Integrated Risk Analysis of Aggregators: Policy Implications for the Development of the Competitive Aggregator Industry

,

,

, and

, and

Abstract

:1. Introduction

2. Methodology

3. The Context and Challenges of Aggregator Industry Development

3.1. Political Drivers

3.2. Economic Factors of Aggregator Business Models

3.3. Social Acceptance and Consumer Engagement

3.4. Technological Challenges

3.5. Legal and Regulatory Framework

3.6. Environmental Effects of Aggregators

4. Exploratory Risk Assessment

5. Discussion of Factors Affecting Aggregators’ Development and Policy Implications

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- European Commission. Clean Energy for All Europeans; Publications Office of the EU, European Commission: Luxembourg, 2019. [Google Scholar]

- Eurelectric. Flexibility and Aggregation—Requirements for Their Interaction in the Market; Eurelectric: Brussels, Belgium, 2014. [Google Scholar]

- IRENA. Innovation Landscape Brief: Aggregators, International Renewable Energy Agency; IRENA: Abu Dhabi, United Arab Emirates, 2019. [Google Scholar]

- Barbero, M.; Corchero, C.; Casals, L.C.; Igualada, L.; Heredia, F.J. Critical evaluation of European balancing markets to enable the participation of Demand Aggregators. Appl. Energy 2020, 264, 114707. [Google Scholar] [CrossRef]

- Ponds, K.T.; Arefi, A.; Sayigh, A.; Ledwich, G. Aggregator of Demand Response for Renewable Integration and Customer Engagement: Strengths, Weaknesses, Opportunities, and Threats. Energies 2018, 11, 2391. [Google Scholar] [CrossRef] [Green Version]

- Kapassa, E.; Touloupou, M.; Themistocleous, M. Local Electricity and Flexibility Markets: SWOT Analysis and Recommendations. In Proceedings of the 2021 6th International Conference on Smart and Sustainable Technologies (SpliTech), Bol and Split, Croatia, 8–11 September 2021; pp. 1–6. [Google Scholar] [CrossRef]

- Mlecnik, E.; Parker, J.; Ma, Z.; Corchero, C.; Knotzer, A.; Pernetti, R. Policy challenges for the development of energy flexibility services. Energy Policy 2020, 137, 111147. [Google Scholar] [CrossRef]

- Lu, X.; Li, K.; Xu, H.; Wang, F.; Zhou, Z.; Zhang, Y. Fundamentals and business model for resource aggregator of demand response in electricity markets. Energy 2020, 204, 117885. [Google Scholar] [CrossRef]

- Wang, S.; Tan, X.; Liu, T.; Tsang, D.H.K. Aggregation of Demand-Side Flexibility in Electricity Markets: Negative Impact Analysis and Mitigation Method. IEEE Trans. Smart Grid 2021, 12, 774–786. [Google Scholar] [CrossRef]

- Capuder, T.; Sprčić, D.M.; Zoričić, D.; Pandžić, H. Review of challenges and assessment of electric vehicles integration policy goals: Integrated risk analysis approach. Int. J. Electr. Power Energy Syst. 2020, 119, 105894. [Google Scholar] [CrossRef]

- Mikulić, J.; Sprčić, D.M.; Holiček, H.; Prebežac, D. Strategic crisis management in tourism: An application of integrated risk management principles to the Croatian tourism industry. J. Destin. Mark. Manag. 2018, 7, 36–38. [Google Scholar] [CrossRef]

- Tavana, M.; Pirdashti, M.; Kennedy, D.T.; Belaud, J.P.; Behzadian, M. A hybrid Delphi-SWOT paradigm for oil and gas pipeline strategic planning in Caspian Sea basin. Energy Policy 2012, 40, 345–360. [Google Scholar] [CrossRef] [Green Version]

- Kauko, K.; Palmroos, P. The Delphi method in forecasting financial markets-An experimental study. Int. J. Forecast. 2014, 30, 313–327. [Google Scholar] [CrossRef]

- Rowe, G.; Wright, G. Expert Opinions in Forecasting: The Role of the Delphi Technique. In Principles of Forecasting; Springer: Boston, MA, USA, 2001; pp. 125–144. [Google Scholar] [CrossRef]

- Okoli, C.; Pawlowski, S.D. The Delphi method as a research tool: An example, design considerations and applications. Inf. Manag. 2004, 42, 15–29. [Google Scholar] [CrossRef] [Green Version]

- Gonan Božac, M. SWOT analiza i TOWS matrica—Sličnosti i razlike. Sveučilište Jurja Dobrile u Puli, Odjel za ekonomiju i turizam “Dr. Mijo Mirković”. Econ. Res.-Ekon. Istraživanja 2008, 21, 19–34. [Google Scholar]

- Bromiley, P.; McShane, M.; Nair, A.; Rustambekov, E. Enterprise Risk Management: Review, Critique, and Research Directions. Long Range Plan. 2015, 48, 265–276. [Google Scholar] [CrossRef] [Green Version]

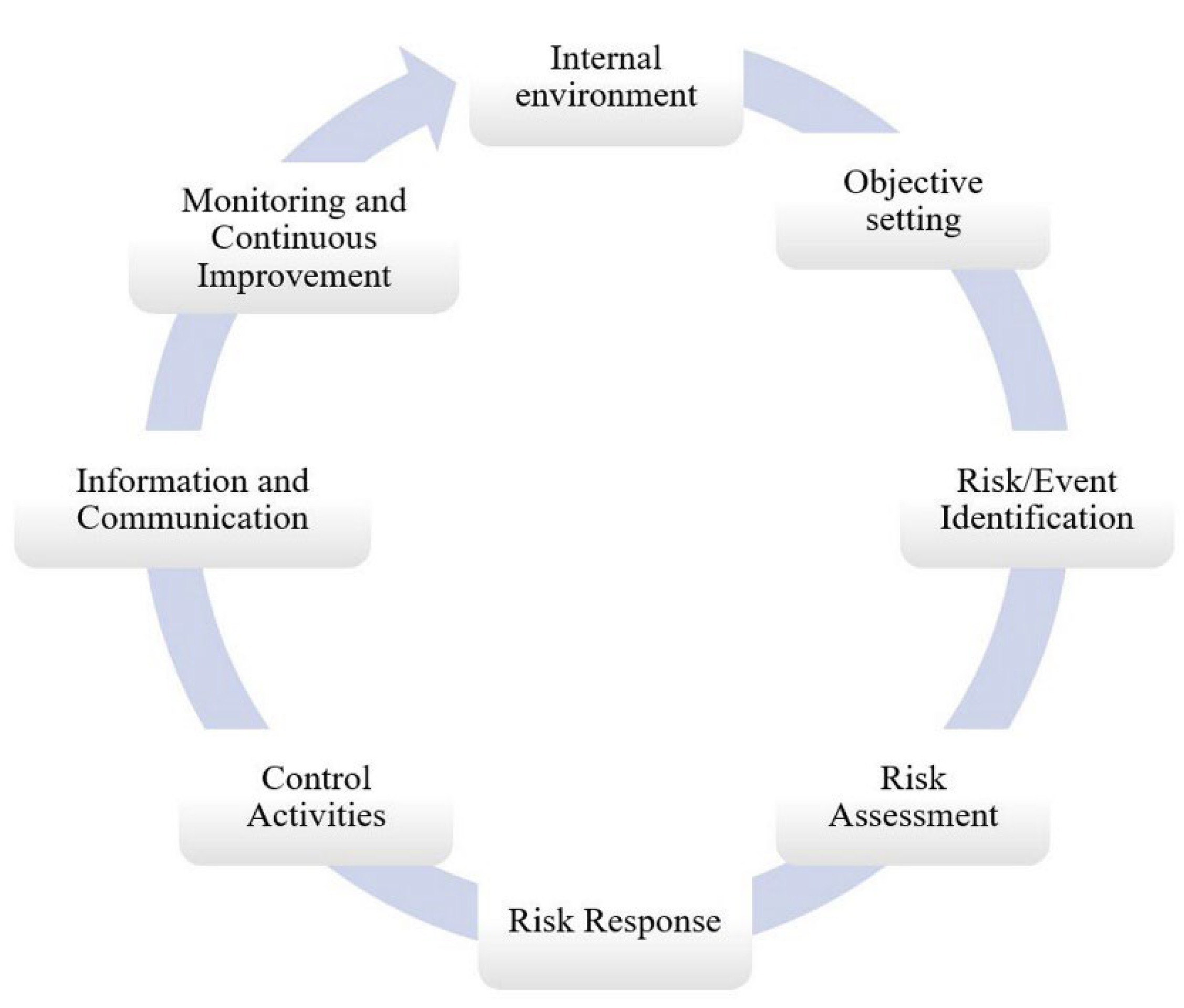

- COSO. Enterprise Risk Management—Integrated Framework; Committee of Sponsoring Organizations of the Treadway Commission: Jersey City, NJ, USA, 2004. [Google Scholar]

- Lundqvist, S.A. An Exploratory Study of Enterprise Risk Management. J. Account. Audit. Financ. 2014, 29, 393–429. [Google Scholar] [CrossRef]

- European Commission. The European Green Deal; European Commission: Luxembourg, 2019. [Google Scholar]

- Munta, M. The European Green Deal: A Game Changer or Simply a Buzzword? Friedrich-Ebert-Stiftung e.V.: Bonn, Germany, 2020. [Google Scholar]

- ENTSO-E. Completing the Map—Power System Needs in 2030 and 2040; ENTSO-E: Brussels, Belgium, 2021. [Google Scholar]

- European Parliament. Directive (EU) 2018/2002 of the European Parliament and of the Council of 11 December 2018—Amending Directive 2012/27/EU on energy efficiency. Off. J. Eur. Union 2018, L328, 210–230. [Google Scholar]

- Digitalising the Energy Sector—EU Action Plan. Have Your Say. 2021. Available online: https://ec.europa.eu/info/law/better-regulation/have-your-say/initiatives/13141-Digitalising-the-energy-sector-EU-action-plan_en (accessed on 25 November 2021).

- Rodríguez, L.R.; Brennenstuhl, M.; Yadack, M.; Boch, P.; Eicker, U. Heuristic optimization of clusters of heat pumps: A simulation and case study of residential frequency reserve. Appl. Energy 2019, 233–234, 943–958. [Google Scholar] [CrossRef]

- Prado, J.C.d.; Qiao, W.; Qu, L.; Agüero, J. The Next-Generation Retail Electricity Market in the Context of Distributed Energy Resources: Vision and Integrating Framework. Energies 2019, 12, 491. [Google Scholar] [CrossRef] [Green Version]

- Okur, Ö.; Heijnen, P.; Lukszo, Z. Aggregator’s business models in residential and service sectors: A review of operational and financial aspects. Renew. Sustain. Energy Rev. 2021, 139, 110702. [Google Scholar] [CrossRef]

- Burger, S.; Chaves-Ávila, J.P.; Batlle, C.; Pérez-Arriaga, I.J. A review of the value of aggregators in electricity systems. Renew. Sustain. Energy Rev. 2017, 77, 395–405. [Google Scholar] [CrossRef]

- Garcia-Rundstadler, B. Reaching the Optimum: From Monopoly to Aggregators; Deloitte, Newsletter Power & Utilities in Europe: London, UK, 2017; p. 3. [Google Scholar]

- BEUC. Electricity Aggregators: Starting off on the Right Foot with Consumers; BEUC: Brussels, Belgium, 2018. [Google Scholar]

- Staffell, I.; Rustomji, M. Maximising the value of electricity storage. J. Energy Storage 2016, 8, 212–225. [Google Scholar] [CrossRef] [Green Version]

- Braeuer, F.; Rominger, J.; McKenna, R.; Fichtner, W. Battery storage systems: An economic model-based analysis of parallel revenue streams and general implications for industry. Appl. Energy 2019, 239, 1424–1440. [Google Scholar] [CrossRef]

- Covic, N.; Braeuer, F.; McKenna, R.; Pandzic, H. Optimal PV and Battery Investment of Market-Participating Industry Facilities. IEEE Trans. Power Syst. 2021, 36, 3441–3452. [Google Scholar] [CrossRef]

- Jaeger-Waldau, A. PV Status Report 2019; Publications Office of the European Union: Luxembourg, 2019. [Google Scholar]

- Lee, Y.M.; Horesh, R.; Liberti, L. Optimal HVAC control as demand response with on-site energy storage and generation system. Energy Procedia 2015, 78, 2106–2111. [Google Scholar] [CrossRef] [Green Version]

- Short, M.; Rodriguez, S.; Charlesworth, R.; Crosbie, T.; Dawood, N. Optimal Dispatch of Aggregated HVAC Units for Demand Response: An Industry 4.0 Approach. Energies 2019, 12, 4320. [Google Scholar] [CrossRef] [Green Version]

- REN21. Renewables 2021, Global Status Report; REN21: Paris, France, 2021. [Google Scholar]

- IRENA. Electricity Storage and Renewables: Costs and Markets to 2030, International Renewable Energy Agency; IRENA: Abu Dhabi, United Arab Emirates, 2017. [Google Scholar]

- Ghose, T.; Pandey, H.W.; Gadham, K.R. Risk assessment of microgrid aggregators considering demand response and uncertain renewable energy sources. J. Mod. Power Syst. Clean Energy 2019, 7, 1619–1631. [Google Scholar] [CrossRef] [Green Version]

- Vatanparvar, K.; al Faruque, M.A. Design Space Exploration for the Profitability of a Rule-Based Aggregator Business Model within a Residential Microgrid. IEEE Trans. Smart Grid 2015, 6, 1167–1175. [Google Scholar] [CrossRef]

- European Smart Grids Task Force Expert Group 3. Demand Side Flexibility Perceived Barriers and Proposed Recommendations. 2019. Available online: https://ec.europa.eu/energy/sites/ener/files/documents/eg3_final_report_demand_side_flexiblity_2019.04.15.pdf (accessed on 7 June 2022).

- Kowalski, J.; Matusiak, B.E. End users’ motivations as a key for the adoption of the home energy management system. Int. J. Manag. Econ. 2019, 55, 13–24. [Google Scholar] [CrossRef] [Green Version]

- Wissner, M. The Smart Grid—A Saucerful of Secrets? Appl. Energy 2011, 88, 2509–2518. [Google Scholar] [CrossRef]

- Ma, Z.; Asmussen, A.; Jørgensen, B. Influential Factors to the Industrial Consumers’ Smart Grid Adoption. In Proceedings of the International Energy Conference (ASTECHNOVA 2016), Yogyakart, Indonesia, 2–3 November 2016. [Google Scholar]

- Ma, Z.; Asmussen, A.; Jørgensen, B. Industrial Consumers’ Smart Grid Adoption: Influential Factors and Participation Phases. Energies 2018, 11, 182. [Google Scholar] [CrossRef] [Green Version]

- Rathnayaka, A.J.D.; Potdar, V.; Ou, M.H. Prosumer management in socio-technical Smart Grid. In Proceedings of the CUBE’12: CUBE International IT Conference & Exhibition, Pune, India, 3–5 September 2012; pp. 483–489. [Google Scholar] [CrossRef]

- Barbu, A.-D.; Griffiths, N.; Morton, G. Achieving Energy Efficiency through Behaviour Change: What Does It Take? EEA Technical report No 5/2013; EEA: Copenhagen, Denmark, 2013. [Google Scholar]

- Trakas, D.; Kleftakis, V. COORDINET—List of KPIs: KPI and Process of Measures. 2019. Available online: https://private.coordinet-project.eu/files/documentos/5d724189a008fCoordiNet_Deliverable_1.6.pdf (accessed on 7 June 2022).

- Sullivan, R. Fiduciary Duty in the 21st Century. SSRN Electron. J. 2016. [Google Scholar] [CrossRef]

- Le Sourd, V.; Martellini, L. The EDHEC European ETF, Smart Beta and Factor Investing Survey; EDHEC-Risk Institute: Nice, France, 2020. [Google Scholar]

- Stolowy, H.; Paugam, L. The expansion of non-financial reporting: An exploratory study. Account. Bus. Res. 2018, 48, 525–548. [Google Scholar] [CrossRef] [Green Version]

- Gils, H.C. Assessment of the theoretical demand response potential in Europe. Energy 2014, 67, 1–18. [Google Scholar] [CrossRef]

- Gyalai-Korpos, M.; Zentkó, L.; Hegyfalvi, C.; Detzky, G.; Tildy, P.; Hegedűsné Baranyai, N.; Pintér, G.; Zsiborács, H. The Role of Electricity Balancing and Storage: Developing Input Parameters for the European Calculator for Concept Modeling. Sustainability 2020, 12, 811. [Google Scholar] [CrossRef] [Green Version]

- Shi, K.; Ye, H.; Song, W.; Zhou, G. Virtual Inertia Control Strategy in Microgrid Based on Virtual Synchronous Generator Technology. IEEE Access 2018, 6, 27949–27957. [Google Scholar] [CrossRef]

- Das, C.K.; Bass, O.; Kothapalli, G.; Mahmoud, T.S.; Habibi, D. Overview of energy storage systems in distribution networks: Placement, sizing, operation, and power quality. Renew. Sustain. Energy Rev. 2018, 91, 1205–1230. [Google Scholar] [CrossRef]

- Roberts, B.P.; Sandberg, C. The role of energy storage in development of smart grids. Proc. IEEE 2011, 99, 1139–1144. [Google Scholar] [CrossRef]

- Luburić, Z.; Bašić, H.; Pandžić, H.; Plavšić, T. Uloga Spremnika Energije u Elektroenergetskom Sustavu; HRO CIGRE: Split, Hrvatska, 2016; p. 1. [Google Scholar]

- Šimić, Z.; Topić, D.; Knežević, G.; Pelin, D. Battery energy storage technologies overview. Int. J. Electr. Comput. Eng. Syst. 2021, 12, 53–65. [Google Scholar] [CrossRef]

- Vedullapalli, D.T.; Hadidi, R.; Schroeder, B. Combined HVAC and Battery Scheduling for Demand Response in a Building. IEEE Trans. Ind. Appl. 2019, 55, 7008–7014. [Google Scholar] [CrossRef]

- European Commisssion. Benchmarking Smart Metering Deployment in the EU-28; Publications Office of the European Union: Luxembourg, 2020. [Google Scholar]

- IoT Analytics. Smart Meter Market Report 2019–2024; IoT Analytics: Hamburg, Germany, 2019. [Google Scholar]

- Landis+Gyr. Capital Markets Day 2021, Presentation Slides from the Virtual Event. 2021. Available online: https://www.landisgyr.eu/webfoo/wp-content/uploads/2021/01/20210127-Capital-Markets-Day-2021-Presentation.pdf (accessed on 8 December 2021).

- Rashidizadeh-Kermani, H.; Vahedipour-Dahraie, M.; Shafie-khah, M.; Catalão, J.P.S. Stochastic programming model for scheduling demand response aggregators considering uncertain market prices and demands. Int. J. Electr. Power Energy Syst. 2019, 113, 528–538. [Google Scholar] [CrossRef]

- Abapour, S.; Mohammadi-Ivatloo, B.; Hagh, M.T. Robust bidding strategy for demand response aggregators in electricity market based on game theory. J. Clean. Prod. 2020, 243, 118393. [Google Scholar] [CrossRef]

- European Commision. M/441 Standardisation Mandate to Cen, Cenelec and Etsi in the Field of Measuring Instruments for the Development of an Open Architecture for Utility Meters Involving Communication Protocols Enabling Interoperability; European Commision: Luxembourg, 2009. [Google Scholar]

- European Telecommunications Standards Institute. Open Smart Grid Protocol (OSGP); Smart Metering/Smart Grid Communication Protocol V2.2.1; European Telecommunications Standards Institute: Sophia Antipolis, France, 2019. [Google Scholar]

- Schoitsch, E. Design for Safety and Security of Complex Embedded Systems: A Unified Approach. In Cyberspace Security and Defense: Research Issues; Springer: Berlin/Heidelberg, Germany, 2005; pp. 161–174. [Google Scholar] [CrossRef]

- European Parliament and Council. Directive 2009/72/EC of the European Parliament and of the Council of 13 July 2009 concerning common rules for the internal market in electricity and repealing Directive 2003/54/EC. Off. J. Eur. Union 2009, L211, 55–93. [Google Scholar]

- European Parliament and Council. Directive 2012/27/EU of the European Parliament and of the Council of 25 October 2012 on Energy Efficiency, Amending Directives 2009/125/EC and 2010/30/EU and Repealing Directives 2004/8/EC and 2006/32/EC Text with EEA Relevance; European Parliament and Council: Brussel, Belgium, 2012. [Google Scholar]

- European Parliament and Council. Directive (EU) 2019/944 of the European Parliament and of the Council of 5 June 2019 on Common Rules for the Internal Market for Electricity and Amending Directive 2012/27/EU (Text with EEA Relevance); European Parliament and Council: Brussel, Belgium, 2019. [Google Scholar]

- Poplavskaya, K.; de Vries, L. A (not so) independent aggregator in the balancing market theory, policy and reality check. In Proceedings of the International Conference on the European Energy Market (EEM), Lodz, Poland, 27–29 June 2018; pp. 1–6. [Google Scholar] [CrossRef] [Green Version]

- d’Halluin, P.; Rossi, R.; Schmela, M. European Market Outlook for Residential Battery Storage 2020–2024; SolarPower Europe: Brussels, Belgium, 2020. [Google Scholar]

- European Parliament and Council. Directive (EU) 2018/844 of the European Parliament and of the Council of 30 May 2018 Amending Directive 2010/31/EU on the Energy Performance of Buildings and Directive 2012/27/EU on Energy Efficiency (Text with EEA Relevance). Off. J. Eur. Union 2018, L156, 75–91. [Google Scholar]

- Kantar. Special Eurobarometer 490: Climate Change; European Union: Maastricht, The Netherlands, 2019. [Google Scholar]

- European Commission. A Clean Planet for All. A European Long-Term Strategic Vision for a Prosperous, Modern, Competitive and Climate Neutral Economy; European Commission: Luxembourg, 2018. [Google Scholar]

- Brautigam, A.; Rothacher, T.; Staubitz, H.; Dibitonto, S. The Energy Storage Market in Germany; GTAI: Berlin, Germany, 2019. [Google Scholar]

- Ahi, P.; Searcy, C.; Jaber, M.Y. A Quantitative Approach for Assessing Sustainability Performance of Corporations. Ecol. Econ. 2018, 152, 336–346. [Google Scholar] [CrossRef]

- EESI. Fact Sheet Energy Storage; Environmental and Energy Study Institute: Washington, DC, USA, 2019. [Google Scholar]

- Engelken, M.; Römer, B.; Drescher, M.; Welpe, I.M.; Picot, A. Comparing drivers, barriers, and opportunities of business models for renewable energies: A review. Renew. Sustain. Energy Rev. 2016, 60, 795–809. [Google Scholar] [CrossRef]

- Mauler, L.; Duffner, F.; Cd, W.G.Z.; Leker, J. Battery cost forecasting: A review of methods and results with an outlook to 2050. Energy Environ. Sci. 2021, 14, 4712. [Google Scholar] [CrossRef]

- Espe, E.; Potdar, V.; Chang, E. Prosumer Communities and Relationships in Smart Grids: A Literature Review, Evolution and Future Directions. Energies 2018, 11, 2528. [Google Scholar] [CrossRef] [Green Version]

- Martinez, J.; Ruiz, A.; Puelles, J.; Arechalde, I.; Miadzvetskaya, Y. Smart grid challenges through the lens of the european general data protection regulation. Lect. Notes Inf. Syst. Organ. 2020, 39, 113–130. [Google Scholar] [CrossRef]

- Althaher, S.; Mancarella, P.; Mutale, J. Automated Demand Response from Home Energy Management System under Dynamic Pricing and Power and Comfort Constraints. IEEE Trans. Smart Grid 2015, 6, 1874–1883. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Strengths | Weaknesses |

|

|

| Opportunities | Threats |

|

|

| Significance | Level |

|---|---|

| Critical | 5 |

| High | 4 |

| Medium | 3 |

| Low | 2 |

| Negligible | 1 |

| Probability | Level | Description |

|---|---|---|

| <5% | 1 | Rare |

| ≥5% <25% | 2 | Unlikely |

| ≥25% <65% | 3 | Possible |

| ≥65% <95% | 4 | Likely |

| >95% | 5 | Almost certain |

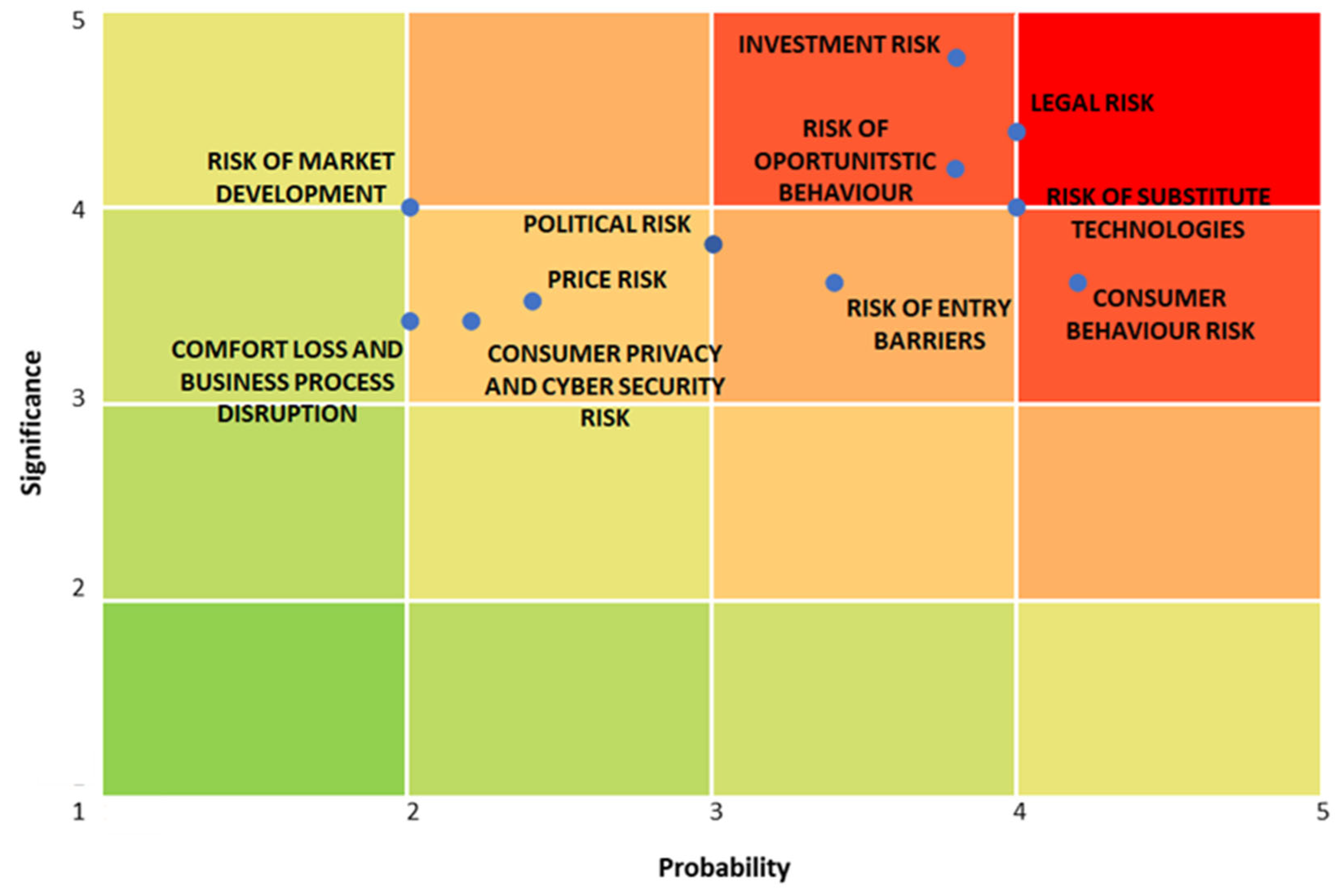

| Type of Risk | Significance | Probability | Risk Value |

|---|---|---|---|

| Investment risk | 4.8 | 3.8 | 18.24 |

| Legal risk | 4.4 | 4 | 17.6 |

| Risk of substitute technologies | 4 | 4 | 16 |

| Risk of aggregators’ opportunistic behavior | 4.2 | 3.8 | 15.96 |

| Consumer behavior risk | 3.6 | 4.2 | 15.12 |

| Risk of entry barriers | 3.6 | 3.4 | 12.24 |

| Political risk | 3.8 | 3 | 11.4 |

| Price risk | 3.5 | 2.4 | 8.4 |

| Risk of market development | 4 | 2 | 8 |

| Consumer privacy and cyber security risk | 3.4 | 2.2 | 7.48 |

| Risk of losing comfort or disrupting business process effectiveness | 3.4 | 2 | 6.8 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zoričić, D.; Knežević, G.; Miletić, M.; Dolinar, D.; Sprčić, D.M. Integrated Risk Analysis of Aggregators: Policy Implications for the Development of the Competitive Aggregator Industry. Energies 2022, 15, 5076. https://doi.org/10.3390/en15145076

Zoričić D, Knežević G, Miletić M, Dolinar D, Sprčić DM. Integrated Risk Analysis of Aggregators: Policy Implications for the Development of the Competitive Aggregator Industry. Energies. 2022; 15(14):5076. https://doi.org/10.3390/en15145076

Chicago/Turabian StyleZoričić, Davor, Goran Knežević, Marija Miletić, Denis Dolinar, and Danijela Miloš Sprčić. 2022. "Integrated Risk Analysis of Aggregators: Policy Implications for the Development of the Competitive Aggregator Industry" Energies 15, no. 14: 5076. https://doi.org/10.3390/en15145076

APA StyleZoričić, D., Knežević, G., Miletić, M., Dolinar, D., & Sprčić, D. M. (2022). Integrated Risk Analysis of Aggregators: Policy Implications for the Development of the Competitive Aggregator Industry. Energies, 15(14), 5076. https://doi.org/10.3390/en15145076