Price Responsiveness of Residential Demand for Natural Gas in the United States

Abstract

:1. Introduction

- KG1: None of the studies considers how price responsiveness has changed over time.

- KG2: None of the studies investigates how price responsiveness differs by season.

- KG3: Little is known about how the parametric specification employed in the study may yield different results. While the critical issue of parametric specification is decades old [36], all 13 studies presume a particular specification (e.g., the double-log or GL) sans consideration of known alternatives like the linear, CES, and TL.

- KG4: None of the studies estimates the impact of cross-section dependence (CD) on the resulting price elasticity estimates.

- KG5: Regional variations in the responsiveness of natural gas to price changes has not been updated recently, as the study by [37] is already 35 years old.

- KG6: None of the studies uses own-price elasticity estimates to quantify natural gas shortage costs, thus overlooking demand response (DR) programs for efficient shortage management.

- (1)

- The US residential demand for natural gas is price inelastic, with statistically significant (p-value ≤ 0.05) estimates of −0.271 to −0.486 for the static own price elasticity, −0.238 to −0.555 for the short run own price elasticity, and −0.323 to −0.796 for the long-run own price elasticity, matching the mid-range estimates of the studies listed in Table A1.

- (2)

- Parametric specification, CD presence, and partial adjustment have statistically significant effects on the own-price elasticity estimates of the US residential natural gas demand.

- (3)

- Erroneously ignoring the highly significant presence of CD tends to shrink the size of the own-price elasticity estimates of the US residential natural gas demand.

- (4)

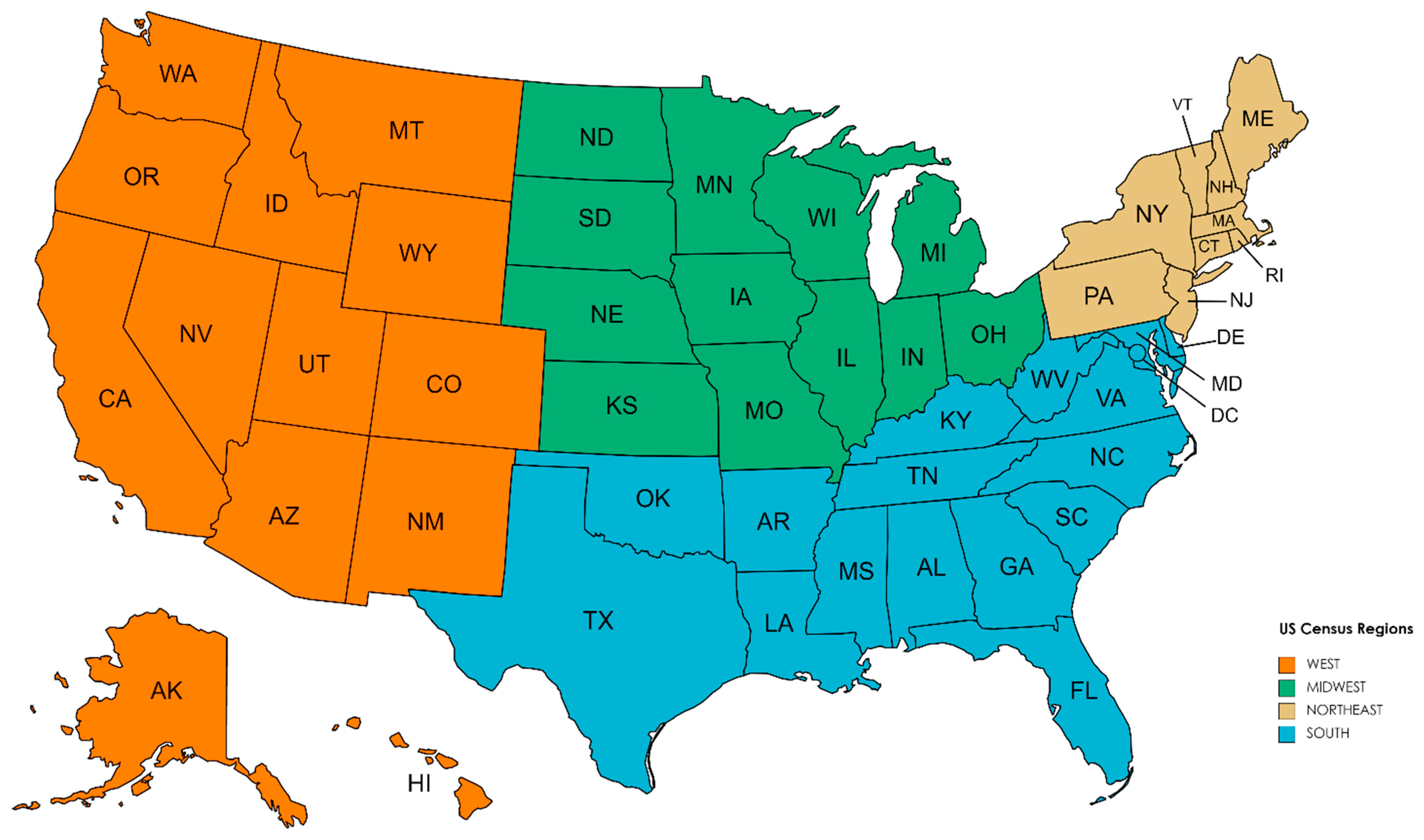

- The US residential natural gas demand’s own-price elasticity estimates vary seasonally and regionally.

- (5)

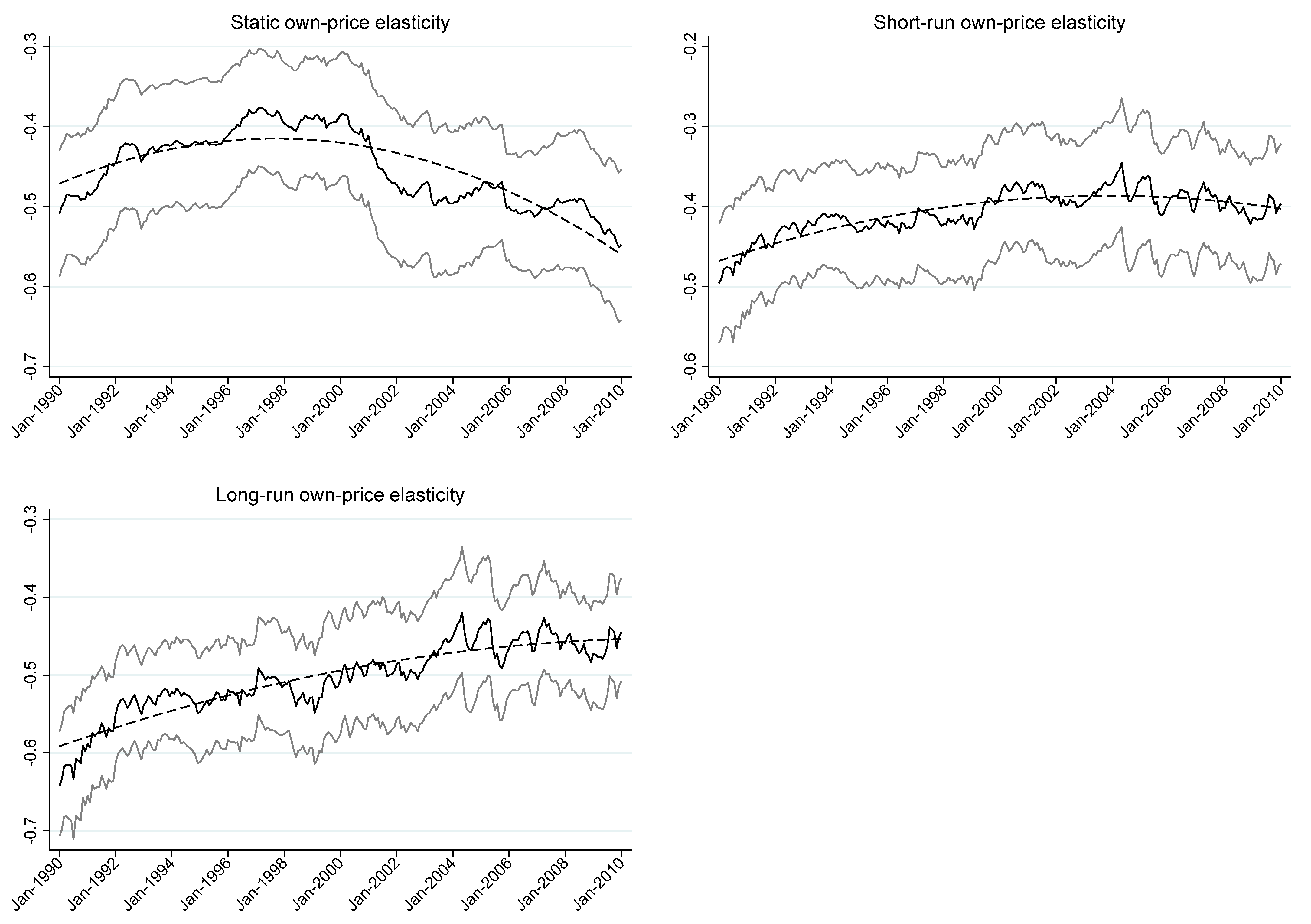

- The US residential natural gas demand’s price responsiveness exhibits a nonlinear time trend.

- (6)

- A hypothetical one-day natural gas shortage that triggers curtailment of 10% of residential demand increases residential energy cost by less than 1%.

2. Materials and Methods

2.1. Nonlinear Pricing of Residential Natural Gas Consumption

2.2. Five Parametric Specifications

2.3. Long-Run Elasticity

2.4. Estimation of Residential Shortage Cost

- (1)

- Consider a one-day shortage of natural gas that triggers curtailment of D% of the residential customer class’s total demand. The size of D is the same for all customer classes if the shortage triggers proportional rationing. However, D may vary by customer class, depending on the established curtailment protocol. For safety and health reasons, the protocol may curtail residential demand relatively less than non-residential demand.

- (2)

- (3)

- Estimate the cost of a one-day shortage of natural gas as a percentage of C:where ΔC = [∂C/∂P1] ΔP1 = Y1 ΔP1 using Shephard’s Lemma [45]. Since (ΔP1/P1) = ΔlnP1, we find:SC = (ΔC/C) ÷ 30 days,SC = (P1 Y1/C) (ΔP1/P1) ÷ 30 days = −S (D/ε) ÷ 30 days.

2.5. Data Description

2.6. Estimation Strategy

- (1)

- Test for CD in the variables using the test developed by [50].

- (2)

- Determine whether the variables are non-stationarity using the [51] panel unit root test that accounts for CD.

- (3)

- For each parametric specification, estimate the coefficients of Equation (13) with IV and non-IV estimation for the four cases formed by (a) φ = 0 vs. φ > 0; and (b) CD presence vs. CD absence. The instruments for the current month’s price-ratio are the lagged price ratios in the prior three months (The lagged price ratios in month t are pre-determined variables as they use average prices based on billing data in the prior three months. As the lagged price ratios are suitable instruments as they are highly correlated with the current price ratio (r ≥ 0.8)).

- (4)

- For each parametric specification, use the Durbin-Wu-Hausman test [52] to determine if current price ratios are endogenous and whether IV estimation is necessary.

3. Results

3.1. Tests of Cross-Section Independence and Non-Stationary Variables

3.2. General Observations

3.3. Regression Details

3.4. Seasonal Pattern of Own-Price Elasticity Estimates

3.5. Factors Affecting the US Residential Demand’s Empirical Price Responsiveness

3.6. Time Trend of Own-Price Elasticity Estimates

3.7. Residential Shortage Costs

3.8. Final Checks

4. Conclusions and Policy Implications

4.1. Conclusions

4.2. Policy Implications

4.3. Limitations and Future Research

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

| Study | Sample Period | Regional Coverage | Data Type | Data Frequency | Non−NG Energy Prices | Parametric Specification | Estimation Method | Static | Short Run | Long Run |

|---|---|---|---|---|---|---|---|---|---|---|

| Beierlein et al. (1981) [56] | 1967–1977 | Nine Northeast states | Panel | Annual | Electricity, fuel oil | Double-log with partial adjustment | Error components—seemingly unrelated regressions | −0.353 | −3.440 | |

| Barnes et al. (1982) [57] | 1972–1973 Consumer expenditure survey | The US | Cross section | Annual | None | Double-log | Instrumental variable estimation | −0.68 | ||

| Blattenberger et al. (1983) [58] | 1960–1974 | The US | Panel | Annual | Electricity | Double-log with partial adjustment | Cross-section/time-series regressions | −0.049 to −0.32 | −0.264 to −0.393 | |

| Liu (1983) [59] | 1967–1978 | The US | Time series | Annual | Electricity, fuel oil | Double-log | OLS | −0.318 to −0.490 | ||

| Lin et al. (1987) [37] | 1967–1983 | Nine regions of the US | Panel | Annual | Electricity, fuel oil | Double-log with partial adjustment | Error components-seemingly unrelated regressions | −0.154 | −1.215 | |

| Garcia−Cerruti (2000) [60] | 1983–1997 | 44 counties of California | Panel | Annual | Electricity | Double-log with partial adjustment | Dynamic random variables models | −0.041 to −0.071 | −0.53 to −0.193 | |

| Bernstein and Griffin (2005) [61] | 1997–2003 | Lower 48 states | Panel | Annual | Electricity | Double-log with partial adjustment | Panel data analysis with fixed effects | −0.12 | −0.36 | |

| Payne et al. (2011) [62] | 1970–2007 | Illinois | Time series | Annual | Electricity | Linear | Error correction model with autoregressive distributed lag | −0.185 | −0.264 | |

| Lavin et al. (2011) [54] | Residential Energy Consumption Survey for 1993 | The US | Cross section | Annual | Electricity | Double-log and linear | −0.007 to −0.72 | |||

| Charles (2016) [28] | 2001–2014 | Lower 48 states | Panel | Monthly | Electricity | Double-log with and without partial adjustment | OLS with fixed effects | −0.297 | −0.211 | −0.360 |

| Auffhammer and Rubin (2018) [39] | 2003–2014 | California | Panel | Monthly | None | Double-log | Instrumental variable estimation | −0.17 to −0.23 | ||

| Gautam and Paudel (2018) [63] | 1997–2011 | Nine Northeast states | Panel | Annual | Electricity, fuel oil | Double-log with autoregressive distributed lag | Pooled Mean Group (PMG) and Dynamic Fixed Effects (DFE) | −0.061 | −0.200 | |

| Woo et al. (2018b) [3] | 2001–2016 | Lower 48 states | Panel | Monthly | Electricity, fuel oil | Generalized Leontief (GL) system of energy intensities with and without partial adjustment | Iterated seemingly unrelated regressions | −0.455 | −0.271 | −0.684 |

| Burns (2021) [64] | 1970–2016 | The US | Time series | Annual | None | Double-log with time-varying elasticities | Maximum likelihood with Kalman filter | −0.08 to −0.18 |

References

- British Petroleum. Statistical Review of World Energy. 2021. Available online: https://www.bp.com/en/global/corporate/energy-economics/statistical-review-of-world-energy.html (accessed on 22 April 2022).

- Gillingham, K.; Huang, P. Is abundant natural gas a bridge to a low-carbon future or a dead-end? Energy J. 2019, 40, 1–26. [Google Scholar] [CrossRef] [Green Version]

- Woo, C.K.; Shiu, A.; Liu, Y.; Luo, X.; Zarnikau, J. Consumption effects of an electricity decarbonization policy: Hong Kong. Energy 2018, 144, 887–902. [Google Scholar] [CrossRef]

- Mahone, A.; Subin, Z.; Orans, R.; Miller, M.; Regan, L.; Calviou, M.; Saenz, M.; Bacalao, N. On the path of decarbonization. IEEE Power Energy Mag. 2018, 16, 58–68. [Google Scholar] [CrossRef]

- Williams, J.H.; DeBenedictis, A.; Ghanadan, R.; Mahone, A.; Moore, J.; Morrow, W.R.; Price, S.; Torn, M.S. The Technology Path to Deep Greenhouse Gas Emissions Cuts by 2050: The Pivotal Role of Electricity. Science 2012, 335, 53–59. [Google Scholar] [CrossRef] [Green Version]

- Zarnikau, J.; Woo, C.; Zhu, S.; Tsai, C. Market price behavior of wholesale electricity products: Texas. Energy Policy 2018, 125, 418–428. [Google Scholar] [CrossRef]

- Li, R.; Woo, C.K.; Tishler, A.; Zarnikau, J. How price responsive is industrial natural gas demand in the US? Util. Policy 2022, 74, 101318. [Google Scholar] [CrossRef]

- Tishler, A.; Lipovesky, S. The flexible CES-GBC family of cost functions: Derivation and application. Rev. Econ. Stat. 1997, 79, 638–646. [Google Scholar] [CrossRef]

- Gillingham, K.; Newell, R.G.; Palmer, K. Energy efficiency economics and policy. Annu. Rev. Resour. Econ. 2009, 1, 597–620. [Google Scholar] [CrossRef]

- Al-Sahlawi, M.A. The demand for natural gas: A survey of price and income elasticities. Energy J. 1989, 10, 77–90. [Google Scholar] [CrossRef]

- Bohi, D.R.; Zimmerman, M.B. An Update on Econometric Studies of Energy Demand Behavior. Annu. Rev. Energy 1984, 9, 105–154. [Google Scholar] [CrossRef]

- Hausman, J.A. Project Independence Report: An Appraisal of U.S. Energy Needs up to 1985. Bell J. Econ. 1975, 6, 517–551. [Google Scholar] [CrossRef]

- Manne, A.S.; Richels, R.G.; Weyant, J.P. Feature article—Energy policy modeling: A survey. Oper. Res. 1979, 27, 1–36. [Google Scholar] [CrossRef] [Green Version]

- Abrell, J.; Weigt, H. Investments in a combined energy network model: Substitution between natural gas and electricity? Energy J. 2016, 37, 63–86. [Google Scholar] [CrossRef]

- Çalci, B.; Leibowicz, B.D.; Bard, J.F. North American Natural Gas Markets Under LNG Demand Growth and Infrastructure Restrictions. Energy J. 2022, 43, 1–24. [Google Scholar] [CrossRef]

- Holz, F.; Richter, P.M.; Egging, R. The Role of Natural Gas in a Low-Carbon Europe: Infrastructure and Supply Security. Energy J. 2016, 37, 33–59. [Google Scholar] [CrossRef]

- Logan, J.; Lopez, A.; Mai, T.; Davidson, C.; Bazilian, M.; Arent, D. Natural gas scenarios in the U.S. power sector. Energy Econ. 2013, 40, 183–195. [Google Scholar] [CrossRef]

- Bianco, V.; Scarpa, F.; Tagliafico, L.A. Scenario analysis of nonresidential natural gas consumption in Italy. Appl. Energy 2014, 113, 392–403. [Google Scholar] [CrossRef]

- Dilaver, Ö.; Dilaver, Z.; Hunt, L.C. What drives natural gas consumption in Europe? Analysis and projections. J. Nat. Gas Sci. Eng. 2014, 19, 125–136. [Google Scholar] [CrossRef]

- Huntington, H.G. Industrial natural gas consumption in the United States: An empirical model for evaluating future trends. Energy Econ. 2007, 29, 743–759. [Google Scholar] [CrossRef]

- Xiang, D.; Lawley, C. The impact of British Columbia’s carbon tax on residential natural gas consumption. Energy Econ. 2019, 80, 206–218. [Google Scholar] [CrossRef]

- Rowland, C.S.; Mjelde, J.W.; Dharmasena, S. Policy implications of considering pre-commitments in U.S. aggregate energy demand system. Energy Policy 2017, 102, 406–413. [Google Scholar] [CrossRef]

- Brown, M.; Siddiqui, S.; Avraam, C.; Bistline, J.; Decarolis, J.; Eshraghi, H.; Giarola, S.; Hansen, M.; Johnston, P.; Khanal, S.; et al. North American energy system responses to natural gas price shocks. Energy Policy 2020, 149, 112046. [Google Scholar] [CrossRef]

- Gong, C.; Tang, K.; Zhu, K.; Hailu, A. An optimal time-of-use pricing for urban gas: A study with a multi-agent evolutionary game-theoretic perspective. Appl. Energy 2015, 163, 283–294. [Google Scholar] [CrossRef]

- Lee, J.-D.; Kim, T.-Y. Ex-ante analysis of welfare change for a liberalization of the natural gas market. Energy Econ. 2004, 26, 447–461. [Google Scholar] [CrossRef]

- Alcaraza, C.; Villalvazo, S. The effect of natural gas shortages on the Mexican economy. Energy Econ. 2017, 66, 147–153. [Google Scholar] [CrossRef] [Green Version]

- Leahy, E.; Devitt, C.; Lyons, S.; Tol, R.S. The cost of natural gas shortages in Ireland. Energy Policy 2012, 46, 153–169. [Google Scholar] [CrossRef] [Green Version]

- Charles, R.K.M. Regional Estimates of the Price Elasticity of Demand for Natural Gas in the United States. Master’s Thesis, Massachusetts Institute of Technology, Cambridge, MA, USA, 2016. Available online: https://dspace.mit.edu/handle/1721.1/104830 (accessed on 22 April 2022).

- Dahl, C. A Survey of Energy Demand Elasticities in Support of the Development of the NEMS; Colorado School of Mines: Golden, CO, USA, 1993. [Google Scholar]

- Dahl, C.; Roman, C. Energy Demand Elasticities—Fact or Fiction: A Survey; Colorado School of Mines: Golden, CO, USA, 2004. [Google Scholar]

- Hartman, R.S. Frontiers in Energy Demand Modeling. Annu. Rev. Energy 1979, 4, 433–466. [Google Scholar] [CrossRef] [Green Version]

- Huntington, H.G.; Barrios, J.J.; Arora, V. Review of key international demand elasticities for major industrializing economies. Energy Policy 2019, 133, 110878. [Google Scholar] [CrossRef] [Green Version]

- Labandeira, X.; Labeaga, J.M.; López-Otero, X. A meta-analysis on the price elasticity of energy demand. Energy Policy 2017, 102, 549–568. [Google Scholar] [CrossRef] [Green Version]

- Suganthia, L.; Samuel, A.A. Energy models for demand forecasting—A review. Renew. Sustain. Energy Rev. 2012, 16, 1223–1240. [Google Scholar] [CrossRef]

- Taylor, L.D. The demand for energy: A survey of price and income elasticities. In International Studies of the Demand for Energy; Nordhaus, W., Ed.; North Holland: Amsterdam, The Netherlands, 1977. [Google Scholar]

- Baxter, R.E.; Rees, R. Analysis of the Industrial Demand for Electricity. Econ. J. 1968, 78, 277–298. [Google Scholar] [CrossRef]

- Lin, W.T.; Chen, Y.H.; Chatov, R. The demand for natural gas, electricity and heating oil in the United States. Resour. Energy 1987, 9, 233–258. [Google Scholar] [CrossRef]

- Li, R.; Woo, C.K.; Cox, K. How price-responsive is residential retail electricity demand in the US? Energy 2021, 232, 120921. [Google Scholar] [CrossRef]

- Auffhammer, M.; Rubin, E. Natural Gas Price Elasticities and Optimal Cost Recovery under Consumer Heterogeneity: Evidence from 300 Million Natural Gas Bills. NBER Working Paper 24295. 2018. Available online: https://www.nber.org/papers/w24295 (accessed on 22 April 2022).

- Davidson, R.; Mackinnon, J.G. Estimation and Inference in Econometrics; Oxford University Press: Oxford, UK, 1993. [Google Scholar]

- Dubin, J.A.; Henson, S.E. An engineering/econometric analysis of seasonal energy demand and conservation in the Pacific Northwest. J. Bus. Econ. Stat. 1988, 6, 121–134. [Google Scholar]

- Woo, C.; Tishler, A.; Zarnikau, J.; Chen, Y. Average residential outage cost estimates for the lower 48 states in the US. Energy Econ. 2021, 98, 105270. [Google Scholar] [CrossRef]

- Diewert, W.E. An Application of the Shephard Duality Theorem: A Generalized Leontief Production Function. J. Political Econ. 1971, 79, 481–507. [Google Scholar] [CrossRef]

- Woo, C.K. Managing water supply shortage: Interruption vs. pricing. J. Public Econ. 1994, 54, 145–160. [Google Scholar] [CrossRef]

- Varian, H. Microeconomics Analysis; Norton: New York, NY, USA, 1992. [Google Scholar]

- Woo, C.; Tishler, A.; Zarnikau, J.; Chen, Y. A back of the envelope estimate of the average non-residential outage cost in the US. Electr. J. 2021, 34, 106930. [Google Scholar] [CrossRef]

- Chudik, A.; Pesaran, M.H. Common correlated effects estimation of heterogeneous dynamic panel data models with weakly exogenous regressors. J. Econ. 2015, 188, 393–420. [Google Scholar] [CrossRef] [Green Version]

- Pesaran, M.H. Estimation and inference in large heterogeneous panels with a multifactor error structure. Econometrica 2006, 74, 967–1012. [Google Scholar] [CrossRef] [Green Version]

- Pesaran, M.H.; Smith, R. Estimating long-run relationships from dynamic heterogeneous panels. J. Econom. 1995, 68, 79–113. [Google Scholar] [CrossRef]

- Pesaran, M.H. General diagnostic tests for cross-sectional dependence in panels. Empir. Econ. 2020, 60, 13–50. [Google Scholar] [CrossRef]

- Pesaran, M.H. A simple panel unit root test in the presence of cross-section dependence. J. Appl. Econom. 2007, 22, 265–312. [Google Scholar] [CrossRef] [Green Version]

- Wooldridge, J.M. Econometric Analysis of Cross Section and Panel Data; MIT Press: Cambridge, MA, USA, 2010. [Google Scholar]

- Baltagi, B.H.; Kao, C. Nonstationary panels, cointegration in panels and dynamic panels: A survey. In Nonstationary Panels, Panel Cointegration, and Dynamic Panels; Baltagi, B.H., Fomby, T.B., Carter Hill, R., Eds.; Advances in Econometrics; Emerald Group Publishing Limited: Bingley, UK, 2001; Volume 15, pp. 7–51. [Google Scholar]

- Lavín, F.V.; Dale, L.; Hanemann, M.; Moezzi, M. The impact of price on residential demand for electricity and natural gas. Clim. Chang. 2011, 109, 171–189. [Google Scholar] [CrossRef]

- Woo, C.; Sreedharan, P.; Hargreaves, J.; Kahrl, F.; Wang, J.; Horowitz, I. A review of electricity product differentiation. Appl. Energy 2014, 114, 262–272. [Google Scholar] [CrossRef]

- Beierlein, J.G.; Dunn, J.W.; McConnon, J.C. The demand for electricity and natural gas in the Northern United States. Rev. Econ. Stat. 1981, 63, 403–408. [Google Scholar] [CrossRef]

- Barnes, R.; Gillingham, R.; Hagemann, R. The short-run residential demand for natural gas. Energy J. 1982, 3, 59–72. [Google Scholar] [CrossRef]

- Blattenberger, G.R.; Taylor, L.D.; Rennhack, R. Natural Gas Availability and the Residential Demand for Energy. Energy J. 1983, 4, 23–45. [Google Scholar] [CrossRef]

- Liu, B.-C. Natural gas price elasticities: Variations by region and by sector in the USA. Energy Econ. 1983, 5, 195–201. [Google Scholar] [CrossRef]

- Garcia-Cerritti, L.M. Estimating elasticities of residential energy demand from panel county data using dynamic random variables models with heteroskedastic and correlated error terms. Resour. Energy Econ. 2000, 22, 355–366. [Google Scholar] [CrossRef]

- Bernstein, M.A.; Griffin, J. Regional Differences in the Price-Elasticity of Demand for Energy; Rand Corporation: Santa Monica, CA, USA, 2005. [Google Scholar]

- Payne, J.E.; Loomis, D.; Wilson, R. Residential natural gas demand in Illinois: Evidence from the ARDL bounds testing approach. J. Reg. Anal. Policy 2011, 41, 138–147. [Google Scholar]

- Gautam, T.K.; Paudel, K.P. The demand for natural gas in the Northeastern United States. Energy 2018, 158, 890–898. [Google Scholar] [CrossRef]

- Burns, K. An investigation into changes in the elasticity of U.S. residential natural gas consumption: A time-varying approach. Energy Econ. 2021, 99, 105253. [Google Scholar] [CrossRef]

- Bartels, R.; Fiebig, D.; Plumb, M.H. Gas or electricity, which is cheaper? An econometric approach with application to Australian expenditure data. Energy J. 1996, 17, 33–77. [Google Scholar] [CrossRef]

- Wadud, Z.; Dey, H.S.; Kabir, M.A.; Khan, S.I. Modeling and forecasting natural gas demand in Bangladesh. Energy Policy 2011, 39, 7372–7380. [Google Scholar] [CrossRef] [Green Version]

- Berndt, E.R.; Watkins, G.C. Demand for Natural Gas: Residential and Commercial Markets in Ontario and British Columbia. Can. J. Econ. 1977, 10, 97–111. [Google Scholar] [CrossRef]

- Hu, W.; Ho, M.S.; Cao, J. Energy consumption of urban households in China. China Econ. Rev. 2019, 58, 101343. [Google Scholar] [CrossRef]

- Li, L.; Luo, X.; Zhou, K.; Xu, T. Evaluation of increasing block pricing for households’ natural gas: A case study of Beijing, China. Energy 2018, 157, 162–172. [Google Scholar] [CrossRef]

- Zeng, S.; Chen, Z.-M.; Alsaedi, A.; Hayat, T. Price elasticity, block tariffs, and equity of natural gas demand in China: Investigation based on household-level survey data. J. Clean. Prod. 2018, 179, 441–449. [Google Scholar] [CrossRef]

- Zhang, Y.; Ji, Q.; Fan, Y. The price and income elasticity of China’s natural gas demand: A multi-sectoral perspective. Energy Policy 2018, 113, 332–341. [Google Scholar] [CrossRef]

- Ackah, I. Determinants of natural gas demand in Ghana. OPEC Energy Rev. 2014, 38, 272–295. [Google Scholar] [CrossRef] [Green Version]

- Kostakis, I.; Lolos, S.; Sardianou, E. Residential natural gas demand: Assessing the evidence from Greece using pseudo-panels, 2012–2019. Energy Econ. 2021, 99, 105301. [Google Scholar] [CrossRef]

- Ota, T.; Kakinaka, M.; Kotani, K. Demographic effects on residential electricity and city gas consumption in the aging society of Japan. Energy Policy 2018, 115, 503–513. [Google Scholar] [CrossRef] [Green Version]

- Lim, C. Estimating Residential and Industrial City Gas Demand Function in the Republic of Korea—A Kalman Filter Application. Sustainability 2019, 11, 1363. [Google Scholar] [CrossRef] [Green Version]

- Yoo, S.-H.; Lim, H.-J.; Kwak, S.-J. Estimating the residential demand function for natural gas in Seoul with correction for sample selection bias. Appl. Energy 2009, 86, 460–465. [Google Scholar] [CrossRef]

- Kahn, M.A. Modelling and forecasting the demand for natural gas in Pakistan. Renew. Sustain. Energy Rev. 2015, 49, 1145–1159. [Google Scholar] [CrossRef]

- Erdogdu, E. Natural gas demand in Turkey. Appl. Energy 2010, 87, 211–219. [Google Scholar] [CrossRef] [Green Version]

- Alberini, A.; Khymych, O.; Ščasný, M. Responsiveness to energy price changes when salience is high: Residential natural gas demand in Ukraine. Energy Policy 2020, 144, 111534. [Google Scholar] [CrossRef]

- Asche, F.; Nilsen, O.B.; Tveteras, R. Natural gas demand in the European household sector. Energy J. 2005, 29, 27–46. [Google Scholar] [CrossRef] [Green Version]

- Estrada, J.; Fugleberg, O. Price Elasticities of Natural Gas Demand in France and West Germany. Energy J. 1989, 10, 77–90. [Google Scholar] [CrossRef]

- Bernstein, R.; Madlener, R. Residential Natural Gas Demand Elasticities in OECD Countries: An ARDL Bounds Testing Approach. 2011. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2078036 (accessed on 22 April 2022).

- Burke, P.J.; Yang, H. The price and income elasticities of natural gas demand: International evidence. Energy Econ. 2016, 59, 466–474. [Google Scholar] [CrossRef] [Green Version]

| Study | Short Run | Long Run |

|---|---|---|

| Gillingham et al. (2009) [9] | −0.14 to −0.44 | −0.32 to −1.89 |

| Al-Sahlawi (1989) [10] | −0.05 to −0.68 | −1.06 to −3.42 |

| Bohi and Zimmerman (1984) [11] | −0.05 to −0.60 | −0.26 to −3.17 |

| Variable (Source) | Definition | Mean | Standard Deviation | Minimum | Maximum | Correlation with Y1 |

|---|---|---|---|---|---|---|

| Y1 (EIA and BLS) | Per capita consumption of natural gas (Mcf) | 1.77 | 1.69 | 0.02 | 11.61 | 1.0 |

| Y3 (EIA and BLS) | Per capita consumption of electricity (kWh) | 618.40 | 956.64 | 21.47 | 11,598.17 | −0.044 |

| P1 (EIA) | Natural gas price ($/Mcf) | 11.10 | 4.89 | 2.42 | 41.56 | −0.247 |

| P2 (EIA) | Fuel oil price ($/gallon) | 1.56 | 0.96 | 0.34 | 4.34 | −0.057 |

| P3 (EIA) | Electricity price ($/kWh) | 0.010 | 0.003 | 0.00 | 0.02 | −0.122 |

| P1/P3 | Natural gas—electricity price ratio | 1138.66 | 431.51 | 364.46 | 4664.42 | −0.144 |

| P2/P3 | Fuel oil—electricity price ratio | 154.44 | 84.37 | 27.57 | 574.36 | 0.002 |

| X (BLS) | Per capita industrial employment | 0.59 | 0.05 | 0.43 | 0.83 | 0.115 |

| CDD (NOAA) | Cooling degree days | 91.01 | 144.01 | 0 | 761 | −0.458 |

| HDD (NOAA) | Heating degree days | 435.19 | 422.63 | 0 | 2111 | 0.824 |

| Variable | H0: Cross-Section Independence | H0: Non-Stationarity |

|---|---|---|

| Y1 | 584.87 (0.000) | −6.120 (0.000) |

| P1/P3 | 459.84 (0.000) | −5.132 (0.000) |

| P2/P3 | 614.44 (0.000) | −4.643 (0.000) |

| X | 401.97 (0.000) | −3.403 (0.000) |

| CDD | 569.56 (0.000) | −6.190 (0.000) |

| HDD | 605.90 (0.000) | −6.190 (0.000) |

| Variable | CD Presence | CD Absence | |||

|---|---|---|---|---|---|

| IV Estimation: No | IV Estimation: Yes | IV Estimation: No | IV Estimation: Yes | ||

| Panel A.1: Double-log specification without partial adjustment | |||||

| RMSE | 0.12 | 0.12 | 0.23 | 0.23 | |

| Adjusted R2 | 0.98 | 0.99 | 0.92 | 0.92 | |

| ln(P1/P3) = ln(natural gas price/electricity price) | −0.396 | −0.334 | −0.326 | −0.507 | |

| ln(P2/P3) = ln(fuel oil price/electricity price) | 0.309 | 0.262 | −0.013 | 0.046 | |

| X = per capita employment | −0.419 | −0.326 | 1.203 | 2.068 | |

| CDD = cooling degree days | 0.000 | 0.000 | −0.001 | −0.001 | |

| HDD = heating degree days | 0.001 | 0.001 | 0.002 | 0.002 | |

| Static own-price elasticity | −0.396 | −0.334 | −0.326 | −0.507 | |

| p-value for testing H0: CD is absent | − | − | 0.000 | 0.000 | |

| p-value for testing H0: natural gas price ratio data are exogeneous | 0.995 | 0.017 | |||

| Panel A.2: Double-log specification with partial adjustment | |||||

| RMSE | 0.09 | 0.09 | 0.15 | 0.15 | |

| Adjusted R2 | 0.99 | 0.99 | 0.97 | 0.97 | |

| ln(P1/P3) = ln(natural gas price/electricity price) | −0.336 | −0.013 | −0.167 | 0.019 | |

| ln(P2/P3) = ln(fuel oil price/electricity price) | 0.186 | 0.029 | −0.017 | −0.076 | |

| X = per capita employment | 0.171 | 0.045 | 1.446 | 0.641 | |

| CDD = cooling degree days | 0.000 | 0.000 | −0.001 | −0.001 | |

| HDD = heating degree days | 0.001 | 0.001 | 0.002 | 0.002 | |

| Lagged lnY1 | 0.271 | 0.296 | 0.308 | 0.316 | |

| Short-run own-price elasticity | −0.336 | −0.013 | −0.167 | 0.019 | |

| Long-run own-price elasticity | −0.460 | −0.018 | −0.242 | 0.028 | |

| p-value for testing H0: CD is absent | − | − | 0.000 | 0.000 | |

| p-value for testing H0: natural gas price ratio data are exogeneous | 0.352 | 0.000 | |||

| Panel B.1: Linear specification without partial adjustment | |||||

| RMSE | 0.00 | 0.00 | 0.00 | 0.00 | |

| Adjusted R2 | 0.98 | 0.98 | 0.93 | 0.93 | |

| (P1/P3) = (natural gas price/electricity price) | −0.0002 | −0.0003 | 0.0000 | −0.0003 | |

| (P2/P3) = (fuel oil price/electricity price) | 0.0013 | 0.0017 | −0.0011 | −0.0005 | |

| X = per capita employment | 0.0000 | 0.0001 | −0.0016 | −0.0001 | |

| CDD = cooling degree days | 0.0000 | 0.0000 | 0.0000 | 0.0000 | |

| HDD = heating degree days | 0.0000 | 0.0000 | 0.0000 | 0.0000 | |

| Static own-price elasticity | −0.486 | −0.684 | 0.018 | −0.651 | |

| p-value for testing H0: CD is absent | − | − | 0.000 | 0.000 | |

| p-value for testing H0: natural gas price ratio data are exogeneous | 0.617 | 0.042 | |||

| Panel B.2: Linear specification with partial adjustment | |||||

| RMSE | 0.00 | 0.00 | 0.00 | 0.00 | |

| Adjusted R2 | 0.99 | 0.99 | 0.97 | 0.97 | |

| (P1/P3) = (natural gas price/electricity price) | −0.0002 | −0.0001 | 0.0001 | 0.0001 | |

| (P2/P3) = (fuel oil price/electricity price) | 0.0012 | 0.0009 | −0.0009 | −0.0010 | |

| X = per capita employment | −0.0002 | −0.0004 | 0.0001 | 0.0000 | |

| CDD = cooling degree days | 0.0000 | 0.0000 | 0.0000 | 0.0000 | |

| HDD = heating degree days | 0.0000 | 0.0000 | 0.0000 | 0.0000 | |

| Lagged Y1 | 0.303 | 0.304 | 0.299 | 0.301 | |

| Short-run own-price elasticity | −0.555 | −0.337 | 0.177 | 0.262 | |

| Long-run own-price elasticity | −0.796 | −0.485 | 0.253 | 0.375 | |

| p-value for testing H0: CD is absent | − | − | 0.000 | 0.000 | |

| p-value for testing H0: natural gas price ratio data are exogeneous | 0.437 | 0.591 | |||

| Panel C.1: CES specification without partial adjustment | |||||

| RMSE | 0.13 | 0.13 | 0.26 | 0.26 | |

| Adjusted R2 | 0.98 | 0.98 | 0.91 | 0.91 | |

| ln(P1/P3) = ln(natural gas price/electricity price) | −0.354 | −0.277 | −0.518 | −0.627 | |

| X = per capita employment | −0.765 | −0.756 | 1.182 | 1.564 | |

| CDD = cooling degree days | −0.001 | −0.001 | −0.003 | −0.003 | |

| HDD = heating degree days | 0.001 | 0.001 | 0.001 | 0.001 | |

| Static own-price elasticity | −0.271 | −0.212 | −0.396 | −0.480 | |

| p-value for testing H0: CD is absent | − | − | 0.000 | 0.000 | |

| p-value for testing H0: natural gas price ratio data are exogeneous | 0.672 | 0.186 | |||

| Panel C.2: CES specification with partial adjustment | |||||

| RMSE | 0.10 | 0.10 | 0.18 | 0.18 | |

| Adjusted R2 | 0.99 | 0.99 | 0.96 | 0.96 | |

| ln(P1/P3) = ln(natural gas price/electricity price) | −0.311 | −0.016 | −0.284 | −0.132 | |

| X = per capita employment | 0.014 | −0.218 | 1.135 | 0.713 | |

| CDD = cooling degree days | −0.001 | −0.001 | −0.003 | −0.003 | |

| HDD = heating degree days | 0.001 | 0.001 | 0.001 | 0.001 | |

| Lagged lnY1 | 0.263 | 0.290 | 0.327 | 0.340 | |

| Short-run own-price elasticity | −0.238 | −0.012 | −0.217 | −0.101 | |

| Long-run own-price elasticity | −0.323 | −0.017 | −0.323 | −0.153 | |

| p-value for testing H0: CD is absent | − | − | 0.000 | 0.000 | |

| p-value for testing H0: natural gas price ratio data are exogeneous | 0.100 | 0.769 | |||

| Panel D.1: GL specification without partial adjustment | |||||

| RMSE | 0.00 | 0.00 | 0.00 | 0.00 | |

| Adjusted R2 | 0.98 | 0.98 | 0.93 | 0.93 | |

| (P2/P1)1/2 = (fuel oil price/natural gas price) 1/2 | 0.0001 | 0.0002 | 0.0004 | 0.0008 | |

| (P3/P1)1/2 = (electricity price/natural gas price) 1/2 | 0.0010 | 0.0008 | −0.0010 | −0.0010 | |

| X = per capita employment | −0.0003 | 0.0004 | −0.0015 | −0.0005 | |

| CDD = cooling degree days | 0.0000 | 0.0000 | 0.0000 | 0.0000 | |

| HDD = heating degree days | 0.0000 | 0.0000 | 0.0000 | 0.0000 | |

| Static own-price elasticity | −0.453 | −0.427 | −0.041 | −0.408 | |

| p-value for testing H0: CD is absent | − | − | 0.000 | 0.000 | |

| p-value for testing H0: natural gas price ratio data are exogeneous | 0.117 | 0.065 | |||

| Panel D.2: GL specification with partial adjustment | |||||

| RMSE | 0.00 | 0.00 | 0.00 | 0.00 | |

| Adjusted R2 | 0.99 | 0.99 | 0.97 | 0.97 | |

| (P2/P1)1/2 = (fuel oil price/natural gas price) 1/2 | 0.0003 | −0.0008 | 0.0001 | 0.0001 | |

| (P3/P1)1/2 = (electricity price/natural gas price) 1/2 | 0.0007 | 0.0029 | −0.0008 | −0.0008 | |

| X = per capita employment | −0.0001 | −0.0012 | 0.0000 | −0.0001 | |

| CDD = cooling degree days | 0.0000 | 0.0000 | 0.0000 | 0.0000 | |

| HDD = heating degree days | 0.0000 | 0.0000 | 0.0000 | 0.0000 | |

| Lagged Y1 | 0.305 | 0.297 | 0.295 | 0.297 | |

| Short-run own-price elasticity | −0.453 | −0.237 | 0.138 | 0.206 | |

| Long-run own-price elasticity | −0.651 | −0.336 | 0.197 | 0.293 | |

| p-value for testing H0: CD is absent | − | − | 0.000 | 0.000 | |

| p-value for testing H0: natural gas price ratio data are exogeneous | 0.763 | 0.234 | |||

| Panel E.1: TL specification without partial adjustment | |||||

| RMSE | 0.02 | 0.02 | 0.04 | 0.04 | |

| Adjusted R2 | 0.97 | 0.98 | 0.87 | 0.87 | |

| ln(P1/P3) = ln(natural gas price/electricity price) | 0.087 | 0.093 | 0.101 | 0.074 | |

| ln(P2/P3) = ln(fuel oil price/electricity price) | 0.010 | 0.008 | −0.021 | −0.012 | |

| X = per capita employment | −0.134 | −0.134 | 0.118 | 0.252 | |

| CDD = cooling degree days | −0.0001 | −0.0001 | −0.0003 | −0.0003 | |

| HDD = heating degree days | 0.0001 | 0.0001 | 0.0002 | 0.0002 | |

| Static own-price elasticity | 0.377 | 0.459 | 0.562 | 0.207 | |

| p-value for testing H0: CD is absent | − | − | 0.000 | 0.000 | |

| p-value for testing H0: natural gas price ratio data are exogeneous | 0.684 | 0.393 | |||

| Panel E.2: TL specification with partial adjustment | |||||

| RMSE | 0.02 | 0.02 | 0.03 | 0.03 | |

| Adjusted R2 | 0.98 | 0.98 | 0.95 | 0.95 | |

| ln(P1/P3) = ln(natural gas price/electricity price) | 0.075 | 0.061 | 0.080 | 0.094 | |

| ln(P2/P3) = ln(fuel oil price/electricity price) | 0.007 | 0.015 | −0.016 | −0.020 | |

| X = per capita employment | 0.021 | 0.034 | 0.099 | 0.039 | |

| CDD = cooling degree days | −0.0001 | −0.0001 | −0.0002 | −0.0002 | |

| HDD = heating degree days | 0.0001 | 0.0001 | 0.0002 | 0.0002 | |

| Lagged lnY1 | 0.344 | 0.361 | 0.396 | 0.390 | |

| Short-run own-price elasticity | 0.223 | 0.043 | 0.294 | 0.480 | |

| Long-run own-price elasticity | 0.340 | 0.068 | 0.487 | 0.788 | |

| p-value for testing H0: CD is absent | − | − | 0.000 | 0.000 | |

| p-value for testing H0: natural gas price ratio data are exogeneous | 0.766 | 0.005 | |||

| Panel F. Seasonal pattern of elasticity estimates based on CD presence and non-IV estimation | |||||

| Specification j | Static Own−Price Elasticity Estimate | Short−Run Own−Price Elasticity Estimate | Long−Run Own−Price Elasticity Estimate | ||

| Results for all 12 months | |||||

| −0.396 | −0.336 | −0.460 | ||

| −0.486 | −0.555 | −0.796 | ||

| −0.271 | −0.238 | −0.323 | ||

| −0.453 | −0.453 | −0.651 | ||

| 0.377 | 0.223 | 0.340 | ||

| Results for the spring months of March, April and May | |||||

| −0.396 | −0.336 | −0.460 | ||

| −0.292 | −0.334 | −0.478 | ||

| −0.259 | −0.227 | −0.308 | ||

| −0.328 | −0.327 | −0.470 | ||

| 0.005 | −0.095 | −0.144 | ||

| Results for the summer months of June, July and August | |||||

| −0.396 | −0.336 | −0.460 | ||

| −0.951 | −1.086 | −1.557 | ||

| −0.314 | −0.276 | −0.374 | ||

| −0.799 | −0.799 | −1.149 | ||

| 1.219 | 0.935 | 1.425 | ||

| Results for the fall months of September, October and November | |||||

| −0.396 | −0.336 | −0.460 | ||

| −0.577 | −0.659 | −0.945 | ||

| −0.281 | −0.247 | −0.335 | ||

| −0.532 | −0.529 | −0.761 | ||

| 0.413 | 0.250 | 0.381 | ||

| Results for the winter months of December, January and February | |||||

| −0.396 | −0.336 | −0.460 | ||

| −0.124 | −0.141 | −0.202 | ||

| −0.229 | −0.201 | −0.272 | ||

| −0.155 | −0.155 | −0.223 | ||

| −0.127 | −0.197 | −0.301 | ||

| Estimate | Standard Error | p−Value | |

|---|---|---|---|

| Adjusted R2 | 0.571 | ||

| RMSE | 0.235 | ||

| Intercept | −0.249 | 0.076 | 0.002 |

| F1 = 1 if linear specification, 0 otherwise | −0.013 | 0.106 | 0.903 |

| F2 = 1 if CES specification, 0 otherwise | 0.001 | 0.080 | 0.992 |

| F3 = 1 if GL specification, 0 otherwise | 0.048 | 0.079 | 0.541 |

| F4 = 1 if TL specification, 0 otherwise | 0.590 | 0.083 | 0.000 |

| IV = 1 if IV estimation, 0 otherwise | 0.063 | 0.061 | 0.306 |

| SR = 1 if short−run, 0 otherwise | 0.181 | 0.070 | 0.012 |

| LR = 1 if long−run, 0 otherwise | 0.174 | 0.081 | 0.036 |

| CD = 1 if CD present, 0 otherwise | −0.260 | 0.061 | 0.000 |

| Variable | Estimate | Standard Error | p−Value |

|---|---|---|---|

| Panel A: Static elasticity | |||

| Regressand’s mean | −0.452 | ||

| Adjusted R2 | 0.715 | ||

| RMSE | 0.024 | ||

| Intercept | −0.473 | 0.004 | 0.000 |

| ID | 0.0012 | 0.0001 | 0.000 |

| ID2 | −6.63 × 10−6 | 3.38 × 10−7 | 0.000 |

| Panel B: Short−run elasticity | |||

| Regressand’s mean | −0.407 | ||

| Adjusted R2 | 0.734 | ||

| RMSE | 0.014 | ||

| Intercept | −0.469 | 0.003 | 0.000 |

| ID | 0.001 | 0.00005 | 0.000 |

| ID2 | −2.95 × 10−6 | 2.05 × 10−7 | 0.000 |

| Panel C: Long−run elasticity | |||

| Regressand’s mean | −0.504 | ||

| Adjusted R2 | 0.829 | ||

| RMSE | 0.019 | ||

| Intercept | −0.593 | 0.005 | 0.000 |

| ID | 0.001 | 0.0001 | 0.000 |

| ID2 | −1.98 × 10−6 | 3.07 × 10−7 | 0.000 |

| Parametric Specification | Static | Short−Run | Long−Run | |||

|---|---|---|---|---|---|---|

| e1 | SC | e1 | SC | e1 | SC | |

| Panel A. CD presence and non−IV estimation | ||||||

| Double−log | −0.396 | 0.2% | −0.336 | 0.2% | −0.46 | 0.1% |

| Linear | −0.486 | 0.1% | −0.555 | 0.1% | −0.796 | 0.1% |

| CES | −0.271 | 0.2% | −0.238 | 0.3% | −0.323 | 0.2% |

| GL | −0.453 | 0.1% | −0.453 | 0.1% | −0.651 | 0.1% |

| TL | 0.377 | −0.2% | 0.223 | −0.3% | 0.340 | −0.2% |

| Panel B. CD absence and non−IV estimation | ||||||

| Double−log | −0.326 | 0.2% | −0.167 | 0.4% | −0.242 | 0.3% |

| Linear | 0.018 | −3.7% | 0.177 | −0.4% | 0.253 | −0.3% |

| CES | −0.396 | 0.2% | −0.217 | 0.3% | −0.323 | 0.2% |

| GL | −0.041 | 1.6% | 0.138 | −0.5% | 0.197 | −0.3% |

| TL | 0.562 | −0.1% | 0.294 | −0.2% | 0.487 | −0.1% |

| Region Definition | Static Elasticity | Short−Run Elasticity | Long−Run Elasticity |

|---|---|---|---|

| Midwest | −0.380 | −0.317 | −0.376 |

| Northeast | −0.148 | −0.166 | −0.300 |

| South | −0.439 | −0.357 | −0.492 |

| West | −0.508 | −0.400 | −0.605 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Li, R.; Woo, C.-K.; Tishler, A.; Zarnikau, J. Price Responsiveness of Residential Demand for Natural Gas in the United States. Energies 2022, 15, 4231. https://doi.org/10.3390/en15124231

Li R, Woo C-K, Tishler A, Zarnikau J. Price Responsiveness of Residential Demand for Natural Gas in the United States. Energies. 2022; 15(12):4231. https://doi.org/10.3390/en15124231

Chicago/Turabian StyleLi, Raymond, Chi-Keung Woo, Asher Tishler, and Jay Zarnikau. 2022. "Price Responsiveness of Residential Demand for Natural Gas in the United States" Energies 15, no. 12: 4231. https://doi.org/10.3390/en15124231

APA StyleLi, R., Woo, C.-K., Tishler, A., & Zarnikau, J. (2022). Price Responsiveness of Residential Demand for Natural Gas in the United States. Energies, 15(12), 4231. https://doi.org/10.3390/en15124231