Carbon-Neutral Steel Production and Its Impact on the Economies of China, Japan, and Korea: A Simulation with E3ME-FTT:Steel

Abstract

:1. Introduction

1.1. Iron and Steelmaking Processes

1.2. Country Profile: China

1.3. Country Profile: Japan

1.4. Country Profile: Korea

2. Materials and Methods

2.1. E3ME

2.2. FTT:Steel

2.3. Learning by Doing

2.4. Baseline Scenario

2.5. Policy Scenarios

2.6. Scenario Assumptions

3. Results

3.1. Technology Diffusion

3.2. Environmental Impact

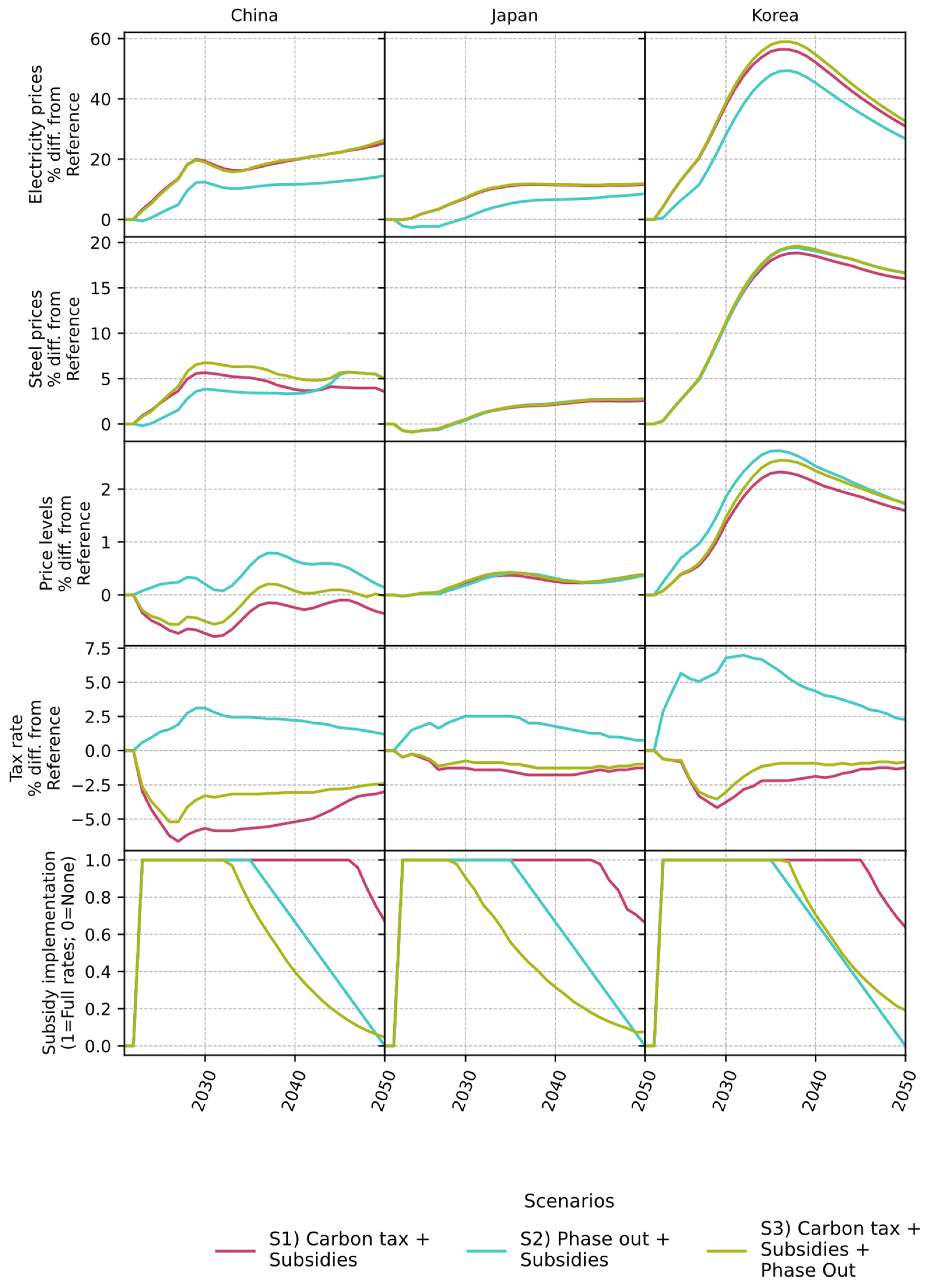

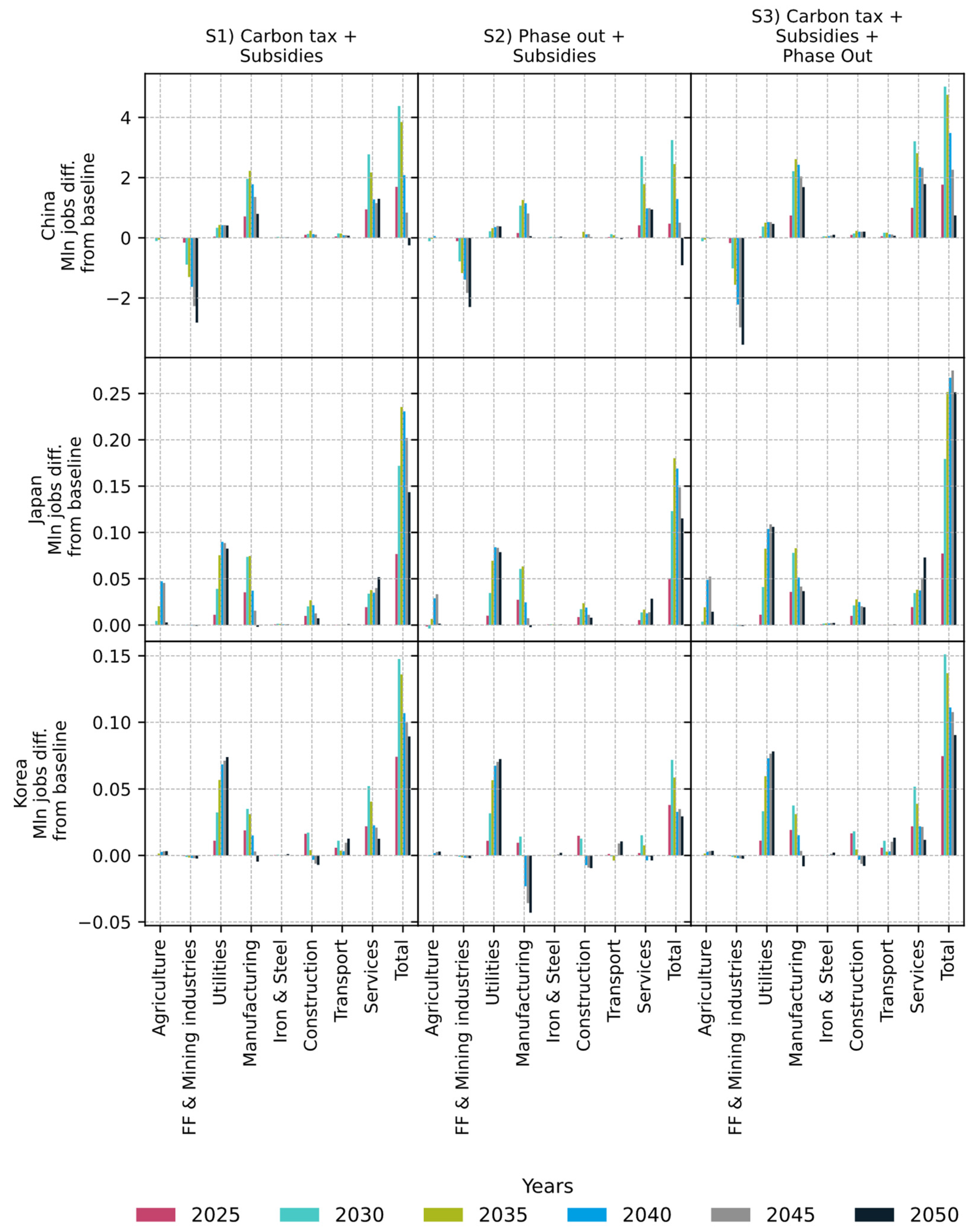

3.3. Economic Impact

4. Discussion

5. Conclusions

Supplementary Materials

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A. Mathematical Framework of E3ME-FTT:Steel

Appendix A.1. Investor Preferences

Appendix A.2. End-of-Lifetime Technology Substitution

Appendix A.3. Premature Technology Substitution

Appendix A.4. Innovator Effect

Appendix A.5. Market Share Dynamics

References

- Ministry of Economy Trade and Industry Technology Roadmap for “Transition Finance” in Iron and Steel Sector. Available online: https://www.meti.go.jp/policy/energy_environment/global_warming/transition/transition_finance_technology_roadmap_iron_and_steel_eng.pdf (accessed on 16 September 2022).

- Yin, R.; Liu, Z.; Shangguan, F. Thoughts on the Implementation Path to a Carbon Peak and Carbon Neutrality in China’s Steel Industry. Engineering 2021, 7, 1680–1683. [Google Scholar] [CrossRef]

- Korea Institute for Industrial Economics & Trade. Strategies and Policy Tasks for Carbon Neutralization in the Steel Industry. 2022. Available online: https://www.kiet.re.kr/research/paperView?paper_no=774&skey=&sval= (accessed on 16 September 2022).

- Zhu, Z. Iron and Steel Technology Roadmap; International Energy Agency: Paris, France, 2022. [Google Scholar]

- Xylia, M.; Silveira, S.; Duerinck, J.; Meinke-Hubeny, F. Weighing Regional Scrap Availability in Global Pathways for Steel Production Processes. Energy Effic. 2018, 11, 1135–1159. [Google Scholar] [CrossRef] [Green Version]

- Morfeldt, J.; Nijs, W.; Silveira, S. The Impact of Climate Targets on Future Steel Production—An Analysis Based on a Global Energy System Model. J. Clean. Prod. 2015, 103, 469–482. [Google Scholar] [CrossRef]

- Vaughan, A. Most Major Carbon Capture and Storage Projects Haven’t Met Targets. Available online: https://www.newscientist.com/article/2336018-most-major-carbon-capture-and-storage-projects-havent-met-targets/ (accessed on 23 May 2023).

- Reiner, D.M. Learning through a Portfolio of Carbon Capture and Storage Demonstration Projects. Nat. Energy 2016, 1, 15011. [Google Scholar] [CrossRef] [Green Version]

- Hauser, A.; Wolf-Zoellner, P.; Haag, S.; Dettori, S.; Tang, X.; Mighani, M.; Matino, I.; Mocci, C.; Colla, V.; Kolb, S.; et al. Valorizing Steelworks Gases by Coupling Novel Methane and Methanol Synthesis Reactors with an Economic Hybrid Model Predictive Controller. Metals 2022, 12, 1023. [Google Scholar] [CrossRef]

- International Energy Agency. Energy Technology Perspectives 2023; International Energy Agency: Paris, France, 2023. [Google Scholar]

- Intergovernmental Panel on Climate Change. Mitigation of Climate Change Climate Change 2022 Working Group III Contribution to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change; Intergovernmental Panel on Climate Change: Geneva, Switzerland, 2022; ISBN 9789291691609. [Google Scholar]

- Gielen, D.; Saygin, D.; Taibi, E.; Birat, J.-P. Renewables-Based Decarbonization and Relocation of Iron and Steel Making: A Case Study. J. Ind. Ecol. 2020, 24, 1113–1125. [Google Scholar] [CrossRef]

- Ren, L.; Zhou, S.; Peng, T.; Ou, X. A Review of CO2 Emissions Reduction Technologies and Low-Carbon Development in the Iron and Steel Industry Focusing on China. Renew. Sustain. Energy Rev. 2021, 143, 110846. [Google Scholar] [CrossRef]

- Muslemani, H.; Liang, X.; Kaesehage, K.; Ascui, F.; Wilson, J. Opportunities and Challenges for Decarbonizing Steel Production by Creating Markets for ‘Green Steel’ Products. J. Clean. Prod. 2021, 315, 128127. [Google Scholar] [CrossRef]

- Kushnir, D.; Hansen, T.; Vogl, V.; Åhman, M. Adopting Hydrogen Direct Reduction for the Swedish Steel Industry: A Technological Innovation System (TIS) Study. J. Clean. Prod. 2020, 242, 118185. [Google Scholar] [CrossRef]

- International Energy Agency. Hydrogen Projects Database. Available online: https://www.iea.org/data-and-statistics/data-product/hydrogen-projects-database#license (accessed on 27 January 2023).

- Kim, J.; Sovacool, B.K.; Bazilian, M.; Griffiths, S.; Lee, J.; Yang, M.; Lee, J. Decarbonizing the Iron and Steel Industry: A Systematic Review of Sociotechnical Systems, Technological Innovations, and Policy Options. Energy Res. Soc. Sci. 2022, 89, 102565. [Google Scholar] [CrossRef]

- Li, Z.; Dai, H.; Song, J.; Sun, L.; Geng, Y.; Lu, K.; Hanaoka, T. Assessment of the Carbon Emissions Reduction Potential of China’s Iron and Steel Industry Based on a Simulation Analysis. Energy 2019, 183, 279–290. [Google Scholar] [CrossRef]

- Ji Chen, A.; Li, S.; Li, X.; Li, Y.; Chen, J. Pursuing Zero-Carbon Steel in China A Critical Pillar to Reach Carbon Neutrality; RMI: Beijing, China, 2021. [Google Scholar]

- Van Ruijven, B.J.; Van Vuuren, D.P.; Boskaljon, W.; Neelis, M.L.; Saygin, D.; Patel, M.K. Long-Term Model-Based Projections of Energy Use and CO2 Emissions from the Global Steel and Cement Industries. Resour. Conserv. Recycl. 2016, 112, 15–36. [Google Scholar] [CrossRef] [Green Version]

- Korea Advanced Institute of Science and Technology. Steel Sector Pathways for Korea’s 2050 Carbon Neutrality. 2022. Available online: https://forourclimate.org/en/sub/data/view.htmlidx40 (accessed on 10 April 2023).

- Mercure, J.-F.; Pollitt, H.; Edwards, N.R.; Holden, P.B.; Chewpreecha, U.; Salas, P.; Lam, A.; Knobloch, F.; Vinuales, J.E. Environmental Impact Assessment for Climate Change Policy with the Simulation-Based Integrated Assessment Model E3ME-FTT-GENIE. Energy Strategy Rev. 2018, 20, 195–208. [Google Scholar] [CrossRef]

- Dwesar, I.; Kőműves, Z.; McGovern, M.; Vu, A.; Arsenio, F.; Heald, S.; Chewpreecha, U.; Pollitt, H. E3ME Model Manual; Cambridge Econometrics: Cambridge, UK, 2022. [Google Scholar]

- World Steel Association World Steel in Figures 2022. Available online: https://worldsteel.org/steel-topics/statistics/world-steel-in-figures-2022/#world-crude-steel-production-1950-to-2021 (accessed on 2 February 2023).

- Nikkei Asia China’s Steelmakers Get 5 More Years to Reach Peak Carbon Output. Available online: https://asia.nikkei.com/Spotlight/Caixin/China-s-steelmakers-get-5-more-years-to-reach-peak-carbon-output (accessed on 30 September 2022).

- Institute for Energy Economics and Financial Analysis China’s Peak Steel Emissions Shift Unlikely to Delay Carbon Reductions. Available online: https://ieefa.org/resources/ieefa-chinas-peak-steel-emissions-shift-unlikely-delay-carbon-reductions (accessed on 20 September 2022).

- Global Times China Counts on New Technology to Decarbonize Steel Production. Available online: https://www.globaltimes.cn/page/202203/1257298.shtml (accessed on 20 September 2022).

- China Iron and Steel Association Industry Yearbook. Available online: http://english.chinaisa.org.cn/do/cn.org.chinaisa.view.Column.d?column=3 (accessed on 12 November 2022).

- Nakano, J. China Unveils Its First Long-Term Hydrogen Plan. Available online: https://www.csis.org/analysis/china-unveils-its-first-long-term-hydrogen-plan (accessed on 27 September 2022).

- State Council The People’s Republic of China China’s Steel Sector Aims for High-Quality Growth. Available online: https://english.www.gov.cn/statecouncil/ministries/202202/07/content_WS620112a6c6d09c94e48a4cd4.html (accessed on 20 September 2022).

- The Japan Iron & Steel Federation. JISF Long-Term Vision for Climate Change Mitigation: A Challenge towards Zero-Carbon Steel; The Japan Iron & Steel Federation: Tokyo, Japan, 2019. [Google Scholar]

- Vercoulen, P.; Lee, S.; Suk, S.; He, Y.; Fujikawa, K.; Mercure, J.-F. Policies to Decarbonize the Steel Industry in East Asia. In Energy, Environmental and Economic Sustainability in East Asia: Policies and Institutional Reforms; Lee, S., Pollitt, H., Fujikawa, K., Eds.; Routledge: London, UK, 2019; ISBN 9781351013468. [Google Scholar]

- Korea Iron and Steel Association Korean Steel Market. Proceedings of the 86th Session of the Steel Committee, 25–26 March 2019; Available online: https://www.oecd.org/sti/ind/86th%20Steel%20Committee%20meeting%20%20Presentation%20by%20KISA,%20Korean%20Steel%20Market.pdf (accessed on 6 November 2022).

- POSCO GROUP 2050 Carbon Neutrality Declaration. Available online: https://www.posco.co.kr/brochure/en/02_Vision_05.html (accessed on 20 February 2023).

- Stangarone, T. South Korea’s Hydrogen Industrial Strategy. Clean Technol Env. Policy 2021, 23, 509–516. [Google Scholar] [CrossRef] [PubMed]

- Cha, B.; Green, R. Korean Hydrogen Market Update; Australian Trade and Investment Commission: Sydney, Australia, 2022. [Google Scholar]

- Li, T.Y. Korea Unveils Steel Plan, Eyes Low-Carbon Project Fund|Argus Media. Available online: https://www.argusmedia.com/en/news/2421608-korea-unveils-steel-plan-eyes-lowcarbon-project-fund (accessed on 23 April 2023).

- Pollitt, H.; Mercure, J.-F. The Role of Money and the Financial Sector in Energy-Economy Models Used for Assessing Climate and Energy Policy. Clim. Policy 2018, 18, 184–197. [Google Scholar] [CrossRef] [Green Version]

- Mercure, J.-F. FTT:Power: A Global Model of the Power Sector with Induced Technological Change and Natural Resource Depletion. Energy Policy 2012, 48, 799–811. [Google Scholar] [CrossRef] [Green Version]

- Mercure, J.-F.; Lam, A. The Effectiveness of Policy on Consumer Choices for Private Road Passenger Transport Emissions Reductions in Six Major Economies. Environ. Res. Lett. 2015, 10, 064008. [Google Scholar] [CrossRef]

- Knobloch, F.; Pollitt, H.; Chewpreecha, U.; Lewney, R.; Huijbregts, M.A.J.; Mercure, J.F. FTT:Heat—A Simulation Model for Technological Change in the European Residential Heating Sector. Energy Policy 2021, 153, 112249. [Google Scholar] [CrossRef]

- Mercure, J.-F. An Age Structured Demographic Theory of Technological Change. J. Evol. Econ. 2015, 25, 787–820. [Google Scholar] [CrossRef] [Green Version]

- Pauliuk, S.; Milford, R.L.; Müller, D.B.; Allwood, J.M. The Steel Scrap Age. Environ. Sci. Technol. 2013, 47, 3448–3454. [Google Scholar] [CrossRef] [Green Version]

- Karali, N.; Park, Y.; Mcneil, M.A. Using Learning Curves on Energy-Efficient Technologies to Estimate Future Energy Savings and Emission Reduction Potentials in the U.S. Iron and Steel Industry; International Energy Studies Group, Energy Analysis and Environmental Impacts Division, Berkeley National Laboratory: Berkeley, CA, USA, 2015. [Google Scholar]

- Saba, S.M.; Müller, M.; Robinius, M.; Stolten, D. The Investment Costs of Electrolysis—A Comparison of Cost Studies from the Past 30 Years. Int. J. Hydrog. Energy 2018, 43, 1209–1223. [Google Scholar] [CrossRef]

- Schoots, K.; Ferioli, F.; Kramer, G.J.; van der Zwaan, B.C.C. Learning Curves for Hydrogen Production Technology: An Assessment of Observed Cost Reductions. Int. J. Hydrog. Energy 2008, 33, 2630–2645. [Google Scholar] [CrossRef]

- Lee, S.; He, Y.; Suk, S.; Morotomi, T.; Chewpreecha, U. Impact on the Power Mix and Economy of Japan under a 2050 Carbon-Neutral Scenario: Analysis Using the E3ME Macro-Econometric Model. Clim. Policy 2022, 22, 823–833. [Google Scholar] [CrossRef]

- Vercoulen, P.; Markkanen, S. Technology, Employment, and Climate Change Mitigation: Modelling the Iron and Steel Industry. Technical Report; The University of Cambridge Institute for Sustainability Leadership (CISL): Cambridge, UK, 2020. [Google Scholar]

- Odenweller, A.; Ueckerdt, F.; Nemet, G.F.; Jensterle, M.; Luderer, G. Probabilistic Feasibility Space of Scaling up Green Hydrogen Supply. Nat. Energy 2022, 7, 854–865. [Google Scholar] [CrossRef]

- Wang, P.; Ryberg, M.; Yang, Y.; Feng, K.; Kara, S.; Hauschild, M.; Chen, W.-Q. Efficiency Stagnation in Global Steel Production Urges Joint Supply- and Demand-Side Mitigation Efforts. Nat. Commun. 2021, 12, 2066. [Google Scholar] [CrossRef]

- Allwood, J.M.; Ashby, M.F.; Gutowski, T.G.; Worrell, E. Material Efficiency: A White Paper. Resour. Conserv. Recycl. 2011, 55, 362–381. [Google Scholar] [CrossRef]

- International Energy Agency. Iron and Steel Technology: Roadmap Towards More Sustainable Steelmaking; International Energy Agency: Paris, France, 2020. [Google Scholar]

- Bass, F.M. A New Product Growth for Model Consumer Durables. Manag. Sci. 1969, 15, 215–227. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Steelmaking Pathway | Assumed Learning Rate | Comment |

|---|---|---|

| BF–BOF | 3% | Mature |

| CCS applications | 6–8% | Configuration is not very different from BF–BOF. |

| DR–gas/coal | 3% | In the commercialization phase (mainly in regions other than China, Korea, and Japan). |

| SR–BOF | 4% | In the commercialization phase. Configuration is somewhat similar to BF–BOF. |

| Advanced SR–BOF | 6% | Early phase of commercialization. Configuration is somewhat similar to BF–BOF. Increased learning rate due to the early phase of commercialization. |

| DR–H2–EAF | 12% | Novel; being developed in Sweden. Similar to DR–gas–EAF, but higher learning rate due to electrolysis. |

| Electrolysis | 15% | In the research phase; a higher learning rate is assumed. |

| Scrap–EAF | 3% | Mature. |

| Policy | Description |

|---|---|

| Subsidies | On upfront investment: 35% on all CCS applications, 30% on all bio-based applications, 80% on hydrogen-based direct reduction, 50% on electrolysis, and 35% on scrap recycling. Energy rebates: 50% on hydrogen and 10% on electricity. All subsidies are implemented from 2023. Where applicable, subsidies are adjusted so that the total subsidy costs do not exceed the carbon tax revenues generated by the ISI. If no carbon tax regime is implemented, the subsidies are linearly phased out between 2035 and 2050. |

| Phase-out regulations | No additional capacity can be added to carbon-intensive processes from 2025 onwards. Capacity declines in line with the natural depreciation rate proportional to the inverse of the lifetime. For BF–BOF, that would be 1/35. |

| Carbon tax | Starting at 10 USD/tCO2 in 2023 and increasing to 140 USD2020/tCO2 in 2050. The carbon tax is targeted at all industries. |

| Emission trading scheme | In Korea, an emission trading scheme has been in place since 2015. The rate is an exogenous input and increases from 21 USD/tCO2 in 2023 to 98 USD/tCO2 in 2050. China implemented an ETS in 2021 and the rate grows from 14 USD/tCO2 in 2023 to 92 USD/tCO2 in 2050. Japan has a voluntary ETS since 2006. This will likely change in 2026. The ETS price is set at 16 USD/tCO2 in 2026, increasing to 75 USD/tCO2 in 2050. |

| Financialization of policy costs via carbon tax revenues | The policy costs due to the subsidies applied to the ISI are financed through carbon tax revenues generated by a tax on the ISI. Therefore, the transition to low-carbon alternatives is financed through carbon-intensive processes. If carbon tax revenues are not sufficient to fully cover the maximum subsidy rates, then the subsidies rates are lowered. Alternatively, if the carbon tax revenues are greater than the policy costs, then the overshoot is used to lower other fiscal rates, which follows the same mechanism as below. Note: ETS revenues are not used to finance policy costs. |

| Financialization of policy costs via other fiscal rates | The policy costs are financed by raising other non-environmental fiscal rates, such as the VAT rate, income tax, and employers’ social security contributions. VAT rates increase the end-use prices of goods and services and thereby decrease disposable income in real terms. Higher income tax makes employment more costly and therefore lowers employment. However, this may lead to higher capital investment as employers’ focus shifts from employees to capital. Raising employers’ social security contributions increases the cost of employment, but also leads to additional benefits. |

| Scenarios | Subsidies | Phase-Out Regulations | Carbon Tax on All Industries | Financialization of Policy Costs via Carbon Tax Revenues from the ISI | Decarbonization Policies for the Power Sector | |

|---|---|---|---|---|---|---|

| S1 | Carbon tax + subsidies | Y | N | Y | Y | N |

| S2 | Subsidies + phase-out regulations | Y | Y | N | N | Y |

| S3 | Carbon tax + subsidies + phase-out regulations | Y | Y | Y | Y | N |

| Policy | Details |

|---|---|

| Subsidies on upfront investment | A 20% rate of upfront investment applied to nuclear power from 2023 and 2030, and a 50% rate of upfront investment applied to all CCS applications from 2023 to 2035. |

| Feed-in tariffs | Applied to onshore and offshore wind power and bio-based electricity generation from 2023 to 2035. |

| Kick-start program | Government programs to kick-start bioenergy with CCS (BECCS) between 2023 and 2026. |

| Phase-out regulations | All carbon-intensive power generation technologies from 2025 and onwards. |

| S1 | S2 | S3 | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Direct | Indirect | Total | Direct | Indirect | Total | Direct | Indirect | Total | |

| China | −33% | −73% | −38% | −52% | −72% | −54% | −91% | −77% | −90% |

| Japan | −21% | −83% | −35% | −56% | −81% | −61% | −85% | −89% | −86% |

| Korea | −65% | −87% | −72% | −82% | −89% | −84% | −88% | −101% | −91% |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Vercoulen, P.; Lee, S.; Han, X.; Zhang, W.; Cho, Y.; Pang, J. Carbon-Neutral Steel Production and Its Impact on the Economies of China, Japan, and Korea: A Simulation with E3ME-FTT:Steel. Energies 2023, 16, 4498. https://doi.org/10.3390/en16114498

Vercoulen P, Lee S, Han X, Zhang W, Cho Y, Pang J. Carbon-Neutral Steel Production and Its Impact on the Economies of China, Japan, and Korea: A Simulation with E3ME-FTT:Steel. Energies. 2023; 16(11):4498. https://doi.org/10.3390/en16114498

Chicago/Turabian StyleVercoulen, Pim, Soocheol Lee, Xu Han, Wendan Zhang, Yongsung Cho, and Jun Pang. 2023. "Carbon-Neutral Steel Production and Its Impact on the Economies of China, Japan, and Korea: A Simulation with E3ME-FTT:Steel" Energies 16, no. 11: 4498. https://doi.org/10.3390/en16114498

APA StyleVercoulen, P., Lee, S., Han, X., Zhang, W., Cho, Y., & Pang, J. (2023). Carbon-Neutral Steel Production and Its Impact on the Economies of China, Japan, and Korea: A Simulation with E3ME-FTT:Steel. Energies, 16(11), 4498. https://doi.org/10.3390/en16114498