A Behavioral Theory of the Income-Oriented Investors: Evidence from Japanese Life Insurance Companies

Abstract

1. Introduction

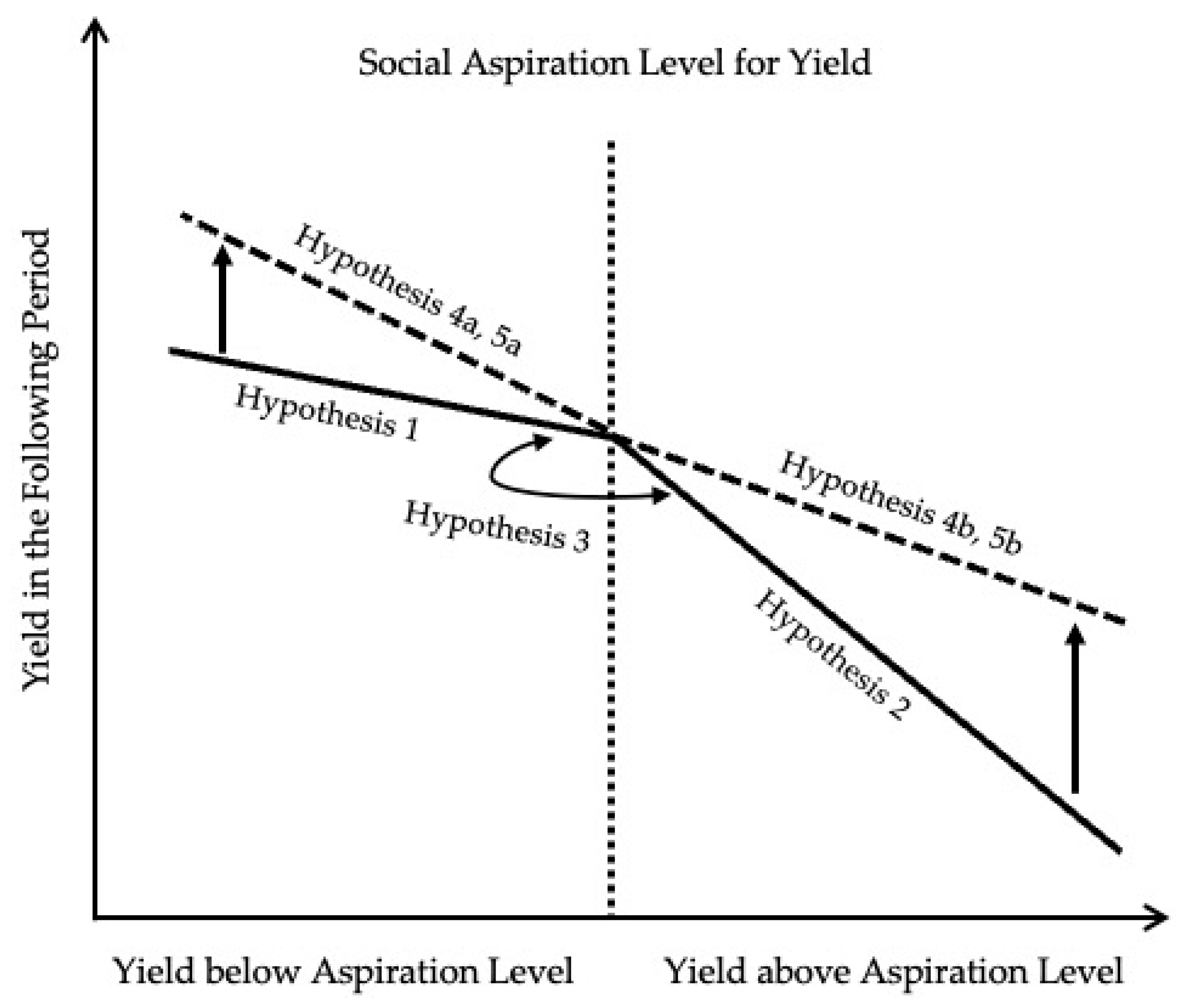

2. Theory and Hypotheses

2.1. Performance Feedback and Aspiration Levels

2.2. Social Aspirations in Asset Management

2.3. Underperforming Social Aspirations

2.4. Outperforming Social Aspirations

2.5. Underperforming Versus Outperforming

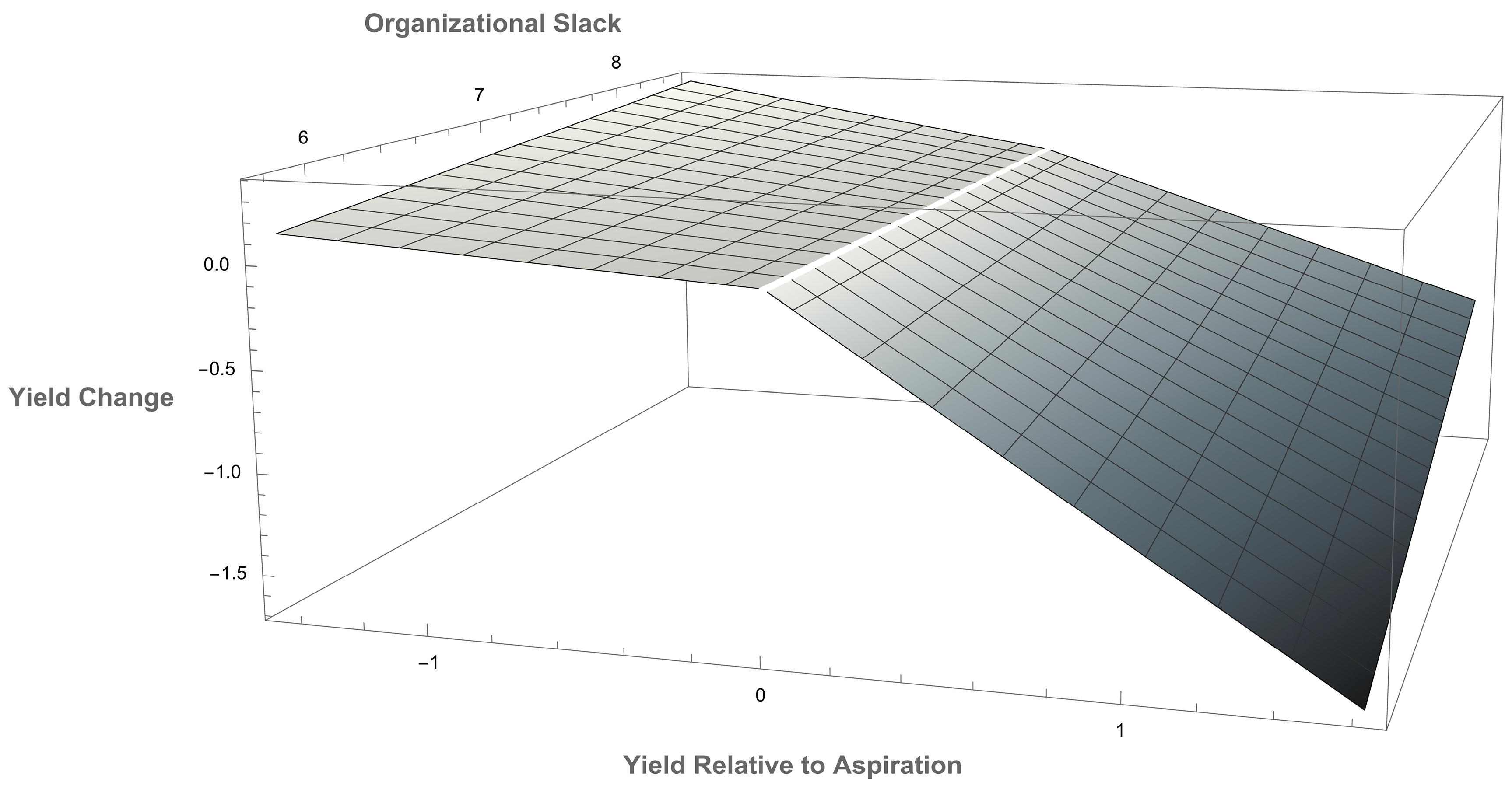

2.6. Moderating Roles of Organizational Slack

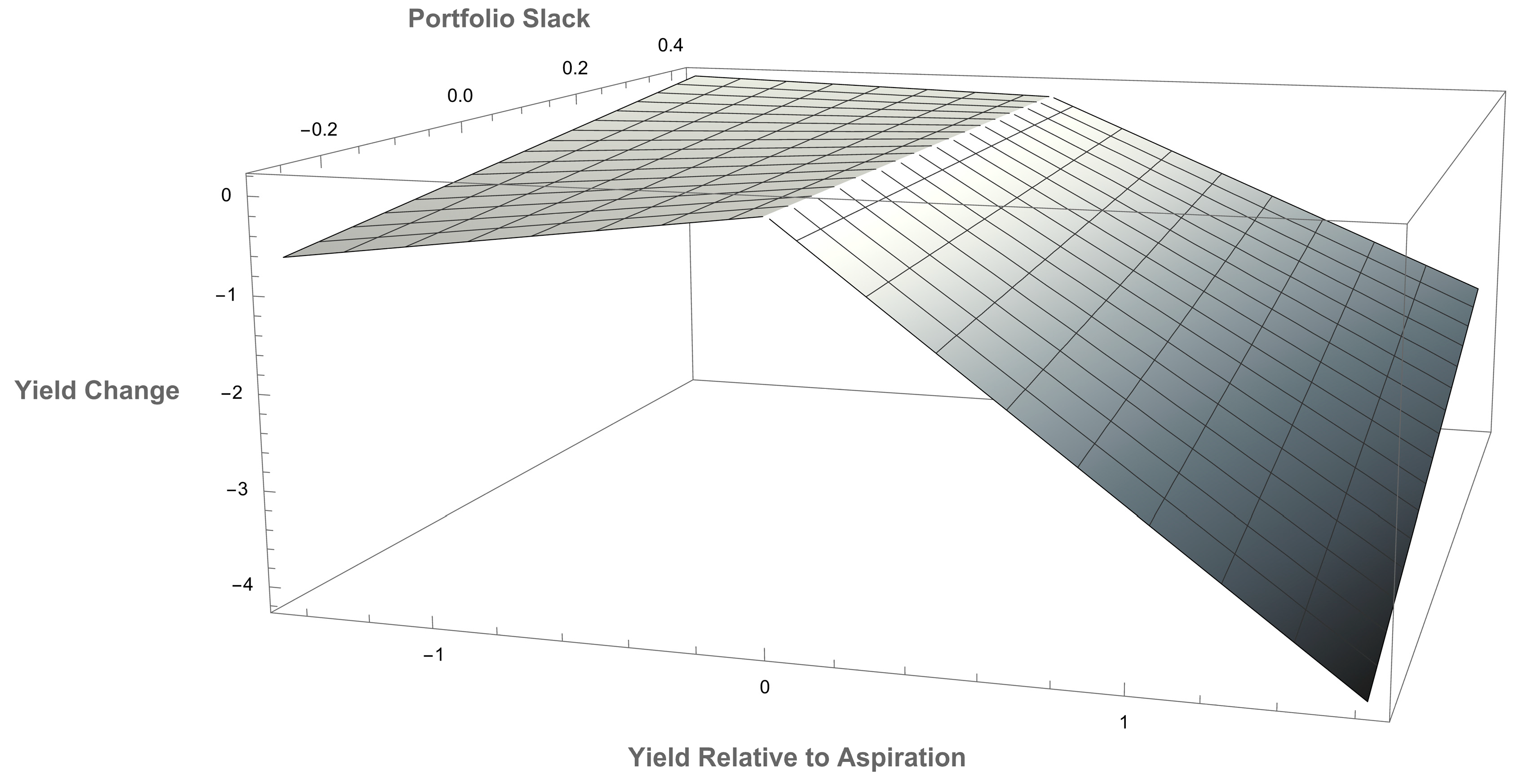

2.7. Moderating Roles of Portfolio Slack

3. Methods

3.1. Sample

3.2. Variables

3.3. Model

4. Results

4.1. Descriptive Statistics and Correlations

4.2. Regression Results

4.3. Robustness Checks and Additional Analyses

5. Discussion

5.1. Main Effects of Performance Feedback

5.2. Moderating and Direct Effects of Slack Resources

5.3. Implications from Robustness Checks

5.4. Contributions

5.5. Practical Implications

5.6. Limitations and Future Research

6. Conclusions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Abbreviations

| VIF | Variance Inflation Factors |

| OLS | Ordinary Least Squares |

| EVS | Economic Value-Based Solvency |

| ALM | Asset-Liability Management |

| QQE | Quantitative and Qualitative Monetary Easing |

| GFC | Global Financial Crisis |

| ROA | Return on Assets |

| M&A | Mergers and Acquisitions |

| JGB | Japanese Government Bond |

| GMM | Generalized Method of Moments |

References

- Allison, P. D. (2009). Fixed effects regression models. SAGE Publications. [Google Scholar]

- Andonov, A., Bauer, R. M., & Cremers, K. M. (2017). Pension fund asset allocation and liability discount rates. The Review of Financial Studies, 30(8), 2555–2595. [Google Scholar] [CrossRef]

- Andraszewicz, S., Kaszas, D., Zeisberger, S., & Holscher, C. (2023). The influence of upward social comparison on retail trading behaviour. Sci Rep, 13(1), 22713. [Google Scholar] [CrossRef] [PubMed] [PubMed Central]

- Audia, P. G., & Greve, H. R. (2006). Less likely to fail: Low performance, firm size, and factory expansion in the shipbuilding industry. Management Science, 52(1), 83–94. [Google Scholar] [CrossRef]

- Audia, P. G., Locke, E. A., & Smith, K. G. (2000). The paradox of success: An archival and a laboratory study of strategic persistence following radical environmental change. Academy of Management Journal, 43(5), 837–853. [Google Scholar] [CrossRef]

- Becker, B., & Ivashina, V. (2015). Reaching for yield in the bond market. The Journal of Finance, 70(5), 1863–1902. [Google Scholar] [CrossRef]

- Bourgeois, L. J., III. (1981). On the measurement of organizational slack. Academy of Management Review, 6(1), 29–39. [Google Scholar] [CrossRef]

- Bromiley, P. (1991). Testing a causal model of corporate risk taking and performance. Academy of Management Journal, 34(1), 37–59. [Google Scholar] [CrossRef]

- Brown, K. C., Harlow, W. V., & Starks, L. T. (1996). Of tournaments and temptations: An analysis of managerial incentives in the mutual fund industry. The Journal of Finance, 51(1), 85–110. [Google Scholar] [CrossRef]

- Cameron, A. C., & Miller, D. L. (2015). A practitioner’s guide to cluster-robust inference. Journal of Human Resources, 50(2), 317–372. [Google Scholar] [CrossRef]

- Chen, W. R., & Miller, K. D. (2007). Situational and institutional determinants of firms’ R&D search intensity. Strategic Management Journal, 28(4), 369–381. [Google Scholar] [CrossRef]

- Chevalier, J., & Ellison, G. (1997). Risk taking by mutual funds as a response to incentives. Journal of Political Economy, 105(6), 1167–1200. [Google Scholar] [CrossRef]

- Choi, J., & Kronlund, M. (2018). Reaching for yield in corporate bond mutual funds. The Review of Financial Studies, 31(5), 1930–1965. [Google Scholar] [CrossRef]

- Cohen, J., & Cohen, P. (1983). Applied multiple regression/correlation analysis for the behavioral sciences (2nd ed.). L. Erlbaum Associates. [Google Scholar]

- Cyert, R. M., & March, J. G. (1963). A behavioral theory of the firm. Prentice-Hall. [Google Scholar]

- Di Maggio, M., & Kacperczyk, M. (2017). The unintended consequences of the zero lower bound policy. Journal of Financial Economics, 123(1), 59–80. [Google Scholar] [CrossRef]

- DiMaggio, P. J., & Powell, W. W. (1983). The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. American Sociological Review, 48(2), 147–160. [Google Scholar] [CrossRef]

- Ellul, A., Jotikasthira, C., & Lundblad, C. T. (2011). Regulatory pressure and fire sales in the corporate bond market. Journal of Financial Economics, 101(3), 596–620. [Google Scholar] [CrossRef]

- Festinger, L. (1954). A theory of social comparison processes. Human Relations, 7(2), 117–140. [Google Scholar] [CrossRef]

- Greve, H. R. (1998). Performance, aspirations, and risky organizational change. Administrative Science Quarterly, 43(1), 58–86. [Google Scholar] [CrossRef]

- Greve, H. R. (2003a). A behavioral theory of R&D expenditures and innovations: Evidence from shipbuilding. Academy of Management Journal, 46(6), 685–702. [Google Scholar] [CrossRef]

- Greve, H. R. (2003b). Investment and the behavioral theory of the firm: Evidence from shipbuilding. Industrial and Corporate Change, 12(5), 1051–1076. [Google Scholar] [CrossRef]

- Greve, H. R. (2003c). Organizational learning from performance feedback: A behavioral perspective on innovation and change. Cambridge University Press. [Google Scholar]

- Greve, H. R. (2008). A behavioral theory of firm growth: Sequential attention to size and performance goals. Academy of Management Journal, 51(3), 476–494. [Google Scholar] [CrossRef]

- Hannan, M. T., & Freeman, J. (1984). Structural inertia and organizational change. American Sociological Review, 49(2), 149–164. [Google Scholar] [CrossRef]

- Iyer, D. N., & Miller, K. D. (2008). Performance feedback, slack, and the timing of acquisitions. Academy of Management Journal, 51(4), 808–822. [Google Scholar] [CrossRef]

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305–360. [Google Scholar] [CrossRef]

- Joseph, J., Klingebiel, R., & Wilson, A. J. (2016). Organizational structure and performance feedback: Centralization, aspirations, and termination decisions. Organization Science, 27(5), 1065–1083. [Google Scholar] [CrossRef]

- Kacperczyk, A., Beckman, C. M., & Moliterno, T. P. (2015). Disentangling risk and change. Administrative Science Quarterly, 60(2), 228–262. [Google Scholar] [CrossRef]

- Kahneman, D., & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. Econometrica, 47(2), 263. [Google Scholar] [CrossRef]

- Kim, J.-Y., Haleblian, J., & Finkelstein, S. (2011). When firms are desperate to grow via acquisition: The effect of growth patterns and acquisition experience on acquisition premiums. Administrative Science Quarterly, 56(1), 26–60. [Google Scholar] [CrossRef]

- Levinthal, D. A., & March, J. G. (1993). The myopia of learning. Strategic Management Journal, 14(S2), 95–112. [Google Scholar] [CrossRef]

- Lindner, F., Kirchler, M., Rosenkranz, S., & Weitzel, U. (2021). Social motives and risk-taking in investment decisions. Journal of Economic Dynamics and Control, 127, 104116. [Google Scholar] [CrossRef]

- March, J. G., & Simon, H. A. (1958). Organizations. Wiley. [Google Scholar]

- Marsh, L. C., & Cormier, D. R. (2001). Spline regression models (Vol. 137). Sage. [Google Scholar]

- Marsh, W. B., & Laliberte, B. (2023). The implications of unrealized losses for banks. Economic Review, 108(2), 27–45. [Google Scholar] [CrossRef]

- Mishina, Y., Dykes, B. J., Block, E. S., & Pollock, T. G. (2010). Why “Good” firms do bad things: The effects of high aspirations, high expectations, and prominence on the incidence of corporate illegality. Academy of Management Journal, 53(4), 701–722. [Google Scholar] [CrossRef]

- Petersen, M. A. (2008). Estimating standard errors in finance panel data sets: Comparing approaches. The Review of Financial Studies, 22(1), 435–480. [Google Scholar] [CrossRef]

- Posen, H. E., Keil, T., Kim, S., & Meissner, F. D. (2018). Renewing research on problemistic search—A review and research agenda. Academy of Management Annals, 12(1), 208–251. [Google Scholar] [CrossRef]

- Shinkle, G. A. (2011). Organizational aspirations, reference points, and goals. Journal of Management, 38(1), 415–455. [Google Scholar] [CrossRef]

- Simon, H. A. (1955). A behavioral model of rational choice. The Quarterly Journal of Economics, 69(1), 99–118. [Google Scholar] [CrossRef]

- Simon, H. A. (1956). Rational choice and the structure of the environment. Psychol Rev, 63(2), 129–138. [Google Scholar] [CrossRef] [PubMed]

- Staw, B. M., Sandelands, L. E., & Dutton, J. E. (1981). Threat rigidity effects in organizational behavior: A multilevel analysis. Administrative Science Quarterly, 26(4), 501–524. [Google Scholar] [CrossRef]

- Tyler, B. B., & Caner, T. (2016). New product introductions below aspirations, slack and R&D alliances: A behavioral perspective. Strategic Management Journal, 37(5), 896–910. [Google Scholar] [CrossRef]

- Wooldridge, J. M. (2013). Introductory econometrics: A modern approach (5th ed.). Cengage Learning. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

| Variable | Mean | S.D. | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1. Yield Change | −0.017 | 0.437 | |||||||||||

| 2. Underperform | −0.348 | 0.553 | −0.154 | ||||||||||

| 3. Outperform | 0.423 | 0.600 | −0.256 | 0.445 | |||||||||

| 4. Organizational Slack b | 7.133 | 0.690 | 0.006 | −0.313 | −0.249 | ||||||||

| 5. Portfolio Slack | 0.072 | 0.174 | −0.004 | 0.005 | −0.012 | −0.011 | |||||||

| 6. Firm Size b | 12.29 | 2.054 | −0.025 | 0.453 | 0.330 | −0.504 | −0.089 | ||||||

| 7. Profitability | −0.030 | 2.056 | 0.010 | 0.095 | 0.029 | −0.231 | 0.001 | 0.225 | |||||

| 8. Firm Age b | 3.219 | 1.087 | −0.025 | 0.499 | 0.316 | −0.525 | 0.019 | 0.599 | 0.085 | ||||

| 9. 3-Year Bonds | 1.110 | 0.502 | −0.044 | −0.083 | 0.019 | 0.025 | −0.086 | −0.083 | −0.026 | −0.146 | |||

| 10. 10-Year Bonds | 1.026 | 0.558 | −0.027 | −0.086 | 0.011 | 0.028 | −0.069 | −0.072 | −0.020 | −0.135 | 0.963 | ||

| 11. 20-Year Bonds | 1.681 | 0.566 | −0.003 | −0.094 | 0.015 | 0.025 | −0.099 | −0.086 | −0.021 | −0.145 | 0.966 | 0.968 | |

| 12. 30-Year Bonds | 1.903 | 0.594 | −0.023 | −0.090 | 0.013 | 0.021 | −0.083 | −0.078 | −0.015 | −0.137 | 0.943 | 0.969 | 0.989 |

| Variable | Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| Firm Size | −0.033 (0.022) | −0.040 (0.027) | −0.052 (0.031) | † | −0.039 (0.026) | −0.051 (0.031) | † | |||

| Profitability | 0.005 (0.007) | 0.006 (0.007) | 0.003 (0.006) | 0.006 (0.007) | 0.003 (0.006) | |||||

| Firm Age | −0.118 (0.076) | −0.143 (0.109) | −0.199 (0.109) | † | −0.128 (0.097) | −0.183 (0.099) | † | |||

| 10-Year Bonds | −0.394 (0.067) | ** | −0.442 (0.098) | ** | −0.479 (0.103) | ** | −0.437 (0.081) | ** | −0.470 (0.086) | ** |

| Underperform | −0.206 (0.115) | † | 0.182 (0.404) | −0.166 (0.121) | 0.227 (0.409) | |||||

| Outperform | −0.713 (0.233) | ** | −2.596 (1.165) | * | −0.814 (0.237) | ** | −2.123 (0.938) | * | ||

| Organizational Slack | −0.152 (0.082) | † | −0.144 (0.087) | |||||||

| Underperform × Organizational Slack | −0.056 (0.052) | −0.056 (0.053) | ||||||||

| Outperform × Organizational Slack | 0.270 (0.147) | † | 0.189 (0.113) | † | ||||||

| Portfolio Slack | −0.947 (0.307) | ** | −0.858 (0.276) | ** | ||||||

| Underperform × Portfolio Slack | −0.889 (0.285) | ** | −0.764 (0.222) | ** | ||||||

| Outperform × Portfolio Slack | 1.816 (0.728) | * | 1.647 (0.637) | * | ||||||

| Year dummies | Yes | Yes | Yes | Yes | Yes | |||||

| R-squared (within) | 0.071 | 0.372 | 0.385 | 0.395 | 0.403 | |||||

| N | 735 | 735 | 735 | 735 | 735 | |||||

| Variable | Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| Firm Size | −0.024 (0.020) | −0.036 (0.031) | −0.042 (0.036) | −0.039 (0.030) | −0.041 (0.035) | |||||

| Profitability | 0.001 (0.004) | 0.002 (0.004) | 0.001 (0.005) | 0.002 (0.004) | 0.001 (0.004) | |||||

| Firm Age | −0.042 (0.066) | −0.083 (0.095) | −0.049 (0.085) | −0.078 (0.108) | −0.047 (0.092) | |||||

| 10-Year Bonds | −0.384 (0.061) | ** | −0.403 (0.071) | ** | −0.397 (0.066) | ** | −0.394 (0.073) | ** | −0.391 (0.068) | ** |

| Underperform | −0.088 (0.061) | −1.379 (0.635) | * | −0.111 (0.059) | † | −1.286 (0.648) | † | |||

| Outperform | −0.742 (0.248) | ** | −3.442 (0.773) | ** | −0.747 (0.269) | ** | −3.435 (0.781) | ** | ||

| Organizational Slack | −0.058 (0.090) | −0.058 (0.091) | ||||||||

| Underperform × Organizational Slack | 0.186 (0.093) | * | 0.170 (0.095) | † | ||||||

| Outperform × Organizational Slack | 0.381 (0.090) | ** | 0.380 (0.089) | ** | ||||||

| Portfolio Slack | 0.100 (0.112) | 0.056 (0.081) | ||||||||

| Underperform × Portfolio Slack | 1.079 (0.902) | 0.726 (0.679) | ||||||||

| Outperform × Portfolio Slack | 0.077 (0.988) | 0.058 (0.804) | ||||||||

| Year dummies | Yes | Yes | Yes | Yes | Yes | |||||

| R-squared (within) | 0.076 | 0.295 | 0.335 | 0.298 | 0.337 | |||||

| N | 698 | 698 | 698 | 698 | 698 | |||||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sasaki, H. A Behavioral Theory of the Income-Oriented Investors: Evidence from Japanese Life Insurance Companies. J. Risk Financial Manag. 2025, 18, 364. https://doi.org/10.3390/jrfm18070364

Sasaki H. A Behavioral Theory of the Income-Oriented Investors: Evidence from Japanese Life Insurance Companies. Journal of Risk and Financial Management. 2025; 18(7):364. https://doi.org/10.3390/jrfm18070364

Chicago/Turabian StyleSasaki, Hiroyuki. 2025. "A Behavioral Theory of the Income-Oriented Investors: Evidence from Japanese Life Insurance Companies" Journal of Risk and Financial Management 18, no. 7: 364. https://doi.org/10.3390/jrfm18070364

APA StyleSasaki, H. (2025). A Behavioral Theory of the Income-Oriented Investors: Evidence from Japanese Life Insurance Companies. Journal of Risk and Financial Management, 18(7), 364. https://doi.org/10.3390/jrfm18070364