The Environmental Aspect in the Concept of Corporate Social Responsibility in the Energy Industry and Sustainable Development of the Economy

Abstract

:1. Introduction

2. Corporate Social Responsibility and Sustainable Development—Review of the Literature

2.1. Corporate Social Responsibility—The Idea and the Possibility of Using

2.2. CSR and Sustainable Development in the Energy Industry

3. Materials and Methods

4. Results

4.1. General Analysis

- −

- Environmental management system;

- −

- Reporting;

- −

- Environmental routines;

- −

- Environmental policies;

- −

- GHG emissions;

- −

- Energy consumption;

- −

- ISO/EMAS certification;

- −

- Environmental requirements inside the supply chain.

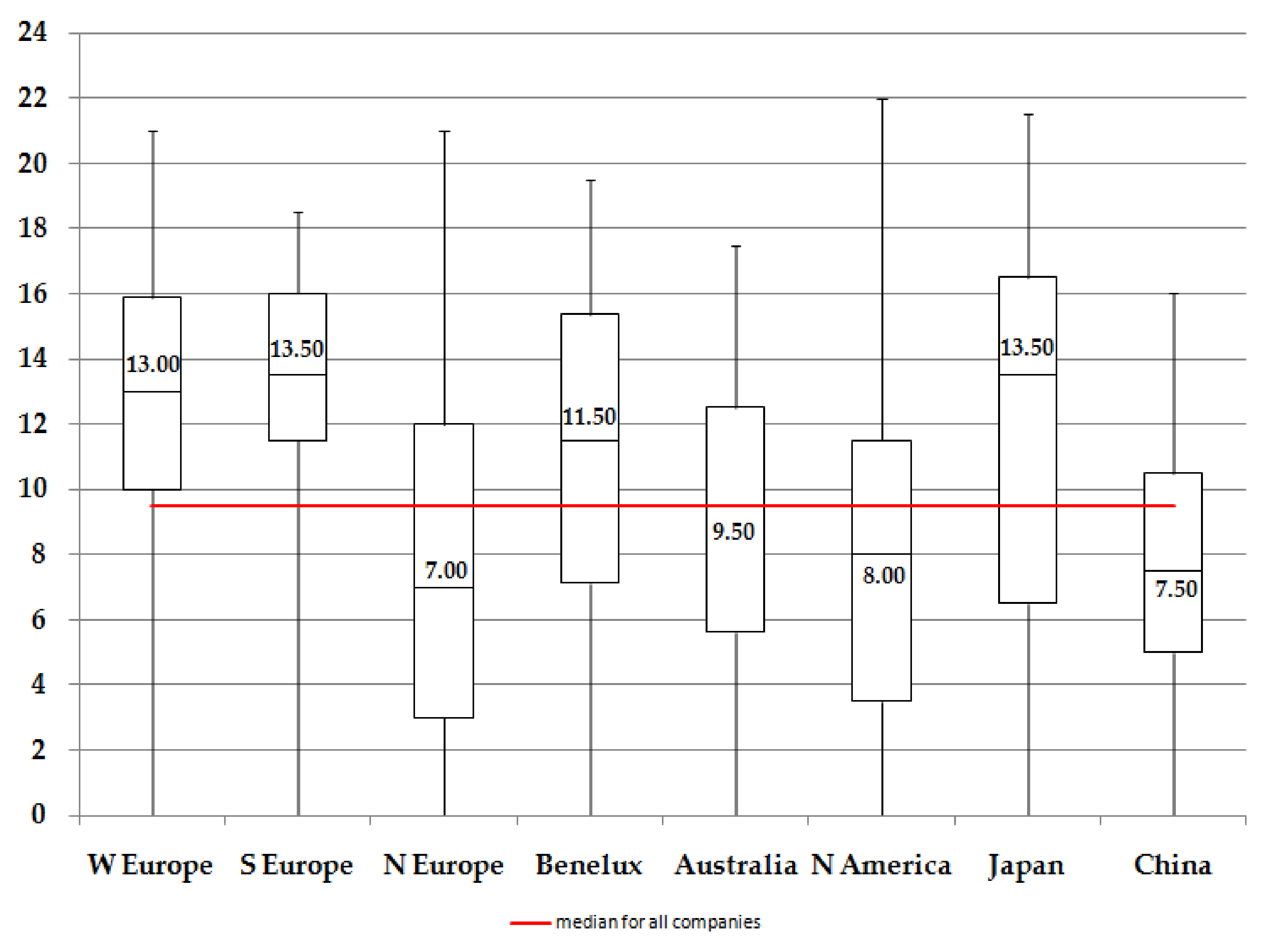

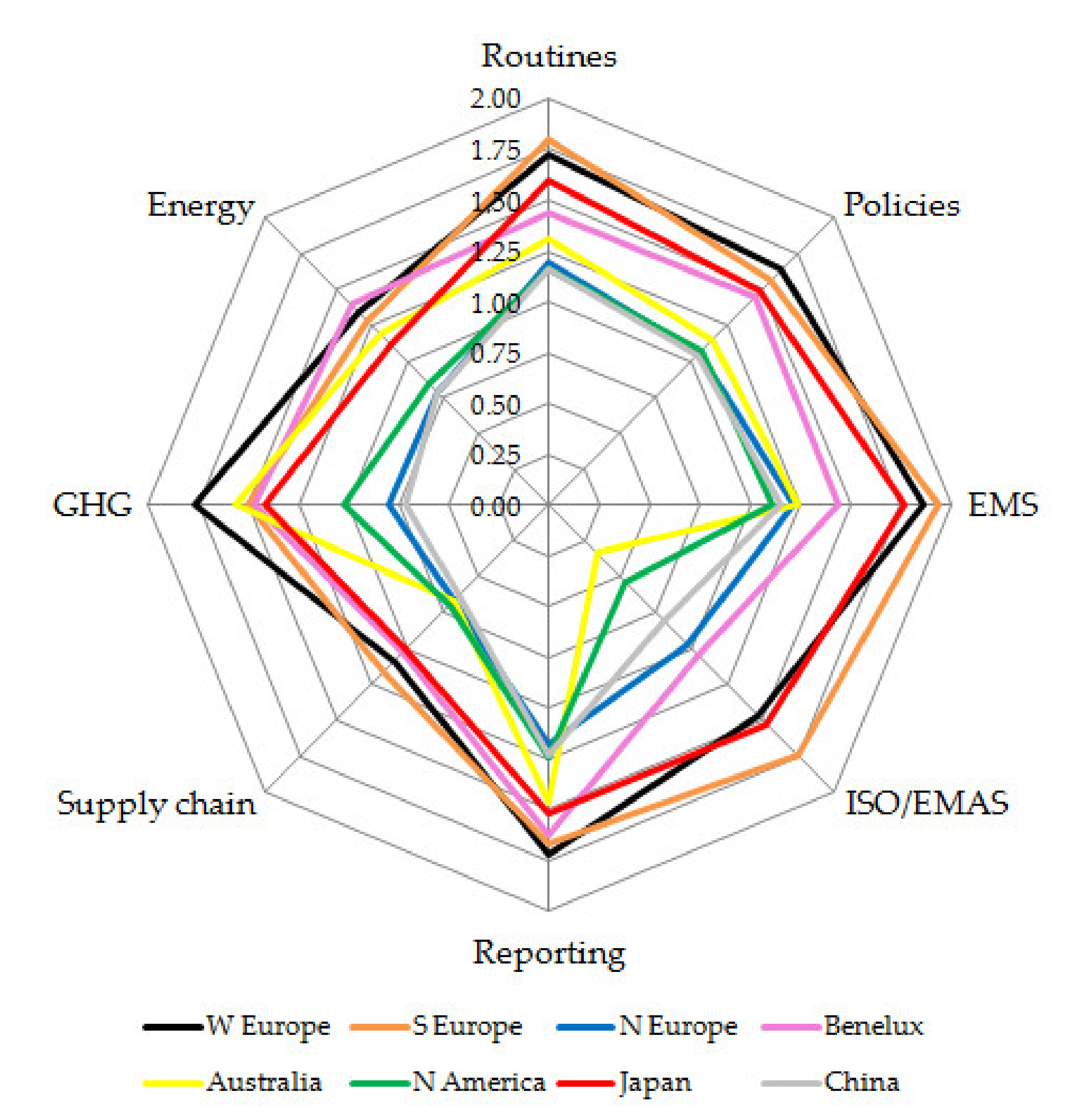

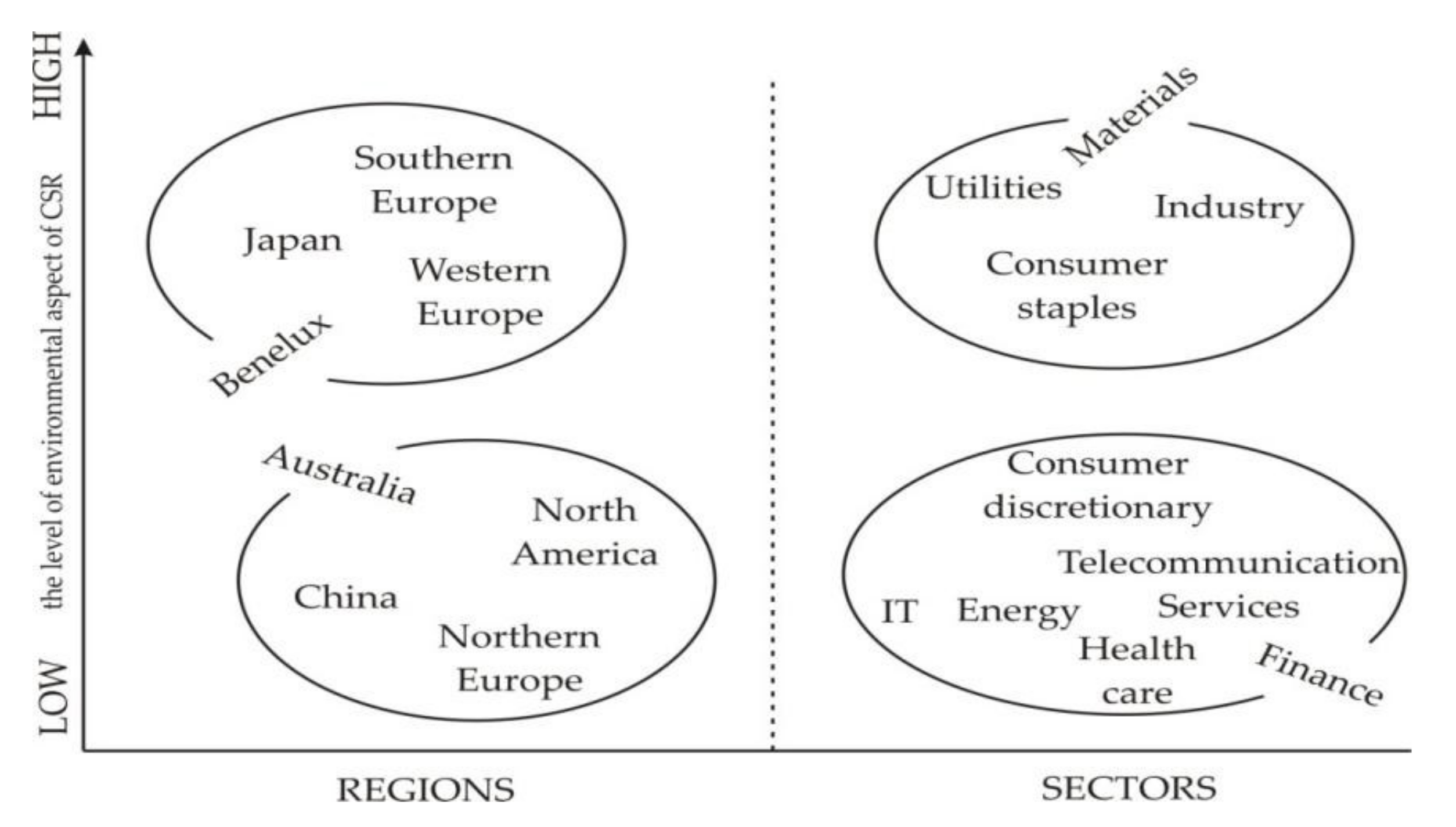

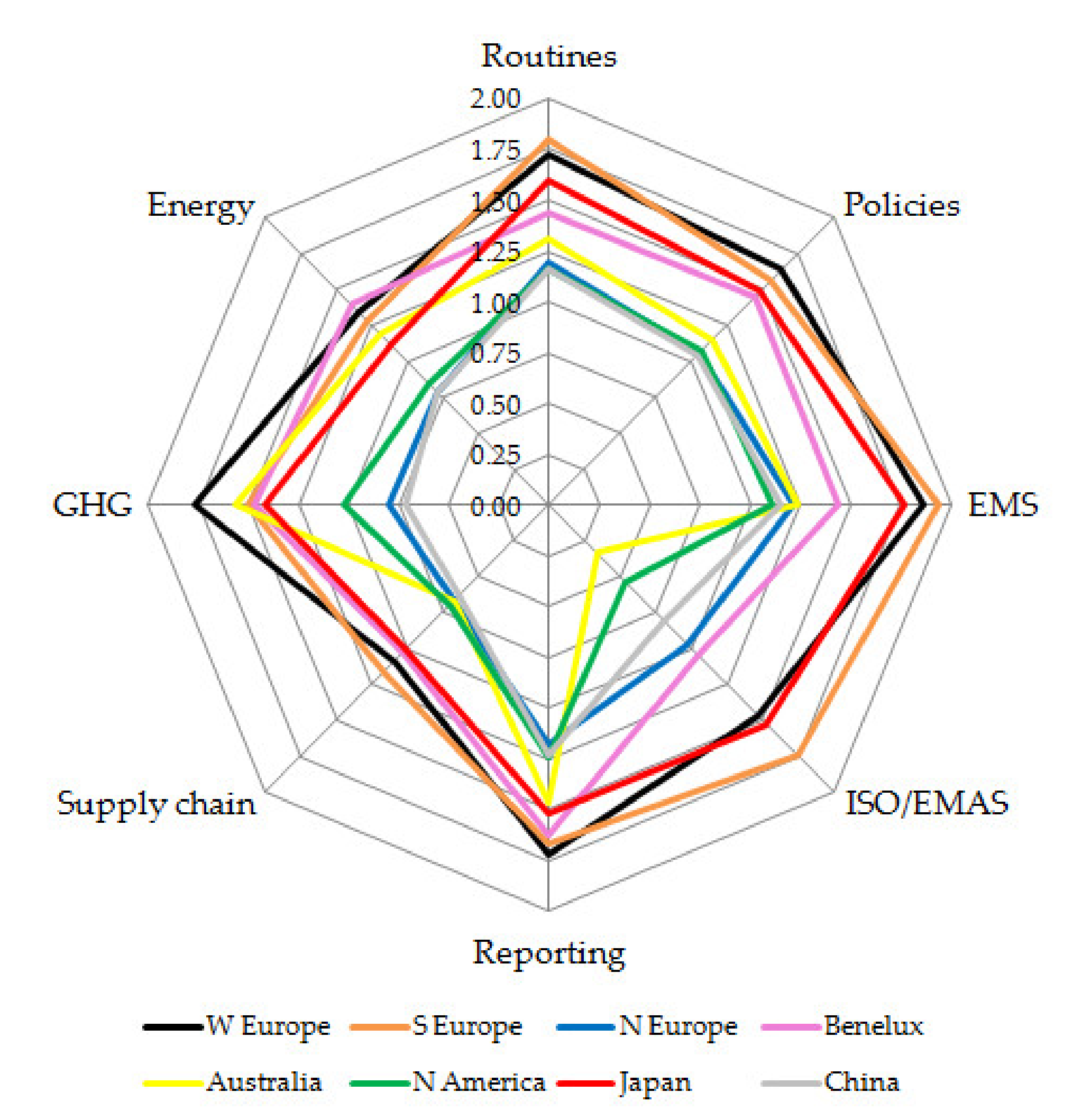

4.2. Regional Comparative Analysis

- −

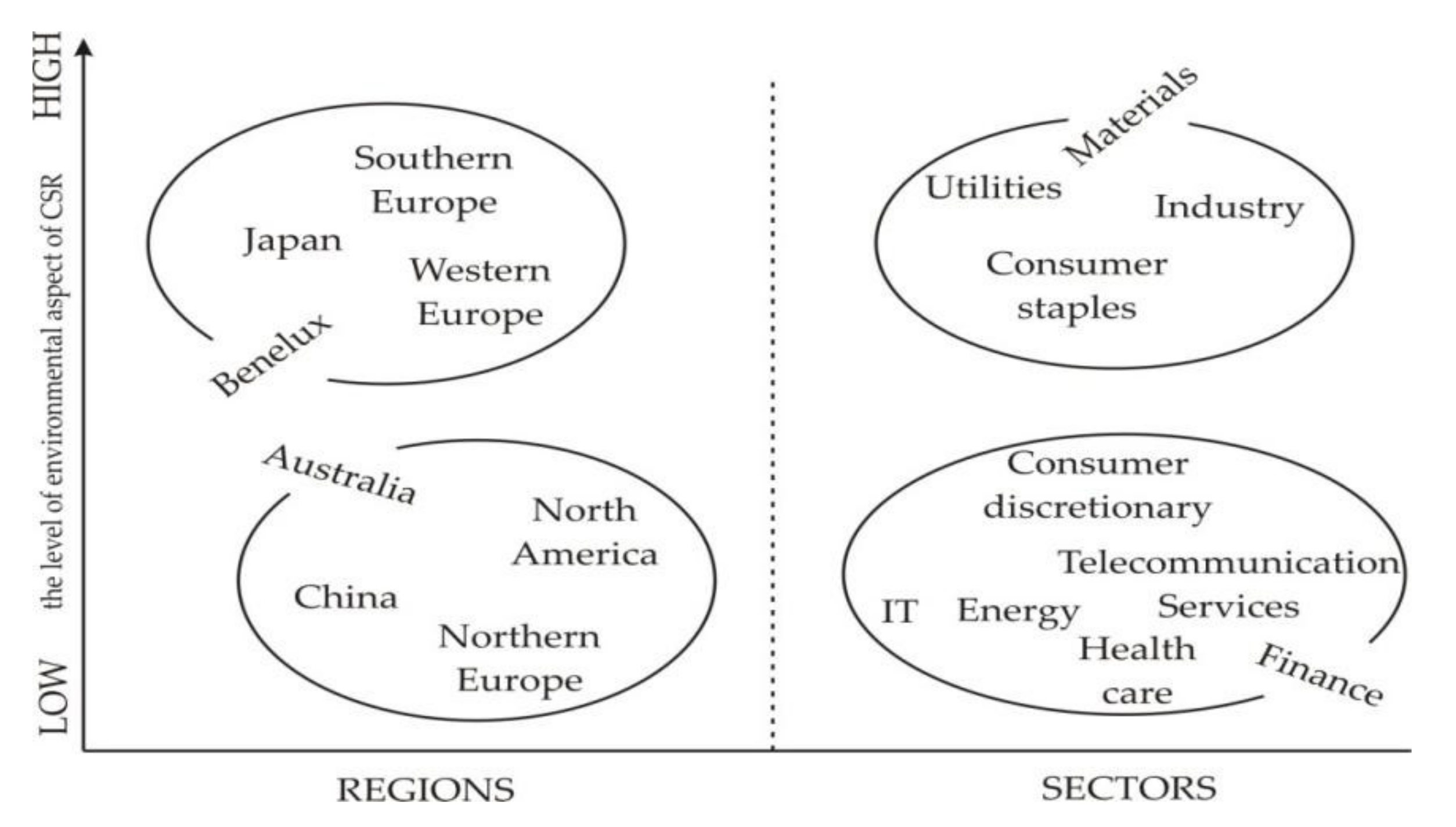

- China, North America, Northern Europe and Australia were the lowest rated regions in terms of the environmental aspect of CSR;

- −

- The highest rated regions were Southern Europe, Western Europe and Japan;

- −

- There was a noticeable problem in the field of supply chains and consumption energy, which is clearly an area for improvement for all regions, as it is a key area for all economies;

- −

- Factors related to management, such as reporting and implementation of the environmental management system, constituted the best-assessed area, which is certainly part of the marketing activities of companies and legal restrictions;

- −

- Large discrepancies could be observed between the perceptions of ISO 14001/EMAS certification systems and standards across countries. This may be the result of trends and fashion in the scope of applied certificates and their departure from them in individual countries. These differences are very noticeable and show that this certification has its supporters and opponents.

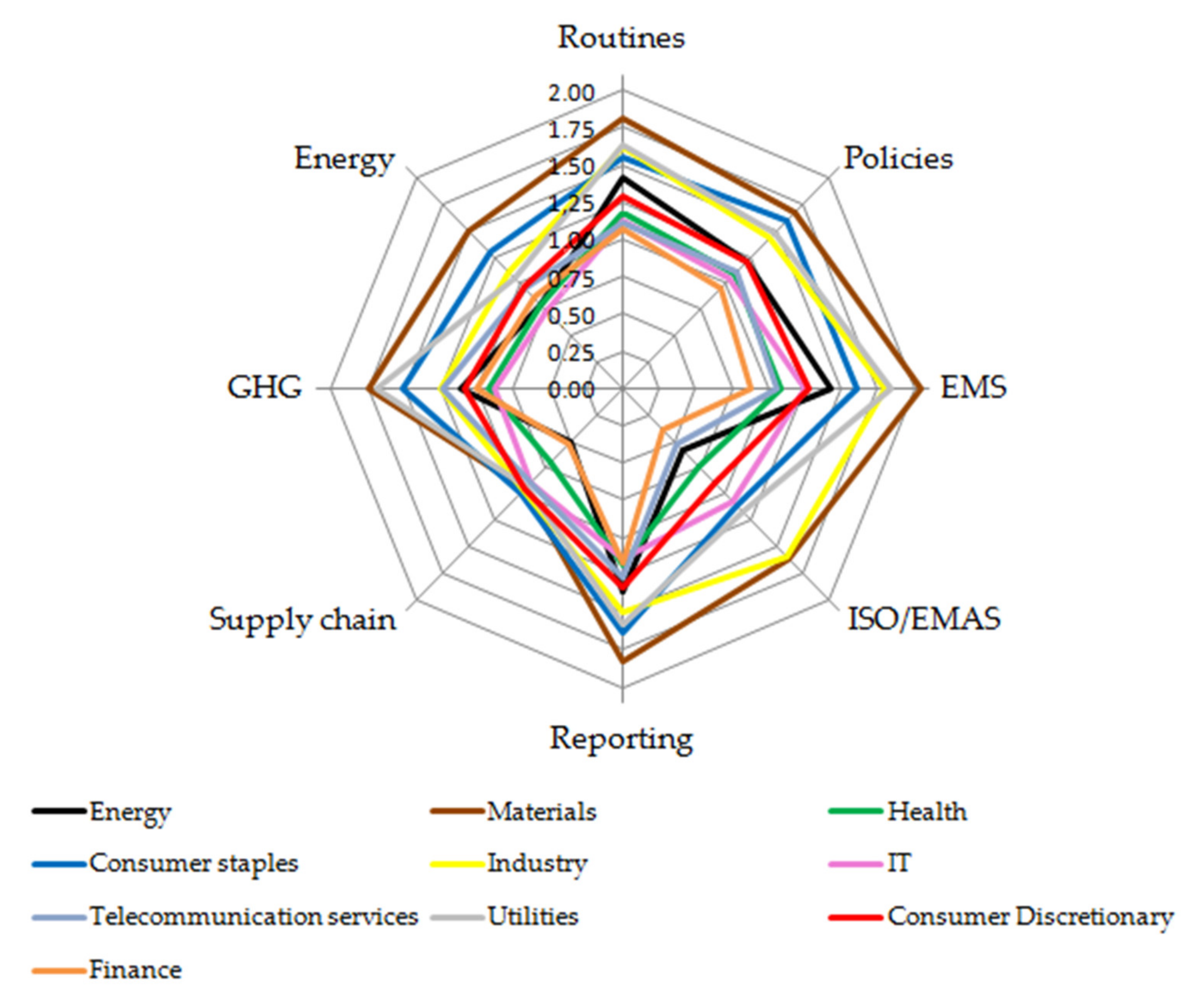

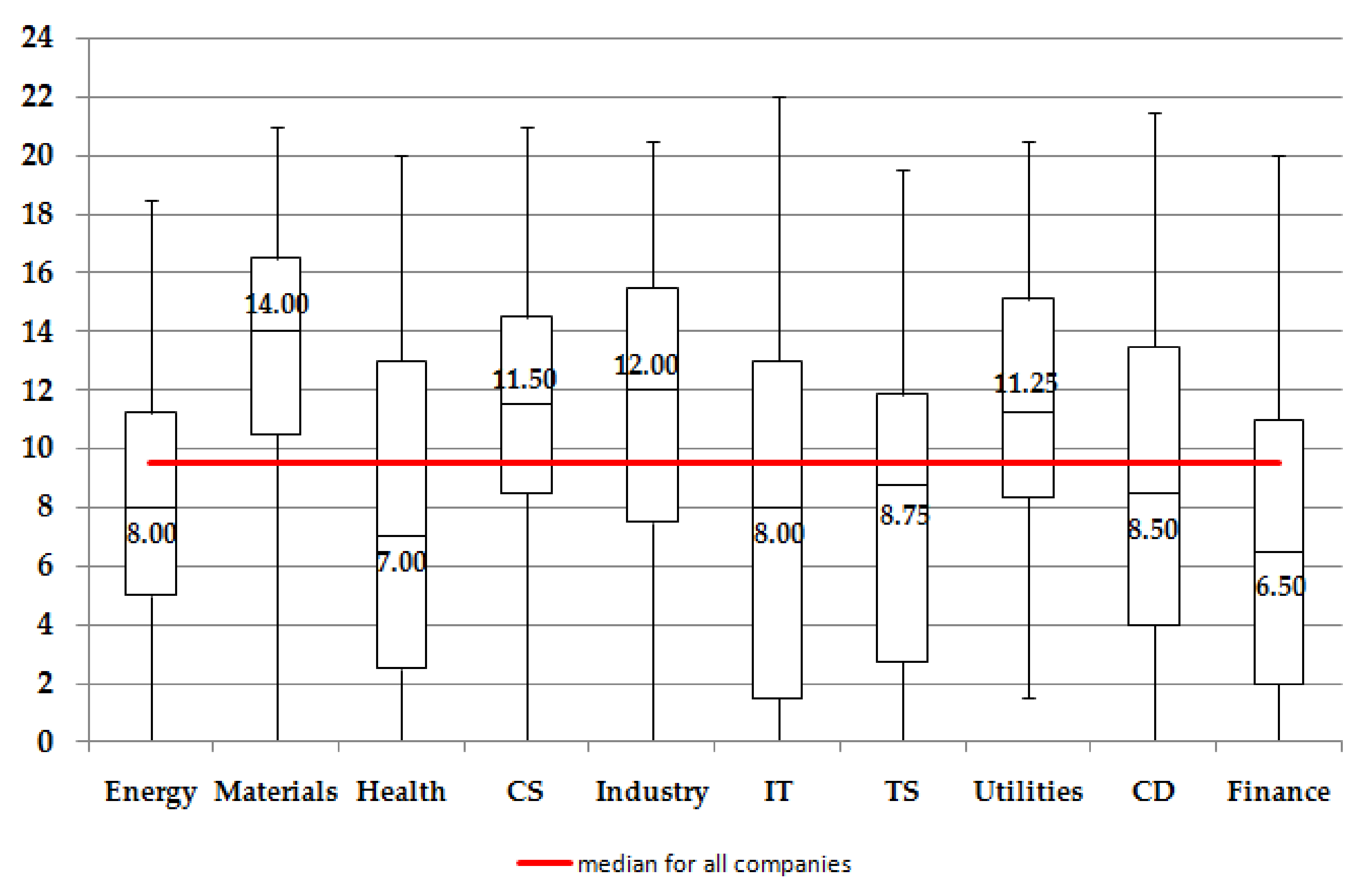

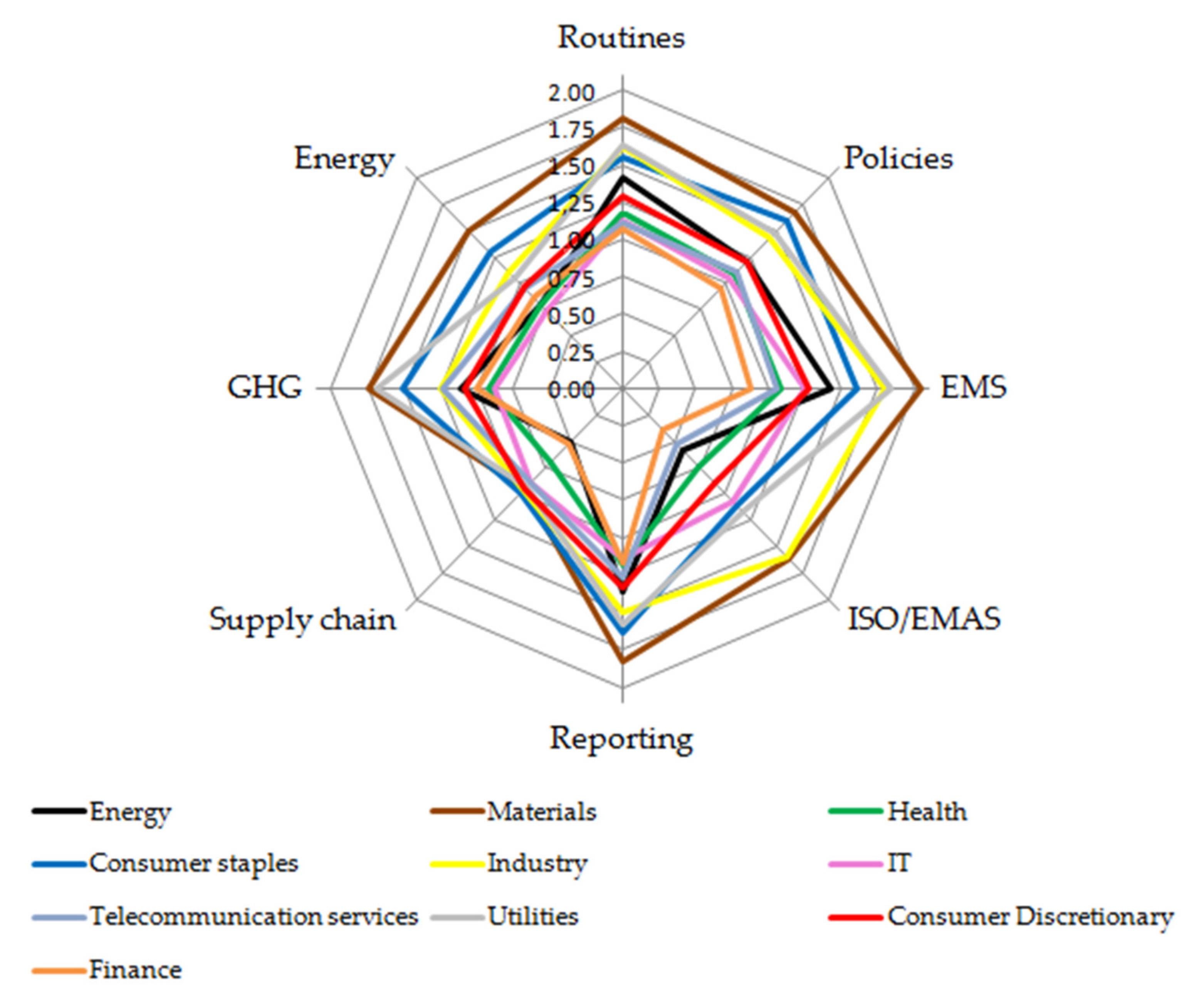

4.3. Sector Comparative Analysis

- −

- The widest spread of the grades was in ISO 14001/EMAS certification, which shows that there are different approaches to the application of ISO and EMAS certification in different sectors;

- −

- The smallest span was observed in environmental requirements in supply chain, and thus, these are areas for improvement in all sectors;

- −

- The highest rated sectors were materials, industry, telecommunication services, consumer staples and utilities;

- −

- The lowest rated sectors were finances, telecommunication services and health care;

- −

- Just like in the regional analysis, in the sector analysis, routines and implementation of environmental management systems (EMS) were rated the highest.

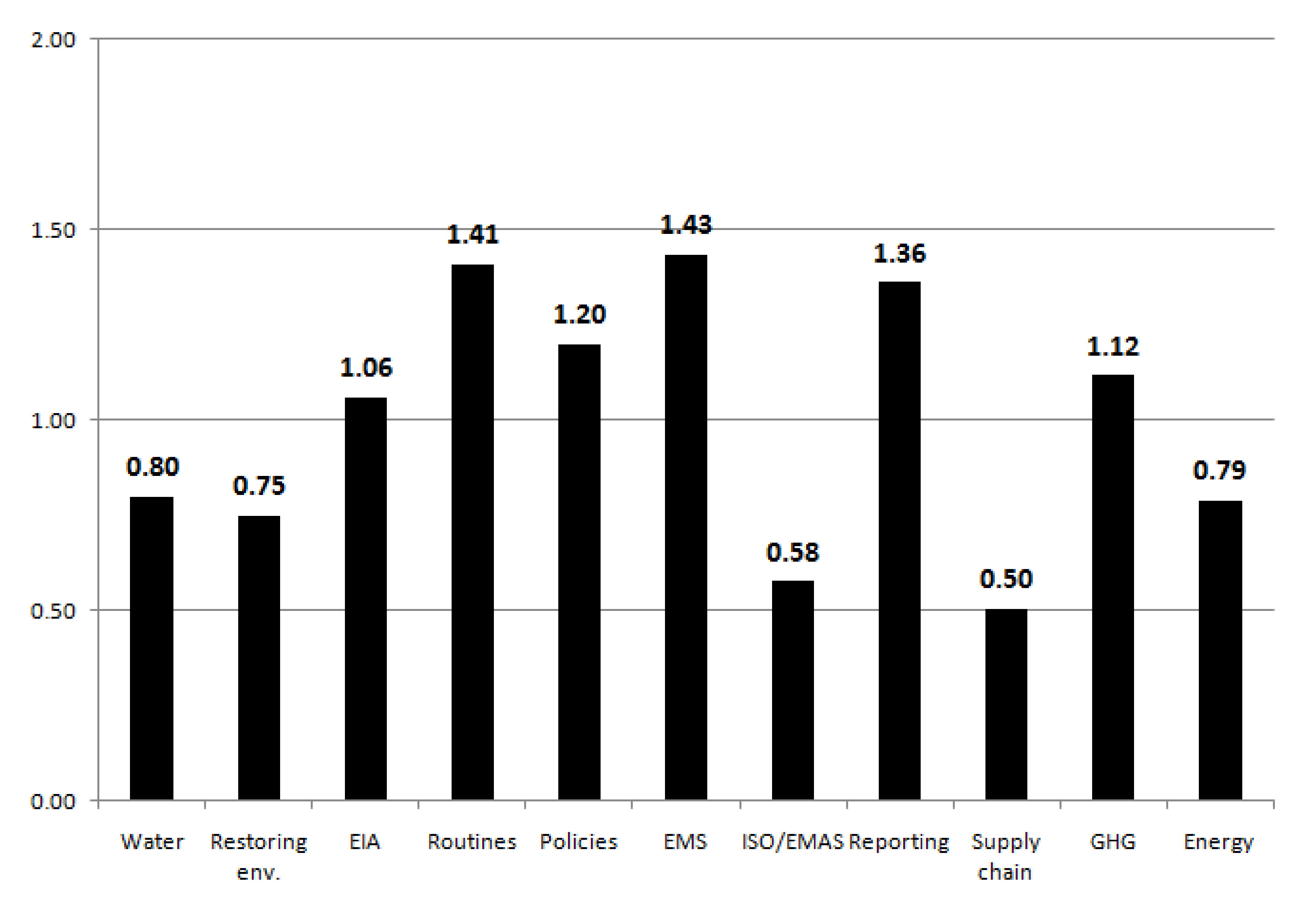

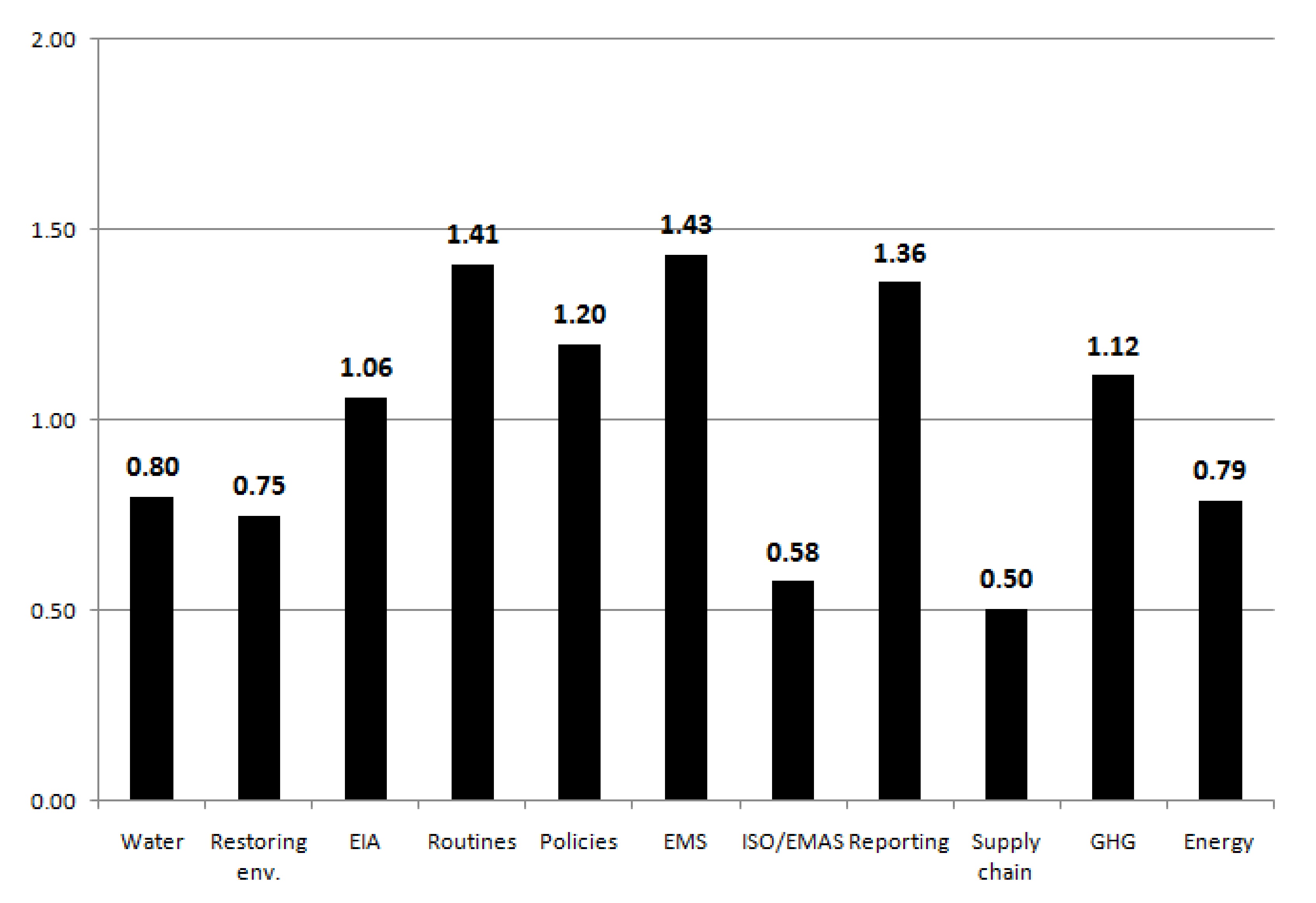

- −

- How has the amount of water consumption changed over time? (Water)

- −

- Is the company taking its responsibilities towards restoring the environment? (Restoring env.)

- −

- Does the company conduct environmental impact assessment in its project development process? (EIA)

- −

- It was worse compared to other sectors of the economy, especially in Northern Europe, North America and China;

- −

- It was in the middle position compared to other sectors;

- −

- CSR in supply chains and ISO 14001/EMAS certification were the worst performers, just like in other sectors. However, when it comes to supply chains, the energy industry has the lowest index. This may be related to the monopoly in this type of production and the reluctance to cooperate with other actors in the supply chain, as these enterprises are the main cooperators of the supply chains;

- −

- Unfortunately, the energy sector was rated very poorly in the area of energy. This raises serious doubts as to the approach of these companies to CSR assumptions and may suggest that these companies operate only on the basis of reporting and public relations obligations;

- −

- The energy industry did not stand out among other sectors, because here the highest rated were routines, reporting and implementing environmental management systems. These are elements that are mandatory for companies and they are even forced to report and use these systems;

- −

- The lowest rated factors were those which were the most influential of the energy industry and which should be perfectly implemented for this sector. Factors specific to the energy industry, such as water consumption, whether the company takes responsibility for environmental restoration and whether they supervise the company’s environmental impact, are rated very low.

5. Discussion

- −

- One of the conclusions that arises after the statistical analysis is the fact that companies achieved the highest grades in implementing environmental management systems and reporting environmental data. The same results were found in the analysis by region and sector. It can be concluded that these are activities related to public relations and legal regulations;

- −

- The biggest problems for the companies are ISO 14001/EMAS certification and setting environmental requirements in the supply chain. The results of the research show that companies pursue a policy of corporate social responsibility in relation to operating within their organization and social environment. Important from the point of view of effective operation, cooperation within supply chains is at a low level. This proves that cooperation within supply chains is the highest level of advancement of this concept;

- −

- Based on our analysis, 61.53% of assessed entities did not demonstrate any meaningful activities in at least one indicator, and 7.74% were passive in all eight parameters.

- −

- It is impossible to arrange the regions consecutively due to their grades in the environmental aspect of CSR. Obtained values and the analysis of statistical significance of differences showed that they should be divided into two groups of high- and low-scoring of the environmental aspect of CSR. Southern Europe, Japan and Western Europe all belong to the first group, while China, North America and Northern Europe belong to the second one. There is no statistically significant difference between Benelux and Australia, which are statistically linked to the high-scoring and low-scoring groups, respectively;

- −

- In the sector analysis, high- and low-scoring groups also exist, but there are no links between them. Instead, there were sectors which stuck out positively and negatively from others. Sectors with the best environmental practices are utilities, industry, consumer staples and materials as a leader of that group. Materials are significantly better than all other sectors except utilities. Consumer discretionary, telecommunication services, IT, energy, health care and finance sectors create a low-scoring group. The financial sector obtained significantly lower results than consumer discretionary;

- −

- Northern Europe was the most internally diversified region in terms of obtained ratings, and the least was Eastern Europe. For the sectors, these groups were IT and materials, respectively;

- −

- The energy sector shows a low level of application of corporate social responsibility. Unfortunately, the energy industry does not apply a high level of CSR guidelines. The application of the ISO/EMAS and energy consumption standards was rated the lowest here, which is related to the given sector.

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Sokołowska, A. Społeczna Odpowiedzialność Małego Przedsiębiorstwa. Identyfikacja-Ocena-Kierunki Doskonalenia; Wyd. Uniwerystetu Ekonomicznego We Wrocławiu: Wrocław, Poland, 2013; p. 18. [Google Scholar]

- Gableta, M. W kierunku operacjonalizacji pojęcia odpowiedzialności społecznej w obszarze zatrudnienia. In Kierunki i Dylematy Rozwoju Nauki i Praktyki Zarządzania Przedsiębiorstwem; Jagoda, H., Lichtarski, J., Eds.; Wyd. UE We Wrocławiu: Wrocław, Poland, 2010; p. 73. [Google Scholar]

- Newell, A.P. Corporate Social Responsibility: Challenges, Benefits and Impact on Business Performance; Nova Publishers: New York, NY, USA, 2014; p. vii. [Google Scholar]

- Huk, K. Logistyka miejska a społeczna odpowiedzialność biznesu—Wspólne obszary zainteresowania. Stud. Ekon. Zesz. Nauk. Uniw. Ekon. W Katowicach 2015, 249, 155–163. [Google Scholar]

- Huk, K.; Witkowski, K.; Wasilewski, W. Social aspects of urban logistics in the context of CSR. Logist. Transp. 2016, 3, 13–20. [Google Scholar]

- Garriga, E.; Melé, D. Corporate Social Responsibility Theories: Mapping the Territory. J. Bus. Ethics 2004, 53, 51–71. [Google Scholar] [CrossRef]

- Carroll, A.B. A Three-Dimensional Conceptual Model of Corporate Performance. Acad. Manag. Rev. 1979, 4, 497–505. [Google Scholar] [CrossRef] [Green Version]

- Carroll, A.B. Busieness and Society. Ethics and Stakeholder Management; College Division South-Western Publishing Co.: Cincinaati, OH, USA, 1993. [Google Scholar]

- Sokołowska, A. Społeczna odpowiedzialność małego przedsiębiorstwa—Przejawy i dylematy. E Mentor 2009, 5, 31–37. [Google Scholar]

- Stareček, A.; Gyurák Babeľová, Z.; Makyšová, H.; Cagáňová, D. Sustainable Human Resource Management and Generations of Employees in Industrial Enterprises. Acta Logist. 2021, 8, 45–53. [Google Scholar] [CrossRef]

- Adamiak, A.; Nowicki, M. Etyka i społeczna odpowiedzialność biznesu. In Podstawy Zarządzania; Zakrzewska-Bielawska, A., Ed.; Oficyna Wolters Kluwer Business: Warszawa, Poland, 2012; p. 504. [Google Scholar]

- Griffin, R.W. Podstawy Zarządzania Organizacjami; PWE: Warszawa, Poland, 2004. [Google Scholar]

- Young, S. Etyczny Kapitalizm: Jak Na Powrót Połączyć Prywatny Interes z Dobrem Publicznym; Metamorfoza: Wrocław, Poland, 2005. [Google Scholar]

- Ackerman, R.W. How Companies Respond to Social Demands. Harv. Univ. Rev. 1973, 51, 88–98. [Google Scholar]

- Jones, T.M. Corporate Social Responsibility Revisited Redefined. Calif. Manag. Rev. 1980, 5, 59–67. [Google Scholar] [CrossRef]

- Vogel, D. The Study of Social Issues in Management. Crit. Appraisal. Calif. Manag. Rev. 1986, 28, 142–151. [Google Scholar] [CrossRef]

- Wartick, S.; Mahon, S. Towards a Substantive Definition of the Corporate Issue Construct: A Review and Synthesis of Literature. Busieness Soc. 1994, 33, 293–311. [Google Scholar] [CrossRef]

- Weber, J.; Wasielewski, D. Corporate Social Responsibility; IABS: Pittsburgh, PA, USA, 2018; p. 40. [Google Scholar]

- Frederick, W.C. The Growing Concern over Business Responsibility. Calif. Manag. Rev. 1960, 2, 54–61. [Google Scholar] [CrossRef]

- Friedman, M. The Social Responsibility of Business Is to Increase Its Profits. New York Times Magazine, 13 September 1970; 122–126. [Google Scholar]

- Bajdor, P.; Pawełoszek, I.; Fidlerova, H. Analysis and Assessment of Sustainable Entrepreneurship Practices in Polish Small and Medium Enterprises. Sustainability 2021, 13, 3595. [Google Scholar] [CrossRef]

- Adamczyk, J. Obszary i kryteria oceny społecznej odpowiedzialności przedsiębiorstw. Pr. Nauk. Uniw. Ekon. We Wrocławiu 2014, 338, 9–19. [Google Scholar] [CrossRef] [Green Version]

- United Nations. UNGC Our Participants. Available online: https://www.unglobalcompact.org/what-is-gc/participants (accessed on 11 August 2020).

- Gore, A. Earth in the Balance; Chelsea Green: New York, NY, USA, 1992. [Google Scholar]

- Norouzi, N.; Ataei, E. Globalization and sustainable development. Int. J. Innov. Res. Humanit. 2021, 1, 69. [Google Scholar]

- Surówka, M.; Popławski, M.; Fidlerová, H. Technical Infrastructure as an Element of Sustainable Development of Rural Regions in Małopolskie Voivodeship in Poland and Trnava Region in Slovakia. Agriculture 2021, 11, 141. [Google Scholar] [CrossRef]

- Kelimeler, A. Constitution and Sustainable Development. İstanbul Hukuk Mecmuası 2020, 78, 1921–1957. [Google Scholar] [CrossRef]

- World Commission on Environment and Development. Our Common Future; Oxford University Press: Oxford, UK, 1987; Available online: https://sustainabledevelopment.un.org/content/documents/5987our-common-future.pdf (accessed on 15 July 2021).

- Fidlerová, H.; Mĺkva, M. Application of Selected Methods of Industrial Engineering in Enterprises in the Context of Sustainable Production. Qual. Prod. Improv. 2018, 2, 71–91. [Google Scholar] [CrossRef]

- Straka, M.; Rosova, A.; Malindzakova, M.; Khouri, S.; Culkova, K. Evaluating the Waste Incineration Process for Sustainable Development through Modelling, Logistics, and Simulation. Pol. J. Environ. Stud. 2018, 27, 1–10. [Google Scholar] [CrossRef]

- Labib, O.; Manaf, L.; Sharaai, A.H.; Zaid, S.S.M. Moderating Effects on Residents’ Willingness in Waste Sorting to Improve Waste Handling in Dammam City, Saudi Arabia. Recycling 2021, 6, 24. [Google Scholar] [CrossRef]

- Quinn, A.K.; Bruce, N.; Puzzolo, E.; Dickinson, K.; Sturke, R.; Jack, D.W.; Mehta, S.; Shankar, A.; Sherr, K.; Rosenthal, J.P. An analysis of efforts to scale up clean household energy for cooking around the word. Energy Sustain. Dev. 2018, 46, 1–10. [Google Scholar] [CrossRef] [PubMed]

- Olajuyin, E.A.; Areola, R.I. Energy and Sustainable development in developing countries. J. Electr. Electron. Eng. 2019, 1412–1415. [Google Scholar]

- Japee, G.P.; Oza, P. Redefining Sustainable Development. Psychol. Educ. 2021, 58, 5610–5619. [Google Scholar]

- Brent, A.C. Renewable Energy for Sustainable Development. Sustainability 2021, 13, 1989. [Google Scholar] [CrossRef]

- Saraswat, S.K.; Digalwar, A.K. Evaluation of energy alternatives for sustainable development of energy sector in India: An integrated Shannon’s entropy fuzzy multi-criteria decision approach. Renew. Energy 2021, 171, 58–74. [Google Scholar] [CrossRef]

- Schlör, H.; Fisher, W.; Hake, F. Methods of measuring sustainable development of the German energy sector. Appl. Energy 2013, 101, 172–181. [Google Scholar] [CrossRef]

- Zha, J.; Tan, T.; Ma, S. How to reduce energy intensity to achieve sustainable development of China’s transport sector? A cross-regional comparison analysis. Socio Econ. Plan. Sci. 2020, 71, 2662. [Google Scholar]

- Abdallah, K.B.; Belloumi, M.; Wolf, D. Indicators for sustainable energy development: A multivariate cointegration and causality analysis from Tunisian road transport sector. Renew. Sustain. Energy Rev. 2013, 25, 34–43. [Google Scholar] [CrossRef]

- Islam, S.M.N. Sustainable economic developments in the australian energy sector: Findings of the australian energy planning system optimization model (AEPSOM). Renew. Sustain. Energy Rev. 1997, 1, 229–238. [Google Scholar] [CrossRef]

- Karaman, A.S.; Orazalin, N.; Uyar, A.; Shahbaz, M. CSR achievement, reporting, and assurance in the energy sector: Does economic development matter? Energy Policy 2021, 149, 1–15. [Google Scholar] [CrossRef]

- Shahbaz, M.; Karaman, A.; Kilic, M.; Uyar, A. Board attributes, CSR engagement, and corporate performance: What is the nexus in the energy sector? Energy Policy 2020, 143, 1–14. [Google Scholar] [CrossRef]

- Stjepcevic, J.; Siksnelyte, I. Corporate Social Responsibility in Energy Sector. Transform. Bus. Econ. 2017, 16, 21–33. [Google Scholar]

- ECOTEC. The Impact on Employment in EU-25 of the Opening of Electricity and Gas Markets, and of Key EU Directives in the Field of Energy. Case Study Country Chapter—SWEDEN and Vattenfall; ECOTEC Research & Consulting: Birmingham UK, 2007. [Google Scholar]

- Latin American Energy Organization (OLADE). Methodology for the Implementation of CSR Actions in Energy Companies with Gender Equality; Latin American Energy Organization (OLADE): Quito, Ecuador, 2014. [Google Scholar]

- Wilde-Ramsing, J. Quality Kilowatts: A Normative-Empirical Approach to the Challenge of Defining and Providing Sustainable Electricity in Developing Countries. 2009. Available online: https://www.somo.nl/wp-content/uploads/2009/06/Quality-Kilowatts.pdf (accessed on 9 September 2021).

- Uusimaa Regional Council; in Cooperation Green Net Finland; District Heating Association of Latvia; Max Planck Institute for Plasmahysics; House of Europe; Energie Plus; Association of Municipalities of Estonia as well as municipalities of Sollefteå, Rehna, Grevesmühlen, Kaunas and Vantaa. Energy. Future. Responsibility. Promoting Energy Saving and Corporate Social Responsibility in the Baltic Sea Region; Uusimaa Regional Council: Helsinki, Finland, 2007. [Google Scholar]

- Razali, N.M.; Yap, B.W. Power Comparisons of Shapiro-Wilk, Kolmogorov-Smirnov, Lilliefors and Anderson-Darling Tests. J. Stat. Model. Anal. 2011, 2, 21–33. [Google Scholar]

- Guo, S.; Zhong, S.; Zhang, A. Privacy-preserving Kruskal–Wallis test. Comput. Methods Programs Biomed. 2013, 112, 135–145. [Google Scholar] [CrossRef]

- Ostertagová, E.; Ostertag, O.; Kováč, J. Methodology and Application of the Kruskal-Wallis Test. Appl. Mech. Mater. 2014, 611, 115–120. [Google Scholar] [CrossRef]

- Zar, J.H. Biostatistical Analysis; Prentice Hall: Hoboken, NJ, USA, 1998. [Google Scholar]

- Warner, R.M. Applied Statistics; SAGE Publications: Thousand Oaks, CA, USA, 2008. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Indicators of Corporate Social Responsibility (CSR) |

|---|

| Environmental Routines—Routines Environmental Policies and Targets—Policies |

| Implementation of Environmental Management System—EMS |

| ISO 14001/EMAS Certification—ISO/EMAS |

| Environmental Reporting—Reporting |

| Environmental Requirements Inside the Supply Chain—Supply Chain |

| The Trend of GHG Emissions—GHG |

| The Trend of Energy Consumption—Energy Consumption |

| Industry | Number of Companies |

|---|---|

| Telecommunication Services (TS) | 102 |

| Health Care (health) | 157 |

| Information Technology (IT) | 205 |

| Materials | 161 |

| Industrials (industry) | 231 |

| Consumer Discretionary (CD) | 241 |

| Consumer Staples (CS) | 138 |

| Energy | 123 |

| Utilities | 84 |

| Finance | 276 |

| SUM | 1718 |

| Regions | Countries | Number of Companies |

|---|---|---|

| Western Europe | (Austria, France, Ireland, Germany, Switzerland, United Kingdom) | 254 |

| Southern Europe | (Spain, Portugal, Italy) | 51 |

| Northern Europe | (Denmark, Finland, Norway, Sweden) | 349 |

| Benelux | (Belgium, The Netherlands, Luxembourg) | 42 |

| Australia | (Australia, New Zealand, Papua New Guinea) | 66 |

| North America | (Bermuda, Jamaica, Cayman Islands, Canada, Panama, USA) | 648 |

| Japan | (Japan) | 271 |

| China | (China, Hong Kong, Singapore) | 37 |

| SUM | 1718 |

| Routines | Policies | EMS | ISO/EMAS | Reporting | Supply Chain | GHG | Energy Consump. | |

|---|---|---|---|---|---|---|---|---|

| Minimum | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Maximum | 2.5 | 3 | 3 | 3 | 3 | 3 | 3 | 3 |

| Mean | 1.35 | 1.24 | 1.39 | 0.97 | 1.37 | 0.82 | 1.19 | 0.99 |

| Median | 1.5 | 1.5 | 1.5 | 0 | 1.5 | 1 | 1 | 1 |

| Standard Deviation | 0.73 | 0.72 | 0.98 | 1.14 | 0.68 | 0.72 | 0.98 | 0.77 |

| Coefficient of Variation (%) | 53.75 | 58.04 | 70.52 | 118.27 | 49.87 | 87.65 | 82.68 | 78.22 |

| 0 Grades (n) | 167 | 196 | 351 | 939 | 144 | 533 | 475 | 423 |

| 0 Grades (%) | 9.72 | 11.41 | 20.43 | 54.66 | 8.38 | 31.02 | 27.65 | 24.62 |

| K-W Test: 4,956E−46 | W Europe | S Europe | N Europe | Benelux | Australia | N America | Japan | China |

|---|---|---|---|---|---|---|---|---|

| W Europe | 0.6678 | 6.22 × 10−23 ** | 0.07149 | 2.96 × 10−8 ** | 1.78 × 10−34 ** | 0.2885 | 1.79 × 10−9 ** | |

| S Europe | 1 | 4.42 × 10−8 ** | 0.08399 | 7.14 × 10−6 ** | 8.75 × 10−11 ** | 0.4928 | 3.28 × 10−7 ** | |

| N Europe | 1.74 × 10−21 ** | 1.24 × 10−6 ** | 0.001135 ** | 0.06559 | 0.9683 | 1.60 × 10−12 ** | 0.9184 | |

| Benelux | 1 | 1 | 0.03177 * | 0.03518 * | 0.000181 ** | 0.319 | 0.001516 ** | |

| Australia | 8.30 × 10−7 ** | 0.0002 ** | 1 | 0.9851 | 0.03616 * | 0.000114 ** | 0.1052 | |

| N America | 4.97 × 10−33 ** | 2.45 × 10−9 ** | 1 | 0.005062 ** | 1 | 2.50 × 10−19 ** | 0.9843 | |

| Japan | 1 | 1 | 4.47 × 10−11 ** | 1 | 0.003204 ** | 6.99 × 10−18 ** | 3.58 × 10−5 ** | |

| China | 5.01 × 10−8 ** | 9.18 × 10−6 ** | 1 | 0.04244 * | 1 | 1 | 0.001001 ** |

| Routine | Policy | EMS | ISO/EMAS | Reporting | Supply Chain | GHG | Energy | |

|---|---|---|---|---|---|---|---|---|

| W Europe | 2 | 1.5 | 2 | 2 | 2 | 1 | 2 | 1 |

| S Europe | 2 | 1.5 | 2 | 2 | 2 | 1 | 1.5 | 1 |

| N Europe | 1 | 1 | 1.5 | 0 | 1 | 0.5 | 0.5 | 0.5 |

| Benelux | 1.5 | 1.5 | 1.5 | 1 | 2 | 1 | 2 | 2 |

| Australia | 1.5 | 1 | 1.5 | 0 | 1.5 | 0.5 | 2 | 1 |

| N America | 1 | 1 | 1 | 0 | 1.5 | 0.5 | 1 | 1 |

| Japan | 2 | 1.5 | 2 | 2 | 1.5 | 1 | 2 | 1 |

| China | 1 | 1 | 1.5 | 0 | 1 | 0.5 | 0.5 | 1 |

| K-W Test: 2.107E−40 | Energy | Materials | Health | CS | Industry | IT | TS | Utilities | CD | Finance |

|---|---|---|---|---|---|---|---|---|---|---|

| Energy | 4.00 × 10−15 ** | 0.1441 | 8.20 × 10−7 ** | 2.94 × 10−7 ** | 0.3567 | 0.8081 | 1.10 × 10−5 ** | 0.4145 | 0.004086 ** | |

| Materials | 1.80 × 10−13 ** | 1.39 × 10−15 ** | 5.11 × 10−5 ** | 0.000373 ** | 1.87 × 10−13 ** | 1.28 × 10−12 ** | 0.001647 ** | 6.63 × 10−13 ** | 3.60 × 10−29 ** | |

| Health | 1 | 6.23 × 10−14 ** | 1.02 × 10−7 ** | 6.11 × 10−9 ** | 0.7625 | 0.5101 | 1.97 × 10−6 ** | 0.02791 * | 0.189 | |

| CS | 3.69 × 10−5 ** | 0.002301 ** | 4.58 × 10−6 ** | 0.5865 | 2.66 × 10−6 ** | 2.27 × 10−5 ** | 0.8758 | 7.92 × 10−5 ** | 6.96 × 10−15 ** | |

| Industry | 1.32 × 10−5 ** | 0.0168 * | 2.75 × 10−7 ** | 1 | 1.38 × 10−7 ** | 2.52 × 10−6 ** | 0.8244 | 8.72 × 10−6 ** | 1.38 × 10−18 ** | |

| IT | 1 | 8.40 × 10−12 ** | 1 | 0.00012 ** | 6.20 × 10−6 ** | 0.7613 | 3.46 × 10−5 ** | 0.08302 | 0.1251 | |

| TS | 1 | 5.76 × 10−11 ** | 1 | 0.00102 ** | 0.000113 ** | 1 | 0.000111 ** | 0.2683 | 0.05337 | |

| Utilities | 0.000493 ** | 0.0741 | 8.86 × 10−5 ** | 1 | 1 | 0.001556 ** | 0.004983 ** | 0.000605 ** | 3.15 × 10−11 ** | |

| CD | 1 | 2.98 × 10−11 ** | 1 | 0.003566 ** | 0.000392 ** | 1 | 1 | 0.02721 * | 7.14 × 10−5 ** | |

| Finance | 0.1839 | 1.62 × 10−27 ** | 1 | 3.13 × 10−13 ** | 6.19 × 10−17 ** | 1 | 1 | 1.42 × 10−9 ** | 0.003212 ** |

| Routine | Policy | EMS | ISO/EMAS | Reporting | Supply Chain | GHG | Energy | |

|---|---|---|---|---|---|---|---|---|

| Energy | 1.5 | 1.5 | 1.5 | 0 | 1 | 0.5 | 1 | 1 |

| Materials | 2 | 2 | 2 | 2 | 2 | 1 | 2 | 2 |

| Health | 1 | 1 | 1 | 0 | 1 | 0.5 | 1 | 1 |

| CS | 1.5 | 1.5 | 1.5 | 1 | 1.5 | 1 | 1.5 | 1 |

| Industry | 1.5 | 1.5 | 2 | 2 | 1.5 | 1 | 1 | 1 |

| IT | 1 | 1 | 1.5 | 0 | 1 | 1 | 0.5 | 0.5 |

| TS | 1 | 1 | 1 | 0 | 1.5 | 1 | 1 | 1 |

| Utilities | 1.5 | 1.5 | 2 | 1 | 1.5 | 1 | 2 | 1 |

| CD | 1 | 1.5 | 1.5 | 0 | 1.5 | 1 | 1 | 1 |

| Finance | 1 | 1 | 1 | 0 | 1 | 0.25 | 1 | 1 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Huk, K.; Kurowski, M. The Environmental Aspect in the Concept of Corporate Social Responsibility in the Energy Industry and Sustainable Development of the Economy. Energies 2021, 14, 5993. https://doi.org/10.3390/en14185993

Huk K, Kurowski M. The Environmental Aspect in the Concept of Corporate Social Responsibility in the Energy Industry and Sustainable Development of the Economy. Energies. 2021; 14(18):5993. https://doi.org/10.3390/en14185993

Chicago/Turabian StyleHuk, Katarzyna, and Mateusz Kurowski. 2021. "The Environmental Aspect in the Concept of Corporate Social Responsibility in the Energy Industry and Sustainable Development of the Economy" Energies 14, no. 18: 5993. https://doi.org/10.3390/en14185993

APA StyleHuk, K., & Kurowski, M. (2021). The Environmental Aspect in the Concept of Corporate Social Responsibility in the Energy Industry and Sustainable Development of the Economy. Energies, 14(18), 5993. https://doi.org/10.3390/en14185993