Nexus between Financial Development, Renewable Energy Consumption, Technological Innovations and CO2 Emissions: The Case of India

,

,  ,

,  , and

, and

Abstract

:1. Introduction

2. Literature Review

3. Econometric Methodology and Data Source

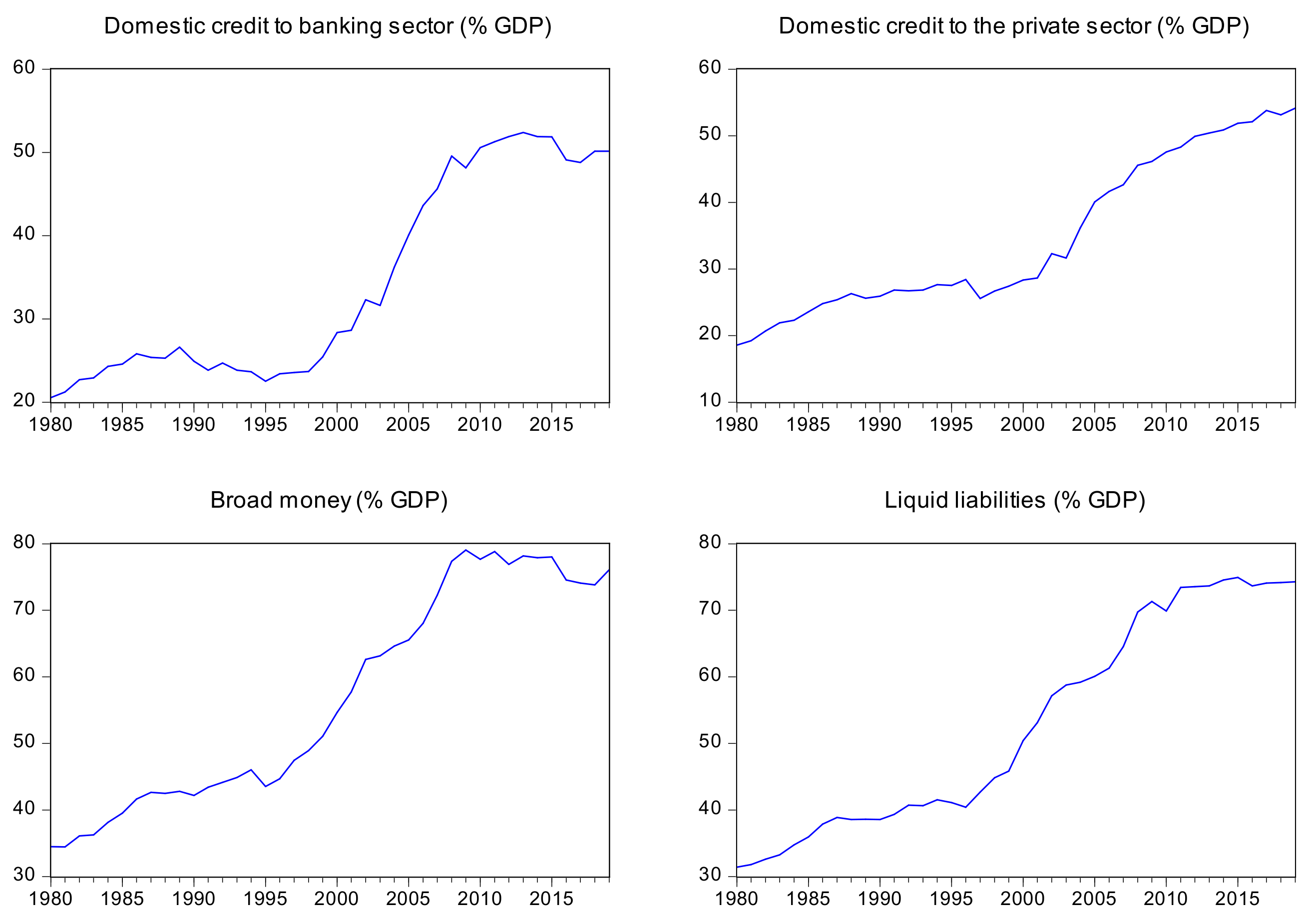

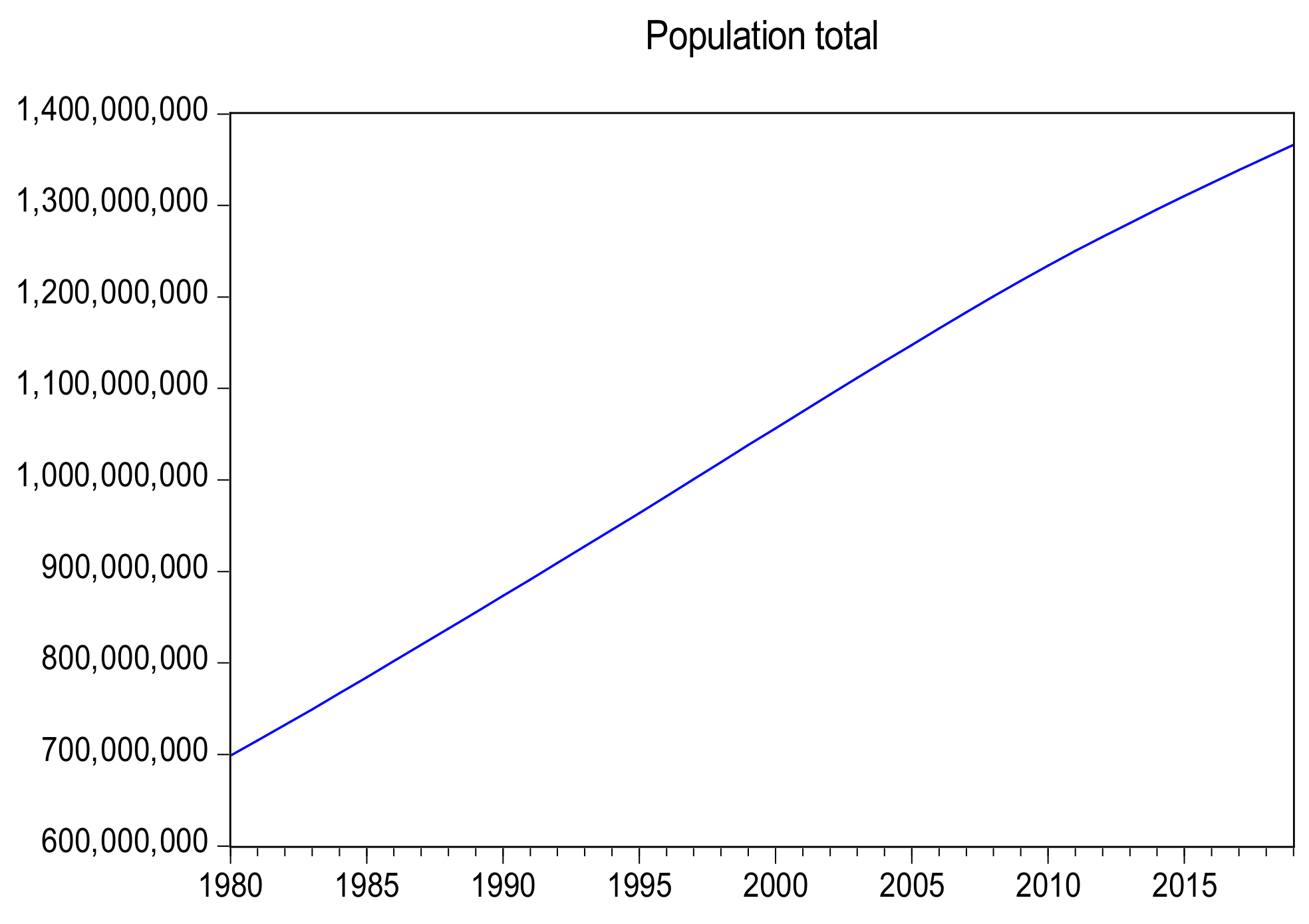

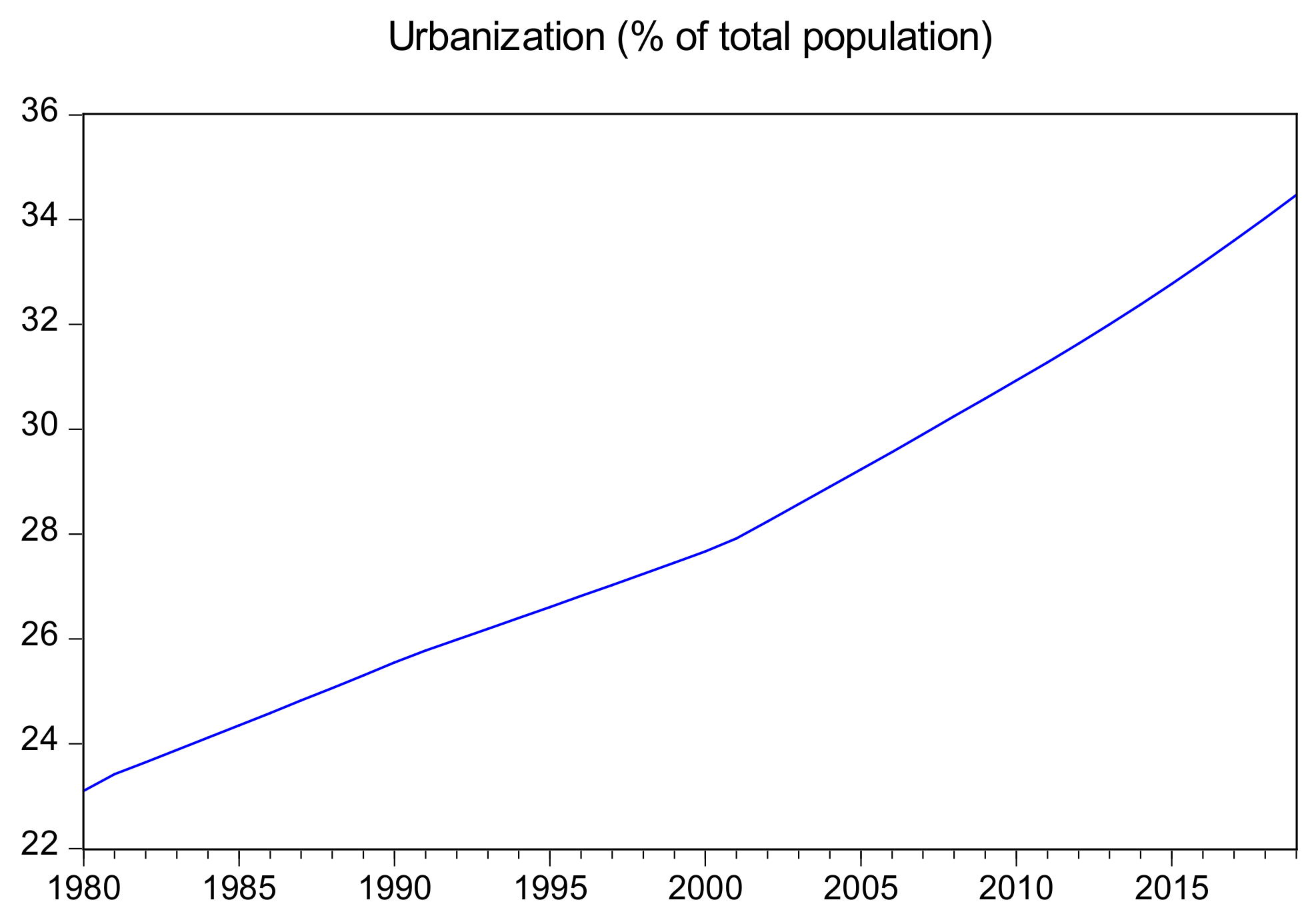

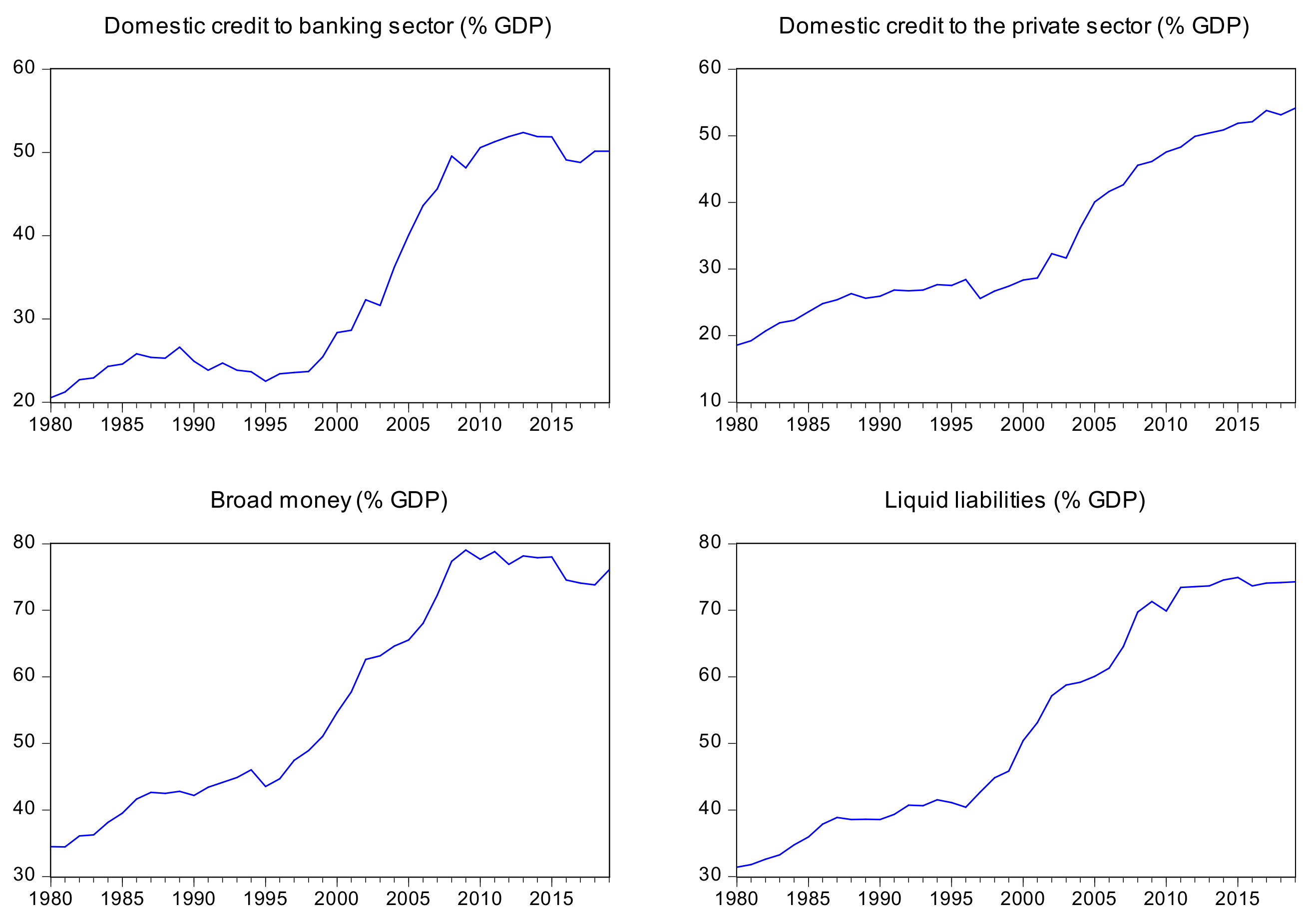

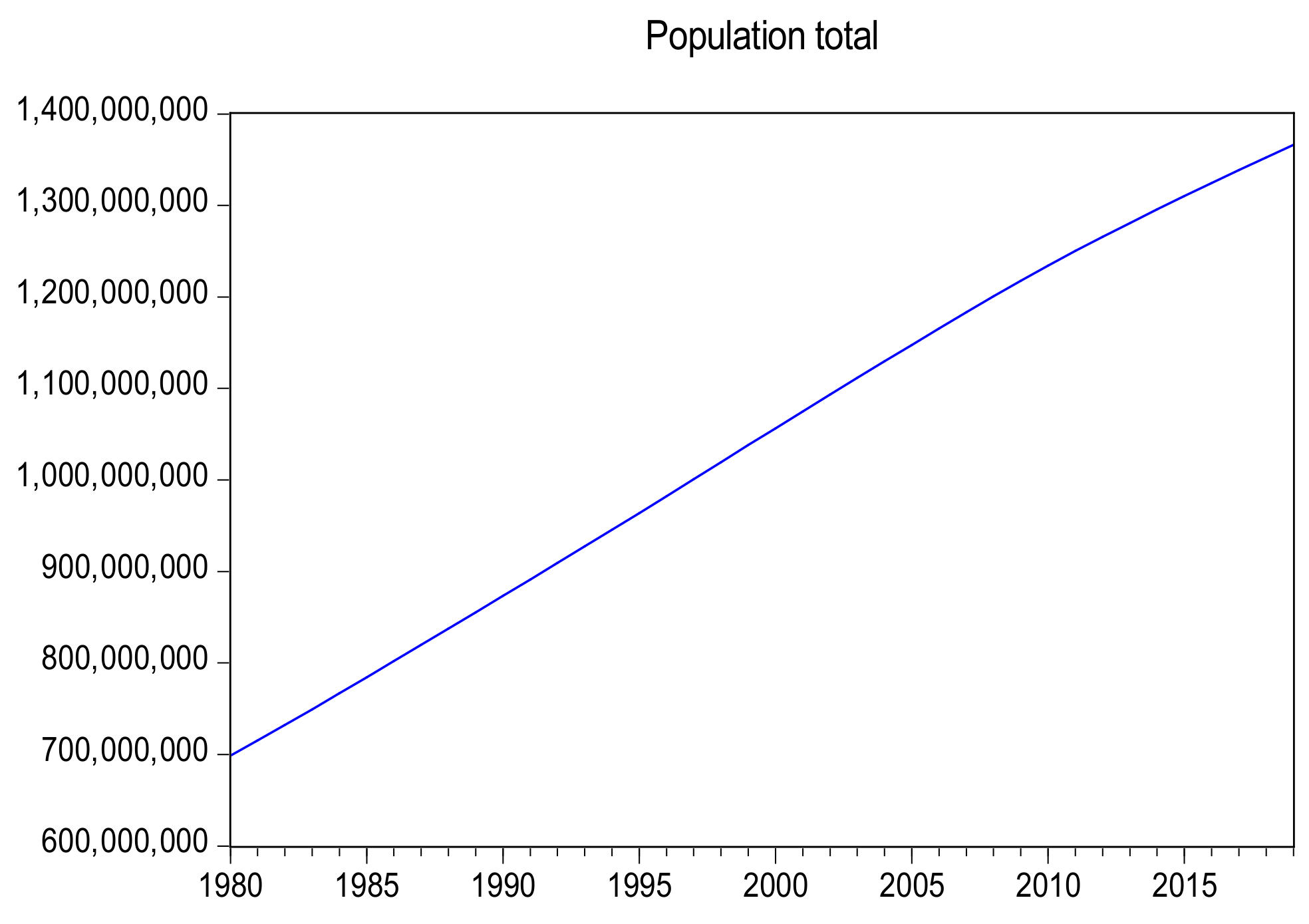

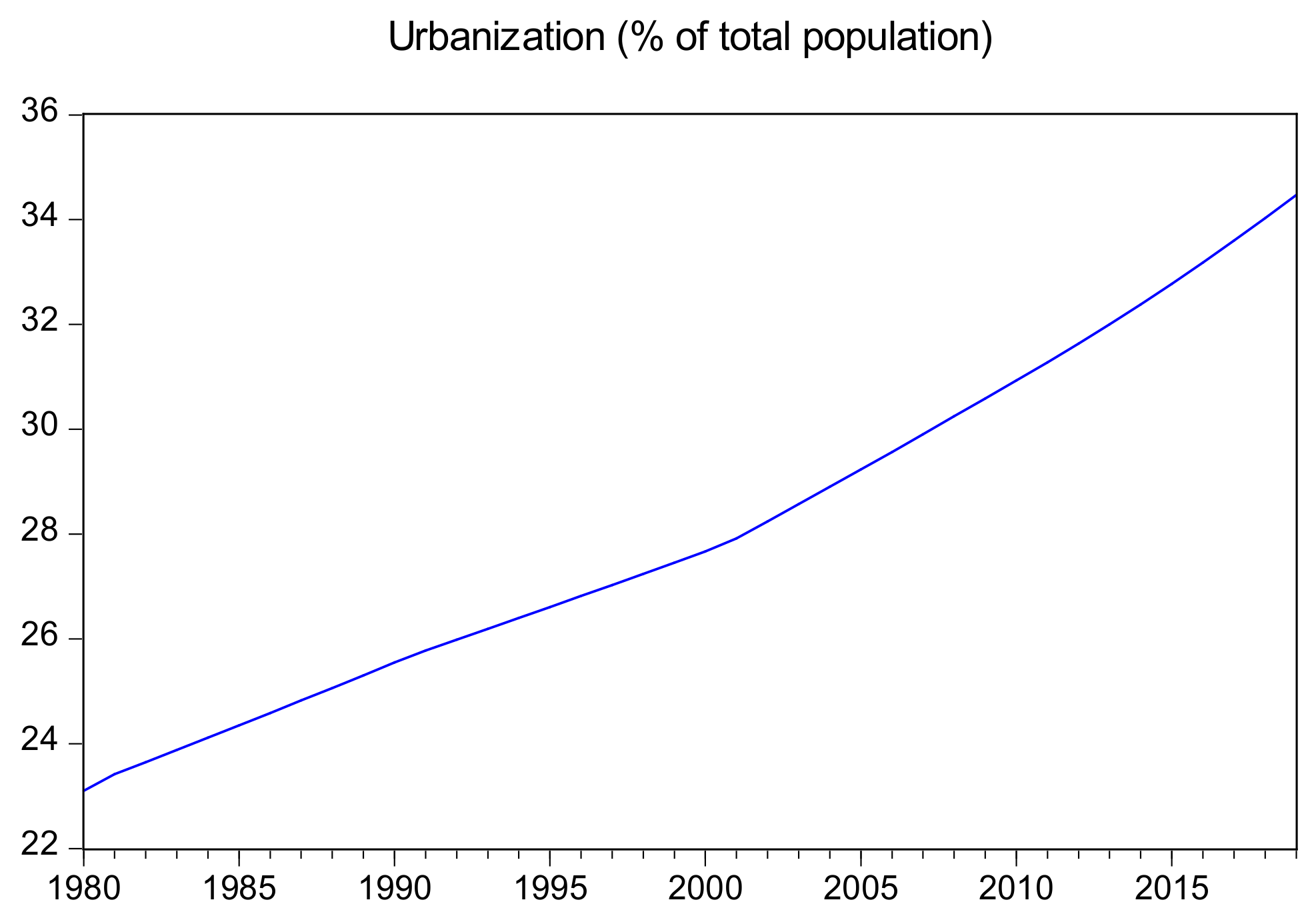

3.1. Data Source

3.2. Composite Financial Development Index

3.3. Theoretical Rationale and Model Specification

3.4. Economic Strategy

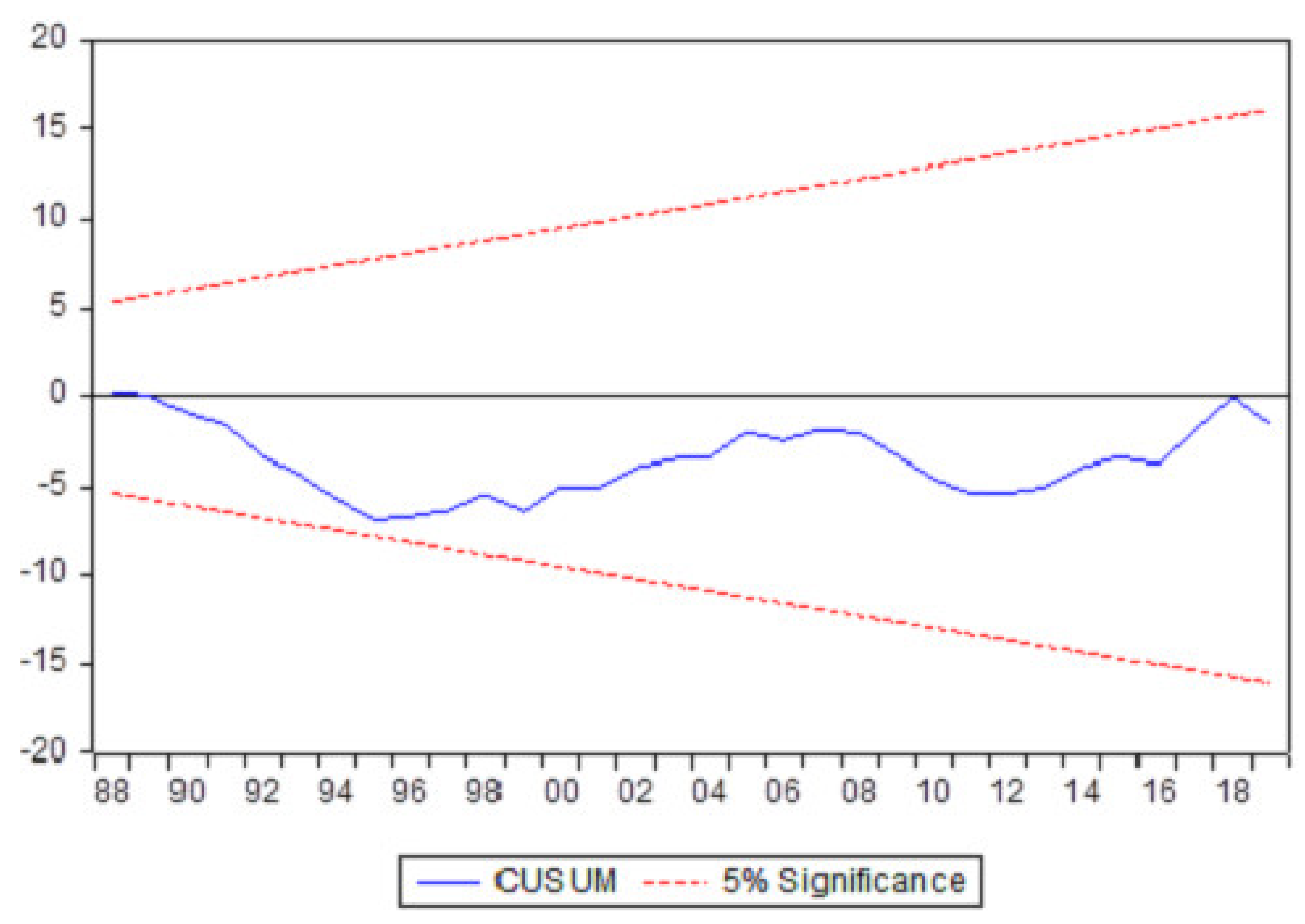

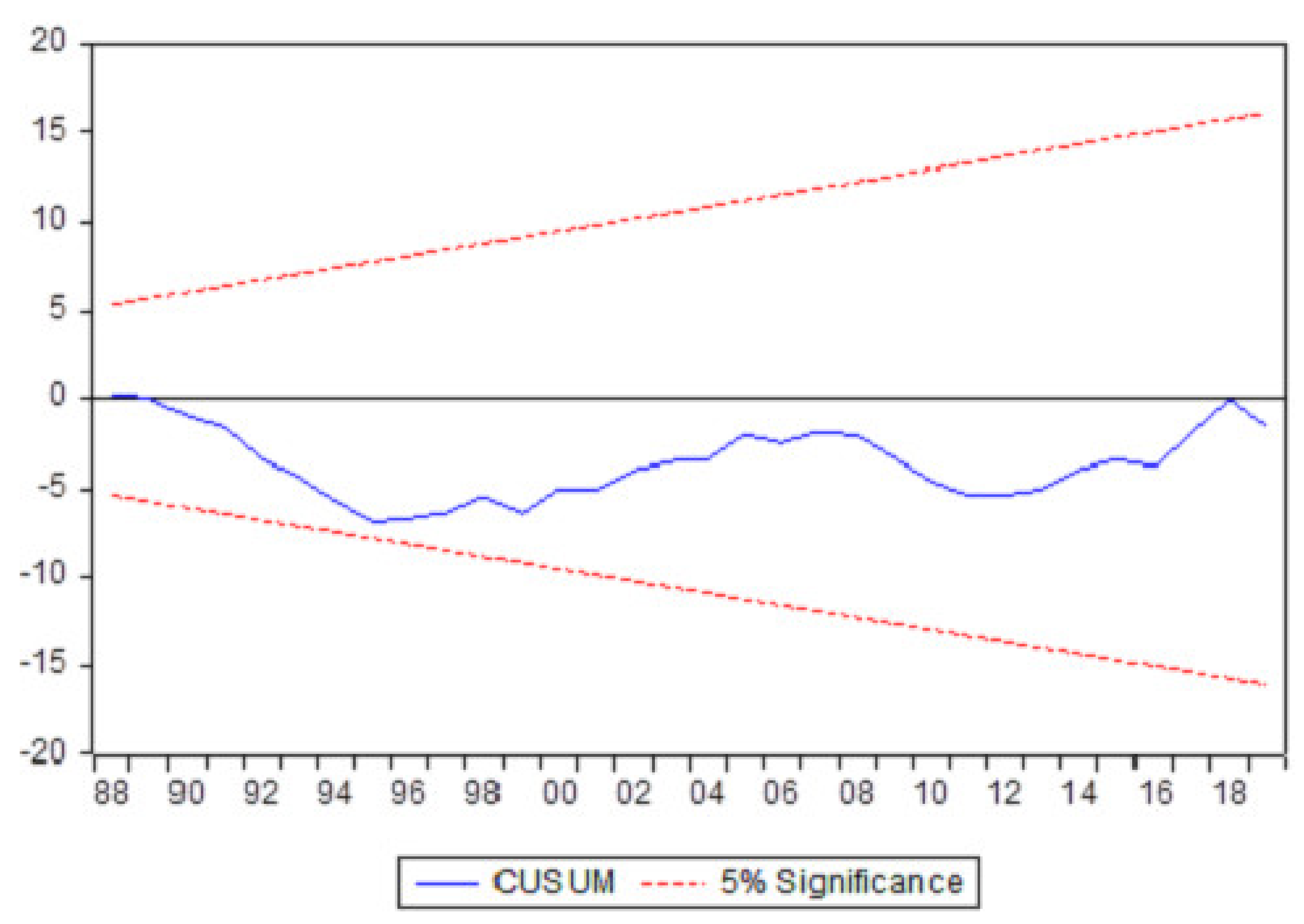

4. Results and Discussion

5. Conclusions and Policy Implications

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- World Bank. World Development Indicators. 2017. Available online: http://databank.worldbank.org (accessed on 3 March 2021).

- Qayyum, M.; Yu, Y.; Li, S. The impact of economic complexity on embodied carbon emission in trade: New empirical evidence from cross-country panel data. Environ. Sci. Pollut. Res. 2021. [Google Scholar] [CrossRef]

- Panwar, N.L.; Kaushik, S.C.; Kothari, S. Role of renewable energy sources in environmental protection: A review. Renew. Sust. Energy Rev. 2011, 15, 1513–1524. [Google Scholar] [CrossRef]

- ECD. European Commission Directorate Annual Activity Report. 2015. Available online: https://ec.europa.eu/info/sites/info/files/activity-report-2015-dg-ener_april2016_en.Pdf (accessed on 30 July 2020).

- BP. Statistical Review of World Energy, London, United Kingdom. 2017. Available online: https://www.bp.com/content/dam/bp/en/corporate/pdf/energy-economics/statistical-review-2017/bp-statistical-review-of-world-energy-2017-full-report.pdf (accessed on 3 August 2020).

- IEA. What Is Energy Security. 2017. Available online: https://www.iea.org/topics/energysecurity/subtopics/whatisenergysecurity (accessed on 3 August 2020).

- Alshehry, A.S.; Belloumi, M. Energy consumption, carbon dioxide emissions and economic growth: The case of Saudi Arabia. Renew. Sustain. Energy Rev. 2015, 41, 237–247. [Google Scholar] [CrossRef]

- Tang, C.F.; Tan, B.W.; Ozturk, I. Energy consumption and economic growth in Vietnam. Renew. Sust. Energy Rev. 2016, 54, 1506–1514. [Google Scholar] [CrossRef]

- Shahbaz, M. Does financial instability increase environmental degradation? Fresh evidence from Pakistan. Econ. Model. 2013, 33, 537–544. [Google Scholar] [CrossRef] [Green Version]

- Ali, M.; Nazir, M.I.; Hashmi, S.H.; Ullah, W. Financial inclusion, institutional quality and financial development: Empirical evidence from OIC countries. Singap. Econ. Rev. 2020. [Google Scholar] [CrossRef]

- Yu, Y.; Qayyum, M. Impacts of Financial Openness on Economic Complexity: Cross‐country Evidence. Int. J. Finance Econ. 2021. [Google Scholar] [CrossRef]

- Sarangi, G.K. Green Energy Finance in India: Challenges and Solutions; ADBI Working Paper; Asian Development Bank Institute: Chiyoda, Tokyo, 2018; (No. 863). [Google Scholar]

- Bhattacharyya, P.; Maheswari, S. Private equity financing for cleantech infrastructure. In India Infrastructure Report; Oxford University Press: New Delhi, India, 2010; pp. 77–86. [Google Scholar]

- Tamazian, A.; Chousa, J.P.; Vadlamannati, K.C. Does Higher economic and financial development lead to environmental degradation: Evidence from BRIC countries. Energy Policy 2009, 37, 246–253. [Google Scholar] [CrossRef]

- Saud, S.; Baloch, M.A.; Lodhi, R.N. The nexus between energy consumption and financial development: Estimating the role of globalization in next-11 countries. Environ. Sci. Pollut. Res. 2018, 25, 18651–18661. [Google Scholar] [CrossRef]

- Adams, S.; Klobodu, E.K.M. Financial development and environmental degradation: Does political regime matter? J. Clean. Prod. 2018, 197, 1472–1479. [Google Scholar] [CrossRef]

- Destek, M.A.; Sarkodie, S.A. Investigation of environmental kuznets curve for ecological footprint: The role of energy and financial development. Sci. Total Environ. 2019, 650, 2483–2489. [Google Scholar] [CrossRef] [PubMed]

- International Monetary Fund, India: Financial System Stability Assessment. 2017. Available online: https://www.imf.org/~/media/Files/Publications/CR/2017/cr17390.ashx (accessed on 20 August 2020).

- Farhani, S.; Ozturk, I. Causal relationship between CO2 emissions, real GDP, energy consumption, financial development, trade openness, and urbanization in Tunisia. Environ. Sci. Pollut. Res. 2015, 22, 15663–15676. [Google Scholar] [CrossRef] [PubMed]

- Dogan, E.; Seker, F. The Influence of real output, renewable and non-renewable energy, trade and financial development on carbon emissions in the top renewable energy countries. Renew. Sustain. Energy Rev. 2016, 60, 1074–1085. [Google Scholar] [CrossRef]

- Frankel, J.A.; Romer, D. Does trade cause growth? Am. Econ. Rev. 1999, 89, 379–399. [Google Scholar] [CrossRef] [Green Version]

- Saud, S.; Chen, S.; Haseeb, A. Impact of financial development and economic growth on environmental quality: An empirical analysis from belt and road initiative (BRI) countries. Environ. Sci. Pollut. Res. 2018, 26, 2253–2269. [Google Scholar] [CrossRef]

- Zafar, M.W.; Saud, S.; Hou, F. The impact of globalization and financial development on environmental quality: Evidence from selected countries in the organization for economic co-operation and development (OECD). Environ. Sci. Pollut. Res. 2019, 26, 13246–13262. [Google Scholar] [CrossRef]

- Kahouli, B. The short and long run causality relationship among economic growth, energy consumption and financial development: Evidence from South Mediterranean countries (SMCs). Energy Econ. 2017, 68, 19–30. [Google Scholar] [CrossRef]

- Guo, M.; Hu, Y.; Yu, J. The role of financial development in the process of climate change: Evidence from different panel models in China. Atmos. Pollut. Res. 2019, 10, 1375–1382. [Google Scholar] [CrossRef]

- Moghadam, H.E.; Dehbashi, V. The impact of financial development and trade on environmental quality in Iran. Empir. Econ. 2017, 54, 1777–1799. [Google Scholar] [CrossRef]

- Zoundi, Z. CO2 emissions, renewable energy and the environmental kuznets curve, a panel cointegration approach. Renew. Sustain. Energy Rev. 2017, 72, 1067–1075. [Google Scholar] [CrossRef]

- Cherni, A.; Jouini, S.E. An ARDL approach to the CO2 emissions, renewable energy and economic growth nexus: Tunisian evidence. Int. J. Hydrog. Energy 2017, 42, 29056–29066. [Google Scholar] [CrossRef]

- Waheed, R.; Chang, D.; Sarwar, S.; Chen, W. Forest, agriculture, renewable energy, and CO2 emission. J. Clean. Prod. 2018, 172, 4231–4238. [Google Scholar] [CrossRef]

- Chen, Y.; Zhao, J.; Lai, Z.; Wang, Z.; Xia, H. Exploring the effects of economic growth, and renewable and non-renewable energy consumption on China’s CO2 emissions: Evidence from a regional panel analysis. Renew. Energy 2019, 140, 341–353. [Google Scholar] [CrossRef]

- Chen, Y.; Wang, Z.; Zhong, Z. CO2 Emissions, economic growth, renewable and non-renewable energy production and foreign trade in China. Renew. Energy 2019, 131, 208–216. [Google Scholar] [CrossRef]

- Charfeddine, L.; Kahia, M. Impact of renewable energy consumption and financial development on CO2 emissions and economic growth in the MENA region: A panel vector autoregressive (PVAR) analysis. Renew. Energy 2019, 139, 198–213. [Google Scholar] [CrossRef]

- Albino, V.; Ardito, L.; Dangelico, R.M.; Petruzzelli, A.M. Understanding the development trends of low-carbon energy technologies: A patent analysis. Appl. Energy 2014, 135, 836–854. [Google Scholar] [CrossRef]

- Raiser, K.; Naims, H.; Bruhn, T. Corporatization of the climate? Innovation, intellectual property rights, and patents for climate change mitigation. Energy Res. Soc. Sci. 2017, 27, 1–8. [Google Scholar] [CrossRef]

- Zhang, Y.-J.; Peng, Y.-L.; Ma, C.-Q.; Shen, B. Can environmental innovation facilitate carbon emissions reduction? Evidence from China. Energy Policy 2017, 100, 18–28. [Google Scholar] [CrossRef]

- Yu, Y.; Du, Y. Impact of technological innovation on CO2 Emissions and emissions trend prediction on ‘new normal’ economy in China. Atmos. Pollut. Res. 2019, 10, 152–161. [Google Scholar] [CrossRef]

- Brandão Santana, N.; Rebelatto, D.A.D.N.; Périco, A.E.; Moralles, H.F.; Leal Filho, W. Technological innovation for sustainable development: An analysis of different types of impacts for countries in the BRICS and G7 groups. Int. J. Sust. Dev. World 2015, 1–12. [Google Scholar] [CrossRef]

- Yii, K.-J.; Geetha, C. The nexus between technology innovation and CO2 emissions in Malaysia: Evidence from granger causality test. Energy Procedia 2017, 105, 3118–3124. [Google Scholar] [CrossRef]

- Jin, L.; Duan, K.; Shi, C.; Ju, X. The impact of technological progress in the energy sector on carbon emissions: An empirical analysis from China. Int. J. Environ. Res. Pub. Health 2017, 14, 1505. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Aldieri, L.; Bruno, B.; Vinci, C.P. Does environmental innovation make us happy? An empirical investigation. Socio Econ. Plan. Sci. 2019, 67, 166–172. [Google Scholar] [CrossRef]

- Su, H.-N.; Moaniba, I.M. Does innovation respond to climate change? Empirical evidence from patents and greenhouse gas emissions. TFSCB 2017, 122, 49–62. [Google Scholar] [CrossRef]

- Jalil, A.; Feridun, M. The impact of growth, energy and financial development on the environment in China: A cointegration analysis. Energy Econ. 2011, 33, 284–291. [Google Scholar] [CrossRef]

- Creane, S.; Goyal, R.; Mobarak, A.; Sab, R. Measuring financial development in the Middle East and North Africa: A new database. IMF Staff Papers 2006, 53, 479–511. Available online: http://www.jstor.org/stable/30035923 (accessed on 5 July 2021).

- Boutabba, M.A. The impact of financial development, income, energy and trade on carbon emissions: Evidence from the Indian Economy. Econ. Model. 2014, 40, 33–41. [Google Scholar] [CrossRef] [Green Version]

- Shahbaz, M.; Hoang, T.H.V.; Mahalik, M.K.; Roubaud, D. Energy consumption, financial development and economic growth in India: New evidence from a nonlinear and asymmetric analysis. Energy Econ. 2017, 63, 199–212. [Google Scholar] [CrossRef] [Green Version]

- Ang, J.B. CO2 emissions, research and technology transfer in China. Ecol. Econ. 2009, 68, 2658–2665. [Google Scholar] [CrossRef] [Green Version]

- Levine, R.; Loayza, N.; Beck, T. Financial intermediation and growth: Causality and causes. J. Monet. Econ. 2000, 46, 31–77. [Google Scholar] [CrossRef] [Green Version]

- Shahbaz, M.; Shahzad, S.J.H.; Ahmad, N.; Alam, S. Financial development and environmental quality: The way forward. Energy Policy 2016, 98, 353–364. [Google Scholar] [CrossRef] [Green Version]

- Katircioğlu, S.T.; Taşpinar, N. Testing the moderating role of financial development in an environmental Kuznets curve: Empirical evidence from Turkey. Renew. Sustain. Energy Rev. 2017, 68, 572–586. [Google Scholar] [CrossRef]

- Yang, B.; Ali, M.; Nazir, M.R.; Ullah, W.; Qayyum, M. Financial instability and CO2 emissions: Cross-country evidence. Air Qual. Atmos. Health 2020, 13, 459–468. [Google Scholar] [CrossRef]

- Yang, B.; Ali, M.; Hashmi, S.H.; Shabir, M. Income inequality and CO2 emissions in developing countries: The moderating role of financial instability. Sustainability 2020, 12, 6810. [Google Scholar] [CrossRef]

- Chen, M.-H. The economy, tourism growth and corporate performance in the Taiwanese hotel industry. Tour. Manag. 2010, 31, 665–675. [Google Scholar] [CrossRef] [PubMed]

- Zakaria, M.; Bibi, S. Financial development and environment in South Asia: The role of institutional quality. Environ. Sci. Pollut. Res. 2019, 26, 7926–7937. [Google Scholar] [CrossRef] [PubMed]

- Bhattacharya, M.; Churchill, S.A.; Paramati, S.R. The dynamic impact of renewable energy and institutions on economic output and CO2 emissions across regions. Renew. Energy 2017, 111, 157–167. [Google Scholar] [CrossRef]

- Saidi, K.; Omri, A. The Impact of renewable energy on carbon emissions and economic growth in 15 major renewable energy-consuming countries. Environ. Res. 2020, 186, 109567. [Google Scholar] [CrossRef]

- Tang, C.F.; Tan, E.C. Exploring the nexus of electricity consumption, economic growth, energy prices and technology innovation in Malaysia. Appl. Energy 2013, 104, 297–305. [Google Scholar] [CrossRef]

- Shahbaz, M.; Nasir, M.A.; Roubaud, D. Environmental degradation in France: The effects of FDI, financial development, and energy innovations. Energy Econ. 2018, 74, 843–857. [Google Scholar] [CrossRef] [Green Version]

- Fan, H.; Hashmi, S.H.; Habib, Y.; Ali, M. How do urbanization and urban agglomeration affect CO2 emissions in South Asia? Testing non-linearity puzzle with dynamic STIRPAT model. Chin. J. Urban Environ. Stud. 2020, 8, 2050003. [Google Scholar] [CrossRef]

- Shahbaz, M.; Lean, H.H.; Shabbir, M.S. Environmental Kuznets curve hypothesis in Pakistan: Cointegration and granger causality. Renew. Sustain. Energy Rev. 2012, 16, 2947–2953. [Google Scholar] [CrossRef] [Green Version]

- Pesaran, M.H.; Shin, Y.; Smith, R.J. Bounds testing approaches to the analysis of level relationships. J. Appl. Econ. 2001, 16, 289–326. [Google Scholar] [CrossRef]

- Engle, R.F.; Granger, C.W.J. Co-Integration and error correction: Representation, estimation, and testing. Econometrica 1987, 55, 251. [Google Scholar] [CrossRef]

- Johansen, S. Statistical analysis of cointegration vectors. J. Econ. Dyn. Control 1988, 12, 231–254. [Google Scholar] [CrossRef]

- Zhang, B.; Wang, B.; Wang, Z. Role of renewable energy and non-renewable energy consumption on EKC: Evidence from Pakistan. J. Clean. Prod. 2017, 156, 855–864. [Google Scholar] [CrossRef]

- Banerjee, A.; Dolado, J.; Mestre, R. Error-correction mechanism tests for cointegration in a single-equation framework. J. Time Ser. Anal. 1998, 19, 267–283. [Google Scholar] [CrossRef] [Green Version]

- Romilly, P.; Song, H.; Liu, X. Car ownership and use in Britain: A Comparison of the empirical results of alternative cointegration estimation methods and forecasts. Appl. Econ. 2001, 33, 1803–1818. [Google Scholar] [CrossRef]

- Phillips, P.C.B.; Hansen, B.E. Statistical inference in instrumental variables regression with I (1) processes. Rev. Econ. Stud. 1990, 57, 99. [Google Scholar] [CrossRef]

- Kalmaz, D.B.; Kirikkaleli, D. Modeling CO2 emissions in an emerging market: Empirical finding from ARDL-based bounds and wavelet coherence approaches. Environ. Sci. Pollut. Res. 2019, 26, 5210–5220. [Google Scholar] [CrossRef]

- Park, J.Y. Canonical cointegrating regressions. Econometrica 1992, 60, 119. [Google Scholar] [CrossRef]

- Kirikkaleli, D.; Athari, S.A.; Ertugrul, H.M. The real estate industry in Turkey: A time series analysis. Serv. Ind. J. 2018, 41, 427–439. [Google Scholar] [CrossRef]

- Pedroni, P. Purchasing power parity tests in cointegrated panels. Rev. Econ. Stat. 2001, 83, 727–731. [Google Scholar] [CrossRef] [Green Version]

- Phillips, P.C.B.; Perron, P. Testing for a unit root in time series regression. Biometrika 1988, 75, 335–346. [Google Scholar] [CrossRef]

- Elliott, G.; Rothenberg, T.J.; Stock, J.H. Efficient tests for an autoregressive unit root. Econometrica 1996, 64, 813. [Google Scholar] [CrossRef] [Green Version]

- Perron, P. Further evidence on breaking trend functions in macroeconomic variables. J. Econom. 1997, 80, 355–385. [Google Scholar] [CrossRef] [Green Version]

- Baloch, P.M. Dynamic Linkages between road transport energy consumption, economic growth, and environmental quality: Evidence from Pakistan. Environ. Sci. Pollut. Res. 2017, 25, 7541–7552. [Google Scholar] [CrossRef]

- Lau, L.-S.; Choong, C.-K.; Eng, Y.-K. Investigation of the environmental Kuznets curve for carbon emissions in Malaysia: Do foreign direct investment and trade matter? Energy Policy 2014, 68, 490–497. [Google Scholar] [CrossRef]

- Narayan, P.K. The saving and investment nexus for China: Evidence from cointegration tests. Appl. Econ. 2005, 37, 1979–1990. [Google Scholar] [CrossRef]

- Saud, S.; Chen, S.; Haseeb, A.; Khan, K.; Imran, M. The Nexus between financial development, income level, and environment in central and eastern European Countries: A perspective on belt and road initiative. Environ. Sci. Pollut. Res. 2019, 26, 16053–16075. [Google Scholar] [CrossRef] [PubMed]

- Wolde-Rufael, Y.; Weldemeskel, E.M. Environmental policy stringency, renewable energy consumption and CO2 emissions: Panel cointegration analysis for BRIICTS countries. Int. J. Green Energy 2020, 17, 568–582. [Google Scholar] [CrossRef]

- Khan, Z.; Ali, M.; Kirikkaleli, D.; Wahab, S.; Jiao, Z. The Impact of technological innovation and public‐private partnership investment on sustainable environment in China: Consumption‐based carbon emissions analysis. J. Sustain. Dev. 2020, 28, 1317–1330. [Google Scholar] [CrossRef]

- Yang, B.; Jahanger, A.; Ali, M. Remittance inflows affect the ecological footprint in BICS countries: Do technological innovation and financial development matter? Environ. Sci. Pollut. Res. 2021, 28, 23482–23500. [Google Scholar] [CrossRef]

- Hafeez, M.; Yuan, C.; Shahzad, K.; Aziz, B.; Iqbal, K.; Raza, S. An empirical evaluation of financial development-carbon footprint nexus in one belt and road region. Environ. Sci. Pollut. Res. 2019, 26, 25026–25036. [Google Scholar] [CrossRef] [PubMed]

- Bekhet, H.A.; Othman, N.S. Impact of urbanization growth on Malaysia CO2 emissions: Evidence from the dynamic relationship. J. Clean. Prod. 2017, 154, 374–388. [Google Scholar] [CrossRef] [Green Version]

- Pata, U.K. Renewable energy consumption, urbanization, financial development, income and CO2 emissions in Turkey: Testing EKC hypothesis with structural breaks. J. Clean. Prod. 2018, 187, 770–779. [Google Scholar] [CrossRef]

- Ali, R.; Bakhsh, K.; Yasin, M.A. Impact of urbanization on CO2 emissions in emerging economy: Evidence from Pakistan. Sustain. Cities Soc. 2019, 48, 101553. [Google Scholar] [CrossRef]

- Sharma, S.S. Determinants of carbon dioxide emissions: Empirical evidence from 69 countries. Appl. Energy 2011, 88, 376–382. [Google Scholar] [CrossRef]

- Ali, H.S.; Abdul-Rahim, A.; Ribadu, M.B. Urbanization and carbon dioxide emissions in Singapore: Evidence from the ARDL approach. Environ. Sci. Pollut. Res. 2016, 24, 1967–1974. [Google Scholar] [CrossRef]

- Samargandi, N.; Fidrmuc, J.; Ghosh, S. Is the relationship between financial development and economic growth monotonic? Evidence from a sample of middle-income countries. World Dev. 2015, 68, 66–81. [Google Scholar] [CrossRef] [Green Version]

- Chen, S.; Saud, S.; Saleem, N.; Bari, M.W. Nexus between financial development, energy consumption, income level, and ecological footprint in CEE countries: Do human capital and biocapacity matter? Environ. Sci. Pollut. Res. 2019, 26, 31856–31872. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Number | Eigenvalue | Proportion | Cumulative |

|---|---|---|---|

| 1 | 3.9168 | 0.9792 | 0.9792 |

| 2 | 0.0794 | 0.0170 | 0.9991 |

| 3 | 0.0235 | 0.0038 | 1.0000 |

| 4 | 0 | 0.0000 | 1.0000 |

| Financial Indicators | Factor loadings | Communalities | Factor scores |

| DCP | 0.9924 | 0.9912 | 0.3012 |

| DCB | 0.9951 | 0.9971 | 0.3121 |

| M2 | 0.8701 | 0.8505 | 0.2669 |

| M3 | 0.9412 | 0.9334 | 0.2801 |

| Variables | Phillips-Perron Test | DF-GLS Test | Decisions | ||

|---|---|---|---|---|---|

| Level | First Difference | Level | First Difference | ||

| CO2 | −1.4685 | −6.0168 *** | −0.8744 | −1.7227 *** | I (1) |

| FD | −0.2639 | −5.7527 *** | 1.4531 | −5.6752 *** | I (1) |

| REC | −0.6785 | −5.6493 *** | −0.2413 | −2.5089 ** | I (1) |

| TI | 6.6707 | −5.2437 *** | 0.3723 | −5.2745 *** | I (1) |

| GDP | 5.5374 | −5.5214 *** | 0.3785 | −5.6097 *** | I (1) |

| URP | 2.3382 | −4.0930 ** | 0.7070 | −1.8910 * | I (1) |

| Variables | At Intercept | At Both Intercept and Trend | ||

|---|---|---|---|---|

| Test Statistic | Time Break | Test Statistic | Time Break | |

| Level | ||||

| CO2 | −3.1735 | 1995 | −3.1362 | 1997 |

| FD | −3.9367 | 2008 | −3.6061 | 2008 |

| REC | −4.1942 | 2003 | −3.4425 | 1989 |

| TI | −3.3694 | 1990 | −4.0176 | 1999 |

| GDP | −3.7003 | 1990 | −4.1231 | 1990 |

| URP | −2.5504 | 1991 | −2.9394 | 1995 |

| First Difference | ||||

| CO2 | −6.8804 *** | 2004 | −7.3099 *** | 1990 |

| FD | −6.2137 *** | 2009 | −6.4915 *** | 2008 |

| REC | −8.2887 *** | 1998 | −8.5296 *** | 1998 |

| TI | −6.2586 *** | 1991 | −6.5319 *** | 1991 |

| GDP | −6.3399 *** | 1991 | −6.6887 *** | 1991 |

| URP | −6.6606 *** | 2001 | −7.0239 *** | 2001 |

| Estimated Model | Lag Selection | F-Value | Remarks |

|---|---|---|---|

| CO2 = f(FD, REC, TI, GDP, URP) | 1,0,0,0,0,0 | 4.3561 ** | Conclusive |

| Critical Value Bounds | |||

| Significance | I0 Bound | I1 Bound | |

| 10% | 2.26 | 3.35 | |

| 5% | 2.62 | 3.79 | |

| 2.5% | 2.96 | 4.18 | |

| 1% | 3.41 | 4.68 |

| Hypothesized No. of CE(s) | Trace Statistic | Prob. ** | Max-Eigen Statistic | Prob. ** |

|---|---|---|---|---|

| None ** | 175.6449 | 0.0000 | 70.10710 | 0.0000 |

| At most 1 ** | 105.5378 | 0.0000 | 36.4119 | 0.0244 |

| At most 2 ** | 69.1259 | 0.0002 | 30.5817 | 0.0200 |

| At most 3 ** | 38.5442 | 0.0038 | 27.1272 | 0.0063 |

| At most 4 | 11.4169 | 0.1871 | 10.6215 | 0.1742 |

| At most 5 | 0.7954 | 0.3725 | 0.7954 | 0.3725 |

| Regressor | Coefficient | Standard Error | p Value |

|---|---|---|---|

| Long run estimate | |||

| FD | 0.6025 *** | 0.1616 | 0.0007 |

| REC | −0.4116 ** | 0.1164 | 0.0283 |

| TI | −0.7759 *** | 0.0928 | 0.0000 |

| GDP | 17.9152 *** | 2.0036 | 0.0000 |

| URP | 5.8529 *** | 1.3333 | 0.0001 |

| C | −119.4584 *** | 12.211 | 0.0000 |

| Short run estimate | |||

| FD | 0.3029 ** | 0.1199 | 0.0167 |

| REC | −0.2126 * | 0.1009 | 0.0644 |

| TI | −0.3902 *** | 0.1142 | 0.0017 |

| GDP | 9.0090 *** | 2.6717 | 0.0020 |

| URP | 2.9433 *** | 1.0593 | 0.0091 |

| CointEq (−1) | −0.5029 *** | 0.1579 | 0.0032 |

| R2 | 0.9993 | ||

| F-Statistics | 7477.628 | 0.0000 | |

| DW Stat | 2.1427 | ||

| Breusch–Godfrey Serial Correlation LM Test | 1.6251 | 0.2178 | |

| ARCH Test | 1.8869 | 0.1785 | |

| Ramsey RESET Test | 2.1352 | 0.1385 |

| FMOLS | DOLS | CCR | |

|---|---|---|---|

| FD | 0.62341 *** | 0.6992 *** | 0.6320 *** |

| −5.4257 | −5.8746 | −5.0375 | |

| [0.0000] | [0.0000] | [0.0000] | |

| REC | −0.6151 *** | −0.5465 *** | −0.6272 *** |

| (−9.6408) | (−3.5243) | (−9.7146) | |

| [0.0041] | [0.0000] | [0.0003] | |

| TI | −0.6895 *** | −0.5751 *** | −0.6765 *** |

| (−11.2415) | (−3.8189) | (−10.9081) | |

| [0.0000] | [0.0015] | [0.0000] | |

| GDP | 16.1220 *** | 13.8123 *** | 15.8307 *** |

| −11.9904 | −3.5595 | −10.8143 | |

| [0.0000] | [0.0026] | [0.0000] | |

| URP | 5.3363 *** | 5.9358 *** | 5.2774 *** |

| −5.8702 | −4.3335 | −6.1136 | |

| [0.0000] | [0.0005] | [0.0000] | |

| Constant | −108.8502 *** | −96.2309 *** | −107.0698 *** |

| (−13.2229) | (−4.5364) | (−12.5334) | |

| [0.0000] | [0.0003] | [0.0000] |

| Wald χ2 Statistics | Long-Term t-Statistics | ||||||

|---|---|---|---|---|---|---|---|

| Variables | CO2 | FD | REC | TI | GDP | URP | ECM(−1) |

| CO2 | 0.0477 (0.721) | −0.03899 * (0.0641) | −1.3499 *** (0.0000) | 31.8866 *** (0.0000) | −2.6691 (0.299) | −0.3638 *** (0.0000) | |

| FD | 0.2354 (0.322) | 0.0123 (0.673) | −0.6208 (0.210) | 14.4350 (0.221) | −2.5304 (0.459) | −0.2258 * (0.0801) | |

| REC | −1.3023 (0.458) | −0.0261 (0.985) | −8.2156 ** (0.0252) | 202.8109 ** (0.0201) | −8.3284 (0.751) | −2.1990 ** (0.0211) | |

| TI | −0.5055 (0.787) | 1.533 (0.293) | −0.0283 (0.902) | −89.7578 (0.334) | −5.6792 (0.839) | −0.4656 (0.647) | |

| GDP | −0.0233 (0.768) | 0.0640 (0.297) | −0.0011 (0.908) | 0.1201 (0.464) | −0.2527 (0.830) | −0.0188 (0.659) | |

| URP | −0.0046 (0.331) | −0.0073 ** (0.0451) | −0.0016 *** (0.0051) | −0.0032 (0.743) | 0.0637 (0.784) | −0.0135 *** (0.0000) | |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Qayyum, M.; Ali, M.; Nizamani, M.M.; Li, S.; Yu, Y.; Jahanger, A. Nexus between Financial Development, Renewable Energy Consumption, Technological Innovations and CO2 Emissions: The Case of India. Energies 2021, 14, 4505. https://doi.org/10.3390/en14154505

Qayyum M, Ali M, Nizamani MM, Li S, Yu Y, Jahanger A. Nexus between Financial Development, Renewable Energy Consumption, Technological Innovations and CO2 Emissions: The Case of India. Energies. 2021; 14(15):4505. https://doi.org/10.3390/en14154505

Chicago/Turabian StyleQayyum, Muhammad, Minhaj Ali, Mir Muhammad Nizamani, Shijie Li, Yuyuan Yu, and Atif Jahanger. 2021. "Nexus between Financial Development, Renewable Energy Consumption, Technological Innovations and CO2 Emissions: The Case of India" Energies 14, no. 15: 4505. https://doi.org/10.3390/en14154505

APA StyleQayyum, M., Ali, M., Nizamani, M. M., Li, S., Yu, Y., & Jahanger, A. (2021). Nexus between Financial Development, Renewable Energy Consumption, Technological Innovations and CO2 Emissions: The Case of India. Energies, 14(15), 4505. https://doi.org/10.3390/en14154505