Identification of Gaps and Barriers in Regulations, Standards, and Network Codes to Energy Citizen Participation in the Energy Transition

, , ,

, , ,

Abstract

:1. Introduction

2. Literature Review

2.1. Energy Efficiency

2.2. Demand Response

2.3. Local Energy Markets

2.4. Smart Meters and Technical Issues

2.5. Taxation

3. Possible Barriers to Accomplishing Enablers of Energy Citizens in Energy Transition

3.1. Barriers to Citizens’ Energy Efficiency Improvement

- 1-1

- Complexity of associated renovation and lack of skills in the supply chain of renovation works. This indicates the necessity of sharing the information and experience gained in accomplishing successful renovation projects.

- 1-2

- Quality of renovation. Sometimes renovations are cosmetic fixes only. The lack of monitoring bodies that enforce building energy efficiency certification can be an important barrier in this regard. The citizens’ awareness about certification should also be improved.

- 1-3

- Institutional and legal frameworks that slow down renovation projects. An example is the resistance of groups involved in urban decision-making, as they believe this may distort the buildings’ view (an RCS conflict barrier).

- 1-4

- Lack of access to finance while renovation costs are high. Renovations are often resource-intensive, both in terms of financing and time. Sometimes, the energy performance improvement achieves less value than the required investment costs. Discrepancies between predicted and actual savings also reduce the citizens’ trust in energy efficiency projects. Therefore, it is important to provide a clear picture of the cost and saving for citizens. Financial incentives are weak and external risks such as price volatility give rise to the lack of citizens’ motives.

- 1-5

- Lack of standards delineating the minimum level of renovation in different classes of buildings. A “deep renovation” standard in the Energy Performance of Buildings Directive (EPBD) is vital for more highly energy-efficient renovations. The Commission “deep renovation” standard can be bolted onto the EPBD, which is promised to be updated later this year. National standards also need to be updated according to the EC EPBD. Currently, such national revisited standards do not exist in most European countries. An ongoing study, i.e., “Renovate2Recover” [16], is analyzing the progress of such standardization in the MSs.

- 1-6

- Split incentives, lack of communication between buyers and building constructors, and a fragmented real estate market [14]. An example is different and sometimes opposing interests of constructors and final building buyers. For instance, the constructor may favor low cost over the efficiency of the equipment. The construction and renovation industries and be overly conservative and rely on traditional methods or can oversize equipment. Building energy policies should be revisited to avoid such barriers.

- 1-7

- Barriers related to citizens’ behavior such as the lack of shared objectives among citizens, and inertia, e.g., aversion to change and lack of understanding about how renewable energy communities operate and share access to RES fairly.

- 1-8

- Lack of information and knowledge regarding energy efficiency and sustainable products. These barriers continue to be an important cause hindering energy efficiency. The citizens’ perception of high investments and long return times is an important issue that should be clarified for end-users.

3.2. Barriers to Sustainable Engagement of Citizens in Demand Response Programs and BEMSs

- 2-1

- Citizens’ unfamiliarity and mistrust

- -

- Unfamiliar technology/technical terms

- -

- Lack of transparency around what DR entails and whom DR benefits

- -

- Mistrust in community-based mechanisms

- 2-2

- Perceived loss of control and associated risk

- -

- Long-term time-varying pricing may hinder enrollment

- -

- Fear of loss of control of the citizens over their demands/tasks

- -

- Unpredictable short-term prices that may deter citizens’ persistence

- -

- The prices should be predictable, but variable enough to guarantee the earning

- -

- Lack of DR models that are understood by citizens and offer acceptable control

- 2-3

- Complexity and effort

- -

- Inconvenience and discomfort associated with demand shift

- -

- Low reimbursement compared to the underlying decrease in comfort level

- -

- Complexity and required effort of responding to time-varying prices

- -

- Unpredictability of the weather in Western European countries

- 2-4

- Need to install new equipment and technologies

- -

- High cost of such technologies

- -

- Space required

- -

- Disruption of services while installing the required equipment

- -

- Lack of trust in additional technology

- -

- Associated complexity and risk of failure of new technologies

- 2-5

- Insufficient wholesale price variation discourage engagement in dynamic pricing DR

- -

- Conflict with other conventional use cases that favor low variation in prices

- 2-6

- Energy and network tariff structure does not support demand shift in time

- -

- Lack of motivation to switch to e-mobility and the use of electrical heating

- 2-7

- Distribution System Operators (DSO) remuneration approach

- -

- Preferring wire solutions over non-wire solutions

- -

- Lack of policies for the gradual transition from old DSO remunerating models

- 2-8

- Necessity to give access to third-party actors

- -

- Low weight of the demand-side stakeholders in policymaking

- -

- Concerns about privacy and security

- 2-9

- Ambiguous or no definitions for rights for direct control of citizen’s loads

- -

- Since different entities might make use of customers’ load control for different purposes, there is a need to define certain rights and obligations which are applicable to the parties responsible for power balance.

- 2-10

- Policymaking barriers

- -

- Potentially higher weight of the supply-side stakeholders in decision-making

- 2-11

- Supply chain barriers

- -

- Old design of energy markets from a supply-side perspective

- 2-12

- Regulation interaction barriers

- -

- Conflicting objectives or priorities when devising supporting policies

- -

- Conflict between price variability to motivate price-based DR and the need to stabilize the prices and make them predictable for other consumers.

3.3. Barriers to Efficient Local Energy Markets

- -

- Expedite the energy transition

- -

- Better fit to current advancements

- -

- Encourage prosumers rather than consumers

- -

- Motivate citizens to participate in collective organization/electricity markets

- -

- Put demand-side flexibility as one of the main priorities

- -

- Prosumer: Consumes energy, produces energy and may provide flexibility. An example of such prosumers is the citizens that have PV panels on their roofs.

- -

- Facilitator: Facilitates implementation of DERs, RESs, RECs, CECs, and so on. In many energy communities, one of the reasons to establish such a community is to facilitate the uptake of RESs and other energy generators in their community by, for example, providing help with financing, awareness increasing, joint purchasing, and knowledge sharing.

- -

- Producer: Generates energy and feeds this energy into the electricity network. If RECs have invested in a collective generation project, such as a collective rooftop PV system or a wind park, they are taking the role of a producer.

- -

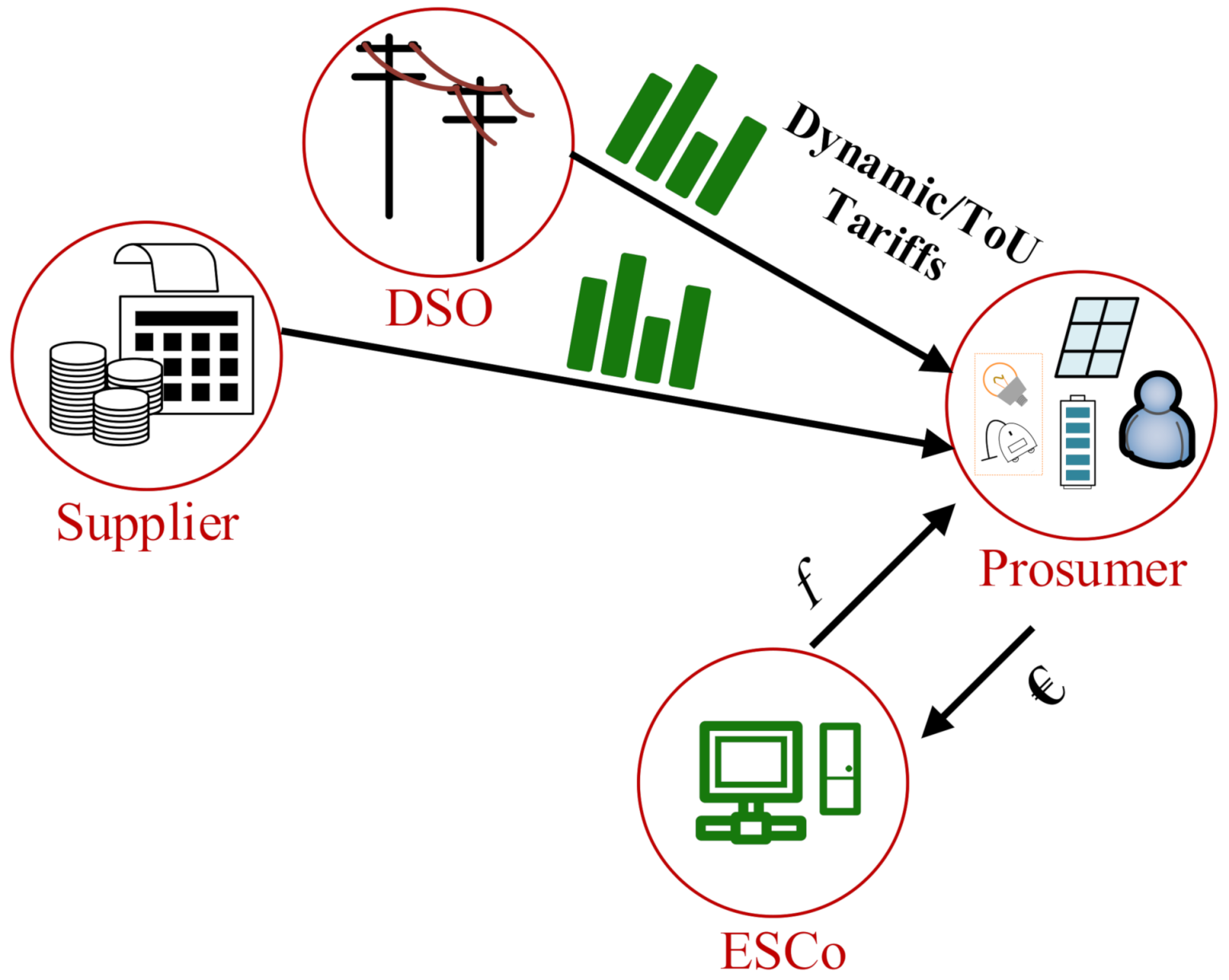

- Energy Service Companies (ESCos): Provide energy profile optimization tools and services. An example of such providers is a company that offers cloud-based building EMSs. An energy community might also be able to provide technologies/management systems that optimize energy profiles in response to varying external signals, e.g., energy or flexibility prices.

- -

- Aggregator: Pools and sells the flexibility that citizens and communities might be able to offer. An energy community itself can combine the flexibility of multiple households and together as a single “package” introduce the collative flexibility to the energy market and perhaps directly sell it to another party that may want to buy flexibility. Aggregators pool enough flexibility from multiple flexibility suppliers (who can be energy citizens or energy communities) to provide a worthwhile amount of flexibility to its users, such as distribution system operators (DSOs), transmission system operators (TSOs), and balance responsible parties (BRPs). The need for demand response aggregation and the aggregator role has been highlighted in the European CEP. This package also provides a series of directives defining such a role in electricity markets. Specifically, Directive 2019/944, Article 17 presents the new features of electricity market designs that deal with demand response through aggregation. This article requires all MSs to develop the necessary regulatory framework for (independent) aggregators and demand response to participate in energy and flexibility markets. In addition, article 32 seeks to motivate the use of the flexibility provided by the aggregators in distribution networks. It encourages the MSs to develop the essential regulatory framework to let the TSOs and DSOs deploy such flexibility to alleviate congestion (for adherence to both line power carrying limits and statutory voltage constraints) in their networks.

- -

- Supplier: Buys/sells the extra energy produced by citizens/communities. Note that an aggregator or the community itself might also take the role of a supplier.

- -

- DSO: Effectively manages the distribution systems at low- and medium-voltage (LV and MV) levels. DSO is generally responsible for regional grid stability and adherence to the power quality standards. In the futuristic scenarios for energy markets, energy communities might be permitted to operate their LV distribution (micro) grid. In the new generations of electricity markets, it has been proposed to regard the DSOs as fully independent bodies and even remove their technical role. Distribution network operators (DNOs) might take this role.

- -

- TSO: Actively manages transmission grid. TSO is regarded as responsible for system balance and adhering to the security and power quality standards at the HV level. The physical extent of TSO’s remit is most often large and beyond the capabilities of energy communities to fulfill. However, in the new setup of energy markets, TSOs are still attractive associates for aggregators/communities as the buyers of flexibility.

- -

- BRP: Manages and is responsible for the balance of demand and supply in its portfolio. This party is responsible for and manages a very large portfolio. Thus, it is interesting for energy communities to collaborate with.

- 3-1

- Financial risk due to the presence of giant investors: Even today, it seems that change is on the way. It is possible that new roles emerge or that the roles listed above are changed. All these changes are not happening in response to new national and EU policies. The industry is striving to get its share from the available opportunity to make a profit. New investors and companies with new specialties are getting interested in investing in the new structure of energy and flexibility provision in power systems. Not that the presence of new investments in the energy sector can necessarily be a challenge, the abovementioned point might distort the whole prospect. Some giant enterprises have started developing business models to take the place of the available organizations [35]. An example is Tesla, with a new “Energy Plan” to offer low electricity rates for citizens [35]. They plan to provide energy to households by rooftop PV systems and Powerwall VPP technology. In turn, it is sought that the households hand over the control of these resources to Tesla. They are targeting both energy and flexibility markets. An uncertain future affects citizens’ choices and the required design of future energy markets and related regulations.

- 3-2

- Complexity of measurement, validation, and baseline methodology: In remuneration of demand-side flexibility, a baseline is the value of demand/generation of flexibility providers before they change it based on the aggregator’s request. A baseline methodology is required to quantify the performance of flexibility service providers towards the customers of the flexibility. How to define appropriate baseline methodologies, roles, and responsibilities is an open question. Frameworks are needed for ensuring accurate and dependable data. It should be clear how to measure or calculate flexibility.

- 3-3

- Joint remuneration of price-based and incentive-based demand response: It is important to find a method to effectively separate the share of price-based and incentive-based demand response when a consumer/energy community changes its demand/generation. In many cases, a flexibility resource may be subject to both price-based and incentive-based demand response. To remunerate the providers, the impacts of the two forms should be separated unambiguously.

- 3-4

- Data confidentiality vs. transparency: A balance between transparency and confidentiality is hard to find. For efficient demand response, each participant in the new structure of the energy market needs some information from others. An example of this is aggregators who need demand, demand reduction capability, and demand reduction data to be able to accurately forecast the demand response, as well as for billing purposes. Nevertheless, some of this information might be commercially sensitive. Finding a balance between transparency and confidentiality is critical for deciding what information can be shared, as well as when and at what aggregation level this information is useful and can be passed to the respective bodies.

- 3-5

- Data security challenges: As discussed above, local energy markets involve dynamic gathering and transferring significant amounts of data. Much of such data is of a sensitive and confidential nature. Secure data handling and protection from cyber security threats in this context are the main concerns. The respective challenges should be dealt with by ensuring a clear definition of responsibilities and updating the data exchange systems of local energy markets.

- 3-6

- Technical responsibilities for nontechnical organizations: To best utilize demand-side flexibility, according to the CEP, aggregators are supposed to conflate the capabilities of a large group of households in a DR pool and join, as a single participant, in the electricity market. To this end, aggregators need to consider the operational constraints of the local LV grids, including the voltage statutory limits. Otherwise, the power quality might be jeopardized. Neglecting the technical limitations, DR potential might be overestimated. This could lead to instability of the market and power systems, as the aggregators are not able to alter their demand/production when called on to do so. Reference [26], as one of the early research papers on the subject, presented a method to deal with such an issue. This method coordinates the actions of the aggregators with DSO operations and assumes that there is another role as the DNO with the functionality of providing the results of state estimation and a set of sensitivity coefficients, using which the operational limits can be modeled. In practice, however, such an assumption does not hold. Some experts believe maintaining the power quality is not a task to be assigned to aggregators. However, if the aggregators benefit from demand-side flexibility, they should handle the power quality issues. The problem is that they do not have the technical knowledge and the required data. This is classified as a conflict barrier, as the DSOs do not willingly help the aggregators if they are not receiving monetary benefits. Regulatory policies need to be amended to remove this conflict.

- 3-7

- Technical limitations and fairness: Reference [26] assumes only one aggregator is in charge of pooling the demand-side resources in the LV feeder. In practice, however, many energy communities that can play the role of an aggregator might be available along with other aggregators. It is not clear which aggregators should share the task of solving the possible power quality issues and to what extent. In other words, there is no agreement on who is in charge of assuring the adherence to the statutory standards among the aggregators in an LV grid. There are other technical issues, such as voltage variations, high system peak levels, congestion and phase imbalances that are identified as the most common [36].

- 3-8

- Recognition of user characteristics for market-oriented DR: Even though price-based DR programs, e.g., critical peak pricing, dynamic pricing, and time of use pricing (for which the challenges and barriers were reviewed in Section 3.2), have been implemented for many years across the globe, market-oriented DR is still taking its early steps. Considering citizens’ intended tasks, their purposes, and electrical safety, demand-side aggregators have no right to regulate user loads, e.g., by forcing the power-producing users to change their production patterns. On the other hand, the ambiguity in the citizens’ manual load alteration might lead to the deviation of the amount of increase/decrease in the production or consumption from the level that has been promised by aggregators. For aggregators, this can be interpreted as the (partial) loss of revenue. The limited data on citizens’ demand response also puts the aggregators far away from the true recognition of citizens’ DR characteristics. This leads to flawed decision-making by aggregators.

- 3-9

- No distribution network operation role is allowed for energy communities: Currently, only industrial or commercial consumers can get exemptions regarding the operation of “closed distribution systems”. Domestic consumers and energy communities are not allowed to get such an exemption. In the future structure of the European energy markets, communities may be permitted to operate their community distribution network. Article 16 of the Electricity Directive should set the regulations to provide energy communities with a solid set of rights, involving an equal playing field and a right to build, keep, operate, and manage distribution networks or micro-grids or coordinately manage public distribution systems as well as ‘community networks’ (known as closed distribution systems, or microgrids). This right should not be discretionary. For this provision to be meaningful, it must be mandatory. On the other hand, the Parliament’s proposal to ensure compliance with national concession rules needs to be supported. However, the MSs should revisit the related regulations in their RCSs.

- 3-10

- Legal issues related to new specially designed grid for energy communities: Local energy systems might require new distribution infrastructure, e.g., to connect the consumers for collative consumption. Such grids might be expanded to private properties, which do not necessarily belong to community members or to publicly owned lands. This gives rise to legal issues that must be anticipated in policies [27]. Further on this subject, it can create conflicts of interest, when the new grid intersects available distribution network rights-of-way.

- 3-11

- Supplier license for sharing energy: Energy sharing within communities is very difficult to organize considering the current hindering legislations/Regulations. One reason is that each party that supplies energy is obliged to have a supplier license. It is sought that, in the futuristic scenarios for energy markets, energy sharing can be accomplished within a community.

- 3-12

- Taxation barriers: The taxation of electricity plays an important role in achieving the climate and energy targets. The rules set under the Directive 2003/96/EC, i.e., Energy Taxation Directive (ETD) aim at ensuring the proper implementation of the LEMs. However, since 2003, the climate and energy policies have been changed radically and ETD is no longer in line with EU policies. More importantly, the ETD is no longer ensuring the proper functioning of the internal markets. Changing the ETD is a part of the European Green Deal (EGD) and the “Fit for 55” legislative package. The former focuses on tackling environmental-related challenges and achieving the EU’s domestic greenhouse gas reductions objectives. In the EGD the European Commission committed to revising the ETD to ensure that energy taxation is in line with climate targets. Taxation plays a direct role in supporting the energy transition by sending the right price signals and providing the right incentives for sustainable consumption and production. The ETD was evaluated in 2019 [25]. Subsequently, the Council concluded that energy taxation plays an important role in steering successful energy transition [29] and, hence, invited the Commission to revisit the ETD. The current ETD, however, hinders the effective energy transition, raises a series of issues linked to its disconnection from climate and energy objectives and its shortcomings regarding the functioning of the internal market. For instance, in Finland, owners of electric storage systems pay taxes for the charging electricity. This not only does not motivate a sustainable energy transition but also leads to double taxation, as consumed electricity from storage is equally taxed [27]. In addition, there are some aspects of the ETD that lack clarity and lead to legal uncertainty, e.g., the definition of taxable products and uses that are out of the scope of the ETD.

- 3-13

- Outdated wholesale market mechanisms: A market clearing mechanism should be fair to aggregators, large renewable producers, and conventional producers, encourage flexibility providers, avoid spillage or renewable energy if it reduces consumers’ payment, and does not cause technical issues. The available cost minimization wholesale market structures should be revisited to achieve these targets.

- 3-14

- Separate Power Exchange and Flexibility Market: In the continuous effort to achieve the targets of the energy transition, the variable energy sources are becoming more prevalent. The relevance of co-optimization of energy and ancillary services, e.g., flexibility reserve, pervades the electricity market structures in Europe. In the US, the integration of transmission constraints in energy markets was underpinned by the advent of electricity restructuring and later led to the integration of ancillary services in the market. However, restructuring in most European countries does not co-optimize energy and reserve and other services [37]. A new EU-wide agent called “European Market Coupling Operator” deals with the transmission but not yet with ancillary services. The growing reliance on renewable energy generation and the services provided by the energy communities and citizens provides the reasons for revisiting the role of co-optimization of energy and services. In addition, energy and ancillary markets obey different rules in different member states and are not subject to EU-wide regulations.

- 3-15

- Pressure of traditional market players: Innovative DER- and customer-centric business projects put pressure on conventional market participants, such as centralized generation companies and operators, to change their business plans and models until they finally reach new market equilibrium. Increased self-generation and share of local energy markets can threaten the ability of DSOs to invest in network expansion and maintenance if their income is reduced from network assets. This leads to increased electricity prices and network costs for citizens who do not engage in energy provision. It is also important to note that the local markets also need the distribution grid for delivering locally generated energy to the consumers. Traditional energy market players are also likely to resist the increased share of local markets as they may fear losing their position in the market. Although new opportunities will arise for these important and experienced market players to offer new types of services at the early stages of the energy transition, they may resist it.

- 3-16

- Unavailability of network codes and effective standards for switching between grid-connected and island modes: Such switching entails a complex sequence of actions and requires special care about frequency and voltage control, due to the imbalances of generation and loads [27].

- 3-17

- Managing instantaneous active/reactive power balances between upstream and downstream networks: is problematic under various voltage profiles [38]. TSO-DSO coordination needs to be revisited to cope with power and frequency control requirements since a significant extent of the generation in downstream comes from intermittent sources.

- 3-18

- Unavailability of Smart meters and lack of standardization on smart metering: Smart meters are the other key components to the operation of and to market flexibility management. Luckily, smart meter rollout is getting momentum in most Member States. The penetration of smart electricity meters has passed the 50% mark in 2020 owing to expanded investments in grid digitalization by utilities in Europe. In 2020, about 150 million smart electricity meters were installed with the bloc recording a 49% penetration rate. However, firstly, such meters have not yet been installed for many other households. On the other hand, there is a need to unify and tighten standardization in metering schemes. Administration of the aspects linked to the data available from such smart meters should be better studied. An example is a need for the analysis of the data that should be availed to citizens to enable them to manage their demand based on the signal of the market price. The need for standardization of the data to be exchanged among the agents, or the plans for taking actions with regards to the access and protection of such data are the issues that should be tackled before causing escalating problems.

- 3-19

- Regulation barriers hindering the effective operation of RESs and ESSs: In some MSs, some other regulatory barriers hinder the development of LEMs. Most of these barriers stem from blocking the effective operation of DERs, RESs, and ESSs that was discussed in the previous subsections. For instance, in some Member States, it is not legal to blend energy generation with storage in the customer premises. In some other states, it has not been viewed in the regulations to feed the citizens’ generated electricity to the grid. These challenges hinder the energy transition and are detrimental to both sustainable adoption of RESs and ESSs and upgrade of market design.

- 3-20

- The regulators often do not permit microgrid islanding: Typically, to avoid resynchronisation issues, voltage stability problems and other challenges related to the safe operation of microgrids, the islanding mode of operation is prohibited for microgrids [30]. To face this, the policymakers and other decision-makers need to push regulatory bodies to accelerate compliance with bi-directionality requirements, at the point of common coupling (PCC), where many technologies should be adopted to assure voltage and frequency stabilities as well as protection coordination. These technologies range from fault current limiters to new methods that have been recently proposed for dynamic stability based on the inverters of RESs. Many required changes in the regulations have been presented in [30].

- 3-21

- Inconsistency of market instruments for incentivizing renewables and the need for further investment in these technologies: Regulations constantly change concerning prosumer feed-in tariffs and the models that decide the level of such tariffs. Such regulations also vary among the MSs. Even though this gives rise to uncertainty of the business model from the perspective of citizens, it is understandable when analyzing the problem from the viewpoints of incentivizing the citizens for the adoption of such technologies and the need for such energy production. What is not rational, however, is that, in some MSs, the feed-in tariffs/premiums are not considered for citizens and energy communities, while the renewable share in their energy markets is way lower than the amount provided in CEP. Except for such inconsistency, in some MSs, there are no customer remuneration schemes for surplus electricity generation. In other cases, it is not possible based on the local regulations to export electricity produced by energy communities to the grid, which keeps these communities away from minimum revenues for market participation. In such situations, eliminating the chance of receiving extra remuneration through such premiums for self-consumption and the unavailability of an effective mechanism to adjust feed-in tariffs/premiums demotivate citizens. In less active countries, the operation of local energy markets entails well-determined and harmonized regulations geared towards permitting citizens to trade surplus electricity with grid operators or other customers [27].

- 3-22

- DSOs regulations motivating investment in wired solutions and conventional production not in demand response and renewable production projects: It was discussed that the economic regulations of DSOs usually lead to their tendency towards employing the products of conventional generation companies since they are remunerated for providing the required assets that make it viable to deliver the power to end-users. As a side effect, such regulations also incentivize infrastructure expansion investments over RESs and demand response. Such legislative frameworks differ considerably across the Member States, and also globally, and will affect the development of efficient local energy markets to make the energy transition possible.

- 3-23

- Long administrative procedures can be an important barrier in getting the rights and incentives to install DERs. Usually, different plants of different sizes are subjected to different authorization requirements and the process can last for a different number of years. Moreover, in some Member States, there are no (or no expediting) regulations for the connection of small-scale renewable generation in rural zones. This is likely to lead to a long administrative process and delay. There should be some mechanisms for obtaining the approvals for starting such a project. An example of such absent regulations is that it is not clear who pays for connecting the small-scale resources to the distribution grid. Another example is the ambiguity around the entities that are responsible for potentially required grid reinforcements [31]. Along with the already unclear policy settings around this subject, such an uncertainty introduces additional risks for shareholders. This accumulated risk negatively affects cost-benefit analyses and reduces the number of potential prosumers in the future of energy systems in the Member States.

4. Barriers Concerning Regulations, Codes, and Standards

4.1. Bulgaria

4.2. Cyprus

- (a)

- the installation of net-metering photovoltaic systems with a capacity of up to 10 KW connected to the grid for all consumers (residential and non-residential). Net metering will be converter to net-billing after 2023, and

- (b)

- the self-generation systems with capacity up to 10 MW for commercial and industrial consumers.

4.3. Ireland

4.4. Italy

4.5. Latvia

4.6. Summary of the Studies on the Sample Below-Average Spending MSs

4.7. Network Connection Code Case Study: RESERVE Project

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Abbreviations

| AVM | Active Voltage Management |

| BRP | Balance Responsible Party |

| CEC | Citizen Energy Community |

| CEP | Clean Energy Package |

| CRU | Commission for Regulation of Utilities |

| CSA | Coordination and Support Action |

| DECC | Department of Environment, Climate and Communications |

| DER | Distributed Energy Resource |

| DNO | Distribution Network Operator |

| DR | Demand Response |

| DSO | Distribution System Operators’ |

| EAC | Electricity Authority of Cyprus |

| EGD | European Green Deal |

| EIRIE | European Interconnection for Research Innovation and Entrepreneurship |

| EMS | Energy Management Systems |

| EPBD | Energy Performance of Buildings Directive |

| ESCo | Energy Service Company |

| ESS | Energy Storage System |

| ETD | Energy Taxation Directive |

| EU | European Union |

| LEM | Local Energy Market |

| LV | Low Voltage |

| MS | Member State |

| MV | Medium Voltage |

| NECP | National Energy and Climate Plan |

| PCC | Point of Common Coupling |

| PANTERA | PAN European Technology Energy Research Approach |

| R&I | Research and Innovation |

| RCS | Regulations, Codes, and Standards |

| REC | Renewable Energy Community |

| RES | Renewable Energy Resource |

| RESS | Renewable Electricity Support Scheme |

| TSO | Transmission System Operator |

| ULTC | Under-Load Tap Changer |

| VC | Voltage Control |

References

- Giordano, V.; Gangale, F.; Fulli, G.; Sánchez Jiménez, M.; Onyeji, I.; Colta, A.; Papaioannou, I.; Mengolini, A.; Alecu, C.; Ojala, T.; et al. Smart Grid Projects in Europe: Lessons Learned and Current Developments; Publications Office of the European Union: Luxembourg, 2011.

- Gangale, F.; Vasiljevska, J.; Covrig, C.F.; Mengolini, A.; Fulli, G. Smart Grid Projects Outlook 2017: Facts, Figures and Trends in Europe; JRC Science for Policy Report; Publications Office of the European Union: Luxembourg, 2017.

- Project Website. Available online: Https://pantera-platform.eu/TitleofSite (accessed on 1 December 2021).

- Carroll, P.; Nouri, A.; Khadem, S.; Papadimitriou, C.; Mutule, A.; Stanev, R.; Cabiati, M. Development of Network Codes to Facilitate the Energy Transition. In Proceedings of the 2021 9th International Conference on Smart Grid (icSmartGrid), Setubal, Portugal, 29 June–1 July 2021; pp. 63–67. [Google Scholar]

- PANTERA Project. The State of R&I, Standardisation and Regulation, Deliverable D3.2. Report on Regulations, Codes and Standards in EU-28. 2020. Available online: https://pantera-platform.eu/wp-content/uploads/2021/01/D3.2_Report-on-Regulations-Codes-and-Standards-in-EU-28.pdf (accessed on 1 December 2021).

- ETIPSNET. ETIP SNET R&I Roadmap 2020–2030; ETIPSNET: Aurora, IL, USA, 2019. [Google Scholar]

- Nouri, A.; Soroudi, A.; Keane, A. Resilient decentralised control of inverter-interfaced distributed energy sources in low-voltage distribution grid. IET Smart Grid 2020, 3, 153–161. [Google Scholar] [CrossRef]

- Nouri, A.; Soroudi, A.; Murphy, R.; Ryan, D.; De Leon, M.P.; Grant, N.; Keane, A. A non-wire solution for the active mangament of distribution networks. In Proceedings of the 9th Renewable Power Generation Conference (RPG Dublin Online 2021), Online, 1–2 March 2021; pp. 372–376. [Google Scholar]

- ENEFIRST Project. Report on Barriers to Implementing E1st in the EU-28. Deliverable D2.4 of the ENEFIRST Project, Funded by the H2020 Programme. 2020. Available online: http://enefirst.eu (accessed on 19 January 2022).

- Giraudet, L.G. Energy efficiency as a credence good: A review of informational barriers to energy savings in the building sector. Energy Econ. 2020, 85, 104698. [Google Scholar] [CrossRef]

- TRIME project. U-Sentric and TU Delft. D3.3 Identifying Barriers, Solutions and Best Practices for Energy Renovations. Report of the TRIME Project. 2016. Available online: https://repository.tudelft.nl/islandora/object/uuid:f806d5a4-0701-4fde-8ae3-826552c1d273/datastream/OBJ/download (accessed on 19 January 2022).

- Renovate Project Website. Available online: https://www.renovate-europe.eu/renovate2recover-how-transformational-are-the-national-recovery-plans-for-buildings-renovation/ (accessed on 29 December 2021).

- Aurora. Power Sector Modelling: System Cost Impact of Renewables. In Report for the National Infrastructure Commission; Aurora Energy Research Limited: Oxford, UK, 2018; Available online: Https://nic.org.uk/app/uploads/Power-sector-modelling-final-report-1-Aurora-Energy-Research.pdf (accessed on 29 December 2021).

- Parrish, B.; Heptonstall, P.; Gross, R.; Sovacool, B.K. A systematic review of motivations, enablers and barriers for consumer engagement with residential demand response. Energy Policy 2020, 138, 111221. [Google Scholar] [CrossRef]

- OVO Energy. Blueprint for a Post-Carbon Society: How Residential Flexibility Is Key to Decarbonising Power, Heat and Transport; OVO Energy: London, UK, 2018. [Google Scholar]

- Parrish, B.; Gross, R.; Heptonstall, P. On demand: Can demand response live up to expectations in managing electricity systems? Energy Res. Soc. Sci. 2019, 51, 107–118. [Google Scholar] [CrossRef]

- US DOE. Customer Acceptance, Retention, and Response to Time-Based Rates from the Consumer Behavior Studies; US Department of Energy: Washington, DC, USA, 2016.

- Hall, N.L.; Jeanneret, T.D.; Rai, A. Cost-reflective electricity pricing: Consumer preferences and perceptions. Energy Policy 2016, 95, 62–72. [Google Scholar] [CrossRef]

- Buchanan, K.; Banks, N.; Preston, I.; Russo, R. The British public’s perception of the UK smart metering initiative: Threats and opportunities. Energy Policy 2016, 91, 87–97. [Google Scholar] [CrossRef] [Green Version]

- Lopes, M.A.R.; Antunes, C.H.; Janda, K.B.; Peixoto, P.; Martins, N. The potential of energy behaviours in a smart(er) grid: Policy implications from a Portuguese exploratory study. Energy Policy 2016, 90, 233–245. [Google Scholar] [CrossRef]

- Bradley, P.; Coke, A.; Leach, M. Financial incentive approaches for reducing peak electricity demand, experience from pilot trials with a UK energy provider. Energy Policy 2016, 98, 108–120. [Google Scholar] [CrossRef] [Green Version]

- Kolokathis, C.; Hogan, M.; Jahn, A. Cleaner, Smarter, Cheaper: Network Tariff Design for a Smart Future; Regulatory Assistance Project: Montpelier, VT, USA, 2018. [Google Scholar]

- Pató, Z.; Baker, P.; Rosenow, J. Performance-Based Regulation: Aligning Incentives with Clean Energy Outcomes; Regulatory Assistance Project: Montpelier, VT, USA, 2019. [Google Scholar]

- CE Delft. The Potential of Energy Citizens in the European Union. 2019. Available online: http://www.cedelft.eu/publicatie/the_potential_of_energy_citizens_in_the_european_union/1845 (accessed on 19 January 2022).

- USEF. Workstream on Aggregator Implementation Models, Recommended Practices and Key Considerations for a Regulatory Framework and Market Design on Explicit Demand Response. 2017. Available online: https://www.usef.energy/app/uploads/2016/12/Recommended-practices-for-DR-market-design.pdf (accessed on 29 December 2021).

- SWD. 329 Final, Restructuring the Community Framework for the Taxation of Energy Products and Electricity. 2019. Available online: Https://ec.europa.eu/info/sites/default/files/swd_2019_0329_en.pdf (accessed on 27 December 2021).

- Mendes, G.; Nylund, J.; Annala, S.; Honkapuro, S.; Kilkki, O.; Segerstam, J. Local energy markets: Opportunities, benefits, and barriers. In Proceedings of the CIRED 2018 Ljubljana Workshop on Microgrids and Local Energy Communities, Ljubljana, Slovenia, 7–8 June 2018. [Google Scholar]

- The USmartConsumer Project. Smart Metering Benefits for European Consumers and Utilities. 2017. Available online: https://pdf4pro.com/cdn/smart-metering-benefits-for-european-2b2ecb.pdf (accessed on 19 January 2022).

- Wouters, C. Towards a regulatory framework for microgrids—The Singapore experience. Sustain. Cities Soc. 2015, 15, 22–32. [Google Scholar] [CrossRef] [Green Version]

- Ali, A.; Li, W.; Hussain, R.; He, X.; Williams, B.W.; Memon, M.H. Overview of Current Microgrid Policies, Incentives and Barriers in the European Union, United States and China. Sustainability 2017, 9, 1146. [Google Scholar] [CrossRef] [Green Version]

- Council Conclusions 29 November 2019 14608/19 FISC 458; EU Monitor: Tbilisi, GA, USA, 2019; Available online: https://data.consilium.europa.eu/doc/document/ST-14594-2019-INIT/en/pdf (accessed on 20 January 2022).

- Chesser, M.; Lyons, P.; O’Reilly, P.; Carroll, P. Air source heat pump in-situ performance. Energy Build. 2021, 251, 111365. [Google Scholar] [CrossRef]

- De Rosa, M.; Carragher, M.; Finn, D.P. Flexibility assessment of a combined heat-power system (chp) with energy storage under real-time energy price market framework. Therm. Sci. Eng. Prog. 2018, 8, 426–438. [Google Scholar] [CrossRef]

- Sun, Z.; Li, L.; Bego, A.; Dababneh, F. Customer-side electricity load management for sustainable manufacturing systems utilizing combined heat and power generation system. Int. J. Prod. Econ. 2015, 165, 112–119. [Google Scholar] [CrossRef]

- Tesla Impact Report. 2018. Available online: www.tesla.com/ns_videos/2018-tesla-impact-report.pdf (accessed on 19 January 2022).

- Dudjak, V.; Neves, D.; Alskaif, T.; Khadem, S.; Pena-Bello, A.; Saggese, P.; Bowler, B.; Andoni, M.; Bertolini, M.; Zhou, Y.; et al. Impact of local energy markets integration in power systems layer: A comprehensive review. Appl. Energy 2021, 301, 117434. [Google Scholar] [CrossRef]

- Smeers, Y.; Martin, S.; Aguado, J.A. Co-optimization of energy and reserve with Incentives to Wind Generation. IEEE Trans. Power Syst. 2021. [Google Scholar] [CrossRef]

- Nouri, A.; Soroudi, A.; Keane, A. Strategic Scheduling of Discrete Control Devices in Active Distribution Systems. IEEE Trans. Power Deliv. 2020, 35, 2285–2299. [Google Scholar] [CrossRef] [Green Version]

- Code for Management and Control of the Electrical Power System; State Gazette 6/21.01.2014; Energy and Water Regulatory Commission of Bulgaria: Sofia, Bulgaria, 2014; Available online: https://www.dker.bg/files/DOWNLOAD/rule_el_15.pdf (accessed on 19 January 2022).

- Energy and Water Regulatory Commission of Bulgaria. Code on the Terms and Conditions for Provision of Network Access to the Electrical Transmission and Distribution System Networks; State Gazette 98/12.11.2013; Energy and Water Regulatory Commission of Bulgaria: Sofia, Bulgaria, 2013; Available online: https://www.dker.bg/files/DOWNLOAD/rule_el_14.pdf (accessed on 20 January 2022).

- Ministry of Energy of Bulgaria. Regulation №3 on the Organization of the Electrical Installations and Electrical Power Lines; State Gazette 108/19.12.207; Ministry of Energy of Bulgaria: Sofia, Bulgaria, 2017. Available online: https://www.gli.government.bg/sites/default/files/upload/documents/2020-09/N3_09.06.2004.pdf (accessed on 20 January 2022).

- Bertoldi, P.; Zancanella, P.; Boza-Kiss, B. Demand response status in EU Member States. Jt. Res. Cent. 2016. [Google Scholar] [CrossRef]

- Cyprus’ Integrated National Energy and Climate Plan under the Regulation (EU) 2018/1999 of the European Parliament and of the Council of 11 December 2018 on the Governance of the Energy Union and Climate Action, NECP Plan, Cyprus. Available online: Https://ec.europa.eu/energy/sites/ener/files/documents/cy_final_necp_main_en.pdf (accessed on 20 January 2022).

- Renewable Electricity Support Scheme (RESS) High Level Design. Available online: https://assets.gov.ie/77091/0c8db804-e10c-47c3-8a11-9a45777601fd.pdf (accessed on 19 January 2022).

- Renewable Electricity Support Scheme 1 (RESS 1) Final Auction Results. 2020. Available online: http://www.eirgridgroup.com/site-files/library/EirGrid/207158-EirGrid-Renewable-Energy-Scheme-LR5.pdf (accessed on 19 January 2022).

- Bertelè, U.; Chiesa, V. Renewable Energy Report; Politecnico di Milano: Milan, Italy, 2021; ISBN 978 88-6493-060-2. Available online: https://www.energystrategy.it/area-riservata/download-id/1023866/ (accessed on 20 January 2022).

- IEA Wind TCP Annual Report 2020, IEA Wind TCP. Available online: https://iea-wind.org/wp-content/uploads/2021/12/IEA-WIND-AR2020.pdf (accessed on 20 January 2022).

- Eurostat. Share of Energy from Renewable Sources (Online). Available online: https://ec.europa.eu/eurostat/databrowser/view/nrg_ind_ren/default/table?lang=en (accessed on 16 December 2021).

- EPSU. Power to the People: Upholding the Right to Clean, Affordable Energy for All in the EU; EPSU: Lindon, UT, USA, 2019. [Google Scholar]

- Bouzarovski, S.; Petrova, S. A global perspective on domestic energy deprivation: Overcoming the energy poverty–fuel poverty binary. Energy Res. Soc. Sci. 2015, 10, 31–40. [Google Scholar] [CrossRef]

- Lazdins, R.; Mutule, A.; Zalostiba, D. PV Energy Communities—Challenges and Barriers from a Consumer Perspective: A Literature Review. Energies 2021, 14, 4873. [Google Scholar] [CrossRef]

- Pētersone, K.; Āboltiņš, R.; Vecvagare, L.; Boyer, M.; Pētersone, A.; Brizga, J. Recommendations for the Development of Community RES Projects in Latvia; Situation Assessment and Proposals: Mallorca, Spain, 2020. (In Latvian) [Google Scholar]

- National Energy and Climate Plan of Latvia 2021–2030; The European Commission: Brussels, Belgium, 2018.

- Soroudi, A.; Nouri, A.; Keane, A.; Karthik Gurumurthy, S.; Monti, A.; Ryan, D.; De Leon, M.P.; Grant, N. Drafting of Ancillary Services and Network Codes, RESERVE Project Deliverales. 2018. Available online: http://www.re-serve.eu/files/reserve/Content/Deliverables/727481_deliverable_D3.8.pdf (accessed on 28 December 2021).

- Soroudi, A.; Nouri, A.; Keane, A.; Karthik Gurumurthy, S.; Monti, A.; Ryan, D.; De Leon, M.P.; Grant, N. Drafting of Ancillary Services and Network Codes V2, RESERVE Project Deliverales. 2019. Available online: http://www.re-serve.eu/files/reserve/Content/Deliverables/727481_RESERVE_D3.9.pdf (accessed on 29 December 2021).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| EE, DR, and BEMSs | LEMs |

|---|---|

| 1-2, 1-3, 1-5, 2-5, 2-6, 2-7, 2-9, 2-12 | 3-2, 3-4, 3-6, 3-7, 3-8, 3-9, 3-13, 3-14, 3-16, 3-17, 3-18, 3-19, 3-20, 3-21, 3-22, 3-23 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Nouri, A.; Khadem, S.; Mutule, A.; Papadimitriou, C.; Stanev, R.; Cabiati, M.; Keane, A.; Carroll, P. Identification of Gaps and Barriers in Regulations, Standards, and Network Codes to Energy Citizen Participation in the Energy Transition. Energies 2022, 15, 856. https://doi.org/10.3390/en15030856

Nouri A, Khadem S, Mutule A, Papadimitriou C, Stanev R, Cabiati M, Keane A, Carroll P. Identification of Gaps and Barriers in Regulations, Standards, and Network Codes to Energy Citizen Participation in the Energy Transition. Energies. 2022; 15(3):856. https://doi.org/10.3390/en15030856

Chicago/Turabian StyleNouri, Alireza, Shafi Khadem, Anna Mutule, Christina Papadimitriou, Rad Stanev, Mattia Cabiati, Andrew Keane, and Paula Carroll. 2022. "Identification of Gaps and Barriers in Regulations, Standards, and Network Codes to Energy Citizen Participation in the Energy Transition" Energies 15, no. 3: 856. https://doi.org/10.3390/en15030856

APA StyleNouri, A., Khadem, S., Mutule, A., Papadimitriou, C., Stanev, R., Cabiati, M., Keane, A., & Carroll, P. (2022). Identification of Gaps and Barriers in Regulations, Standards, and Network Codes to Energy Citizen Participation in the Energy Transition. Energies, 15(3), 856. https://doi.org/10.3390/en15030856