Nonlinear Causality between Crude Oil Prices and Exchange Rates: Evidence and Forecasting

Abstract

:1. Introduction

- First, we found strong nonlinear causal relationships between crude oil prices and most investigated exchange rates;

- Second, we showed that the significance of the detected relationships has changed in recent years;

- Third, we applied SVR models of different kernels and regressors to verify if it is possible to exploit the detected relationships for effective forecasting.

2. Materials and Methods

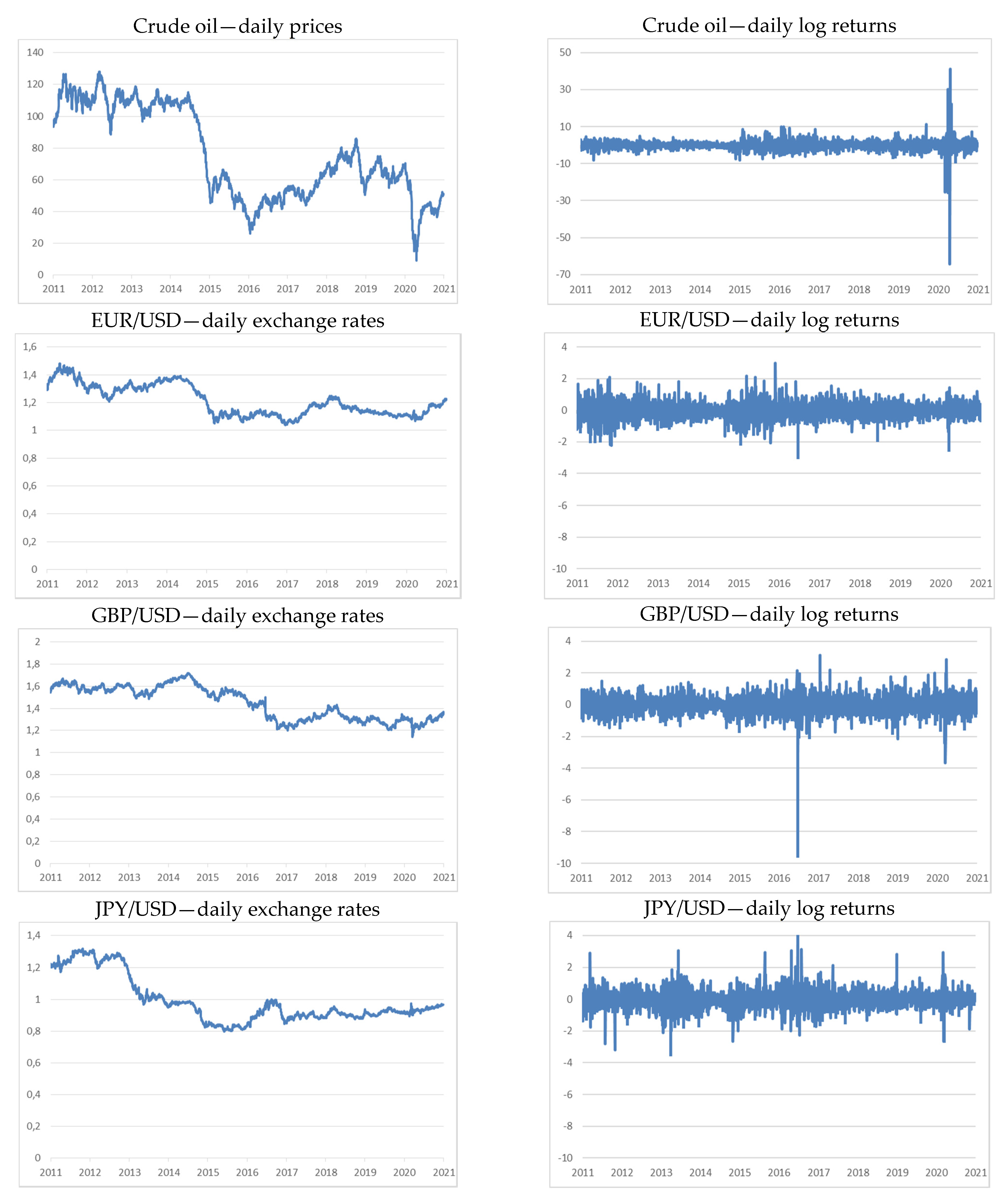

2.1. Data

2.2. Nonlinear Causality Tests

2.3. Support Vector Regression

- Linear: ;

- Radial Basis Function (RBF): ;

- Polynomial: ;

3. Results

3.1. Nonlinear Granger Causality Testing

3.2. Forecasting

- The autoregressive model of type (25) with the linear kernel (SVR_ar_lin);

- The autoregressive model of type (25) with the RBF kernel (SVR_ar_rbf);

- The extended model of type (26) with the linear kernel (SVR_reg_lin);

- The extended model of type (26) with the RBF kernel (SVR_reg_rbf).

4. Discussion

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Beckmann, J.; Czudaj, R.L.; Arora, V. The relationship between oil prices and exchange rates: Revisiting theory and evidence. Energy Econ. 2020, 88, 104772. [Google Scholar] [CrossRef]

- Gomez-Gonzalez, J.E.; Hirs-Garzon, J.; Uribe, J. Giving and receiving: Exploring the predictive causality between oil prices and exchange rates. Int. Financ. 2020, 23, 175–194. [Google Scholar] [CrossRef] [Green Version]

- Liu, Y.; Failler, P.; Peng, J.; Zheng, Y. Time-varying relationship between crude oil price and exchange rate in the context of structural breaks. Energies 2020, 13, 2395. [Google Scholar] [CrossRef]

- Habib, M.M.; Bützer, S.; Stracca, L. Global exchange rate configurations: Do oil shocks matter? IMF Econ. Rev. 2016, 64, 443–470. [Google Scholar] [CrossRef] [Green Version]

- Fratzscher, M.; Schneider, D.; Van Robays, I. Oil Prices, Exchange Rates and Asset Prices; Working Paper no 1689; European Central Bank: Frankfurt, Germany, 2014; pp. 1–45. [Google Scholar]

- Baek, J.; Kim, H.-Y. On the relation between crude oil prices and exchange rates in sub-Saharan African countries: A nonlinear ARDL approach. J. Int. Trade Econ. Dev. 2019, 29, 119–130. [Google Scholar] [CrossRef]

- Brahmasrene, T.; Huang, J.-C.; Sissoko, Y. Crude oil prices and exchange rates: Causality, variance decomposition and impulse response. Energy Econ. 2014, 44, 407–412. [Google Scholar] [CrossRef]

- Wen, F.; Xiao, J.; Huang, C.; Xia, X. Interaction between oil and US dollar exchange rate: Nonlinear causality, time-varying influence and structural breaks in volatility. Appl. Econ. 2017, 50, 319–334. [Google Scholar] [CrossRef]

- Suliman, T.H.M.; Abid, M. The impacts of oil price on exchange rates: Evidence from Saudi Arabia. Energy Explor. Exploit. 2020, 38, 2037–2058. [Google Scholar] [CrossRef]

- Fiszeder, P.; Orzeszko, W. Nonlinear granger causality between grains and livestock, agricultural economics. Zemĕdĕlská Ekon. 2018, 64, 328–336. [Google Scholar]

- Thalassinos, E.J.; Politis, E.D. The Evaluation of the USD currency and the oil prices: A var analysis. Eur. Res. Stud. 2012, 14, 137–146. [Google Scholar]

- Shadab, S.; Gholami, A. Analysis of the relationship between oil prices and exchange rates in Tehran stock exchange. Int. J. Res. Bus. Stud. Manag. 2014, 1, 8–18. [Google Scholar]

- Sharma, N. Cointegration and causality among stock prices, oil prices and exchange rate: Evidence from India. Int. J. Stat. Syst. 2017, 12, 167–174. [Google Scholar]

- Kim, J.-M.; Jung, H. Dependence structure between oil prices, exchange rates, and interest rates. Energy J. 2018, 39. [Google Scholar] [CrossRef] [Green Version]

- Adam, P.; Rosnawintang, R.; Saidi, L.O.; Tondi, L.; Sani, L.O.A. The causal relationship between crude oil price, exchange rate and rice price. Int. J. Energy Econ. Policy 2018, 8, 90–94. [Google Scholar]

- Houcine, B.; Zouheyr, G.; Abdessalam, B.; Youcef, H.; Hanane, A. The relationship between crude oil prices, EUR/USD Exchange rate and gold prices. Int. J. Energy Econ. Policy 2020, 10, 234–242. [Google Scholar] [CrossRef]

- Baek, E.G.; Brock, W.A. A General Test for Nonlinear Granger Causality: Bivariate Model; Technical, Report; Iowa State University: Ames, IA, USA; University of Wisconsin: Madison, WI, USA, 1992. [Google Scholar]

- Hiemstra, C.; Jones, J.D. Testing for linear and nonlinear granger causality in the stock price volume relation. J. Financ. 1994, 49, 1639–1664. [Google Scholar]

- Bekiros, S.D.; Diks, C.G. The relationship between crude oil spot and futures prices: Cointegration, linear and nonlinear causality. Energy Econ. 2008, 30, 2673–2685. [Google Scholar] [CrossRef] [Green Version]

- Benhmad, F. Modeling nonlinear Granger causality between the oil price and U.S. dollar: A wavelet based approach. Econ. Model. 2012, 29, 1505–1514. [Google Scholar] [CrossRef]

- Wang, Y.; Wu, C. Energy prices and exchange rates of the U.S. dollar: Further evidence from linear and nonlinear causality analysis. Econ. Model. 2012, 29, 2289–2297. [Google Scholar] [CrossRef]

- Drachal, K. Exchange rate and oil price interactions in selected CEE countries. Economies 2018, 6, 31. [Google Scholar] [CrossRef] [Green Version]

- Kumar, S. Asymmetric impact of oil prices on exchange rate and stock prices. Q. Rev. Econ. Financ. 2019, 72, 41–51. [Google Scholar] [CrossRef]

- Ajala, K.; Sakanko, M.A.; Adeniji, S.O. The asymmetric effect of oil price on the exchange rate and stock price in Nigeria. Int. J. Energy Econ. Policy 2021, 11, 202–208. [Google Scholar] [CrossRef]

- Hamilton, J.D. This is what happened to the oil price-macroeconomy relationship. J. Monet. Econ. 1996, 38, 215–220. [Google Scholar] [CrossRef]

- Hamilton, J.D. What is an oil shock? J. Econom. 2003, 113, 363–398. [Google Scholar] [CrossRef]

- Hamilton, J.D. Non-linearities and the macroeconomic effects of oil prices. Macroecon. Dyn. 2011, 15, 364–378. [Google Scholar] [CrossRef] [Green Version]

- Elder, J.; Serletis, A. Oil price uncertainty. J. Money Crédit. Bank. 2010, 42, 1137–1159. [Google Scholar] [CrossRef]

- Diks, C.; Panchenko, V. A new statistic and practical guidelines for nonparametric Granger causality testing. J. Econ. Dyn. Control. 2006, 30, 1647–1669. [Google Scholar] [CrossRef] [Green Version]

- Vapnik, V.N.; Golowich, S.; Smola, A. Support vector method for function approximation, regression estimation, and signal processing. In Advances in Neural Information Processing Systems 9; Mozer, M., Jordan, M., Petsche, T., Eds.; MIT Press: Cambridge, MA, USA, 1997; pp. 281–287. [Google Scholar]

- Vapnik, V.N. The Nature of Statistical Learning Theory; Springer: Berlin/Heidelberg, Germany, 1995. [Google Scholar]

- Hsu, M.-W.; Lessmann, S.; Sung, M.-C.; Ma, T.; Johnson, J.E. Bridging the divide in financial market forecasting: Machine learners vs. financial economists. Expert Syst. Appl. 2016, 61, 215–234. [Google Scholar] [CrossRef] [Green Version]

- Makridakis, S.; Spiliotis, E.; Assimakopoulos, V. Statistical and machine learning forecasting methods: Concerns and ways forward. PLoS ONE 2018, 13, e0194889. [Google Scholar] [CrossRef] [Green Version]

- Ryll, L.; Seidens, S. Evaluating the performance of machine learning algorithms in financial market forecasting: A comprehensive survey. arXiv 2019, arXiv:1906.07786. Available online: https://arxiv.org/abs/1906.07786 (accessed on 10 June 2021).

- Fiszeder, P.; Orzeszko, W. Covariance matrix forecasting using support vector regression. Appl. Intell. 2021, 51, 7029–7042. [Google Scholar] [CrossRef]

- Xie, W.; Yu, L.; Xu, S.; Wang, S. A new method for crude oil price forecasting based on support vector machines. In International Conference on Computational Science; Springer: Berlin/Heidelberg, Germany, 2006; pp. 444–451. [Google Scholar]

- Li, S.; Ge, Y. Crude oil price prediction based on a dynamic correcting support vector regression machine. Abstr. Appl. Anal. 2013, 2013, 528678. [Google Scholar]

- Fan, L.; Pan, S.; Li, Z.; Li, H. An ICA-based support vector regression scheme for forecasting crude oil prices. Technol. Forecast. Soc. Chang. 2016, 112, 245–253. [Google Scholar] [CrossRef]

- Li, T.; Zhou, M.; Guo, C.; Luo, M.; Wu, J.; Pan, F.; Tao, Q.; He, T. Forecasting crude oil price using EEMD and RVM with adaptive PSO-based kernels. Energies 2016, 9, 1014. [Google Scholar] [CrossRef] [Green Version]

- Yu, J.; Weng, Y.; Rajagopal, R. Robust mapping rule estimation for power flow analysis in distribution grids. arXiv 2017, arXiv:1702.07948. Available online: https://arxiv.org/abs/1702.07948 (accessed on 10 June 2021).

- Li, T.; Zhou, Y.; Li, X.; Wu, J.; He, T. Forecasting daily crude oil prices using improved CEEMDAN and ridge regression-based predictors. Energies 2019, 12, 3603. [Google Scholar] [CrossRef] [Green Version]

- Ni, H.; Yin, H. Exchange rate prediction using hybrid neural networks and trading indicators. Neurocomputing 2009, 72, 2815–2823. [Google Scholar] [CrossRef]

- Sermpinis, G.; Stasinakis, C.; Theofilatos, K.; Karathanasopoulos, A. Modeling, forecasting and trading the EUR exchange rates with hybrid rolling genetic algorithms—Support vector regression forecast combinations. Eur. J. Oper. Res. 2015, 247, 831–846. [Google Scholar] [CrossRef] [Green Version]

- Fu, S.; Li, Y.; Sun, S.; Li, H. Evolutionary support vector machine for RMB exchange rate forecasting. Phys. Stat. Mech. Appl. 2019, 521, 692–704. [Google Scholar] [CrossRef]

- Nayak, R.K.; Mishra, D.; Rath, A.K. An optimized SVM-k-NN currency exchange forecasting model for Indian currency market. Neural Comput. Appl. 2017, 31, 2995–3021. [Google Scholar] [CrossRef]

- Shen, M.-L.; Lee, C.-F.; Liu, H.-H.; Chang, P.-Y.; Yang, C.-H. An effective hybrid approach for forecasting currency exchange rates. Sustainability 2021, 13, 2761. [Google Scholar] [CrossRef]

- Granger, C.W.J. Testing for causality: A personal viewpoint. J. Econ. Dyn. Control. 1980, 2, 329–352. [Google Scholar] [CrossRef]

- Denker, M.; Keller, G. On U-statistics and von mises’ statistics for weakly dependent processes. Z. Wahrscheinlichkeitstheorie Verwandte Geb. 1983, 64, 505–522. [Google Scholar] [CrossRef]

- Diks, C.; Panchenko, V. A note on the Hiemstra-Jones test for granger non-causality. Stud. Nonlinear Dyn. Econ. 2005, 9. [Google Scholar] [CrossRef]

- Francis, B.B.; Mougoue, M.; Panchenko, V. Is there a symmetric nonlinear causal relationship between large and small firms? J. Empir. Financ. 2010, 17, 23–38. [Google Scholar] [CrossRef]

- Smola, A.J.; Schölkopf, B. A tutorial on support vector regression. Stat. Comput. 2004, 14, 199–222. [Google Scholar] [CrossRef] [Green Version]

- Cherkassky, V.; Ma, Y. Practical selection of SVM parameters and noise estimation for SVM regression. Neural Netw. 2004, 17, 113–126. [Google Scholar] [CrossRef] [Green Version]

- Lee, S.; Kim, C.K.; Lee, S. Hybrid CUSUM change point test for time series with time-varying volatilities based on support vector regression. Entropy 2020, 22, 578. [Google Scholar] [CrossRef]

- Martínez-Álvarez, F.; Troncoso, A.; Asencio-Cortés, G.; Riquelme, J.C. A survey on data mining techniques applied to electricity-related time series forecasting. Energies 2015, 8, 13162–13193. [Google Scholar] [CrossRef] [Green Version]

- Fałdziński, M.; Fiszeder, P.; Orzeszko, W. Forecasting volatility of energy commodities: Comparison of GARCH models with support vector regression. Energies 2020, 14, 6. [Google Scholar] [CrossRef]

- Peng, L.-L.; Fan, G.-F.; Huang, M.-L.; Hong, W.-C. Hybridizing DEMD and quantum PSO with SVR in electric load forecasting. Energies 2016, 9, 221. [Google Scholar] [CrossRef]

- Gavrishchaka, V.V.; Ganguli, S.B. Volatility forecasting from multiscale and high-dimensional market data. Neurocomputing 2003, 55, 285–305. [Google Scholar] [CrossRef]

- Awad, M.; Khanna, R. Support vector regression. In Efficient Learning Machines; Awad, M., Khanna, R., Eds.; Apress: Berkeley, CA, USA, 2015; pp. 67–80. [Google Scholar]

- Santamaría-Bonfil, G.; Frausto-Solís, J.; Vázquez-Rodarte, I. Volatility forecasting using support vector regression and a hybrid genetic algorithm. Comput. Econ. 2013, 45, 111–133. [Google Scholar] [CrossRef]

- Wang, H.; Xu, D. Parameter selection method for support vector regression based on adaptive fusion of the mixed kernel function. J. Control Sci. Eng. 2017, 2017, 1–12. [Google Scholar] [CrossRef]

- Probst, P.; Bischl, B.; Boulesteix, A.-L. Tunability: Importance of hyperparameters of machine learning algorithms. J. Mach. Learn. Res. 2019, 20, 1–32. [Google Scholar]

- Gelbart, M.; Snoek, J.; Adams, R.P. Bayesian optimization with unknown constraints. arXiv 2014, arXiv:1403.5607. Available online: https://arxiv.org/abs/1403.5607 (accessed on 10 June 2021).

- Bayat, T.; Nazlioglu, S.; Kayhan, S. Exchange rate and oil price interactions in transition economies: Czech Republic, Hungary and Poland. Panoeconomicus 2015, 62, 267–285. [Google Scholar] [CrossRef]

- Chen, Y.-C.; Rogoff, K.S.; Rossi, B. Can exchange rates forecast commodity prices? Q. J. Econ. 2010, 125, 1145–1194. [Google Scholar] [CrossRef] [Green Version]

- Alquist, R.; Kilian, L.; Vigfusson, R.J. Forecasting the price of oil. In Handbook of Economic Forecasting; Elliott, G., Granger, C., Timmermann, A., Eds.; Elsevier: Amsterdam, The Netherlands, 2013; pp. 427–507. [Google Scholar]

- Meese, R.A.; Rogoff, K. Empirical exchange rate models of the seventies: Do they fit out of sample? J. Int. Econ. 1983, 14, 3–24. [Google Scholar] [CrossRef]

- Rossi, B. Exchange rate predictability. J. Econ. Lit. 2013, 51, 1063–1119. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

| Mean | Min | Max | SD | Skew | Kurt | LB(10) | |

|---|---|---|---|---|---|---|---|

| 3 January 2011–31 December 2020 | |||||||

| Crude oil | −0.024 | −64.370 | 41.202 | 2.920 | −3.270 | 121.79 | 0.000 |

| EUR/USD | −0.002 | −2.948 | 2.962 | 0.526 | −0.087 | 2.123 | 0.382 |

| GBP/USD | −0.005 | −9.505 | 3.130 | 0.572 | −1.809 | 31.663 | 0.263 |

| JPY/USD | −0.009 | −3.466 | 4.136 | 0.564 | 0.113 | 5.298 | 0.655 |

| 3 January 2011–31 December 2015 (Period 1) | |||||||

| Crude oil | −0.074 | −8.245 | 8.508 | 1.696 | −0.062 | 3.175 | 0.051 |

| EUR/USD | −0.015 | −2.230 | 2.962 | 0.595 | −0.012 | 1.524 | 0.485 |

| GBP/USD | −0.003 | −1.649 | 1.490 | 0.462 | −0.085 | 0.562 | 0.250 |

| JPY/USD | −0.031 | −3.466 | 3.032 | 0.577 | −0.221 | 4.110 | 0.402 |

| 4 January 2016–31 December 2020 (Period 2) | |||||||

| Crude oil | 0.026 | −64.370 | 41.202 | 3.756 | −3.081 | 87.576 | 0.000 |

| EUR/USD | 0.010 | −2.948 | 1.803 | 0.448 | −0.186 | 2.507 | 0.718 |

| GBP/USD | −0.007 | −9.505 | 3.130 | 0.664 | −2.271 | 34.228 | 0.339 |

| JPY/USD | 0.013 | −2.653 | 4.136 | 0.551 | 0.503 | 6.583 | 0.244 |

| Test | Number of Lags lx = ly | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | ||

| BrentEUR/USD (Period 1) | |||||||||

| 1 | H-J | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| D-P | 0.0001 | 0.0000 | 0.0004 | 0.0022 | 0.0039 | 0.0055 | 0.0170 | 0.0257 | |

| 1.5 | H-J | 0.0005 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| D-P | 0.0007 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0002 | |

| BrentEUR/USD (Period 2) | |||||||||

| 1 | H-J | 0.1128 | 0.3092 | 0.1869 | 0.3024 | 0.3411 | 0.1714 | 0.1495 | 0.1228 |

| D-P | 0.1183 | 0.3502 | 0.2668 | 0.4334 | 0.5253 | 0.2647 | 0.3567 | 0.2685 | |

| 1.5 | H-J | 0.0724 | 0.2511 | 0.1410 | 0.2270 | 0.2121 | 0.2871 | 0.2542 | 0.2738 |

| D-P | 0.0737 | 0.2548 | 0.1481 | 0.2267 | 0.2526 | 0.3231 | 0.2894 | 0.2821 | |

| EUR/USDBrent(Period 1) | |||||||||

| 1 | H-J | 0.0017 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| D-P | 0.0028 | 0.0000 | 0.0015 | 0.0013 | 0.0031 | 0.0192 | 0.0175 | 0.0175 | |

| 1.5 | H-J | 0.0242 | 0.0001 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| D-P | 0.0240 | 0.0001 | 0.0000 | 0.0000 | 0.0000 | 0.0001 | 0.0001 | 0.0003 | |

| EUR/USDBrent(Period 2) | |||||||||

| 1 | H-J | 0.2438 | 0.0659 | 0.2864 | 0.3981 | 0.6039 | 0.4586 | 0.5040 | 0.4584 |

| D-P | 0.2785 | 0.0811 | 0.3206 | 0.4528 | 0.5708 | 0.4194 | 0.5161 | 0.4944 | |

| 1.5 | H-J | 0.0812 | 0.0564 | 0.3510 | 0.2544 | 0.4281 | 0.3952 | 0.4743 | 0.5211 |

| D-P | 0.0798 | 0.0665 | 0.3918 | 0.2936 | 0.4838 | 0.4705 | 0.5652 | 0.5735 | |

| Test | Number of Lags lx = ly | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | ||

| BrentGBP/USD (Period 1) | |||||||||

| 1 | H-J | 0.0154 | 0.0017 | 0.0006 | 0.0000 | 0.0000 | 0.0002 | 0.0003 | 0.0089 |

| D-P | 0.0200 | 0.0059 | 0.0079 | 0.0064 | 0.0138 | 0.0290 | 0.0474 | 0.1421 | |

| 1.5 | H-J | 0.1482 | 0.0029 | 0.0026 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| D-P | 0.1692 | 0.0047 | 0.0069 | 0.0012 | 0.0009 | 0.0003 | 0.0002 | 0.0009 | |

| BrentGBP/USD (Period 2) | |||||||||

| 1 | H-J | 0.0132 | 0.2492 | 0.1748 | 0.0290 | 0.0134 | 0.0075 | 0.0130 | 0.0657 |

| D-P | 0.0154 | 0.3152 | 0.2010 | 0.0493 | 0.0344 | 0.0410 | 0.0453 | 0.1207 | |

| 1.5 | H-J | 0.0047 | 0.0308 | 0.0162 | 0.0023 | 0.0015 | 0.0005 | 0.0003 | 0.0006 |

| D-P | 0.0046 | 0.0399 | 0.0192 | 0.0028 | 0.0023 | 0.0012 | 0.0008 | 0.0020 | |

| GBP/USDBrent(Period 1) | |||||||||

| 1 | H-J | 0.0477 | 0.0017 | 0.0030 | 0.0007 | 0.0014 | 0.0079 | 0.0140 | 0.0206 |

| D-P | 0.0574 | 0.0041 | 0.0130 | 0.0166 | 0.0339 | 0.0544 | 0.0562 | 0.0785 | |

| 1.5 | H-J | 0.0669 | 0.0026 | 0.0087 | 0.0006 | 0.0012 | 0.0033 | 0.0061 | 0.0029 |

| D-P | 0.0716 | 0.0027 | 0.0129 | 0.0035 | 0.0069 | 0.0163 | 0.0235 | 0.0149 | |

| GBP/USDBrent(Period 2) | |||||||||

| 1 | H-J | 0.0186 | 0.1343 | 0.5399 | 0.1944 | 0.1731 | 0.1291 | 0.0985 | 0.1465 |

| D-P | 0.0212 | 0.1805 | 0.5493 | 0.2012 | 0.1657 | 0.1406 | 0.1829 | 0.2603 | |

| 1.5 | H-J | 0.0315 | 0.0628 | 0.4332 | 0.1904 | 0.2265 | 0.1261 | 0.0164 | 0.0104 |

| D-P | 0.0311 | 0.0644 | 0.4081 | 0.1787 | 0.2515 | 0.1579 | 0.0269 | 0.0181 | |

| Test | Number of Lags lx = ly | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | ||

| BrentJPY/USD (Period 1) | |||||||||

| 1 | H-J | 0.3999 | 0.3858 | 0.6696 | 0.3276 | 0.2312 | 0.0538 | 0.0321 | 0.0092 |

| D-P | 0.4608 | 0.3947 | 0.6248 | 0.2041 | 0.2074 | 0.1337 | 0.0980 | 0.0925 | |

| 1.5 | H-J | 0.5198 | 0.6875 | 0.8965 | 0.9217 | 0.9594 | 0.8297 | 0.5170 | 0.3306 |

| D-P | 0.5192 | 0.7003 | 0.9109 | 0.9355 | 0.9686 | 0.8229 | 0.4534 | 0.3344 | |

| BrentJPY/USD (Period 2) | |||||||||

| 1 | H-J | 0.0405 | 0.3544 | 0.3852 | 0.4075 | 0.3559 | 0.4972 | 0.7010 | 0.7573 |

| D-P | 0.0579 | 0.4407 | 0.5160 | 0.5377 | 0.4822 | 0.5730 | 0.6791 | 0.6939 | |

| 1.5 | H-J | 0.0293 | 0.2695 | 0.2326 | 0.1326 | 0.1741 | 0.3503 | 0.5965 | 0.5193 |

| D-P | 0.0328 | 0.3097 | 0.2666 | 0.1528 | 0.2097 | 0.3706 | 0.6288 | 0.5560 | |

| JPY/USDBrent(Period 1) | |||||||||

| 1 | H-J | 0.5404 | 0.7095 | 0.5646 | 0.1271 | 0.0053 | 0.0042 | 0.0066 | 0.0039 |

| D-P | 0.5813 | 0.6788 | 0.4553 | 0.1219 | 0.0326 | 0.0267 | 0.0437 | 0.0567 | |

| 1.5 | H-J | 0.5028 | 0.8275 | 0.8776 | 0.5392 | 0.3383 | 0.3392 | 0.2614 | 0.1260 |

| D-P | 0.5102 | 0.8482 | 0.8728 | 0.4764 | 0.2832 | 0.2534 | 0.1995 | 0.1070 | |

| JPY/USDBrent(Period 2) | |||||||||

| 1 | H-J | 0.0133 | 0.0027 | 0.0136 | 0.1000 | 0.2297 | 0.4628 | 0.2631 | 0.1618 |

| D-P | 0.0192 | 0.0049 | 0.0242 | 0.1400 | 0.2772 | 0.4756 | 0.2513 | 0.1392 | |

| 1.5 | H-J | 0.0042 | 0.0004 | 0.0002 | 0.0008 | 0.0034 | 0.0129 | 0.0141 | 0.0142 |

| D-P | 0.0037 | 0.0003 | 0.0002 | 0.0006 | 0.0034 | 0.0160 | 0.0207 | 0.0239 | |

| Modeled Relationship | |

|---|---|

| BrentEUR/USD | 3 |

| EUR/USDBrent | 2 |

| BrentGBP/USD | 6 |

| GBP/USDBrent | 8 |

| BrentJPY/USD | 8 |

| JPY/USDBrent | 8 |

| Modeled Relation | Period | Model | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| WN | SVR_ar_lin | SVR_ar_rbf | SVR_reg_lin | SVR_reg_rbf | |||||||

| MAE | MSE | MAE | MSE | MAE | MSE | MAE | MSE | MAE | MSE | ||

| BrentEUR/USD | Period 1 | 0.430 | 0.352 | 0.434 | 0.363 | 0.431 | 0.352 | 0.431 | 0.353 | 0.431 | 0.353 |

| Period 2 | 0.304 | 0.162 | 0.308 | 0.164 | 0.303 | 0.161 | 0.313 | 0.180 | 0.303 | 0.161 | |

| EUR/USDBrent | Period 1 | 1.353 | 3.924 | 1.359 | 3.943 | 1.359 | 3.943 | 1.359 | 3.943 | 1.359 | 3.943 |

| Period 2 | 2.512 | 27.948 | 2.513 | 27.616 | 2.501 | 27.749 | 2.519 | 28.540 | 2.515 | 27.934 | |

| BrentGBP/USD | Period 1 | 0.332 | 0.202 | 0.332 | 0.203 | 0.331 | 0.202 | 0.345 | 0.217 | 0.331 | 0.202 |

| Period 2 | 0.453 | 0.389 | 0.452 | 0.389 | 0.453 | 0.388 | 0.466 | 0.450 | 0.455 | 0.391 | |

| GBP/USDBrent | Period 1 | 1.353 | 3.924 | 1.360 | 3.972 | 1.361 | 3.929 | 1.371 | 4.041 | 1.361 | 3.958 |

| Period 2 | 2.512 | 27.948 | 2.526 | 27.925 | 2.529 | 28.096 | 2.558 | 29.170 | 2.518 | 27.987 | |

| BrentJPY/USD | Period 1 | 0.358 | 0.250 | 0.360 | 0.256 | 0.360 | 0.252 | 0.368 | 0.269 | 0.359 | 0.251 |

| Period 2 | 0.303 | 0.221 | 0.326 | 0.341 | 0.305 | 0.222 | 0.323 | 0.264 | 0.304 | 0.222 | |

| JPY/USDBrent | Period 1 | 1.353 | 3.924 | 1.369 | 3.997 | 1.353 | 3.933 | 1.358 | 3.962 | 1.356 | 3.944 |

| Period 2 | 2.512 | 27.948 | 2.504 | 27.846 | 2.717 | 41.748 | 2.513 | 27.834 | 2.599 | 30.809 | |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Orzeszko, W. Nonlinear Causality between Crude Oil Prices and Exchange Rates: Evidence and Forecasting. Energies 2021, 14, 6043. https://doi.org/10.3390/en14196043

Orzeszko W. Nonlinear Causality between Crude Oil Prices and Exchange Rates: Evidence and Forecasting. Energies. 2021; 14(19):6043. https://doi.org/10.3390/en14196043

Chicago/Turabian StyleOrzeszko, Witold. 2021. "Nonlinear Causality between Crude Oil Prices and Exchange Rates: Evidence and Forecasting" Energies 14, no. 19: 6043. https://doi.org/10.3390/en14196043

APA StyleOrzeszko, W. (2021). Nonlinear Causality between Crude Oil Prices and Exchange Rates: Evidence and Forecasting. Energies, 14(19), 6043. https://doi.org/10.3390/en14196043