Aslan, A. Global evidence from the link between economic growth, natural resources, energy consumption, and gross capital formation. Resour. Policy 2020, 66, 101622. [Google Scholar] [CrossRef]

- Streimikiene, D.; Kasperowicz, R. Review of economic growth and energy consumption: A panel cointegration analysis for EU countries. Renew. Sustain. Energy Rev. 2016, 59, 1545–1549. [Google Scholar] [CrossRef]

- Menegaki, A.N.; Marques, A.C.; Fuinhas, J.A. Redefining the energy-growth nexus with an index for sustainable economic welfare in Europe. Energy 2017, 141, 1254–1268. [Google Scholar] [CrossRef]

- Armeanu, D.Ş.; Vintilă, G.; Gherghina, Ş.C. Does Renewable Energy Drive Sustainable Economic Growth? Multivariate Panel Data Evidence for EU-28 Countries. Energies 2017, 10, 381. [Google Scholar] [CrossRef]

- Marinaș, M.-C.; Dinu, M.; Socol, A.-G.; Socol, C. Renewable energy consumption and economic growth. Causality Relationship in Central and Eastern European Countries. PLoS ONE 2018, 13, e0202951. [Google Scholar] [CrossRef]

- Papież, M.; Śmiech, S.; Frodyma, K. Effects of renewable energy sector development on electricity consumption—Growth nexus in the European Union. Renew. Sustain. Energy Rev. 2019, 113, 109276. [Google Scholar] [CrossRef]

- Ozcan, B.; Ozturk, I. Renewable energy consumption-economic growth nexus in emerging countries: A bootstrap panel causality test. Renew. Sustain. Energy Rev. 2019, 104, 30–37. [Google Scholar] [CrossRef]

- Costa-Campi, M.; García-Quevedo, J.; Trujillo-Baute, E. Electricity regulation and economic growth. Energy Policy 2018, 113, 232–238. [Google Scholar] [CrossRef]

- Gozgor, G.; Lau, C.K.M.; Lu, Z. Energy consumption and economic growth: New evidence from the OECD countries. Energy 2018, 153, 27–34. [Google Scholar] [CrossRef]

- Lazăr, D.; Minea, A.; Purcel, A.-A. Pollution and economic growth: Evidence from Central and Eastern European countries. Energy Econ. 2019, 81, 1121–1131. [Google Scholar] [CrossRef]

- Muço, K.; Valentini, E.; Lucarelli, S. The relationships between gdp growth, energy consumption, renewable energy production and CO2 emissions in european transition economies. Int. J. Energy Econ. Policy 2021, 11, 362–373. [Google Scholar] [CrossRef]

- Myszczyszyn, J.; Suproń, B. Relationship among Economic Growth, Energy Consumption, CO2 Emission, and Urbanization: An Econometric Perspective Analysis. Energies 2022, 15, 9647. [Google Scholar] [CrossRef]

- Litavcová, E.; Chovancová, J. Economic Development, CO2 Emissions and Energy Use Nexus-Evidence from the Danube Region Countries. Energies 2021, 14, 3165. [Google Scholar] [CrossRef]

- Cialani, C. CO2 emissions, GDP and trade: A panel cointegration approach. Int. J. Sustain. Dev. World Ecol. 2016, 24, 193–204. [Google Scholar] [CrossRef]

- Li, R.; Jiang, H.; Sotnyk, I.; Kubatko, O.; Almashaqbeh, I.Y.A. The CO2 Emissions Drivers of Post-Communist Economies in Eastern Europe and Central Asia. Atmosphere 2020, 11, 1019. [Google Scholar] [CrossRef]

- Gardiner, R.; Hajek, P. Interactions among energy consumption, CO2, and economic development in European Union countries. Sustain. Dev. 2019, 28, 723–740. [Google Scholar] [CrossRef]

- Im, K.S.; Pesaran, M.; Shin, Y. Testing for unit roots in heterogeneous panels. J. Econ. 2003, 115, 53–74. [Google Scholar] [CrossRef]

- Unit Root Tests in Panel Data: Asymptotic and Finite-Sample Properties—ScienceDirect. Available online: https://www.sciencedirect.com/science/article/pii/S0304407601000987 (accessed on 20 August 2023).

- Pesaran, M.H. A simple panel unit root test in the presence of cross-section dependence. J. Appl. Econ. 2007, 22, 265–312. [Google Scholar] [CrossRef]

- Dickey, D.A.; Fuller, W.A. Distribution of the Estimators for Autoregressive Time Series with a Unit Root. J. Am. Stat. Assoc. 1979, 74, 427–431. [Google Scholar] [CrossRef]

- Phillips, P.C.B.; Perron, P. Testing for a unit root in time series regression. Biometrika 1988, 75, 335–346. [Google Scholar] [CrossRef]

- McCoskey, S.; Kao, C. A residual-based test of the null of cointegration in panel data. Econ. Rev. 1998, 17, 57–84. [Google Scholar] [CrossRef]

- Pedroni, P. Purchasing Power Parity Tests in Cointegrated Panels. Rev. Econ. Stat. 2001, 83, 727–731. [Google Scholar] [CrossRef]

- Pesaran, M.H.; Shin, Y.; Smith, R.J. Bounds testing approaches to the analysis of level relationships. J. Appl. Econom. 2001, 16, 289–326. [Google Scholar] [CrossRef]

- Pedroni, P. Fully Modified OLS for Heterogeneous Cointegrated Panels. In Nonstationary Panels, Panel Co-Integration, and Dynamic Panels; Baltagi, B.H., Fomby, T.B., Carter Hill, R., Eds.; Advances in Econometrics; Emerald Group Publishing Limited: Bingley, UK, 2001; Volume 15, pp. 93–130. ISBN 978-1-84950-065-4. [Google Scholar]

- Dreger, C.; Reimers, H.-E. Health Care Expenditures in OECD Countries: A Panel Unit Root and Co-integration Analysis. Int. J. Appl. Econom. Quant. Stud. 2005, 2, 5–20. [Google Scholar] [CrossRef]

- Kao, C.; Chiang, M.-H. On the Estimation and Inference of a Cointegrated Regression in Panel Data. In Nonstationary Panels, Panel Co-Integration, and Dynamic Panels; Baltagi, B.H., Fomby, T.B., Carter Hill, R., Eds.; Advances in Econometrics; Emerald Group Publishing Limited: Bingley, UK, 2001; Volume 15, pp. 179–222. ISBN 978-1-84950-065-4. [Google Scholar]

- Pesaran, M.H.; Shin, Y. An Autoregressive Distributed-Lag Modelling Approach to Co-integration Analysis. In Econometrics and Economic Theory in the 20th Century: The Ragnar Frisch Centennial Symposium; Strøm, S., Ed.; Econometric Society Monographs; Cambridge University Press: Cambridge, UK, 1999; pp. 371–413. ISBN 978-0-521-63323-9. [Google Scholar]

- Engle, R.F.; Granger, C.W.J. Co-Integration and Error Correction: Representation, Estimation, and Testing. Econometrica 1987, 55, 251–276. [Google Scholar] [CrossRef]

- Toda, H.Y.; Yamamoto, T. Statistical inference in vector autoregressions with possibly integrated processes. J. Econom. 1995, 66, 225–250. [Google Scholar] [CrossRef]

- Breusch, T.S. Testing for autocorrelation in dynamic linear models. Aust. Econ. Pap. 1978, 17, 334–355. [Google Scholar] [CrossRef]

- Engle, R.F. Autoregressive Conditional Heteroscedasticity with Estimates of the Variance of United Kingdom Inflation. Econometrica 1982, 50, 987–1007. [Google Scholar] [CrossRef]

- Breusch, T.S.; Pagan, A.R. A Simple Test for Heteroscedasticity and Random Coefficient Variation. Econometrica 1979, 47, 1287. [Google Scholar] [CrossRef]

- Brown, R.L.; Durbin, J.; Evans, J.M. Techniques for Testing the Constancy of Regression Relationships over Time. J. R. Stat. Soc. Ser. B 1975, 37, 149–163. [Google Scholar] [CrossRef]

- Uçak, H.; Aslan, A.; Yucel, F.; Turgut, A. A Dynamic Analysis of CO2 Emissions and the GDP Relationship: Empirical Evidence from High-income OECD Countries. Energy Sources Part B Econ. Plan. Policy 2014, 10, 38–50. [Google Scholar] [CrossRef]

- Mitić, P.; Ivanović, O.M.; Zdravković, A. A Cointegration Analysis of Real GDP and CO2 Emissions in Transitional Countries. Sustainability 2017, 9, 568. [Google Scholar] [CrossRef]

- Khan, M.W.A.; Panigrahi, S.K.; Almuniri, K.S.N.; Soomro, M.I.; Mirjat, N.H.; Alqaydi, E.S. Investigating the Dynamic Impact of CO2 Emissions and Economic Growth on Renewable Energy Production: Evidence from FMOLS and DOLS Tests. Processes 2019, 7, 496. [Google Scholar] [CrossRef]

- Salazar-Núñez, H.F.; Venegas-Martínez, F.; Tinoco-Zermeño, M.Á. Impact of Energy Consumption and Carbon Dioxide Emissions on Economic Growth: Cointegrated Panel Data in 79 Countries Grouped by Income Level. Int. J. Energy Econ. Policy 2020, 10, 218–226. [Google Scholar] [CrossRef]

- Daysi, G.; Karla, M.-M.; Paco, A.-S.; Santiago, O.-M. CO2 Emissions, High-Tech Exports and GDP per Capita. In Proceedings of the 2021 16th Iberian Conference on Information Systems and Technologies (CISTI), Chaves, Portugal, 23–27 June 2021; pp. 1–5. [Google Scholar]

- Huang, Z. Analyze the Relationship Between CO2 Emissions and GDP from the Global Perspective. In Proceedings of the 2021 International Conference on Financial Management and Economic Transition (FMET 2021), Virtual, 27–29 August 2023; pp. 442–451. [Google Scholar]

- Chavaillaz, Y.; Roy, P.; Partanen, A.-I.; Da Silva, L.; Bresson, É.; Mengis, N.; Chaumont, D.; Matthews, H.D. Exposure to excessive heat and impacts on labour productivity linked to cumulative CO2 emissions. Sci. Rep. 2019, 9, 1–11. [Google Scholar] [CrossRef]

- Caporale, G.M.; Claudio-Quiroga, G.; Gil-Alana, L.A. CO2 Emissions and GDP: Evidence from China. SSRN J. 2019. [Google Scholar] [CrossRef]

- Kochtcheeva, L.V. Environmental Disaster in the Post-Communist Countries: Is There a Solution? Environ. Pract. 2002, 4, 10–13. [Google Scholar] [CrossRef]

- Hannesson, R. CO2 intensity and GDP per capita. Int. J. Energy Sect. Manag. 2019, 14, 372–388. [Google Scholar] [CrossRef]

- Ali, Q.; Raza, A.; Narjis, S.; Saeed, S.; Khan, M.T.I. Potential of renewable energy, agriculture, and financial sector for the economic growth: Evidence from politically free, partly free and not free countries. Renew. Energy 2020, 162, 934–947. [Google Scholar] [CrossRef]

- Shabbir, S.; Zeshan, M.; Muhammad, S. Renewable and Non-Renewable Energy Consumption, Real GDP and CO2 Emissions Nexus: A Structural VAR Approach in Pakistan; University Library of Munich: Munich, Germany, 2011. [Google Scholar]

- Belaïd, F.; Zrelli, M.H. Renewable and Non-Renewable Electricity Consumption, Carbon Emissions and GDP: Evidence from Mediterranean Countries. Energy Policy 2019, 133, 110929. [Google Scholar] [CrossRef]

- Al-Mulali, U.; Fereidouni, H.G.; Lee, J.Y. Electricity consumption from renewable and non-renewable sources and economic growth: Evidence from Latin American countries. Renew. Sustain. Energy Rev. 2014, 30, 290–298. [Google Scholar] [CrossRef]

- Sahlian, D.N.; Popa, A.F.; Creţu, R.F. Does the Increase in Renewable Energy Influence GDP Growth? An EU-28 Analysis. Energies 2021, 14, 4762. [Google Scholar] [CrossRef]

- Ohler, A.; Fetters, I. The causal relationship between renewable electricity generation and GDP growth: A study of energy sources. Energy Econ. 2014, 43, 125–139. [Google Scholar] [CrossRef]

- Afonso, T.L.; Marques, A.C.; Fuinhas, J.A.; Saldanha, E.M.M. Interactions between electricity generation sources and economic activity in two Nord Pool systems. Evidence from Estonia and Sweden. Appl. Econ. 2017, 50, 3115–3127. [Google Scholar] [CrossRef]

- Halkos, G.E.; Tzeremes, N.G. The effect of electricity consumption from renewable sources on countries’ economic growth levels: Evidence from advanced, emerging and developing economies. Renew. Sustain. Energy Rev. 2014, 39, 166–173. [Google Scholar] [CrossRef]

- Liu, Y.; Wei, T.; Park, D. Macroeconomic impacts of energy productivity: A general equilibrium perspective. Energy Effic. 2019, 12, 1857–1872. [Google Scholar] [CrossRef]

| Source | Country | Causality | Model | Time |

|---|---|---|---|---|

| Huang et al. [6] | 26 OECD countries | EC → GDP | VECM and PVAR | 1971–2016 |

| Rajaguru and Khan [13] | 48 countries | EC → GDP | ARDL | - |

| Myszczyszyn and Suproń [14] | Visegrad countries | EC ↔ GDP | ARDL | 1992–2015 |

| Topcu et al. [15] | 124 countries | EC → GDP | PVAR | 1980–2018 |

| Streimikiene and Kasperovich [16] | EU countries | EC → GDP | FMOLS, DOLS | 1995–2015 |

| Menegaki et al. [17] | EU countries | EC ↔ GDP | PARDL | 2000–2012 |

| Armeanu et al. [18] | EU countries | REW → GDP | PVAR | 2003–2014 |

| Marinaș et al. [19] | CEE countries | REW ↔ GDP | ARDL | 1990–2014 |

| Papież et al. [20] | EU countries | REW ↔ GDP | PVECM | 1990–2014 |

| Ozcan and Ozturk [21] | Emerging countries | REW ≠ GDP | Causality panel | 1990–2016 |

| Costa-Campi et al. [22] | EU countries | EC → GDP | OLS panel | 2007–2013 |

| Gozgor et al. [23] | OECD | NREW → GDP REW → GDP | ARDL | 1990–2013 |

| Papież et al. [20] | EU countries | REW ≠ GDP NREW ≠ GDP | PVAR | 1995–2015 |

| Lazăr et al. [24] | CEE countries | CO2 → GDP | FMOLS | 1996–2015 |

| Muço et al. [25] | European transition economies | CO2 ↔ GDP REW → GDP | PVAR | 1990–2018 |

| Myszczyszyn and Suproń [26] | Visegrad countries | CO2 ↔ GDP EC → GDP | ARDL | 1992–2016 |

| Litavcová and Chovancová [27] | Danube Region countries | Mixed | ARDL | 1990–2019 |

| Cialani [28] | 150 countries | CO2 ↔ GDP | ECM panel | 1960–2008 |

| Li et al. [29] | Post-communist economies | CO2 → GDP | OLS panel | 1996–2018 |

| Gardiner and Hajek [30] | EU countries | CO2 → GDP EC → GDP | PVECM | 1990–2015 |

| Variable | Country | Mean | Median | Max | Min | Std. Dev. | n |

|---|---|---|---|---|---|---|---|

| lnGDP | Czech Republic | 9.589 | 9.679 | 9.916 | 9.234 | 0.223 | 31 |

| Hungary | 9.259 | 9.330 | 9.648 | 8.899 | 0.233 | 31 | |

| Poland | 9.095 | 9.114 | 9.669 | 8.465 | 0.366 | 31 | |

| Slovak Republic | 9.361 | 9.425 | 9.812 | 8.779 | 0.344 | 31 | |

| lnCO2 | Czech Republic | 2.401 | 2.432 | 2.614 | 2.232 | 0.106 | 31 |

| Hungary | 1.615 | 1.678 | 1.868 | 1.364 | 0.138 | 31 | |

| Poland | 2.063 | 2.043 | 2.248 | 1.955 | 0.085 | 31 | |

| Slovak Republic | 1.795 | 1.828 | 2.094 | 1.455 | 0.124 | 31 | |

| lnREW | Czech Republic | −3.276 | −3.434 | −2.346 | −4.509 | 0.681 | 31 |

| Hungary | −4.758 | −4.140 | −2.795 | −6.383 | 1.319 | 31 | |

| Poland | −3.982 | −4.405 | −2.642 | −4.845 | 0.796 | 31 | |

| Slovak Republic | −2.517 | −2.498 | −2.185 | −3.485 | 0.290 | 31 | |

| lnNREW | Czech Republic | −0.456 | −0.382 | −0.302 | −0.717 | 0.142 | 31 |

| Hungary | −1.225 | −1.217 | −1.071 | −1.393 | 0.078 | 31 | |

| Poland | −1.068 | −1.049 | −0.897 | −1.211 | 0.085 | 31 | |

| Slovak Republic | −0.806 | −0.803 | −0.658 | −0.958 | 0.081 | 31 |

| Variable | Level | First Differences | |||||

|---|---|---|---|---|---|---|---|

| CIPS | Levin, Lin, and Chu | IPS | CIPS | Levin, Lin, and Chu | IPS | CIPS | |

| lnCO2 | −2.16 | −1.93 ** | −2.16 | −5.63 * | −4.97 * | −4.48 * | −2.16 |

| lnGDP | −1.55 | −1.93 ** | 0.97 | −3.60 * | −4.97 * | −4.48 * | −1.55 |

| lnNREW | −2.07 | −1.58 * | −0.78 | −4.94 * | −4.51 * | −5.25 * | −2.07 |

| lnREW | −1.24 | 0.27 | 0.67 | −3.34 * | −5.28 * | −5.38 * | −1.24 |

| Country | Variable | Level | First Differences | ||||||

|---|---|---|---|---|---|---|---|---|---|

| ADF | PP | ADF | PP | ||||||

| t-Stat | p-Value | t-Stat | p-Value | t-Stat | p-Value | t-Stat | p-Value | ||

| Czech Republic | lnGDP | −0.81 | 0.801 | −0.36 | 0.904 | −4.11 | 0.004 | −4.46 | 0.001 |

| lnNREW | −1.56 | 0.491 | −1.54 | 0.501 | −4.90 | 0.001 | −4.94 | 0.000 | |

| lnREW | −1.25 | 0.639 | 0.19 | 0.967 | −5.98 | 0.000 | −4.33 | 0.002 | |

| lnCO2 | −1.82 | 0.363 | −2.04 | 0.271 | −4.98 | 0.000 | −4.92 | 0.000 | |

| Hungary | lnGDP | 0.26 | 0.972 | −0.36 | 0.904 | −4.60 | 0.001 | −4.46 | 0.001 |

| lnNREW | −1.49 | 0.526 | 0.72 | 0.991 | −5.05 | 0.000 | −4.01 | 0.004 | |

| lnREW | −1.48 | 0.531 | 3.30 | 1.000 | −6.13 | 0.000 | −2.97 | 0.050 | |

| lnCO2 | 0.89 | 0.994 | −1.79 | 0.379 | −3.78 | 0.033 | −5.6 | 0.000 | |

| Poland | lnGDP | −2.64 | 0.099 | 5.08 | 1.000 | −4.69 | 0.001 | −5.16 | 0.000 |

| lnNREW | −0.61 | 0.854 | 0.72 | 0.991 | −4.92 | 0.001 | −4.01 | 0.004 | |

| lnREW | 0.93 | 0.995 | 2.43 | 1.000 | −4.25 | 0.003 | −4.31 | 0.002 | |

| lnCO2 | −2.02 | 0.278 | −2.00 | 0.287 | −5.24 | 0.000 | −5.13 | 0.000 | |

| Slovak Republic | lnGDP | −1.54 | 0.502 | −0.23 | 0.923 | −4.17 | 0.003 | −4.95 | 0.000 |

| lnNREW | −2.44 | 0.140 | 0.72 | 0.991 | −6.14 | 0.000 | −4.01 | 0.004 | |

| lnREW | −1.86 | 0.346 | 2.43 | 1.000 | −5.17 | 0.000 | −4.31 | 0.002 | |

| lnCO2 | −3.99 | 0.005 | −2.85 | 0.064 | −5.33 | 0.000 | −7.04 | 0.000 | |

| Test | Statistic | Weighted Statistic |

|---|---|---|

| Within-Dimension | ||

| v-Statistic panel | 1.25 *** | 1.34 *** |

| rho-Statistic panel | −0.67 | −0.30 |

| PP-Statistic panel | −1.84 ** | −1.46 *** |

| ADF-Statistic Panel | −2.22 ** | −2.47 * |

| Between-Dimension | ||

| Group rho-Statistic | 0.62 | |

| Group PP-Statistic | −2.20 ** | |

| Group ADF-Statistic | −2.99 * | |

| Kao-Cointegration test | ||

| ADF | −2.37 * | |

| Country | F-Statistics Value | F-Statistics | I(0) | I(1) |

|---|---|---|---|---|

| Czech Republic | 7.294 * | 10% | 2.676 | 3.586 |

| 5% | 3.272 | 4.306 | ||

| 1% | 4.614 | 5.966 | ||

| Hungary | 5.497 ** | 10% | 3.097 | 4.118 |

| 5% | 3.715 | 4.878 | ||

| 1% | 5.205 | 6.640 | ||

| Poland | 11.492 * | 10% | 3.770 | 4.535 |

| 5% | 4.535 | 5.415 | ||

| 1% | 6.428 | 7.505 | ||

| Slovak Republic | 8.227 * | 10% | 3.097 | 4.118 |

| 5% | 3.715 | 4.878 | ||

| 1% | 5.205 | 6.640 |

| Variables | Co-Efficient | Std. Error | t-Statistics | Prob. |

|---|---|---|---|---|

| DOLS | ||||

| lnCO2 | −1.275 | 0.431 | −2.959 | 0.004 |

| lnNREW | 0.857 | 0.350 | 2.447 | 0.017 |

| lnREW | 0.088 | 0.053 | 1.670 | 0.099 |

| R-squared | 0.870014 | |||

| FMOLS | ||||

| lnCO2 | −1.102 | 0.340 | −3.244 | 0.002 |

| lnNREW | 0.920 | 0.304 | 3.026 | 0.003 |

| lnREW | 0.112 | 0.047 | 2.388 | 0.019 |

| R-squared | 0.769619 | |||

| Country | Variables | Co-Efficient | Std. Error | t-Statistics | Prob. |

|---|---|---|---|---|---|

| Czech Republic | |||||

| CO2 | −1.088 | 0.806 | −1.350 | 0.188 | |

| NREW | 3.067 | 0.876 | 3.500 | 0.002 | |

| REW | 0.408 | 0.551 | 0.740 | 0.466 | |

| Poland | Const. | 2.098 | 0.767 | 2.734 | 0.011 |

| CO2 | −1.857 | 0.412 | −4.511 | 0.000 | |

| NREW | 1.683 | 0.649 | 2.593 | 0.015 | |

| REW | −0.129 | 0.094 | −1.374 | 0.181 | |

| Const. | 3.109 | 1.076 | 2.888 | 0.008 | |

| Hungary | CO2 | −2.951 | 0.542 | −5.447 | 0.000 |

| NREW | 0.523 | 0.515 | 1.015 | 0.319 | |

| REW | 0.205 | 0.058 | 3.563 | 0.001 | |

| Const. | −3.147 | 0.818 | −3.849 | 0.001 | |

| Slovak Republic | CO2 | −1.166 | 0.523 | −2.229 | 0.035 |

| NREW | −1.950 | 0.491 | −3.971 | 0.001 | |

| REW | 0.297 | 0.149 | 1.995 | 0.057 |

| Country | Variables | Co-Efficient | Std. Error | t-Statistics | Prob. |

|---|---|---|---|---|---|

| Czech Republic | ΔlnGDPt−1 | 0.469 | 0.189 | 2.487 | 0.021 |

| ΔlnCO2 | 0.287 | 1.916 | 0.150 | 0.882 | |

| ΔlnCO2t−1 | −1.685 | 2.122 | −0.794 | 0.436 | |

| Poland | ΔlnNREW | −0.054 | 2.145 | −0.025 | 0.980 |

| ΔlnNREWt−1 | 1.078 | 1.885 | 0.572 | 0.574 | |

| ΔlnREW | 0.564 | 0.412 | 1.371 | 0.185 | |

| ΔlnREWt−1 | −0.263 | 0.355 | −0.742 | 0.466 | |

| ECTt−1 | −0.341 | 0.155 | −2.202 | 0.039 | |

| ΔlnGDPt−1 | 0.408 | 0.169 | 2.415 | 0.025 | |

| ΔlnCO2 | −0.824 | 0.378 | −2.179 | 0.042 | |

| ΔlnCO2t−1 | 0.436 | 0.444 | 0.981 | 0.338 | |

| ΔlnNREW | −0.080 | 0.821 | −0.097 | 0.923 | |

| ΔlnNREWt−1 | 0.222 | 1.020 | 0.218 | 0.830 | |

| ΔlnREW | 0.018 | 0.229 | 0.080 | 0.937 | |

| ΔlnREWt−1 | 0.172 | 0.218 | 0.789 | 0.439 | |

| ECTt−1 | −0.982 | 0.214 | −4.829 | 0.000 | |

| Hungary | ΔlnGDPt−1 | −0.230 | 0.167 | −1.372 | 0.185 |

| ΔlnCO2 | −0.455 | 0.500 | −0.910 | 0.374 | |

| ΔlnCO2t−1 | 0.584 | 0.591 | 0.987 | 0.335 | |

| ΔlnNREW | −0.024 | 0.421 | −0.058 | 0.954 | |

| ΔlnNREWt−1 | −0.329 | 0.420 | −0.784 | 0.442 | |

| ΔlnREW | −0.005 | 0.102 | −0.045 | 0.965 | |

| ΔlnREWt−1 | 0.115 | 0.093 | 1.230 | 0.233 | |

| ECTt−1 | −0.555 | 0.144 | −3.841 | 0.001 | |

| Slovak Republic | ΔlnGDPt−1 | 0.524 | 0.178 | 2.942 | 0.008 |

| ΔlnCO2 | −0.605 | 0.524 | −1.155 | 0.261 | |

| ΔlnCO2t−1 | 0.401 | 0.617 | 0.650 | 0.523 | |

| ΔlnNREW | −0.735 | 0.541 | −1.359 | 0.189 | |

| ΔlnNREWt−1 | 0.070 | 0.492 | 0.143 | 0.887 | |

| ΔlnREW | 0.259 | 0.157 | 1.649 | 0.114 | |

| ΔlnREWt−1 | −0.092 | 0.153 | −0.603 | 0.553 | |

| ECTt−1 | −0.335 | 0.161 | −2.081 | 0.048 |

| Cause → Effect | Czech Republic | Poland | Hungary | Slovakia | ||||

|---|---|---|---|---|---|---|---|---|

| χ2 | Prob. | χ2 | Prob. | χ2 | Prob. | χ2 | Prob. | |

| CO2 → GDP | 18.82 | 0.000 | 1.34 | 0.854 | 0.14 | 0.934 | 5.29 | 0.259 |

| GDP → CO2 | 2.68 | 0.443 | 19.36 | 0.001 | 3.57 | 0.168 | 3.20 | 0.525 |

| GDP → REW | 0.73 | 0.867 | 1.81 | 0.771 | 1.21 | 0.547 | 9.06 | 0.060 |

| REW → GDP | 14.83 | 0.002 | 6.01 | 0.199 | 1.73 | 0.420 | 11.98 | 0.018 |

| GDP → NREW | 2.29 | 0.514 | 5.82 | 0.213 | 6.02 | 0.049 | 2.42 | 0.659 |

| NREW → GDP | 17.65 | 0.001 | 7.79 | 0.095 | 1.30 | 0.522 | 20.80 | 0.001 |

| CO2 → REW | 0.42 | 0.935 | 10.15 | 0.038 | 1.07 | 0.585 | 7.59 | 0.108 |

| REW → CO2 | 7.35 | 0.062 | 21.18 | 0.000 | 4.35 | 0.114 | 4.56 | 0.335 |

| CO2 → NREW | 3.67 | 0.299 | 1.25 | 0.869 | 11.38 | 0.003 | 1.08 | 0.898 |

| NREW → CO2 | 5.66 | 0.129 | 8.16 | 0.086 | 1.75 | 0.418 | 3.79 | 0.436 |

| REW → NREW | 12.61 | 0.006 | 4.30 | 0.367 | 8.18 | 0.017 | 3.62 | 0.459 |

| NREW → REW | 1.07 | 0.785 | 4.66 | 0.324 | 4.55 | 0.103 | 12.19 | 0.016 |

| Country | Ser. Corr χ2 (Breusch-Godfrey LM Test) | Homoskedasticity χ2 (Breusch-Pagan-Godfrey Test) | Heteroskedasticity χ2 Test (ARCH) | Stable (Ramsey RESET Test) |

|---|---|---|---|---|

| Czech Republic | 0.910 | 0.356 | 0.151 | Stable |

| Poland | 0.552 | 0.444 | 0.582 | Stable |

| Hungary | 0.591 | 0.397 | 0.341 | Stable |

| Slovak Republic | 0.413 | 0.544 | 0.660 | Stable |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Suproń, B.; Myszczyszyn, J. Impact of Renewable and Non-Renewable Energy Consumption and CO2 Emissions on Economic Growth in the Visegrad Countries. Energies 2023, 16, 7163. https://doi.org/10.3390/en16207163

Suproń B, Myszczyszyn J. Impact of Renewable and Non-Renewable Energy Consumption and CO2 Emissions on Economic Growth in the Visegrad Countries. Energies. 2023; 16(20):7163. https://doi.org/10.3390/en16207163

Chicago/Turabian StyleSuproń, Błażej, and Janusz Myszczyszyn. 2023. "Impact of Renewable and Non-Renewable Energy Consumption and CO2 Emissions on Economic Growth in the Visegrad Countries" Energies 16, no. 20: 7163. https://doi.org/10.3390/en16207163

APA StyleSuproń, B., & Myszczyszyn, J. (2023). Impact of Renewable and Non-Renewable Energy Consumption and CO2 Emissions on Economic Growth in the Visegrad Countries. Energies, 16(20), 7163. https://doi.org/10.3390/en16207163