Management of an oil well has some real options at hand. As usual, maximizing the value of the oil well requires to optimally exercise these options. Among them we can identify: (a) the option to develop an undeveloped oil well; (b) the option to complete a developed but uncompleted well; (c) the option to temporarily shut down a producing well that turns unprofitable (in principle this involves the possibility to restart operations at some time in the future under the “right” conditions); (d) the option to definitely abandon an unprofitable producing well.

Right now, with crude oil prices at relatively low levels, all of these options do not seem equally alluring (recent agreements by OPEC and its allies to cut production notwithstanding). We aim to explore the most relevant ones in this scenario, namely the delay option and the abandonment option. The former clearly refers to the possibility to defer investment up to a pre-specified date in the future (the option maturity); in our case, whenever the investment happens to be undertaken the oil producer will be able to exploit the well over the following 10 years at most (the well’s expected useful lifetime). Indeed, although long-term fundamentals of oil look attractive, [

24] reckons that exploration and production firms are taking a wait-and-see approach. The ultimate purpose when assessing the option to defer investment is to determine the optimal time to invest. Following [

6], we assume that the decision to defer has no impact on the resource’s depletion pattern (which is fixed). Upon investment, production continues without any interruption; this looks reasonable since most of the available reserves are depleted during the first two years of operation. For simplicity, we also assume that the investment outlay takes place by means of an instantaneous lump-sum expense; this way the owner of an undeveloped reserve receives the developed reserve immediately after that start of development; Reference [

25] similarly does not take time-to-build into account. In [

26] instead, the facility (an offshore oil platform) takes one year to complete since the initial disbursement; from then on, available reserves can be extracted over 15 years.

The option to delay encompasses several circumstances. For one, the model can be applied to the case in which no capital expenditure has been made and the option holder can turn an undeveloped oil well into a completed one. Similarly, a fraction of the capital expenditures may have been made to develop the well but it is still uncompleted. In both cases full completion requires some (additional) fixed costs to be paid up. Needless to say, the particular level of the unit cost (including variable cost) would be different in each case, depending on the development costs already incurred. The model could also be applied in principle when the option holder has closed the well early and suddenly wants to re-open it up again. Note, however, that this possibility seems unlikely since most of the reserves are taken from the ground during a short time span and the cost (including reopening costs) could be pretty high. In sum, these three possibilities fall be more or less within the realm of the option de delay investment. This said, upon investment oil production is assumed to take place without any interruption or abandonment. This seems reasonable because most reserves are taken from the ground during the first two years; we can think of this as selling future production at the time of investment in the futures market. In what follows we assess this option along with the option to abandon the producing well.

For this purpose we use Monte Carlo simulation below. Specifically, we simulate 200,000 random paths. In our discrete-time approximation we adopt time steps of length

, i.e., almost weekly steps. Since the investment/abandonment horizon is 5 years, each simulation path comprises 250 steps; Reference [

26] takes the same 5-year period since the beginning of the offshore oil project until the last date at which the platform can be installed. As further explained in [

12], we calculate the corresponding spot prices, long-term prices and volatilities using the following discrete-time scheme:

where

,

and

are independent and identically distributed samples from a univariate N (0, 1) distribution. Equations (13)–(15) follow a general method to obtain correlated random samples

ν1,

ν2 and

ν3:

Correlation coefficients as estimated in

Table 1 are used throughout.

5.1. Valuation and Management of the Option to Delay

The time series simulated for and allow compute at any time the (unit) npv of an investment at that time as the difference between the PV of the (unit) income and the one of the cost (the sum of whatever fixed cost is pending and the variable cost); see Equation (12). We also have the time series of volatility along each path. We consider an American-type call option with T = 5 years to maturity. We stick to a producing well with 10 years of expected useful lifetime since its inception. It is possible to invest at any time before the option expiration, so the optimal exercise time is the one that maximizes the option value.

As a previous step to the valuation itself it makes sense to check the goodness of the simulation as such. One way to do it is by comparing the average values (over the 200,000 runs) of the three state variables at the option maturity (

= 5) with their earlier numerical estimates. According to our results, the average spot price is

= 49.29

$/bbl; this figure is fairly close to the price 49.33

$/barrel derived from Equation (6) above. Regarding the long-term level,

, the average value at

= 5 is 49.95

$/bbl, which is also very close to the price 49.94

$/bbl estimated before (see

Table 1). As for the volatility, the average value of

is 0.3526; our earlier estimate was 0.3529 (

Table 1). These results attest to the overall goodness of fit of our simulation.

Given the values of

at any time t (with

≤

= 5) along each path, the Least Squares Monte Carlo (LSMC) approach is used [

9]. At the option expiration

) the value of the investment opportunity

, in each path is the maximum of two numbers, namely the value of exercising the option and zero (because the option contract entails a right, not an obligation; should the payoff be negative the holder would simply leave the option expire unexercised):

The optimal strategy is to exercise the option if it is in-the-money:

.

At earlier times, the same payoff structure remains. A noticeable difference is, of course, that leaving the option unexercised means keeping it alive for one more period, in which case the payoff is no longer zero but the (expected) value of the option next period. The option must be exercised only if exercising immediately is more valuable than the expected cash flows from continuing (i.e., the value of keeping on waiting to invest). This comparison clearly calls for identifying the conditional expected value of continuation in the first place. Since the continuation value depends on expectations about future events, it must be computed by backward induction: one must proceed from some known future value (e.g., at the option maturity) back to the present. Reference [

9] uses the cross-sectional information in the simulated paths to identify the conditional expectation function (see also [

27]). Specifically, they regress the subsequent realized cash flows from continuation on a set of basis functions of the state variables:

At any time, considering those paths that are in-the-money and applying ordinary least squares we can get numerical estimates of the coefficients

. Hence it is possible to estimate the “continuation value” at each step from the state variables at that step. Thus before expiration the investment opportunity is worth:

Proceeding backwards, at the initial date we get the time-0 option value (together with the optimal exercise pattern all the way through expiration) for that particular random sample:

Then we calculate the average option value across all random samples.

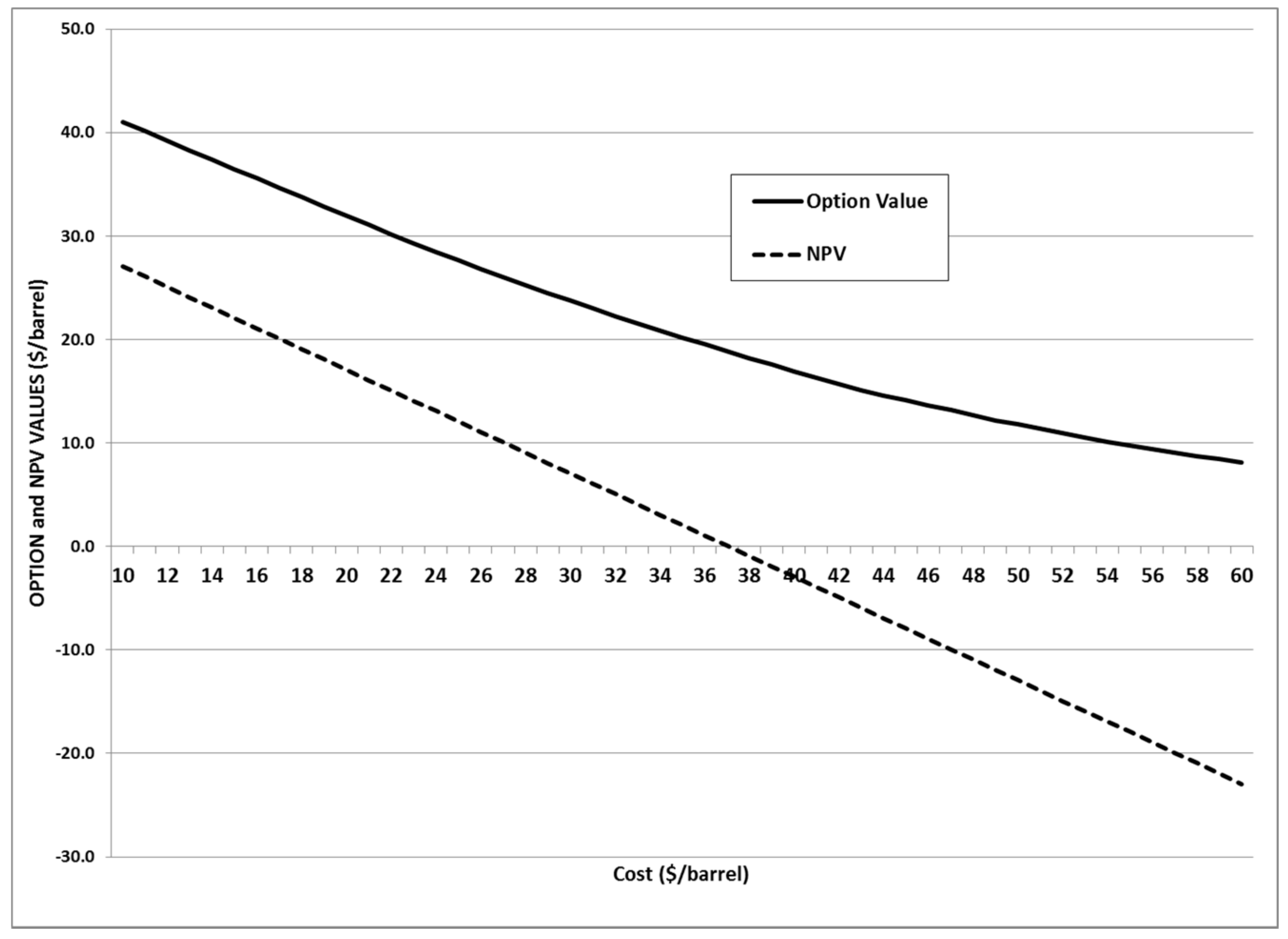

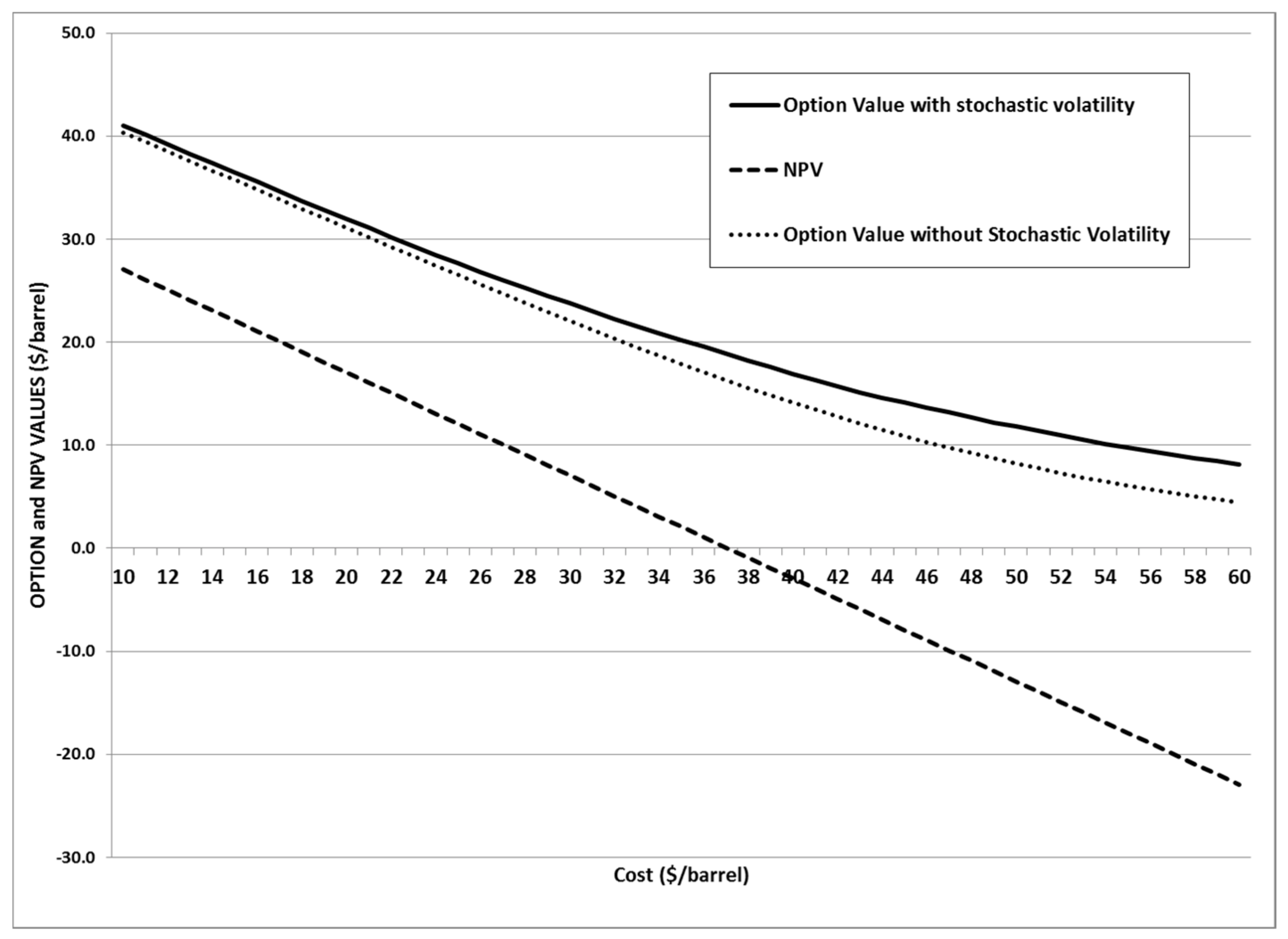

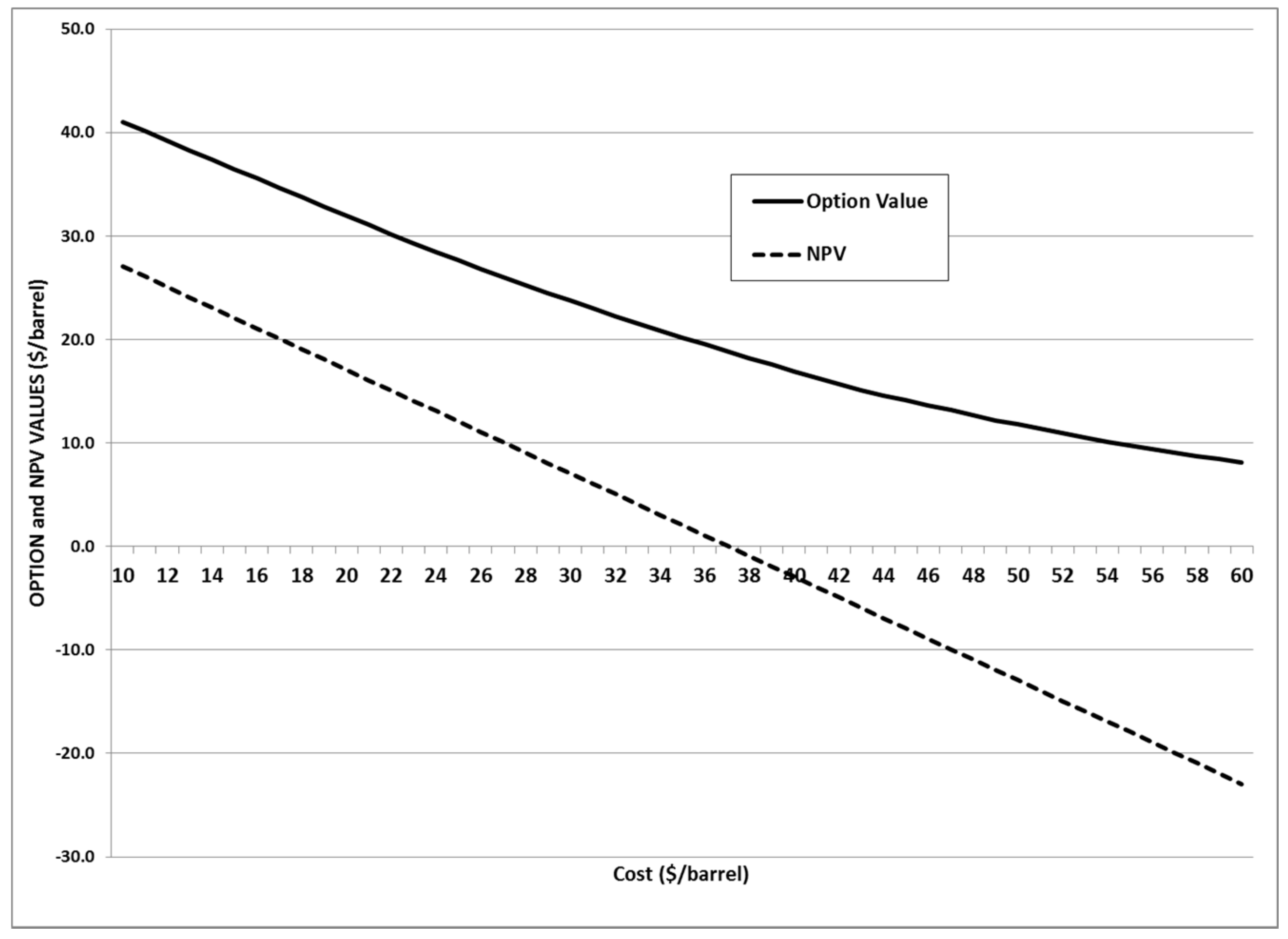

Figure 1 shows the net present value and the option value as decreasing functions of the cost of producing a barrel of oil

. The npv, i.e., the value of investing immediately, can be either positive or negative depending on the level of

. Instead, the value of the option to invest now or later (if at all) is bounded from below by zero. Besides, it evolves above the npv curve or overlaps it. The vertical distance between them represents the value of the opportunity to wait. Intuition suggests that the distance will increase as the cost

increases; in this case it would be optimal to keep the option alive (and not exercising it). Conversely, there can well be a cost which is so low that the option to wait is worthless and the two curves overlap. In our case, under the initial values of

and

the option value evolves way above the npv: if it is possible to wait then it is optimal to defer investment.

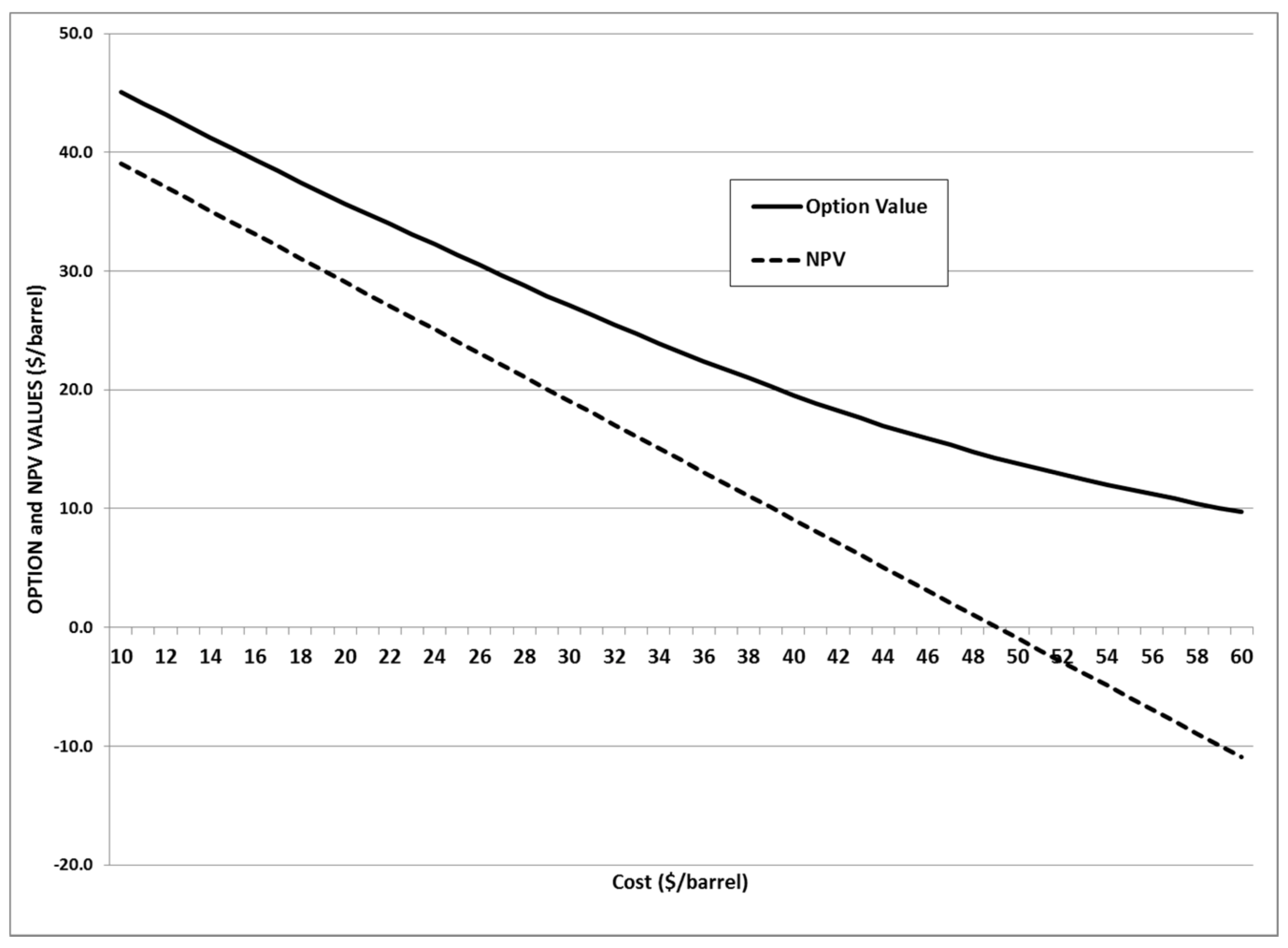

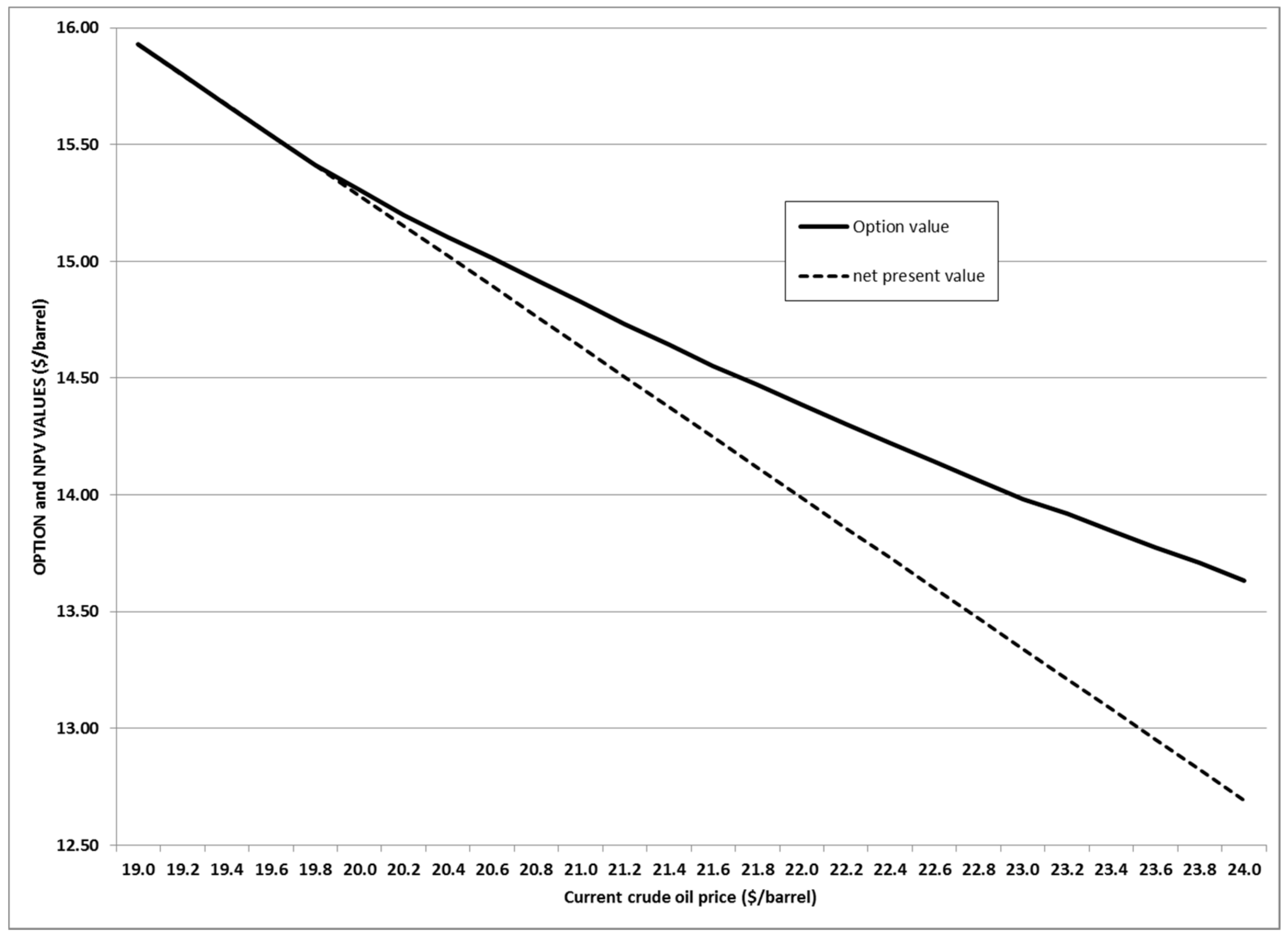

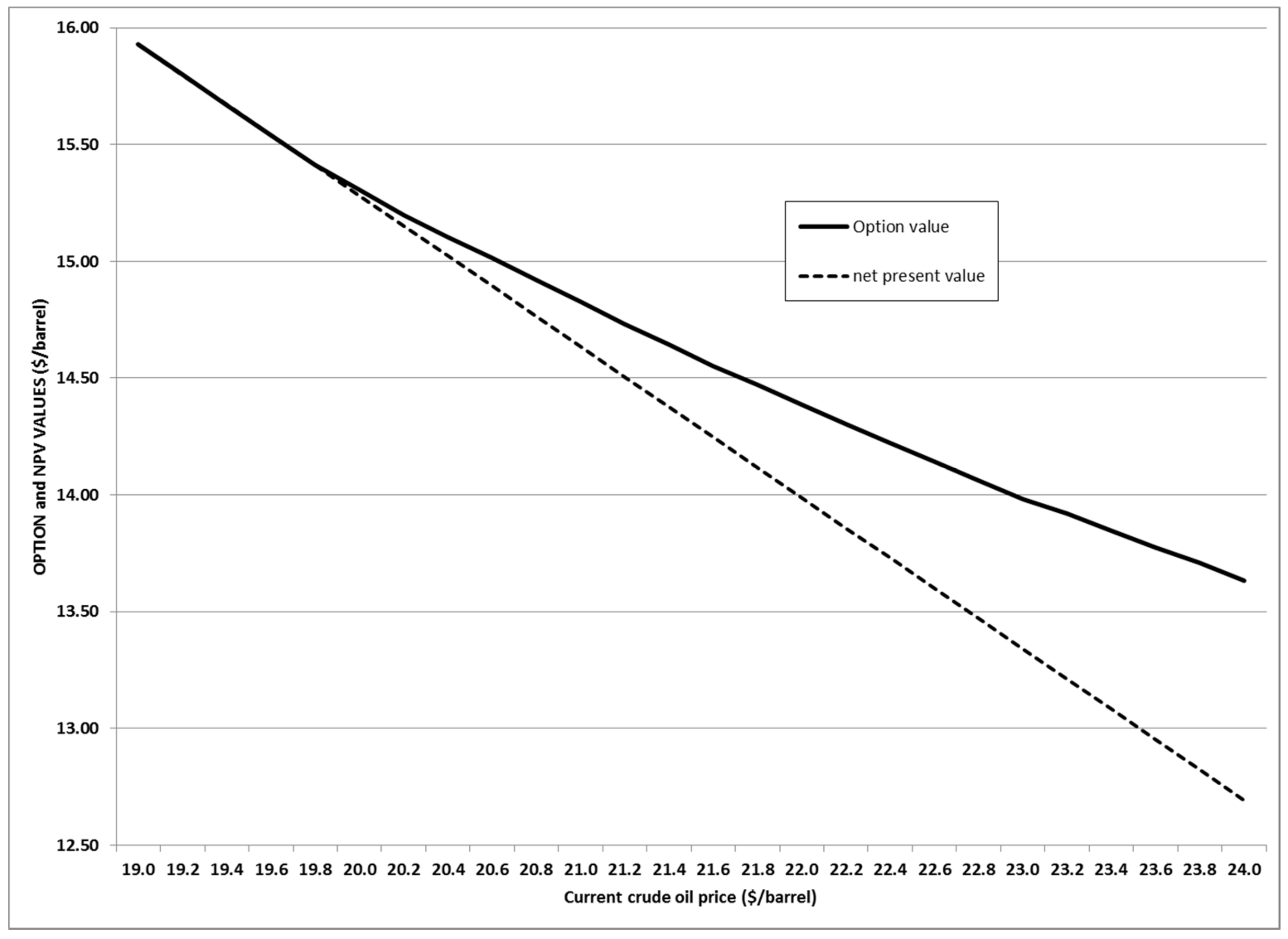

Figure 2 displays the option value and the net present value in the particular case in which

= 49.94

$/bbl. Both curves shift upwards but the npv curve undergoes a wider shift than the option value; look for example at the intercept with the horizontal axis. So if there is an option to delay, the optimal decision is to delay investment. Nonetheless the gap between both loci has narrowed significantly: as before, the option holder should not invest yet, but immediate investment is now closer.

As shown in the above figures, at the spot prices considered, if it is possible to wait the optimal strategy is to delay investment. The vertical distance between the two curves remains positive along the costs range considered. This means that there is a value to waiting. As a consequence, the investment should be postponed.

Clearly, when there is no option to wait the decision boils down to whether invest immediately or not. In this case only the npv curve applies and we can follow the standard NPV rule. For example, in the base case (

Figure 1) when

= 30

$/bbl we have npv = 7.07

$/bbl, i.e., the trigger cost is 37.07

$/bbl. This value is higher than the current oil price

= 31.36

$/bbl (see

Table 1); this is mainly caused by the growing pattern (contango) of the crude oil futures market (as of the end of our sample period). Therefore, at the current oil prices under the NPV rule the optimal strategy is not to invest. If current oil price matches the long-term level at 49.94

$/bbl (

Figure 2) a cost

= 49.08 makes the npv drop to zero; that number is a bit lower than

= 49.94 owing to the impact of time discounting. As production cost

, gets lower the option value and the npv get closer.

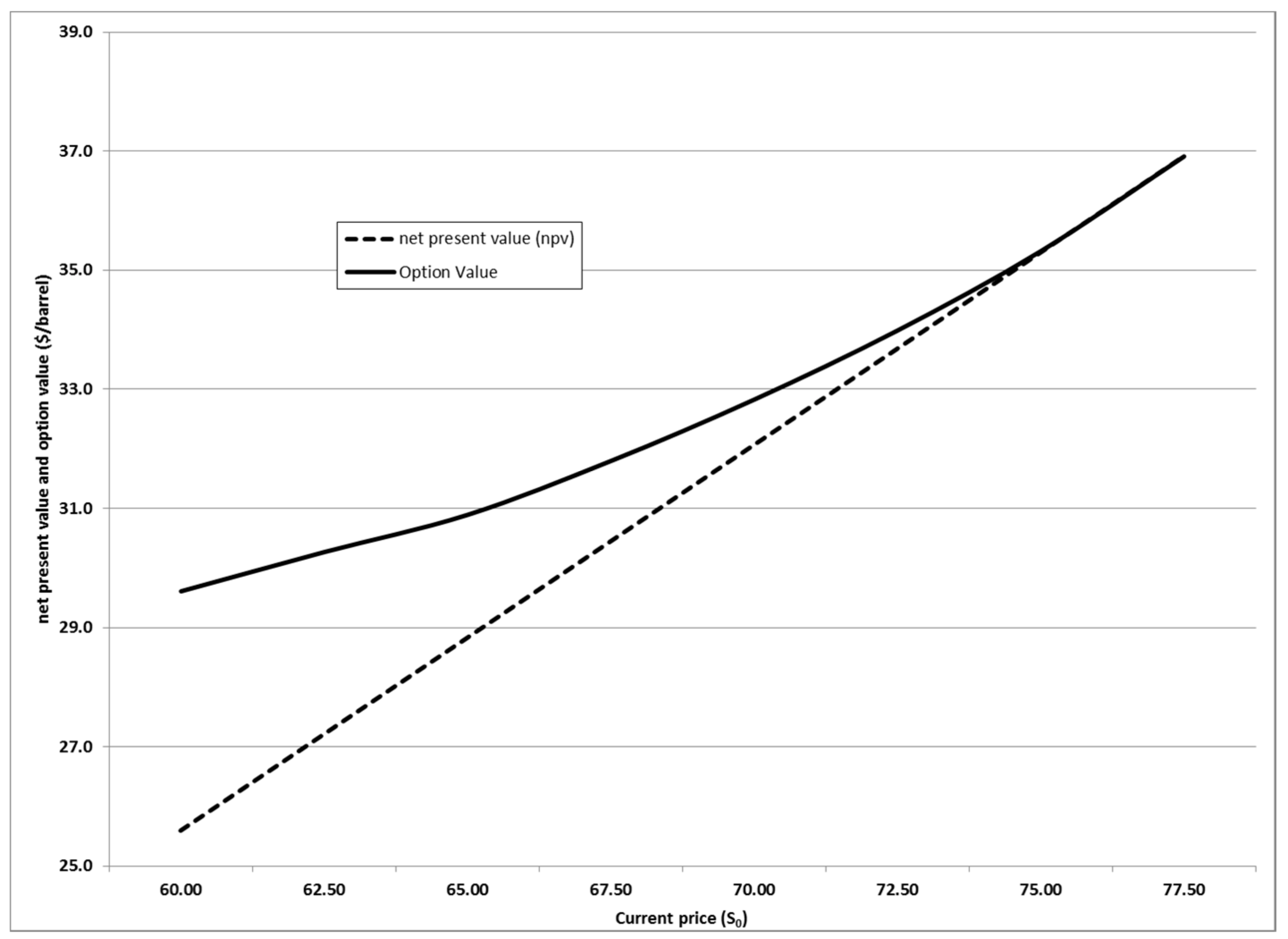

In general, for each cost level

there exists a current price

(given the oil price in the long run, 49.94

$/bbl) above which it is optimal to exercise the option to invest in a well. For one,

Figure 3 displays both the option value curve and the npv for a unit cost

= 30

$/bbl. It will be optimal to invest (thus killing the option to wait) when the two curves start overlapping; this happens at a ‘trigger’ spot price

= 75.39

$/bbl. However, when only the NPV applies, with

= 30 we undertake the investment immediately because the PV of the prospective income (37.07

$/bbl) surpasses the cost which results in a positive npv = 37.07 − 30 = 7.07

$/bbl.

In

Figure 3 the unit cost is fixed at 30

$/bbl. Now

Table 2 shows the spot price that triggers investment for a number of different costs (while keeping the long-term price constant). In principle, as the unit cost

increases the spot price required for investing to make sense increases too; this is actually the case here. The PV of future income evolves in the same way.

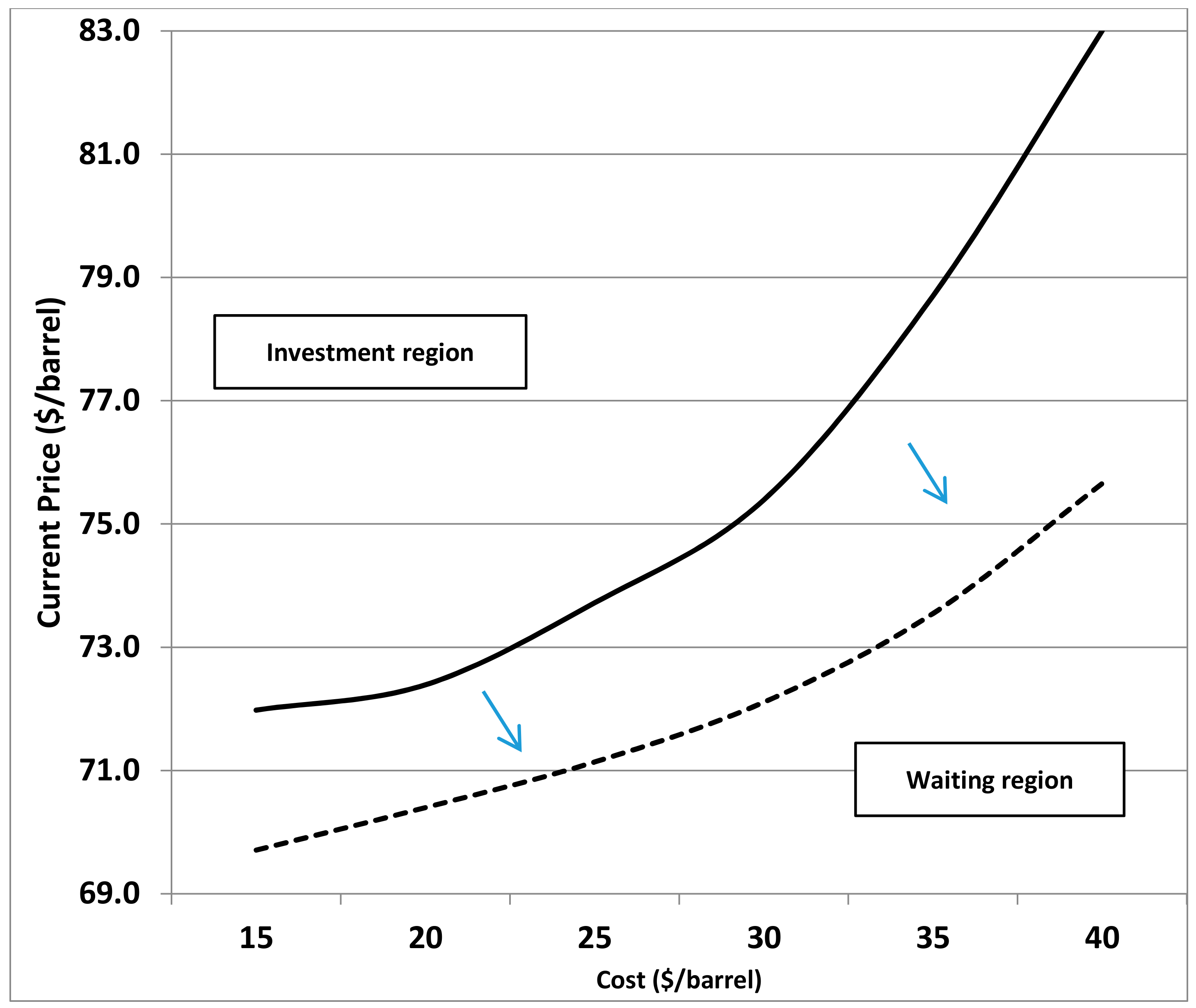

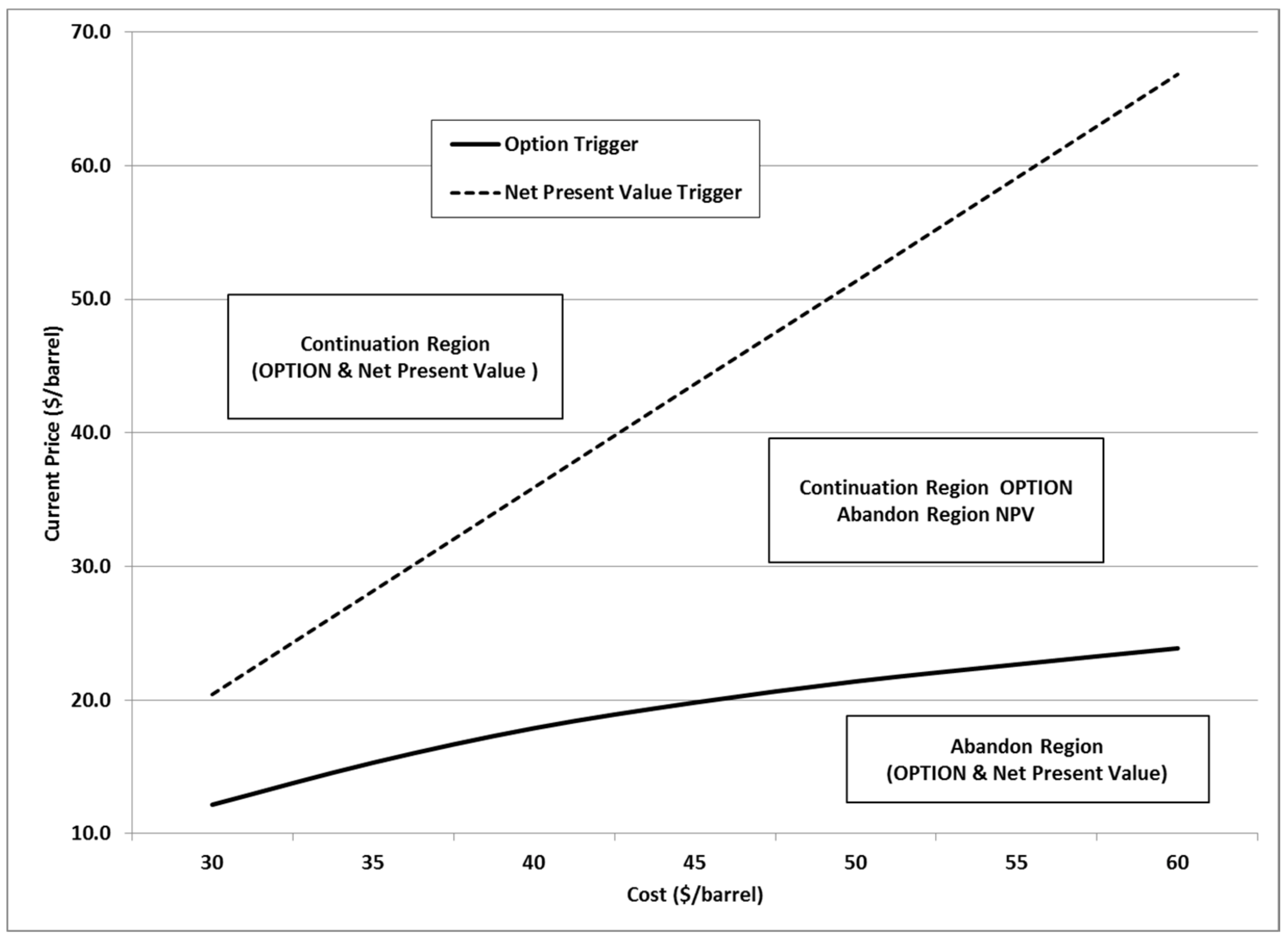

The former relationship is displayed in

Figure 4. Intuitively, when the cost is low and the spot price is high it is optimal to invest (and stop waiting): this is the so-called investment region. Conversely, if the cost is high while the price is low it is better to wait: this is the continuation region. The upward-sloping bold locus represents the pairs (unit cost, spot price) for which the npv and the option value are exactly equal; in this case, management is indifferent between investing and waiting to invest. Out of this boundary one decision is strictly preferred to the other.

5.2. Valuation and Management of the Option to Delay: Myopic Volatility

Now we consider the option to defer without stochastic volatility. Reference [

3] observes that failure to respond to changes in oil price volatility by oil producers can entail a substantial cost. Consequently they have a strong financial incentive to assess their options as rationally as possible.

The parameter values are the same as in

Table 1, but here we use the long-term equilibrium volatility

as crude oil price change volatility (i.e., we leave the parameters

,

, and

aside along with the correlations with the spot price and long-term price processes). In this case, with just two (correlated) stochastic processes left we develop a two-dimensional binomial lattice over

= 5 years with 100 steps per year (

= 1/100); see [

16]. As shown in

Figure 5, ignoring the stochastic behavior of volatility consistently underestimates the value of the option de delay.

Since the option to defer is worth less, the reasons for keeping it alive are weaker than before. In terms of

Figure 4 this translates into an investment region that grows at the expense of the continuation region. Graphically the optimal boundary (bold line) shifts toward the south east (dashed line); we thank an anonymous referee for raising this point. Further, the underestimation gets more severe as the unit cost increases.

Table 3 sheds more light on this. Thus, undervaluation is relatively less of a problem while unit cost remains below 30

$/bbl. Henceforth the option to delay becomes grossly undervalued.

The ensuing shift in

Figure 4 has at least one practical implication. The area that stretches between the two boundaries represents pairs cost-price in which it would be optimal to not invest, yet the firm will do exactly that. This will surely eat into the firm’s profitability and prospects for the longer term. To make matters worse, we observe that the failure aggravates (the gap widens) as the investment cost rises; see also

Table 3.

5.3. Valuation and Management of the Option to Abandon

The option to abandon a producing well is conceptually equivalent to an American put option: the option holder can sell the underlying asset or project in exchange for the exercise price at any time up to the option maturity date. We calculate the option value per barrel of remaining oil in the well (at the time when we evaluate the abandonment option). Specifically, a producing oil well involves this real option: upon exercise of the abandonment option its holder gets the difference between the production cost (now saved) and the asset value (now foregone). We set a maximum of = 5 years for exercising this option. We numerically evaluate it at a particular date, namely the initial time of exploitation, when the well is assumed to have a remaining useful lifetime of 10 years.

At the option expiration (

) the value of the option to abandon at the final node on any random path is the maximum of two numbers, namely the value of exercising the option and zero:

Obviously the npv refers now to the decision to abandon the well definitively:

. Another difference with the timing option is that the abandonment option depends on time

because the remaining lifetime of the oil well is 10 –

. Further, at time

the PV of the prospective revenues is (see Equation (11)):

At earlier times 0 ≤

<

the PV of the cumulative (unit) income becomes:

Each particular simulation run gives rise to a particular value of . The average simulated unit income across the 200,000 runs at time is 48.50 $/bbl. Time means that the option is exercised at maturity (5 years), and hence the producing well has still 5 years ahead. According to Equation (6), the expected spot price at that date is 49.33 $/bbl. If we now replace for this value in Equation (22) the resulting analytic value is 48.62 $/bbl, which pretty much resembles the simulation average 48.50 $/bbl. So this robustness check seems to perform well.

Similarly to the option to delay, given the values of

along each path the LSMC approach is used. At the option expiration (

) the value of the abandonment option is determined by Equation (21). At earlier times we follow the same approach as before, Equation (18). Prior to the option maturity the abandonment option is worth the maximum of the exercise value and the continuation value:

Proceeding backwards, at the initial time

= 0 we get the option value (along with the optimal exercise pattern from then on):

Assuming an initial spot price

= 31.36

$/bbl (see

Table 1), a producing oil well with 10 years of expected lifetime, and a saved cost of

= 30

$/bbl, the value of the option to abandon the well is 3.29

$/bbl. Compared to the well’s npv for the same cost (7.07

$/bbl) this means that the abandonment option is worth as much as 45% of the former. Similarly, Reference [

26] considers several real options in an offshore oil project, namely learning options, the option to develop, and the option to abandon; the most valuable of them, by and large, is the abandonment option; see also [

6,

7,

28].

Table 4 shows the option value as a function of

and

. All else equal, if the initial spot price of oil increases the abandonment option is less likely to be exercised and consequently less valuable. Conversely, a rise in the extraction cost renders cessation of operations ever more economically reasonable and the option is worth more.

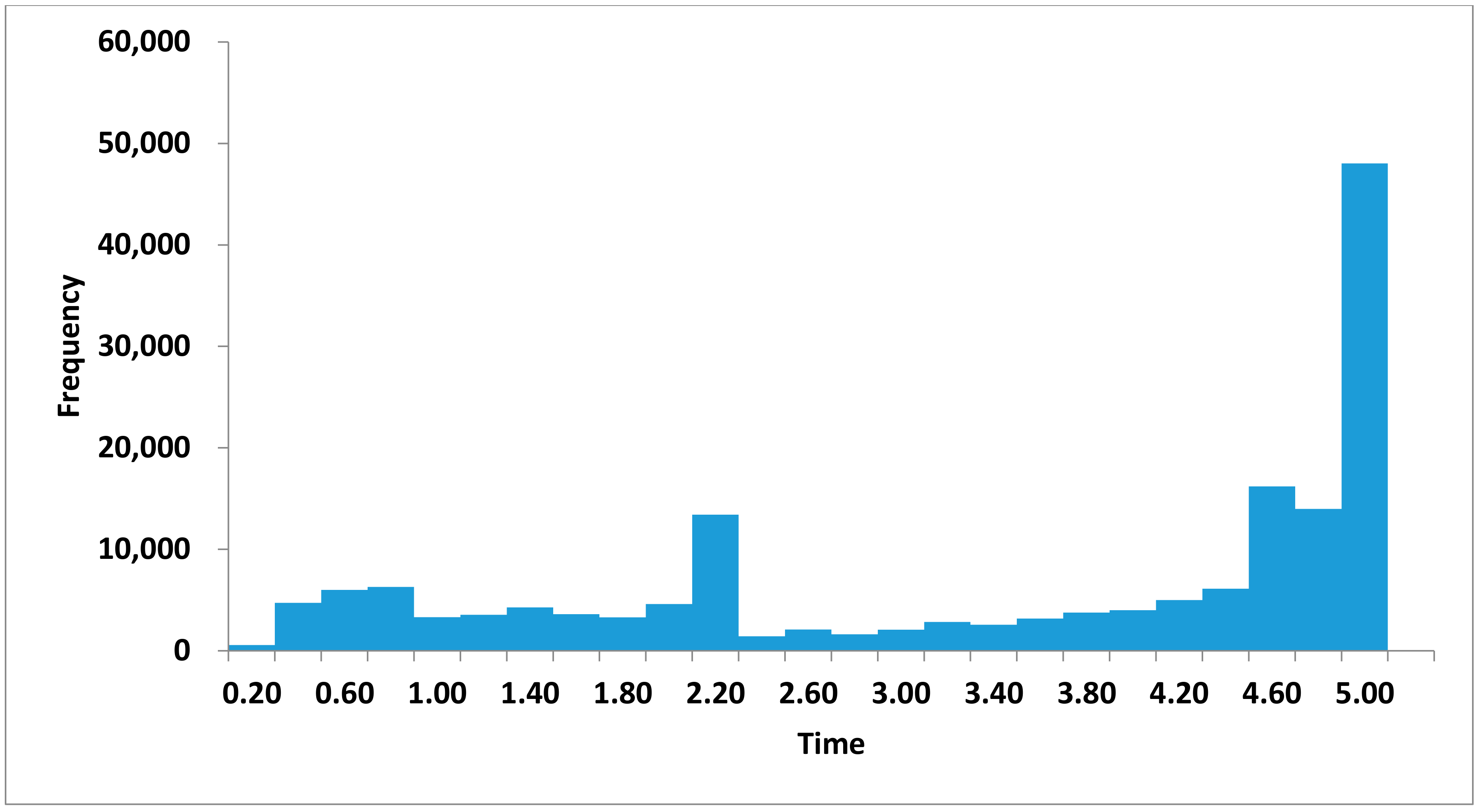

Figure 6 displays the npv and the option value as a function of the current oil price (

) for a particular cost (

= 45

$/bbl). Moving leftwards both functions overlap for the first time at

= 19.81

$/bbl; above this threshold the option value is higher than the npv so it is better to keep it alive (by not exercising) and wait, because oil price can rise more than expected (note that the abandonment option has 5 years to maturity). Instead, below 19.81

$/bbl the two functions overlap, i.e., there is nothing extra to be gained from the option with respect to immediate abandonment. Therefore the optimal strategy is to exercise the option and leave the oil well; this specific trigger price (19.81) depends on the specific cost

saved by leaving. If for whatever reason the firm cannot afford losses and is unable to preserve the option alive then the NPV rule applies. The question here is: given

= 45, at what spot price does the npv switch from positive to negative? In other words, what is the intercept of the npv curve along the horizontal axis? Though not shown in

Figure 6 the trigger price is

= 43.63

$/bbl. Apart from this, as a general rule the option trigger price converges to the npv trigger price as the option’s time to maturity decreases.

Now

Figure 7 draws the optimal boundary between the abandonment region and the continuation region (bold line) in the spot price/unit cost space; along this line the producer is indifferent between remaining in business and quitting. The boundary of the NPV rule is displayed too (dashed line); along this line npv = 0. Starting with the latter, the dashed line divides the space in two parts. On the north-west side

, which suggests that the producing well is making a profit (npv > 0) and should be kept open. Instead, to the south-east

and the well is making a loss (npv > 0) so closure is optimal. Regarding the option boundary, it obviously applies when it is possible to abandon the well in the future. Since uncertainty can unfold favorably in the future but abandonment is considered an irreversible decision, for any given production cost optimally abandoning the oil well will require a lower oil price than before. This is why this locus evolves below the npv boundary (and is closer to the horizontal axis). We thus have three different regions: (i) the high region, in which the oil well is definitively open (whether or not there is an option to abandon because this is worthless); (ii) the intermediate region, in which the oil well makes a loss but remains open in presence of the abandonment option or is closed otherwise; (iii) the low region, in which the firm is making a loss and there is no point in waiting to abandon, so it is time to definitely close the oil well down.

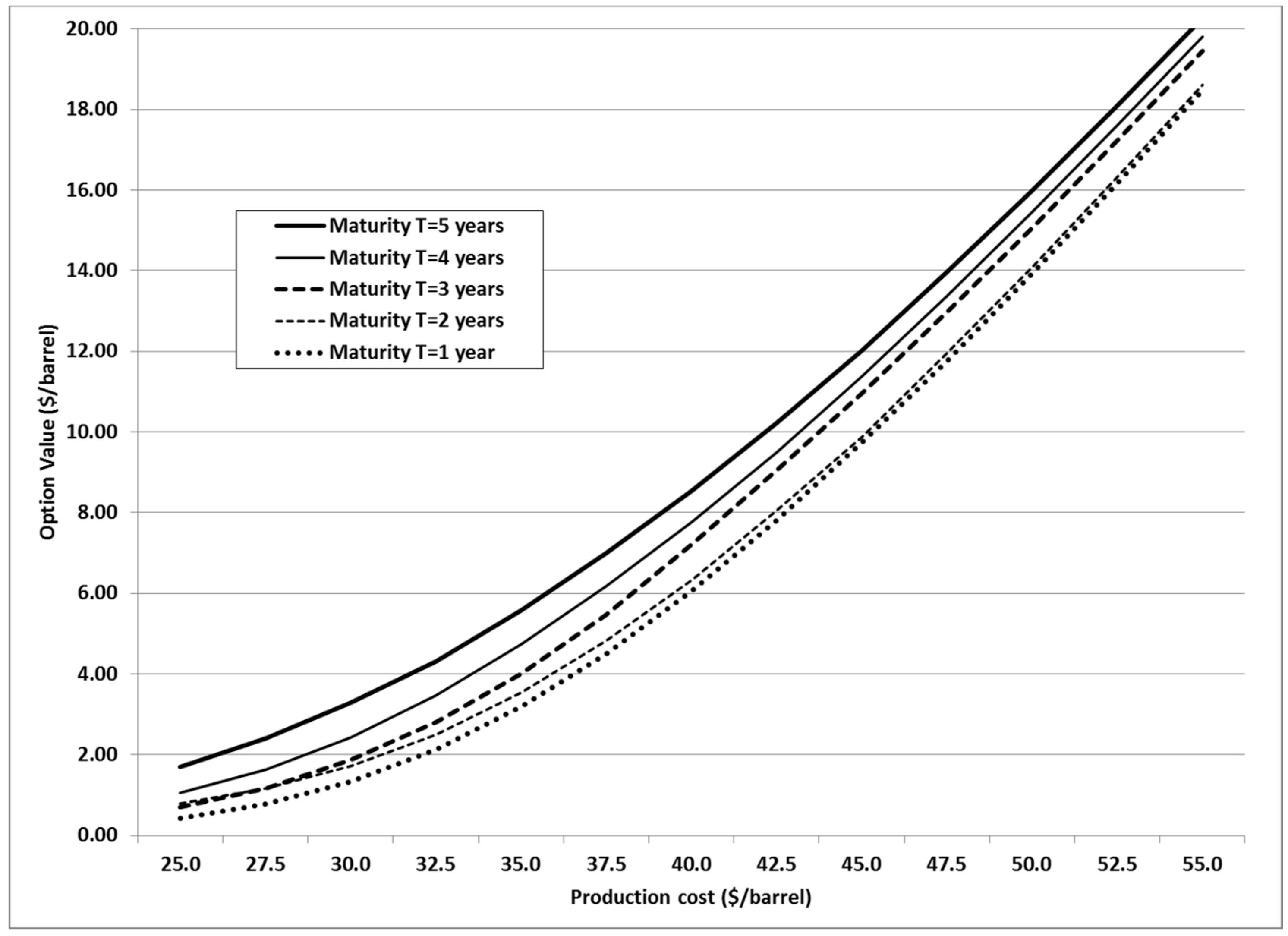

Last, the value of the option to abandon clearly depends on the option time to expiration.

Figure 8 displays this relationship. The abandonment option is more valuable as the saved production cost increases. Nonetheless, whatever the level of

, the option is worth less as it approaches maturity: as expiration gets closer there is less room for favorable surprises, so the line jumps downward steadily.

5.4. Exercise of the Option to Defer and the Option to Abandon

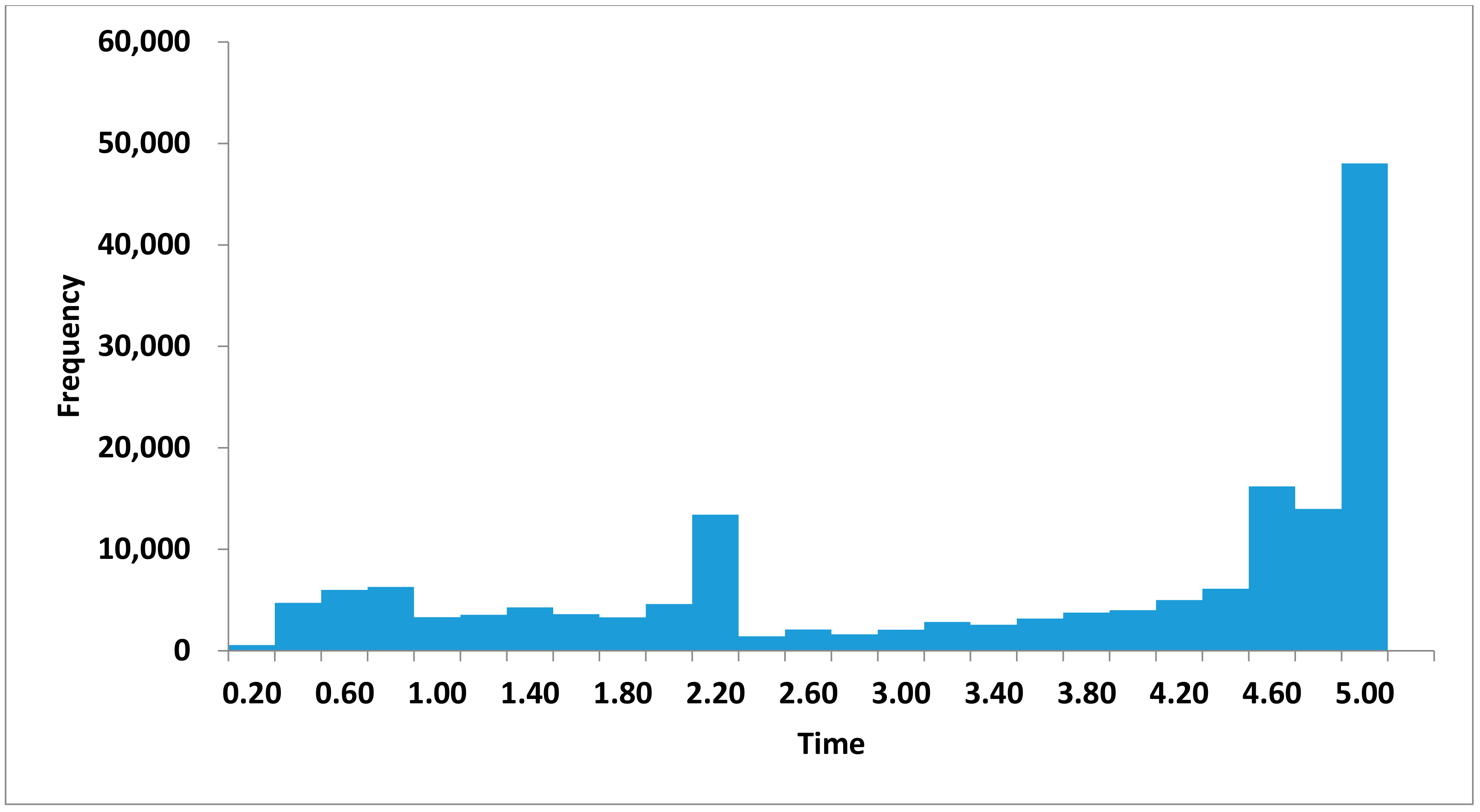

The time at which an oil producer should invest for taking oil from the ground, or close down the well definitively, can well be of interest for its future viability; we thank again an anonymous reviewer for bringing this issue to our attention. We address this suggestion for both options. In addition to the base maturity of T = 5 years, below we also consider the case with T = 1. Remember that we run 200,000 simulations.

Regarding the option to defer, the results are summarized in

Table 5. Looking at the bottom block (

T = 5, base case), we learn that 16.7% of the times there is no investment. In the remaining 83.3% of the cases the average time to invest is 3.43 years, with a standard deviation of 1.61 years.

Figure 9 sheds more light on this issue. Clearly, for the sample period considered, most of the investment cases take place at the very end of the option’s lifetime. This suggests that the incentives for waiting are rather powerful: only when it is no longer possible to wait there seems to be a strong case for investing. A closer look also shows a small peak around the middle of the time to maturity; at this time the value of the option is still important (it is at its half-life) but oil prices (foregone revenues) may be too high for keeping on waiting to invest.

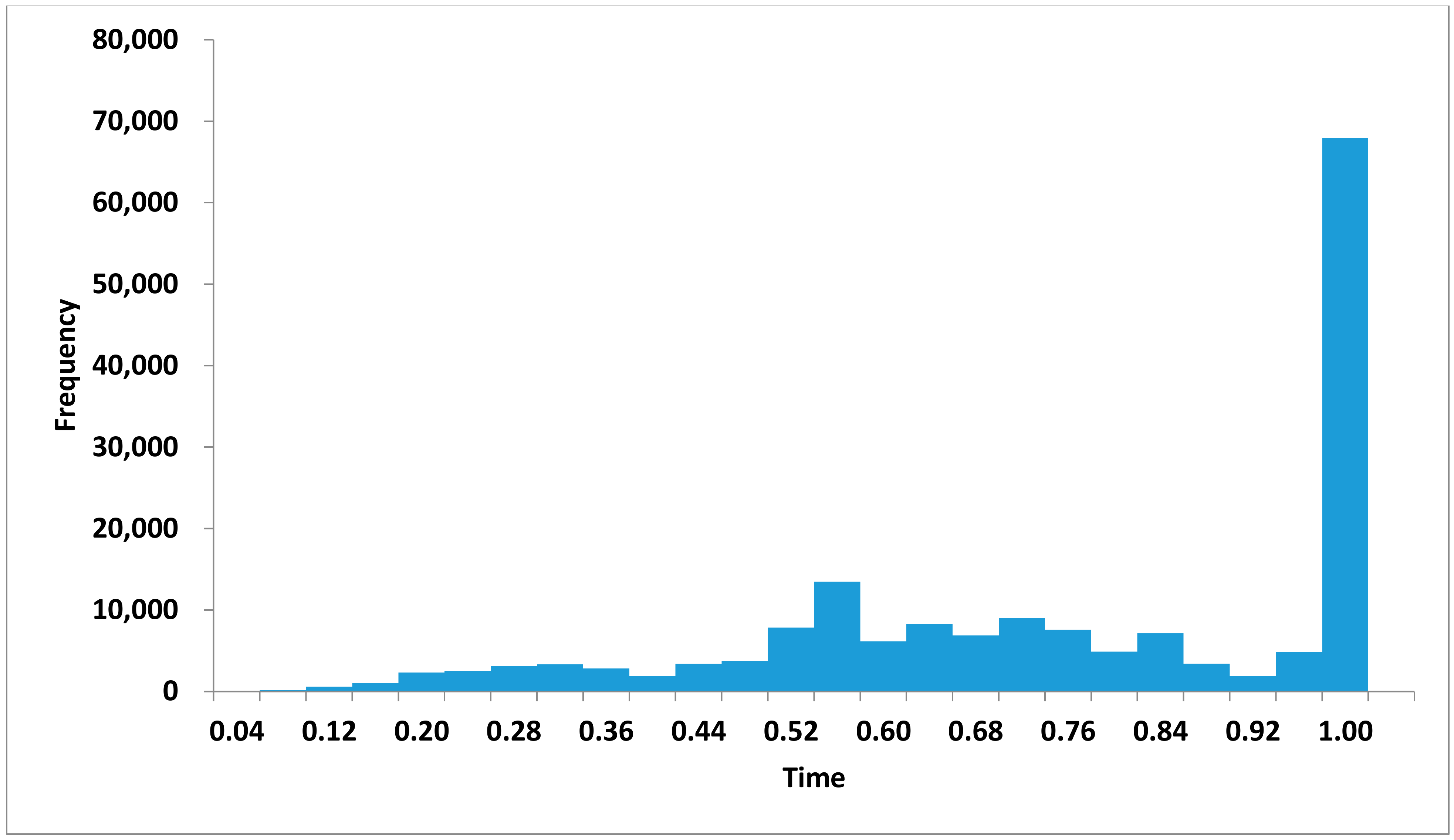

We have undertaken a similar analysis for a much shorter maturity of

T= 1 year (top block in

Table 5). The fraction of samples with no investment drops to 12.4%. Intuitively, the value of the option to defer is now much lower than before (

T = 5), so the overall value of the opportunity to invest gets closer to the

npv, the benchmark for a now-or-never investment. This effect shows up as an increase in the number of cases in which the firms invest, from 83.3% (with

T = 5) to 87.6% (with

T = 1). They nonetheless take their time for investing; the average is 0.75 (out of 1 year) with a standard deviation of 0.24 years. As can be seen in

Figure 10, again most of the firms that undertake investment do so at the very end of the option’s lifetime.

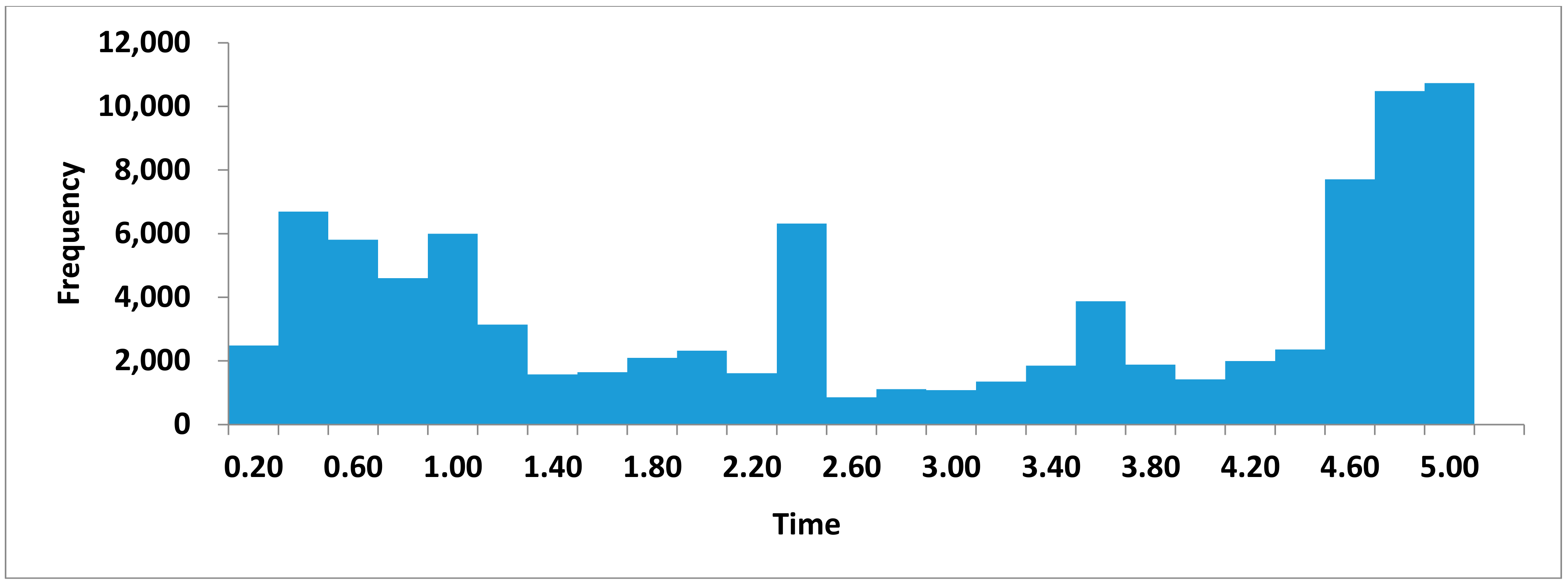

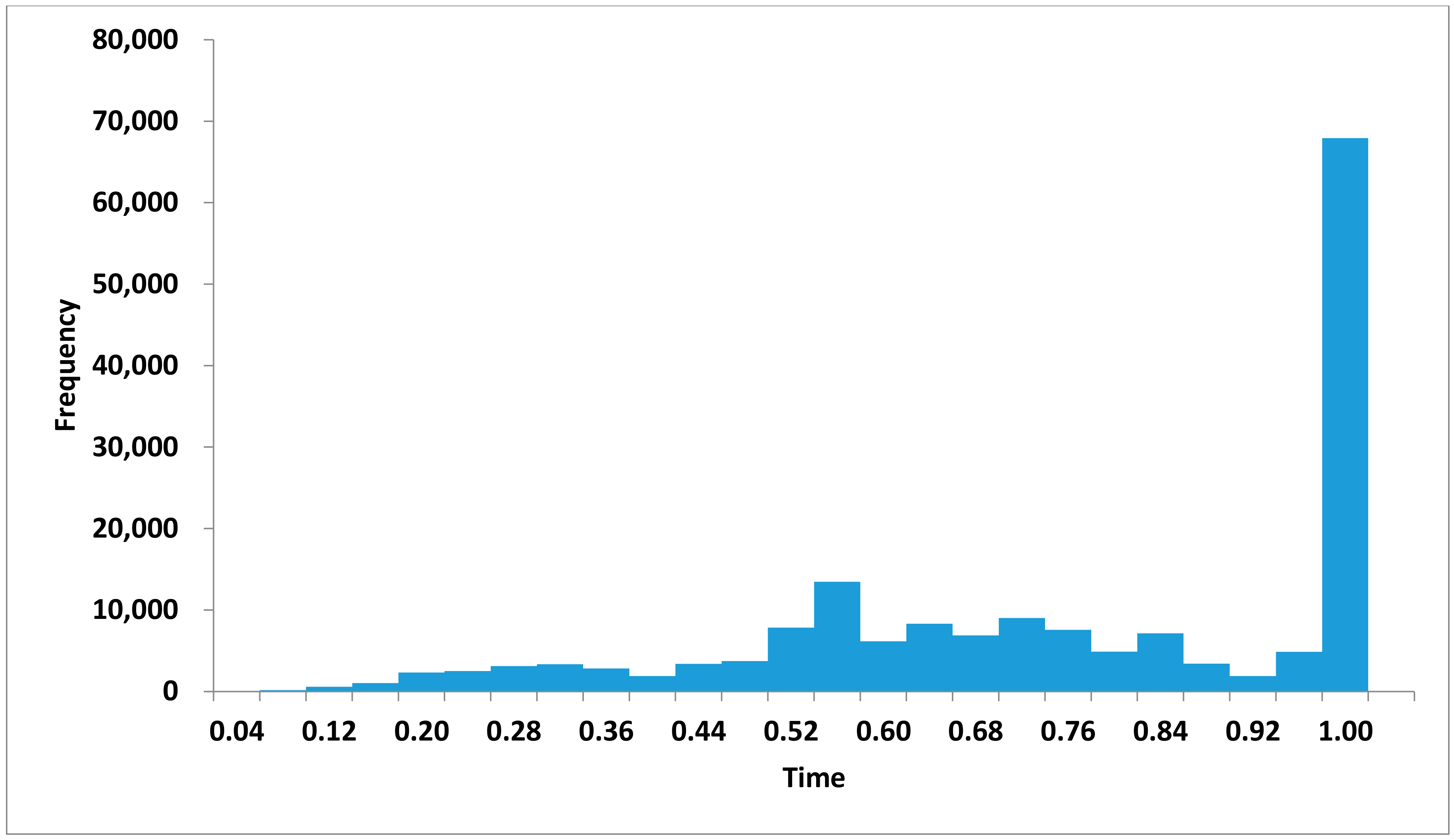

Concerning the option to abandon, the results are summarized in

Table 6. As shown in the lower block (

T = 5, base case), 54.5% of the times there is no abandonment. When the firm exercises the option (in 45.5% of the random samples) the average time to do so is 2.73 years, with a standard deviation of 1.74 years. The two proportions are close to each other; this suggests that the decision to abandon looks to some extent like a matter or chance (say, flipping a coin) with a small advantage in favor of continuing business.

Figure 11 displays the frequency distribution. In this case, for the sample period considered, abandonments tend to concentrate on the tails: they take place either close to the beginning or close to the end of the option time to maturity. They also spread more or less equally on both tails, with a small peak in the middle. This again resembles a matter of chance. Maybe the spot price happens to start from a low level but, since volatility increases with time and maturity is still far in the future, it makes sense to wait and see (instead of abandoning early). Yet if the circumstances do not improve enough by mid course then it is time to stop waiting and definitively abandon business (the small central peak). Conversely, if the spot price happens to start from a high level then it is profitable to remain in business; the situation can well turn sour (volatility is there after all), but there is ample room for maneuver (the option maturity is still very distant). In short, it makes sense to keep operations for a while. If, in the end, the prospects justify it, it is time to quit.

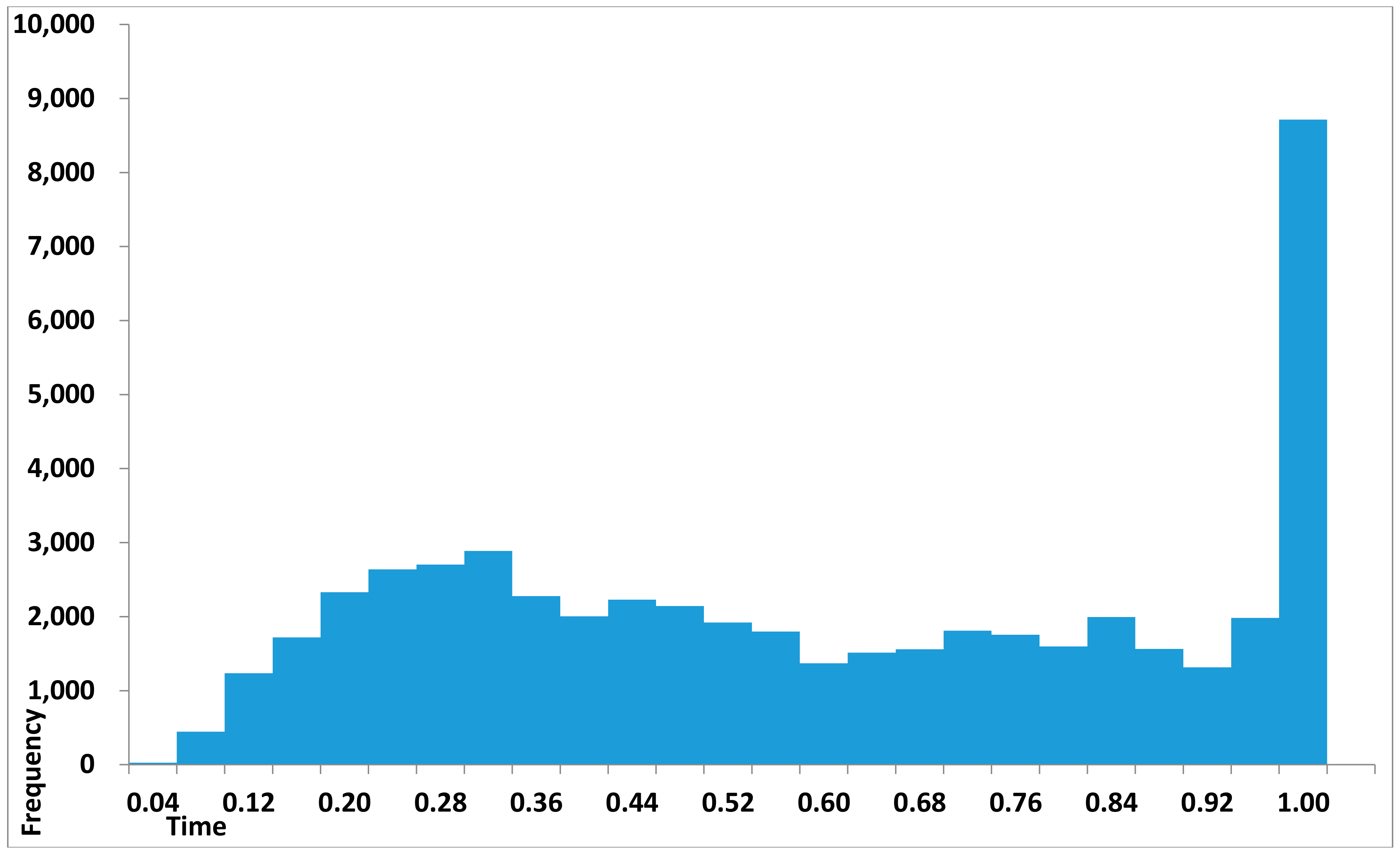

We have developed a similar analysis for a maturity of just

T = 1 year (upper block in

Table 6). The fraction of samples with no abandonment jumps up to 74.2%. As the time to maturity shortens dramatically the value of the option to abandon is much lower than before (

T = 5), so the overall value of the opportunity to invest gets closer to the

npv (so the

npv-rule applies). This effect shows up as a decrease in the number of cases in which the firm closes down permanently, from 45.5% (with

T = 5) to 25.8% (with

T = 1). They take some time for abandoning; the average is 0.58 (out of 1 year) with a standard deviation of 0.29 years. As shown in

Figure 12, many of them only give up their business in the very end (note that abandonment is irreversible).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}