1. Introduction

Climate risk encompasses a broad spectrum of threats arising from climate change, including direct physical impacts, such as extreme weather events, rising sea levels, and shifting rainfall patterns, as well as indirect transition risks associated with policy, technology, and market adjustments. These risks can significantly affect both natural ecosystems and human-built environments (

Battiston et al., 2021). At the same time, financial stability refers to the ability of the financial system to function efficiently in allocating resources, assessing and managing risks, and supporting economic activity without experiencing systemic disruptions (

Mishkin, 1999). Climate change poses growing threats to financial stability by impairing asset valuations, increasing default risks, and undermining institutional resilience.

For example, frequent tropical storms and extreme heat events can damage infrastructure and property, raising default rates on mortgage loans and triggering large-scale insurance claims. These disruptions may depress real estate prices and destabilize capital markets. Transition risks—such as carbon taxes, stricter emissions regulations, or changes in investor sentiment—can impose severe financial burdens on carbon-intensive industries, potentially leading to stranded assets, corporate bankruptcies, and market volatility (

Christophers, 2017). This dynamic demonstrates the increasingly systemic nature of climate-related financial risks.

In the context of emerging economies, financial systems are particularly vulnerable due to institutional weaknesses and limited adaptive capacity. However, they also have the potential to drive change. (

Behera et al., 2024) show that green finance instruments, such as green bonds and ESG investments, have significantly reduced CO

2 emissions in 14 developing countries between 1990 and 2021. Their findings highlight that renewable energy deployment, when supported by green financial mechanisms and strong political institutions, plays a vital role in mitigating climate risk and enhancing financial system resilience. This underscores the dual role of financial actors in emerging markets—as both vulnerable entities and key agents of transition.

Previous research on the effects of climate risk on financial stability has been conducted. For instance, a study by (

Chabot & Bertrand, 2023) highlights that climate-related risks have become a major concern for financial regulators and pose significant threats to financial stability. Their research estimates the influence of physical and transition risks on the European financial system by measuring financial stability at the bank and system-wide levels. The findings reveal that Scope 3 greenhouse gas emissions and chronic climate risks negatively affect financial stability, both at the financial institution level and the system level. Temperature anomalies, heatwaves, wildfires, and droughts are some of the most significant risks. Since Europe is warming twice as fast as other parts of the world, the theoretical and empirical results of this study urge regulators to mandate corporate climate risk assessments and disclosures to enable banks to adjust their prudential capital requirements accordingly.

Similarly, research by (

Karydas & Xepapadeas, 2022) yields aligned findings, noting that in addition to extreme macroeconomic events (e.g., wars, financial crises, and pandemics), climate change also threatens financial stability through the increasing frequency and intensity of extreme climate events and policy risks that depress asset valuations. Their study supports the hypothesis that real interest rates decline as the planet warms, while rising climate policy risks reduce the participation of “brown” assets in market portfolios. In financial terms, a decline in the participation of brown assets indicates that these assets are becoming less desirable or invested in market portfolios, especially due to rising risks associated with stricter climate policies, such as carbon taxes or regulations limiting emissions. This may cause investors to shift away from brown assets and toward green assets, which are more environmentally sustainable.

Earlier studies have established that climate change is one of the greatest threats to global financial stability, with impacts spanning various economic sectors. However, several limitations and gaps remain in the current literature. First, most research has focused on specific geographic regions, particularly in developed economies such as those in Europe and North America. There has been limited comprehensive research examining the impact of climate risks on financial stability in developing countries, which often face higher vulnerability due to weaker financial infrastructure, limited adaptive capacity, and less resilient institutions. Second, methodological approaches in prior studies tend to emphasize micro-level empirical analysis, whereas systemic and macro-financial impacts especially in emerging economies remain underexplored. Third, there is a need to understand how the interaction between physical and transition risks affects financial stability over time, particularly in the context of global climate policy uncertainty. Addressing these gaps is critical, as developing economies are likely to experience disproportionate climate-related shocks but lack the tools and policy frameworks necessary for effective risk mitigation. Therefore, future research should place greater emphasis on the unique challenges and policy needs of financial systems in emerging markets.

This study seeks to address these gaps through a systematic literature review (SLR) supported by bibliometric analysis. Unlike prior reviews, it employs a structured and data-driven bibliometric approach using tools such as VOSviewer to analyze 174 Scopus-indexed publications from 1988 to 2024. By integrating SLR with bibliometrics, the study provides a longitudinal mapping of the field’s evolution, identifies influential authors and journals, tracks keyword trends, and uncovers underexplored research areas.

The novelty of this study lies in its combined methodological approach and global scope, which enhances the understanding of climate–financial linkages beyond specific case studies. Furthermore, by explicitly highlighting research gaps and emerging themes including adaptation finance, ESG integration, and disclosure harmonization, the study contributes actionable insights for scholars, regulators, and policymakers. This integrated perspective offers a clearer pathway for strengthening financial system resilience in the face of accelerating climate change.

The author conducts bibliometric analysis using technologies such as VOSviewer software Version 1.6.20, Microsoft Excel 2013 spreadsheets, and data analysis tools available on the Scopus database to better understand the progress of research in the fields of green finance and the renewable industry. This study aims to answer the following questions:

To analyze the annual publications on climate risk and financial stability from 1988 to 2024.

What are the current research trends and key themes in the study of climate risk and financial stability?

Who are the most cited authors in the field of climate risk and financial stability?

Which journals have produced the most articles related to climate risk and financial stability?

What are the most frequently occurring keywords in publications on climate risk and financial stability?

How are the keywords or variables related to climate risk and financial stability interconnected?

What research methodologies have been employed in previous studies on climate risk and financial stability?

What are the research gaps and future directions in the study of climate risk and financial stability?

To address these research questions, this study will perform a bibliometric analysis of 174 articles. The bibliometric analysis will be conducted in several stages, starting with the use of relevant keywords to gather a suitable set of documents. The search results will then be filtered to ensure that the required number of documents is obtained, all of which must meet the predetermined criteria. The process will also ensure the inclusion of all relevant documents by verifying their alignment with specific keywords, subject areas, document types, and language. Any irrelevant or unsuitable documents will be excluded from the analysis. The research will be structured into five main sections. The first section will provide an introduction, followed by a review of the literature in

Section 2.

Section 3 will describe the research methodology, while

Section 4 will present the results and discussion. Finally,

Section 5 presents the conclusions and final discussion.

2. Literature Review

Climate risk refers to the potential negative impacts arising from climate change caused by human activities, affecting various aspects of life, including the economy and public policy. This risk encompasses a range of physical threats, such as the increased frequency of natural disasters like floods, droughts, and storms, which can damage infrastructure, disrupt food production, and interfere with economic activities. Additionally, climate risk is often accompanied by uncertainty regarding its impacts and an uneven distribution across different regions and time periods. Some areas may be more vulnerable to the effects of climate change, with varying impacts depending on the timing and intensity of the disruptions. The challenge in addressing climate risk lies in how to integrate information and risk analysis into public policy. For instance, an ideal policy should balance the costs and benefits of various scenarios, whether driven by regulatory interventions or business-as-usual projections. However, every aspect of climate risk analysis, such as modeling long-term impacts, addressing model uncertainty, and choosing an appropriate discount rate, remains complex and frequently debated. A real-world example is the European Union Emissions Trading System (EU ETS), which places a cap on total greenhouse gas emissions and allows for the trading of emission allowances. While the system incentivizes decarbonization, it also creates financial exposure for firms in carbon-intensive sectors, illustrating the trade-offs involved in climate policy design.

The 1992 United Nations Framework Convention on Climate Change (UNFCCC) called on countries to take action to prevent “dangerous human interference with the climate system”. However, the convention did not provide detailed guidance on how to achieve this goal or indicators to measure success. In this context, climate risk also involves policy risks to the economy, businesses, or other actors that arise from political decisions made in response to climate change. For example, the implementation of cap-and-trade systems, carbon taxes, or adaptation decisions can influence how companies operate and how the economy as a whole adapts to climate change. Therefore, understanding both the physical risks of climate change and the policy risks that emerge from political decisions is crucial for designing effective strategies to manage and mitigate the impacts of climate change (

Hultman et al., 2010).

In this context, climate-related financial risks are generally categorized into physical risks and transition risks, as outlined by (

Dikau & Volz, 2021). Physical risks stem from the direct impacts of climate change—such as floods, droughts, storms, or sea-level rise—which can damage infrastructure, disrupt business operations, and impair asset values. In contrast, transition risks refer to the financial uncertainties and costs associated with the shift to a low-carbon economy, such as those arising from regulatory changes, technological advancements, or shifting investor preferences. For example, policies like carbon taxes or restrictions on fossil fuel usage may reduce the profitability of certain industries, potentially affecting credit markets and financial valuations. Understanding both types of risks is essential, as they jointly influence the resilience of financial systems and require different policy responses. The recent literature has begun to explore how mandatory climate-related disclosures affect investor behavior and market stability. Such disclosures help reduce information asymmetry, improve risk pricing, and promote long-term investment strategies aligned with sustainability goals. In line with this, (

Yaala & Henchiri, 2024) employed the NARX model to predict stock market crises in the MENA region based on investor sentiment, demonstrating that investors’ perceptions of risk and market information play a crucial role in decision-making. These findings highlight the importance of integrating behavioral approaches and advanced technologies in understanding financial market dynamics influenced by external factors such as climate risk.

Financial stability refers to the characteristics of an economic system that is resilient to financial instability. A key feature of a financially stable economy is its ability to absorb shocks, rather than amplify their effects. However, similar to physics, there are various aspects to this characteristic. For instance, an economy may be capable of absorbing minor shocks effectively, but at the same time, it could exacerbate the impact of larger shocks. Thus, while the economy might handle small disturbances without issue, when faced with larger shocks, it may struggle to absorb them and could worsen the consequences (

Allen & Wood, 2006). From the definitions of climate risk and financial stability, it is clear that climate change is a key factor contributing to financial risk, and the pace of increasing climate risks influences the efficiency of financial markets.

Research on developing countries highlights the importance of addressing climate change risks. A study analyzing the impact of climate change on the Financial Stability Composite Index (FSCI) in China used panel data from 30 provinces (2005–2020), including robustness tests, heterogeneity analysis, and mediation effect tests. The results show that climate change significantly negatively affects financial stability. Specifically, greater deviations from average temperatures are associated with decreased financial stability. In other words, unusually high or low temperatures can undermine financial stability. This suggests that extreme temperature fluctuations may destabilize the financial sector, potentially triggering broader economic instability (

Meng et al., 2023).

This finding is reinforced by (

Christophers, 2017), who critiques the dominant global regulatory approach to climate-related financial risks. He argues that the increasing reliance on market discipline and climate risk disclosure, rather than more interventionist strategies may heighten the likelihood of a “climate Minsky moment”, particularly in financial systems already vulnerable to systemic shocks. A climate Minsky moment refers to a sudden and severe market correction triggered by the realization of climate-related risks that had been previously underestimated or ignored, leading to abrupt asset devaluations and financial instability.

Despite the expanding literature on climate-related financial risks, several important research gaps remain. Most existing studies predominantly focus on developed economies, while comprehensive insights into developing countries are still scarce—despite their heightened exposure and institutional vulnerabilities. In addition, prior research has tended to emphasize micro-level financial impacts rather than the broader systemic and macro-financial consequences of climate risk. Moreover, limited studies have integrated bibliometric trends with empirical evidence to map how the field is evolving and to guide future policy development. This study seeks to address these gaps by combining a systematic literature review (SLR) with bibliometric analysis, offering a structured synthesis of the academic landscape and highlighting the need for more inclusive, cross-country, and interdisciplinary approaches to understanding climate–financial linkages.

3. Methodology

This study is a structured review that focuses on commonly used methodologies, theories, and concepts, and falls within the category of systematic review publications. The primary goal of this framework-based and bibliometric study is to develop a model/framework. Bibliometrics is the most widely used approach to explore the knowledge framework of a research field and is employed to analyze the research subject in this study. A systematic literature review (SLR) and bibliometric analysis are used to summarize previous research content, reduce bias, identify potential research needs, and delve deeper into the domain. To analyze co-citation patterns and merge bibliographic data, standard bibliometric methods were applied to identify similarities among cited publications and authors. This study employed publication trend analysis, citation network analysis, keyword co-occurrence mapping, and co-citation analysis to cluster key themes and reveal the research structure. VOSviewer software was used for visualization, where the distance between nodes represents the strength of relationships, based on the “visualization of similarities” (VOS) principle.

For the systematic literature review (SLR), 174 journal articles were selected from the Scopus database using a combination of bibliographic coupling and co-citation techniques. Only peer-reviewed articles written in English and directly addressing both climate risk and financial stability were included. Editorials, conference papers, and unrelated studies were excluded after abstract and full-text screening (

Goyal & Kumar, 2021). The Scopus database was selected as the primary source due to its broad coverage of peer-reviewed literature, particularly in the fields of economics, finance, and environmental sciences. Compared to alternatives such as Web of Science or Google Scholar, Scopus offers more comprehensive metadata, including detailed author affiliations, citation tracking, and keyword indexing features essential for accurate bibliometric and co-citation analyses. Furthermore, Scopus integrates robust tools for data export and compatibility with software such as VOSviewer, which are crucial for mapping research trends and conducting visual network analysis with high precision and reliability. The literature search was conducted on August 2024, and the data used in this study were obtained from Scopus on that same date.

In

Table 1, the bibliometric analysis process in this study consists of five stages: first, conducting a search using relevant keywords to gather a set of appropriate documents; second, filtering the search results to obtain a number of documents that meet the pre-determined criteria; third, ensuring that all relevant documents are included in the analysis by verifying their alignment with specific keywords, subject areas, document types, and languages; and finally, excluding documents that are irrelevant or do not meet the defined criteria. The keywords used were “climate risk” AND “financial stability”, and only peer-reviewed journal articles in English were considered. Gray literature such as reports, policy briefs, theses, and conference abstracts were excluded from the analysis. Some articles that appeared relevant based on keywords and abstracts were excluded during the full-text screening stage because they were not written in English. Although these articles discussed topics related to climate risk and financial stability, they did not meet the language criteria set for inclusion. To ensure consistency and accurate bibliometric analysis, only English-language publications were retained in the final dataset.

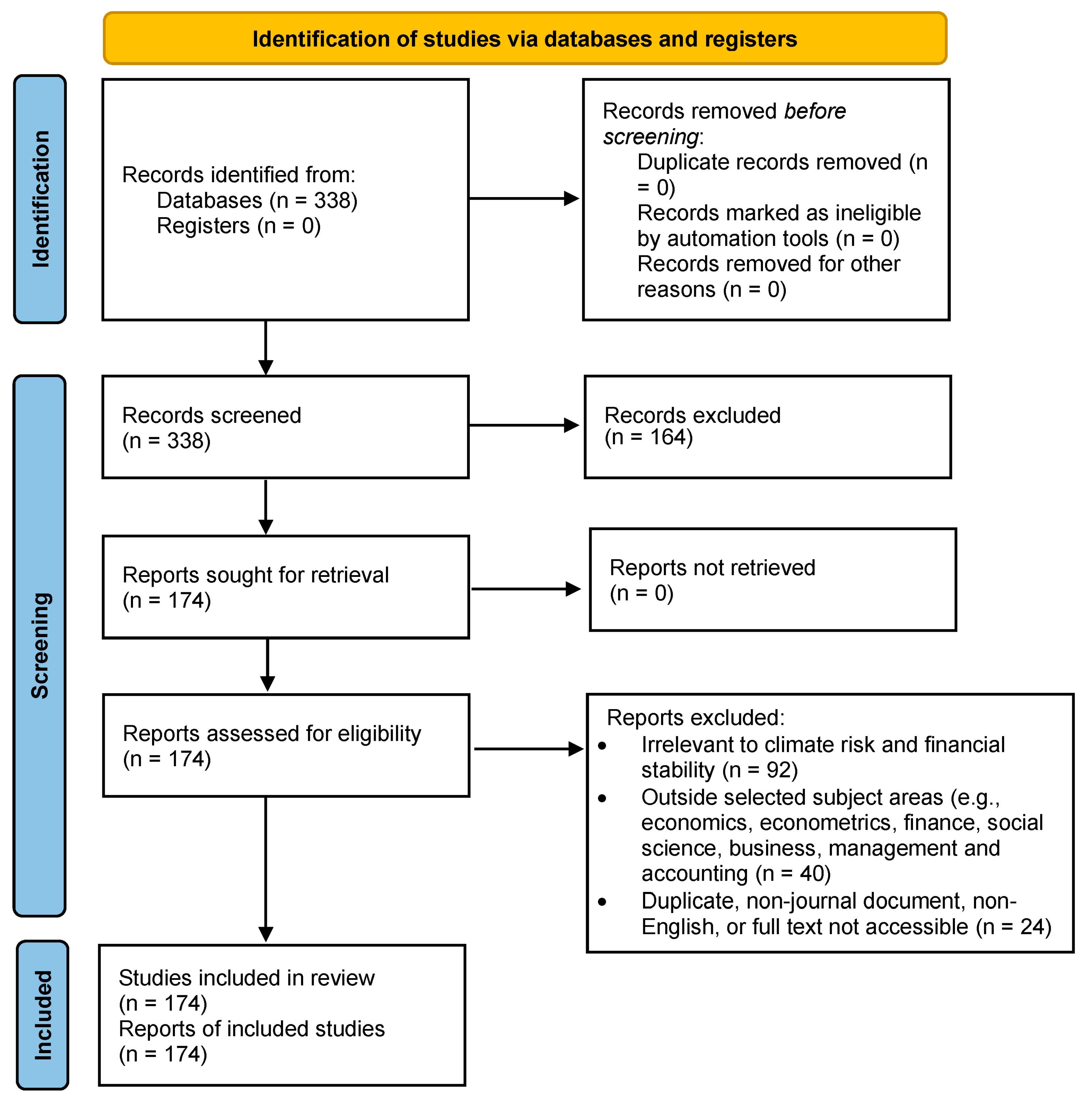

Out of a total of 338 documents retrieved from Scopus, 174 articles were included in the final dataset after applying the inclusion and exclusion criteria. A total of 164 records were excluded, consisting of 92 articles that were irrelevant to the topic of climate risk and financial stability, 40 articles that fell outside the selected subject areas (e.g., economics, econometrics, finance, social science, business, management, and accounting), and 24 records that were either duplicates, non-journal documents, not in English, or had inaccessible full texts. These exclusions were essential to ensure the quality, focus, and consistency of the bibliometric and SLR analysis.

The article selection process is illustrated in the PRISMA flow diagram (

Figure 1), which outlines the stages of identification, screening, eligibility, and inclusion.

The detailed query used to retrieve the relevant literature from the Scopus database is presented in

Table 1 below. This query was designed to ensure the inclusion of studies that specifically address both climate risk and financial stability within peer-reviewed journal articles.

4. Result and Discussion

In this study, out of a total of 338 publications, after applying the selected criteria, 174 publications on climate risk and financial stability published between 1988 and 2024 were identified and collected from the Scopus publication database. Among these, five key sources were identified as having the most articles published on the topic of climate risk and financial stability. These sources are the Journal of Financial Stability, Journal of Cleaner Production, Applied Economics Letters, Finance Research Letters, and Sustainability (Switzerland), as shown in the following figure.

In

Figure 2, from the total documents in the Scopus database, the

Journal of Financial Stability contains the highest number of documents, with 11 publications, representing 6.32% of the entire database. The

Journal of Cleaner Production ranks second, while

Applied Economics Letters,

Finance Research Letters, and

Sustainability (Switzerland) all hold third place, each with 2.87%. The fact that the

Journal of Financial Stability has the most articles related to climate risk and financial stability means that researchers and practitioners can find more references on this topic in that journal compared to others in the Scopus database. The progression of the number of articles published on climate risk and financial stability in the Scopus database from 1988 to 2024 is illustrated in

Figure 2 below.

Figure 2 illustrates the development of articles on the topic of climate risk and financial stability from 1988 to 2024. The first sample work does not specifically address climate risk and financial stability; rather, it focuses solely on the condition of financial stability. This work, published in 1988, has only 1 citation. Titled “The International Equities Market: Recent Developments and Prospects” by (

Torrisi, 1988), it appeared in the Review of Economic Conditions in Italy. This initial article discusses considerations and prospects regarding the opening of credit markets, the liberalization and integration of financial markets, European financial market integration and its implications for banking, international equity markets, international financial innovation, and capital market stability, relating to trade-offs, risks, and opportunities for major Italian banks.

Although the article does not explicitly mention climate-related risks, it reflects the early academic focus on financial system stability and systemic vulnerabilities, which later evolved into broader frameworks that incorporate environmental and climate-related dimensions. Including this publication in the analysis helps trace the historical trajectory of the literature—from traditional financial stability themes to the emerging intersection with climate risk. Its presence at the beginning of the dataset also highlights how the thematic scope of the field has expanded over time.

Between 1988 and 2024, articles specifically addressing climate risk and financial stability began to emerge. As shown in

Figure 3, In 2019 there was a significant increase of 500% in publications compared to 1988, indicating that the topic of climate risk and financial stability was becoming an important issue that required further analysis. Following the 2015 Paris Agreement, policy developments, particularly those related to climate policy uncertainty, began influencing both market volatility and research intensity. These developments, including the global push for decarbonization and financial disclosures, likely drove increased academic focus on the intersection of climate change and financial systems, encouraging studies on risk measurement, regulatory frameworks, and the resilience of financial institutions.

The most cited article on this topic in 2019, with 53 citations, is by

Nieto (

2019), titled “Banks, Climate Risk and Financial Stability”, published in the

Journal of Financial Regulation and Compliance. This article aims to quantify the exposure of syndicated loans to environmentally high-risk sectors within the banking systems of the US, EU, China, Japan, and Switzerland. The findings indicate that such exposures are significant across the countries studied. Additionally, the paper identifies several challenges in assessing risks related to the transition to a low-carbon economy, including the lack of a clear taxonomy to distinguish between “brown” and “green” sectors. Other findings highlight limitations in supervisory reporting, which has not fully utilized existing international statistical frameworks, such as the Common Reporting Framework (COREP) and the Financial Reporting Framework (FINREP) used within the European Union. The article also notes the absence of uniform reporting standards for environmental risks and weaknesses in supervisory governance that have not yet internalized such risks (for instance, in the revision of the Basel Core Principles for Effective Banking Supervision). The author emphasizes two critical elements that must be considered in prudential regulation concerning environmental risks: first, whether climate risk should be treated as a credit risk; and second, how environmental risks affect the probability of default throughout the business cycle.

In 2022, the number of articles discussing climate risk and financial stability increased by 267% compared to 2019. The most-cited article in that year was “Things Are Different Today: The Challenge of Global Systemic Risks” by (

Renn et al., 2019). This article discusses how, despite the OECD countries having successfully reduced risks to human life, health, and environmental quality, their track record in addressing new global risks such as climate change, pandemics, financial collapses, and social inequality remains inadequate. The main challenge faced is systemic risk. The article aims to clarify the concept of systemic risk by starting with paradigmatic examples from the financial crisis. This approach leads to an understanding of the global system as an interaction between the micro and macro dynamics inherent in the system, which also interacts with its environment. Typically, such dynamics indicate periods of stability interspersed with situations that open possibilities for different futures.

In 2024, articles on climate risk and financial stability continued to rise significantly, with an increase of 650% compared to 2022. This suggests that the topic is becoming increasingly interesting for further analysis, appealing to both academic and practitioner audiences. The most-cited article in 2024 specifically discussing climate risk and financial stability received 10 citations, authored by (

Liu et al., 2024) and titled “Impact of Climate Risk on Financial Stability: Cross-Country Evidence”. This article highlights the growing awareness that climate change poses new risks to the financial system, yet cross-country evidence regarding the impact of climate risk on financial stability remains limited. The study empirically investigates the impact of climate risk on financial stability using panel data from 2007 to 2019 across 53 countries. The findings reveal that climate risk negatively impacts financial stability, with adverse effects varying based on economic development levels, financial development, and competition among countries. Furthermore, macroprudential policies have proven effective in maintaining financial stability in countries affected by climate risk. However, the macroprudential policies imposed on borrowers differ from balance sheet-based and buffer-based macroprudential tools. Additionally, good national governance quality can mitigate the impact of climate risk on financial stability. Following exposure to climate risk, strengthening political stability, improving government efficiency, oversight, and legal systems, rigorously controlling corruption, and enhancing free speech and accountability contribute to maintaining the financial stability of countries across various levels. This study enriches existing research in the field of climate-related financial risk and provides references for government departments to mitigate climate risk impacts and maintain financial stability.

Research on climate risk and financial stability remains highly relevant and important today and in the foreseeable future, as climate risks can significantly affect various indicators of financial stability across different sectors and countries. Among the articles in the Scopus database from 1988 to 2024 on climate risk and financial stability, there are 20 publications with the highest citations out of 227 articles collected for bibliometric analysis. The table below provides an overview of the most cited documents related to climate risk and financial stability over the years, enabling authors to identify and select appropriate references.

Table 2 presents the top 20 most cited authors in the Scopus database whose works focus on climate risk and financial stability. Leading the list is (

Dikau & Volz, 2021) with 220 citations. Their article, “Central Bank Mandates, Sustainability Objectives, and the Promotion of Green Finance”, offers a qualitative assessment of how central banks address climate-related risks in line with their institutional mandates. The authors examine how to manage climate-related risks while supporting mitigation and adaptation policies that align with the objectives of central banks. The study analyzes the mandates and objectives of central banks using the IMF’s Central Bank Legislation Database and compares them with sustainability-related policies adopted in practice. Among the 135 central banks assessed, only 12% have an explicit sustainability mandate, while 40% are required to support national policy priorities, many of which include sustainability objectives. Given that climate risks can directly impact the core responsibilities of traditional central banks, the authors argue that all central banks must integrate both physical and transition climate risks into their policy frameworks to preserve macro-financial stability. Physical risks include extreme weather events and natural disasters, while transition risks arise from shifts in policies, technologies, or market dynamics related to the low-carbon transition. This contribution is significant in positioning monetary authorities as key actors in managing climate-related financial risks.

The high citation count of this work can be attributed to its pioneering role in linking central banking mandates with climate sustainability objectives. By systematically examining how environmental goals are embedded explicitly or implicitly within central bank frameworks, the study opened new pathways in the literature on green finance governance. Its methodological rigor, global comparative scope, and policy relevance have made it a foundational reference for scholars and regulators seeking to integrate climate considerations into macroprudential and monetary policy. This explains why the study has gained significant academic and policy traction since its publication.

Building on the evolving role of central banks in addressing climate-related financial risks, the recent literature has increasingly emphasized how monetary policy instruments can be leveraged to mitigate these risks. Beyond regulatory supervision and financial stability mandates, central banks are now seen as active agents in promoting climate resilience through tools such as green quantitative easing, climate-aligned refinancing operations, and adjustments to collateral eligibility criteria. These measures allow monetary authorities to influence credit allocation toward sustainable sectors and away from carbon-intensive industries. However, the effectiveness, transmission mechanisms, and potential trade-offs of such interventions remain underexplored—especially in emerging and developing economies, where institutional capacities and monetary independence vary widely. Consequently, further empirical research is essential to evaluate how central banks can balance their traditional macroeconomic objectives with the growing imperative of climate risk mitigation.

The second most cited article is authored by (

Liang et al., 2022), with 165 citations. Titled “Climate Policy Uncertainty and World Renewable Energy Index Volatility Forecasting”, and published in Technological Forecasting and Social Change, the study investigates the influence of climate policy uncertainty (CPU) on the volatility of the renewable energy sector. Utilizing the GARCH-MIDAS model, the study successfully identifies the predictive power of CPU in explaining fluctuations in the renewable energy index. In addition to CPU, the authors incorporate eight other uncertainty indices, including economic policy uncertainty and geopolitical risk indices, providing deeper insights into a broader range of factors influencing volatility in the renewable energy sector. Out-of-sample forecast accuracy tests, employing methods such as ROS2, Model Confidence Set (MCS), and Direction-of-Change (DoC), confirm that climate policy uncertainty exhibits stronger predictive capabilities than other uncertainty indices. This indicates that climate policy is not only relevant to energy markets but also plays a critical role in providing assurance for sustainable development across both energy and financial markets. While the study primarily reflects transition risks, particularly those arising from policy shifts or uncertainty, it also indirectly addresses physical risks, noting that delays or ineffectiveness in climate policy implementation may heighten exposure to climate shocks. These findings offer a valuable perspective on how climate-related policy uncertainty affects renewable energy stability and highlight the importance of regulatory clarity in supporting long-term market stability and sustainability.

Ranked third is (

Capasso et al., 2020), with a total of 137 citations. Their article, “Climate Change and Credit Risk”, provides empirical evidence on the relationship between climate change exposure and firm-level credit risk. Utilizing Merton’s structural model, which measures the market-based probability of corporate default through the distance-to-default metric, the authors demonstrate that firms with higher carbon emissions and carbon intensity tend to have lower distance-to-default values, indicating an elevated risk of default, all else being equal (ceteris paribus). The study further finds that this negative relationship becomes more pronounced following key policy events, such as the Paris Agreement, which signal stronger governmental commitments to stricter climate regulations. This underscores the materiality of transition risks—those arising from policy changes, regulatory tightening, and shifts in investor and market expectations during the transition to a low-carbon economy.

While the primary emphasis is on transition risk, the authors also acknowledge the relevance of physical risks stemming from climate-related events such as natural disasters and operational disruptions, which can directly affect firm solvency and asset value. The findings suggest that exposure to climate-related risks significantly influences the creditworthiness of corporate loans and bonds. As a result, the study calls on financial regulators and credit risk modelers to incorporate both transition and physical risks into credit assessment frameworks. Doing so is critical for ensuring the long-term stability and resilience of the banking sector and corporate bond markets in the face of escalating climate challenges.

Capasso et al. (

2020)’s work offers a valuable contribution to the climate–finance literature by quantifying how environmental factors, particularly carbon footprint, impact market perceptions of credit risk, and by advocating for the integration of environmental risk data into mainstream financial risk management practices.

In the bibliometric analysis of this research, after illustrating the percentage distribution of publishers in articles within the Scopus database, the growth in the number of articles published annually from 1988 to 2024, as well as the highest-cited authors, the final stage of the analysis related to climate risk and financial stability using the Scopus database involves a keyword occurrence analysis to categorize and evaluate research subfields. For this analysis, publications were selected if the documents contained the terms “climate risk” AND “financial stability” in the title, abstract, or keywords. As illustrated in

Figure 4, the document selection process was conducted in four stages, encompassing the subject, document type, keyword criteria, and language of published articles, resulting in documents published between 1988 and 2024. Using VOSviewer software and the Binary Counting method, a total of 227 articles were utilized for bibliometric analysis. The results of this analysis are as follows.

The circles depicted on the map represent specific items, with larger circles indicating higher scores for the occurrence of those terms. Items are grouped into clusters marked by the same color. Additionally, the closer the circles are to each other, the more frequently these terms appear together, and the thicker the connecting lines, the more significant their co-occurrence. An exploration of the dominant themes in climate risk and financial stability was conducted using VOSviewer through keyword analysis. This highlights the clear interconnections among factors such as climate change, financial stability, climate risk, sustainable development, macroprudential policy, and other variables present in this research.

In

Figure 4, which illustrates the correlation between climate risk and financial stability, keywords such as sustainable finance and macroprudential policy are also correlated with climate risk. This indicates that climate risk can influence not only financial stability but also how sustainable finance and macroprudential policy are formulated and implemented. Based on keyword frequency, climate change, financial stability, and climate risk appear as mature themes, reflecting their established importance in the literature. In contrast, keywords such as sustainable finance, environmental policy, and central banks show lower co-occurrence, suggesting they are emerging themes gaining scholarly attention. This highlights both well-explored areas and those that warrant further investigation.

Within the context of the relationship between climate risk and financial stability, one notable article that discusses the theoretical framework of this relationship is the study by

Roncoroni et al. (

2021), published in the

Journal of Financial Stability. Titled “Climate risk and financial stability in the network of banks and investment funds”, the article has been cited 94 times. This study develops a comprehensive framework for analyzing how the interaction between climate transition risks and market conditions, such as asset price recovery and volatility affects financial stability.

This study develops a comprehensive framework for analyzing the linkages between climate change risk and financial stability by integrating several models and theories. Drawing on the Climate Stress Testing Framework proposed by (

Battiston et al., 2017), the study examines how climate policy shocks can affect the resilience of financial systems by influencing financial assets through both direct and indirect channels. To further advance the analysis, it incorporates the Network Valuation of Assets (NEVA) framework introduced by (

Barucca et al., 2020), which assesses joint exposures among financial institutions and models contagion effects resulting from systemic interconnections. NEVA helps quantify how distress can propagate through common exposures and contractual obligations.

In addition, the research incorporates models used by (

Roncoroni et al., 2021) to simulate financial contagion. It employs the DebtRank model, which measures the systemic importance of a financial institution by estimating the total economic loss it could trigger across a financial network if it were to fail. The Eisenberg–NOE model is also used to assess how the default of one institution on its interbank obligations may cause cascading failures in the network. Furthermore, the study examines common exposure contagion, where multiple institutions holding similar asset classes experience concurrent losses, as well as distress contagion, which maps the domino effects caused by direct contractual relationships between institutions.

This framework also considers the limitations of traditional risk assessment tools, such as value-at-risk (VaR), which may not adequately capture forward-looking climate risks. By using a network-based approach, the study emphasizes systemic interdependencies and aims to better understand how climate-related risks propagate through financial systems. It also reflects on the influence of international climate policies, particularly the Paris Agreement, and the need for updated systemic risk assessments that account for transition-related exposures. Finally, by applying second-round effects theory and economic shock modeling, supported by the DebtRank and Eisenberg–NOE approaches, the study analyzes how financial contagion may amplify macroeconomic instability. Combined, these frameworks offer policymakers and regulators a more robust toolset for designing effective climate-related financial risk mitigation strategies.

Furthermore, expanding on the broader macroeconomic consequences, a study employing a dynamic CAPM framework with rare disasters, (

Karydas & Xepapadeas, 2022) highlights that climate change not only increases the frequency and unpredictability of extreme events but also significantly raises the climate risk premium. This elevated premium, surprisingly, may not be fully reflected in the overall market risk premium, which combines macroeconomic and environmental risks. The study also supports the hypothesis of a declining real interest rate as the planet warms, while rising climate policy uncertainty reduces the participation of carbon-intensive (“brown”) assets in the market portfolio. These findings underscore the importance of incorporating climate risk into macroeconomic models and evaluating its potential to trigger systemic shocks and global financial contagion.

In addition to macroeconomic disruptions, another important but underexplored dimension of climate-related financial risk is the potential for geopolitical instability, especially in regions vulnerable to resource scarcity. Climate-induced conflicts such as those driven by water shortages, food insecurity, and climate-related migration can have destabilizing effects on national and regional economies. These risks may propagate through global financial networks, influencing investor sentiment, commodity markets, and sovereign credit ratings. Future research should assess the financial system’s exposure to such geopolitical risks and incorporate conflict-related scenarios into climate stress testing frameworks.

Recent developments in the empirical literature also highlight regional variations in the relationship between climate risk and financial stability. These studies offer additional perspectives on how local conditions, diverse financial system structures, and varying policy responses can shape the dynamics between climate risk and financial stability. For instance,

Gaies (

2024) investigates the predictive power of climate-related news encompassing both physical and transition risks on financial instability across the United States, the European Union, and the East and Southeast Asian economies, including China, Japan, and South Korea, over the period 2003–2022. Using advanced time-varying causality methods, the study finds that financial systems in East and Southeast Asia respond more strongly to local and regional climate-related events, underscoring the importance of regional context in understanding climate–financial interactions. These findings reinforce the view that research priorities and financial vulnerabilities differ significantly between developed and developing regions. While studies in advanced economies often emphasize regulatory innovation, green finance instruments, and transition risk disclosures, research from developing regions tends to focus more on adaptation challenges, exposure to physical climate risks, and the lack of institutional capacity to implement climate-resilient financial frameworks.

By examining the interconnections of the variables or keywords in

Figure 4, future research can investigate and analyze the relationships among these variables, identifying research gaps and the analytical frameworks employed based on articles discussing these variables and keywords. Subsequently, in

Table 3, using the same Scopus database related to climate risk and financial stability, the top 15 keywords based on frequency of occurrence are provided as follows:

Table 3 shows that the keyword “climate change” appears 71 times, making it the most frequently used term. The next two most common keywords are “financial stability” (51 occurrences) and “climate risk” (24 occurrences). Other keywords that appear in

Figure 4 include risk assessment, sustainable development, systemic risk, financial system, financial market, environmental economics, finance, sustainability, banking, environmental policy, central banks, and sustainable finance. This indicates that much of the research on climate risk and financial stability centers on the impact of climate change on financial systems. The prominence of “climate change” highlights its central role in financial risk discussions. In other words, researchers often begin their analyses from the climate perspective before examining implications for financial stability. However, the relatively low frequency of keywords such as “climate finance” and “environmental policy” suggests limited research explicitly addressing the role of financial instruments (e.g., green bonds, ESG investments) and regulatory responses. These areas present important opportunities for future exploration.

In addition to the 15 main keywords discussed above, other important but less frequent keywords also emerge, including “green finance”, which appears with fewer than eight occurrences. Notably, this is addressed in the article by (

Behera et al., 2024), titled “Decoupling the role of renewable energy, green finance and political stability in achieving the sustainable development goal 13: Empirical insight from emerging economies”. This study highlights the critical role of green finance in reducing CO

2 emissions across 14 emerging economies from 1990 to 2021. It shows that renewable energy use and green financial instruments significantly contribute to climate risk mitigation. The study further suggests that political stability enhances the effectiveness of green finance, underscoring the necessity of strong institutional frameworks in achieving long-term sustainability. These findings emphasize the importance of exploring how instruments such as green bonds, ESG investments, and carbon markets influence both environmental outcomes and financial system resilience an area that deserves more attention in future research.

To illustrate the evolving interrelationship between keywords related to the variables of climate risk and financial stability over the years,

Figure 5 below will provide further insight.

The keywords appearing from 1988 to 2024 can be observed from the size of each keyword, as seen in

Figure 5. In 2022, the keyword “climate change” was the most prominent, indicating that it was the most frequently used keyword that year. This was followed by the keyword “sustainability” and other variables or keywords. Then, from 2022 to 2023, the keyword “financial stability” became the most significant, showing that it was the most commonly used keyword during that period, followed by “climate risk”, “climate finance”, and other variables or keywords. From the bibliometric literature analysis conducted on climate risk and financial stability, our research findings suggest that financial stability can be influenced by one factor: climate risk. Climate risk refers to the risks arising from climate change that affect financial stability, through both physical and transition risks. Physical risks include the direct impacts of extreme weather events, such as floods, storms, and droughts, which can damage physical assets and reduce investment value. Meanwhile, transition risks involve changes in policies, technologies, and market preferences due to efforts to reduce carbon emissions, which can affect asset values and increase market volatility. According to (

Schumacher et al., 2020) in the

Journal of Sustainable Finance & Investment, transition risks can lead to market dislocations if not managed properly, given the importance of transitioning to a low-carbon economy. The interaction between these risks has the potential to exacerbate instability in the financial system, particularly within interconnected networks of financial institutions, making climate risk management crucial for financial authorities. Next, using the same software, VOSviewer, a bibliometric (density) analysis was conducted using the same database, yielding the results shown in

Figure 6 below.

In

Figure 6, the keyword “climate change” is the largest, indicating that it is the most frequently used keyword. This is followed by the keywords “financial stability” and “climate risk”, along with other variables or keywords. From the bibliometric literature analysis conducted using the Scopus database, the results in

Figure 6 align with the findings in

Figure 4, which utilized articles from the Scopus database, highlighting a significant emphasis on the keywords “climate change”, “climate risk”, and “financial stability”. Additionally, in

Figure 6, keywords with smaller font sizes, such as “climate finance”, “environmental policy”, and “sustainable finance”, indicate that these topics or variables have not been extensively researched and thus present opportunities for further investigation in future research directions.

5. Conclusions

This study provides a comprehensive synthesis of the literature on climate risk and financial stability by systematically answering eight key research questions through a systematic literature review and bibliometric analysis. The number of annual publications on climate risk and financial stability has increased significantly from 1988 to 2024, especially after the adoption of the Paris Agreement in 2015, reflecting growing scholarly attention to the topic. The 2015 Paris Agreement marked a turning point in climate–financial research by formalizing global commitments to climate action, which in turn heightened the urgency for financial institutions and policymakers to understand and mitigate climate-related financial risks. A closer examination of the publication origins reveals that the surge is predominantly driven by studies from developed countries, although contributions from emerging economies have also begun to increase in recent years, particularly in Asia and Latin America.

Research trends indicate a growing focus on the financial implications of both physical and transition climate risks, particularly their effects on market stability, regulatory frameworks, and financial resilience. The most frequently discussed topics include asset pricing under climate uncertainty, the role of macroprudential and public policies, the influence of climate risks on banking and insurance sectors, and the integration of sustainability into portfolio and risk management strategies.

Among the most influential authors in the field is

Dikau and Volz (

2021), with 220 citations, followed by

Liang et al. (

2022), whose work connects climate policy uncertainty with volatility in renewable energy markets. Leading journals that frequently publish on this subject are the

Journal of Financial Stability,

Journal of Cleaner Production,

Finance Research Letters, and

Sustainability, providing interdisciplinary insights that bridge finance, policy, and environmental science. In particular, several studies have begun to examine how specific climate policies such as carbon taxes, emissions trading schemes, and subsidies for green technologies affect financial stability. These policy instruments are found to influence market expectations, asset valuations, and institutional investment behavior, underscoring the importance of integrating policy analysis into climate–finance research. To ensure more effective management of climate-related financial risks across borders, the study emphasizes the urgent need for globally consistent climate risk disclosure frameworks. Harmonized standards can reduce discrepancies in reporting, enhance transparency, and support more informed decision-making by regulators and investors.

Keyword analysis reveals frequent terms such as “climate risk”, “financial stability”, “sustainability”, “risk management”, and “environmental policy”, indicating consistent thematic focus and interconnectedness across studies. The co-occurrence mapping of keywords shows strong linkages among key concepts, particularly climate risk, macroprudential regulation, and sustainable finance, emphasizing the integrated nature of research in this area. Methodologies employed across the most cited articles are diverse, including quantitative approaches such as GARCH-MIDAS models, panel regressions (CS-ARDL, MMQR), network-based stress testing, Merton’s Distance-to-Default models, and climate stress simulations; as well as qualitative and conceptual approaches like document analysis, policy comparisons, systemic risk frameworks, and content analysis.

The study identifies several important research gaps and future directions, including the need for longitudinal and cross-country studies, the development of more robust empirical models to predict climate risk, and a deeper investigation into the role of governance and institutional quality in enhancing financial resilience. Another underexplored area is adaptation finance specifically, how financial systems can support initiatives such as resilient infrastructure, early warning systems, and ecosystem-based adaptation. Future research should evaluate financing mechanisms and investment frameworks that effectively channel capital toward climate adaptation efforts, particularly in vulnerable regions. In addition, an important avenue for future exploration is the integration of Environmental, Social, and Governance (ESG) criteria into traditional risk assessment frameworks to enhance financial system resilience. This approach enables financial institutions to better anticipate and manage long-term sustainability risks by embedding ESG factors into investment decisions, credit risk evaluations, and macroprudential policies.

This study’s limitations include the lack of longitudinal research specifically aimed at evaluating the long-term effects of climate risk on financial stability. Such research is essential to reveal how climate-related risks evolve over time and shape financial outcomes. To address this gap, future studies should implement longitudinal designs that monitor the progression and cumulative impact of climate risks on financial institutions, markets, and regulatory structures. Another limitation is the heavy reliance on secondary data in many existing studies, which can introduce bias and affect analytical accuracy. Moreover, methodological constraints in prior models may fail to capture the complex, dynamic relationships between economic and environmental variables. In addition, this review relies solely on the Scopus database, which, although comprehensive and reputable, has certain limitations. Scopus predominantly indexes English-language publications and journals from certain regions, which may lead to language bias and the underrepresentation of research from linguistically diverse nations, particularly those in Africa, Latin America, and parts of Asia. Consequently, there is an urgent need for future studies to develop more inclusive predictive models, incorporate diverse and multilingual data sources, and further examine the role of public policy in addressing climate-related risks and safeguarding financial stability.

This research offers valuable insights for several key stakeholders. For policymakers, the findings help inform the design of effective climate-related financial regulations and macroprudential policies that address systemic risks. Regulatory bodies, including central banks and financial supervisors, can utilize the identified risk propagation mechanisms and frameworks to improve stress testing and climate risk disclosure requirements. Investors and asset managers may benefit from understanding the financial market implications of climate risks, enabling better portfolio diversification and the integration of environmental risks into investment decisions. By synthesizing diverse perspectives, this study supports more resilient, forward-looking financial systems in the face of climate change.

By offering a structured synthesis of existing literature, this research strengthens our understanding of the evolution, current landscape, and future trajectory of studies at the intersection of climate risk and financial stability. It provides actionable insights for researchers, regulators, and policymakers committed to building more resilient financial systems in the face of accelerating climate change. Then, to further reinforce the contribution of this research, the study encourages stronger interdisciplinary collaboration among the fields of economics, environmental science, and data analytics. Integrating insights from these disciplines can enhance the accuracy of climate risk modeling, improve the development of predictive financial tools, and strengthen policy recommendations through a more holistic understanding of ecological and economic interdependencies. Such collaboration is essential for building adaptive and robust financial systems capable of withstanding complex climate-driven disruptions.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}