Abstract

The pulp and paper industry (PPI) has several opportunities to contribute to meeting prevailing climate targets. It can cut its own CO2 emissions, which currently account for 2% of global industrial fossil CO2 emissions, and it has an opportunity to produce renewable energy, fuels, and materials for other sectors. The purpose of this study is to improve understanding of the decarbonization prospects of the PPI. The study provides insights on the magnitude of needed annual renewal rates for several possible net-zero target years of industrial fossil CO2 emissions in the PPI and discusses decarbonization opportunities, namely, energy and material efficiency improvement, fuel switching, electrification, renewable energy production, carbon capture, and new products. The effects of climate policies on the decarbonization opportunities are critically evaluated to provide an overview of the current and future business environment of the European PPI. The focus is on Europe, but other regions are analyzed briefly to widen the view. The analysis shows that there are no major technical barriers to the fossil-free operation of the PPI, but the sector renovates slowly, and many new opportunities are not implemented on a large scale due to immature technology, poor economic feasibility, or unclear political environment.

1. Introduction

Industrial energy consumption accounts for nearly 40% of total global energy consumption [1]. The energy use of industry is dominated by fossil fuels, and direct industrial CO2 emissions were 8.7 GtCO2 in 2020, which represents 26% of global emissions. Industry has been considered as one of the most challenging sectors to decarbonize. The facilities have typically long lifetimes, and many technologies needed for decarbonization are still in the development phase. The demand for industrial products is expected to rise in the future, which may increase CO2 emissions [2]. In addition to CO2 emission reductions, it is expected that the industrial sector renovates by creating new products, services, additional markets, jobs, and new business models as well as shifts toward a circular and sustainable economy. Political guidance will play a central role in meeting the expectations.

Limitation of global warming to 1.5 °C requires rapid cuts in greenhouse gas emissions (GHG). The Intergovernmental Panel on Climate Change (IPPC) estimates remaining carbon budget at roughly 400–800 GtCO2, and with the current annual emissions of 42 GtCO2, the budget will be surpassed in 10–19 years [3]. The European Union (EU) aims to be the first climate-neutral continent by 2050 [4]. In 2021, the EU tightened its 2030 CO2 emissions reduction target significantly: the cut must be 55% instead of 40% in comparison with 1990 levels [4,5]. The new target includes improvements in land use, land use change, and the forestry (LULUCF) sector. Other targets were tightened as well to achieve the ambitious CO2 emissions reduction goal. A binding target for the share of renewable energy in the energy mix in 2030 increased from 32% to 40%, and the energy efficiency improvement (EEI) should deliver 36–39% lower energy consumption by 2030 in comparison with expected levels. Additionally, a proposed revision of the Energy Efficiency Directive (EED) suggests tightened requirements for annual energy savings: for 2024–2030, the annual EEI should be increased from 0.8% to 1.5% [6]. Moreover, the EU aims to cut CO2 emissions by strengthening natural carbon sinks: 310 MtCO2/a should be absorbed and stored by 2030.

The ambitious EU policies affect the PPI that is the fourth largest industrial energy user and the fifth largest CO2 emitter after the steel and iron, cement, chemicals and petrochemicals, and aluminum sectors [7]. Unlike other industrial sectors, the PPI uses significant amounts of renewable energy: nearly 60% of all used fuels were bio-based in 2019 [8]. However, there is still 1.3 EJ of gas, 1.1 EJ of coal, and 0.2 EJ of oil in the PPI’s fuel mix globally [8]. The PPI has notable potential to contribute to the emissions reduction. Many studies claim the sector can significantly improve its energy efficiency [9,10,11,12]. Substantial amounts of fossil fuels in processes and energy production can be replaced with bio-based alternatives [13,14]. Recent publications suggest that pulp mills may provide a platform for negative emissions using bioenergy carbon capture and storage or utilization (BECCS/U) technologies [15,16]. Due to the availability of wood residues and excess energy, many mills can produce biomaterials and biofuels or e-fuels that are highly needed in sectors that are difficult to electrify [17].

The aim of this study is to improve the understanding of the decarbonization prospects of the European PPI and critically evaluate the effects of various policies of the upcoming EU Green Deal on business environment and decarbonization opportunities for the PPI. The study considers the following issues: (1) a required investment rate (the approximate renewal rate) for several possible net-zero target years of industrial CO2 emissions in the PPI, (2) opportunities to cut CO2 emissions within the PPI and changes caused by possible incentives to create negative emissions to outline what should be changed from a policy point of view to enable an efficient decarbonization of the PPI, and (3) differences between developing countries and Organization for Economic Co-operation and Development (OECD) countries. The studied decarbonization prospects focus on industrial operations of the European PPI, leaving, for example, offsite electricity production, transport, and forest management outside the scope. It is expected that the energy and transport sectors will decarbonize in the future, and harvesting of forest by the PPI does not surpass the annual growth rate.

2. Materials and Methods

Evaluation of development opportunities requires understanding of the current state. This section briefly introduces the current state of the European PPI, presents the methods utilized in this study, and introduces the used data sources and background assumptions.

2.1. Energy Consumption and CO2 Emissions in the European Pulp and Paper Industry

The current status of the European PPI is presented in Table 1. The presented values were based on the Confederation of European Paper Industries (CEPI) database presenting the situation in 2020 [18]. The data covered ~91% of European pulp and paper production, and thus, the values were scaled to cover the whole of Europe.

Table 1.

Current status of the European pulp and paper industry. Data from CEPI [18].

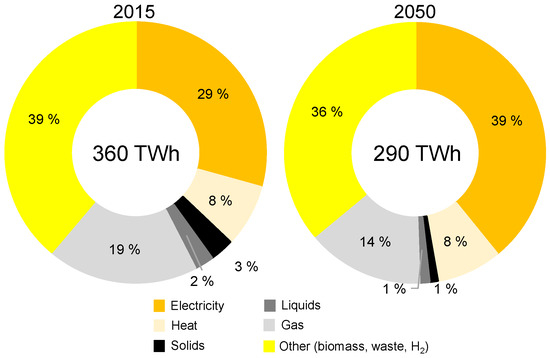

The European Commission has created a reference scenario for reflecting the development of the EU energy system, transport, and GHG emissions [19]. The scenario took into account the EU-level policies adopted until the end of 2019, member state projections, national contributions, and planned policies, as well as fuel prices, macro-economics, and technology trends. As a large and energy-intensive sector, the PPI was included in the European Commission’s future projections. Figure 1 presents the current state and expected development of energy use in the European PPI. The scenario claimed that the role of electricity in the energy mix would increase. The already low use of solid and liquid fossil fuels would be practically phased out. The use of bioenergy for energy decreased as a result of EEI, and natural gas was expected to remain in the energy mix. The scenario assumed that technologies for emission abatement, i.e., carbon capture technologies, were difficult to adopt. The projection expected that fossil fuel use in the mill sites would decrease by 44%, which led to a significant reduction in direct fossil CO2 emissions. Despite that, the PPI can, and needs to, do more.

Figure 1.

Energy use in the European pulp and paper industry in 2015 and 2050. Data from European Commission [19].

It should be noted that the scenario was published in 2021. The geopolitical situation in Europe changed in 2022, which has significantly affected the energy prices and energy supply security. The changes in the business environment could lead to rapid development, for example, to an accelerated reduction of fossil fuels.

2.2. Evaluation of the Future Prospects of CO2 Emissions

The business environment has a significant effect on the operation of an industrial sector, and therefore, a brief review was conducted to provide insights on expected and ongoing future trends. The European Emission Trading System (EU ETS) is one of the most important measures for CO2 emissions reduction in Europe, and it thus affects the business environment of the PPI. Hence, the effect of the EU ETS on the PPI was looked at in this study. The participants of the ETS pay for the emitted fossil CO2 emissions. In its first 15 years (2005–2020), the EU ETS did not exceed a carbon price of EUR 30/tCO2, but at the beginning of 2022, the price was almost EUR 100/tCO2 [20]. In this study, the effect of the high carbon price (EUR 100/tCO2) on different pulp and paper mill types was calculated. Data on fossil CO2 emissions and production volumes of different mill types from every Finnish and Swedish mill were collected during previous studies [21,22,23] and were used in this study as an illustrative example of the differences between mill types. The mills were grouped based on their main products. The costs of the EU ETS were divided by production volumes to receive the effect of ETS on the production cost of pulp and paper. The structure of the Finnish and Swedish PPI is not similar to the European PPI. Many European countries focus on paper production, whereas Finland and Sweden are important pulp producers. However, the data on the Finnish and Swedish mills provided a good approximation of the differences between the mill types.

A required renewal rate was calculated for the European PPI within several net-zero target years to evaluate the magnitude of needed annual changes. The key assumption was that new or renovated capacity does not emit any fossil CO2. The renewal rate was calculated for constant production volumes. Both production volumes and CO2 emissions were based on the 2019 levels presented in Table 1. Therefore, it was calculated how much existing capacity needed to be replaced annually in order to proceed from 2019 fossil CO2 emission level to a PPI that did not emit direct fossil CO2 emissions in the mills. The calculations and assumptions were rough but provided indicative insights on the magnitude of needed renewal rates.

In addition to discussion on changes in business environment and needed renewal rates, this study looked at the future opportunities of the PPI. The potentials of different development paths were evaluated based on previous studies and current volume and structure of the production in the European PPI. The political environment will play a major role in the development of the PPI, and thus, the expected effects and importance of prevailing and upcoming policy measures were discussed. The study highlighted the improvement potential and outlined what should be changed from a policy point of view to enable an efficient decarbonization of the PPI. The study utilized data on the Finnish and Swedish forest industries gathered during the authors’ previous studies [21,22,23] as illustrative examples on the ongoing industrial development. Finland and Sweden have been forerunners in energy-efficient operation and decarbonization of the PPI, and thus, the countries provide interesting insights. However, it was not expected that the European PPI would follow the same pathways as the Finnish and Swedish ones, because the structure of the PPI varies significantly within the countries.

Reduction of energy consumption was evaluated taking into account energy efficiency improvement and changes in production mix. This was estimated using production volumes from the Food and Agriculture Organization of the United Nations (FAO) [24] and specific energy consumption (SEC) values provided by Farla et al. [25]. Although the SEC values (Table 2) were estimated already in 1997 and energy efficiency has improved since then, the values illustrate differences between pulp and paper grades and can therefore be used for estimating changes in energy consumption caused by the changes in production mix.

Table 2.

Examples of the energy consumptions of different products. Data from Farla et al. [25].

Opportunities for fuel switching and electrification were investigated by mapping how the PPI uses fossil fuels at the moment and how those fuels could be replaced by fossil-free energy sources. In addition to fossil fuels in energy production, PPI processes that combust fuels were discussed as well. Lime kiln is the most significant emission source in the sulphate (kraft) pulp mill. Finland and Sweden have been forerunners in fuel switching in lime kilns, and therefore, the fuel use in the lime kilns in Finland was studied by collecting data from environmental reports and permits [26] mapping how mills have succeeded in fuel switching.

Opportunities to provide additional CO2 savings were considered looking at increased renewable electricity production and novel opportunities. A literature survey was conducted to improve understanding of the opportunities. A simplified mass and energy balance for a typical kraft pulp mill was constructed to illustrate the potential of a pulp mill as a producer of bio-based side streams, renewable electricity, and CO2. The mill balance was based on a mill model used in previous studies [27,28]. Based on the collected data, the potential, the effects of new processes on the mills, and the magnitudes of possible CO2 savings were estimated.

2.3. Distribution and Progress of the CO2 Emissions in the Global Pulp and Paper Industry

The European PPI covers only approximately one-fourth of the global pulp and paper production, and therefore, it is important to briefly widen the perspective of this study to other PPI countries. A geographical distribution of fossil and biogenic CO2 emissions originating from global pulp and paper production was evaluated to understand the role of different regions in CO2 emissions generation. The expected progress is discussed by comparing the development of the PPI in the OECD countries and developing countries.

CO2 emissions were estimated for all continents that produce pulp and paper (Europe, North America, South America, Australia, Asia, and Africa). In this study, the continents were compared, but it should be noted that there were differences also within the countries located on the same continent. Data on CO2 emissions were collected, but to the authors’ knowledge, no comprehensive statistics on regional emissions or fuel use of the PPI exist, and especially biogenic CO2 emissions are poorly reported. Thus, when the emission data were not available, the CO2 emissions were estimated by the authors.

Due to variation in data availability, two main approaches were used for estimating the CO2 emissions of the regions. In the first approach, the emissions were calculated by multiplying fuel use by CO2 emission intensity of the fuel (Equation (1)).

where Fi stands for fuel consumption by fuel type (GJ), and Ii is the CO2 emission intensity of a certain fuel (kgCO2/GJ). The second approach utilized production volumes of the regions and specific CO2 emissions of products (Equation (2)).

where Pi stands for production volume (tons), and ii is the specific fossil CO2 emissions of the product (kgCO2/ton).

CO2 emission intensities were adopted from a comprehensive fuel properties database provided by the Statistic Finland [29]. Production volumes were collected from FAO [24], and reports on energy use and emissions [18,30,31,32,33] were utilized. Data on the use of biofuels were poorly available, and thus, assumptions were needed to calculate the consumption of biofuels to be able to estimate the emissions. Moreover, the calcination process in kraft pulp mills generates biogenic CO2 emissions. Due to the lack of data, the biogenic CO2 emissions from calcination were calculated using production volumes and an average value for the emissions. The following assumptions were used:

- Pulp production generates approximately 19 GJ/ADt of black liquor and 0.7–3 GJ/ADt of wood residues, which are typically combusted to energy [34].

- The calcination process in chemical pulp mills produces about 196 kgCO2/ADt of biogenic CO2 [35].

The total fuel use provided by the International Energy Agency (IEA) [1] was utilized to estimate global fossil and biogenic CO2 emissions of the PPI. The overall emissions were used to evaluate the validity of the regional values.

3. Results and Discussion

This section presents future prospects for the European PPI. Expected changes in the business environment are reviewed, and the magnitude of the required annual renewal rate is evaluated. The section presents the possible development pathways and measures for CO2 emissions reduction. The study discusses how the current political environment guides the sector’s transformation and points out what should be changed in a policy point of view to enable an efficient decarbonization. Finally, the section highlights differences in progress on the decarbonization of the OECD and developing countries.

3.1. Future Prospects of CO2 Emissions

The business environment of the PPI is continuously changing. Prices on CO2 emissions and energy are increasing, demand for products is changing, and competition on biomass may grow. The reaching of net-zero industrial emissions depends on the business environment, and even if the environment would be suitable, significant renovations are needed to achieve a fossil CO2-neutral sector.

3.1.1. Changes in the Business Environment

The demand for different products is changing, which forces mills to modify their product portfolio. The need for packaging materials is increasing, for example, due to growing global markets and the need to substitute plastic packages, whereas digitalization has led to a notably decreasing demand for graphic papers in the OECD countries. In addition to traditional products, the demand for several kinds of novel wood-based solutions such as textiles is increasing.

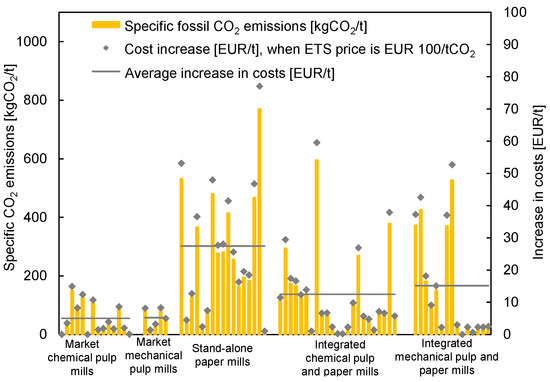

Increasing prices for energy and especially CO2 will force mills to change their energy use practices. The effect of high ETS prices on the pulp and paper mills is presented in Figure 2. The effect varies notably within the mills. The variation can be caused by several factors, such as energy efficiency, integration rate of the mills, implemented decarbonization actions, or the energy supply strategy. However, clear differences between mill types can be seen.

Figure 2.

Impact of high EU ETS carbon prices (EUR 100/tCO2) on the production costs of different mill types.

Stand-alone paper mills do not have large bio-based side streams that could be combusted to energy, and therefore, those mills typically utilize fossil fuel for both energy production and paper drying. Thus, stand-alone paper mills have the greatest pressure to cut emissions. Applying a bubble policy [36], which allows even increasing the emissions in some facilities as long as total emissions are reducing, could be the most cost-effective way toward a low-carbon sector. That is because, for example, the mills with access to bio-based waste streams may have better opportunities to replace fossil fuels by intensifying the use of biomass. Chemical pulp mills represent mill types that can already meet most of their energy demand by bio-based fuels. If a chemical pulp mill is integrated with a paper mill, the energy consumption of the unit increases, and current mills typically require fossil fuels in addition to biofuels. The direct effect of EU ETS is low in the case of mechanical pulp mills because most of those mills cover their energy demand largely by purchasing electricity. However, the EU ETS affects indirectly also the prices of purchased electricity and the costs of transportation.

The production costs of pulp and paper vary significantly, and typically, those costs are not publicly available. RISI [37] presents that the production cost for paper in Europe could be around EUR 500/ton, and hence, the EU ETS can increase the costs notably in some mills. It should be noted that at the moment, energy-intensive industries receive a significant amount of free emission allowances to secure competitiveness, which may change in the future. Moreover, the high EU ETS prices can increase competition on biomass that does not belong to the EU ETS. The EU ETS is not the only factor affecting the energy use of the PPI at the moment. The prices for fossil fuels are expected to rise. Electricity prices are currently unusually high, but future development remains to be seen.

In addition to the EU ETS, other factors may influence the availability of bio-based raw materials. Ambitious targets for saving and restoring biodiversity may affect the markets for raw materials. The EU has published a biodiversity strategy, which expands protected land and sea areas to 30% in Europe [38]. Moreover, there is a target to cut a significant amount of CO2 emissions by strengthening natural carbon sinks. The targets have led to discussions on the acceptable harvesting rates.

3.1.2. Required Investment Rates for Net-Zero Target Years of Industrial CO2 Emissions

The required renewal rates for different net-zero target years in the European PPI were calculated assuming that the new-built or renewed capacity is fossil-free. The results presented in Table 3 show that decarbonization of the sector within the next 10–20 years requires large annual investments. Reaching carbon neutrality by 2050 requires moderate but continuous annual improvements. The energy efficiency of existing technologies and processes increases continuously, and new opportunities come into the markets. Thus, the sector has an opportunity to move toward significantly more sustainable operation. Despite that, it should be noted that the pulp and paper mills have long lifetimes, and the renovation rate is slow. A typical technical lifetime of a mill is between 30 and 50 years, and thus, the renewal rate in Europe is roughly 2–3% of the capacity per year. The fossil CO2 emission reduction within the PPI cannot be considered as a straightforward task. The annual renewal rates will vary depending for example on the global economy. In addition, some CO2 sources are significantly easier to eliminate than others; for example, switching to electric dryers does not require large changes in the mills, whereas renewal of the energy system of a whole mill is a huge investment. The following sections will evaluate the decarbonization opportunities and potential.

Table 3.

Required renewal rates for achieving carbon neutrality in different net-zero target years.

3.2. Reduction of Energy Consumption

The lion’s share of the CO2 emissions of the PPI industry originates from energy production, and therefore, a decrease in energy consumption is key in emissions reduction. The energy consumption of the sector depends strongly on the production volume and mix. Energy can be saved by EEI, for example, by recovering waste heat and by material efficiency improvement, but also the production mix and volume of the sector affect the energy consumption.

3.2.1. Changes in Production Volume and Mix

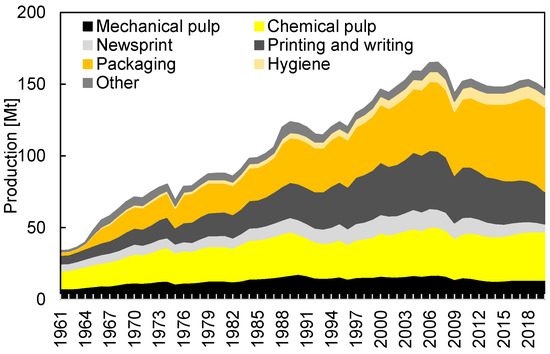

The total production volume in the European PPI has been rather stable during the last 10 years, but the structure has changed (Figure 3). The share of wrapping and packaging materials in paper production increased from 40% to 59% between 2000 and 2020, and the share of graphic papers dropped from 49% to 28%. It can be expected that the trend will continue. Typically, the production of packaging materials consumes around 20% to 30% less energy per ton than the production of graphic papers. Thus, the structural change has an effect on the energy consumption. If the total production volume is kept constant, and the share of packaging materials increases to 75% by 2050, the expected annual heat and electricity savings due to changes in the production mix is roughly 4%. Increased utilization of recycled fibers in paper production has enabled lower energy consumption in the European PPI, but the recycling rate is already high, and no major savings are expected due to increased recycling rates [39].

Figure 3.

Development of pulp and paper production in the European pulp and paper industry. Data from FAO [24].

The structural changes of the PPI are not limited to changes between conventional pulp and paper grades. The sector has become interested in widening its product portfolio, which may affect notably the energy consumption of the whole sector. For example, if the sector starts to produce hydrogen-based products, the energy consumption of the PPI will increase notably. One illustrative example of the ongoing transition is the UPM Leuna biorefinery in Germany [40]. The plant will start to produce wood-based chemicals in 2023. If the biorefinery is statistically included in the PPI, the energy consumption of the sector will increase, whereas energy demand in the chemical sector decreases as the biorefinery replaces current production. This highlights the challenge of setting energy savings targets for sectors. The possible future products will be discussed in Section 3.4.

3.2.2. Energy Efficiency Improvement

The EEI has been considered the most cost-effective way to reduce energy use and related CO2 emissions [41]. Several studies have investigated energy savings potential through EEI measures, and for example, Moya and Pavel [42] suggest that the European PPI can cut its energy consumption cost effectively by 14% (~190 PJ) between 2015 and 2050, and the CEPI [43] claims that EEI can lead to a 7 MtCO2/a emission reduction by 2050. In addition to allowing the reduction of fossil fuel use, the EEI may enable the use of generated biomass elsewhere. Table 4 presents the development of specific energy consumption in the Finnish PPI, which illustrates the continuous EEI. In spite of the EEI, high-quality requirements may increase the consumption, as in the case of mechanical pulp. Updating the existing mills to operate with the currently best available technologies can cut energy demand notably, but emerging technologies are expected to enable even larger cuts; for example, the use of deep eutectic solvent may reduce the primary energy demand of pulping by 40% [44]. However, the adoption of new technologies that significantly change the pulping or paper-making processes may be difficult and slow due to concerns about the effects on the operation.

Table 4.

An example of development of specific energy consumptions. Estimates were created for the Finnish pulp and paper industry based on Carlson and Heikkinen, and Pöyry [45,46].

A proposed revision of the EED calls for increasing the annual energy savings requirement for 2024–2030 from 0.8% to 1.5% [6]. As a large energy user, the PPI must significantly contribute to the energy savings. The authors’ previous study shows that the Finnish and Swedish PPIs managed to substantially improve their energy efficiency between 2002 and 2017 [21], but the improvement pace did not meet the requirements of the EED. Thus, the improvement pace must be accelerated, and the need applies most probably also to other PPI countries. The EEI can lead to notable savings in energy costs in energy-intensive industries, and therefore, it has been discussed if there is a real need to support the industrial EEI by policy incentives or if market forces can drive the change toward energy savings [47]. However, barriers to EEI, such as technical risks or a lack of access to capital, are hindering even the adoption of cost-effective measures [48]. Thus, political stimulation is needed for overcoming the barriers.

3.3. Fuel Switching and Electrification

In the PPI, fossil fuels are used in steam production and pulping (lime kilns) and papermaking (dryers) processes. All fossil fuels are technically possible to replace with biofuels or electricity [49], but the likelihood to reach net-zero emissions depends on the mill type. Modern chemical pulp mills can already achieve fossil carbon-free operation [50], and consequently, it is realistic to expect that new-build mills do not need fossil fuels during normal operation. Decarbonization of stand-alone paper mills is more challenging because the energy production relies on fossil fuels instead of biomass, which is a dominating fuel in the pulp mills. Currently, electricity and steam are produced in boilers that combust mainly natural gas, but also some amounts of coal-fired boilers are used.

The pulp and paper-making processes are technically possible to decarbonize. Electricity-based paper dryers are already used in some mills, and further electrification of the dryers could reduce annual emissions by 1–2 MtCO2 in Europe [51]. Some mills have also stated an aim to combust hydrogen in dryers [52]. Recent studies suggest that also lime kilns can be electrified using electric gas-plasma technology in the future [53], which may be an interesting opportunity especially for mills that have no excess biomass. In addition, indirect electrification, i.e., the use of renewable hydrogen or hydrocarbon, is a possible but currently costly and rather inefficient opportunity to decarbonize the lime kilns. So far, the use of biofuels has been a leading solution as many pulp mills have bio-based residues that can be combusted in lime kilns.

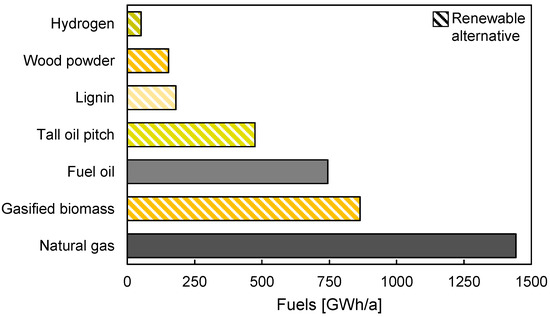

Production of pulp consumes approximately 250 kg/ADt of lime (CaO) [35], and the production of lime requires 6–10 GJ/kgCaO of heat [54]. The European PPI produces annually 32 Mt of kraft pulp, and mills combust mainly natural gas in the lime kilns, which means that annual fossil CO2 emissions are around 3–4 MtCO2 or roughly 10% of total industrial fossil CO2 emissions of the sector. At the moment, Finland and Sweden have been leading the decarbonization of their lime kilns (Figure 4) [21]. Thus, switching to biofuels is feasible, but it comes with some economical and technical challenges, especially in cases of retrofits. Biofuels have different properties, for example, lower heating value than conventionally used oil and natural gas, which make it difficult to operate existing lime kilns without supporting fossil fuels. It can be expected that new-build lime kilns use biofuels or other renewable alternatives. Moreover, the availability of biomass varies within the mills, which affects the feasibility to use biofuel for decarbonizing the lime kilns.

Figure 4.

Estimated current fuel mix in lime kilns of the Finnish pulp and paper industry.

The estimate for the CO2 emission reduction potential of energy efficiency improvement was at 7 MtCO2/a. In addition, changes in production mix may lead to lower energy consumptions and therefore lower emissions, but the total fossil CO2 emission reduction due to energy savings is estimated to remain below 10 MtCO2/a. It was estimated that the emission reduction potential of dryers and lime kilns are 1–2 MtCO2/a and 3–4 MtCO2/a, and thus, the decarbonization of processes can lead to an emission reduction of 4–6 MtCO2/a. As the European PPI currently emits 34 MtCO2/a, the decarbonization of energy production plays the largest role in the reaching carbon-neutral PPI. As the PPI has access to wood residues and most of the energy supply is already covered using renewables, in the near future, electrification will not play as significant a role in the PPI as in other industrial sectors such as the steel industry. Even though part of the energy demand can be covered by the intensified use of current biofuels, biomass can be considered as a limited resource, and therefore, electricity-based solutions are also needed. High-temperature heat pumps have been seen as a significant part of the future energy supply in the PPI [55]. Increasing competition for renewable electricity and rising prices may be a matter of concern. Obrist et al. [55] claim that the Swiss paper industry that does not produce any chemical pulp can reach net-zero emissions by 2050, but this would lead to an 8–15% increase in paper production costs. Moreover, the re-structuring of energy supply and processes requires significant modifications in the mills. In the long-term future, the role of electricity may increase in the PPI as the increasing share of bio-based residues may be utilized as products. Even though the direct use of electricity is the best solution in terms of efficiency, it is possible that hydrogen will play a role in industrial energy systems as a storage for renewable energy.

3.4. Opportunities to Provide Additional CO2 Savings

The PPI has access to sustainably harvested biomass. The raw materials cannot be fully converted to pulp and paper, and therefore, large bio-based side streams enable the sector to contribute to the decarbonization of other sectors by producing renewable energy, fuels, and products and capturing biogenic carbon. Hence, in addition to targeting the cut of industrial emissions, the PPI’s potential to provide additional CO2 savings must be exploited.

3.4.1. Additional Renewable Electricity Production

The PPI can increase its renewable electricity production. A recovery boiler is most importantly a process component that regenerates used cooking chemicals in a kraft pulp mill, but it is additionally a large steam and electricity producer. The most important criterion for a recovery boiler has been high availability. Later, the mitigation of air emissions became an issue. Currently, the increasing production of renewable electricity is a key trend. An increase in steam parameters and black liquor dry solids contents and heat recovery from flue gases as well as improved preheating of both water and air can lead to notable growth in the electricity generation. According to Vakkilainen et al. [56], electricity generation in modern recovery boilers increased by 20% within 10 years, and thus, veritable opportunities for higher electricity production exist. Sweden is an example of a country which has notably increased electricity generation in the PPI [21]. The most important reasons behind the shift are an increase in the electricity price due to an electricity market reformation as well as an introduction of the EU ETS and a green electricity certificate system that supports the production of renewable electricity [57]. Thus, future energy markets as well as incentives for renewable electricity production most probably affect the development of electricity production in the PPI.

Table 5 presents recovery boiler parameters for an average European mill and for a modern mill. Based on rough calculations presented by Valmet [58], it can be estimated that if all European recovery boilers operated as modern boilers, renewable electricity production could increase by roughly 7 TWh. If the electricity is used for replacing current European electricity production with an emission intensity of 296 gCO2/kWh [59], an annual savings of approximately 2 MtCO2 could be achieved. It is noteworthy that the additional energy production in the PPI conflicts with the energy efficiency target that aims to limit energy consumption to a certain value; i.e., in spite of the increased production of excess energy, the input energy to the mill might not change.

Table 5.

Recovery boiler parameters: a European average and a modern mill.

Despite the potential to increase renewable electricity production, alternative routes could lead to reduced generation. Processing of biomass to high-value products decreases available combustible material. For example, lignin separation has become an attractive option as lignin can be used as a versatile raw material or biofuel. Separating 30% of the lignin in black liquor decreases the electricity production in the recovery boiler by approximately 29% [60]. In addition, possible electrification may have an effect on onsite electricity production; i.e., if electricity is used for heating purposes, production of electricity in combined heat and power (CHP) units decreases.

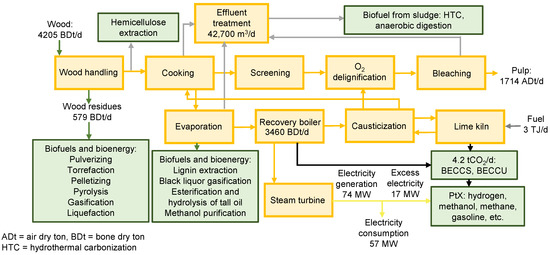

3.4.2. Renewable Fuels and Materials

The PPI can play a notable role in creating bioeconomy. Its side streams can be utilized in the production of biofuels (e.g., biogas and biodiesel) and bioproducts (e.g., textile fibers, fertilizers, and lignin derivatives). As an example, Figure 5 presents a simplified balance and opportunities of a northern stand-alone mill producing 600,000 ADt/a of softwood pulp. The mill generates approximately 340 kg/ADt and 760 kg/ADt of wood residues and dissolved lignin, which indicates the potential for enlarging the product portfolio to new bioproducts. In spite of several opportunities and existing pilot plants, the number of large-scale retrofits in mills is low even though many technologies are available [17]. Releasing the potential of PPI as a producer of new products requires a stable and consistent political framework including, for example, ambitious targets for bioenergy use or quota obligations [61]. Additionally, the PPI should have clear future prospects for affordable raw materials. Currently, the role of biomass in the EU’s decarbonization strategies is slightly unclear, and the role of forests as carbon sinks as well as possible competition on biomass with other sector creates uncertainties.

Figure 5.

A northern stand-alone mill producing 600,000 ADt/a of softwood pulp and its future opportunities.

3.4.3. Carbon Capture and Production of E-Fuels

Pulp mills have a unique opportunity to turn to carbon sinks using BECCS/U [16]. Achieving a carbon-neutral society might not be possible without carbon capture technologies [62], but there has been little progress on CCS and especially BECCS. The possibilities of BECCS in the PPI were already discussed at the beginning of the 21st century [63], and Jönsson et al. [64] estimated that the European PPI has a large potential to capture CO2 (60 MtCO2/a). Post-combustion carbon capture using monoethanolamine (MEA) is a commercially available process and thus the most studied option for pulp mills [64,65,66,67]. The process consumes approximately 3.8 GJ/tCO2 and 0.1 MWh/tCO2, of heat and electricity [68], which means capturing 60 MtCO2/a would lead to additional heat and electricity consumption of 228 PJ/a and 6 TWh/a. In addition to the effects on energy balance, questions on storage sites, transportation, utilization, and economic feasibility exist. Several previous studies underline a lack of economic incentives and clear policy framework, and they call for recognizing negative CO2 emissions and crediting all removed CO2 emissions apart from the origin [65,69,70,71,72,73]. BECCS will not be adopted in mills without clear incentives. Santos et al. [74] suggest that a negative CO2 credit of 42 e/tCO2 could overcome the costs of carbon capture via calcium looping, and Onarheim et al. [65] claim that a negative emissions credit of 60–80 e/tCO2 is needed to make BECCS attractive for the mills.

Captured CO2 can be combined with hydrogen (H2) to produce e-fuels such as methane, methanol, gasoline, and ethanol [75]. E-fuels may play a versatile role in the future energy system: they can substitute fossil fuels in energy production as well as in the chemicals industry, balance intermittent renewable energy production by providing energy storage and flexible load, and decrease the need for electricity grid reinforcement by acting as an energy carrier [76]. The production of e-fuels consumes a lot of electricity. For methane, methanol, and dimethyl ether, the electricity-to-fuel efficiencies are in the range of 30–75% (1.33–3.33 MWhel/MWhfuel), and the production requires roughly 0.21–0.28 tCO2/MWhfuel [77]. As the PPI is a stationary producer of both biogenic CO2 and renewable electricity, and the mills have an opportunity to utilize side streams of e-fuel processes (oxygen and heat), the mills are interesting platforms for e-fuels production. If currently produced excess electricity in the mills (13 TWh) was converted to e-fuels, the production would yield as 3.9–9.8 TWhfuel, and the production would bind 0.8–2.7 MtCO2. The biogenic CO2 from the European PPI facilitates a production of 290–390 TWhfuel, but the electricity consumption would be 390–1300 TWh. This would account for a fraction of the demand; for comparison, the European transport sector alone consumed 4889 TWh of energy in 2017 [78].

A political framework for e-fuels is still incomplete, but current proposals do not support the use of bioenergy for the production of renewable e-fuels [79,80]. Therefore, pulp mills would need to purchase renewable electricity that is of non-biological origin. This, along with other rules, makes the business environment complicated for pulp mill operators and decreases the attractiveness to invest. Moreover, the requirement to use variable renewable electricity instead of continuously produced bioelectricity may crucially decrease the profitability of the e-fuels production due to lower operational hours. At the moment, there are no requirements for the origin of CO2, and therefore, the PPI does not benefit from its biogenic emissions. Under the current constraints, e-fuels production does not seem attractive in the European PPI mills even though the platform for production could be suitable. Furthermore, it should be noted that carbon capture and especially the production of e-fuels conflict with the energy efficiency improvement target due to the high energy intensity.

3.5. Progress in Developing vs. OECD Countries

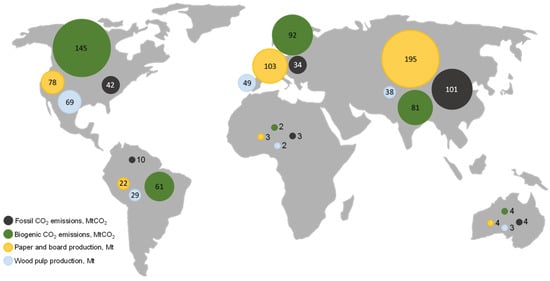

The geographical distribution of CO2 emissions and production volumes of the global PPI are presented in Figure 6. The combustion of fossil fuels in the PPI produces annually approximately 194 MtCO2, and the combustion- and process-based biogenic CO2 emissions are approximately 357 MtCO2 per year. The production mix and volume are important factors when decarbonization in a certain region is considered. Pulp mills can cover their energy demand by their own wood residues, whereas stand-alone paper mills typically rely on fossil fuels. Therefore, decarbonization can be considered easier in pulp producer regions, for example, South America, and challenging in paper producer countries such as China. In addition to production-related factors, national resources such as the availability of biomass or fossil fuels affect the fuel mix in the PPI. For example, natural gas is the main fossil fuel in Europe and North America, whereas energy production in the Chinese PPI relies on coal. Most of the virgin pulp mills are located in forested countries, and those countries are also the largest users of biomass as fuel.

Figure 6.

The geographical distribution of CO2 emissions and production volumes of the global pulp and paper industry.

According to Kuparinen [16], mills in the OECD countries are more eager to adopt new technologies and change their business than mills in developing countries, which has been seen as innovative products such as lignin-based solutions. However, conditions for novel energy-intensive technologies, for example, the production of hydrogen and carbon capture processes, might be more attractive in developing countries. In southern countries, for example, in South America, the stand-alone pulp mills may have an excess of heat and electricity that cannot be sold due to limited access to the electric grid, whereas in northern countries, pulp mills are typically integrated into paper-making, or the mills can sell energy to the electricity grid and district heating network. Political environment varies between regions as well, and often the OECD countries have a higher pressure to decrease CO2 emissions (e.g., the EU ETS), which also affects the progress of the PPI.

4. Conclusions

The pulp and paper industry has several opportunities to decarbonize its own operation and contribute to the emissions reduction in other sectors. The sector has no crucial barriers to reaching net-zero industrial emissions, but achieving that potential requires significant changes. In the European PPI, the theoretical annual capacity renewal rate of 3.2% would be needed to eliminate industrial fossil CO2 emissions by 2050 even if all new-build capacity was fossil-free. The prospects for and the progress of decarbonization vary within the mill types as well as the regions. Kraft pulp mills have good premises to achieve carbon neutrality or even act as carbon sinks. Stand-alone paper mills that cover their energy demand combusting fossil fuels need the significant changes of energy supply. Decarbonization pathways will vary within the regions due to different production volumes, mill types, available resources, used fuels, and prevailing trends.

The opportunities of the PPI in CO2 emissions reduction are versatile but also overlapping; i.e., it must be decided how valuable biomass should be utilized in the future. In the near future, the PPI can intensify the energy use of bio-based waste streams, which facilitates the transition toward fossil fuel-free mills together with the energy efficiency improvement and electrification of processes and energy production. In the long-term future, the residues of the PPI industry may play a key role in the bioeconomy that aims to eliminate fossil raw materials, which might increase the role of the electrification of the sector. The technologies for the production of novel renewable products are mostly available, but the number of implemented projects is low due to poor economic feasibility and because the continuously changing business environment is not attractive for investors, and some policies are hindering the enlargement of the product portfolio (e.g., the production of e-fuels). To advance, the role of bioeconomy and e-fuels in the sustainable transition needs to be clarified, and the role of the PPI should not be underestimated, as there will be a huge need for renewable materials.

Author Contributions

Conceptualization, S.L. and E.V.; methodology, S.L.; investigation, S.L.; data curation, S.L.; writing—original draft preparation, S.L.; writing—review and editing, E.-L.A. and E.V.; visualization, S.L.; supervision, E.V. All authors have read and agreed to the published version of the manuscript.

Funding

The authors gratefully acknowledge the funding from the Academy of Finland for the project “Role of forest industry transformation in energy efficiency improvement and reducing CO2 emissions”, grant number 315019.

Data Availability Statement

Data is contained within the article: sources for utilized data are given in this article.

Conflicts of Interest

The authors declare no conflict of interest.

References

- International Energy Agency (IEA). Tracking Industry 2021. 2022. Available online: https://www.iea.org/reports/tracking-industry-2021 (accessed on 8 December 2021).

- International Energy Agency (IEA). World Energy Outlook 2021—Revised Version. 2022. Available online: https://www.iea.org/reports/world-energy-outlook-2021 (accessed on 12 February 2022).

- Masson-delmotte, V.P.; Zhai, H.O.; Pörtner, D.; Roberts, J.; Skea, P.R.; Shukla, A.; Pirani, W.; Moufouma-Okia, C.; Péan, R.; Pidcock, S.; et al. Summary for Policymakers, in Global Warming of 1.5 °C, An IPCC Special Report on the Impacts of Global Warming of 1.5 °C above Pre-Industrial Levels and Related Global Greenhouse Gas Emission Pathways, in the Context of Strengthening the Global Response to the Threat of Climate Change, IPCC. 2018, pp. 1–23. Available online: https://www.ipcc.ch/sr15/chapter/spm/ (accessed on 12 February 2022).

- European Commission. Delivering the European Green Deal. 2021. Available online: https://ec.europa.eu/info/strategy/priorities-2019-2024/european-green-deal/delivering-european-green-deal_en (accessed on 21 March 2022).

- European Commission. 2030 Climate & Energy Framework. 2021. Available online: https://ec.europa.eu/clima/eu-action/climate-strategies-targets/2030-climate-energy-framework_en (accessed on 5 April 2022).

- European Commission. Energy Efficiency Directive. 2021. Available online: https://ec.europa.eu/energy/topics/energy-efficiency/targets-directive-and-rules/energy-efficiency-directive_en (accessed on 5 April 2022).

- International Energy Agency (IEA). Energy Technology Perspectives 2020. 2020. Available online: https://www.iea.org/reports/energy-technology-perspectives-2020 (accessed on 13 February 2022).

- International Energy Agency (IEA). Pulp and Paper. 2022. Available online: https://www.iea.org/fuels-and-technologies/pulp-paper (accessed on 2 April 2022).

- Klugman, S.; Karlsson, M.; Moshfegh, B. A Scandinavian chemical wood-pulp mill. Part 2. International and model mills comparison. Appl. Energy 2007, 84, 340–350. [Google Scholar] [CrossRef]

- Peng, L.; Zeng, X.; Wang, Y.; Hong, G. Analysis of energy efficiency and carbon dioxide reduction in the Chinese pulp and paper industry. Energy Policy 2015, 80, 65–75. [Google Scholar] [CrossRef]

- Kong, L.; Price, L.; Hasanbeigi, A.; Liu, H.; Li, J. Potential for reducing paper mill energy use and carbon dioxide emissions through plant-wide energy audits: A case study in China. Appl. Energy 2013, 102, 1334–1342. [Google Scholar] [CrossRef]

- Fleiter, T.; Fehrenbach, D.; Worrell, E.; Eichhammer, W. Energy efficiency in the German pulp and paper industry—A model-based assessment of saving potentials. Energy 2012, 40, 84–99. [Google Scholar] [CrossRef]

- Kuparinen, K.; Vakkilainen, E. Green pulp mill: Renewable alternatives to fossil fuels in lime kiln operations. BioResources 2017, 12, 4031–4048. [Google Scholar] [CrossRef]

- Laurijssen, J.; Faaij, A.; Worrell, E. Energy conversion strategies in the European paper industry—A case study in three countries. Appl. Energy 2012, 98, 102–113. [Google Scholar] [CrossRef]

- Onarheim, K.; Santos, S.; Kangas, P.; Hankalin, V. Performance and costs of CCS in the pulp and paper industry part 1: Performance of amine-based post-combustion CO2 capture. Int. J. Greenh. Gas Control 2017, 59, 58–73. [Google Scholar] [CrossRef]

- Kuparinen, K. Transforming the Chemical Pulp Industry—From an Emitter to a Source of Negative CO2 Emissions. LUT University. 2019. Available online: https://lutpub.lut.fi/handle/10024/160057 (accessed on 13 January 2022).

- Mäki, E.; Saastamoinen, H.; Melin, K.; Matschegg, D.; Pihkola, H. Drivers and barriers in retrofitting pulp and paper industry with bioenergy for more efficient production of liquid, solid and gaseous biofuels: A review. Biomass Bioenergy 2021, 148, 106036. [Google Scholar] [CrossRef]

- Confederation of European Paper Industries (CEPI). Key Statistics 2020. 2021. Available online: https://www.cepi.org/key-statistics-2020/ (accessed on 13 January 2022).

- European Commission. EU Reference Scenario 2020. 2021. Available online: https://energy.ec.europa.eu/data-and-analysis/energy-modelling/eu-reference-scenario-2020_en (accessed on 13 January 2022).

- Trading Economics. EU Carbon Permits. 2022. Available online: https://tradingeconomics.com/commodity/carbon (accessed on 18 August 2022).

- Lipiäinen, S.; Kuparinen, K.; Sermyagina, E.; Vakkilainen, E. Pulp and paper industry in energy transition: Towards energy-efficient and low carbon operation in Finland and Sweden. Sustain. Prod. Consum. 2021, 29, 421–431. [Google Scholar] [CrossRef]

- Kähkönen, S.; Vakkilainen, E.; Laukkanen, T. Impact of structural changes on energy efficiency of Finnish pulp and paper industry. Energies 2019, 12, 3689. [Google Scholar] [CrossRef]

- Kuparinen, K.; Lipiäinen, S.; Vakkilainen, E.; Laukkanen, T. Effect of biomass-based carbon capture on the sustainability and economics of pulp and paper production in the Nordic mills. Environ. Dev. Sustain. 2021, 23, 13707–13730. [Google Scholar] [CrossRef]

- Food and Agriculture Organization of the United Nations (FAO). Forestry Production and Trade. 2022. Available online: http://www.fao.org/faostat/en/#data/FO (accessed on 21 January 2022).

- Farla, J.; Blok, K.; Schipper, L. Energy efficiency developments in the pulp and paper industry: A cross-country comparison using physical production data. Energy Policy 1997, 25, 745–758. [Google Scholar] [CrossRef]

- Regional State Administrative Agency Environmental Permits. 2022. Available online: https://avi.fi/en/services/businesses/licence-notices-and-applications/water-and-the-environment/environmental-permits (accessed on 7 October 2022).

- Vakkilainen, E.; Kivistö, A. Fossil Fuel Replacement in the Pulp Mills, LUT University. 2008. Available online: https://lutpub.lut.fi/bitstream/handle/10024/149415/BSMax_Report_Final4.pdf?sequence=1 (accessed on 20 December 2022).

- Lipiäinen, S.; Kuparinen, K.; Vakkilainen, E. Effect of polysulfide pulping process on the energy balance of softwood and hardwood kraft pulp mills. Nord. Pulp Pap. Res. J. 2021, 36, 570–581. [Google Scholar] [CrossRef]

- Statistics Finland. Fuel Classification. 2022. Available online: https://www.stat.fi/tup/khkinv/khkaasut_polttoaineluokitus.html (accessed on 11 February 2022).

- United States Environmental Protection Agency (EPA). GHGRP Pulp and Paper. 2021. Available online: https://www.epa.gov/ghgreporting/ghgrp-pulp-and-paper#2019-subsector (accessed on 5 April 2022).

- Government of Canada. Industrial GHG Emissions by Industry–Including Electricity-Related Emissions. 2020. Available online: https://oee.nrcan.gc.ca/corporate/statistics/neud/dpa/showTable.cfm?type=HB§or=agg&juris=00&rn=3&page=3 (accessed on 5 April 2022).

- Fisher, R. Carbon Emissions in the Pulp and Paper Industry. 2013. Available online: https://www.tappi.org/content/enewsletters/ahead/2013/issues/2013-09-18.html (accessed on 5 April 2022).

- Man, Y.; Li, J.; Hong, M.; Han, Y. Energy transition for the low-carbon pulp and paper industry in China. Renew. Sustain. Energy Rev. 2020, 131, 109998. [Google Scholar] [CrossRef]

- Yang, F.; Meerman, J.C.; Faaij, A.P.C. Carbon capture and biomass in industry: A techno-economic analysis and comparison of negative emission options. Renew. Sustain. Energy Rev. 2021, 144, 111028. [Google Scholar] [CrossRef]

- Miner, R.; Upton, B. Methods for estimating greenhouse gas emissions from lime kilns at kraft pulp mills. Energy 2002, 27, 729–738. [Google Scholar] [CrossRef]

- European Environment Agency (EEA). Bubble Policy (Emissions Trading). 2022. Available online: https://www.eea.europa.eu/help/glossary/gemet-environmental-thesaurus/bubble-policy-emissions-trading (accessed on 20 April 2022).

- RISI. Direct Manufacturing Cost Structure of the European Pulp & Paper Industry in 2017; 4th Quarter; RISI: Boston, MA, USA, 2017. [Google Scholar]

- European Commission. EU Biodiversity Strategy for 2030: Bringing Nature Back into our Lives. 2002. Available online: https://op.europa.eu/en/publication-detail/-/publication/31e4609f-b91e-11eb-8aca-01aa75ed71a1 (accessed on 16 August 2022).

- European Paper Recycling Council (EPRC). European Declaration on Paper Recycling 2021–2030. 2022. Available online: https://www.cepi.org/press-release-the-paper-value-chain-is-ready-to-take-circularity-to-a-new-level-with-2030-recycling-rate-target-%EF%BF%BC/ (accessed on 16 August 2022).

- UPM Biochemicals Building a State-of-the-Art Biorefinery in Leuna. 2022. Available online: https://www.upmbiochemicals.com/about-upm-biochemicals/biorefinery-leuna/ (accessed on 15 December 2022).

- Worrell, E.; Bernstein, L.; Roy, J.; Price, L.; Harnisch, J. Industrial energy efficiency and climate change mitigation. Energy Effic. 2009, 2, 109–123. [Google Scholar] [CrossRef]

- Moya, J.A.; Pavel, C.C. Energy Efficiency and GHG Emissions: Prospective Scenarios for the Pulp and Paper Industry; Publications Office of the European Union: Luxembourg, 2018; Available online: https://publications.jrc.ec.europa.eu/repository/handle/JRC111652 (accessed on 15 February 2022).

- Confederation of European Paper Industries (CEPI). Investing in Europe for Industry Transformation: 2050 Roadmap to a Low-Carbon Bioeconomy. 2017. Available online: https://www.cepi.org/investing-in-europe-for-industry-transformation-2050-roadmap-to-a-low-carbon-bioeconomy/ (accessed on 16 August 2022).

- Confederation of European Paper Industries (CEPI). Two Team Project; Confederation of European Paper Industries (CEPI): Brussels, Belgium, 2013. [Google Scholar]

- Carlson, E.; Heikkinen, P. Energian Käyttö Suomen Massa—Ja Paperiteollisuudessa, Ostosähkön Hintavertailu Eräissä Euroopan Maissa; Energy Usage in Finnish Pulp and Paper Industry, Comparison of Electricity Prices in Certain European Countries; Oy Keskuslaboratorio: Espoo, Finland, 1998. (In Finnish) [Google Scholar]

- Pöyry. Suomen Metsäteollisuus 2015–2035; The Finnish Forest Industry 2015–2035; Pöyry: Helsinki, Finland, 2016. [Google Scholar]

- Stenqvist, C. Industrial Energy Efficiency Improvement: The Role of Policy and Evaluation. Ph.D. Thesis, Lund University, Lund, Sweden, 2013. [Google Scholar]

- Thollander, P.; Ottosson, M. An energy efficient Swedish pulp and paper industry—Exploring barriers to and driving forces for cost-effective energy efficiency investments. Energy Effic. 2008, 1, 21–34. [Google Scholar] [CrossRef]

- Ericsson, K.; Nilsson, L.J. Climate Innovations in the Paper Industry: Prospects for Decarbonization. 2018. Available online: https://portal.research.lu.se/en/publications/climate-innovations-in-the-paper-industry-prospects-for-decarboni (accessed on 16 August 2022).

- International Renewable Energy Agency (IRENA). Bioenergy from Finnish Forests: Sustainable, Efficient and Modern Use of Wood. 2018. Available online: https://www.irena.org/publications/2018/mar/bioenergy-from-finnish-forests (accessed on 14 April 2022).

- Confederation of European Paper Industries (CEPI). The Forest Fibre Industry. 2011. Available online: https://www.cepi.org/the-forest-fibre-industry-2050-roadmap-to-a-low-carbon-bio-economy/ (accessed on 16 August 2022).

- FuelCellsWorks. German Paper Mill Manufacturer Relying on Hydrogen. 2022. Available online: https://fuelcellsworks.com/news/german-paper-mill-manufacturer-relying-on-hydrogen/ (accessed on 18 December 2022).

- Svensson, E.; Wiertzema, H.; Harvey, S. Potential for negative emissions by carbon capture and storage from a novel electric plasma calcination process for pulp and paper mills. Front. Clim. 2021, 3, 129. [Google Scholar] [CrossRef]

- Francey, S.; Tran, H.; Jones, A. Current status of alternative fuel use in lime kilns. Tappi J. 2009, 8, 33–39. [Google Scholar]

- Obrist, M.D.; Kannan, R.; Schmidt, T.J.; Kober, T. Long-term energy efficiency and decarbonization trajectories for the Swiss pulp and paper industry. Sustain. Energy Technol. Assess. 2022, 52, 101937. [Google Scholar] [CrossRef]

- Vakkilainen, E.; Kaikko, J.; Hamaguchi, M. Once-Through and Reheater Recovery Boiler–Concept Studies; LUT University Research Report: Lappeenranta, Finland, 2010. [Google Scholar]

- Ericsson, K.; Nilsson, L.J.; Nilsson, M. New energy strategies in the Swedish pulp and paper industry-The role of national and EU climate and energy policies. Energy Policy 2011, 39, 1439–1449. [Google Scholar] [CrossRef]

- Valmet. XXL Size Recovery Boilers–Present Status and Future Prospects. 2017. Available online: https://www.valmet.com/media/articles/up-and-running/new-technology/VPXXLRB/ (accessed on 14 April 2022).

- European Environment Agency (EEA). CO2 Emission Intensity. 2020. Available online: https://www.eea.europa.eu/data-and-maps/daviz/co2-emission-intensity-5 (accessed on 20 April 2022).

- Hamaguchi, M.; Vakkilainen, E.; Ryder, P. The impact of lignin removal on the dimensioning of eucalyptus pulp mills. Appita J. 2011, 64, 433–439. [Google Scholar]

- Palgan, Y.V.; Mccormick, K. Biorefineries in Sweden: Perspectives on the opportunities, challenges and future. Biofuels Bioprod. Bioref. 2016, 10, 523–533. [Google Scholar] [CrossRef]

- International Energy Agency (IEA). Net Zero by 2050—A Roadmap for the Global Energy Sector. 2021. Available online: https://www.iea.org/reports/net-zero-by-2050 (accessed on 23 February 2022).

- Möllersten, K.; Gao, L.; Yan, J.; Obersteiner, M. Efficient energy systems with CO2 capture and storage from renewable biomass in pulp and paper mills. Renew. Energy 2004, 29, 1583–1598. [Google Scholar] [CrossRef]

- Jönsson, J.; Berntsson, T. Analysing the potential for implementation of CCS within the European pulp and paper industry. Energy 2012, 44, 641–648. [Google Scholar] [CrossRef]

- Onarheim, K.; Santos, S.; Kangas, P.; Hankalin, V. Performance and cost of CCS in the pulp and paper industry part 2: Economic feasibility of amine-based post-combustion CO2 capture. Int. J. Greenh. Gas Control 2017, 66, 60–75. [Google Scholar] [CrossRef]

- Leeson, D.; Mac Dowell, N.; Shah, N.; Petit, C.; Fennell, P.S. A Techno-economic analysis and systematic review of carbon capture and storage (CCS) applied to the iron and steel, cement, oil refining and pulp and paper industries, as well as other high purity sources. Int. J. Greenh. Gas Control 2017, 61, 71–84. [Google Scholar] [CrossRef]

- Kuparinen, K.; Vakkilainen, E.; Tynjälä, T. Biomass-based carbon capture and utilization in kraft pulp mills. Mitig. Adapt. Strateg. Glob. Chang. 2019, 24, 1213–1230. [Google Scholar] [CrossRef]

- Onarheim, K.; Garðarsdòttir, S.; Mathisen, A.; Nord, L.; Berstad, D. Industrial Implementation of Carbon Capture in Nordic Industry Sectors. 2015. Available online: https://www.sintef.no/en/publications/publication/1308897/ (accessed on 12 March 2022).

- Hektor, E.; Berntsson, T. Future CO2 removal from pulp mills–Process integration consequences. Energy Convers. Manag. 2007, 48, 3025–3033. [Google Scholar] [CrossRef]

- Teir, S.; Tsupari, E.; Arasto, A.; Koljonen, T.; Kärki, J.; Lehtilä, A.; Kujanpää, L.; Aatos, S.; Nieminen, M. Prospects for application of CCS in Finland. Energy Procedia 2011, 4, 6174–6181. [Google Scholar] [CrossRef]

- McGrail, B.P.; Freeman, C.J.; Brown, C.F.; Sullivan, E.C.; White, S.K.; Reddy, S.; Garber, R.D.; Tobin, D.; Gilmartin, J.J.; Steffensen, E.J. Overcoming business model uncertainty in a carbon dioxide capture and sequestration project: Case study at the Boise White Paper Mill. Int. J. Greenh. Gas Control 2012, 9, 91–102. [Google Scholar] [CrossRef]

- Onarheim, K.; Mathisen, A.; Arasto, A. Barriers and opportunities for application of CCS in Nordic industry-A sectorial approach. Int. J. Greenh. Gas Control 2015, 36, 93–105. [Google Scholar] [CrossRef]

- Fridahl, M.; Lehtveer, M. Bioenergy with carbon capture and storage (BECCS): Global potential, investment preferences, and deployment barriers. Energy Res. Soc. Sci. 2018, 42, 155–165. [Google Scholar] [CrossRef]

- Santos, M.P.S.; Manovic, V.; Hanak, D.P. Unlocking the potential of pulp and paper industry to achieve carbon-negative emissions via calcium looping retrofit. J. Clean. Prod. 2021, 280, 124431. [Google Scholar] [CrossRef]

- Brynolf, S.; Taljegard, M.; Grahn, M.; Hansson, J. Electrofuels for the transport sector: A review of production costs. Renew. Sustain. Energy Rev. 2018, 81, 1887–1905. [Google Scholar] [CrossRef]

- Inkeri, E. Modelling of component dynamics and system integration in power-to-gas process, Lappeenranta-Lahti University of Technology LUT. 2021. Available online: https://lutpub.lut.fi/handle/10024/163488 (accessed on 14 April 2022).

- Armstrong, K.; Berger, A.H.; Hansson, J. The Potential for electrofuels Production in Sweden Utilizing Fossil and Biogenic CO2 Point sources. Front. Energy Res. 2017, 5, 1–12. [Google Scholar] [CrossRef]

- European Environment Agency (EEA). Final Energy Consumption in Europe by Mode of Transport. 2021. Available online: https://www.eea.europa.eu/data-and-maps/indicators/transport-final-energy-consumption-by-mode/assessment-10 (accessed on 11 March 2022).

- European Commission. Commission Delegated Regulation (EU) …/… of XXX Supplementing Directive (EU) 2018/2001 of the European Parliament and of the Council by Establishing a Union Methodology Setting Out Detailed Rules for the Production of Renewable Liquid and Gaseous Transport Fuels of Non-Biological Origin; European Commission: Brussels, Belgium, 2022. [Google Scholar]

- European Commission Directive (EU). 2018/2001 of the European Parliament and of the Council of 11 December 2018 on the Promotion of the Use of Energy from Renewable Sources. 2018. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=uriserv:OJ.L_.2018.328.01.0082.01.ENG (accessed on 16 August 2022).

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).