On the Use of Base Temperature by Heat Cost Allocation in Buildings

Abstract

:1. Introduction

2. Method

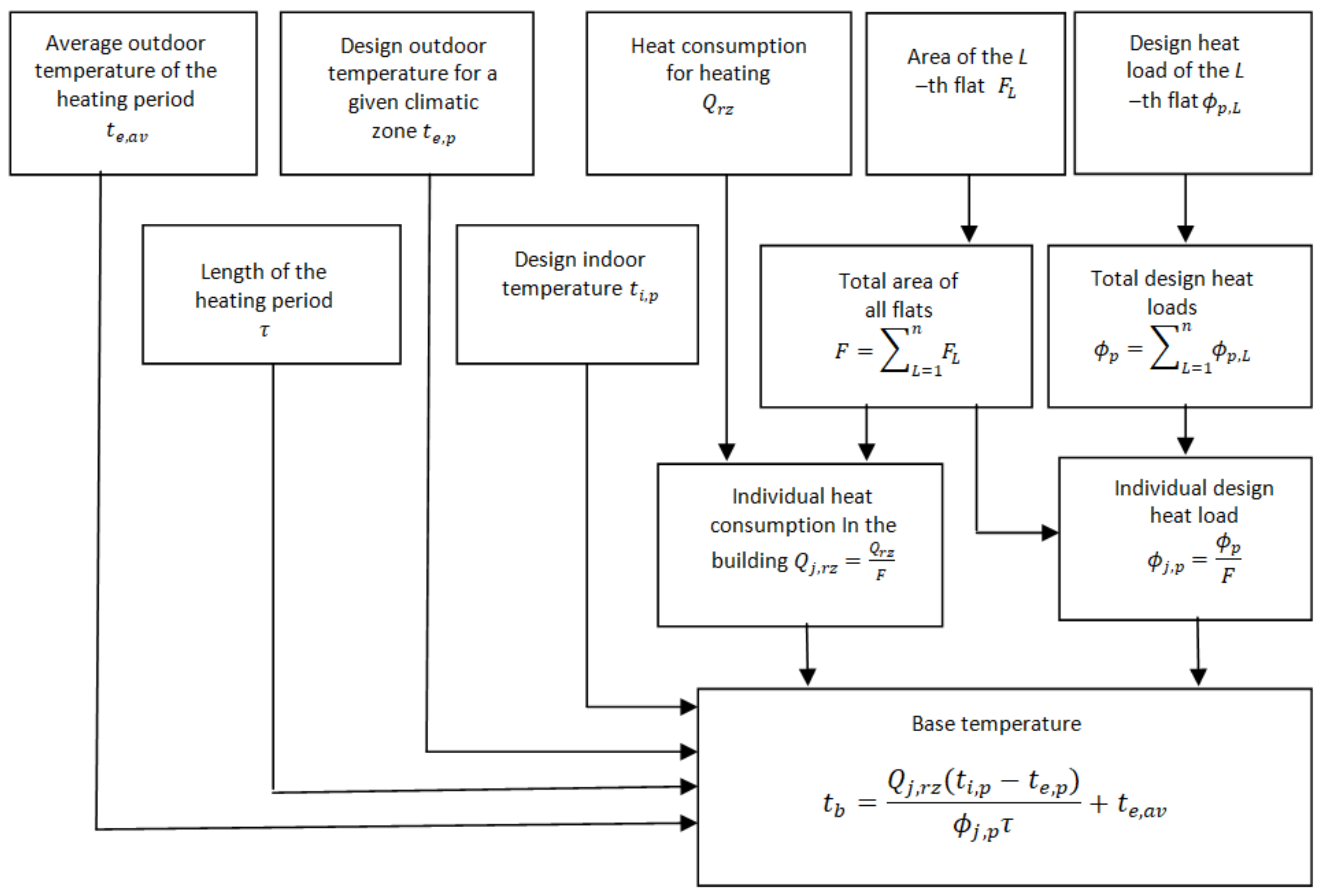

2.1. Estimation of Base Temperature for the Building

- –

- Individual heat consumption in the heating period () in the variant without heat gains.

- –

- Individual heat consumption during the heating period () in the variant, taking into account internal and solar heat gains.

- -

- The actual heat consumption for heating per unit area in a given heating period ;

- -

- The individual design heat load under the design conditions , obtained from the design documentation or calculations using design programs, e.g., EnergyPlus;

- -

- The hourly length of the heating period ;

- -

- The average outdoor temperature in a given heating period

- -

- The design outdoor temperature for a given climatic zone;

- -

- The design indoor temperature of rooms in the building, for example = 20 °C.

2.2. Scheme of Variable Heat Costs Allocation for Systems with HCAs with the Function of Determining the Average Indoor Temperature in the Flat (Scheme A)

- -

- It allows for the allocation of heat costs coming only from external sources, excluding internal heat gains and solar gains;

- -

- It establishes a balance mechanism between the energy-saving behaviour of users and the rational operation of the building in terms of the required minimum temperature and necessary ventilation of the flats;

- -

- It partially takes into account the influence of other heat (apart from the radiator), delivered to the building from external sources and distributed inside the building, e.g., risers and heat transfer through the internal walls of the building.

2.3. Scheme of Variable Heat Costs Allocation for Systems with HCAs Using Only Indications of Consumption Values (Scheme B)

- -

- It allows for the elimination of incorrect indications of the HCAs, which are quite numerous under the conditions of multi-family buildings;

- -

- It does not require the knowledge of the indoor temperature in the flats, where heat cost allocation is made;

- -

- It eliminates discrepancies in the indications of HCAs in individual flats, which do not have technical justification and violate the norms of social coexistence.

3. Case Study

3.1. Materials and Methods

- -

- Surface area (lump sum allocation)—method 1;

- -

- Indications of HCAs without indoor temperature registration—method 2;

- -

- Indications of HCAs without indoor temperature registration, taking into account location correction factor (LCF) of the flats in the body of the building—method 3;

- -

- Scheme A (using the recorded average indoor temperature of the flats)—method 4;

- -

- Scheme B (using the indications of the HCAs without indoor temperature registration, taking into account the correction of ± 4 °C from the base temperature of the building)—method 5.

3.2. Results and Discussion

3.2.1. Heat Costs Allocation Using HCAs with the Function of Determining the Average Indoor Temperature in the Flat (Scheme A)

3.2.2. Heat Costs Allocation Using HCAs with Classic Indications (Scheme B)

3.2.3. Comparison of the Results of Variable Heat Costs Allocation Using Methods 1–5

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Nomenclature

| F | Area (m2) |

| tb | Base temperature (°C) |

| te | Outdoor temperature (°C) |

| ti | Indoor temperature (°C) |

| LCF | Location correction factor (-) |

| Q | Heat consumption (GJ) |

| Qj | Individual heat consumption for heating the building (GJ/m2) |

| Zj | Individual indications of heat cost allocator in the building (-) |

| Z′ | Final value of normalized consumption units (-) |

| Length of the heating season (h) | |

| Individual heat load for heating the building by average indoor temperature (W/m2) | |

| Subscripts | |

| av | Mean |

| p | Design |

| L | Local |

References

- European Parliament. Directive 2012/27/EU, Official Journal of the European Union. 2012. Available online: https://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=OJ:L:2012:315:0001:0056:en:PDF (accessed on 14 November 2012).

- Canale, L.; Dell’Isola, M.; Ficco, G.; Di Pietra, B.; Frattolillo, A. Estimating the impact of heat accounting on Italian residential energy consumption in different scenarios. Energy Build. 2018, 168, 385–398. [Google Scholar] [CrossRef]

- Terés-Zubiaga, J.; Pérez-Iribarren, E.; González-Pino, I.; Sala, J.M. Effects of individual metering and charging of heating and domestic hot water on energy consumption of buildings in temperate climates. Energy Convers. Manag. 2018, 171, 491–506. [Google Scholar] [CrossRef]

- Slijepčević, S.; Mikulić, D.; Horvat, K. Evaluation of the Cost-Effectiveness of the Installation of Heat-Cost Allocators in Multifamily Buildings in Croatia. Energies 2019, 12, 507. [Google Scholar] [CrossRef] [Green Version]

- Calise, F.; Cappiello, F.; D’Agostino, D.; Vicidomini, M. Heat metering for residential buildings: A novel approach through dynamic simulations for the calculation of energy and economic savings. Energy 2021, 234, 121204. [Google Scholar] [CrossRef]

- Andersen, S.; Andersen, R.K.; Olesen, B.W. Influence of heat cost allocation on occupants’ control of indoor environment in 56 apartments: Studied with measurements, interviews and questionnaires. Build. Environ. 2016, 101, 1–8. [Google Scholar] [CrossRef] [Green Version]

- Cholewa, T.; Siggelsten, S.; Balen, I.; Ficco, G. Heat cost allocation in buildings: Possibilities, problems and solutions. J. Build. Eng. 2020, 31, 101349. [Google Scholar] [CrossRef]

- Canale, L.; Dell’Isola, M.; Ficco, G.; Cholewa, T.; Siggelsten, S.; Balen, I. A comprehensive review on heat accounting and cost allocation in residential buildings in EU. Energy Build. 2019, 202, 109398. [Google Scholar] [CrossRef]

- Pakanen, J.; Karjalainen, S. Estimating static heat flows in buildings for energy allocation systems. Energy Build. 2006, 38, 1044–1052. [Google Scholar] [CrossRef]

- Siggelsten, S. Reallocation of heating costs due to heat transfer between adjacent apartments. Energy Build. 2014, 75, 256–263. [Google Scholar] [CrossRef]

- Michnikowski, P. Allocation of heating costs with consideration to energy transfer from adjacent apartments. Energy Build. 2017, 139, 224–231. [Google Scholar] [CrossRef]

- Dell’Isola, M.; Ficco, G.; Canale, L.; Frattolillo, A.; Bertini, I. A new heat cost allocation method for social housing. Energy Build. 2018, 172, 67–77. [Google Scholar] [CrossRef]

- Dell’Isola, M.; Ficco, G.; Arpino, F.; Cortellessa, G.; Canale, L. A novel model for the evaluation of heat accounting systems reliability in residential buildings. Energy Build. 2017, 150, 281–293. [Google Scholar] [CrossRef]

- Dell’Isola, M.; Ficco, G.; Canale, L.; Palella, B.I.; Puglisi, G. An IoT Integrated Tool to Enhance User Awareness on Energy Consumption in Residential Buildings. Atmosphere 2019, 10, 743. [Google Scholar] [CrossRef] [Green Version]

- Saba, F.; Fernicola, V.; Masoero, M.C.; Abramo, S. Experimental Analysis of a Heat Cost Allocation Method for Apartment Buildings. Buildings 2017, 7, 20. [Google Scholar] [CrossRef] [Green Version]

- Canale, L.; Slott, B.P.; Finsdóttir, S.; Kildemoes, L.R.; Andersen, R.K. Do in-home displays affect end-user consumptions? A mixed method analysis of electricity, heating and water use in Danish apartments. Energy Build. 2021, 246, 111094. [Google Scholar] [CrossRef]

- Michnikowski, P.; Szczechowiak, E. Determination of heat load released by a radiator by an electronic heating cost allocator. Arch. Thermodyn. 2009, 30, 15–36. [Google Scholar]

- EN 834:2013. Heat Cost Allocators for the Determination of the Consumption of Room Heating Radiators—Appliances with Electrical Energy Supply. 2013. Available online: https://standards.iteh.ai/catalog/standards/cen/bc0ddd66-a1ef-416f-834c-ceb1df5a5855/en-834-2013 (accessed on 7 August 2013).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| External wall | U = 0.259 W/(m2 W) |

| Internal (load-bearing) walls | U = 1.055 W/(m2 W) |

| Internal walls | U = 2.205 W/(m2 W) |

| Ceiling above the basement | U = 0.886 W/(m2 W) |

| Flat roof | U = 0.210 W/(m2 W) |

| Windows | U = 2.000 W/(m2 W) |

| Number of Flats | FL (m2) | ZL (-) | ti,L (°C) | (°C) | (-) | ZL′ (-) | ZL′—ZL (-) | (ZL′—ZL)/ZL (%) |

|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) |

| 1 | 54 | 6580 | 21.6 | 0.9 | 5310 | 5945 | −635 | −9.65 |

| 2 | 54.5 | 5253 | 22.6 | 1.9 | 5746 | 5500 | 247 | 4.70 |

| 3 | 43.9 | 6260 | 21.7 | 1 | 4346 | 5303 | −957 | −15.29 |

| 4 | 43.9 | 6073 | 20.9 | 0.2 | 4081 | 5077 | −996 | −16.40 |

| 5 | 59.4 | 4764 | 19.8 | −0.9 | 4994 | 4879 | 115 | 2.42 |

| 6 | 32.7 | 7609 | 20.5 | −0.2 | 2933 | 5271 | −2338 | −30.73 |

| 7 | 54 | 325 | 19.4 | −1.3 | 4369 | 2347 | 2022 | 622.70 |

| 8 | 54.5 | 4166 | 22.2 | 1.5 | 5600 | 4883 | 717 | 17.22 |

| 9 | 43.9 | 2205 | 20.5 | −0.2 | 3950 | 3077 | 872 | 39.56 |

| 10 | 43.9 | 4325 | 22.3 | 1.6 | 4539 | 4432 | 107 | 2.47 |

| 11 | 59.4 | 3189 | 19.8 | −0.9 | 5021 | 4105 | 916 | 28.73 |

| 12 | 32.7 | 1880 | 20.5 | −0.2 | 2931 | 2405 | 525 | 27.95 |

| 13 | 54 | 3274 | 21.2 | 0.5 | 5140 | 4207 | 933 | 28.50 |

| 14 | 54.5 | 4135 | 20.9 | 0.2 | 5072 | 4603 | 469 | 11.34 |

| 15 | 43.9 | 3014 | 20.5 | −0.2 | 3948 | 3481 | 467 | 15.50 |

| 16 | 43.9 | 5288 | 20.2 | −0.5 | 3827 | 4557 | −730 | −13.81 |

| 17 | 59.4 | 2452 | 18.8 | −1.9 | 4553 | 3502 | 1051 | 42.85 |

| 18 | 32.7 | 5253 | 21.9 | 1.2 | 3272 | 4262 | −991 | −18.86 |

| 19 | 54 | 4410 | 22.1 | 1.4 | 5509 | 4960 | 549 | 12.46 |

| 20 | 54.5 | 3599 | 21.7 | 1 | 5376 | 4487 | 889 | 24.69 |

| 21 | 43.9 | 534 | 20.6 | −0.1 | 3968 | 2251 | 1717 | 321.62 |

| 22 | 43.9 | 2321 | 18.5 | −2.2 | 3265 | 2793 | 472 | 20.34 |

| 23 | 59.4 | 2848 | 19.6 | −1.1 | 4901 | 3874 | 1027 | 36.06 |

| 24 | 32.7 | 3456 | 20.2 | −0.5 | 2857 | 3157 | −300 | −8.67 |

| 25 | 54 | 4770 | 18.7 | −2 | 4094 | 4432 | −338 | −7.09 |

| 26 | 54.5 | 7343 | 22.5 | 1.8 | 5710 | 6527 | −816 | −11.12 |

| 27 | 43.9 | 8665 | 21.0 | 0.3 | 4092 | 6378 | −2287 | −26.39 |

| 28 | 43.9 | 4681 | 20.5 | −0.2 | 3927 | 4304 | −377 | −8.06 |

| 29 | 59.4 | 7599 | 19.7 | −1 | 4969 | 6284 | −1315 | −17.30 |

| 30 | 32.7 | 4785 | 19.8 | −0.9 | 2755 | 3770 | −1015 | −21.22 |

| Σ | 1442 | 131,054 | 131,054 | 131,054 | ||||

| Number of Flats | FL (m2) | ZL (-) | ZL′ (-) | ZL′—ZL (-) | (ZL′—ZL)/ZL (%) |

|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) |

| 1 | 54.00 | 6580 | 6111 | −469 | −7 |

| 2 | 54.50 | 5253 | 5253 | 0 | 0 |

| 3 | 43.90 | 6260 | 4968 | −1292 | −21 |

| 4 | 43.90 | 6073 | 4968 | −1104 | −18 |

| 5 | 59.40 | 4764 | 4764 | 0 | 0 |

| 6 | 32.70 | 7609 | 3701 | −3909 | −51 |

| 7 | 54.00 | 325 | 3040 | 2716 | 836 |

| 8 | 54.50 | 4166 | 4166 | 0 | 0 |

| 9 | 43.90 | 2205 | 2472 | 267 | 12 |

| 10 | 43.90 | 4325 | 4325 | 0 | 0 |

| 11 | 59.40 | 3189 | 3344 | 156 | 5 |

| 12 | 32.70 | 1880 | 1880 | 0 | 0 |

| 13 | 54.00 | 3274 | 3274 | 0 | 0 |

| 14 | 54.50 | 4135 | 4135 | 0 | 0 |

| 15 | 43.90 | 3014 | 3014 | 0 | 0 |

| 16 | 43.90 | 5288 | 4968 | −319 | −6 |

| 17 | 59.40 | 2452 | 3344 | 893 | 36 |

| 18 | 32.70 | 5253 | 3701 | −1552 | −30 |

| 19 | 54.00 | 4410 | 4410 | 0 | 0 |

| 20 | 54.50 | 3599 | 3599 | 0 | 0 |

| 21 | 43.90 | 534 | 2472 | 1938 | 363 |

| 22 | 43.90 | 2321 | 2472 | 151 | 6 |

| 23 | 59.40 | 2848 | 3344 | 497 | 17 |

| 24 | 32.70 | 3456 | 3456 | 0 | 0 |

| 25 | 54.00 | 4770 | 4770 | 0 | 0 |

| 26 | 54.50 | 7343 | 6168 | −1175 | −16 |

| 27 | 43.90 | 8665 | 4968 | −3697 | −43 |

| 28 | 43.90 | 4681 | 4681 | 0 | 0 |

| 29 | 59.40 | 7599 | 6722 | −877 | −12 |

| 30 | 32.70 | 4785 | 3701 | −1085 | −23 |

| Σ | 1442.00 | 131,054 | 122,192 |

| Number of Flats | FL (m2) | LCF (-) | ZL (-) from HCA | ti,L (°C) | ZL (-) | W (%) | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Method 1 | Method 2 | Method 3 | Method 4 | Method 5 | Method 1 | Method 2 | Method 3 | Method 4 | Method 5 | |||||

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | (12) | (13) | (14) | (15) |

| 1 | 54 | 0.77 | 6580 | 21.6 | 4908 | 6580 | 3779 | 5189 | 4706 | 100.00 | 134.08 | 124.84 | 115.74 | 122.30 |

| 2 | 54.5 | 0.75 | 5253 | 22.6 | 4953 | 5253 | 3715 | 4843 | 3940 | 100.00 | 106.05 | 96.18 | 107.04 | 101.45 |

| 3 | 43.9 | 0.78 | 6260 | 21.7 | 3990 | 6260 | 3112 | 4614 | 3875 | 100.00 | 156.90 | 147.99 | 126.61 | 123.88 |

| 4 | 43.9 | 0.72 | 6073 | 20.9 | 3990 | 6073 | 2873 | 4227 | 3577 | 100.00 | 152.21 | 132.52 | 115.97 | 114.35 |

| 5 | 59.4 | 0.76 | 4764 | 19.8 | 5398 | 4764 | 4103 | 4307 | 3620 | 100.00 | 88.24 | 81.09 | 87.34 | 85.53 |

| 6 | 32.7 | 0.74 | 7609 | 20.5 | 2972 | 7609 | 2199 | 4282 | 2739 | 100.00 | 256.05 | 229.12 | 157.73 | 117.53 |

| 7 | 54 | 0.92 | 325 | 19.4 | 4908 | 325 | 4515 | 2334 | 2797 | 100.00 | 6.62 | 7.36 | 52.06 | 72.69 |

| 8 | 54.5 | 0.95 | 4166 | 22.2 | 4953 | 4166 | 4705 | 4779 | 3957 | 100.00 | 84.10 | 96.61 | 105.62 | 101.90 |

| 9 | 43.9 | 1 | 2205 | 20.5 | 3990 | 2205 | 3990 | 3077 | 2472 | 100.00 | 55.26 | 66.83 | 84.43 | 79.01 |

| 10 | 43.9 | 0.9 | 4325 | 22.3 | 3990 | 4325 | 3591 | 4216 | 3892 | 100.00 | 108.40 | 117.97 | 115.66 | 124.43 |

| 11 | 59.4 | 0.96 | 3189 | 19.8 | 5398 | 3189 | 5183 | 4041 | 3211 | 100.00 | 59.06 | 68.56 | 81.94 | 75.85 |

| 12 | 32.7 | 0.93 | 1880 | 20.5 | 2972 | 1880 | 2764 | 2340 | 1748 | 100.00 | 63.25 | 71.14 | 86.18 | 75.03 |

| 13 | 54 | 0.92 | 3274 | 21.2 | 4908 | 3274 | 4515 | 4076 | 3012 | 100.00 | 66.71 | 74.21 | 90.92 | 78.28 |

| 14 | 54.5 | 0.95 | 4135 | 20.9 | 4953 | 4135 | 4705 | 4500 | 3928 | 100.00 | 83.48 | 95.89 | 99.46 | 101.15 |

| 15 | 43.9 | 1 | 3014 | 20.5 | 3990 | 3014 | 3990 | 3481 | 3014 | 100.00 | 75.53 | 91.34 | 95.50 | 96.34 |

| 16 | 43.9 | 0.9 | 5288 | 20.2 | 3990 | 5288 | 3591 | 4293 | 4471 | 100.00 | 132.53 | 144.23 | 117.79 | 142.94 |

| 17 | 59.4 | 0.96 | 2452 | 18.8 | 5398 | 2452 | 5183 | 3453 | 3211 | 100.00 | 45.41 | 52.72 | 70.02 | 75.85 |

| 18 | 32.7 | 0.93 | 5253 | 21.9 | 2972 | 5253 | 2764 | 4078 | 3442 | 100.00 | 176.74 | 198.76 | 150.22 | 147.71 |

| 19 | 54 | 0.92 | 4410 | 22.1 | 4908 | 4410 | 4515 | 4783 | 4057 | 100.00 | 89.86 | 99.97 | 106.69 | 105.45 |

| 20 | 54.5 | 0.95 | 3599 | 21.7 | 4953 | 3599 | 4705 | 4397 | 3419 | 100.00 | 72.66 | 83.47 | 97.19 | 88.04 |

| 21 | 43.9 | 1 | 534 | 20.6 | 3990 | 534 | 3990 | 2251 | 2472 | 100.00 | 13.38 | 16.18 | 61.76 | 79.01 |

| 22 | 43.9 | 0.9 | 2321 | 18.5 | 3990 | 2321 | 3591 | 2677 | 2224 | 100.00 | 58.18 | 63.31 | 73.45 | 71.11 |

| 23 | 59.4 | 0.96 | 2848 | 19.6 | 5398 | 2848 | 5183 | 3817 | 3211 | 100.00 | 52.75 | 61.23 | 77.41 | 75.85 |

| 24 | 32.7 | 0.93 | 3456 | 20.2 | 2972 | 3456 | 2764 | 3036 | 3214 | 100.00 | 116.30 | 130.79 | 111.82 | 137.95 |

| 25 | 54 | 0.71 | 4770 | 18.7 | 4908 | 4770 | 3484 | 3741 | 3387 | 100.00 | 97.20 | 83.45 | 83.44 | 88.02 |

| 26 | 54.5 | 0.72 | 7343 | 22.5 | 4953 | 7343 | 3566 | 5499 | 4441 | 100.00 | 148.25 | 129.07 | 121.53 | 114.35 |

| 27 | 43.9 | 0.78 | 8665 | 21.0 | 3990 | 8665 | 3112 | 5425 | 3875 | 100.00 | 217.19 | 204.85 | 148.86 | 123.88 |

| 28 | 43.9 | 0.69 | 4681 | 20.5 | 3990 | 4681 | 2753 | 3578 | 3230 | 100.00 | 117.33 | 97.90 | 98.18 | 103.26 |

| 29 | 59.4 | 0.73 | 7599 | 19.7 | 5398 | 7599 | 3941 | 5258 | 4907 | 100.00 | 140.77 | 124.26 | 106.63 | 115.94 |

| 30 | 32.7 | 0.73 | 4785 | 19.8 | 2972 | 4785 | 2169 | 3124 | 2702 | 100.00 | 161.02 | 142.14 | 115.07 | 115.94 |

| Σ | 1442 | 131,054 | 131,054 | 131,054 | 108,377 | 119,715 | 102,751 | |||||||

| Method | Correlation Coefficient K |

|---|---|

| Method 1 | 0.0966 |

| Method 2 | 0.2953 |

| Method 3 | 0.3478 |

| Method 4 | 0.5260 |

| Method 5 | 0.4468 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Michnikowski, P.; Cholewa, T. On the Use of Base Temperature by Heat Cost Allocation in Buildings. Energies 2021, 14, 6346. https://doi.org/10.3390/en14196346

Michnikowski P, Cholewa T. On the Use of Base Temperature by Heat Cost Allocation in Buildings. Energies. 2021; 14(19):6346. https://doi.org/10.3390/en14196346

Chicago/Turabian StyleMichnikowski, Paweł, and Tomasz Cholewa. 2021. "On the Use of Base Temperature by Heat Cost Allocation in Buildings" Energies 14, no. 19: 6346. https://doi.org/10.3390/en14196346

APA StyleMichnikowski, P., & Cholewa, T. (2021). On the Use of Base Temperature by Heat Cost Allocation in Buildings. Energies, 14(19), 6346. https://doi.org/10.3390/en14196346