Economic Development, CO2 Emissions and Energy Use Nexus-Evidence from the Danube Region Countries

Abstract

1. Introduction

2. The Literature Background

3. Materials and Methods

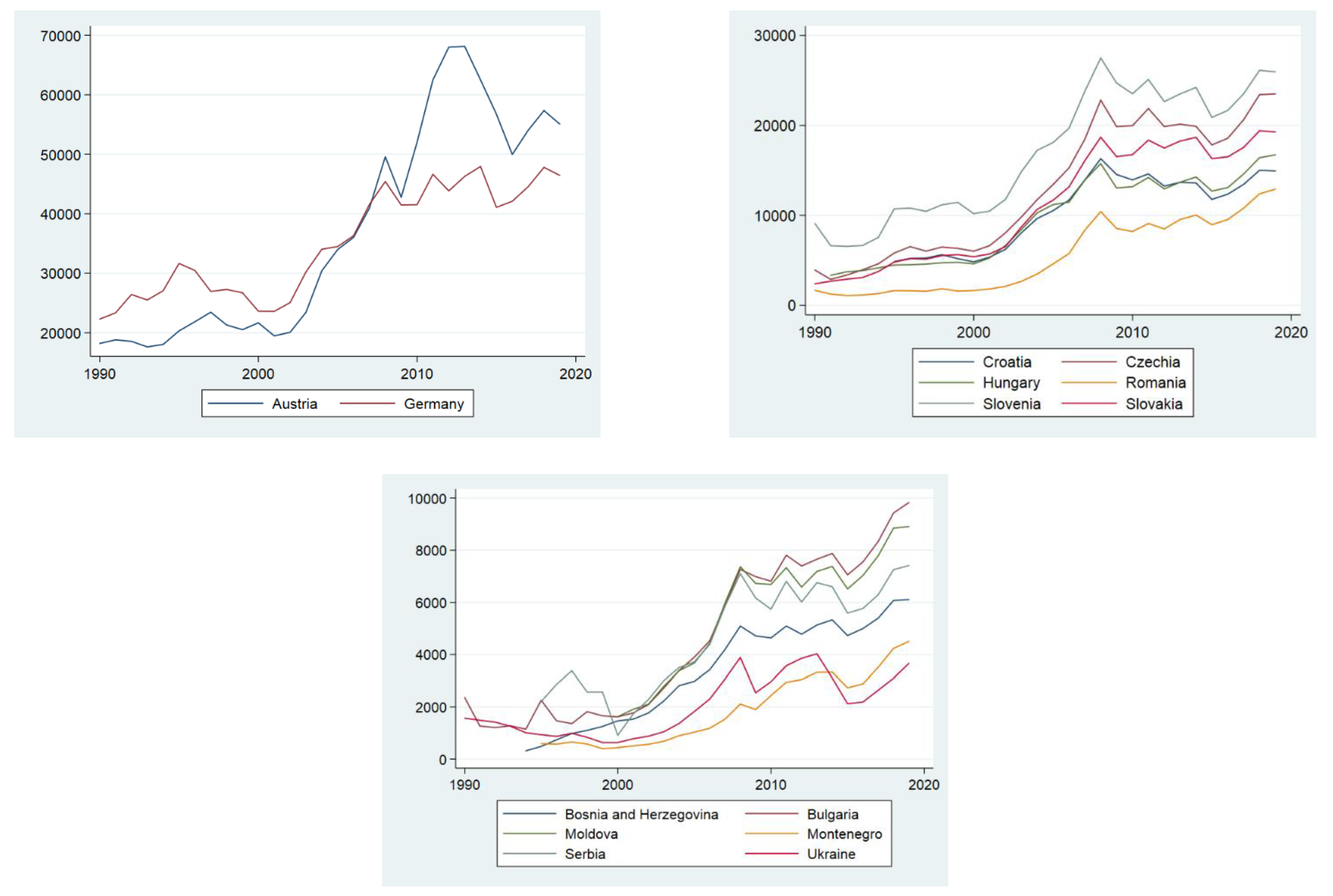

3.1. Data

3.2. Methodology

4. Results and Discussion

4.1. Results for Unit Root Test

4.2. Results for ARDL Bound Testing for Cointegration

4.3. Estimates for Causal Relationship

5. Discussion

6. Conclusions

Supplementary Materials

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

References

- OECD. Economic Policies to Foster Green Growth; OECD: Paris, France, 2014. [Google Scholar]

- UNEP. Green Economy—What Is GEI? UNEP: Nairobi, Kenya, 2014. [Google Scholar]

- United Nations. Transforming Our World: The 2030 Agenda for Sustainable Development; United Nations: New York, NY, USA, 2015.

- European Commission. The European Green Deal. European Commission; European Commission: Brussels, Belgium, 2019. [Google Scholar] [CrossRef]

- European Commission. Powering a Climate-Neutral Economy: An EU Strategy for Energy System Integration. Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions. Available online: https://ec.europa.eu/energy/sites/ener/files/energy_system_integration_strategy_pdf (accessed on 1 March 2021).

- European Commission. A Hydrogen Strategy for a Climate-Neutral Europe. Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions. Available online: https://ec.europa.eu/energy/sites/ener/files/hydrogen_strategy.pdf (accessed on 1 March 2021).

- Hamilton, F.I.; Andrews, K.D.; Pichler-Milanovic, N. Transformation of Cities in Central and Eastern Europe: Towards Globalization; United Nations Publications: New York, NY, USA, 2005. [Google Scholar]

- Giffinger, R.; Suitner, J. Danube region strategy—Arguments for a territorial capital based multilevel approach. Spat. Int. Rev. 2005, 23, 9–16. [Google Scholar] [CrossRef]

- Borowski, P.F. Zonal and Nodal Models of energy market in European Union. Energies 2020, 13, 4182. [Google Scholar] [CrossRef]

- Ferrer, J.N.; Mihnea, C.; Stroia, C.; Bryhn, J. Comparative Study on the Governance Structure and Energy Policies in EU Macro-Regional Strategies. Available online: https://www.ceps.eu/wp-content/uploads/2019/07/RR2019-02_EU-macroregional-strategies.pdf (accessed on 5 March 2021).

- Chalvatzis, K.J.; Ioannidis, A. Energy supply security in the EU: Benchmarking diversity and dependence of primary energy. Appl. Energy 2017, 207, 465–476. [Google Scholar] [CrossRef]

- Hawker, G.; Bell, K.; Gill, S. Electricity security in the European Union—The conflict between national capacity mechanisms and the single market. Energy Res. Soc. Sci. 2017, 24, 51–58. [Google Scholar] [CrossRef]

- Siksnelyte, I.; Zavadskas, E.K.; Bausys, R.; Streimikiene, D. Implementation of EU energy policy priorities in the Baltic Sea Region countries: Sustainability assessment based on neutrosophic MULTIMOORA method. Energy Policy 2019, 125, 90–102. [Google Scholar] [CrossRef]

- De Bruyn, S.M.; Van Den Bergh, J.C.J.M.; Opschoor, J.B. Economic growth and emissions: Reconsidering the empirical basis of environmental Kuznets curves. Ecol. Econ. 1998. [Google Scholar] [CrossRef]

- Heiskanen, E.; Jalas, M. Dematerialization through Services—A Review and Evaluation of the Debate; The Finnish Environment: Helsinki, Finland, 2000. [Google Scholar]

- Vehmas, J.; Luukkanen, J.; Kaivo-Oja, J. Linking analyses and environmental Kuznets curves for aggregated material flows in the EU. J. Clean. Prod. 2007, 15, 1662–1673. [Google Scholar] [CrossRef]

- Szulecki, K. European energy governance and decarbonization policy: Learning from the 2020 strategy. Clim. Policy 2016, 16, 543–547. [Google Scholar] [CrossRef]

- Steger, S.; Bleischwitz, R. Decoupling GDP from resource use, resource productivity and competitiveness: A cross-country comparison. In Sustainable Growth and Resource Productivity: Economic and Global Policy Issues; Routledge: London, UK, 2017. [Google Scholar] [CrossRef]

- Chovancová, J.; Tej, J. Decoupling economic growth from greenhouse gas emissions: The case of the energy sector in V4 countries. Equilibrium 2020, 15, 235–251. [Google Scholar] [CrossRef]

- Sanyé-Mengual, E.; Secchi, M.; Corrado, S.; Beylot, A.; Sala, S. Assessing the decoupling of economic growth from environmental impacts in the European Union: A consumption-based approach. J. Clean. Prod. 2019, 236, 117535. [Google Scholar] [CrossRef]

- Zhang, Y.; Song, W.; Fu, S.; Yang, D. Decoupling of land use intensity and ecological environment in Gansu province, China. Sustainability 2020, 12, 2779. [Google Scholar] [CrossRef]

- Finel, N.; Tapio, P. Decoupling Transport CO2 from GDP; Finland Futures Research Centre Ebook: Turku, Finland, 2012. [Google Scholar]

- Tapio, P. Towards a theory of decoupling: Degrees of decoupling in the EU and the case of road traffic in Finland between 1970 and 2001. Transp. Policy 2005, 12, 137–151. [Google Scholar] [CrossRef]

- Ru, X.; Chen, S.; Dong, H. An empirical study on relationship between economic growth and carbon emissions based on decoupling theory. J. Sustain. Dev. 2012, 5, 43. [Google Scholar] [CrossRef]

- Jiang, X.T.; Su, M.; Li, R. Investigating the factors influencing the decoupling of transport-related carbon emissions from turnover volume in China. Sustainability 2018, 10, 3034. [Google Scholar] [CrossRef]

- Zhang, L.; Kou, C.; Zheng, J.; Li, Y. Decoupling analysis of CO2 emissions in transportation sector from economic growth during 1995–2015 for six cities in Hebei, China. Sustainability 2018, 10, 4149. [Google Scholar] [CrossRef]

- Wang, Q.; Wang, S.; Li, R. Determinants of decoupling economic output from carbon emission in the transport sector: A comparison study of four municipalities in China. Int. J. Environ. Res. Public Health 2019, 16, 3729. [Google Scholar] [CrossRef]

- Zhang, X.; Ke, S. Linkage Analysis of the Resources, Population, and Economy in China’s Key State-Owned Forest Areas. Sustainability 2020, 12, 3855. [Google Scholar] [CrossRef]

- Balcilar, M.; Ozdemir, Z.A.; Tunçsiper, B.; Ozdemir, H.; Shahbaz, M. On the nexus among carbon dioxide emissions, energy consumption and economic growth in G-7 countries: New insights from the historical decomposition approach. Environ. Dev. Sustain. 2020, 22, 8097–8134. [Google Scholar] [CrossRef]

- Apergis, N.; Payne, J.E. Renewable energy consumption and economic growth: Evidence from a panel of OECD countries. Energy Policy 2010, 32, 1392–1397. [Google Scholar] [CrossRef]

- Apergis, N.; Payne, J.E. Energy consumption and economic growth in Central America: Evidence from a panel cointegration and error correction model. Energy Econ. 2009, 69, 2255–2260. [Google Scholar] [CrossRef]

- Ozturk, I.; Aslan, A.; Kalyoncu, H. Energy consumption and economic growth relationship: Evidence from panel data for low and middle income countries. Energy Policy 2010, 38, 4422–4428. [Google Scholar] [CrossRef]

- Fan, W.; Meng, M.; Lu, J.; Dong, X.; Wei, H.; Wang, X.; Zhang, Q. Decoupling Elasticity and Driving Factors of Energy Consumption and Economic Development in the Qinghai-Tibet Plateau. Sustainability 2020, 12, 1326. [Google Scholar] [CrossRef]

- Omri, A. An international literature survey on energy-economic growth nexus: Evidence from country-specific studies. Renew. Sustain. Energy Rev. 2014, 38, 951–959. [Google Scholar] [CrossRef]

- Kan, S.; Chen, B.; Chen, G. Worldwide energy use across global supply chains: Decoupled from economic growth? Appl. Energy 2019, 250, 1235–1245. [Google Scholar] [CrossRef]

- Vural, G. Renewable and non-renewable energy-growth nexus: A panel data application for the selected Sub-Saharan African countries. Resour. Policy 2020, 65, 101568. [Google Scholar] [CrossRef]

- Ozturk, I.; Al-Mulali, U. Natural gas consumption and economic growth nexus: Panel data analysis for GCC countries. Renew. Sustain. Energy Rev. 2015, 51, 998–1003. [Google Scholar] [CrossRef]

- Ozcan, B.; Ari, A. Nuclear energy-economic growth nexus in OECD countries: A panel data analysis. J. Econ. Manag. Perspect. 2017, 11, 138–154. [Google Scholar]

- Shahbaz, M.; Shafiullah, M.; Papavassiliou, V.G.; Hammoudeh, S. The CO2–growth nexus revisited: A nonparametric analysis for the G7 economies over nearly two centuries. Energy Econ. 2017, 65, 183–193. [Google Scholar] [CrossRef]

- Zhou, X.; Zhang, M.; Zhou, M.; Zhou, M. A comparative study on decoupling relationship and influence factors between China’s regional economic development and industrial energy-related carbon emissions. J. Clean. Prod. 2017, 142, 783–800. [Google Scholar] [CrossRef]

- Naminse, E.; Zhuang, J. Economic Growth, Energy Intensity, and Carbon Dioxide Emissions in China. Pol. J. Environ. Stud. 2018, 27, 2193–2201. [Google Scholar] [CrossRef]

- Chovancová, J.; Vavrek, R. (De)coupling Analysis with Focus on Energy Consumption in EU Countries and Its Spatial Evaluation. Pol. J. Environ. Stud. 2020, 29, 2091–2100. [Google Scholar] [CrossRef]

- Yang, Y.; Jia, J.; Chen, C. Residential Energy-Related CO2 Emissions in China’s Less Developed Regions: A Case Study of Jiangxi. Sustainability 2020, 12, 2000. [Google Scholar] [CrossRef]

- Sadorsky, P. Energy related CO2 emissions before and after the financial crisis. Sustainability 2020, 12, 3867. [Google Scholar] [CrossRef]

- Turner, K.; Hanley, N. Energy efficiency, rebound effects and the environmental Kuznets Curve. Energy Econ. 2011, 33, 709–720. [Google Scholar] [CrossRef]

- Dogan, E.; Turkekul, B. CO2 emissions, real output, energy consumption, trade, urbanization and financial development: Testing the EKC hypothesis for the USA. Environ. Sci. Pollut. Res. 2016, 23, 1203–1213. [Google Scholar] [CrossRef] [PubMed]

- Balado-Naves, R.; Baños-Pino, J.F.; Mayor, M. Do countries influence neighbouring pollution? A spatial analysis of the EKC for CO2 emissions. Energy Policy 2018, 123, 266–279. [Google Scholar] [CrossRef]

- Ang, J.B. CO2 emissions, energy consumption, and output in France. Energy Policy 2007, 30, 271–278. [Google Scholar] [CrossRef]

- Tiba, S.; Omri, A. Literature survey on the relationships between energy, environment and economic growth. Renew. Sustain. Energy Rev. 2017, 69, 1129–1146. [Google Scholar] [CrossRef]

- Zhang, X.; Zhang, H.; Yuan, J. Economic growth, energy consumption, and carbon emission nexus: Fresh evidence from developing countries. Environ. Sci. Pollut. Res. 2019, 26, 26367–26380. [Google Scholar] [CrossRef]

- Odugbesan, J.A.; Rjoub, H. Relationship among economic growth, energy consumption, CO2 emission, and urbanization: Evidence from MINT countries. Sage Open 2020, 10, 2158244020914648. [Google Scholar] [CrossRef]

- Raggad, B. Carbon dioxide emissions, economic growth, energy use, and urbanization in Saudi Arabia: Evidence from the ARDL approach and impulse saturation break tests. Environ. Sci. Pollut. Res. 2018, 25, 14882–14898. [Google Scholar] [CrossRef]

- Farhani, S.; Ozturk, I. Causal relationship between CO2 emissions, real GDP, energy consumption, financial development, trade openness, and urbanization in Tunisia. Environ. Sci. Pollut. Res. 2015, 22, 15663–15676. [Google Scholar] [CrossRef]

- Dickey, D.A.; Fuller, W.A. Distribution of the estimators for autoregressive time series with a unit root. J. Am. Stat. Assoc. 1979, 74, 427–431. [Google Scholar]

- Kwiatkowski, D.; Phillips, P.C.B.; Schmidt, P.; Shin, Y. Testing the null hypothesis of stationarity against the alternative of a unit root: How sure are we that economic time series have a unit root? J. Econom. 1992, 54, 159–178. [Google Scholar] [CrossRef]

- Pesaran, M.H.; Shin, Y.; Smith, R.J. Bounds testing approaches to the analysis of level relationships. J. Appl. Econom. 2001, 16, 289–326. [Google Scholar] [CrossRef]

- Kripfganz, S.; Schneider, D.C. Response surface regressions for critical value bounds and approximate p-values in equilibrium correction models. Oxf. Bull. Econ. Stat. 2020, 82, 1456–1481. [Google Scholar] [CrossRef]

- Pesaran, M.H.; Shin, Y. An autoregressive distributed lag modelling approach to cointegration analysis. In Proceedings of the Symposium at the Centennial of Ragnar Frisch, the Norwegian Academy of Science and Letters, Oslo, Norway, 3–5 March 1995; pp. 371–413. [Google Scholar]

- Baum, C.F. Stata: The language of choice for time-series analysis? Stata J. 2005, 5, 46–63. [Google Scholar] [CrossRef]

- Hobijn, B.; Franses, P.H.; Ooms, M. Generalizations of the KPSS-Test for Stationarity; Econometric Institute Report 9802/A; Econometric Institute, Erasmus University Rotterdam: Rotterdam, The Netherlands, 1998. [Google Scholar]

- Türsoy, T. Causality between stock prices and exchange rates in Turkey: Empirical evidence from the ARDL bounds test and a combined cointegration approach. Int. J. Financ. Stud. 2017, 5, 8. [Google Scholar] [CrossRef]

- Magazzino, C. The relationship between real GDP, CO2 emissions, and energy use in the GCC countries: A time series approach. Cogent Econ. Financ. 2016, 4, 1152729. [Google Scholar] [CrossRef]

- Liu, H.; Lei, M.; Zhang, N.; Du, G. The causal nexus between energy consumption, carbon emissions and economic growth: New evidence from China, India and G7 countries using convergent cross mapping. PLoS ONE 2019, 14, e0217319. [Google Scholar] [CrossRef]

- Chukwunonso Bosah, P.; Li, S.; Kwaku Minua Ampofo, G.; Akwasi Asante, D.; Wang, Z. The nexus between electricity consumption, economic growth, and CO2 emission: An asymmetric analysis using nonlinear ARDL and nonparametric causality approach. Energies 2020, 13, 1258. [Google Scholar] [CrossRef]

- Narayan, P.K.; Smyth, R. Energy consumption and real GDP in G7 countries: New evidence from panel cointegration with structural breaks. Energy Econ. 2008, 30, 2331–2341. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| GDP per Capita | Per Capita CO2 Emissions | Energy Consumption per Capita | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| n | Mean | Minimum | Maximum | Std. Dev. | n | Mean | Minimum | Maximum | Std. Dev. | n | Mean | Minimum | Maximum | Std. Dev. | |

| AT | 30 | 36,789.24 | 17,634.53 | 68,150.11 | 17,892.76 | 30 | 8.286 | 7.439 | 9.594 | 0.617 | 30 | 46,652.33 | 42,664.20 | 50,621.48 | 2254.917 |

| BH | 26 | 3359.70 | 319.01 | 6108.51 | 1934.13 | 30 | 4.368 | 0.814 | 8.065 | 1.814 | 25 | 17,226.60 | 7641.65 | 24,397.52 | 4741.948 |

| BG | 30 | 4524.79 | 1148.49 | 9828.15 | 2982.73 | 30 | 6.582 | 5.665 | 8.675 | 0.587 | 30 | 29,741.49 | 26,584.99 | 36,510.57 | 2025.429 |

| HR | 25 | 10,560.15 | 4841.59 | 16,296.81 | 4056.02 | 30 | 4.506 | 3.481 | 5.696 | 0.622 | 30 | 21,877.24 | 16,847.95 | 24,910.58 | 2330.444 |

| CZ | 30 | 12,927.16 | 2896.61 | 23,494.60 | 7345.48 | 30 | 11.839 | 9.450 | 15.879 | 1.528 | 30 | 47,113.08 | 43,317.38 | 52,778.71 | 2459.065 |

| DE | 30 | 35,068.21 | 22,303.96 | 47,959.99 | 9001.18 | 30 | 10.769 | 8.405 | 13.312 | 1.068 | 30 | 47,967.87 | 43,703.38 | 52,872.98 | 2129.842 |

| HU | 29 | 9682.84 | 3350.26 | 16,731.82 | 4688.72 | 30 | 5.644 | 4.444 | 7.080 | 0.637 | 30 | 27,931.73 | 24,560.78 | 31,349.12 | 1502.863 |

| MO | 20 | 5711.76 | 1627.07 | 8908.93 | 2336.99 | 30 | 1.860 | 0.850 | 6.363 | 1.384 | 25 | 9517.87 | 7428.63 | 17,673.63 | 2247.433 |

| ME | 25 | 1864.02 | 399.62 | 4503.52 | 1322.17 | 30 | 3.012 | 1.971 | 4.195 | 0.609 | 11 | 21,309.14 | 18,880.79 | 26,932.86 | 2409.799 |

| SR | 25 | 4659.06 | 914.79 | 7411.84 | 2014.25 | 30 | 5.130 | 3.736 | 6.654 | 0.816 | 25 | 20,644.23 | 13,785.32 | 23,829.86 | 2432.372 |

| RO | 30 | 5479.76 | 1102.10 | 12,919.53 | 4076.15 | 30 | 4.736 | 3.818 | 7.207 | 0.787 | 30 | 21,118.14 | 18,010.16 | 31,213.36 | 2757.741 |

| SK | 30 | 11,100.08 | 2405.54 | 19,406.35 | 6361.32 | 30 | 7.726 | 6.105 | 11.655 | 1.180 | 30 | 38,001.23 | 32,904.99 | 46,765.89 | 3164.200 |

| SI | 30 | 16,883.70 | 6562.02 | 27,483.34 | 7143.82 | 30 | 7.689 | 6.547 | 9.006 | 0.674 | 30 | 38,933.52 | 31,935.45 | 45,695.76 | 3126.459 |

| UA | 30 | 2019.46 | 635.70 | 4029.71 | 1122.81 | 30 | 7.093 | 4.984 | 13.715 | 2.107 | 30 | 33,351.75 | 21,501.22 | 61,620.08 | 9212.049 |

| Country | LGDP | CO2 | LEC | ||||

|---|---|---|---|---|---|---|---|

| Level | First Difference | Level | First Difference | Level | First Difference | ||

| Austria | AT | −0.694 | −3.923 ** | −1.388 | −5.993 *** | −2.204 | −8.166 *** |

| Bosnia and Herzegovina | BH | −5.939 *** | −3.081 * | 0.007 | −4.751 *** | −1.634 | −7.637 *** |

| Bulgaria | BG | −0.276 | −7.166 *** | −5.082 *** | −6.114 *** | −4.770 *** | −6.148 *** |

| Croatia | HR | −1.232 | −2.970 * | −1.393 | −6.704 *** | −1.371 | −5.746 *** |

| Czechia | CZ | −0.878 | −5.103 *** | −2.558 | −5.636 *** | −2.533 | −5.232 *** |

| Germany | DE | −1.213 | −4.551 *** | −1.109 | −6.339 *** | −1.748 | −8.602 *** |

| Hungary | HU | −1.163 | −3.689 ** | −2.248 | −4.935 *** | −2.636 | −4.386 *** |

| Moldova | MO | −2.849 | −2.919 * | −7.396 *** | −4.262 *** | −4.264 *** | −3.979 ** |

| Montenegro | ME | 0.066 | −3.688 ** | −2.253 | −9.797 *** | −4.528 *** | −6.131 *** |

| Serbia | SR | −1.382 | −5.482 *** | −2.483 | −6.992 *** | −2.642 | −5.893 *** |

| Romania | RO | 0.064 | −3.929 ** | −3.672 ** | −5.074 *** | −4.337 *** | −4.565 *** |

| Slovakia | SK | −2.106 | −3.317 * | −4.923 *** | −5.491 *** | −2.407 | −7.161 *** |

| Slovenia | SI | −0.670 | −4.936 *** | −0.871 | −4.888 *** | −1.885 | −6.057 *** |

| Ukraine | UA | −0.438 | −3.364 * | −5.454 *** | −3.286 * | −1.421 | −3.762 ** |

| Country | Variable | F-Statistic | I (0) Bound (5%) | I (1) Bound (5%) | Cointegration | Decision | |

|---|---|---|---|---|---|---|---|

| Austria | AT | LGDP | 4.164 | 4.364 | 5.613 | No | short-run model |

| CO2 | 14.306 | 4.366 | 5.666 | Yes | error correction model | ||

| LEC | 4.820 | 4.378 | 5.935 | No | short-run model | ||

| Bosnia and Herzegovina | BH | LGDP | crashed | error correction model | |||

| CO2 | crashed | error correction model | |||||

| LEC | crashed | error correction model | |||||

| Bulgaria | BG | LGDP | 0.557 | 4.364 | 5.613 | No | short-run model |

| CO2 | 1.509 | 4.366 | 5.666 | No | short-run model | ||

| LEC | 1.790 | 4.366 | 5.666 | No | short-run model | ||

| Croatia | HR | LGDP | 11.169 | 4.705 | 6.435 | Yes | error correction model |

| CO2 | 14.444 | 4.705 | 6.435 | Yes | error correction model | ||

| LEC | crashed | error correction model | |||||

| Czechia | CZ | LGDP | 5.558 | 4.364 | 5.613 | No | short-run model |

| CO2 | 21.747 | 4.364 | 5.613 | Yes | error correction model | ||

| LEC | 4.015 | 4.366 | 5.666 | No | short-run model | ||

| Germany | DE | LGDP | 0.442 | 4.364 | 5.613 | No | short-run model |

| CO2 | 0.701 | 4.366 | 5.666 | No | short-run model | ||

| LEC | 2.372 | 4.366 | 5.666 | No | short-run model | ||

| Hungary | HU | LGDP | 1.568 | 4.397 | 5.660 | No | short-run model |

| CO2 | 3.046 | 4.407 | 5.778 | No | short-run model | ||

| LEC | 2.091 | 4.402 | 5.719 | No | short-run model | ||

| Serbia | SR | LGDP | crashed | short-run model | |||

| CO2 | crashed | error correction model | |||||

| LEC | 21.533 | 4.855 | 6.415 | Yes | error correction model | ||

| Romania | RO | LGDP | 1.783 | 4.366 | 5.666 | No | short-run model |

| CO2 | 1.162 | 4.373 | 5.828 | No | short-run model | ||

| LEC | 2.365 | 4.366 | 5.666 | No | short-run model | ||

| Slovakia | SK | LGDP | 3.136 | 4.369 | 5.720 | No | short-run model |

| CO2 | 7.648 | 4.364 | 5.613 | Yes | error correction model | ||

| LEC | 2.914 | 4.366 | 5.666 | No | short-run model | ||

| Slovenia | SI | LGDP | 0.524 | 4.366 | 5.666 | No | short-run model |

| CO2 | 7.538 | 4.366 | 5.666 | Yes | error correction model | ||

| LEC | 23.935 | 4.364 | 5.613 | Yes | error correction model | ||

| Ukraine | UA | LGDP | 4.966 | 4.369 | 5.720 | No | short-run model |

| CO2 | 18.00 | 4.376 | 8.882 | Yes | error correction model | ||

| LEC | 4.428 | 4.366 | 5.666 | No | short-run model |

| Long-Run Statistics | Diagnostic Test | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Dependent | LGDPt | CO2t | LECt | ECT | Normality | Ser. Corr | Homoskedasticity | Stability | |

| Variable | p-Value | p-Value | p-Value | ||||||

| AT | ΔLGDPt | 0.87 | 0.51 | 0.48 | stable | ||||

| ΔCO2t | −0.56 ** | 10.50 *** | −0.61 *** | 0.10 | 0.76 | 0.82 | stable | ||

| ΔLECt | 0.61 | 0.01 ** | 0.41 | stable | |||||

| BH | ΔLGDPt | 0.43 *** | −2.59 * | −0.38 * | 0.27 | 0.44 | 0.39 | stable | |

| ΔCO2t | 1.99 *** | 3.39 * | −1.10 ** | 0.01 ** | 0.02 * | 0.39 | stable | ||

| ΔLECt | −0.40 *** | 0.25 *** | −2.00 ** | 0.64 | 0.75 | 0.39 | stable | ||

| BG | ΔLGDPt | 0.61 | 0.49 | 0.02 * | stable | ||||

| ΔCO2t | 0.34 | 0.25 | 0.88 | stable | |||||

| ΔLECt | 0.46 | 0.63 | 0.78 | stable | |||||

| HR | ΔLGDPt | −3.50 | 45.21 | −0.09 | 0.00 *** | 0.67 | 0.40 | stable | |

| ΔCO2t | −0.80 ** | 12.38 *** | −0.92 ** | 0.00 *** | 0.19 | 0.40 | stable | ||

| ΔLECt | 0.05 ** | 0.08 *** | −2.17 *** | 0.00 *** | 0.33 | 0.40 | stable | ||

| CZ | ΔLGDPt | 0.76 | 0.09 | 0.41 | stable | ||||

| ΔCO2t | −1.64 *** | 15.54 *** | −0.64 *** | 0.18 | 0.53 | 0.12 | stable | ||

| ΔLECt | 0.65 | 0.92 | 0.71 | stable | |||||

| DE | ΔLGDPt | 0.93 | 0.78 | 0.41 | stable | ||||

| ΔCO2t | 0.07 | 0.41 | 0.47 | stable | |||||

| ΔLECt | 0.82 | 0.60 | 0.73 | stable | |||||

| HU | ΔLGDPt | 0.87 | 0.99 | 0.40 | stable | ||||

| ΔCO2t | 0.19 | 0.63 | 0.26 | stable | |||||

| ΔLECt | 0.44 | 0.08 | 0.40 | stable | |||||

| SR | ΔLGDPt | 0.00 ** | 0.52 | 0.39 | stable | ||||

| ΔCO2t | −0.52 * | 12.31 ** | −1.68 * | 0.00 *** | 0.03 * | 0.39 | stable | ||

| ΔLECt | 0.02 | 0.04 ** | −1.37 *** | 0.00 *** | 0.22 | 0.39 | stable | ||

| RO | ΔLGDPt | 0.48 | 0.77 | 0.41 | stable | ||||

| ΔCO2t | 0.61 | 0.11 | 0.41 | stable | |||||

| ΔLECt | 0.15 | 0.73 | 0.05 | stable | |||||

| SK | ΔLGDPt | 0.66 | 0.92 | 0.82 | stable | ||||

| ΔCO2t | −0.38 * | 7.85 *** | −0.49 *** | 0.05 | 0.99 | 0.29 | stable | ||

| ΔLECt | 0.62 | 0.44 | 0.64 | stable | |||||

| SI | ΔLGDPt | 0.36 | 0.31 | 0.41 | stable | ||||

| ΔCO2t | −1.04 ** | 11.41 *** | −0.59 ** | 0.40 | 0.82 | 0.96 | stable | ||

| ΔLECt | 0.07 *** | 0.08 *** | −0.84 *** | 0.99 | 0.10 | 0.19 | stable | ||

| UA | ΔLGDPt | 0.20 | 0.41 | 0.76 | stable | ||||

| ΔCO2t | 0.39 ** | 4.22 *** | −0.57 *** | 0.00 *** | 0.65 | 0.41 | stable | ||

| ΔLECt | 0.85 | 0.65 | 0.22 | stable | |||||

| Country | Long-Run | Short-Run |

| AT |  |  |

| BH |  |  |

| BG |  |  |

| HR |  |  |

| CZ |  |  |

| DE |  |  |

| HU |  |  |

| SR |  |  |

| RO |  |  |

| SK |  |  |

| SI |  |  |

| UA |  |  |

Uni-directional long-run relationship;

Uni-directional long-run relationship;  Bi-directional long-run relationship;

Bi-directional long-run relationship;  Uni-directional short-run relationship;

Uni-directional short-run relationship;  Bi-directional short-run relationship. Note 2: GDP—gross domestic product, CO2—carbon dioxide, EC—energy consumption.

Bi-directional short-run relationship. Note 2: GDP—gross domestic product, CO2—carbon dioxide, EC—energy consumption.| Short-Run Statistics | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Dependent | ΔLGDP | ΔCO2 | ΔLEC | |||||||||||||

| Variable | t | t−1 | t−2 | t−3 | t−4 | t | t−1 | t−2 | t−3 | t−4 | t | t−1 | t−2 | t−3 | t−4 | |

| AT | ΔLGDPt | 0.37 | 0.14 | −0.44 | ||||||||||||

| ΔCO2t | 1.28 *** | |||||||||||||||

| ΔLECt | 0.02 | −0.04 | 0.06 | 0.15 **** | 0.03 ** | −0.02 | −0.13 | −0.06 | 0.23 | 0.43 ** | ||||||

| BH | ΔLGDPt | −0.12 | −0.78 ** | −0.02 | −0.09 | 0.80 ** | 0.22 | −0.24 | −0.29 * | |||||||

| ΔCO2t | 1.55 | −0.74 | 2.45 | 0.51 * | −2.49 | −1.26 | 1.10 | 1.57 ** | ||||||||

| ΔLECt | −0.30 * | −0.33 ** | −0.20 * | −0.05 | 0.93 ** | 0.45 * | ||||||||||

| BG | ΔLGDPt | −0.28 | 0.01 | 0.07 | ||||||||||||

| ΔCO2t | 0.01 | 0.003 | 6.95 *** | |||||||||||||

| ΔLECt | 0.02 | 0.10 *** | −0.07 | |||||||||||||

| HR | ΔLGDPt | 0.46 ** | 0.47 *** | −2.46 * | −2.66 ** | −1.83 ** | −1.14 ** | |||||||||

| ΔCO2t | 0.42 * | −0.04 | −1.07 ** | −5.89 ** | −3.46 * | −2.55 * | ||||||||||

| ΔLECt | 0.14 | −0.10 | −0.13 * | −0.00 | 0.13 ** | 0.94 * | 0.64 * | 0.26 | ||||||||

| CZ | ΔLGDPt | 0.30 | −0.33 | 0.63 ** | −0.27 * | 0.06 | 0.06 | 0.15 * | 1.38 | |||||||

| ΔCO2t | ||||||||||||||||

| ΔLECt | 0.10 * | 0.06 ** | −0.14 | |||||||||||||

| DE | ΔLGDPt | 0.54 * | −0.50 * | 0.35 | −0.39 | 0.37 * | −3.64 * | |||||||||

| ΔCO2t | 0.46 | 0.04 | 10.97 *** | |||||||||||||

| ΔLECt | −0.03 | 0.08 *** | −0.13 | |||||||||||||

| HU | ΔLGDPt | 0.62 ** | −0.43 | 0.70 * | −0.40 | 0.36 | −1.47 | |||||||||

| ΔCO2t | 0.17 | −0.04 | 4.80 *** | |||||||||||||

| ΔLECt | −0.03 | −0.002 | −0.02 | 0.13 * | 0.14 *** | 0.04 | 0.08 * | −0.15 | −0.43 * | |||||||

| SR | ΔLGDPt | −0.88 | 0.17 | 0.50 | 0.21 | 0.22 | 0.52 * | 0.42 * | −2.52 | −1.70 | −0.15 | −3.06 | −2.30 | |||

| ΔCO2t | 2.15 * | 2.86 * | 0.80 | −0.21 | −0.45 | −11.72 | −11.40 * | −10.01 | ||||||||

| ΔLECt | 0.51 ** | 0.39 * | ||||||||||||||

| RO | ΔLGDPt | 0.18 | 0.36 * | 0.35 * | −0.28 | −2.13 ** | 0.76 * | 1.54 ** | −0.49 | |||||||

| ΔCO2t | 0.73 * | −0.48 * | −0.25 * | −0.23 * | 0.89 *** | 3.02 ** | ||||||||||

| ΔLECt | 0.03 | 0.14 *** | −0.11 | |||||||||||||

| SK | ΔLGDPt | 0.45 * | 0.23 * | −0.49 * | ||||||||||||

| ΔCO2t | ||||||||||||||||

| ΔLECt | −0.06 | 0.10 ** | −0.28 | |||||||||||||

| SI | ΔLGDPt | 0.09 | −0.40 * | 0.07 | 0.09 | 0.08 | 0.11 * | −0.11 * | 0.62 | |||||||

| ΔCO2t | 0.77 | |||||||||||||||

| ΔLECt | ||||||||||||||||

| UA | ΔLGDPt | 0.27 * | 0.34 ** | 0.44 | ||||||||||||

| ΔCO2t | 0.59 * | 0.58 * | −0.31 ** | −0.12 * | 1.26 | |||||||||||

| ΔLECt | 0.03 | 0.11 ** | −0.09 | |||||||||||||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Litavcová, E.; Chovancová, J. Economic Development, CO2 Emissions and Energy Use Nexus-Evidence from the Danube Region Countries. Energies 2021, 14, 3165. https://doi.org/10.3390/en14113165

Litavcová E, Chovancová J. Economic Development, CO2 Emissions and Energy Use Nexus-Evidence from the Danube Region Countries. Energies. 2021; 14(11):3165. https://doi.org/10.3390/en14113165

Chicago/Turabian StyleLitavcová, Eva, and Jana Chovancová. 2021. "Economic Development, CO2 Emissions and Energy Use Nexus-Evidence from the Danube Region Countries" Energies 14, no. 11: 3165. https://doi.org/10.3390/en14113165

APA StyleLitavcová, E., & Chovancová, J. (2021). Economic Development, CO2 Emissions and Energy Use Nexus-Evidence from the Danube Region Countries. Energies, 14(11), 3165. https://doi.org/10.3390/en14113165