Critical Assessment of Feed-In Tariffs and Solar Photovoltaic Development in Vietnam

,

,  ,

,  , , and

, , and

Abstract

:

1. Introduction

2. Policy Development for Solar PV in Vietnam

3. Results of the FIT Deployment for Solar PV in the Current Years

4. Challenges and Opportunities in Deploying the FITs

4.1. Unsustainable FIT Mechanism

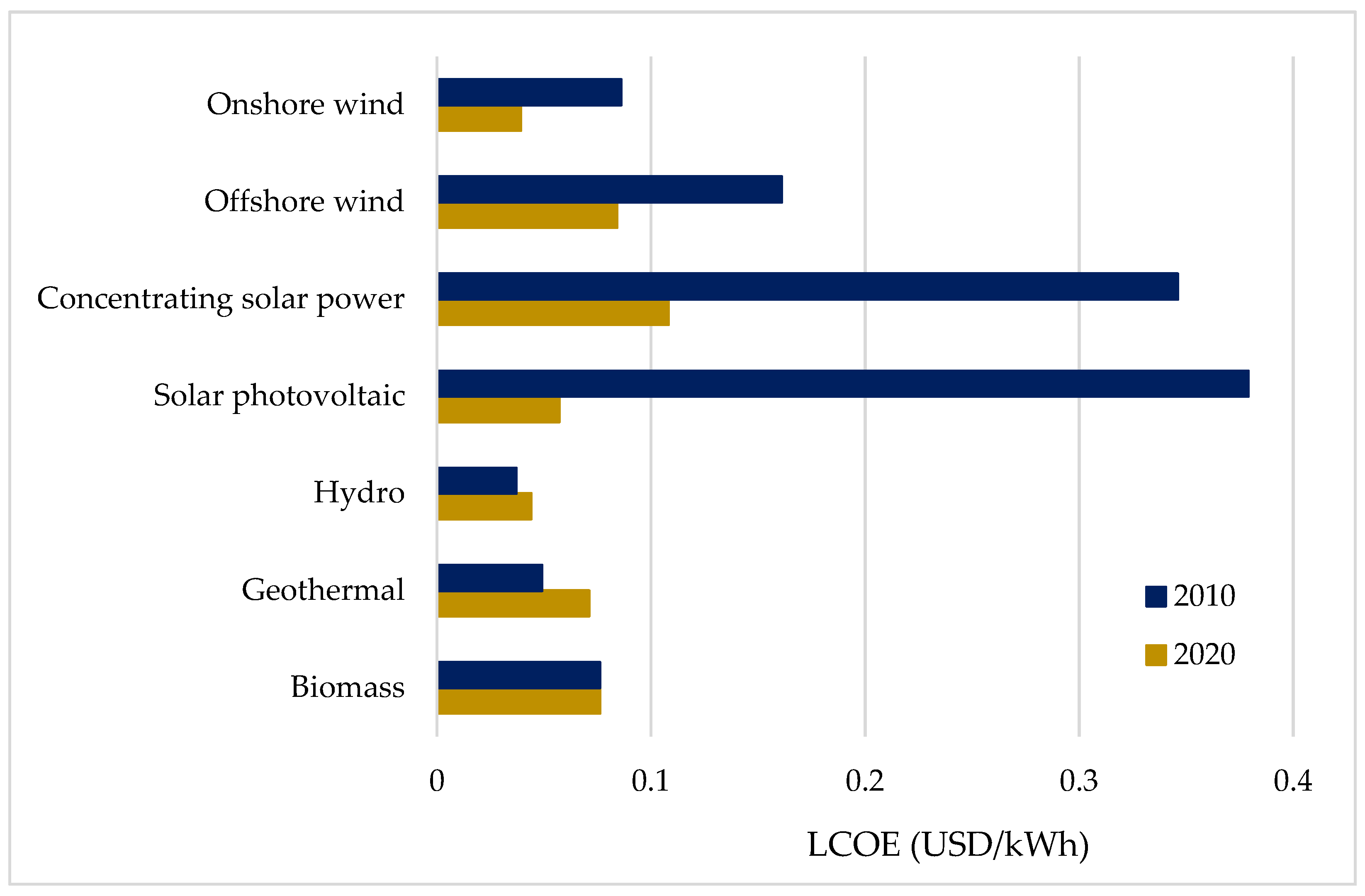

4.2. Relatively High Levelized Cost of Electricity

4.3. Disadvantages on Electricity Price

4.4. Policy Inconsistencies

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Jäger-Waldau, A. PV Status Report 2019; Publications Office of the European Union: Luxembourg, 2019; ISBN 978-92-76-12608-9.

- REN21. Renewables 2020. Global Status Report; REN21 Secretariat: Paris, France, 2020; ISBN 978-3-9818911-7-1. [Google Scholar]

- REN21. Renewables 2021. Global Status Report; REN21 Secretariat: Paris, France, 2021; ISBN 9783948393038. [Google Scholar]

- Riva Sanseverino, E.; Le Thi Thuy, H.; Pham, M.-H.; Di Silvestre, M.L.; Nguyen Quang, N.; Favuzza, S. Review of Potential and Actual Penetration of Solar Power in Vietnam. Energies 2020, 13, 2529. [Google Scholar] [CrossRef]

- Tvaronaciene, M.; Slusarczyk, B. Energy Transformation towards Sustainability; Elsevier Inc.: Amsterdam, The Netherlands, 2019; ISBN 9780128176887. [Google Scholar]

- UN. Report of the Conference of the Parties on its Third Session, Held at Kyoto from 1 to 11 December 1997; United Nations: Kyoto, Japan, 1998.

- COP21. Paris Agreement under the United Nations Framework Convention on Climate Change; United Nations: Paris, France, 2015.

- COP26. Glasgow Agreement under the United Nations Framework Convention on Climate Change; United Nations: Glasgow, Scotland, 2021.

- IRENA. Renewable Power Generation Costs in 2020; International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2021; ISBN 978-92-9260-348-9. [Google Scholar]

- IRENA. Renewable Power Generation Costs in 2019; International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2020; ISBN 9789292602444. [Google Scholar]

- Taylor, B.Y.M. Energy Subsidies: Evolution in the Global Energy Transformation to 2050; International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2020; ISBN 9789292601256. [Google Scholar]

- Lazard Lazard’s Levelized Cost of Energy Analysis—Version 14.0. Available online: https://www.lazard.com/perspective/levelized-cost-of-energy-and-levelized-cost-of-storage-2020/ (accessed on 19 October 2020).

- Gray, M.; Ljungwaldh, S.; Watson, L.; Kok, I. Powering Down Coal—Navigating the Economic and Financial Risks in the Last Years of Coal Power; Carbon Tracker Initiative: London, UK, 2018. [Google Scholar]

- Perez-Arriaga, I.J.; Batlle, C. Impacts of Intermittent Renewables on Electricity Generation System Operation. Econ. Energy Environ. Policy 2012, 1, 3–18. [Google Scholar] [CrossRef] [Green Version]

- Hart, E.K.; Stoutenburg, E.D.; Jacobson, M.Z. The Potential of Intermittent Renewables to Meet Electric Power Demand: Current Methods and Emerging Analytical Techniques. Proc. IEEE 2012, 100, 322–334. [Google Scholar] [CrossRef]

- Milanés-Montero, P.; Arroyo-Farrona, A.; Pérez-Calderón, E. Assessment of the Influence of Feed-In Tariffs on the Profitability of European Photovoltaic Companies. Sustainability 2018, 10, 3427. [Google Scholar] [CrossRef] [Green Version]

- Ye, L.-C.; Rodrigues, J.F.D.; Lin, H.X. Analysis of feed-in tariff policies for solar photovoltaic in China 2011–2016. Appl. Energy 2017, 203, 496–505. [Google Scholar] [CrossRef]

- Dusonchet, L.; Telaretti, E. Economic analysis of different supporting policies for the production of electrical energy by solar photovoltaics in eastern European Union countries. Energy Policy 2010, 38, 4011–4020. [Google Scholar] [CrossRef]

- Dusonchet, L.; Telaretti, E. Economic analysis of different supporting policies for the production of electrical energy by solar photovoltaics in western European Union countries. Energy Policy 2010, 38, 3297–3308. [Google Scholar] [CrossRef]

- Abolhosseini, S.; Heshmati, A. The main support mechanisms to finance renewable energy development. Renew. Sustain. Energy Rev. 2014, 40, 876–885. [Google Scholar] [CrossRef] [Green Version]

- Johnstone, N.; Haščič, I.; Popp, D. Renewable Energy Policies and Technological Innovation: Evidence Based on Patent Counts. Environ. Resour. Econ. 2010, 45, 133–155. [Google Scholar] [CrossRef]

- Haas, R.; Panzer, C.; Resch, G.; Ragwitz, M.; Reece, G.; Held, A. A historical review of promotion strategies for electricity from renewable energy sources in EU countries. Renew. Sustain. Energy Rev. 2011, 15, 1003–1034. [Google Scholar] [CrossRef]

- Lüthi, S.; Wüstenhagen, R. The price of policy risk—Empirical insights from choice experiments with European photovoltaic project developers. Energy Econ. 2012, 34, 1001–1011. [Google Scholar] [CrossRef] [Green Version]

- Couture, T.; Gagnon, Y. An analysis of feed-in tariff remuneration models: Implications for renewable energy investment. Energy Policy 2010, 38, 955–965. [Google Scholar] [CrossRef]

- Muhammad-Sukki, F.; Abu-Bakar, S.H.; Munir, A.B.; Mohd Yasin, S.H.; Ramirez-Iniguez, R.; McMeekin, S.G.; Stewart, B.G.; Sarmah, N.; Mallick, T.K.; Abdul Rahim, R.; et al. Feed-in tariff for solar photovoltaic: The rise of Japan. Renew. Energy 2014, 68, 636–643. [Google Scholar] [CrossRef]

- Arias, J. Solar Energy, Energy Storage and Virtual Power Plants in Japan—Potential Opportunities of Collaboration between Japanese and European Firms; EU-Japan Centre for Industrial Cooperation: Tokyo, Japan, 2018. [Google Scholar]

- Lüthi, S. Effective deployment of photovoltaics in the Mediterranean countries: Balancing policy risk and return. Solar Energy 2010, 84, 1059–1071. [Google Scholar] [CrossRef]

- FMENCNS. Act on Granting Priority to Renewable Energy Sources (Renewable Energy Sources Act, Germany, 2000). Solar Energy 2001, 70, 489–504. [Google Scholar] [CrossRef]

- Grau, T. Responsive feed-in tariff adjustment to dynamic technology development. Energy Econ. 2014, 44, 36–46. [Google Scholar] [CrossRef]

- Di Dio, V.; Favuzza, S.; La Cascia, D.; Massaro, F.; Zizzo, G. Critical assessment of support for the evolution of photovoltaics and feed-in tariff(s) in Italy. Sustain. Energy Technol. Assess. 2015, 9, 95–104. [Google Scholar] [CrossRef]

- Homma, T.; Akimoto, K. Analysis of Japan’s energy and environment strategy after the Fukushima nuclear plant accident. Energy Policy 2013, 62, 1216–1225. [Google Scholar] [CrossRef]

- METI. Act on Purchase of Renewable Energy Sourced Electricity by Electric Utilities; Japan Ministry of Economy Trade and Industry: Tokyo, Japan, 2011.

- CEERP. BP Statistical Review of World Energy 2019; BP International Limited: London, UK, 2019. [Google Scholar]

- EREA&DEA. Vietnam Energy Outlook Report 2019; Vietnam Ministry of Industry and Trade: Hanoi, Vietnam, 2019.

- Zissler, R. Renewable Energy to Replace Coal Power in Southeast Asia. Pragmatism to Deliver a Sustainable Bright Future; Renewable Energy Institute: Tokyo, Japan, 2019. [Google Scholar]

- Prime Minister. Decision 02/2019/QD-TTg on Amendments and Supplements to Certain Articles of Decision No. 11/2017/QD-TTG on the Mechanism for Encouragement of Development of Solar Power in Vietnam; Vietnam Government: Hanoi, Vietnam, 2019.

- Prime Minister. Decision 11/2017/QD-TTg on Mechanism for Encouragement of the Development of Solar Power Projects in Vietnam; Vietnam Government: Hanoi, Vietnam, 2017.

- Prime Minister. Decision 13/2020/QD-TTg on Mechanism for Encouragement of the Development of Solar Power in Vietnam; Vietnam Government: Hanoi, Vietnam, 2020.

- VGO. Notice 402/TB-VPCP of Prime Minister’s Conclusions on the Draft of Solar Power Promotion Mechanism in Vietnam, Applied from July 1, 2019, Following Decision 11/2017/QD-TTg; Vietnam Goverment Office: Hanoi, Vietnam, 2019.

- MoIT. Dispatch 9608/BCT-DL on Suspension of Proposal and Agreement for Solar Power Projects under FIT Price Mechanism; Vietnam Ministry of Industry and Trade: Hanoi, Vietnam, 2019.

- MoIT. Dispatch 89/BCT-DL on on Implementation of Agreements with Rooftop Solar Power; Vietnam Ministry of Industry and Trade: Hanoi, Vietnam, 2020.

- MoIT. Proposal 10170/TTr-BCT of a New Draft Decision on the Mechanism for Developing Solar Power Projects in Vietnam; Vietnam Ministry of Industry and Trade: Hanoi, Vietnam, 2019.

- VEPG. Vietnam Factsheet on Rooftop Solar Development 2019; Viet Nam Energy Partnership Group: Hanoi, Vietnam, 2019. [Google Scholar]

- EVN. Press Release on Capacity Release of Renewable Energy Sources of Vietnam Electricity. Available online: https://www.evn.com.vn/d6/news/Den-3062019-Tren-4460-MW-dien-mat-troi-da-hoa-luoi-6-12-23925.aspx (accessed on 10 September 2020).

- Minh Khuong, P.; McKenna, R.; Fichtner, W. A Cost-Effective and Transferable Methodology for Rooftop PV Potential Assessment in Developing Countries. Energies 2020, 13, 2501. [Google Scholar] [CrossRef]

- Lan, T.T.; Techato, K.; Jirakiattikul, S. The challenge of feed-in-tariff (FIT) policies applied to the development of electricity from sustainable resources—Lessons for Vietnam. Int. Energy J. 2019, 19, 199–212. [Google Scholar]

- Shem, C.; Simsek, Y.; Hutfilter, U.F.; Urmee, T. Potentials and opportunities for low carbon energy transition in Vietnam: A policy analysis. Energy Policy 2019, 134, 110818. [Google Scholar] [CrossRef]

- Nguyen, P.A.; Abbott, M.; Nguyen, T.L.T. The development and cost of renewable energy resources in Vietnam. Util. Policy 2019, 57, 59–66. [Google Scholar] [CrossRef]

- Phap, V.M.; Thu Huong, N.T.; Hanh, P.T.; Van Duy, P.; Van Binh, D. Assessment of rooftop solar power technical potential in Hanoi city, Vietnam. J. Build. Eng. 2020, 32, 101528. [Google Scholar] [CrossRef]

- MoIT&DEA. Vietnam Energy Outlook 2017; Danish Energy Agency: Hanoi, Vietnam, 2017.

- WB Group. Solar Resource Maps for More Than 200 Countries on the World. Available online: https://solargis.com/maps-and-gis-data/download (accessed on 8 May 2021).

- IEA. Southeast Asia Energy Outlook 2017; OECD: Bangkok, Thailand, 2017; ISBN 9789264285576. [Google Scholar]

- Prime Minister. Decision 1855/QD-TTg of Approving Vietnam’s National Energy Development Strategy up to 2020, with Vision to 2050; Vietnam Government: Hanoi, Vietnam, 2007.

- Prime Minister. Decision 1208/QD-TTg Dated 21 July 2011 of Approving the National Master Plan for Power Development in the 2011–2020 Period, with Considerations to 2030; Vietnam Government: Hanoi, Vietnam, 2011.

- Prime Minister. Decision 2081/QD-TTg of Approving the Program on Electricity Supply in Rural, Mountainous and Island Areas in Period of 2013–2020; Vietnam Government: Hanoi, Vietnam, 2013.

- Prime Minister. Decision 2068/QD-TTg of Approving the Viet Nam’s Renewable Energy Development Strategy up to 2030 with an Outlook to 2050; Vietnam Government: Hanoi, Vietnam, 2015.

- Prime Minister. Decision 428/QD-TTg of Approval of the Revised National Power Development Master Plan for the 2011–2020 Period with the vision to 2030; Vietnam Government: Hanoi, Vietnam, 2016.

- Prime Minister. Decision 37/2011/QD-TTg on the Mechanism Supporting the Development of wind Power Project in Vietnam; Vietnam Government: Hanoi, Vietnam, 2011.

- Sinh, T.D.; Long, N.H.; Dung, N.T.M. Report on Rural Electrification Policies and Supporting Mechanisms for Off-Grid Community; Green Innovation and Development Centre: Hanoi, Vietnam, 2017. [Google Scholar]

- MoIT. Decision 2023/QD-BCT of Approving the Program to Promote the Development of Rooftop Solar Power in Vietnam in Period of 2019–2025; Vietnam Ministry of Industry and Trade: Hanoi, Vietnam, 2019.

- MoIT. Circular 16/2017/TT-BCT on Project Development and Model Power Purchase Agreements Applied to Solar Power Projects; Vietnam Ministry of Industry and Trade: Hanoi, Vietnam, 2017.

- MoIT. Circular 18/2020/TT-BCT on Project Development and Model Power Purchase Agreements Applied to Solar Power Projects; Vietnam Ministry of Industry and Trade: Hanoi, Vietnam, 2020.

- MoIT. Circular 05/2019/TT-BCT of Amendments to Circular 16/2017/TT-BCT on Development of Solar Power Projects and Standard form Power Purchase Agreement; Vietnam Ministry of Industry and Trade: Hanoi, Vietnam, 2019.

- VEPG. Vietnam Factsheet on Rooftop Solar Development 2020; Viet Nam Energy Partnership Group: Hanoi, Vietnam, 2020. [Google Scholar]

- EVN Press Release on Capacity Release of Renewable Energy Sources of Vietnam Electricity. Available online: https://www.evn.com.vn/d6/news/Khi-dien-mat-troi-bung-no-141-17-27530.aspx (accessed on 6 January 2021).

- Polo, J.; Martínez, S.; Fernandez-Peruchena, C.M.; Navarro, A.A.; Vindel, J.M.; Gastón, M.; Ramírez, L.; Soria, E.; Guisado, M.V.; Bernardos, A.; et al. Maps of Solar Resource and Potential in Vietnam; Vietnam Ministry of Industry and Trade: Hanoi, Vietnam, 2015.

- Lee, N.; Flores-espino, F.; Oliveira, R.; Roberts, B.; Bowen, T.; Katz, J. Exploring Renewable Energy Opportunities in Select Southeast Asian Countries: A Geospatial Analysis of the Levelized Cost of Energy of Utility-Scale Wind and Solar Photovoltaics; National Renewable Energy Laboratory: Washington, DC, USA, 2020.

- WB Group. Vietnam Solar Competitive Bidding Strategy and Framework; World Bank Group: Washington, DC, USA, 2019. [Google Scholar]

- Zahedi, A. A review on feed-in tariff in Australia, what it is now and what it should be. Renew. Sustain. Energy Rev. 2010, 14, 3252–3255. [Google Scholar] [CrossRef]

- Yoomak, S.; Patcharoen, T.; Ngaopitakkul, A. Performance and Economic Evaluation of Solar Rooftop Systems in Different Regions of Thailand. Sustainability 2019, 11, 6647. [Google Scholar] [CrossRef] [Green Version]

- Orioli, A.; Franzitta, V.; Di Gangi, A.; Foresta, F. The Recent Change in the Italian Policies for Photovoltaics: Effects on the Energy Demand Coverage of Grid-Connected PV Systems Installed in Urban Contexts. Energies 2016, 9, 944. [Google Scholar] [CrossRef] [Green Version]

- Brückmann, R.; Jirouš, F.; Spitzley, J.-B.; Herling, J.; Bauknecht, D. Integration of Electricity from Renewables to the Electricity Grid and to the Electricity Market—RES National Report: Slovakia; Institute for Applied Ecology: Berlin, Germany, 2012. [Google Scholar]

- WB Group. Turkey—Rooftop Solar PV Market Assessment: Final Report; World Bank Group: Washington, DC, USA, 2018. [Google Scholar]

- Ayoub, N.; Yuji, N. Governmental intervention approaches to promote renewable energies—Special emphasis on Japanese feed-in tariff. Energy Policy 2012, 43, 191–201. [Google Scholar] [CrossRef]

- EC. Support Schemes for Renewable Electricity in the EU, No. 408; European Commission: Brussels, Belgium, 2010; ISBN 9789279148941. [Google Scholar]

- Schallenberg-Rodriguez, J.; Haas, R. Fixed feed-in tariff versus premium: A review of the current Spanish system. Renew. Sustain. Energy Rev. 2012, 16, 293–305. [Google Scholar] [CrossRef]

- IEA. Solar Energy: Maping the Road Ahead; International Energy Agency: Paris, France, 2019. [Google Scholar]

- Ragwitz, M.; Winkler, J.; Klessmann, C.; Gephart, M.; Resch, G. Recent Developments of Feed-in Systems in the EU—A Research Paper for the International Feed-In Cooperation; Ministry for the Environment, Nature Conservation and Nuclear Safety (BMU): Munich, Germany, 2012. [Google Scholar]

- Lesser, J.A.; Su, X. Design of an economically efficient feed-in tariff structure for renewable energy development. Energy Policy 2008, 36, 981–990. [Google Scholar] [CrossRef]

- EPIA. Retrospective Measures at National Level and Their Impact on the Photovoltaic Sector; European Photovoltaic Industry Association: Brussels, Belgium, 2013. [Google Scholar]

- EREA&DEA. Detailed grid modelling of the Vietnamese power system. Background to the Vietnam Energy Outlook Report 2019; Vietnam Ministry of Industry and Trade: Hanoi, Vietnam, 2019.

- Singh, R.; Banerjee, R. Estimation of rooftop solar photovoltaic potential of a city. Solar Energy 2015, 115, 589–602. [Google Scholar] [CrossRef]

- IRENA. Renewable Energy Statistics 2019; International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2019; ISBN 978-92-9260-033-4. [Google Scholar]

- IEA-PVPS. Photovoltaic Power Systems: Annual Report 2018; International Energy Agency: Fribourg, Switzerland, 2018; ISBN 978-3-906042-84-8. [Google Scholar]

- Prime Minister. Decision 34/2017/QD-TTg of the Price Frame of the Average Electricity Retail Price for a Period of 2016–2020; Vietnam Government: Hanoi, Vietnam, 2017.

- MoIT. Decision 648/QD-BCT of Adjusting the Average Electricity Retail Price and Stipulating Electricity Selling Price from 20th March 2019; Vietnam Ministry of Industry and Trade: Hanoi, Vietnam, 2019.

- MoIT. Decision 4495/QD-BCT of Electricity Retail Price from 1st December 2017; Vietnam Ministry of Industry and Trade: Hanoi, Vietnam, 2017.

- MoIT. Decision 2093/QĐ-BCT on Approved the Scheme of Competitive Retail Electricity Market Model Design; Vietnam Ministry of Industry and Trade: Hanoi, Vietnam, 2020.

- Martinez, R.; Hosein, P. The Impact of Low Electricity Prices on Renewable Energy Production. In Proceedings of the 2018 International Conference and Utility Exhibition on Green Energy for Sustainable Development (ICUE), Phuket, Thailand, 24–26 October 2018; pp. 1–6. [Google Scholar]

- Kok, G.; Shang, K.; Yucel, S. Impact of Electricity Pricing Policy on Renewable Energy Investments and Carbon Emissions. SSRN Electron. J. 2014, 64, 1–48. [Google Scholar] [CrossRef]

- White, W.; Lunnan, A.; Nybakk, E.; Kulisic, B. The role of governments in renewable energy: The importance of policy consistency. Biomass Bioenergy 2013, 57, 97–105. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Le, H.T.-T.; Sanseverino, E.R.; Nguyen, D.-Q.; Di Silvestre, M.L.; Favuzza, S.; Pham, M.-H. Critical Assessment of Feed-In Tariffs and Solar Photovoltaic Development in Vietnam. Energies 2022, 15, 556. https://doi.org/10.3390/en15020556

Le HT-T, Sanseverino ER, Nguyen D-Q, Di Silvestre ML, Favuzza S, Pham M-H. Critical Assessment of Feed-In Tariffs and Solar Photovoltaic Development in Vietnam. Energies. 2022; 15(2):556. https://doi.org/10.3390/en15020556

Chicago/Turabian StyleLe, Hang Thi-Thuy, Eleonora Riva Sanseverino, Dinh-Quang Nguyen, Maria Luisa Di Silvestre, Salvatore Favuzza, and Manh-Hai Pham. 2022. "Critical Assessment of Feed-In Tariffs and Solar Photovoltaic Development in Vietnam" Energies 15, no. 2: 556. https://doi.org/10.3390/en15020556

APA StyleLe, H. T.-T., Sanseverino, E. R., Nguyen, D.-Q., Di Silvestre, M. L., Favuzza, S., & Pham, M.-H. (2022). Critical Assessment of Feed-In Tariffs and Solar Photovoltaic Development in Vietnam. Energies, 15(2), 556. https://doi.org/10.3390/en15020556