A Margin Design Method Based on the SPAN in Electricity Futures Market Considering the Risk of Power Factor

Abstract

:1. Introduction

2. The Impact of Power Factor on Electrical Commodities

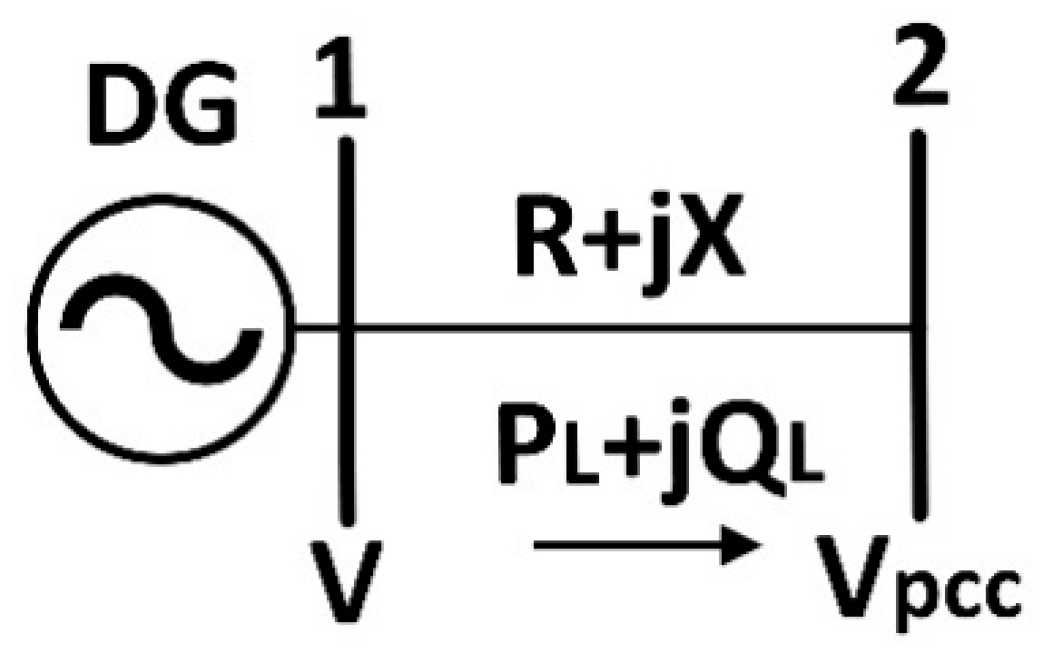

2.1. Power Factor and Power Transfer

2.2. Economic Value of Reactive Power Demand

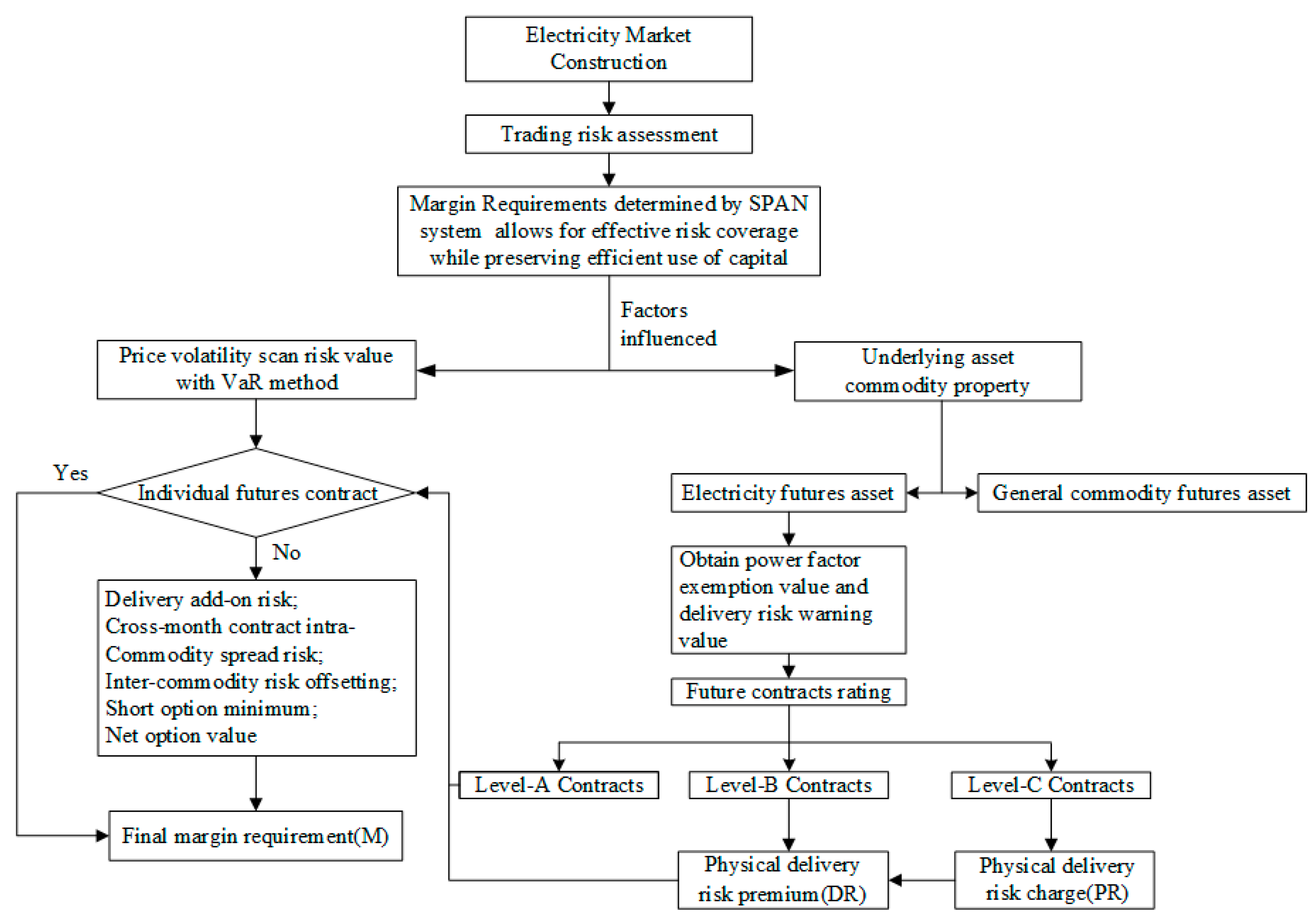

3. SPAN-Based Margin Design for Electricity Futures

3.1. Brief Review of SPAN

3.2. SPAN-Based Margin Calculation

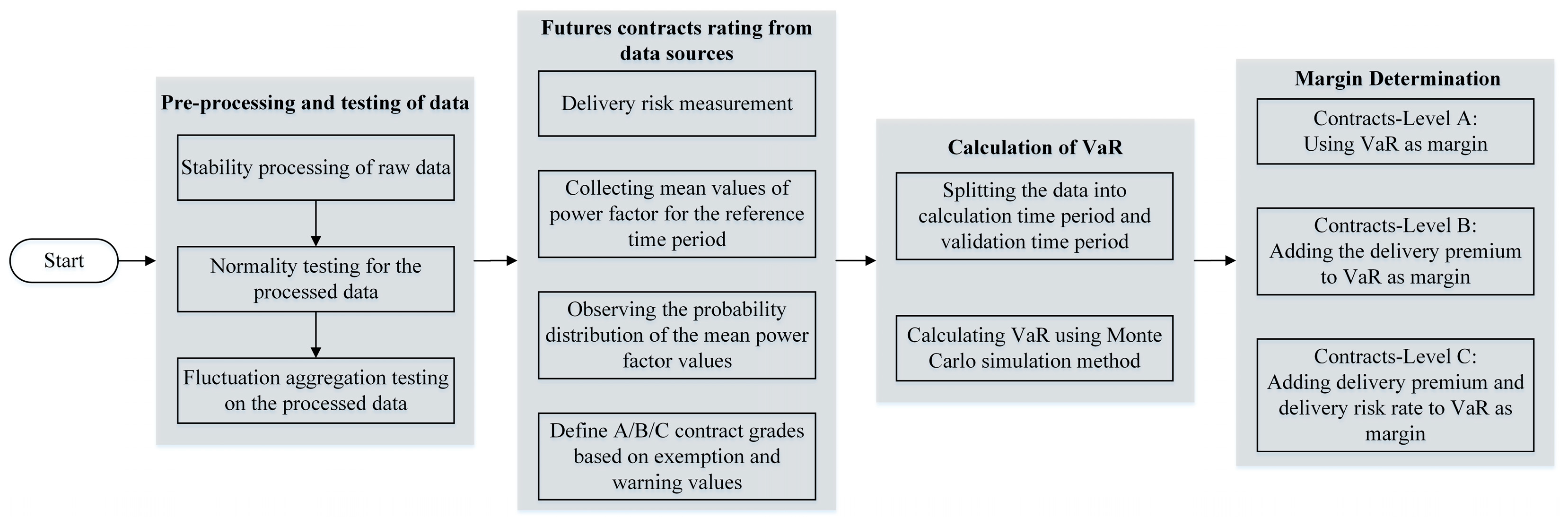

3.2.1. Value at Risk (VaR) Calculation

3.2.2. Physical Delivery Risk Rates

- Step 1: The exchange determines the power factor exemption value based on the requirements of the futures contract and the average value of the delivery risk warning value .

- Step 2: Select the actual power factor sampling time period T and acquire m data points in the time period according to the unit time t: .

- Step 3: Count the frequency distribution of all data points and observe the distribution.

- Step 4: Select the percentage of the distribution where the power factor is less than the exemption value required: .

- Step 5: Select the percentage of the distribution where the power factor is less than the delivery risk warning value required: .

- Step 6: Calculate the delivery premium and delivery risk rate.

3.2.3. SPAN-Based Margin Calculation Model

4. Empirical Study

4.1. Data

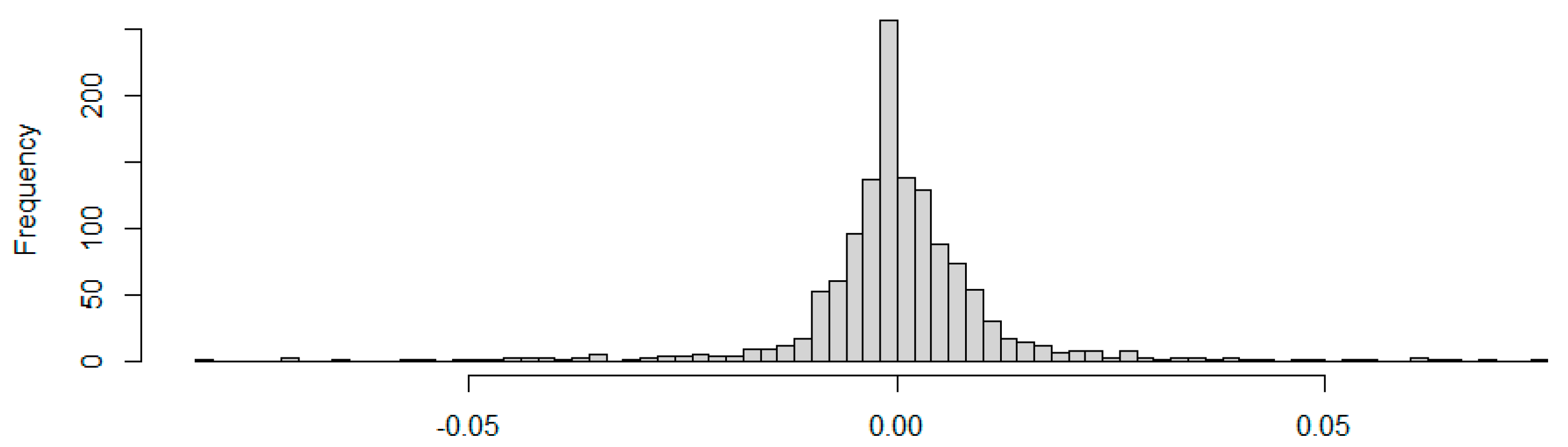

4.2. Summary Statistics

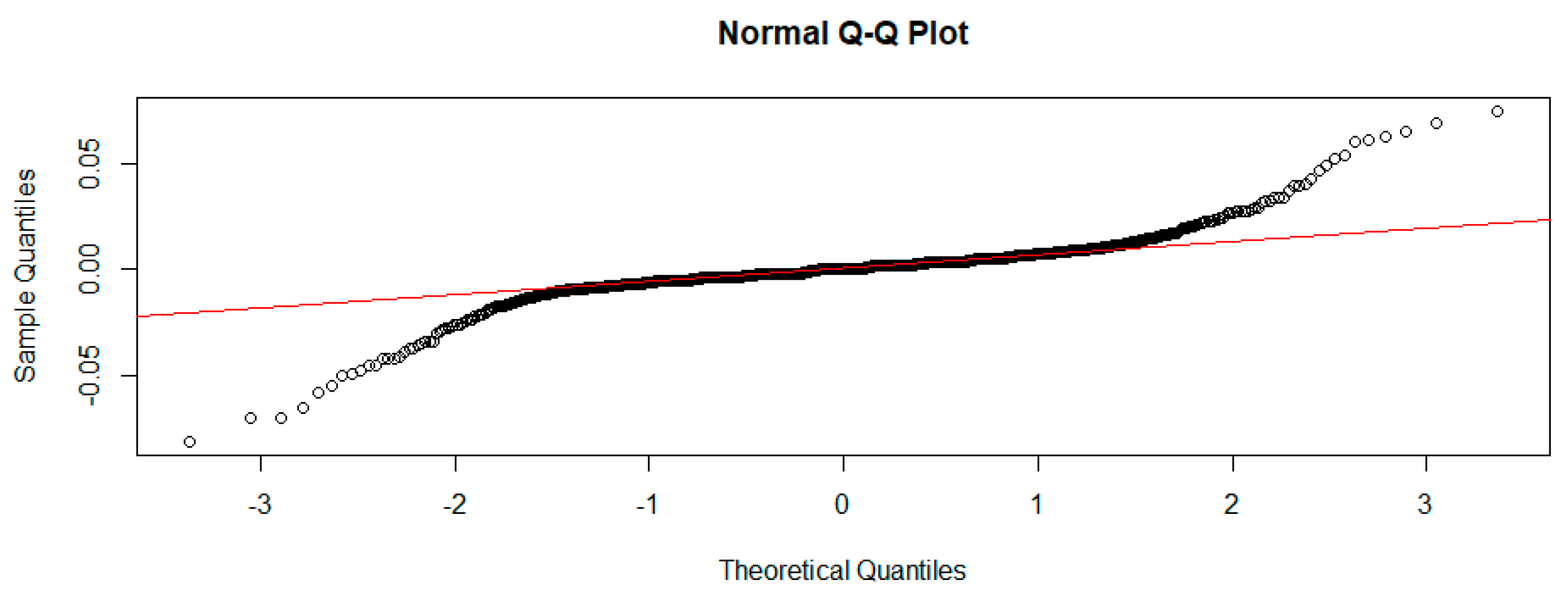

4.2.1. Normality Test (Quantile–Quantile Plot)

4.2.2. Normality Test (Jarque-Bera Test)

4.2.3. Volatility Clustering Test

4.3. Calculation Results

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Lin, J.; Kahrl, F.; Yuan, J.; Liu, X.; Zhang, W. Challenges and strategies for electricity market transition in China. Energy Policy 2019, 133, 110899. [Google Scholar] [CrossRef]

- Spodniak, P.; Bertsch, V. Is flexible and dispatchable generation capacity rewarded in electricity futures markets? A multina-tional impact analysis. Energy 2020, 196, 117050. [Google Scholar] [CrossRef]

- Zhang, Y.; Farnoosh, A. Analyzing the dynamic impact of electricity futures on revenue and risk of renewable energy in China. Energy Policy 2019, 132, 678–690. [Google Scholar] [CrossRef]

- Deng, W.; Dai, N.; Lao, K.-W.; Guerrero, J.M. A Virtual-Impedance Droop Control for Accurate Active Power Control and Reactive Power Sharing Using Capacitive-Coupling Inverters. IEEE Trans. Ind. Appl. 2020, 56, 6722–6733. [Google Scholar] [CrossRef]

- Deng, W.; Liu, Z.; Qin, H.; Chen, M.; Zhang, Y. Study of a virtual-impedance of the capacitor-series inverter for wider ac-curate power control range. Energy Rep. 2022, 8, 27–36. [Google Scholar] [CrossRef]

- Tang, Y.; Zhuang, Z.; Li, X. Revision Suggestion on the Policy of Tariff Regulation by Power Factor. Power Capacit. React. Power Compens. 2009, 30, 15–20. [Google Scholar]

- Lien, D.; Yang, L. Availability and settlement of individual stock futures and options expiration-day effects: Evidence from high-frequency data. Q. Rev. Econ. Finance 2005, 45, 730–747. [Google Scholar] [CrossRef]

- Adil, F.; Siddiqui, D.-A. Exploring the Effect of Physical Delivery Verses Cash Settled Futures Contracts with the Prospective of Obligatory Delivery in Islamic Contract of Sales. Int. J. Soc. Adm. Sci. 2019, 4, 155–177. [Google Scholar] [CrossRef] [Green Version]

- He, Y.; Su, F.; Xia, Y. PJM Electric Future Trading Experience and Its Enlightment to Electric Future Construction in China. Guangdong Electr. Power 2021, 34, 37–42. [Google Scholar]

- Huisman, R.; Kilic, M. Electricity Futures Prices: Indirect Storability, Expectations, and Risk Premiums. Energy Econ. 2012, 34, 892–898. [Google Scholar] [CrossRef]

- Al Boucherbi, M.; Askari, Q. Modern financial investment tools, future contracts as a model. Eurasian J. Hist. Geogr. Econ. 2022, 9, 22–32. [Google Scholar]

- Klimontowicz, M.; Losa-Jonczyk, A.; Zacny, B. Banks’ Energy Behavior: Impacts of the Disparity in the Quality and Quantity of the Disclosures. Energies 2021, 14, 7325. [Google Scholar] [CrossRef]

- Pressmair, G.; Amann, C.; Leutgöb, K. Business Models for Demand Response: Exploring the Economic Limits for Small- and Medium-Sized Prosumers. Energies 2021, 14, 7085. [Google Scholar] [CrossRef]

- Fishe, R.P.H.; Goldberg, L.G.; Gosnell, T.F.; Sinha, S. Margin requirements in futures markets: Their relationship to price volatility. J. Futur. Mark. 1990, 10, 541–554. [Google Scholar] [CrossRef]

- Wang, J.; Ge, Y.; Tang, K.; Deng, Y. Can Adjustments of Futures Trading Rules Reduce Investor’s Leverage? J. Man-Agement Sci. China 2019, 24, 99–110. [Google Scholar]

- Sun, Q.; Liang, Z.; Wang, X.; Zheng, W. Research on Dynamic Calculation Method of Margin in Electricity Market-Design of calculation method based on electricity price characteristics and SPAN system. Price Theory Pract. 2021, 7, 145–150. [Google Scholar]

- Si, J.; Huang, R.; Gong, P. Nonparametric VaR Method′s Application in Standard Portfolio Analysis of Risk. Journal of Wuhan University of Technology. Transp. Sci. Eng. 2007, 31, 664–667. [Google Scholar]

- Kupiec, P.H.; White, P. Regulatory competition and the efficiency of alternative derivative product margining systems. J. Futures Mark. 1997, 16, 943–969. [Google Scholar] [CrossRef] [Green Version]

- Eldor, R.; Hauser, S.; Yaari, U. Safer Margins for Option Trading: How Accuracy Promotes Efficiency. Multinatl. Finance J. 2011, 15, 217–234. [Google Scholar] [CrossRef]

- Zhao, Z.; Cheng, R.; Yan, B.; Zhang, J.; Zhang, Z.; Zhang, M.; Lai, L.L. A dynamic particles MPPT method for photovoltaic systems under partial shading conditions. Energy Convers. Manag. 2020, 220, 113070. [Google Scholar] [CrossRef]

- Alexander, C.; Kaeck, A.; Sumawong, A. A parsimonious parametric model for generating margin requirements for futures. Eur. J. Oper. Res. 2018, 273, 31–43. [Google Scholar] [CrossRef]

- Westgaard, S.; Frydenberg, S.; Sveinsson, J.A.; Aalokken, M. Performance of value-at-risk averaging in the Nordic power futures market. J. Energy Mark. 2021, 13, 25–55. [Google Scholar] [CrossRef]

- Guo, Z. Stochastic multifactor models in risk management of energy futures. J. Future Mark. 2020, 40, 1918–1934. [Google Scholar] [CrossRef]

- Pena, J.I.; Rodriguez, R.; Mayoral, S. Tail risk of electricity futures. arXiv 2020, arXiv:2202.01732. [Google Scholar]

- Cotter, J.; Dowd, K. Extreme spectral risk measures: An application to futures clearinghouse margin requirements. J. Bank. Finance 2006, 30, 3469–3485. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Mean | Median | Maximum | Minimum | Stdev | Skewness | Kurtosis | Jarque-Bera | p-Value |

|---|---|---|---|---|---|---|---|---|

| 0.0004 | 0.000 | 0.0750 | −0.0813 | 0.0119 | −0.1253 | 11.1845 | 6821.523 | 0.000 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lin, D.; Deng, W.; Dai, S. A Margin Design Method Based on the SPAN in Electricity Futures Market Considering the Risk of Power Factor. Energies 2022, 15, 5138. https://doi.org/10.3390/en15145138

Lin D, Deng W, Dai S. A Margin Design Method Based on the SPAN in Electricity Futures Market Considering the Risk of Power Factor. Energies. 2022; 15(14):5138. https://doi.org/10.3390/en15145138

Chicago/Turabian StyleLin, Deqin, Wenyang Deng, and Siting Dai. 2022. "A Margin Design Method Based on the SPAN in Electricity Futures Market Considering the Risk of Power Factor" Energies 15, no. 14: 5138. https://doi.org/10.3390/en15145138

APA StyleLin, D., Deng, W., & Dai, S. (2022). A Margin Design Method Based on the SPAN in Electricity Futures Market Considering the Risk of Power Factor. Energies, 15(14), 5138. https://doi.org/10.3390/en15145138