Analysis of Carbon Leakage under Phase III of the EU Emissions Trading System: Trading Patterns in the Cement and Aluminium Sectors

Abstract

1. Introduction

- The move to a single union-wide cap, instead of national caps, standardised the approach to improve the harmonisation of ambition between Member States and therefore the level of allocation to their industries.

- Auctioning became the default method for allowance distribution, reducing the number of allowances that are provided for free.

- Harmonised rules for free allocation based on (emission performance) benchmarks (for products and fallback approaches for heat and fuels) standardised the approach for installations within each sector or sub-sector.

- The direct and indirect costs induced by the implementation of the ETS directive 2003/87/EC (and updates) would increase production cost, calculated as a proportion of the gross value added, by at least 5%; and;

- the sector’s trade intensity with non-EU countries (imports and exports) is above 10%.

- the sum of direct and indirect additional costs is at least 30%; or;

- the non-EU trade intensity is above 30%.

- (1)

- Cement manufacturing can be divided in two main steps: ‘clinker manufacturing (90% to 95% of emissions, virtually all from direct emissions), and blending and grinding clinker with other materials to produce cement (generating indirect emissions due to electricity use)’ [8]. Given that the majority of the emissions associated with the production of cement are embodied within an intermediate product, the import of clinker from non-regulated countries represents a carbon leakage risk [8]. The fact that cement is a relatively homogenous product adds to this risk as producers of cement essentially compete on price alone due to the lack of product specialisation. However, according to estimates by [9] the average total production cost per tonne of cement for Egypt (47 €/t), the EU (48 €/t) and Ukraine (53 €/t) were similar in 2011/12. In the assessment, the energy costs of the EU were lower than both Egypt and Ukraine but this was offset by relatively higher raw material and labour costs. To date, high transportation costs relative to product value have led to the creation of regional markets largely protected from international competition; despite regional variations in production costs. In the current carbon leakage list, the manufacture of cement is defined as being at a significant risk of carbon leakage for reasons of induced carbon costs alone as it well exceeds the 30% threshold (i.e., 45.5%) [6]. Despite the potential risk of carbon leakage for the cement sector due to carbon costs, recent ex-post evaluations in the literature suggest that this risk has not, so far, been realised and that carbon pricing impacts are more limited than experienced in other industrial sectors [7,10,11].

- (2)

- Aluminium production refers to both upstream (i.e., production of primary aluminium from alumina, which is energy intensive and the production of secondary aluminium from refining recycled waste and scrap that is less energy intensive) and downstream (i.e., aluminium rolling and aluminium extrusion) processes. Given the energy intensive nature of primary aluminium production, there is a risk that the impact of the EU ETS on energy prices is undermining the competitiveness of the sector. According to estimates by [9] the average cast aluminium prices ‘during 2012 and 2013 were 1572 €/t and 1391 €/t, respectively and the average of the estimated production costs of the EU industry for those years 1411 €/t and 1295 €/t, respectively’. Several countries were estimated to have lower total production costs per tonne of cast aluminium than the EU in 2012/13 (i.e., Kazakhstan: approx. 700 €/t and Iceland: approx. 1200 €/t) primarily due to lower energy prices. Interestingly the assessment shows that production costs for China were slightly higher than in the EU in 2012/13 reflecting the large number of smaller inefficient plants that still operate to meet domestic demand in the country. In the current leakage list, aluminium production is defined as being at a significant risk of carbon leakage for reasons of trade intensity alone as it exceeds the 30% threshold (35.9%) [6]. Evidence of carbon leakage effects in the aluminium sector is limited, so far, with several ex-post assessments [12,13] unable to observe beyond negligible effects of the EU ETS on trade patterns.

2. Methodology

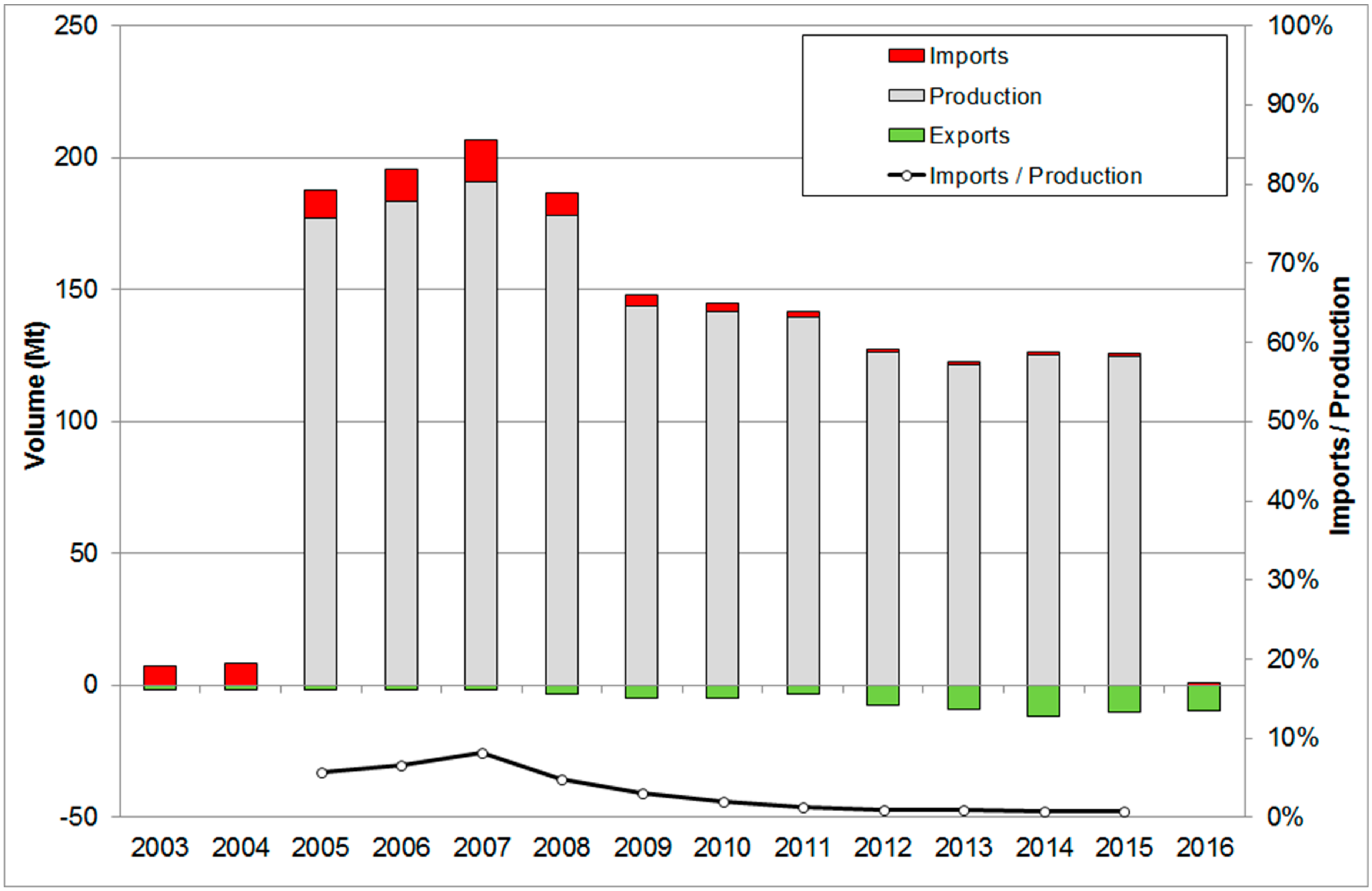

- EU-28 production, extra-European import and extra-European export volume

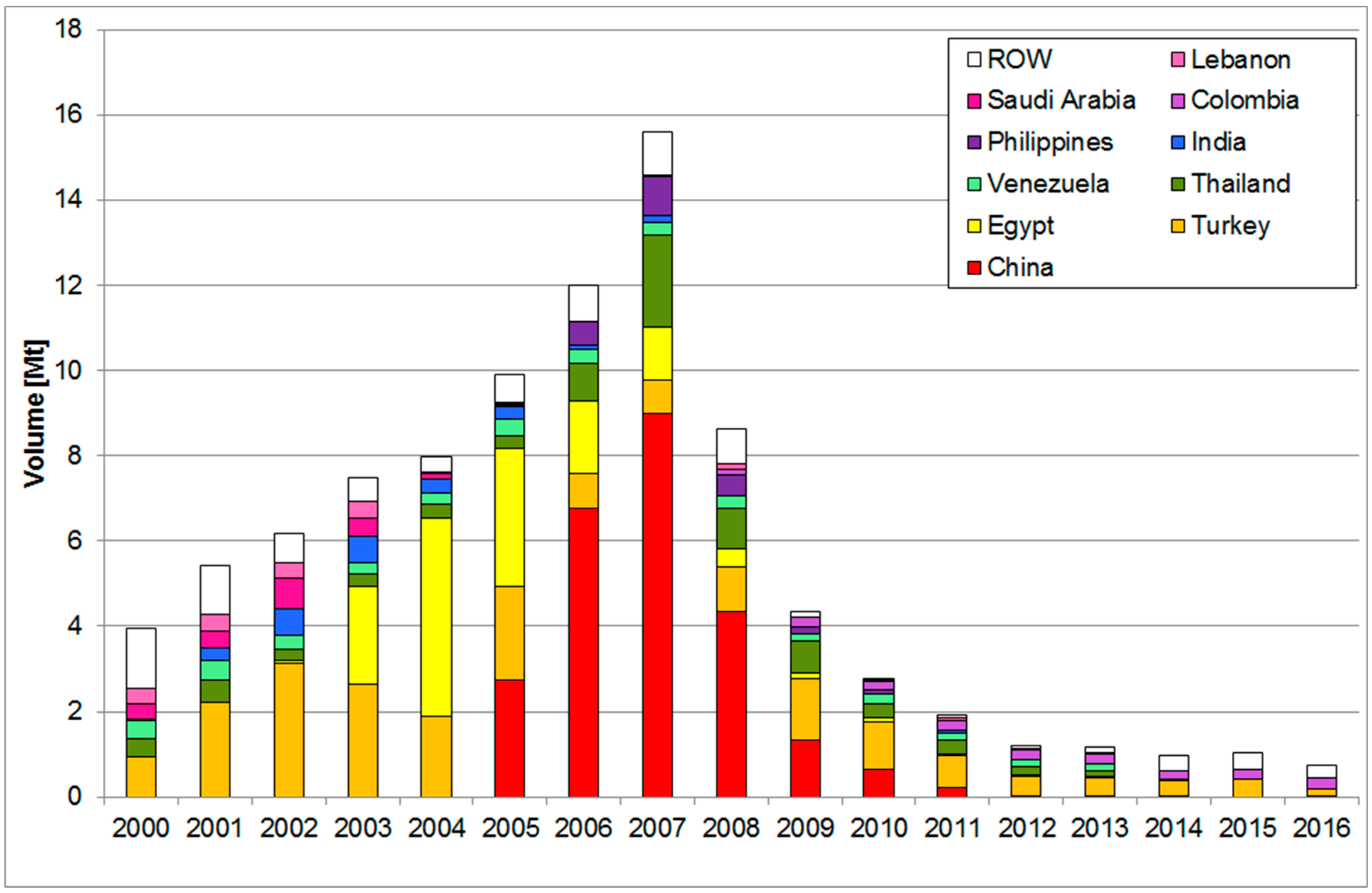

- EU-28 extra import volume by trading partner

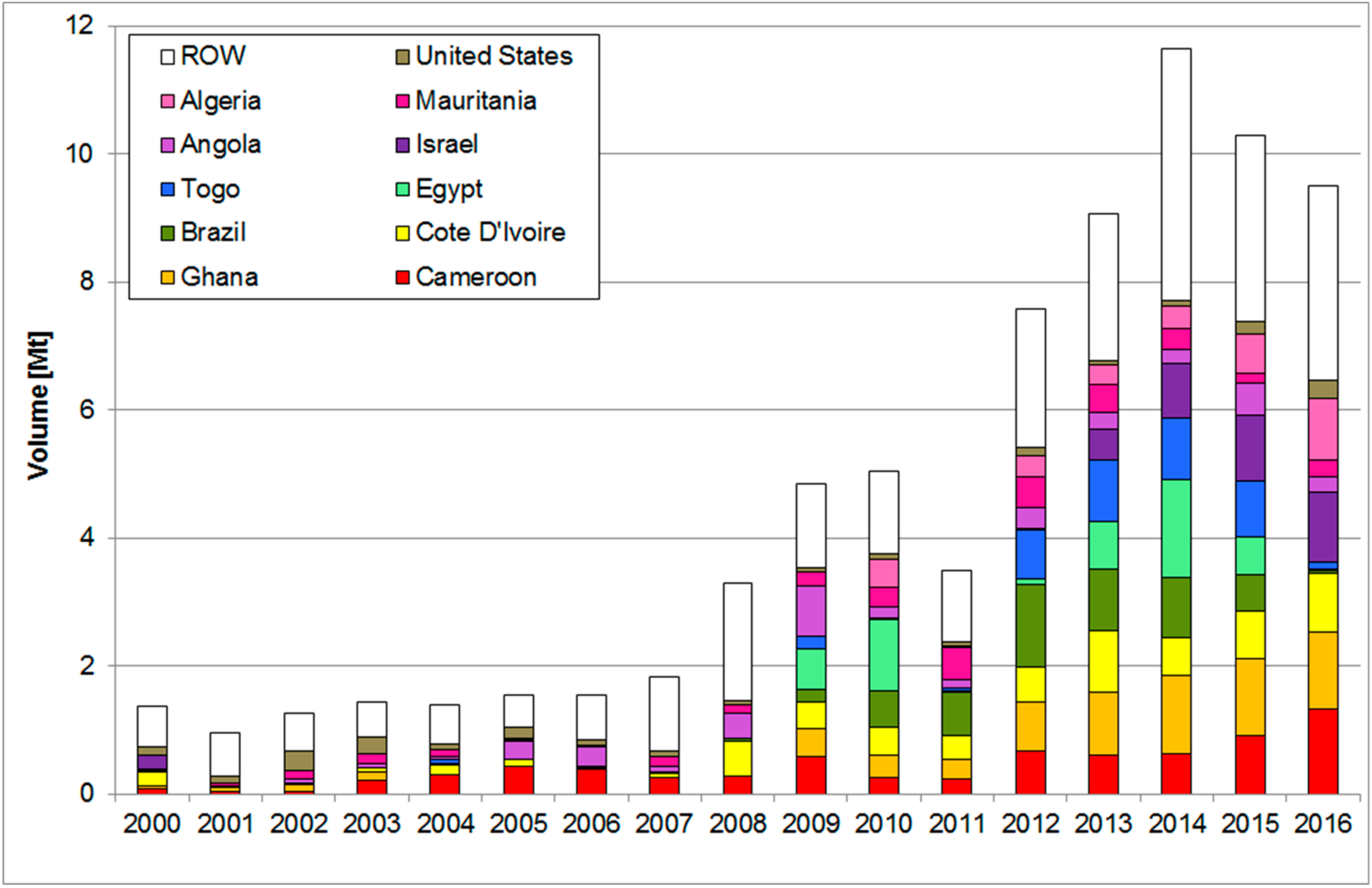

- EU-28 extra export volume by trading market

- Ratio extra-EU-28 imports / production

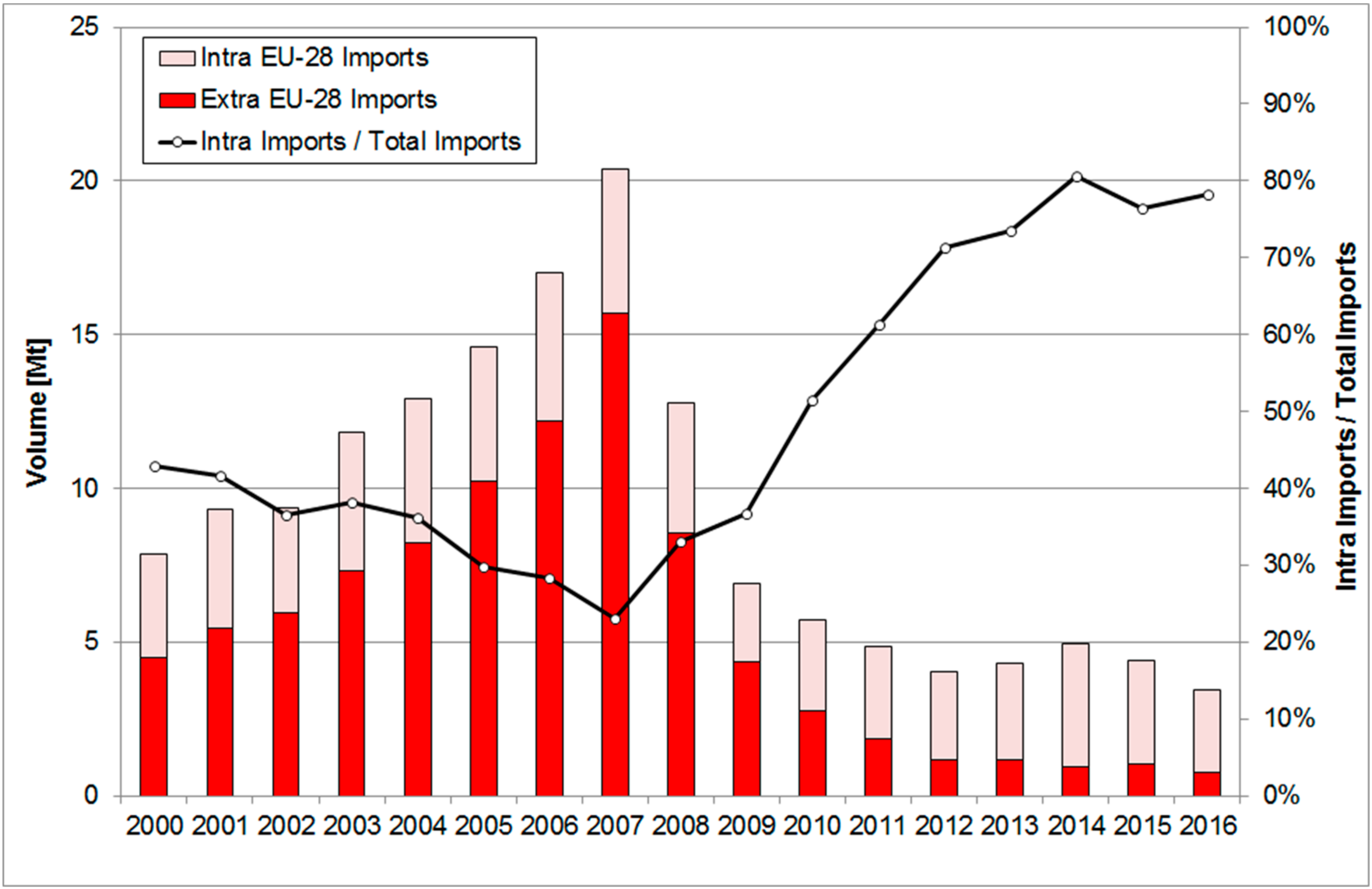

- Ratio EU-28 extra and intra import volume

- Ratio EU-28 intra and extra export volume

- EU-28 share in its main export markets

- (1)

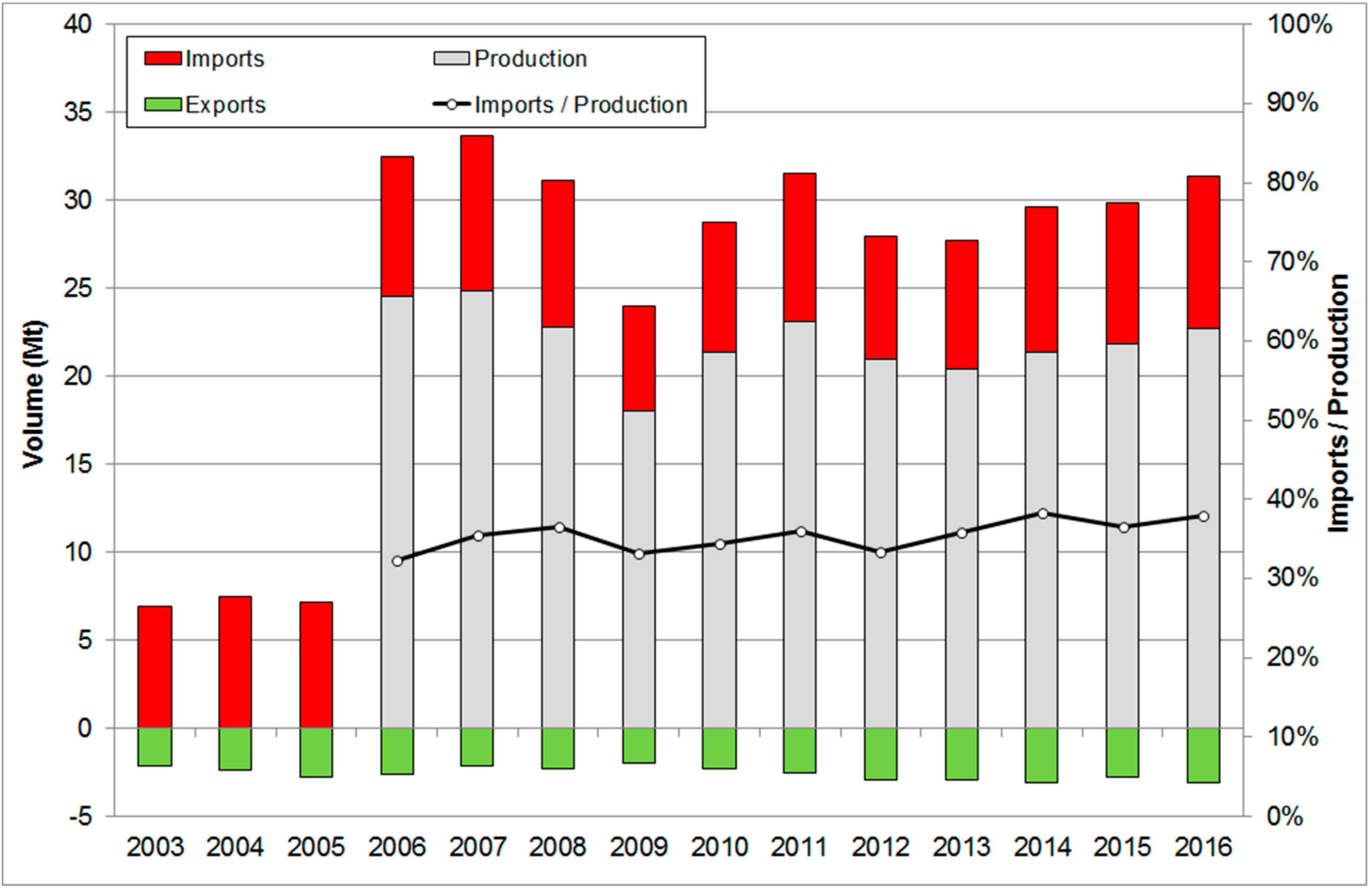

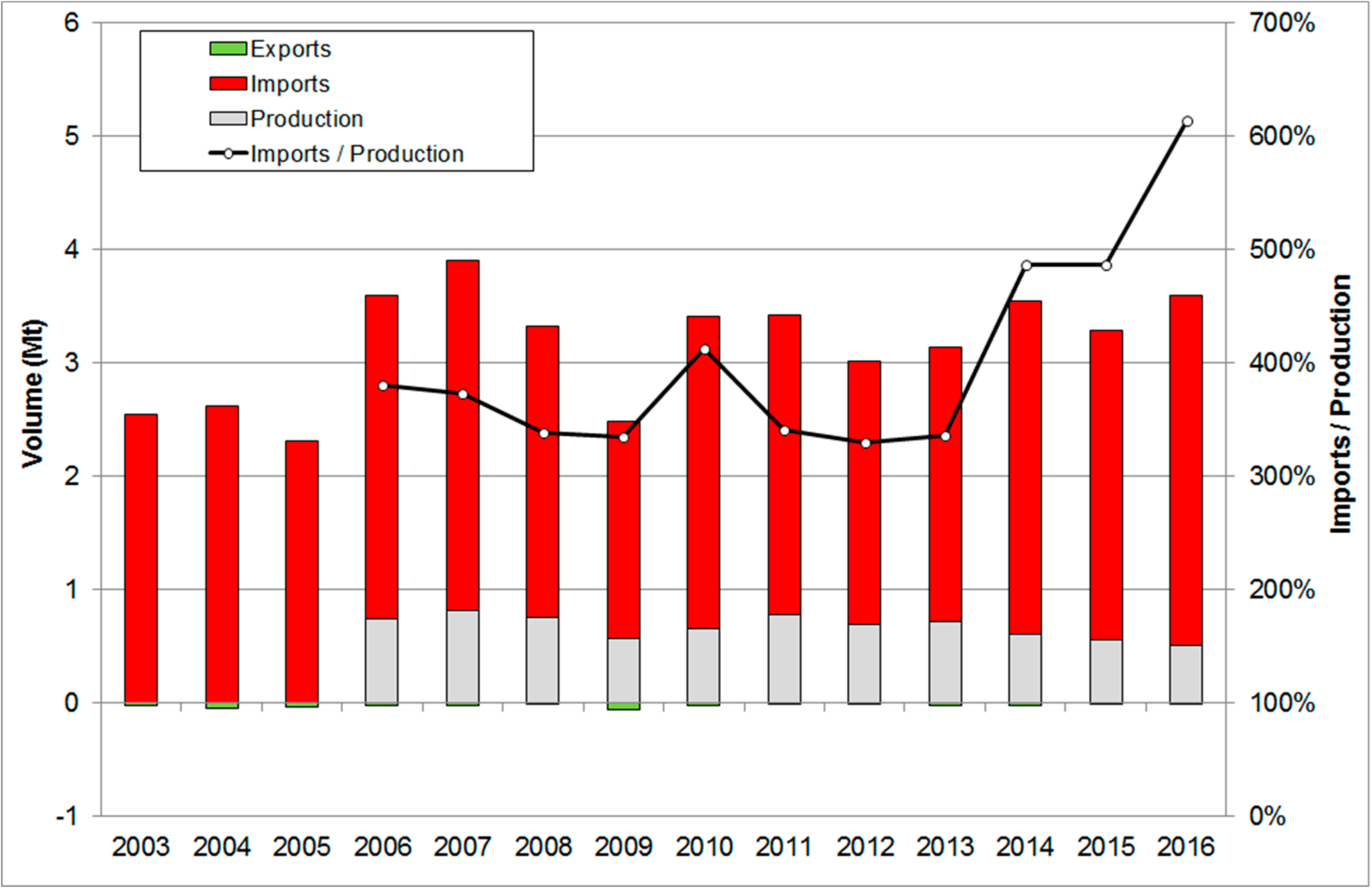

- PRODCOM: provides statistics on the production of manufactured goods together with related external trade data, which is obtained by the National Statistical Institutes who conduct a survey of enterprises. The survey is based on the PRODCOM List, consisting of about 3900 products. The eight digit codes used in the list are based on the six digit CPA headings (i.e., refers to the Statistical Classification of Products by Activity in the European Economic Community) and the four digit NACE rev 1.1 (i.e., refers to the Statistical classification of economic activities in the European Community). From 2008 onwards the PRODCOM code is linked to CPA 2008 and NACE Rev. 2 [14]. The dataset entitled, Sold production, exports and imports by PRODCOM list (NACE Rev. 2)—annual data, provides information on extra EU-28 imports and exports at an eight digit level of product disaggregation, which enables the assessment to observe the trade developments of specific products in the cement and aluminium sectors (i.e., cement clinker and unwrought non-alloyed aluminium, which were selected based upon the sector specific guidance document from the European Commission [15]). In addition, the dataset provides information on levels of sold production. Therefore this dataset can be used to consistently evaluate the relationship between domestic sold production, external imports and exports for products in the cement and aluminium sectors, and develop useful indicators to provide evidence of carbon leakage over time. However, if more reliable production data from industry is publically available then the assessment may include this information to ensure the production of a sector is accurately represented. In this first step, if we observe the ratio of imports to domestic production increasing for products in the European cement and aluminium sectors this may provide evidence of carbon leakage that would require further assessment to understand the explanatory factors driving this trend over the time period.

- (2)

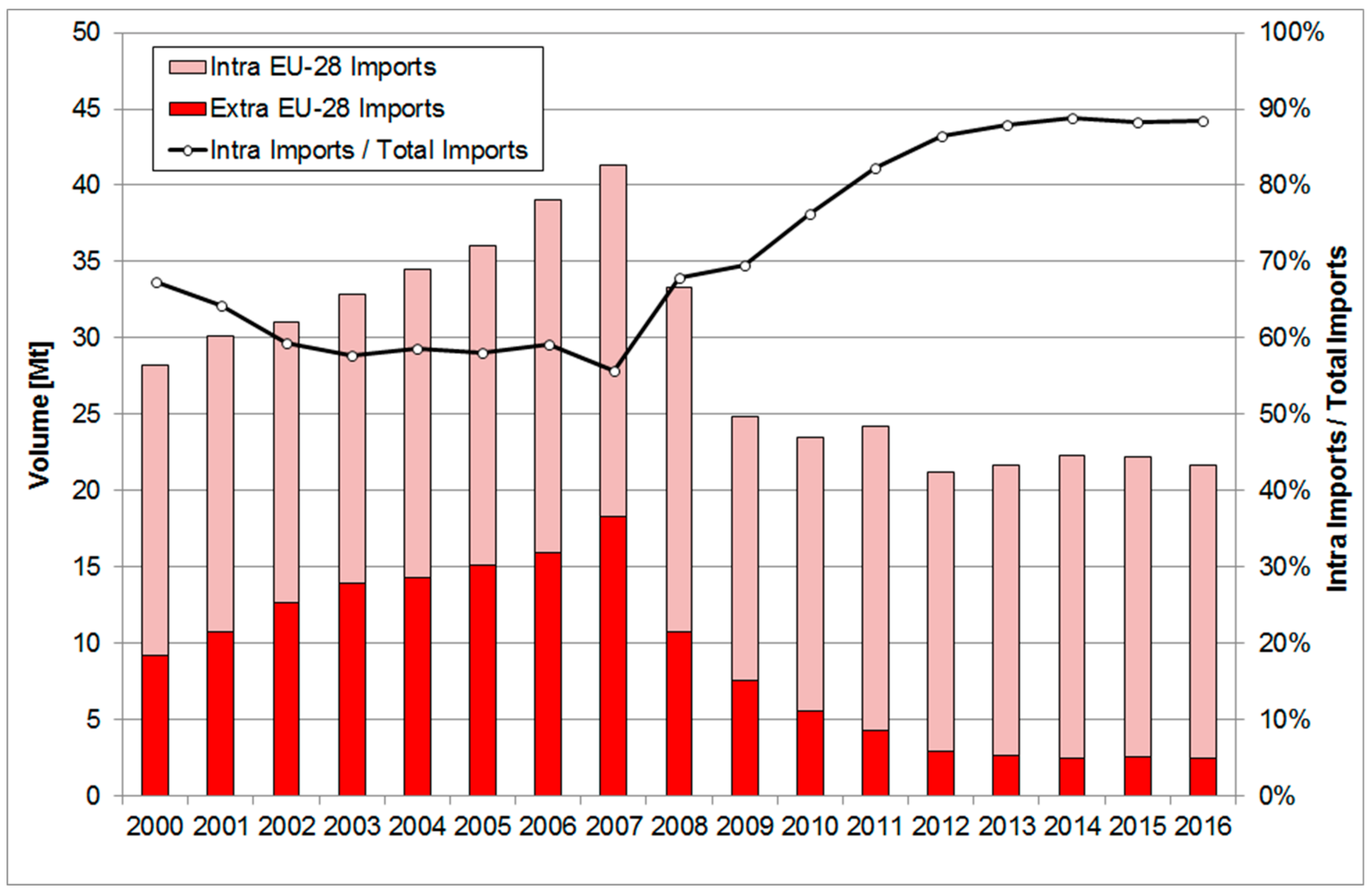

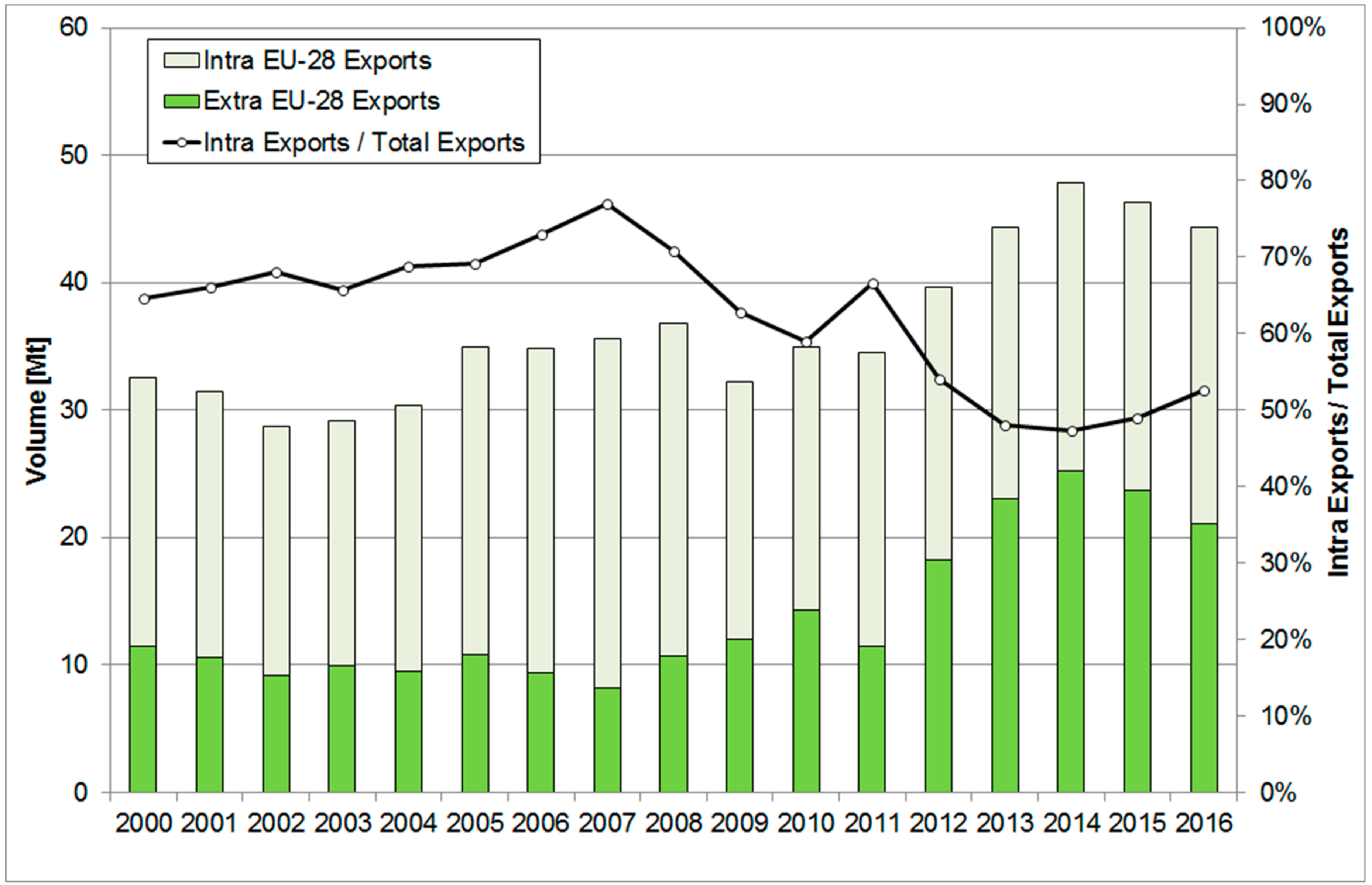

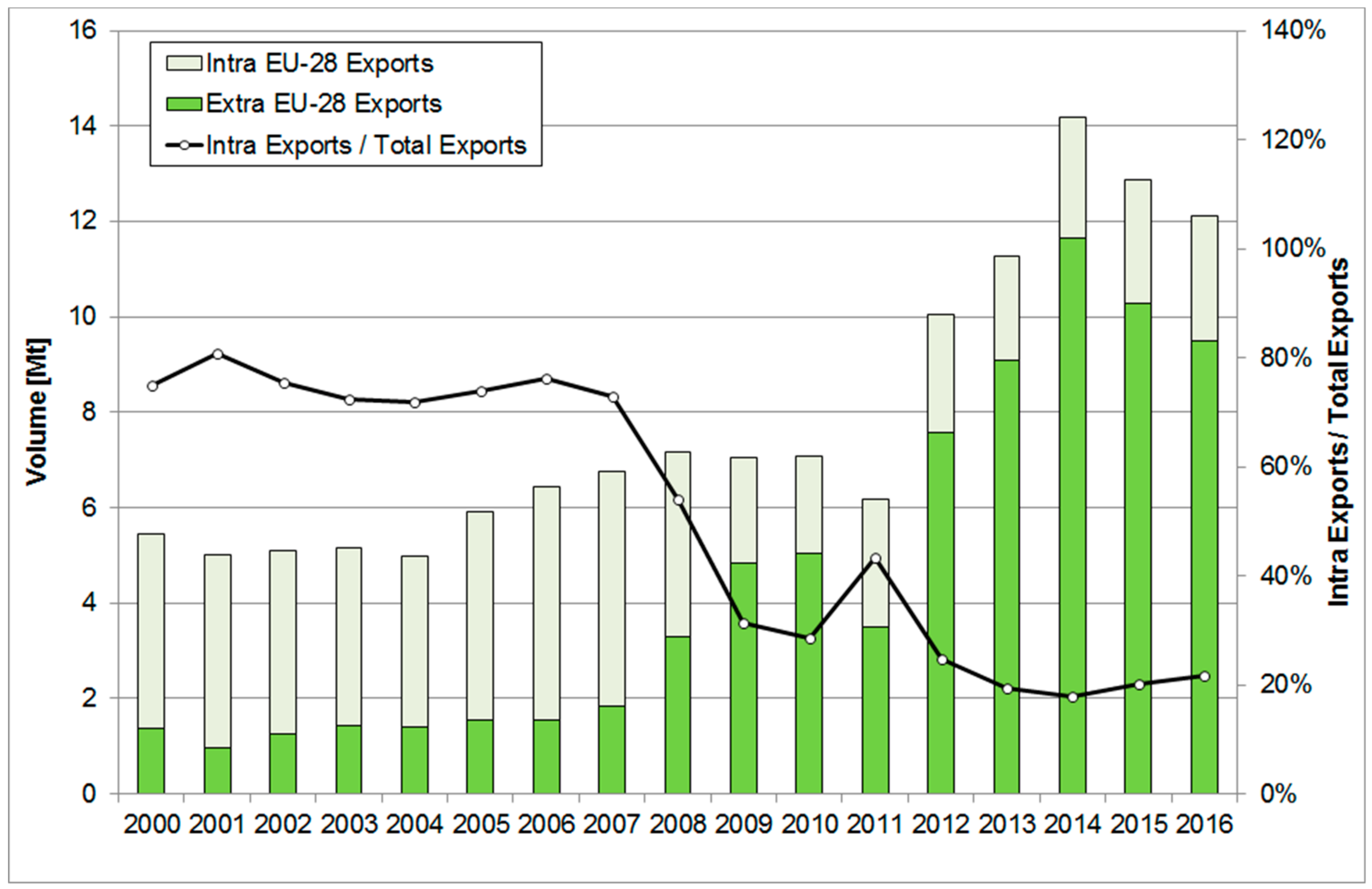

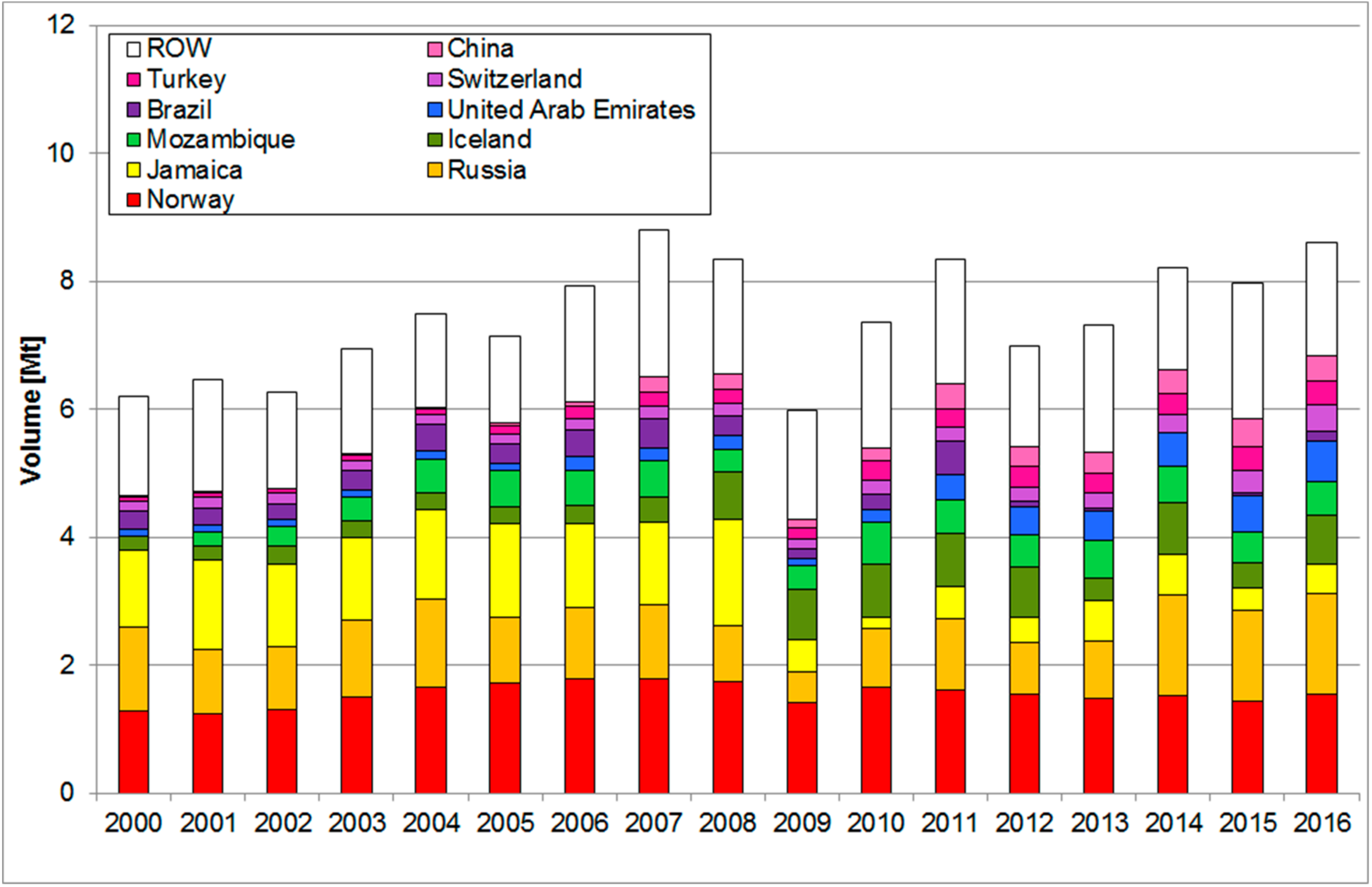

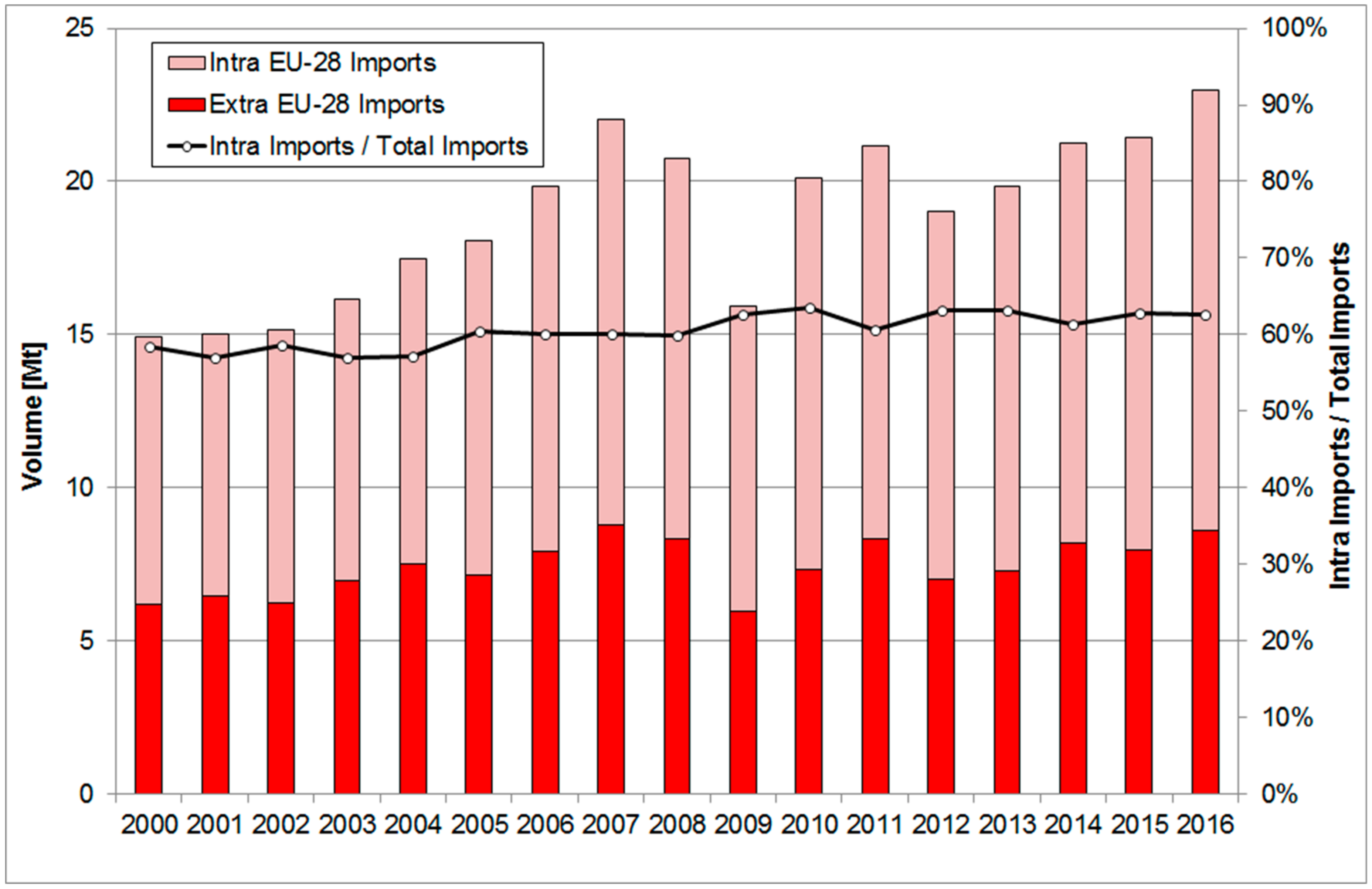

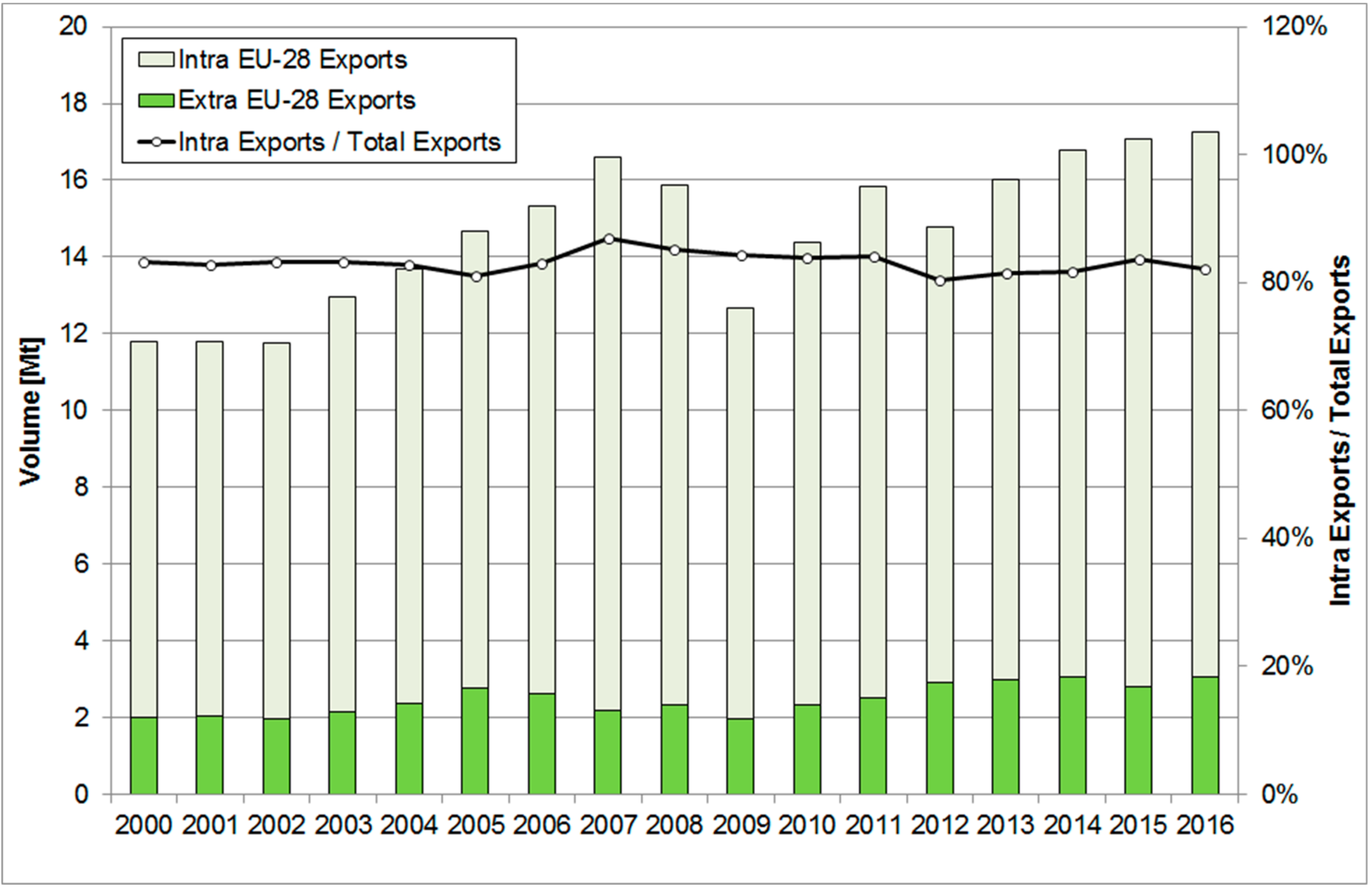

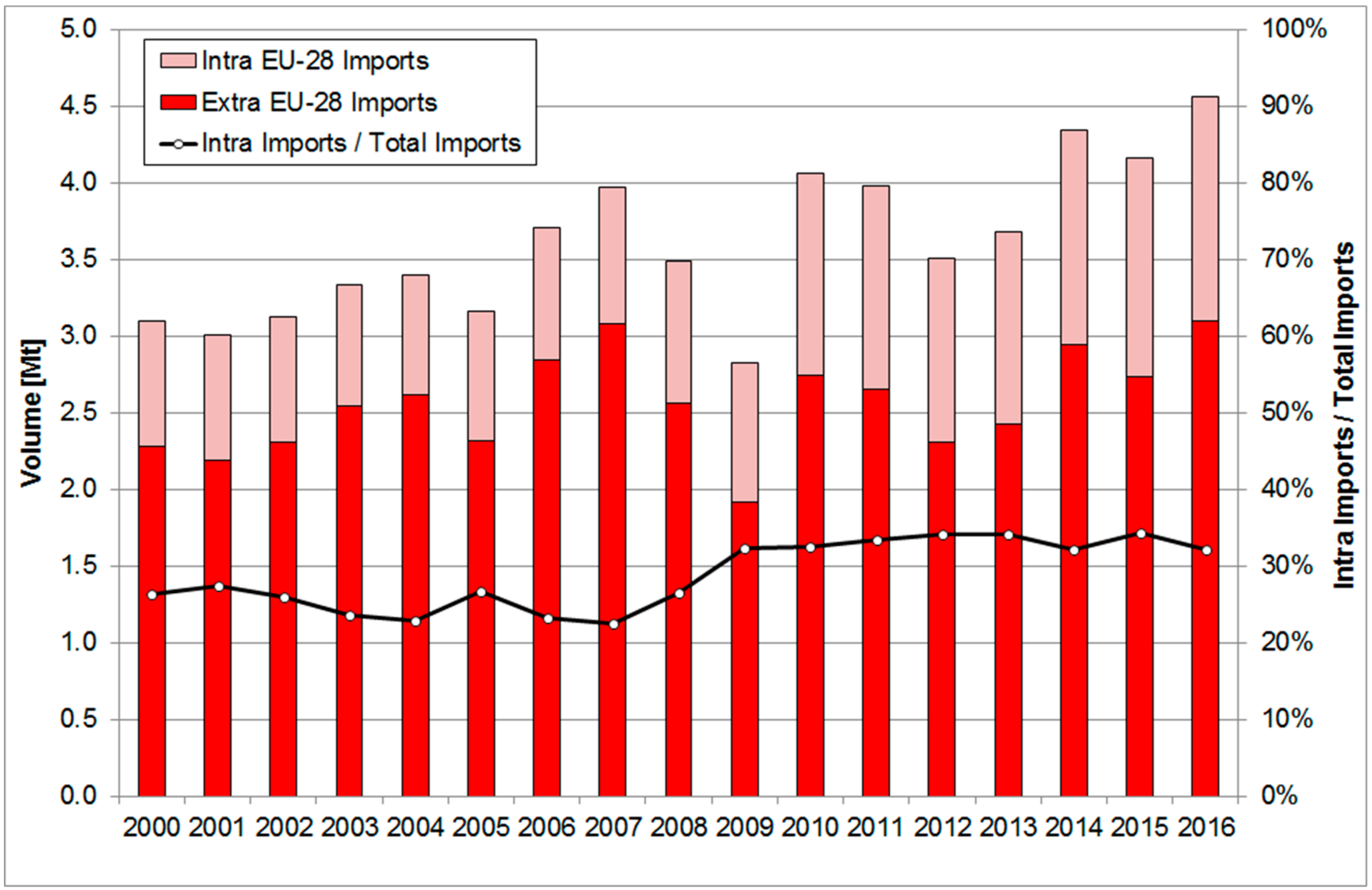

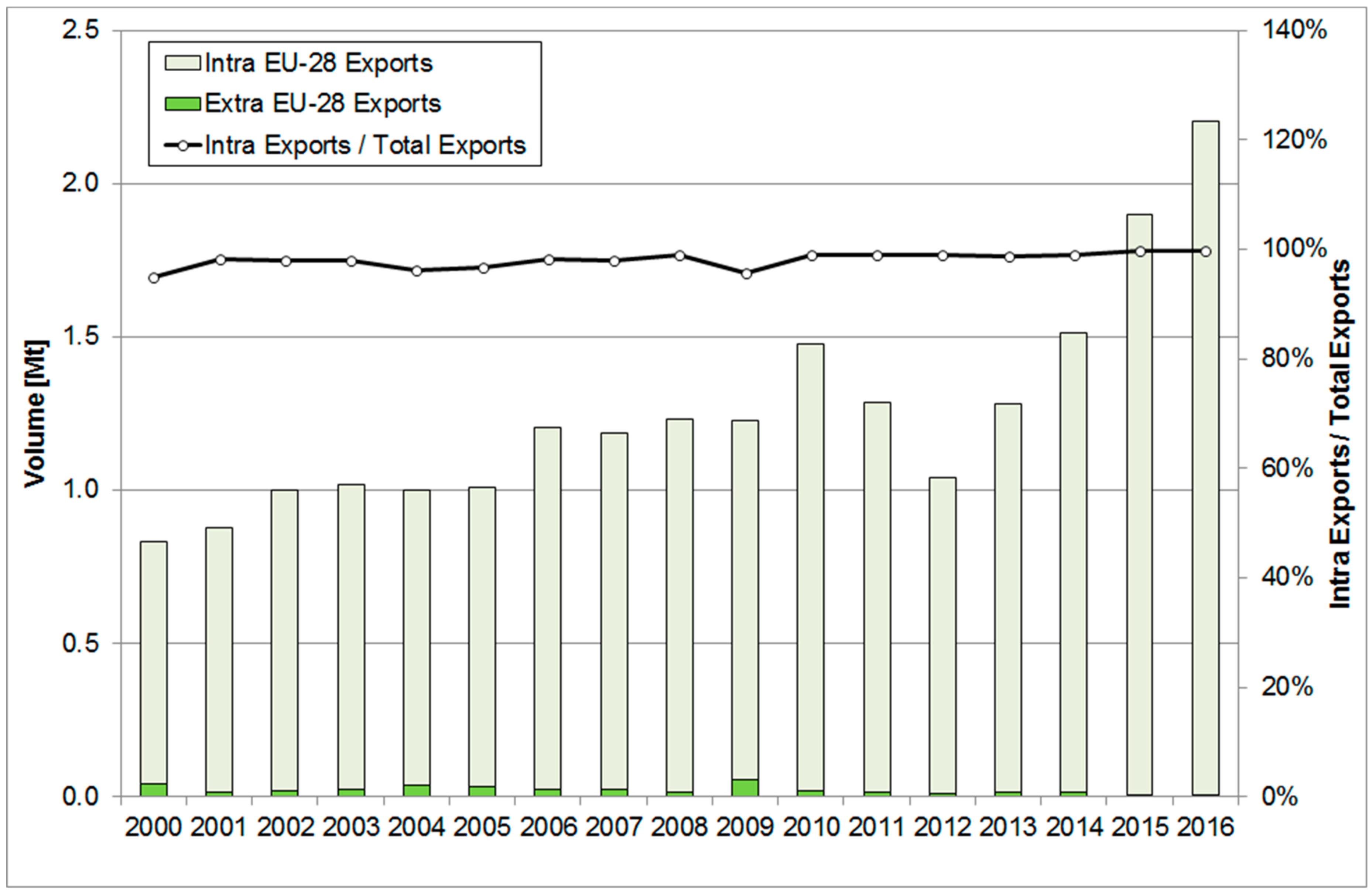

- COMEXT: provides statistics on the international trade of goods. This statistical information is collected from traders on the basis of Customs (extra-EU) and Intrastat (intra-EU) declarations. Products are disseminated according to the Combined Nomenclature (CN8), which first six digit codes coincide with the Harmonised Commodity Description and Coding System (HS), products are disseminated as well according to the Standard International Trade Classification (SITC) and the Broad Economic Categories (BEC) [16]. The datasets entitled, EU Trade Since 1988 By CPA_2008 and EU trade since 1988 by HS2, 4, 6 and CN8, provide information on both intra and extra EU-28 imports and exports at a four and eight digit level of product disaggregation. The datasets also provide information on the trade flows of both European cement and aluminium products with partner countries. In this second step, we identify the key export markets for the European cement and aluminium sectors that will then be further assessed qualitatively in the third step (based on additional country specific information) to determine whether any changes in trade can be linked to the effects of carbon leakage. The development of internal trade amongst EU Member States will also be considered by developing an indicator that tracks the share of internal EU-28 trade in relation to the total EU-28 trade for cement and aluminium products. This may provide further evidence of carbon leakage. For example, if the share of internal EU-28 imports declines, this may imply that the EU-28 is more dependent on imports from third countries (if domestic production does not increase).

- (3)

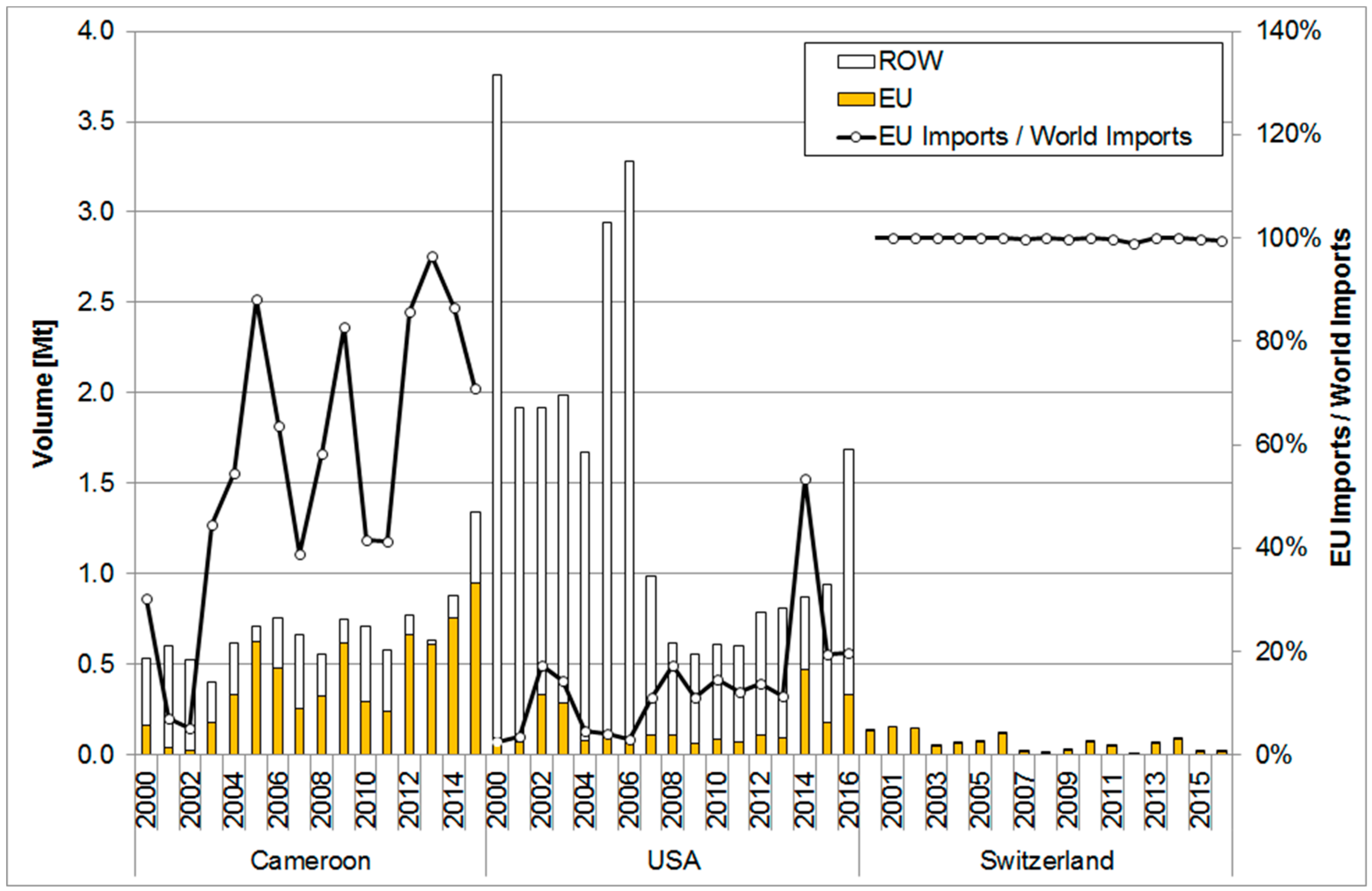

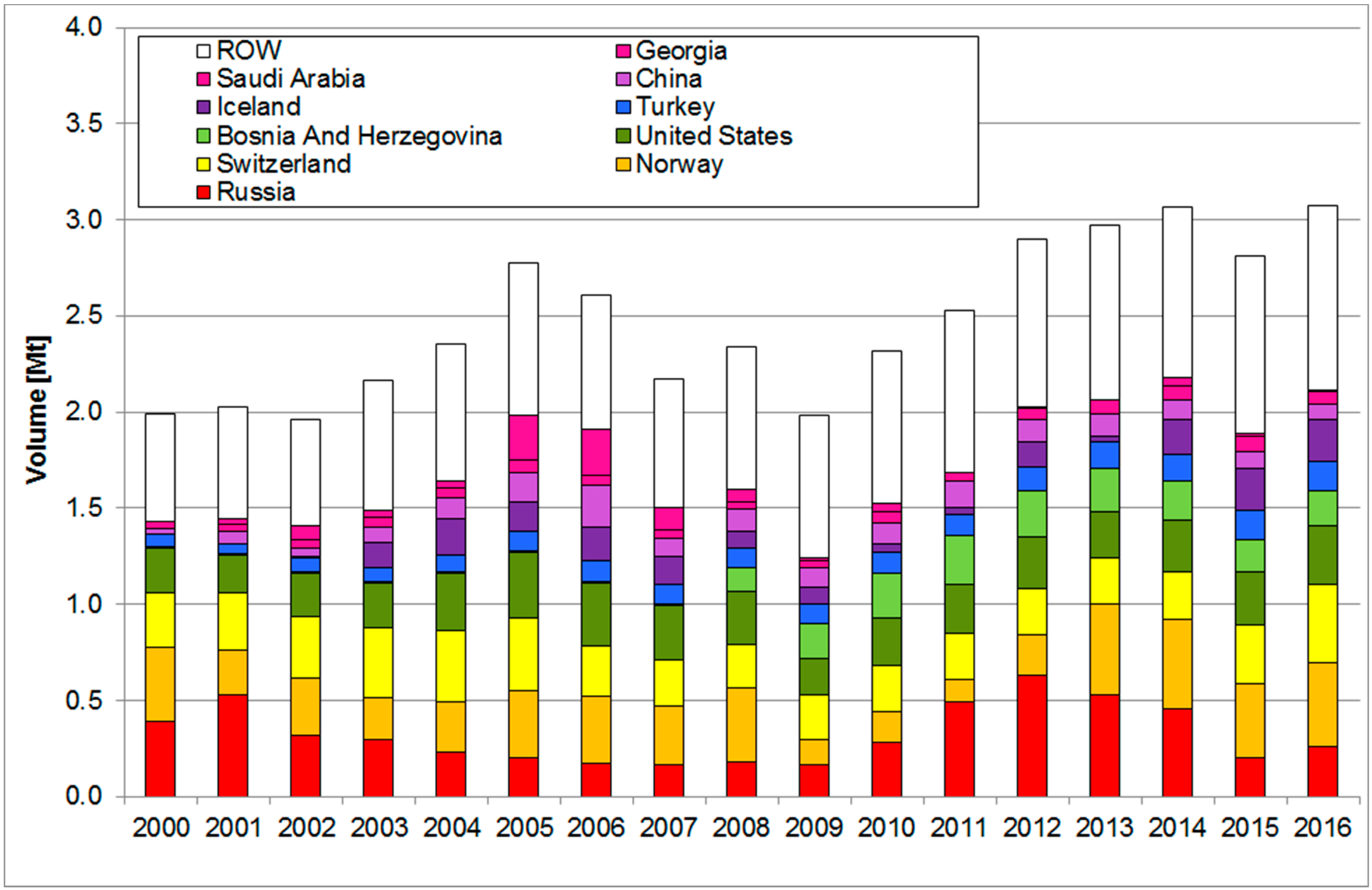

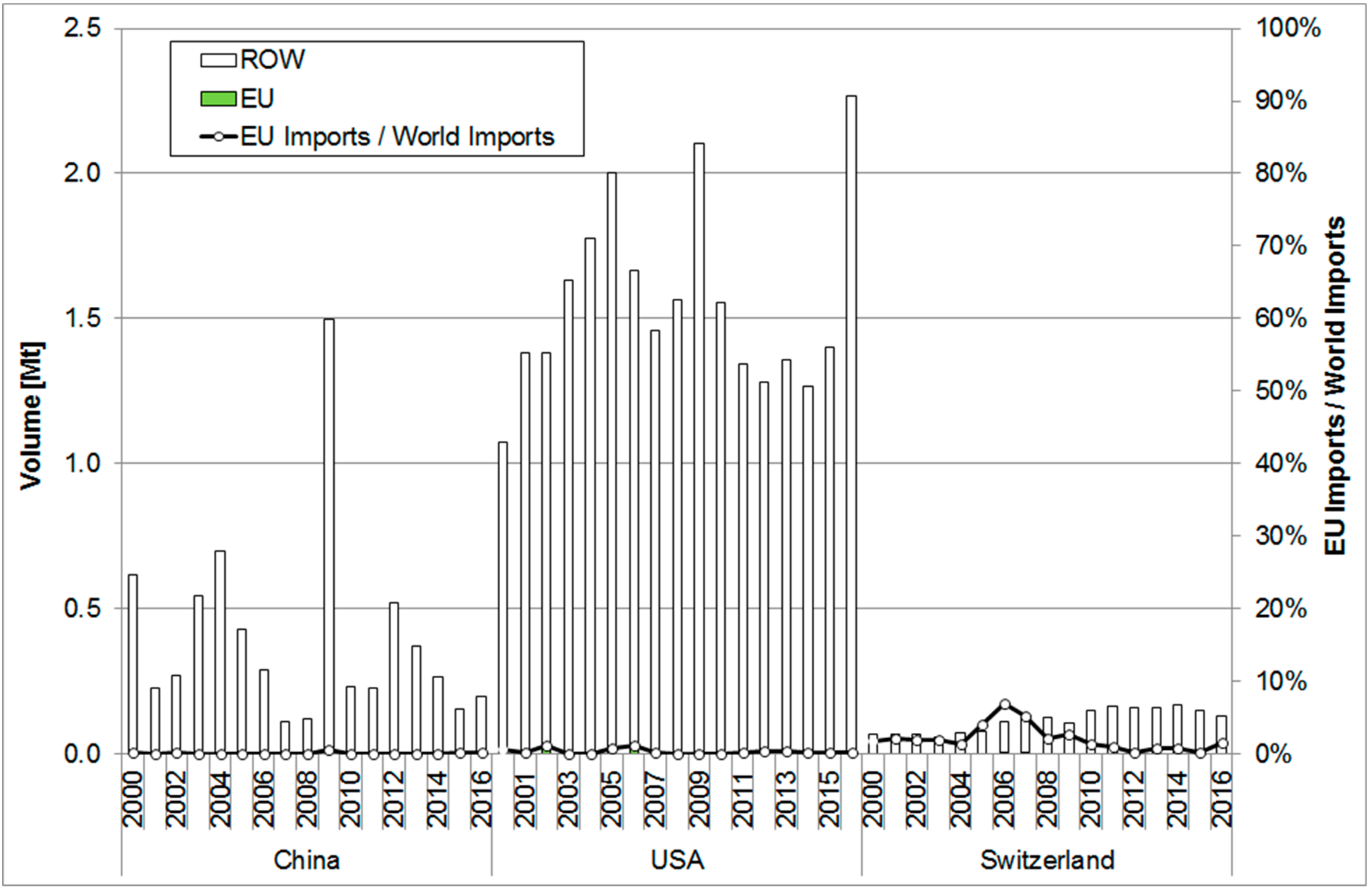

- United Nations Commodity Trade Statistics (UN COMTRADE): The dataset is the largest depository of international trade data and relies upon over 170 reporter countries/areas providing the UNSD (United Nations Statistics Division) with their annual international trade statistics data according to commodities/service categories and partner countries. Commodities are reported in the current classification and revision (HS 2012 in most cases as of 2016) [17]. The dataset complements the other datasets in this final step by providing information on the trade flows of third countries, which is used to assess the imports of the third countries that were previously identified as key EU-28 export markets for the European cement and aluminium sectors. The identification of such third countries furthers any discussion on carbon leakage as it is possible to track how the share of EU imports in these key markets changes over time and to put forward reasons for why other countries may be more competitive (i.e., geographical proximity, competitive production costs) and whether or not similar environmental policies are implemented in these third countries. However, changes in trade patterns before and after the introduction of the EU ETS may occur for many longer term reasons (i.e., loss/gain in competitiveness independent from carbon markets) and shorter term reasons (i.e., economic cycles in different parts of the world resulting in different levels of capacity utilisation).

3. Results

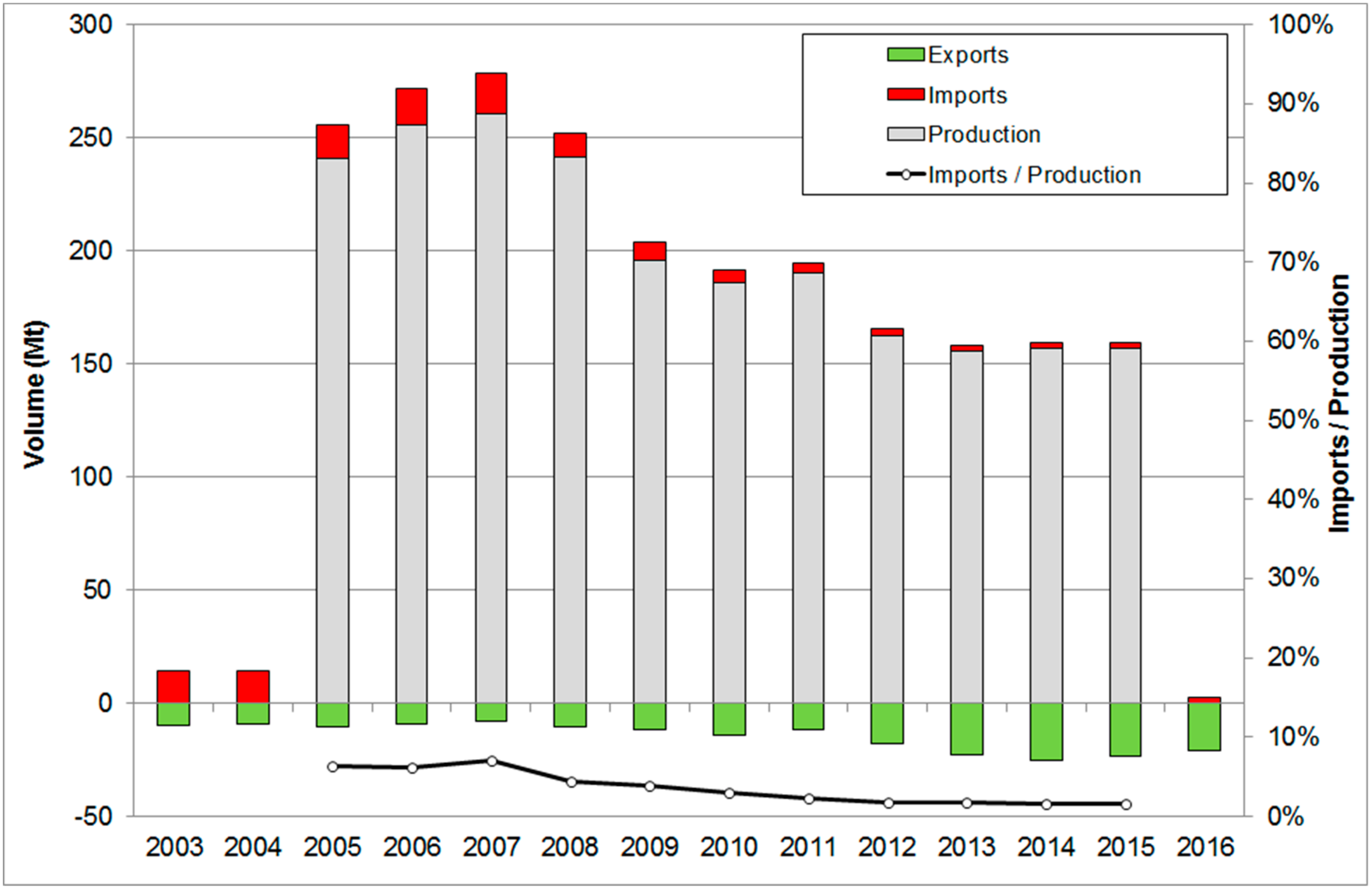

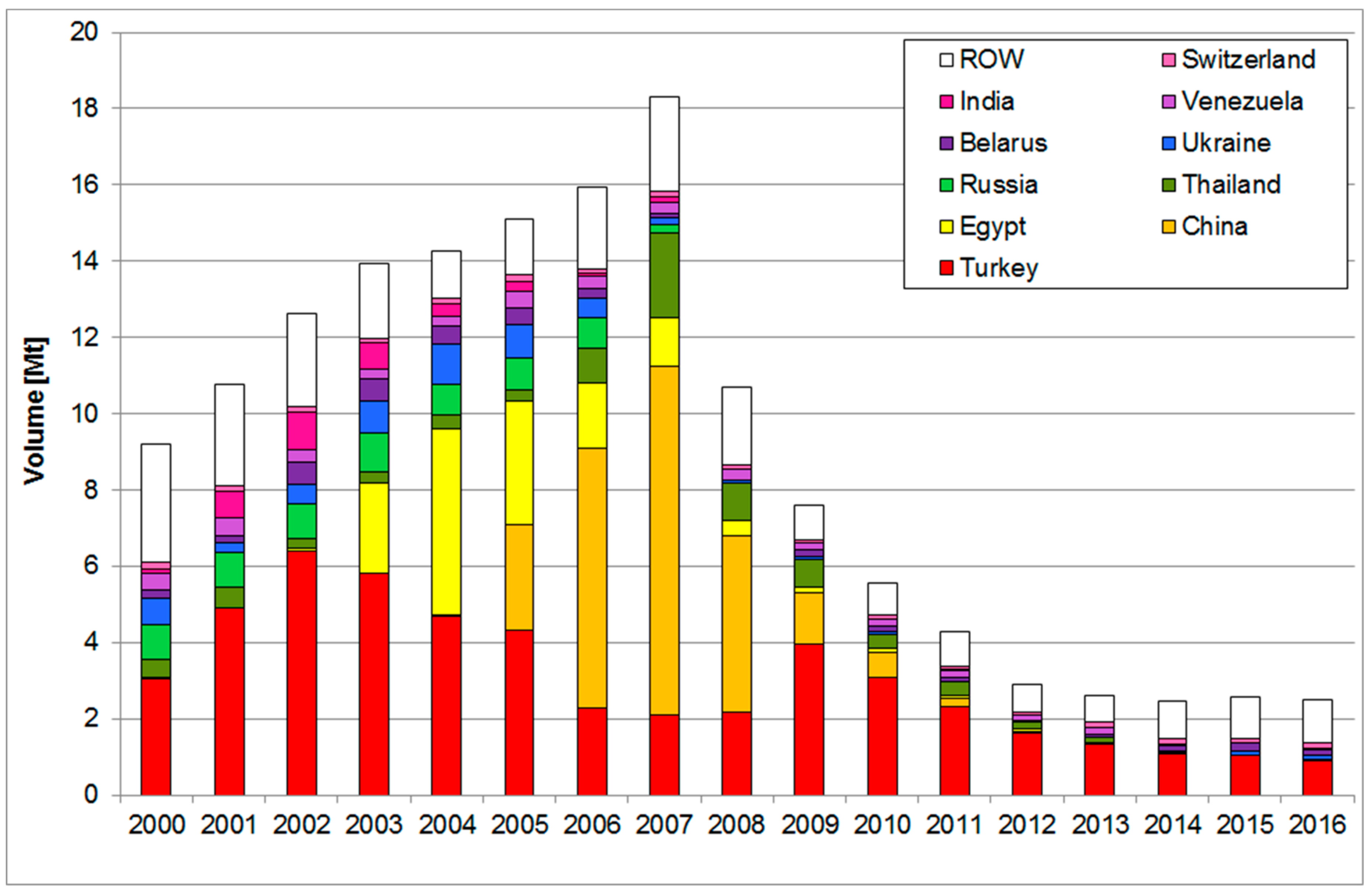

3.1. Cement

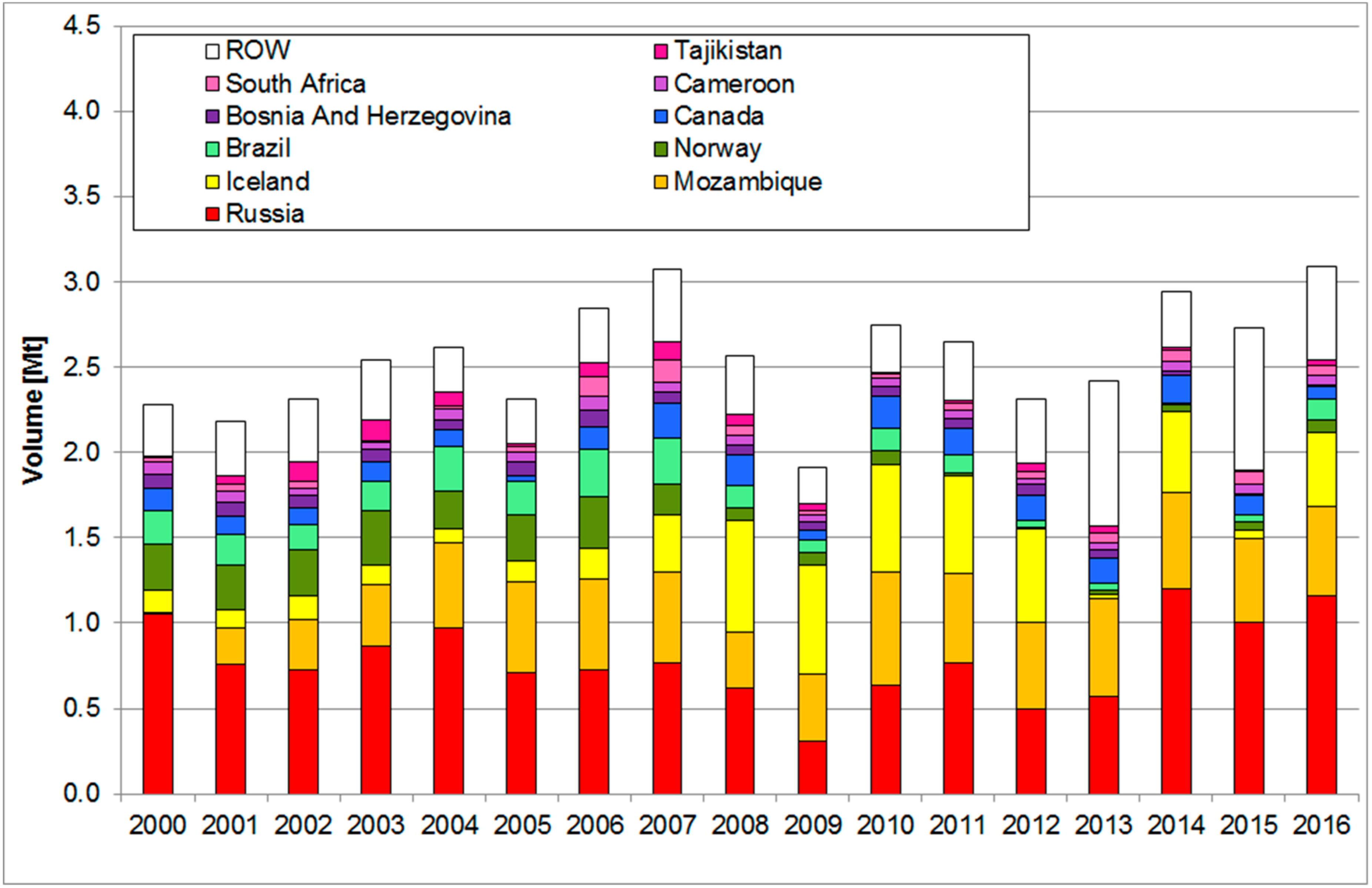

3.2. Cement Clinker

3.3. Aluminium

3.4. Unwrought Non-Alloyed Aluminium

4. Discussion

Author Contributions

Acknowledgments

Conflicts of Interest

References

- European Commission. Carbon Leakage. 2018. Available online: https://ec.europa.eu/clima/policies/ets/allowances/leakage_en (accessed on 10 February 2018).

- Xin, W.; Fei, T.; Shaojie, Z.; Bofeng, C. Identifying the industrial sectors at risk of carbon leakage in China. Clim. Policy 2017, 4, 443–457. [Google Scholar]

- Roy, J.; Ghosh, D.; Ghosh, S. Leakage Risks in South Korea: Potential Impacts on Global Emissions. Climate Strategies. 2017. Available online: http://climatestrategies.org/wp-content/uploads/2014/10/CS-Roy-et-al.-Policy-Paper-3-Rev.-3-format.pdf (accessed on 10 February 2018).

- Xin, W.; Fei, T.; Gehua, W.; Shaojie, Z.; Bofeng, C. Carbon leakage scrutiny in ETS and non-ETS industrial sectors in China. Resour. Conserv. Recycl. 2018, 129, 424–431. [Google Scholar]

- Marcu, A.; Egenhofer, C.; Roth, S.; Stoefs, W. Carbon Leakage: An Overview. CEPS. 2013. Available online: https://www.ceps.eu/system/files/Special Report No 79 Carbon Leakage_0.pdf (accessed on 10 February 2018).

- Bolscher, H.; Graichen, V.; Hay, G.; Healy, S.; Lenstra, J.; Meindert, L.; Regeczi, D.; von Schickfus, M.; Schumacher, K.; Timmons-Smakman, F. Carbon Leakage Evidence Project: Factsheets for Selected Sectors. 2013. Available online: https://ec.europa.eu/clima/sites/clima/files/ets/allowances/leakage/docs/cl_evidence_factsheets_en.pdf (accessed on 10 February 2018).

- Helene, N.; Aleksandar, Z. Does the EU ETS Cause Carbon Leakage in European Manufacturing? DIW Berlin. 2017. Available online: https://www.diw.de/documents/publikationen/73/diw_01.c.565609.de/dp1689.pdf (accessed on 13 April 2018).

- Branger, F.; Sato, M. Solving the clinker dilemma with hybrid output-based allocation. Clim. Chang. 2017, 140, 483–501. [Google Scholar] [CrossRef]

- Moya, J.; Boulamanti, A. Production Costs from Energy-Intensive Industries in the EU and Third Countries. 2016. Available online: http://publications.jrc.ec.europa.eu/repository/bitstream/JRC100101/ldna27729enn.pdf (accessed on 10 February 2018).

- Zhou, H.; Sheng, J. Has EU ETS caused carbon leakage in the EU carbon-intensive industries? A study from the perspective of bilateral trade. Chin. J. Popul. Resour. Environ. 2015, 13, 132–138. [Google Scholar] [CrossRef]

- Boutabba, M.A.; Lardic, S. EU Emissions trading scheme, competitiveness and carbon leakage: New evidence from cement and steel industries. Ann. Oper. Res. 2017, 255, 47–61. [Google Scholar] [CrossRef]

- Sartor, O. Carbon Leakage in the Primary Aluminium Sector: What Evidence after 6½ Years of the EU ETS? 2012. Available online: https://www.i4ce.org/download/carbon-leakage-in-the-primary-aluminium-sector-what-evidence-after-6-%C2%BD-years-of-the-eu-ets-2/ (accessed on 10 April 2018).

- Amine, B.M.; Sandrine, L. Does European Primary Aluminum Sector Is Exposed to Carbon Leakage? New Insights from Rolling Analysis. Econ. Bull. 2017, 37, 614–618. [Google Scholar]

- Eurostat. Statistics on the Production of Manufactured Goods (prom). 2018. Available online: http://ec.europa.eu/eurostat/cache/metadata/EN/prom_esms.htm (accessed on 10 April 2018).

- European Commission. Guidance Document no 9 on the Harmonized Free Allocation Methodology for the EU-ETS Post 2012. 2011. Available online: https://ec.europa.eu/clima/sites/clima/files/ets/allowances/docs/gd9_sector_specific_guidance_en.pdf (accessed on 14 April 2018).

- Eurostat. International Trade (ei_et). 2018. Available online: http://ec.europa.eu/eurostat/cache/metadata/EN/ei_et_esms.htm (accessed on 10 April 2018).

- UN Trade Statistics. What is UN Comtrade? 2017. Available online: https://unstats.un.org/unsd/tradekb/Knowledgebase/50075/What-is-UN-Comtrade (accessed on 10 April 2018).

- Eurostat. Sold Production, Exports and Imports by PRODCOM List (NACE Rev. 2)—Annual Data. 2018. Available online: http://ec.europa.eu/eurostat/web/prodcom/data/database (accessed on 10 April 2018).

- WBCSD Cement. GNR Project. 2015. Available online: http://www.wbcsdcement.org/GNR-2015/index.html (accessed on 10 April 2018).

- Cook, G. Investment, Carbon Pricing and Leakage: A Cement Sector Perspective. 2011. Available online: http://climatestrategies.org/wp-content/uploads/2011/09/cs-investment-carbon-pricing-leakage-cement-sector-perspective-cook.pdf (accessed on 10 February 2018).

- COMEXT. EU Trade Since 1988 By CPA_2008. Available online: http://epp.eurostat.ec.europa.eu/newxtweb/ (accessed on 10 April 2018).

- Global Cement. PPC to Enter Algeria. Available online: http://www.globalcement.com/news/item/2310-ppc-to-enter-algeria (accessed on 10 April 18).

- UN COMTRADE. UN COMTRADE Database. 2018. Available online: https://comtrade.un.org/data (accessed on 10 April 2018).

- COMEXT. EU Trade Since 1988 by HS2, 4, 6 and CN8. 2008. Available online: http://epp.eurostat.ec.europa.eu/newxtweb/ (accessed on 10 April 2018).

- Branger, F.; Ponssard, J.-P.; Sartor, O.; Sato, M. EU ETS, Free Allocations, and Activity Level Thresholds: The Devil Lies in the Details. J. Assoc. Environ. Resour. Econ. 2015, 2, 401–437. [Google Scholar] [CrossRef]

- Byiers, B.; Karaki, K.; Vanheukelo, J. Regional Markets, Politics and Value Chains: The Case of West African Cement. 2017. Available online: http://ecdpm.org/wp-content/uploads/DP216-Cement-Byiers-Karaki-Vanheukelom-September-2017.pdf (accessed on 14 April 2018).

- United States International Trade Commission. Aluminum: Competitive Conditions Affecting the U.S. Industry. 2017. Available online: https://www.usitc.gov/publications/332/pub4703.pdf (accessed on 10 April 2018).

- Marcu, A.; Stoefs, W.; Tuokko, K.; Egenhofer, C.; Renda, A.; Simonelli, F.; Genoese, F.; Storti, E.; Drabik, E.; Hähl, T.; et al. Composition and Drivers of Energy Prices and Costs: Case Studies in Selected Energy-intensive Industries: Final Report. 2016. Available online: https://www.ceps.eu/publications/composition-and-drivers-energy-prices-and-costs-case-studies-selected-energy-intensive (accessed on 15 April 2018).

- European Commission. Energy Prices and Costs in Europe: SWD(2016) 420 Final. 2016. Available online: https://ec.europa.eu/energy/sites/ener/files/documents/com_2016_769.en_.pdf (accessed on 10 April 2018).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | Change | |

| PRODCOM (Extra EU-28 Imports/Production) | ||||||||||||||||||

| Cement | 6% | 6% | 7% | 4% | 4% | 3% | 2% | 2% | 2% | 2% | 2% | −4.6% | ||||||

| Clinker | 6% | 7% | 8% | 5% | 3% | 2% | 1% | 1% | 1% | 1% | 1% | −4.9% | ||||||

| Aluminium * | 32% | 35% | 37% | 33% | 34% | 36% | 33% | 36% | 38% | 36% | 38% | 5.6% | ||||||

| Unwrought ** | 380% | 373% | 339% | 335% | 413% | 341% | 330% | 336% | 487% | 487% | 613% | 232.8% | ||||||

| COMEXT (Intra EU-28 Imports/Total EU-28 Imports) | ||||||||||||||||||

| Cement | 67% | 64% | 59% | 58% | 59% | 58% | 59% | 56% | 68% | 69% | 76% | 82% | 86% | 88% | 89% | 88% | 88% | 21.1% |

| Clinker | 43% | 42% | 36% | 38% | 36% | 30% | 28% | 23% | 33% | 37% | 52% | 61% | 71% | 73% | 81% | 76% | 78% | 35.2% |

| Aluminium * | 58% | 57% | 59% | 57% | 57% | 60% | 60% | 60% | 60% | 63% | 63% | 61% | 63% | 63% | 61% | 63% | 63% | 4.1% |

| Unwrought ** | 26% | 27% | 26% | 24% | 23% | 27% | 23% | 23% | 26% | 32% | 32% | 33% | 34% | 34% | 32% | 34% | 32% | 5.9% |

| UN COMTRADE (EU share of import volume of its main export markets) | ||||||||||||||||||

| Cement Products | ||||||||||||||||||

| Algeria | 52% | 46% | 42% | 39% | 23% | 20% | 27% | 33% | 32% | 32% | 52% | 64% | 89% | 87% | 77% | 73% | 69% | 17.0% |

| USA | 18% | 17% | 17% | 13% | 16% | 15% | 11% | 7% | 6% | 7% | 8% | 6% | 16% | 17% | 25% | 30% | 11.5% | |

| Switzerland | 99% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 99% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 0.7% |

| Cement Clinker | ||||||||||||||||||

| Cameroon | 30% | 7% | 5% | 44% | 54% | 88% | 64% | 39% | 58% | 83% | 42% | 41% | 86% | 97% | 87% | 71% | 40.8% | |

| USA | 3% | 4% | 17% | 14% | 5% | 4% | 3% | 11% | 17% | 11% | 15% | 12% | 14% | 11% | 54% | 19% | 20% | 17.3% |

| Switzerland | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 99% | 100% | 100% | 100% | 99% | −0.6% |

| Aluminium Products | ||||||||||||||||||

| China | 3% | 2% | 1% | 1% | 11% | 3% | 4% | 2% | 3% | 2% | 3% | 4% | 2% | 3% | 2% | 2% | 3% | 0.1% |

| USA | 4% | 4% | 5% | 5% | 6% | 6% | 7% | 6% | 4% | 5% | 6% | 6% | 6% | 5% | 5% | 5% | 5% | 0.9% |

| Switzerland | 70% | 70% | 72% | 72% | 70% | 73% | 59% | 56% | 57% | 58% | 53% | 52% | 53% | 54% | 54% | 61% | 67% | −2.5% |

| Unwrought Non-Alloyed Aluminium | ||||||||||||||||||

| China | 0% | 0% | 0% | 0% | 0% | 0% | 0% | 0% | 0% | 1% | 0% | 0% | 0% | 0% | 0% | 0% | 0% | 0.0% |

| USA | 1% | 0% | 1% | 0% | 0% | 1% | 1% | 0% | 0% | 0% | 0% | 0% | 0% | 0% | 0% | 0% | 0% | −0.4% |

| Switzerland | 2% | 2% | 2% | 2% | 1% | 4% | 7% | 5% | 2% | 3% | 1% | 1% | 0% | 1% | 1% | 0% | 2% | −0.2% |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Healy, S.; Schumacher, K.; Eichhammer, W. Analysis of Carbon Leakage under Phase III of the EU Emissions Trading System: Trading Patterns in the Cement and Aluminium Sectors. Energies 2018, 11, 1231. https://doi.org/10.3390/en11051231

Healy S, Schumacher K, Eichhammer W. Analysis of Carbon Leakage under Phase III of the EU Emissions Trading System: Trading Patterns in the Cement and Aluminium Sectors. Energies. 2018; 11(5):1231. https://doi.org/10.3390/en11051231

Chicago/Turabian StyleHealy, Sean, Katja Schumacher, and Wolfgang Eichhammer. 2018. "Analysis of Carbon Leakage under Phase III of the EU Emissions Trading System: Trading Patterns in the Cement and Aluminium Sectors" Energies 11, no. 5: 1231. https://doi.org/10.3390/en11051231

APA StyleHealy, S., Schumacher, K., & Eichhammer, W. (2018). Analysis of Carbon Leakage under Phase III of the EU Emissions Trading System: Trading Patterns in the Cement and Aluminium Sectors. Energies, 11(5), 1231. https://doi.org/10.3390/en11051231