Evaluation of Energy Transition Scenarios in Poland

Abstract

1. Introduction

- What are the real scenarios for the development of the energy mix for Poland in the 2040 perspective?

- How will the energy mix develop in the described scenarios?

- What will be the impact of each of the proposed energy transformation scenarios on the Polish economy and society?

2. Literature Review

3. Methodology

- I equitable transition (providing new development opportunities for regions and communities most negatively affected by the energy transition);

- II zero-emission energy system (achieving zero-emission in the energy sector will be possible through the construction of a nuclear power plant, implementation of offshore energy, development of prosumer energy while increasing the share of gas in the electricity generation sector);

- III good air quality (moving away from fossil fuels not only in the energy sector but also in transport and construction) [33].

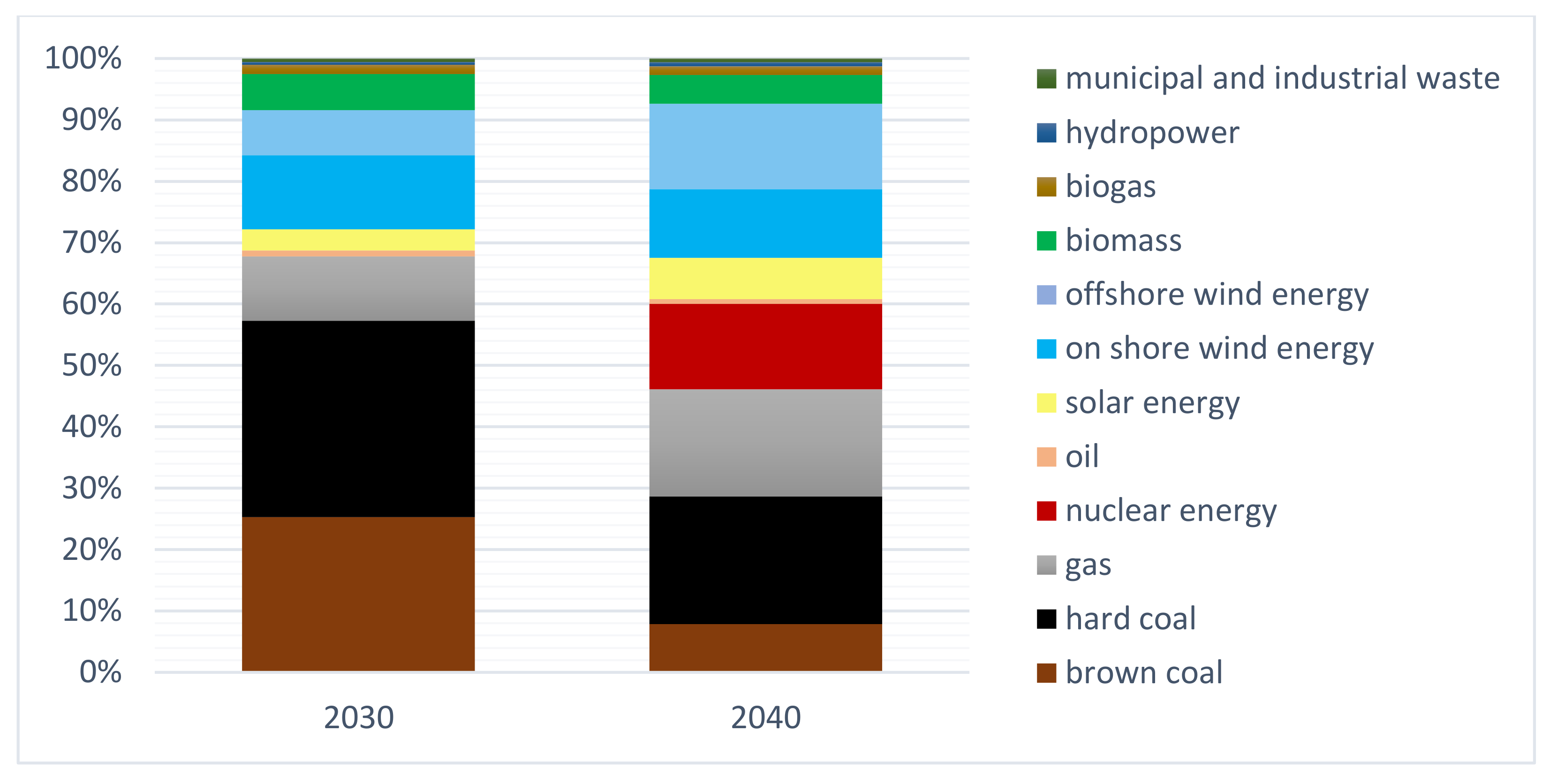

4. Polish Energy Transformation Scenarios

4.1. Diversified Scenario with Nuclear Energy

4.2. Diversified Scenario with Natural Gas

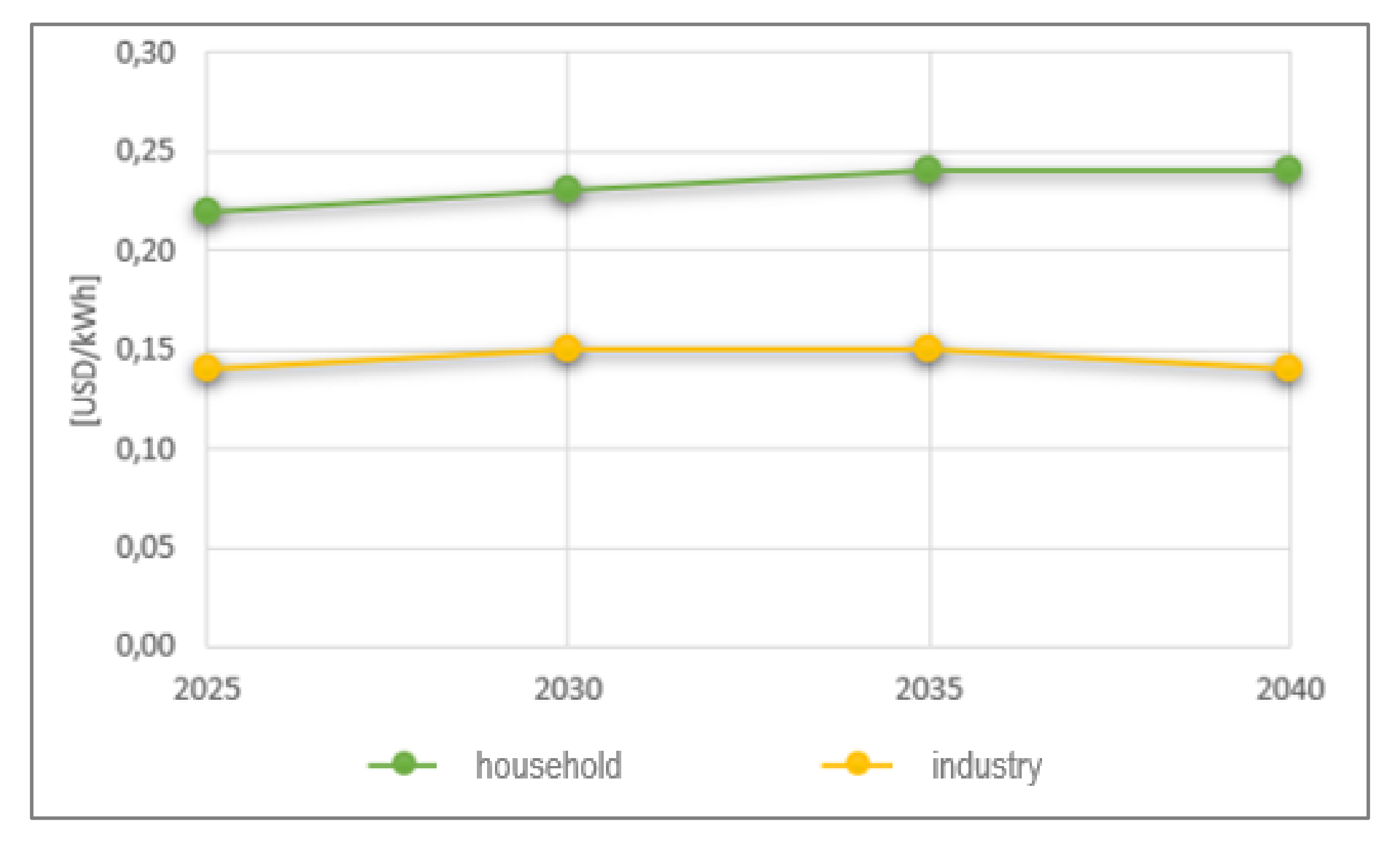

5. Conclusions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Paris Agreement. 2015. Available online: https://unfccc.int/process-and-meetings/the-paris-agreement/the-paris-agreement (accessed on 13 June 2021).

- European Green Deal. 2019. Available online: https://www.consilium.europa.eu/en/policies/green-deal/ (accessed on 23 June 2021).

- Jastrzębska, G. Odnawialne Źródła Energii i Pojazdy Proekologiczne; WNT: Warszawa, Poland, 2007. [Google Scholar]

- Neutralna Emisyjnie Polska 2050; Raport; McKinsey & Company: Warszawa, Poland, 2020.

- Snoek, M. The Use and Methodology of Scenario Making. Eur. J. Teach. Educ. 2003, 26, 9–19. [Google Scholar] [CrossRef]

- Kraan, O.; Chappin, E.; Kramer, G.J.; Nikolic, I. The influence of the energy transition on the significance of key energy metrics. Renew. Sustain. Energy Rev. 2019, 111, 215–223. [Google Scholar] [CrossRef]

- Edmonts, J.; Wilson, T.; Wise, M.; Weyant, M. Electrification of the economy and CO2 emissions mitigation. Environmental. Econ. Policy Stud. 2006, 7, 175–203. [Google Scholar] [CrossRef]

- Gabriel, J. A scientific enquiry into the future. Eur. J. Futur. Res. 2014, 2, 1–9. [Google Scholar] [CrossRef]

- Dahl, C.A. Book Review—International Energy Markets: Understanding Pricing, Policies, and Profits. Energy J. 2006, 27, 179–181. [Google Scholar] [CrossRef]

- Hölsgens, R.; Lübke, S.; Hasselkuß, M. Social innovations in the German energy transition: An attempt to use the heuristics of the multi-level perspective of transitions to analyze the diffusion process of social innovations. Energy Sustain. Soc. 2018, 8, 8. [Google Scholar] [CrossRef]

- Raven, R.; Van den Bosch, S.; Weterings, R. Transitions and strategic niche management: Towards a competence kit for practitioners. Int. J. Technol. Manag. 2010, 51, 57–74. [Google Scholar] [CrossRef]

- Bento, N.; Fontes, M. Spatial diffusion and the formation of a technological innovation system in the receiving country: The case of wind energy in Portugal. Environ. Innov. Soc. Transit. 2015, 15, 158–179. [Google Scholar] [CrossRef]

- Zimm, C.; Goldemberg, J.; Nakicenovic, N.; Busch, S. Is the renewables transformation a piece of cake or a pie in the sky? Energy Strat. Rev. 2019, 26, 100401. [Google Scholar] [CrossRef]

- Sartorius, C.; Zundel, S. Time Strategies, Innovation and Environmental Policy; Edward Elgar Publishing: Cheltenham, UK, 2005. [Google Scholar]

- Gielen, D.; Boshell, F.; Saygin, D.; Bazilian, M.D.; Wagner, N.; Gorini, R. The role of renewable energy in the global energy transformation. Energy Strategy Rev. 2019, 24, 38–50. [Google Scholar] [CrossRef]

- Höfer, T.; Madlener, R. A participatory stakeholder process for evaluating sustainable energy transition scenarios. Energy Policy 2020, 139, 111277. [Google Scholar] [CrossRef]

- Rouzbahani, H.M.; Karimipour, H.; Lei, L. A review on virtual power plant for energy management. Sustain. Energy Technol. Assess. 2021, 47, 101370. [Google Scholar] [CrossRef]

- Bhuiyan, E.A.; Hossain, Z.; Muyeen, S.; Fahim, S.R.; Sarker, S.K.; Das, S.K. Towards next generation virtual power plant: Technology review and frameworks. Renew. Sustain. Energy Rev. 2021, 150, 111358. [Google Scholar] [CrossRef]

- Teufel, B.; Sentic, A.; Barmet, M. Blockchain energy: Blockchain in future energy systems. J. Electron. Sci. Technol. 2019, 17, 100011. [Google Scholar] [CrossRef]

- Lei, N.; Masanet, E.; Koomey, J. Best practices for analyzing the direct energy use of blockchain technology systems: Review and policy recommendations. Energy Policy 2021, 156, 112422. [Google Scholar] [CrossRef]

- Marangos, J. Consistency and Viability of Islamic Economic Systems and the Transition Process; Springer: New York, NY, USA, 2013. [Google Scholar]

- Adam, J. The transition to a market economy in Poland. Camb. J. Econ. 1994, 18, 607–618. [Google Scholar] [CrossRef]

- Borowski, P. Adaptation strategy on regulated markets of power companies in Poland. Energy Environ. 2019, 30, 1. [Google Scholar]

- Kochanek, E. Wielowymiarowość Interesów Energetycznych w Dobie Transformacji Systemowej; WAT: Warsaw, Poland, 2021. [Google Scholar]

- Borowski, P. Development Strategies for Electric Utilities. Acta Energ. 2016, 4, 16–21. [Google Scholar] [CrossRef]

- Jacobsson, S.; Lauber, V. The politics and policy of energy system transformation—Explaining the German diffusion of renewable energy technology. Energy Policy 2006, 34, 256–275. [Google Scholar] [CrossRef]

- Sawin, J.L.; Sverrisson, F.; Leidreiter, A. Renewable Energy and Sustainable Development. Accounting for Impacts on the Path to 100% RE; World Future Council: Hamburg, Germany, 2016. [Google Scholar]

- Jacobsson, S.; Bergek, A. Transforming the Energy Sector: The Evolution of Technological Systems in Renewable Energy Technology. Ind. Corp. Chang. 2006, 13, 5. [Google Scholar] [CrossRef]

- Figueres, C.; Schellnhuber, H.J.; Whiteman, G.; Rockström, J.; Hobley, A.; Rahmstorf, S. Three years to safeguard our climate. Nature 2017, 546, 593. [Google Scholar] [CrossRef] [PubMed]

- Miller, C.A.; Richter, J.; O’Leary, J. Socio-energy systems design: A policy framework for Energy transitions. Energy Res. Soc. Sci. 2015, 6, 29–40. [Google Scholar] [CrossRef]

- Dehdarian, A. Three Essays on Methodologies for Dynamic Modeling of Emerging Socio-technical Systems: The Case of Smart Grid Development. EPFL 2017. [Google Scholar] [CrossRef]

- Bishop, P.; Hines, A.; Collins, T. The current state of scenario development: An overview of techniques. Foresight 2007, 9, 5–25. [Google Scholar] [CrossRef]

- Polityka Energetyczna Polski 2040, Załącznik do Uchwały nr 22/2021 Rady Ministrów z Dnia 2 Lutego 2021 r; Ministerstwo Klimatu i Środowiska: Warsaw, Poland, 2021.

- Szczerbowski, R. The forecast of Polish power production sector development by 2050—Coal scenario. Energy Policy J. 2018, 19, 3. [Google Scholar]

- Badora, A.; Kud, K.; Woźniak, M. Nuclear Energy Perception and Ecological Attitudes. Energies 2021, 14, 4322. [Google Scholar] [CrossRef]

- Gibas, K.; Glinicki, M.A.; Jóźwiak-Niedźwiedzka, D.; Dąbrowski, M.; Nowowiejski, G.; Gryziński, M. Properties of the Thirty Years Old Concrete in Unfinished Żarnowiec Nuclear Power Plant. Procedia Eng. 2015, 108, 124–130. [Google Scholar] [CrossRef][Green Version]

- Mielczarski, W. Kosztowna energetyka jądrowa. Energetyka 2010, 11, 715–719. [Google Scholar]

- Sainati, T.; Locatelli, G.; Smith, N. Project financing in nuclear new build, why not? The legal and regulatory barriers. Energy Policy 2019, 129, 111–119. [Google Scholar] [CrossRef]

- Tarasova, E. (Non) Alternative energy transitions: Examining neoliberal rationality inofficial nuclear energy discourses of Russia and Poland. Energy Res. Soc. Sci. 2018, 41, 128–135. [Google Scholar] [CrossRef]

- Uchwała nr 141 Rady Ministrów z 2.10.2020 r. w Sprawie Aktualizacji Programu Wieloletniego Pod Nazwą. Program Polskiej Energetyki Jądrowej Monitor Polski; Rada Ministrów: Warsaw, Poland, 2020; p. 946.

- Strzelecki, W. Poland Bets on Nuclear to Meet EU Climate Goals. Nucl. Eng. Int. 2021. Available online: https://www.nsenergybusiness.com/features/poland-climate-goals-nuclear/ (accessed on 23 June 2021).

- Portugal-Pereira, J.; Ferreira, P.; Cunha, J.; Szklo, A.; Schaeffer, R.; Araújo, M. Better late than never, but never late is better: Risk assessment of nuclear power construction projects. Energy Policy 2018, 120, 158–166. [Google Scholar] [CrossRef]

- Slovak Regulator Issues Permit for Commissioning of Mochovce 3. Nuclear Engineering International. Available online: https://www.neimagazine.com/news/newsslovak-regulator-issues-permit-for-commissioning-of-mochovce-3-8749322 (accessed on 23 June 2021).

- Barakah Nuclear Power Plant. Power Technology. Available online: https://www.power-technology.com/projects/barakah-nuclear-power-plant-abu-dhabi/ (accessed on 23 June 2021).

- Młynarski, T.; Tarnawski, M. Źródła Energii i ich Znaczenie dla Bezpieczeństwa Energetycznego w XXI Wieku; Difin: Warszawa, Poland, 2016. [Google Scholar]

- Wnioski z Analiz Prognostycznych na Potrzeby Polityki Energetycznej Polski do 2050 Roku, Załącznik 2; Ministerstwo Klimatu i Środowiska: Warsaw, Poland, 2021.

- Księżopolski, K.; Maśloch, G. Time Delay Approach to Renewable Energy in the Visegrad Group. Energies 2021, 14, 1928. [Google Scholar] [CrossRef]

- Gabryś, H. Elektroenergetyka w Polsce 2020. Energetyka 2020, 8, 365–373. [Google Scholar]

- Robaina, M.; Neves, A. Complete decomposition analysis of CO2 emissions intensity in the transport sector in Europe. Res. Transp. Econ. 2021, 87, 101074. [Google Scholar] [CrossRef]

- Polski Sektor Energetyczny 2050. 4 Scenariusze; Forum Energii: Warsaw, Poland, 2018. [Google Scholar]

- Gürsan, C.; de Gooyert, V. The systemic impact of a transition fuel: Does natural gas help or hinder the energy transition? Renew. Sustain. Energy Rev. 2021, 138, 110552. [Google Scholar] [CrossRef]

- Council Agrees on New Rules for Cross-Border Energy Infrastructure. Available online: https://www.consilium.europa.eu/en/press/press-releases/2021/06/11/council-agrees-on-new-rules-for-cross-border-energy-infrastructure/ (accessed on 29 June 2021).

- Gawlik, L.; Mokrzycki, E. Changes in the Structure of Electricity Generation in Poland in View of the EU Climate Package. Energies 2019, 12, 3323. [Google Scholar] [CrossRef]

- Kochanek, E. Regional cooperation on gas security in Central Europe. Energy Policy J. 2019, 22, 19–38. [Google Scholar] [CrossRef]

- Ruszel, M. Ocena bezpieczeństwa dostaw gazu ziemnego do Polski—Stan obecny i perspektywa do 2025 r. Energy Policy J. 2017, 20, 5–22. [Google Scholar]

- Perspektywy gazu Ziemnego w Elektroenergetyce w Polsce i Unii Europejskiej; Raport DISE; DISE: Wrocław, Poland, 2020.

- ENSTOG 2050. Roadmap Action Plan; Enstog: Brussels, Belgium, 2020. [Google Scholar]

- Ananicz, S.; Buras, P.; Smoleńska, A. Nowy Rozdział. Transformacja Unii Europejskiej a Polska; Fundacja Batorego: Warsaw, Poland, 2021. [Google Scholar]

- Ustawa z dnia 20 maja 2016 r. o inwestycjach w zakresie elektrowni wiatrowych, (Dz.U. 2016 poz. 961). Available online: https://isap.sejm.gov.pl/isap.nsf/DocDetails.xsp?id=WDU20160000961/ (accessed on 23 June 2021).

- Uwagi Rady Przedsiębiorczości do Polityki Energetycznej Polski 2040. Available online: https://kig.pl/wp-content/uploads/2021/05/uwagi-do-polityki-energetycznej-polski-2040.pdf (accessed on 3 July 2021).

- Nagy, S. Dekarbonizacja gospodarki i jej możliwy wpływ na rozwój sektora gazowniczego do roku 2050. Wiad. Naft. Gazow. 2020, 3. [Google Scholar]

- Ruszkowski, P. Bełchatów 2030: Alternatywne scenariusze transformacji. Energ. Społecz. Pol. 2021, 1. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kochanek, E. Evaluation of Energy Transition Scenarios in Poland. Energies 2021, 14, 6058. https://doi.org/10.3390/en14196058

Kochanek E. Evaluation of Energy Transition Scenarios in Poland. Energies. 2021; 14(19):6058. https://doi.org/10.3390/en14196058

Chicago/Turabian StyleKochanek, Ewelina. 2021. "Evaluation of Energy Transition Scenarios in Poland" Energies 14, no. 19: 6058. https://doi.org/10.3390/en14196058

APA StyleKochanek, E. (2021). Evaluation of Energy Transition Scenarios in Poland. Energies, 14(19), 6058. https://doi.org/10.3390/en14196058