Snapshot of Photovoltaics—February 2019 †

Abstract

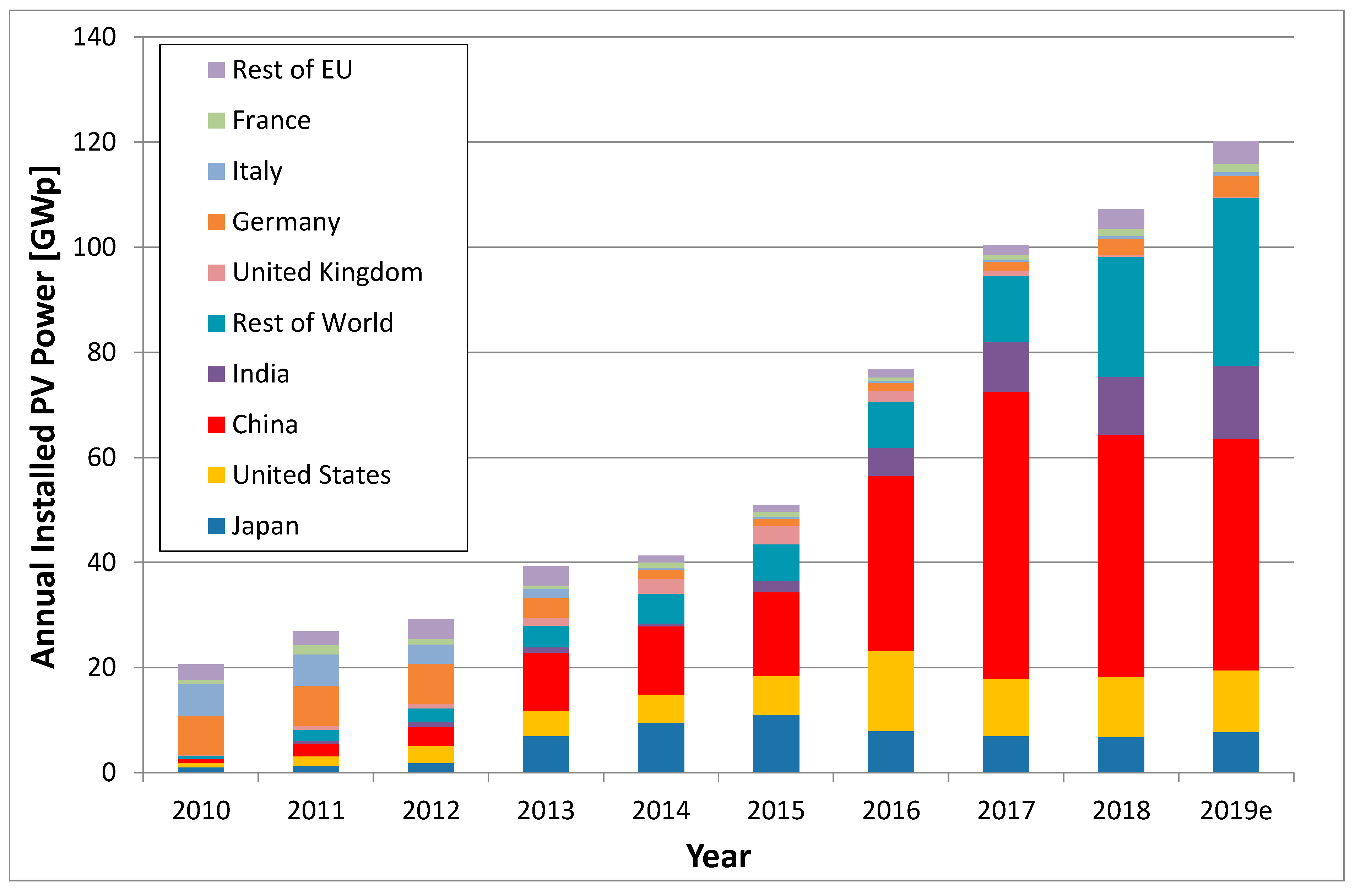

:1. Introduction

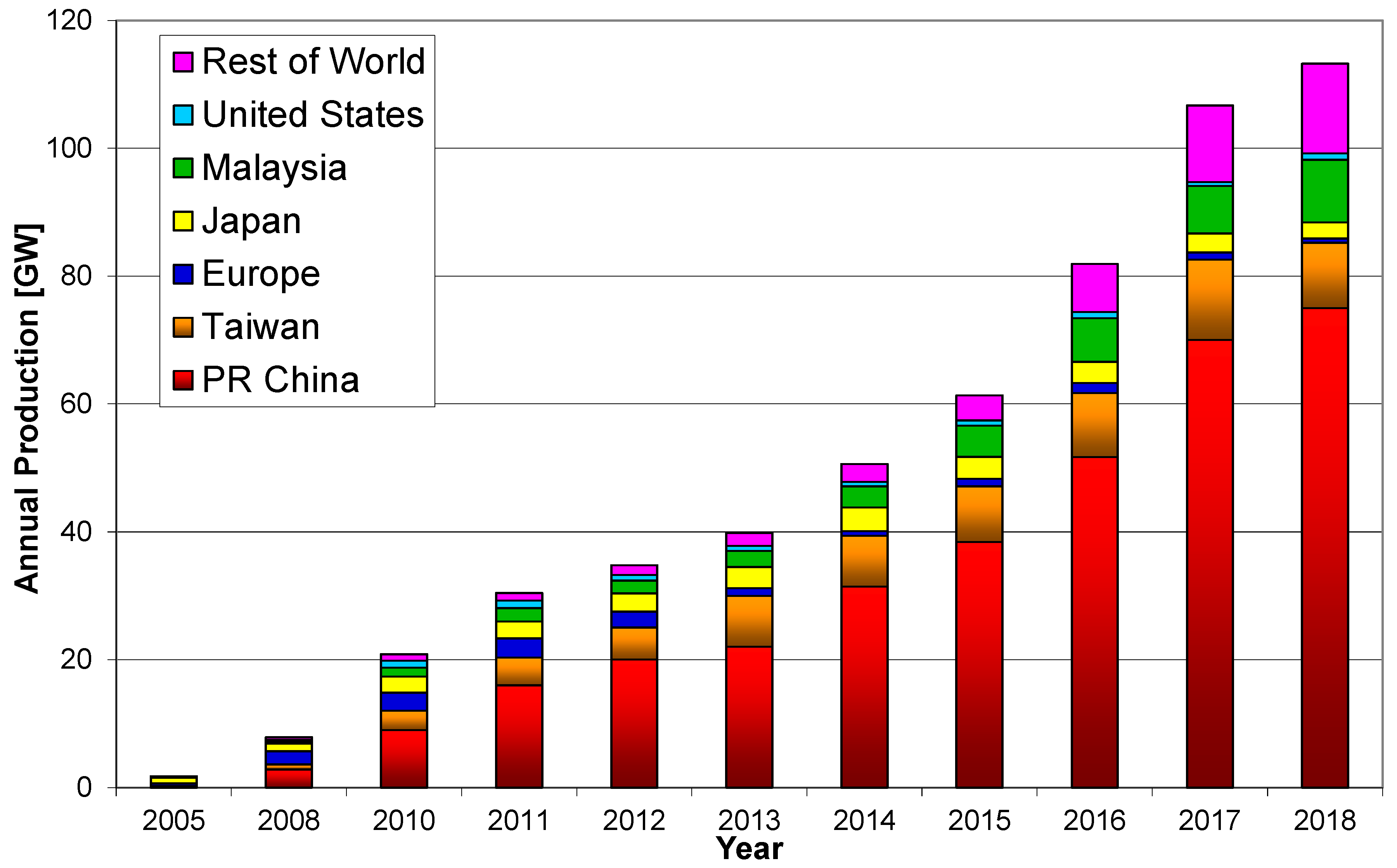

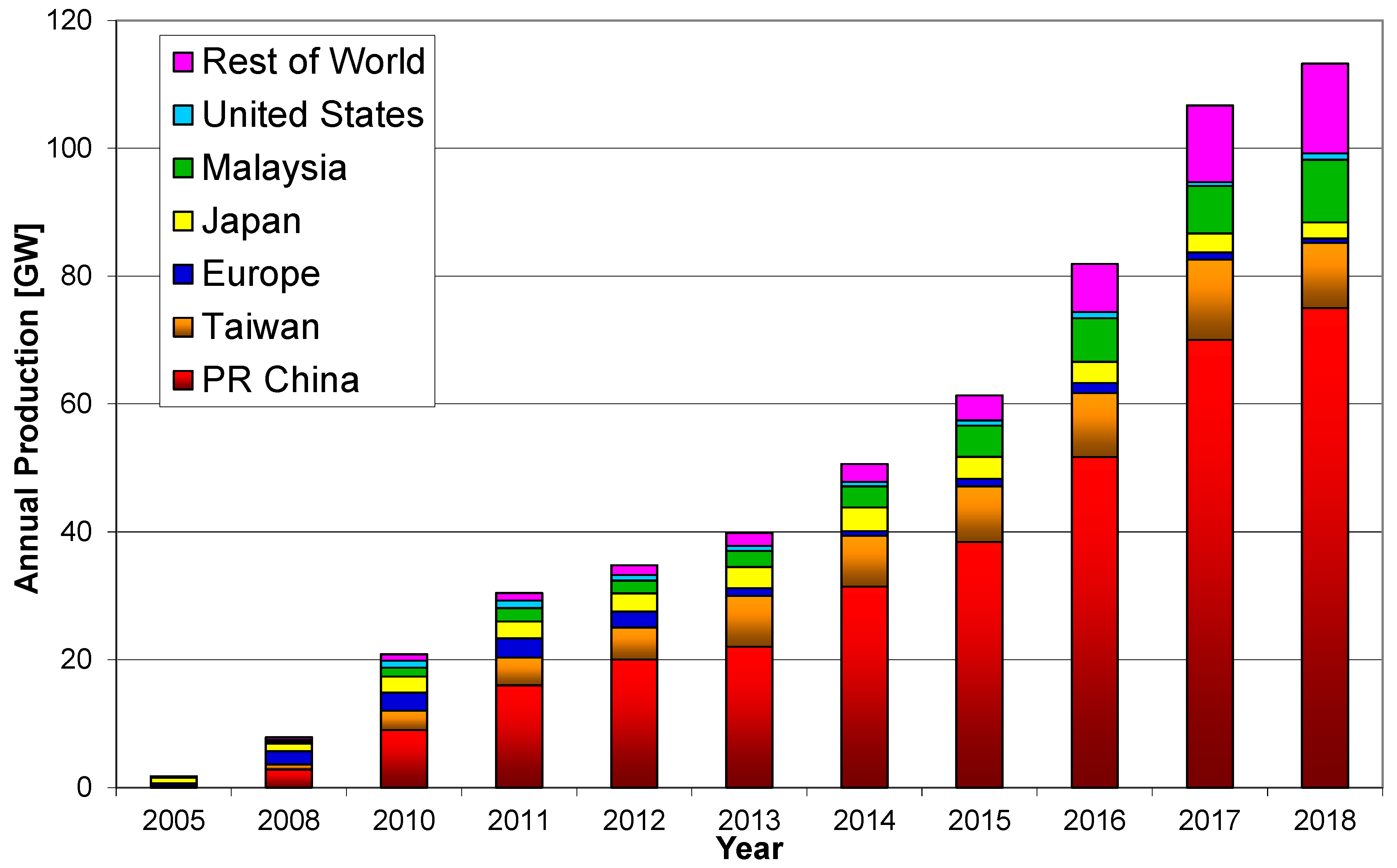

2. Photovoltaic Solar Cell Production

- Solar cell or thin film module production data are reported by a few companies only.

- Products in stock, but produced in the previous year, can be included in shipment data.

- The report of “solar products” in the shipment figures, which is often used, in general does not differentiate between the different products like wafers, cells, or modules.

- The risk of double counting has increased with the major uptake of original equipment manufacturing (OEM).

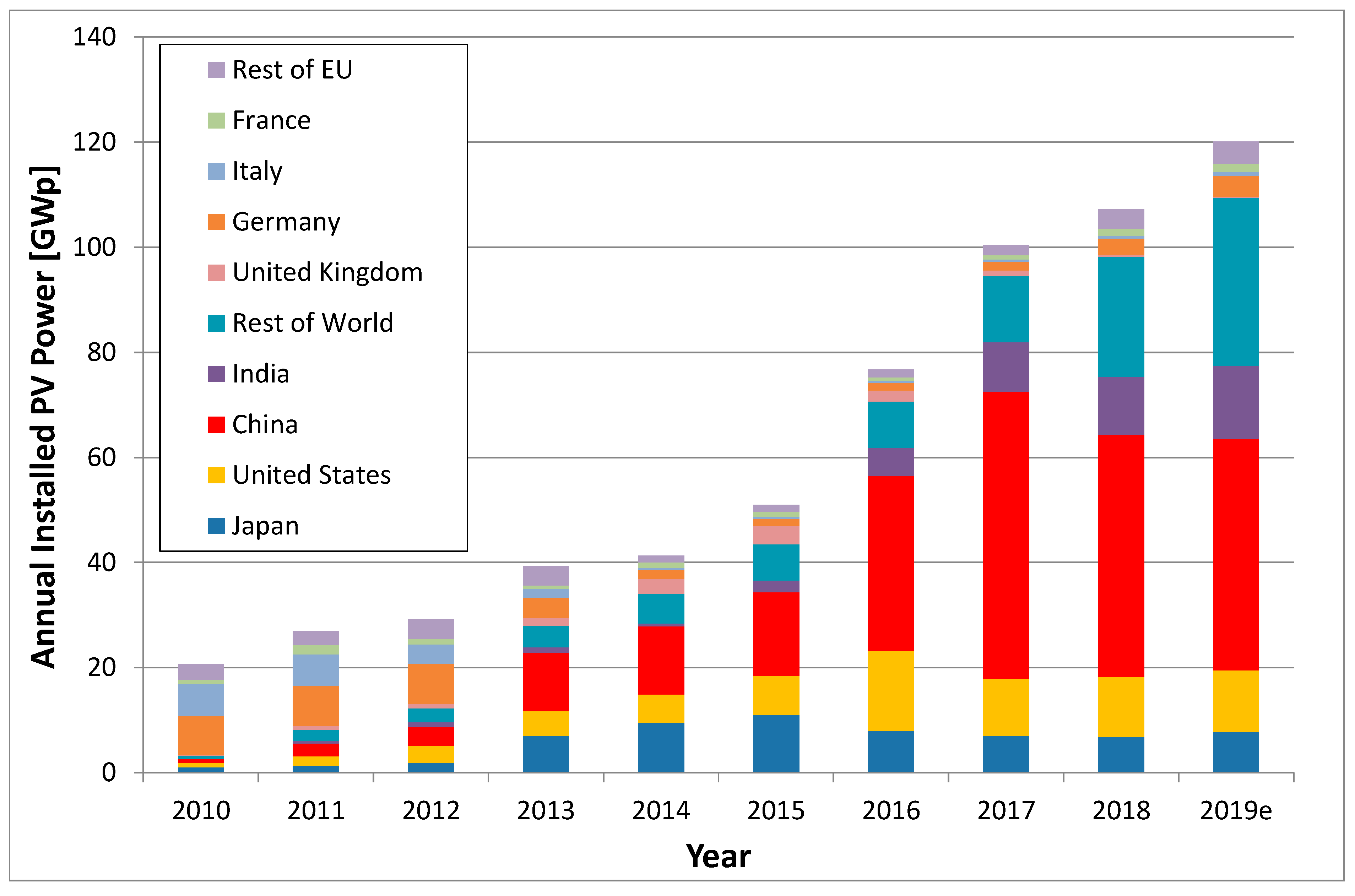

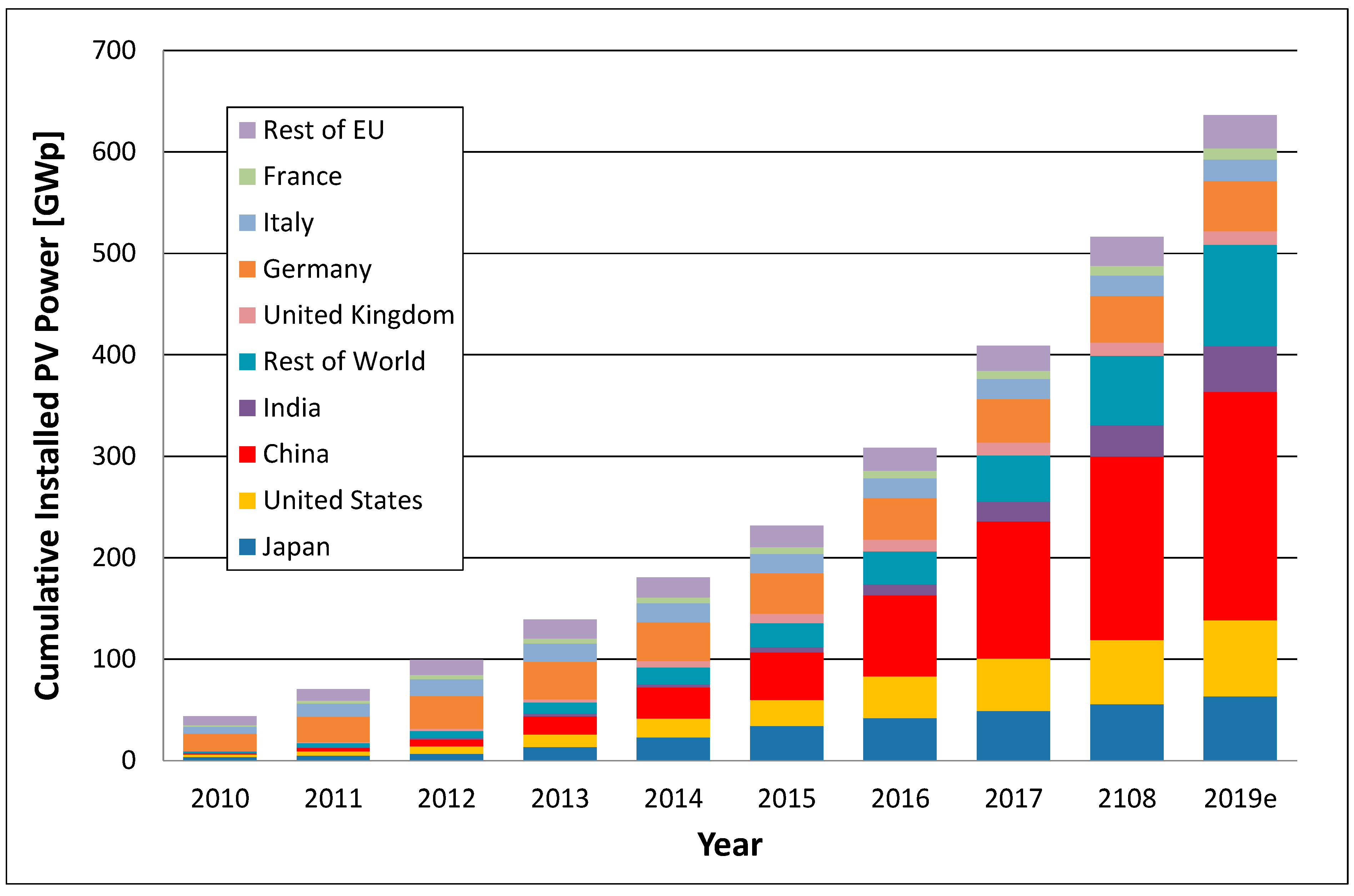

3. Solar PV Electricity generation and Markets

- Some statistics report system hardware installations, others report the actual connection to the grid or the start of electricity delivery. Missing grid capacities or administrative reasons have a major impact on the later.

- The installation figures in this communication report the physical installation of the PV system.

- Capacity figures can either be reported in nominal DC peak power (Wp) under standard test conditions (1000 W irradiance, air mass 1.5 light spectrum, and 25 °C device temperature) or utility peak AC power. In some statistics, both capacities are sometimes mixed, e.g., Eurostat.

- PV capacity figures in this communication are nominal DC peak power (Wp) for reasons of consistency.

- Not all countries have official PV capacity statistics, system installations, nor sales statistics.

4. Conclusions

Funding

Conflicts of Interest

References

- International Energy Agency. CO2 Emissions from Fuel Combustion; International Energy Agency: Paris, France, 2017; ISBN 978-92-64-27819-6. [Google Scholar]

- International Energy Agency. World Energy Outlook 2017; International Energy Agency: Paris, France, 2017; ISBN 978-92-64-28230-8. [Google Scholar]

- Breyer, Ch.; Bogdanov, D.; Aghahosseini, A.; Gulagi, A.; Child, M.; Oyewo, A.S.; Farfan, J.; Kristina Pasi Vainikka, S. Solar photovoltaics demand for the global energy transition in the power sector. Prog. Photovolt. Res. Appl. 2017, 1–19. [Google Scholar] [CrossRef]

- Jäger-Waldau, A. PV Status Report 2018; Publications Office of the European Union: Luxembourg, 2018; ISBN 978-92-79-97466-3. [Google Scholar]

- Hwang, A. Solar Wafer Production to See Over-Capacity by Year-End 2018. DIGITIMES, 9 January 2018. [Google Scholar]

- New Energy Finance. Q3 Levelised Cost of Energy Outlook; EU: Brussels, Belgium, 2009. [Google Scholar]

- Bloomberg New Energy Finance. 2H 2018 LCOE Update: PV; EU: Brussels, Belgium, 2018. [Google Scholar]

- Scaling Solar Senegal, Latest Tender Results. 3 April 2018. Available online: http://www.finergreen.com/wp-content/uploads/2017/04/18-04-06-Senegal-Scaling-Solar-Tender-Results.pdf (accessed on 21 February 2019).

- Bloomberg New Energy Finance. 4Q 2018 Global PV Market Outlook; EU: Brussels, Belgium, 2018. [Google Scholar]

- Solar Power Europe. Global Market Outlook for Solar Power 2018–2022; Solar Power Europe: Brussels, Belgium, 2018. [Google Scholar]

- International Energy Agency. Renewable Energy Market Report 2018—Market Trends and Projections to 2023; International Energy Agency: Paris, France, 2018; 210p, ISBN 978-92-64-30684-4. [Google Scholar]

- Solar Power Europe. Global Market Outlook for Photovoltaics; Solar Power Europe: Brussels, Belgium, 2018. [Google Scholar]

- Masson, G.; Kaizuka, I.; Lindahl, J.; Jaeger-Waldau, A.; Neubourg, G.; Ahm, P.; Donoso, J.; Tilli, F. A Snapshot of Global PV Markets—The Latest Survey Results on PV Markets and Policies from the IEA PVPS Programme in 2017. In Proceedings of the 2018 IEEE 7th World Conference on Photovoltaic Energy Conversion, WCPEC 2018—A Joint Conference of 45th IEEE PVSC, 28th PVSEC and 34th EU PVSEC, Waikaloa, HI, USA, 10–15 June 2018; Article number 8547794. pp. 3825–3828. [Google Scholar] [CrossRef]

- EurObserverPhotovoltaic Energy Barometer 2018. In Systèmes Solaires, le Journal du Photovoltaique; PE Barometer: London, UK, 2018.

- European Commission Statement/18/4155. 14 June 2018. Available online: http://europa.eu/rapid/press-release_STATEMENT-18-4155_en.htm (accessed on 30 January 2019).

- DIRECTIVE (EU) 2018/2001 of the European Parliament and of the Council of 11 December 2018 on the Promotion of the Use of Energy from Renewable Sources (Recast). Off. J. Eur. Union 2018, 328, 82–209.

- De Santi, G.; Jäger-Waldau, A.; Taylor, N.; Ossenbrink, H. Realizing solar power’s potential in the European Union. Philos. Trans. R. Soc. A 2013. [CrossRef] [PubMed]

- European Commission Communication. A Clean Planet for all—A European Strategic Long-Term Vision for a Prosperous, Modern, Competitive and Climate Neutral Economy; European Commission Communication: Brussels, Belgium, 2018. [Google Scholar]

- Greenpeace International; European Renewable Energy Council (EREC); Global Wind Energy Council (GWEC). Energy [R]evolution, 5th Edition 2015 World Energy Scenario, October 2015. Available online: http://www.greenpeace.org/international/en/publications/Campaign-reports/Climate-Reports/Energy-Revolution-2015 (accessed on 21 February 2019).

- Ram, M.; Bogdanov, D.; Aghahosseini, A.; Oyewo, A.S.; Gulagi, A.; Child, M.; Fell, H.-J.; Breyer, C. Global Energy System Based on 100% Renewable Energy—Power Sector; Lappeenranta University of Technology: Lappeenranta, Finland, 2017. [Google Scholar]

- Bloomberg New Energy Finance. New Energy Outlook 2018; EU: Brussels, Belgium, 2018. [Google Scholar]

- International Energy Agency. World Energy Outlook; International Energy Agency: Paris, France, 2016; ISBN 978-92-64-26495-3. [Google Scholar]

- International Energy Agency. World Energy Outlook; International Energy Agency: Paris, France, 2018; ISBN 978-92-64-30677-6. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

| Year | 2018 [GW] | 2020 [GW] | 2025 [GW] | 2030 [GW] | 2040 [GW] |

|---|---|---|---|---|---|

| Actual Installations | 516 | - | - | - | - |

| Greenpeace (reference scenario) | - | 332 | 413 | 494 | 635 |

| Greenpeace (advanced [r]evolution scenario) | - | 844 | 2000 | 3725 | 6678 |

| LUT 100% RES Power Sector | - | 1168 | 3513 | 6980 | 13,805 |

| BNEF NEO 2018 | - | 759 | 1353 | 2144 | 4527 |

| IEA New Policy Scenario 2016 | - | 481 | 715 | 949 | 1405 |

| IEA 450 ppm Scenario 2016 * | - | 517 | 814 | 1278 | 2108 |

| IEA New Policy Scenario 2018 * | - | 665 | 1109 | 1589 | 2540 |

| IEA Sustainable Development Scenario 2018 * | - | 750 | 1472 | 2346 | 4240 |

© 2019 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Jäger-Waldau, A. Snapshot of Photovoltaics—February 2019. Energies 2019, 12, 769. https://doi.org/10.3390/en12050769

Jäger-Waldau A. Snapshot of Photovoltaics—February 2019. Energies. 2019; 12(5):769. https://doi.org/10.3390/en12050769

Chicago/Turabian StyleJäger-Waldau, Arnulf. 2019. "Snapshot of Photovoltaics—February 2019" Energies 12, no. 5: 769. https://doi.org/10.3390/en12050769

APA StyleJäger-Waldau, A. (2019). Snapshot of Photovoltaics—February 2019. Energies, 12(5), 769. https://doi.org/10.3390/en12050769