1. Introduction

With the deepening of the industrial revolution and the continuous improvement of internal combustion engine technology, contemporary society is developing rapidly with the support of coal, oil, natural gas and other traditional energy sources. However, the use of traditional energy has also brought a huge environmental disaster to human society [

1]. The Chinese nation has always respected and loved nature. The 5000-year Chinese civilization has nurtured a rich ecological culture [

2]. As an important part of renewable energy, solar energy has become a significant trend of energy development.

This is a milestone event in the global response to climate change and will significantly accelerate the progress of global green and low-carbon development. In order to achieve the goal of achieving carbon neutrality, China must build a clean energy system in which new energy sources occupy a dominant position. By 2030, the proportion of non-fossil energy in China’s primary energy consumption will reach about 25%, and the total installed capacity of wind and solar power will reach more than 1.2 billion kilowatts, so as to build a new power system with new energy as the mainstay. Among the new energy power supply main bodies, such as photovoltaics, wind power and biomass power generation, photovoltaics has significant advantages and is the main force of new energy development. The advantages of photovoltaics are mainly reflected in two aspects: firstly, there are many application scenarios, large potential and few constraints; secondly, there is much room for cost reduction and strong economic competitiveness. It is also widely recognized internationally that PV has better development prospects among many new energy sources in the long-term energy strategy [

3].

At present, China is in the key period of energy price mechanism transformation and power system reform, so it is urgent to develop photovoltaic power generation. The reform and development of the photovoltaic industry need theory and systems to guide the direction. Law is characterized by stability, authority, and coerciveness. It plays a central role in promoting the development and utilization of solar energy, which cannot be replaced by policy or administrative means. China has promulgated the Renewable Energy Law, which provides a basic legal guarantee for the development and utilization of solar energy. However, solar energy’s characteristics determine the limitations of applying the Renewable Energy Law, and there are also many deficiencies in related supporting policies and local regulations. Therefore, there is a lack of institutional supply problem in China’s solar energy development and utilization of the legal guarantee.

3. Existing Legal System of Photovoltaic Industry

In recent years, with the improvement of understanding of renewable resources, China has a legal policy about solar energy resources are also constantly increased, has published and revised the circular economy promotion law, renewable energy law, the electric power law and the energy conservation law, and form a complete set of administrative regulations, department regulations, local laws, and regulations. These legal systems provide guiding principles for the development and utilization of solar energy resources in China, promote the steady and healthy development of China’s society and the economy as a common goal, and play a guiding role in the development of the solar photovoltaic industry.

3.1. Relevant Laws

From the perspective of legal distribution, China’s current laws on solar energy development and utilization are scattered. The relevant articles in the Constitution Law, The Energy Conservation Law, and the Environmental Protection Law only provide guidance and suggestions for China’s solar energy development and utilization but do not make specific provisions according to their characteristics. In contrast, China’s Renewable Energy Law, for the first time, clearly stipulates the importance of solar energy in China’s economic development in the form of law, such as the renewable energy law in the provisions of article 4, the state shall encourage and support the development and utilization of renewable energy, from the national level to help establish and develop renewable energy market, article 17 from photovoltaic industry technology promotion and application aspects, strongly encourages units and individuals to buy the use of photovoltaic power generation related products. The Renewable Energy Law also makes it clear that solar energy will be regarded as one of the clean energy resources that China will vigorously develop in the future and supporting guarantee mechanisms and compensation mechanisms of renewable energy development and utilization, namely a quota system and fixed-price system, will be established for them. Both of these systems promote the development of the photovoltaic industry. In addition, the Renewable Energy Law has also set up five systems that serve the sound development of all types of renewable energy, namely, the total volume target system, the cost-sharing system, the development fund system, the classified electricity price system, and the compulsory Internet access system. To better play the role of the above system in practice, relevant functional departments have also issued supporting implementation rules to explain and clarify laws and detailed specific provisions to ensure the effective development and utilization of all renewable energy.

3.2. Departmental Rules and Local Regulations

Since the Renewable Energy Law starts from the macro perspective of renewable energy, seeks for the commonalities of all renewable energy, and formulates supporting laws, the space involved in photovoltaic energy is limited. When the core solar energy legislation is not available, the departmental regulations issued by relevant departments of the State Council and local regulations issued by local authorities bear the burden of adjusting the development of the photovoltaic industry. These administrative regulations, departmental regulations, and local regulations act as the implementation rules of the Renewable Energy Law in the field of photovoltaic power generation.

First, they have detailed regulations on the construction of the photovoltaic industry. The first is the departmental regulation, which is to approve the construction of many solar photovoltaic power stations in northeast, northwest and North China. To develop the photovoltaic power purchase preferential subsidy system; to solve the specific legal issues surrounding the construction of photovoltaic power stations. The second is the local laws and regulations, which mainly include guiding photovoltaic power generation online, photovoltaic power generation into the grid operation, and photovoltaic power station line construction. After local regulations of active guidance, has given rise to a series, such as photovoltaic building application demonstration projects, golden sun demonstration projects, solar roof plans and franchise bidding demonstration projects, this makes photovoltaic prices drop substantially, fast development of the photovoltaic industry in China, franchise bidding online electricity price dropped to below 1.15 yuan/kWh [

14].

Secondly, in terms of policies, specific development plans have been formulated, such as the Outline of the National Medium and Long Term Development Plan for Science and Technology (2006–2020), the Development Plan for The National Strategic Emerging Industries during the 13th Five-Year Plan period, and the 13th Five-Year Plan for Energy Development. The National Development and Reform Commission has formulated the 13th Five-Year Plan for Solar PV Industry, the Medium and Long-term Development Plan for Renewable Energy, and the National Energy Administration has formulated the 13th Five-year Plan for Solar Power Generation.

To sum up, China’s photovoltaic industry legal system has formed a relatively complete legal system guided by the Renewable Energy Law and supplemented by departmental rules and local regulations.

4. Limitations of the Existing Legal System of the Photovoltaic Industry

At the present stage, China’s solar energy legislation is generally in line with the rules and regulations to guide the development of the photovoltaic industry. However, China’s photovoltaic industry legislation is constantly moving forward with the industry development to fill loopholes, so there is a lack of core legal command, uneven legal levels, and uneven distribution of regulations, which is quite different from photovoltaic legislation in developed countries.

4.1. The Legal Level of the Adjustment of the Photovoltaic Industry Is Low, and the Relevant Laws Are Not Practicable

The core law guiding solar energy is the Renewable Energy Law, which came into effect in 2006 and was revised in 2009, both quite a long time ago. Therefore, this law does not include supporting systems for adjusting and solving photovoltaic industry development problems, such as quota system and green certificate system. In addition, throughout the whole Renewable Energy Law, only Article 17 explicitly mentions the development and utilization of solar energy, but it is only a principle stipulation, and legislators regulate from a relatively high legislative height. Only the state expresses its attitude and position, which cannot play a good role in a specific practice.

From the perspective of the legal level, their legal level is relatively low and scattered at various administrative levels. Focusing on the State Council, relevant departments of the State Council have issued a series of departmental rules to guide the national work and the construction of solar power stations to implement the national strategic deployment of developing the photovoltaic industry. Focusing on the local government, due to different geographical conditions and climate temperatures, the development of the local photovoltaic industry cannot fully comply with the guiding policies issued by the State Council, so the local authorities have issued a series of local regulations and local policies in cooperation with the local authorities. However, this way of law-making is too arbitrary to summarize experience well, lacks high-level legal guidance, and fails to achieve unity of principle across the country. This law lag phenomenon is bound to hurt the further development of China’s photovoltaic industry.

4.2. The Solar Energy Law Has Not Formed a System and Lacks the Core Law of Solar Energy Development and Utilization

In solar energy, China lacks a solar law covering everything from regulating generation standards and industry norms to the pricing of online utilization, and other solar-related legal systems are formulated in conjunction with other renewable energy sources. Solar power, for example, is subject to a “feed-in tariff” along with other renewable energy sources, and a “fully guaranteed acquisition” and a “development fund” are also applied. This weakens the legal authority of solar energy development from the side. Such system design is not conducive to giving full play to the distinct advantages of solar power generation and promoting the characteristic development of the photovoltaic industry.

Similarly, focusing on the current photovoltaic industry law itself, the proportion of formulating the implementation rules of solar energy development and utilization is very uneven. Among the few implementation rules, the specification of the field of the solar water heater or the field of the solar energy and building combination takes up a large proportion. On the other hand, the photovoltaic power generation part, such as the relevant legislation on the construction of photovoltaic power stations, power grids, and generation terminal standards, no matter in terms of laws, departmental regulations, or even industry standards, is insufficient in terms of quantity. The current solution is to use the general rules for other renewable sources of electricity to adjust the feed-in tariff portion of photovoltaic power [

15].

Finally, from the point of view of punishment, the current photovoltaic industry lacks error correction and accountability machines. Although the Renewable Energy Law has been implemented for more than a decade, the government has not initiated a plan to hold photovoltaic companies accountable for failing to meet industry standards. It is necessary to seriously consider establishing an accountability system to implement the principle of governing the energy industry.

Therefore, if the existing photovoltaic industry supporting laws and regulations are not timely summarized and improved and the core solar energy law is issued, it is bound to hurt the future development of the photovoltaic industry. Government departments should pay attention to it and cooperate with the authorities to speed up the release of the core solar energy development and utilization law.

4.3. The Photovoltaic Industry Development Fund System Needs to Be Further Improved

To support the development of renewable energy, especially wind power and photovoltaic power generation, China adopts a fixed price policy of on-grid electricity prices. Under this policy, the difference between the price of renewable energy power generation and the benchmark price of local thermal power generation needs to be subsidized through the power surcharge set by the government, which makes the photovoltaic industry highly dependent on government policies and unable to fully enter the market stage. The demand for renewable energy subsidies rose from 7.3 billion yuan in 2009 to 125 billion yuan in 2017, according to the data. Photovoltaic power subsidies accounted for a sharp increase, only 791 million yuan in 2012, accounting for 4% of the total funds; By 2017, the subsidy demand for photovoltaic power generation had reached 53 billion RMB, accounting for 43% of the total funds, which is not far from the subsidy quota for wind power. Subsidies for photovoltaic power have been rising, but the efficiency of photovoltaic power has not. In 2017, photovoltaic power generation was 118.2 billion kWh, while wind power generation was 305.7 billion kWh. Photovoltaic power generation was only one-third of wind power generation [

14]. In the era of quality and efficiency, this situation runs counter to the concept of sustainable development. Although the renewable energy surcharge has been revised from 0.1 cents/kWh to 1.9 cents/kWh, the subsidy still falls far short of its income. In 2009, the subsidy gap stood at 1.3 billion yuan. In 2017, the gap widened to 112.7 billion yuan and now exceeds 200 billion yuan [

14]. At the same time, there are some problems in the operation process of implementing subsidies, which inevitably leads to the failure of partial subsidy funds, which is the failure of rules and systems. For example, the reporting and approval processes are too complex due to the lack of coordination between relevant departments and the complexity of the reporting process, which makes it impossible to provide subsidies promptly.

In general, due to the high cost of photovoltaic power generation, China’s photovoltaic market has not yet formed an effective supply and demand relationship. As a result, government subsidies have become a bottomless pit, unable to keep pace with growth. Previous subsidies were not in place, and the need for new subsidies followed, creating a vicious circle in which subsidies were not available and the gap grew year by year. As a result, the problem of insufficient subsidies for renewable energy is becoming more and more serious, and the shortage of subsidy funds has become a major problem restricting the development of the industry.

5. Relevant Legal Systems of Foreign Photovoltaic Industry and Their Implications for China

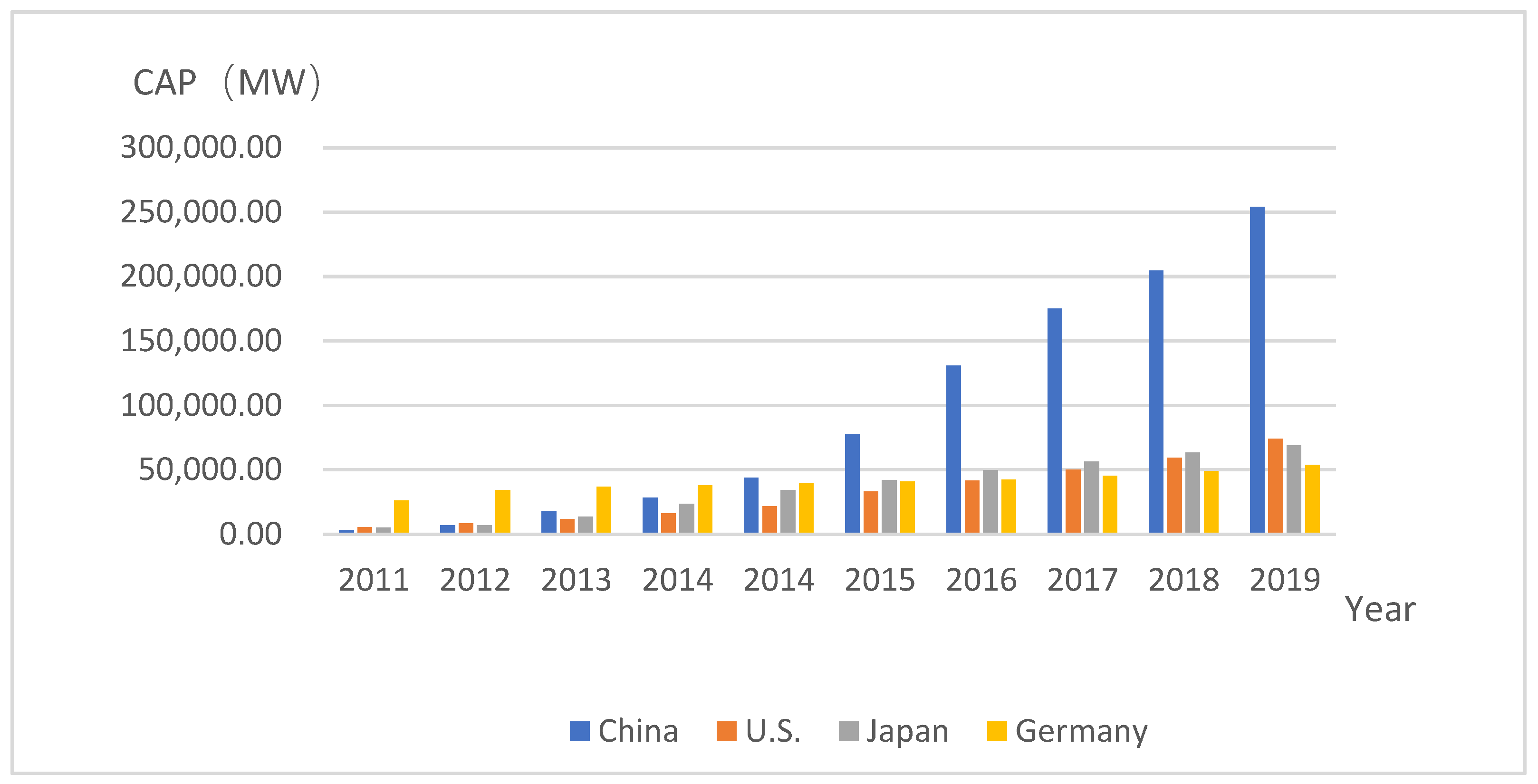

The data on solar photovoltaic for China, the U.S., Japan and Germany from 2011 to 2019 can be found in the following bar chart. It can be seen from the

Figure 1 that the amount of photovoltaic capacity (CAP) in China rises dramatically from 2014 to 2019, which is much higher than the other three countries. Additionally, the amount in the other three countries is showing an upward trend.

5.1. German Photovoltaic Industry Law

To improve the energy structure, Germany has been increasing its efforts to support the development of the photovoltaic industry. In 1999, to encourage its citizens to install photovoltaic power on a large scale, Germany proposed the “100,000 Solar Roofs Project”. Under the program, the government provides residents with subsidized loans to buy and install photovoltaic equipment, and the government buys residential solar power at market prices, incorporating that power into the national grid. The plan is a leap forward for Germany’s solar industry. In 2000, Germany passed the Renewable Energy Law (EEG200), which was amended in 2004, 2009 and 2017. The 2017 revision is the most notable. At the same time, in line with the implementation of the Renewable Energy Law, Germany also promulgated the Renewable Energy Heating Law in 2009, proposing the obligation to use renewable energy for heating.

First, in the revised version in 2017, the photovoltaic industry introduced the “tenant model”, which stipulates that if the power supply is targeted at a residential building and is consumed by the occupants of that building, the photovoltaic facility operator will only have to pay a relatively favorable share of the electricity generated to the occupants of that building. Under the new rules, the tenants will be given the same subsidy as the self-sustaining model currently supported [

16].

Second, the 2017 revision transforms the national pricing system for renewable energy subsidies into an open competitive bidding process to determine the amount of funding available for wind, solar, and biomass power. At the same time, the new regulations also provide for various exceptions to the exemption of bidding procedures. These rules are particularly significant for small businesses with a small market share and are reluctant to participate in the bidding process. The new law provides an opportunity for distributed power providers, such as the tenant model and local model. Whether these opportunities materialize depends largely on the active response of the federal states to the enactment of regulations mandated by law. The actual introduction of relevant regulations will mean new choices and business opportunities for renewable energy market players.

In Germany, the climate and energy policy has been developed through the so-called Energiewende. (Erneuerbare-Energien-Gesetz or EEG) [

17]. In order to meet the 2030 carbon emissions target, a new revised Renewable Energy Act (EEG-2021) will come into force in Germany on 1 January 2021. The Renewable Energy Act (EEG-2021) adjusts the total renewable energy target for 2030 from 50% to 65% of the total energy supply and includes for the first time the statutory goal of “greenhouse gas neutrality”; mandates the installation of smart meters in renewable energy plants to monitor the generation, feed-in and use of renewable energy; and requires the installation of smart meters in renewable energy plants. In addition to the fixed tariff for small-scale renewable energy plants, the tariff subsidy for general renewable energy generation has been increased, drawing on the lessons learned from the Renewable Energy Law (EEG-2017), which significantly reduced renewable energy subsidies. In addition to maintaining the fixed tariff for small-scale renewable energy plants, the tariff subsidy for general renewable energy generation was increased [

18].

5.2. U.S. Photovoltaic Industry Law

The United States is the first country to formulate the development plan for photovoltaic power generation. It is also the country with the fastest development and highest benefit of the world’s solar photovoltaic power generation industry. In 1974, the Solar Energy Research and Development Act was promulgated; in 1978, the Solar Photovoltaic Energy Research and Development and Model Law was promulgated; and in 1980, the Us Energy Security Act was promulgated, with special reference to the development of new energy strategies. In 2009, the US introduced the Clean Energy and Security Act. The Act sets targets for renewable energy generation projects, proposing that 6% of electricity demand should come from renewable energy generation projects by 2012 and the share should rise to 20% by 2020. In 2009, the Obama administration’s new energy policy proposed that solar and wind power should account for 10% of total electricity generation by 2012 and 25% by 2025 [

19]. To encourage residents to install and use solar power generation systems actively, the United States also issued the Photovoltaic Investment Tax Exemption Policy, which exempted and exempted the investment tax of residents’ income from the installation of photovoltaic power generation equipment.

At the same time, the third-party proprietary solar finance lease service is gradually emerging in the United States, which greatly encourages the development of the Solar industry in the United States. Residents are no longer required to buy solar power equipment by themselves. Instead, a specialized solar energy development company leases such equipment to residents. On the one hand, the solar energy development company leases such equipment to residents for use; on the other hand, the solar energy development company signs purchase agreements with residents. This third party property rights solar financing not only benefits residents and the third party issuer but building owners or users can also save the solar power equipment purchase, and the third party financiers can enjoy tax breaks that are favorable, which greatly promote the rapid development of the solar industry. The U.S. PV industry is highly dependent on government regulations and subsidies, and the cost of fully commercial PV power projects is not yet competitive with traditional power generation methods. The ITC policy was extended again in 2016 to provide a favorable policy environment for the development of the PV industry, but with the rapid development of renewable energy in recent years, state RPS standards have been largely met, and PV projects will need to compete more economically with traditional generation sources for energy consumption in the future [

20].

5.3. Japan’s Photovoltaic Industry Law

Japan has also introduced a variety of solar support policies so that solar users can enjoy many subsidies, and enterprises have also received varying degrees of tax incentives. In 2010, the Japanese government enacted a new power purchase policy, requiring power companies to recycle some of their surplus solar power at twice the original price, and revised it in 2017, introducing a “bidding system” and a “price reduction schedule”. In 2012, the Japanese government launched the new Feed-In Tariff Act (FIT), which aimed at promoting the stable, integrated rise of renewable energy in the wake of the Fukushima nuclear accident. Solar photovoltaic (PV) energy on both the residential (installation capacity less than 10 kW) and non-residential side (installation capacity 10 kW and above) have been associated with significant benefits with the passage of the new FIT Act [

21].

In addition, Japan has a green power certificate system, which promotes the research and development and production of renewable energy, such as solar energy by electric power units [

21]. The Japanese government launched the “Solar Power Surplus Acquisition System” in November 2009 and implemented the “Fixed Tariff Acquisition Policy” on 1 July 2012, to encourage the development and use of renewable energy, including solar power, by businesses and the private sector. These policies have been effective in promoting the use of renewable energy for power generation, including solar power. These policies have effectively boosted investment in renewable energy generation, which grew by 46 million kilowatts by the end of 2018, including 5.83 million kilowatts of residential solar photovoltaic and 37.22 million kilowatts of non-residential solar photovoltaic. To reduce the acquisition price of solar photovoltaic, the Japanese government has implemented a competitive bidding mechanism for solar photovoltaic power generation of 2 MW or more capacity since 2017. Through competitive bidding, the winning bid price decreased from 17.2 to 21.0 yen/kWh in November 2017 to 10.5 to 13.99 yen/kWh in September 2019 [

21].

5.4. Comparison of the Photovoltaic Industry Law in German, U.S., Japan, and China

5.4.1. Comparison with German

Firstly, to set medium and long-term development goals for renewable energy. From the German experience, aggregate targets are a gas pedal for renewable energy development. By setting specific and reasonable aggregate targets, we can also better stimulate renewable energy laws and regulations to work effectively. China should moderately adjust its renewable energy subsidy policy, abolish WTO prohibited subsidies, and implement tariff subsidies in different categories; strengthen subsidies for renewable energy R&D, and reduce the cost of renewable energy generation as soon as possible. Second, the implementation of benchmark feed-in tariffs and bidding tariffs should be categorized. Germany’s Renewable Energy Act (EEG-2021) restored moderate subsidies for renewable energy power, which is a correction of the blind elimination of subsidies in the past, and China should take this as a warning. In addition, the government should develop a supporting mechanism for market-based competition in renewable energy and strengthen supervision to avoid vicious competition [

22].

5.4.2. Comparison with U.S.

The U.S. photovoltaic industry has perfect legal protection, and its industrial development policies are mainly expressed in the form of federal energy legislation, federal environmental policy, state legislation, and agricultural legislation. In contrast, China’s PV industry lacks legal protection and its development policies are mainly introduced and implemented in the form of government policy documents [

23].

As a relatively new financing model, the third-party proprietary solar financing is not recognized by all states in the United States. Its impact on the development of renewable energy and our economic development is also unknown for China. We can actively pay attention to the application and development of third-party proprietary solar energy financing in the United States, draw lessons from the practical experience of solar energy development legislation in the United States, and create a good legal environment for the development and utilization of solar energy.

5.4.3. Comparison with Japan

At present, Japan’s photovoltaic power generation is still mainly residential, and the energy conversion efficiency of its solar energy equipment is not high, and it is difficult to improve. There are also many technical problems to be solved in the process of merging electricity. In the development of residential photovoltaic power generation, China should also pay attention to the promotion of public facilities and large and medium-sized enterprises photovoltaic power generation, accelerate the construction process of China’s solar power station, and actively improve the technology and equipment of China’s solar power generation, and improve the efficiency and safety of China’s solar power generation.

5.5. The Reference Significance of Solar Energy Policy Legislation in Developed Countries for China

By studying and studying the relevant legislation and policies of solar energy development and utilization in the above developed countries, we can see that the particularity of the legislation of solar energy and other renewable energy requires strong environmental protection and energy technology level in the legislative work. From the experience of foreign countries, we can establish and encourage the development and utilization of solar energy mainly through legislation mode, and the incentive mechanism mainly includes government financial subsidy, tax preferential system, price subsidy, and compulsory purchase system. These systems themselves are relatively scattered and involve a wide range, which requires China to first sort out a core solar energy law with an overall nature.

6. Suggestions on the Future Development of the Photovoltaic Industry Legal System

To perfect the legal system of the photovoltaic industry and promote the development of the photovoltaic industry, the following suggestions are put forward.

6.1. Promulgate Special Legislation on the Photovoltaic Industry

Solar energy is a key field and an important renewable energy branch, which is different from other renewable energy sources. If we want to play a legal role in the photovoltaic industry, we must take legislative precedence and play the leading and driving role of the law. It is important to promote scientific and democratic legislation and strengthen legislation in key areas. Therefore, it is not only the need to develop the photovoltaic industry itself but also to accumulate experience to develop renewable energy to bring photovoltaic industry legislation into the national legal step.

The vacancy, shortage and defect of solar energy legislation will affect the establishment of the solar energy legal system, and the legal process of solar energy development and utilization. From the experience accumulated in the development of other types of renewable energy in China, scientific and systematic institutional design can make the development of renewable energy stable. Therefore, to make photovoltaic power generation flourish, eliminate the black hole of subsidy, and form an effective supply-demand relationship in the market, it is necessary to construct a special photovoltaic power generation legal system, optimize and integrate the current legal system involving solar energy, and finally build a comprehensive and overall solar legal system.

6.2. Optimize the Special Fund System

As new energy and renewable energy, solar energy, has a high investment cost in the development and utilization of the solar energy industry, which requires a large amount of investment in capital, equipment, and personnel. However, China’s current consumer market is not perfect, and it is highly dependent on state subsidies, so the living environment of solar energy enterprises is relatively difficult. This requires the state to take various measures to optimize the special fund system. The first step is to enrich fund-raising measures, explore the loan mechanism for electricity and projects by establishing a financing platform with loan qualification and loan ability, and introduce securitization into distributed electricity. Establish and improve the credit system, realize information accessibility and transparency as soon as possible, improve the project risk assessment mechanism, and create favorable conditions for distributed power project financing.

The second step should be to optimize the subsidy system constantly. The subsidy mode should change from price difference subsidy to fixed price subsidy, gradually reduce the subsidy standard and adjust the direction of subsidy. To achieve the goal of subsidy mechanism reform, the price of renewable energy subsidies, including photovoltaic power generation, needs to be adjusted constantly, to continue to lower the subsidy standard before the subsidy disappears. Improve the distribution and payment methods of subsidies for photovoltaic power generation and stipulate that grid companies manage the revenue and expenditure of electricity prices and renewable energy surcharges on behalf of the government and photovoltaic enterprises.

Finally, from the perspective of finance and tax, more welfare subsidy policies should be given to photovoltaic industry practitioners to encourage scientific and technological personnel to carry out technological innovation, create star products and improve industry standards. Then, from the perspective of expanding domestic demand, we will introduce the policy of purchasing solar products, reduce and exempt taxes, and improve the enthusiasm of the majority of consumers to use photovoltaic products. For example, the real estate industry has developed rapidly in China. The new design of the high-end community has the right conditions for the use of photovoltaic power generation. This is a small solar power product installed good opportunity. Suppose welfare policies on purchasing or replacing solar energy products are introduced. In that case, they will promote the residents’ enthusiasm in the community and thus increase the sales of solar energy products. Of course, to avoid temporary and delayed defects, it is suggested that all legal systems related to subsidies, such as finance, tax, and subsidy, should be integrated into the Renewable Energy Law, or the special solar core law, to make it a development experience.

6.3. Speed up the Construction of the Tradable Green Certificate Market and Quota System

At present, there is a serious problem of “abandoning light” in the photovoltaic industry. The implementation of a quota system and green certificate market system can, to a certain extent, enhance the absorption capacity of China’s renewable energy and curb the phenomenon of “abandonment”. The quota system policy sets long-term and relatively positive renewable energy development goals. In addition to providing a more stable external policy environment for power generation enterprises, it also sets grid planning that can better adapt to the development of renewable energy and other necessary conditions to promote the development of renewable energy. At the same time, the quota system has a clear division of responsibilities and a supporting punishment mechanism, which will help stimulate the enthusiasm of all subjects and make photovoltaic workers no longer rely solely on state subsidies, so the quota system policy should be implemented at an accelerated pace.

The National Development and Reform Commission and the National Energy Administration issued the Third Notice on the Implementation of the Renewable Energy Power Quota System on 15 November 2018, to promote the early introduction of the quota system and the green license system. Among them, renewable energy quotas shall be set for power consumption, quota targets shall be determined according to the provincial administrative regions, the provincial people’s governments shall bear the responsibility for quota implementation, electricity selling enterprises and power users shall jointly assume quota obligations, and power grid enterprises shall bear the responsibility for quota implementation in operating areas. At the same time, the implementation of quotas shall be well connected with power trading.

Compared with the previous two versions, the renewable energy trading mechanism is simplified, reducing the unpredictability of prices and other factors that put excessive pressure on users and stakeholders.

6.4. Strengthen the Government’s Responsibility for Guidance

The government has been playing a leading role in energy utilization, social development, and economic growth. The photovoltaic industry is a typical public enterprise. From the experience of various countries, its development degree is closely related to the support of their governments. Therefore, government support will be the key to the timely and rapid development of the photovoltaic power generation industry.

Therefore, three steps should be taken: First, the government must enhance the strategic height of photovoltaic industry development. The development and utilization of the photovoltaic industry have not been paid much attention by society due to the long-term habit of the energy system with fossil energy as the main body in China. To promote the development of the photovoltaic industry, the development plan of solar energy utilization must be incorporated into the strategic deployment and implementation plan of China’s energy, the popularization education of relevant knowledge of solar power generation should be strengthened, the public’s understanding of the photovoltaic industry should be enhanced, and the public’s participation should be enhanced. Secondly, for photovoltaic enterprises, the government should take the initiative to guide the energy-using subjects, clarify their legal obligations and responsibilities through the combination of constraint mechanism and incentive mechanism, urge them to improve energy efficiency and strengthen the enthusiasm and consciousness of enterprises through policy guidance. Finally, the government also decides the layout of regional photovoltaic utilization development. There are differences between the north and the south and between the east and the west in China’s photovoltaic industry. How to give play to the regional advantages of different regions also tests the decision-making level of national macro-control.

7. Conclusions

At present, the photovoltaic industry has a good momentum of development in China, but related problems are increasingly prominent, such as laws and policies lag behind industrial development, photovoltaic power generation is difficult to get online, financing channels are narrow, the phenomenon of abandoning light is serious. The photovoltaic industry will be the unity of technological innovation and institutional innovation, which depends on the protection and guidance of the legal system. So, when there is a problem do not give up, the emergence of the problem is to perfect the legal system. Along the way, firstly, we need to continuously implement the green development concept, adhere to the basic state policy of resource conservation and environmental protection, insist on saving and protection of preference, and the principle of natural recovery. To implement the strictest possible ecological environment protection system, and comprehensively build the system of efficient utilization of resources, improve the system of ecological protection and restoration, with the strict liability system of ecological environment protection. Secondly, the legal system of the photovoltaic industry should be adjusted timely according to the form of the photovoltaic industry and the photovoltaic market. Finally, the supporting legal system should be constantly improved and the core laws in the field of photovoltaic should be accelerated. Only in this way can the photovoltaic industry be promoted to develop in a good and rapid way and the institutional role of the law can be brought into play.

{kind=link}