1. Introduction

The issue of financial exclusion continues to be an important barrier to equitable development in the global financial landscape, even with all the economic progress we are seeing around the world. A significant segment of the population continues to face challenges in accessing the formal financial system (

Senyo and Osabutey 2020). The World Bank’s 2021 report shows this unequal access to financial services and highlights the necessity for some creative solutions to fix this gap (

Demirgüç-Kunt et al. 2022). FinTech has emerged as a tech-savvy solution to make financial services way more accessible for everyone, especially those who are underserved (

Aleemi et al. 2023;

Senyo and Osabutey 2020).

FinTech is changing the way how individuals handle money. Individuals can now do their financial transactions anytime, anywhere, thanks to FinTech platforms (

Yang and Zhang 2022). Fintech companies are using technology to create easy and innovative channels for financial services. Fintech is a game-changer, especially in places where traditional banking facilities are scarce, which enables individuals to perform financial transactions using their smartphones (

Asif et al. 2023;

Yeyouomo et al. 2023). FinTech services are way more cost-effective than traditional financial services (

Shaikh et al. 2023). That means financial services become more affordable and reachable for a larger group of people, having a real effect on financial inclusion. In developing countries such as India, the support of digital financial literacy is essential to ensure access to financial services. Prominent international organizations such as the World Bank and the United Nations are seeing FinTech as a key player in the fight against poverty and a driver for economic development (

Feyen et al. 2023).

The Digital India policy of the government and the technology adoption mindset of people have sparked a digital financial services boom in the context of India (

Vyas and Jain 2021). The Global Findex database of 21 reveals that 24 percent of adults worldwide were unbanked globally and 30 percent in India (

Paul 2022). In India, around 35 percent of the population uses digital methods of transactions though over 70 percent have bank accounts. Government initiatives such as UPI, AePS, Bharat QR code, and BHIM are transforming how individuals and businesses handle their money, which has a real impact on improving financial inclusion (

Asif et al. 2023). However, the swift adoption of FinTech services has presented new challenges. Users face risks such as identity theft, privacy problems, unregulated service providers, and security issues (

Jangir et al. 2022;

Nasir et al. 2023). In response to these challenges, the role of digital financial literacy (DFL) becomes important, which involves knowledge about FinTech products and their management (

Ravikumar et al. 2022).

A distinction should be made between ‘digital literacy’ and ‘financial literacy’. While financial literacy is related to the ability of an individual to understand the fundamentals of economics and finance that help in making financial decisions, digital literacy is concerned with an individual’s proficiency in using digitally delivered financial products (

Prete 2022). Financial literacy thus focuses on the knowledge itself and the ability of an individual to acquire financial knowledge, whereas using technologies to create, evaluate, and acquire cognitive and technical skills to use digital technology is called ‘digital financial literacy’ (

Zait and Bertea 2014).

For the purpose of using FinTech services effectively, education in the digital age must include digital financial literacy (

Morgan et al. 2020). Even individuals with a reasonable amount of financial literacy may face difficulty in using FinTech services without adequate digital financial literacy (

Kakinuma 2022). In this study, it is acknowledged that digital financial literacy has a substantial impact on the widespread usage of FinTech services. This underscores the necessity of a concise evaluation of digital financial literacy that accommodates unique opportunities and challenges presented by digital finance, in addition to traditional financial literacy.

This study is going to explore the relationship between FinTech and financial inclusion, considering digital financial literacy as a mediator and perceived regulatory support as a moderator. Previous studies on FinTech have focused on factors related to adoption of FinTech services or the direct effect of FinTech on financial inclusion (

Alrawad et al. 2023;

Asif et al. 2023;

Bajunaied et al. 2023;

Savitha et al. 2022;

Shaikh et al. 2023;

Xie et al. 2021). As far as our knowledge extends, there is a gap in the research concerning the examination of digital financial literacy as a mediator in the FinTech use and financial inclusion relationship. By understanding the crucial role of digital financial literacy in FinTech-enabled financial inclusion, this study intends to evaluate the mediating function of digital financial literacy in the pathway from FinTech use to financial inclusion. Previous research on perceived regulatory support has primarily focused on its direct effects on FinTech adoption (

Ng and Kwok 2017;

Nugraha et al. 2022). This study selects perceived regulatory support as a key moderator because its presence is essential for customers to use FinTech to meet their day-to-day financial needs. Perceived regulatory support (PRS) is defined as the extent to which individuals engaged in FinTech activities believe that the regulatory environment is supportive, transparent, and capable of safeguarding their interests (

Chandra et al. 2010;

Khan et al. 2023). It denotes the subjective perceptions and levels of confidence that participants have in the legal framework, which is crucial for FinTech adoption (

Madan and Yadav 2016).

This study makes three significant contributions to the literature in behavioral finance. Firstly, it provides evidence indicating that the adoption of FinTech alone does not lead to improved financial inclusion. The association between FinTech usage and financial inclusion is indirect and complex, and a positive relationship is possible with the involvement of mediating and moderating factors. Secondly, the FinTech use and financial inclusion relationship is mediated by digital financial literacy, emphasizing the significance of digital financial literacy in our contemporary, progressively digitized society. Thirdly, the research discloses a notable moderating impact of perceived regulatory support on FinTech-enabled financial inclusion. People who believe there is strong regulatory support are more likely to use FinTech services with confidence to meet their financial needs. This sense of regulatory support fosters confidence that FinTech services are perceived to be subject to strict government regulation to protect the interests of consumers. The goal of this study is to provide valuable insights that can guide the development of strategies to enhance FinTech-enabled financial inclusion, through the analysis of these key elements. In addition, this study aims to contribute to the domain of our present knowledge related to FinTech usage and financial inclusion and offer practical recommendations for both industry stakeholders and policymakers.

The paper’s remaining segments are arranged in the following order:

Section 2 undertakes a literature review, theoretical foundations, and hypotheses development.

Section 3 outlines the data and methodology utilized in this study.

Section 4 shows the results and provides an explanation of their implications.

Section 5 includes the conclusion, study limitations, and suggestions for further work.

2. Theoretical Foundation, Review of Literature, and Hypothesis Development

2.1. Theoretical Foundation

The present study is grounded in the theoretical frameworks of the Unified Theory of Acceptance and Use of Technology (UTAUT2) (

Venkatesh et al. 2003) and the Value-based Adoption Model (VAM) (

Kim et al. 2007). These models serve as the theoretical underpinnings for the research. UTAUT2 helps us to understand the factors influencing behavioral intentions of adopting and using technology in the human–computer interface (

Gansser and Reich 2021;

Kilani et al. 2023). Prior researchers have used the UTAUT2 framework in assessing and predicting technology adoption in various contexts (FinTech use, mobile apps, and information systems) (

De Blanes Sebastián et al. 2023;

Ong et al. 2023). This study employs the UTAUT2 framework as a theoretical perspective due to its effective explanatory capabilities.

This study also builds on the Value-based Adoption Model (VAM) (

Kim et al. 2007) in explaining the proposed hypothesized relationships in this study. The gist of VAM is that individuals’ use of new technology largely depends on the perceived advantages and disadvantages of adopting new technology (

Jun et al. 2018)—customers intention and adoption of FinTech hinges upon value-based adoption (

Lee et al. 2015). Since trust, service quality, and perceived security add value to adopting new technology, i.e., FinTech, we applied VAM in this study. Furthermore, digital financial literacy and perceived regulatory support enhance the value. Some of the contemporary researchers also used VAM in explaining FinTech adoption (

Hasan et al. 2021b). Thus, this research uses both UTAUT2 and VAM in FinTech adoption by individuals.

2.2. Trust and FinTech Use

Trust, in the context of FinTech services, denotes the faith or assurance that users place in the safety, dependability, and ethical conduct of financial technology platforms (

Alrawad et al. 2023). Studies consistently demonstrate that trust has a strong influence on individuals’ willingness to utilize FinTech platforms (

Bajunaied et al. 2023;

Savitha et al. 2022;

George and Sunny 2021;

Roh et al. 2022). This is especially relevant in the payment service domain, where maintaining a significant level of trust is considered crucial due to the frequent incidents of fraudulent activities, posing financial risks (

Kilani et al. 2023). If users have a high level of trust in a FinTech platform, they are inclined to embrace and utilize it for their financial requirements (

Nugraha et al. 2022). Confidence regarding the protection, privacy, and integrity of digital products is heightened while users place trust in FinTech platforms (

Zhang et al. 2023). Consumers who have trust in FinTech platforms perceive lower risks associated with utilizing these services (

Shahzad et al. 2022). Users who have trust in a platform are more likely to remain loyal to it, engaging in repeated use of the services and possibly referring it to others (

Bajunaied et al. 2023). Among the primary determinants of users’ attitudes and behaviors toward FinTech services, trust stands out as a fundamental factor (

Zarifis and Cheng 2022). It contributes to user confidence, increases user loyalty, diminishes perceived risk, and promotes positive word-of-mouth (

Amnas et al. 2023;

Savitha et al. 2022;

Wang et al. 2019). Based on the empirical evidence, the following hypothesis was formulated.

H1. Trust significantly and positively influences the use of FinTech services.

2.3. Service Quality and FinTech Use

Service quality is defined as the overall benefit or superiority of a service in meeting customer expectations (

George and Sunny 2021). The acceptance and continued use of FinTech platforms can be significantly impacted by users’ perception of the quality of services offered (

Ahmed et al. 2021;

George and Sunny 2023). Customer satisfaction with FinTech services is associated with service quality (

Gautam and Sah 2023). The degree to which FinTech platforms are adopted and used can be significantly influenced by users’ experience of reliable, efficient, and fulfilling interactions with a FinTech platform (

Ahmed et al. 2021;

George and Sunny 2023). When the users believe FinTech services exceed their expectations in terms of quality, they are more likely to use them (

Ghosh 2018). The customers evaluate the value they receive from FinTech, based on the quality of the services (

Patnaik et al. 2023). Higher service quality contributes to a positive perception of value, which encourages them to keep using services (

Roh et al. 2022). High service quality includes secure and reliable services, which positively influence users’ confidence in the digital platform (

Mujinga 2020). Customer loyalty and sustainable use of FinTech services are facilitated by positive perception of service quality, which also contributes to satisfaction and overall positive user experiences (

George and Sunny 2023;

Gautam and Sah 2023;

Sultana et al. 2023). As a result, the following hypothesis was framed.

H2. Service Quality significantly and positively influences the use of FinTech services.

2.4. Perceived Security and FinTech Use

In the context of FinTech, perceived security refers to individuals’ subjective assessment of the safety and protection associated with their financial data and transactions (

Chandra et al. 2010;

Nasir et al. 2023). Customer confidence in FinTech platforms is directly influenced by their perception of security (

George and Sunny 2023). High levels of perceived security of users contribute to greater reliability of FinTech platforms, which is necessary for FinTech use (

Putri et al. 2023). Using FinTech services will be less risky for users if they are confident that their financial information is secure (

Jangir et al. 2022). Secure FinTech experiences contribute to customer retention and lower perception of risk (

Bajunaied et al. 2023). If users feel that their data are secure, they are more inclined to remain loyal to FinTech platforms (

Zhang et al. 2023). The common barriers to the utilization of FinTech such as concern about identity theft, data breaches, and unauthorized access can be eliminated by improving the perception of security (

Bajunaied et al. 2023;

Lim et al. 2019;

Meng et al. 2019;

Nasir et al. 2023). Hence the following hypothesis was proposed, based on the literature mentioned above.

H3. Perceived security significantly and positively influences the use of FinTech services.

2.5. FinTech Use and Financial Inclusion

FinTech makes it possible for customers in underserved or rural locations to obtain financial services via digital platforms, doing away with the necessity for physical bank branches (

Arner et al. 2020;

Shaikh et al. 2023;

Yang and Zhang 2022). FinTech is making financial services both convenient and budget-friendly. FinTech can cut down the costs associated with traditional banking (

Shen et al. 2020). So, FinTech is not just for tech-savvy customers; it is making financial services way more affordable for underserved people. This opens up the door for those who might not have been part of a formal financial system to start using FinTech services and become part of a formal financial system (

Bongomin and Munene 2021;

Senyo and Osabutey 2020). FinTech is helping small businesses and individuals who might not qualify for traditional loans to receive financial assistance through microfinance and peer-to-peer lending services. This sparks more economic activity and entrepreneurship in underserved communities (

Björkegren and Grissen 2018;

Yue et al. 2022). FinTech companies collaborate with the government to make initiatives for financial inclusion, which facilitate the disbursement of social benefits, subsidies, and other financial assistance effectively to the people (

Asif et al. 2023). FinTech is breaking down the barriers that used to keep people away from formal financial systems and using tech magic to make it more accessible (

Aleemi et al. 2023;

Yeyouomo et al. 2023). In the light of the literature mentioned above, the following hypothesis was developed.

H4. The use of FinTech services significantly and positively influences financial inclusion.

2.6. FinTech Use and Digital Financial Literacy

FinTech platforms provide educational content like articles, videos, and tutorials related to finance within their websites or apps. They are breaking down financial concepts and investment strategies and covering all kinds of useful topics to boost the financial literacy of the users (

He et al. 2024;

Kumar et al. 2023;

Setiawan et al. 2022). Some of these apps even provide budgeting and financial management tools, helping users track spending, set goals, and manage finances more effectively (

Carè et al. 2023;

Uthaileang and Kiattisin 2023). These FinTech companies use artificial intelligence (AI) to provide personalized financial advice (

Zarifis and Cheng 2022). It is like having a virtual money guru helping you make savvy decisions (

Gautam et al. 2022;

Shen et al. 2018). FinTech apps make learning about finance joyful by adding game elements (

Lai and Langley 2023). Users can play around with virtual financial activities, gain some real-world experience, and level up their financial know-how in a risk-free way (

Kakinuma 2022;

Şenol and Onay 2023). FinTech platforms facilitate community engagement, where users can chat with other users, share experiences, pose inquiries, and gain knowledge from one another (

Ravikumar et al. 2022). A collaborative learning environment is fostered by this sense of community, especially for individuals who are new to digital financial tools (

Malladi et al. 2021). Hence the following hypothesis was proposed.

H5. Use of FinTech services significantly and positively influences digital financial literacy (DFL).

2.7. Digital Financial Literacy and Financial Inclusion

Digital financial literacy (DFL) provides people with the knowledge and understanding of financial technology, promoting greater awareness and comprehension of digital financial services, which ultimately leads to digital financial inclusion (

Choung et al. 2023;

Malladi et al. 2021). Digital financial literacy enhances people’s ability to effectively mitigate potential risks, and it has positive influence on individuals’ perception of risks associated with using digital services (

Kumar et al. 2023;

Panos and Wilson 2020). Higher levels of digital financial literacy generate greater confidence in using digital financial services, which contributes to a positive attitude toward the formal financial system (

Lyons and Kass-Hanna 2021). Digital financial literacy plays a crucial role in empowering individuals to make informed decisions through the use of digital financial services, facilitating their greater integration into the digital financial landscape (

Prasad et al. 2018;

Shen et al. 2018). Digital financial literacy has a favorable influence on financial inclusion by encouraging greater use of digital services, empowering people to make informed decisions, raising security awareness, and enhancing decision-making in digital transactions (

Hasan et al. 2021a;

Ravikumar et al. 2022;

Uthaileang and Kiattisin 2023). The following hypothesis was put forward in light of the earlier empirical research.

H6. Digital financial literacy (DFL) significantly and positively influences financial inclusion.

2.8. Digital Financial Literacy as a Mediator

Previous research studies indicate FinTech use and financial inclusion have a complex relationship that is influenced by various factors (

Sampat et al. 2023;

Yue et al. 2022;

Wang 2023).

Bongomin and Ntayi (

2020) found that digital consumer protection acted as a mediator in the pathway from FinTech adoption to financial inclusion. In a similar vein,

Al-Slehat (

2023) discovered digital marketing acts as a mediator in the FinTech usage and financial inclusion relationship. However, a detailed analysis of the literature revealed a research gap; none of the studies had looked at digital financial literacy as a mediator in the connection between FinTech use and financial inclusion. This study asserts that the use of FinTech not only has direct impact on financial inclusion but also exerts an indirect effect through digital financial literacy. Digital financial literacy significantly aids FinTech-enabled financial inclusion by empowering individuals with the capabilities and guidance required to proficiently use digital platforms (

Kumar et al. 2023;

Panos and Wilson 2020;

Ravikumar et al. 2022). However, the direct effects of FinTech on financial inclusion are well documented in the existing literature, but no prior study has, as far as we are aware, examined the indirect pathway of FinTech through digital financial literacy. Considering the available literature, the following exploratory mediation hypothesis was formulated.

H7. Digital financial literacy mediates the relationship between FinTech use and financial inclusion.

2.9. Perceived Regulatory Support as a Moderator

In the context of FinTech services, perceived regulatory support denotes the individuals’ subjective beliefs about the degree of encouragement, support, and regulatory environment that the government offers (

Chandra et al. 2010;

Khan et al. 2023). Following the VAM, we argue that users’ perceptions of regulatory support play a crucial role in contributing to the reliability and confidence that individuals have in FinTech platforms (

Nugraha et al. 2022). FinTech platforms are trusted by users if they perceive that regulators support and endorse them (

Madan and Yadav 2016;

Xia et al. 2023). When users are confident that their financial transactions are conducted within a regulated and secure environment, they are more likely to use these digital services (

Ediagbonya and Tioluwani 2023;

Ng and Kwok 2017). Perceived regulatory support implies that there are regulations and mechanisms in place to protect the rights and interests of consumers (

Brown and Piroska 2022). When consumers believe that regulatory bodies are actively monitoring and enforcing consumer protection laws, they are more willing to utilize FinTech services (

AlBenJasim et al. 2023). This assurance promotes the broader use of FinTech, especially among those who have limited access to traditional banking services (

Otieno and Kiraka 2023). Perceived regulatory support acted as a critical factor in facilitating the integration of FinTech services into the formal financial system, thereby contributing to the inclusion of more individuals in mainstream finance (

Bu et al. 2022). This study argues that the connection between FinTech use and financial inclusion is subject to moderation by the perception of regulatory support. Lack of research on the moderating effect of perceived regulatory support was identified; it would be interesting to see how perceived regulatory support affects the strength of the positive association between FinTech usage and financial inclusion. Consequently, the following exploratory moderating hypothesis based on the limited empirical evidence, was formulated.

H4a. Perceived regulatory support moderates the relationship between FinTech use and financial inclusion such that higher (lower) levels of perceived regulatory support are associated with stronger (weaker) relationship between FinTech use and financial inclusion.

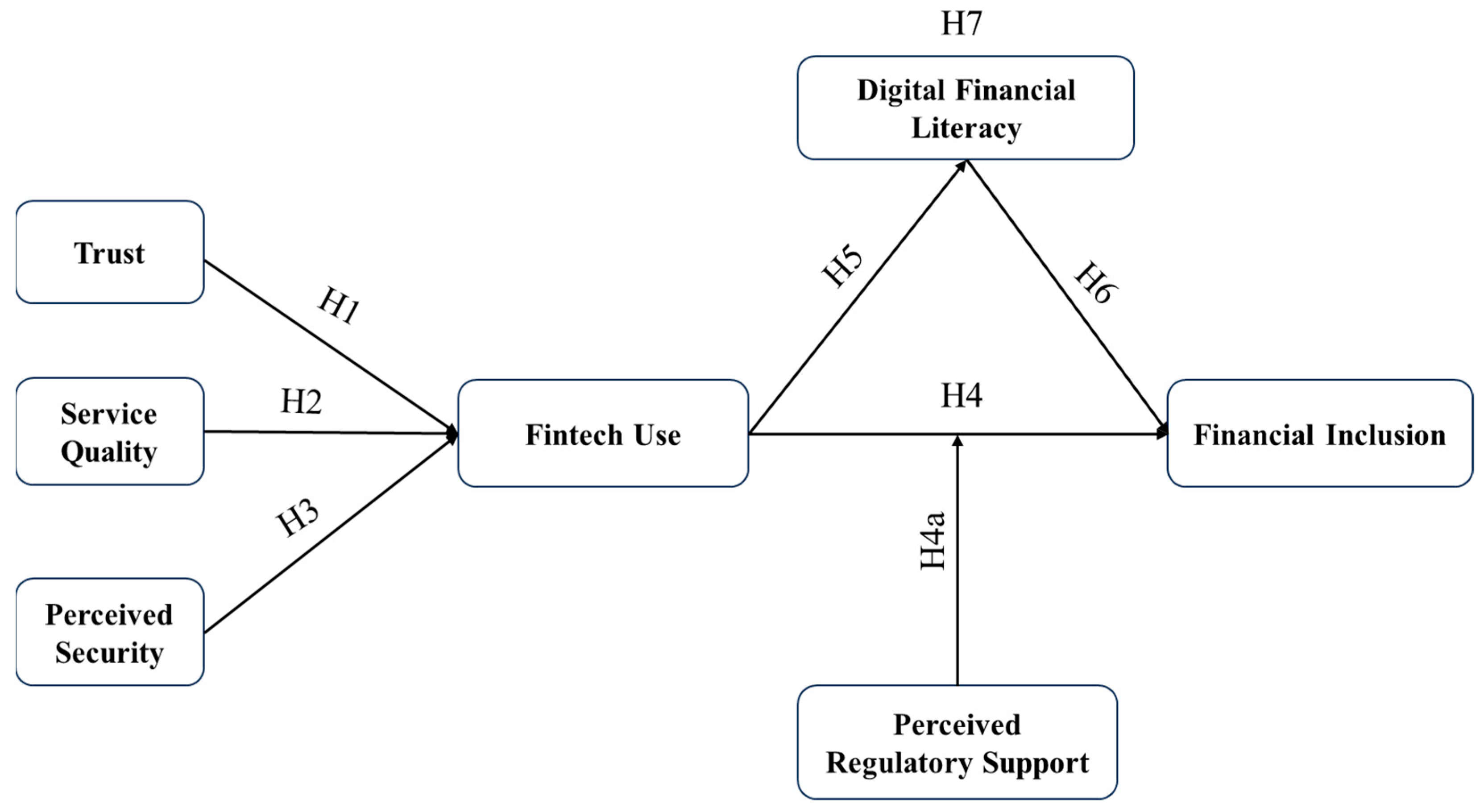

The conceptual model is presented in

Figure 1.

3. Research Methodology

3.1. Measurement Development

A research framework was created in order to meet this study’s goals, and it is depicted in

Figure 1. This study employed seven variables, which were assessed by using different items, adapted from the existing literature (

Appendix A). The variable, trust, was measured by using items adapted from

Singh and Srivastava (

2018) and

Kumar et al. (

2018), and items for evaluating perceived security were taken from

George and Sunny (

2023). The measures of service quality were modified from

Zhou (

2013), while items evaluating perceived regulatory support were borrowed from

Chandra et al. (

2010). Items for measuring the variable FinTech use were adapted from the previous study by

Venkatesh et al. (

2012). The variables utilized in this study were assessed through multiple items derived from the existing literature, and they were then adjusted to suit the specific research context. The items employed to gauge FinTech usage were adapted from

Venkatesh et al. (

2012). Users primarily utilize FinTech platforms for four main types of services: payment services, investment or wealth management services, credit services, and insurance services. In this study, we employ the items from

Venkatesh et al. (

2012) to measure these four types of services. For example, the statement ‘I leverage FinTech investment platforms to oversee my investment portfolio’ is employed to assess whether users utilize FinTech for managing their investments. A recently conducted study on FinTech use by

Xia et al. (

2023) employed the same measure to tap the FinTech construct. Furthermore, previous scholars (e.g.,

Xie et al. 2021) measured the variable of wealth management by adapting items from

Venkatesh et al. (

2012). Additionally,

Senyo and Osabutey (

2020) and

George and Sunny (

2023) also utilized items from

Venkatesh et al. (

2012) to measure mobile money usage behavior and mobile wallet continuous intention, respectively. Similarly, in this study, we used items from

Venkatesh et al. (

2012) to measure the utilization of FinTech platforms.

The items used to test digital financial literacy were modified from those developed by

Ravikumar et al. (

2022), and those items related to financial inclusion were taken from

Bongomin and Ntayi (

2020). A five-point Likert scale with the values of ‘strongly disagree’ to ‘strongly agree’ was employed to assess each measurement item.

The questionnaire was divided into two sections: the first was used to gather demographic data, while the second was designed to garner respondents’ opinions about each variable in the research model. Before collecting data, we received informed consent from the respondents and assured them about the anonymity of their responses. We adhered to ethical guidelines when gathering data. The questionnaire was finalized after careful scrutinization and confirmation by two persons from the FinTech industry and four academic experts. Each survey item was assessed by the experts for clarity and understandability. They considered factors such as the use of language, possible ambiguity, and the suitability of terminology for the intended audience. To confirm that the measurement tool was suitable, a pilot study with thirty people was tested before administering the questionnaire to the intended participants. Some items were modified after the pilot test in response to the initial validity evaluation of the pilot sample. Notably, some survey items were modified to enhance clarity and mitigate the likelihood of participant misunderstanding. To improve the flow and continuity of the survey, structural changes were also made, such as the order of questions. We also ensured that the survey instrument was very long so that the mandatory questions in Google Forms do not discourage the respondents from filling out the form dispassionately.

3.2. Sample and Data Collection

The research focuses on people, who were engaged with FinTech services in India. The organized survey instrument was made with Google Forms and distributed to individuals using FinTech platforms. The lack of information regarding the population that used FinTech services led to the employment of the convenience sampling method, which was suggested by previous research (

Alrawad et al. 2023;

Kakinuma 2022;

Kilani et al. 2023;

Senyo and Osabutey 2020). The three months, ranging from September 2023 to November 2023, were used for data collection. In the non-availability of a predefined list of individuals using FinTech, we followed the snowball sampling technique of data collection by using Google Forms and sent the link to various social media platforms (email, WhatsApp, and Facebook). The first respondents were requested to spread the survey instrument widely to obtain a large sample. During the pandemic and post-pandemic period, several researchers used Google Forms to collect data considering health-related issues and periodical social distancing problems, and we followed an approach that is consistent with the contemporary method of data collection.

We received 608 fully completed questionnaires. Google Forms gives the option to mark questions as mandatory, which forbids respondents from moving forward without answering all questions. Using the G*Power software version 3.1, researchers have calculated the sample size required to meet this study’s objectives (

Faul et al. 2007). In this study, the model comprised five predictors. A sample size of 138 was recommended by the software with a power level of 0.95 and an effect size of 0.15. This study’s actual sample size of 608 was more than four times larger than the required size. By comparing the first 75 respondents with the last 75 respondents, we assessed for non-response bias and discovered no notable distinction between these two groups. The respondents’ demographic details are shown in

Table 1.

4. Data Analysis and Results

To conduct measurement and structural model analyses, we used the partial least squares structural equation model (PLS-SEM). This study’s data analysis was performed by using Smart PLS version 4.0 (

Hair et al. 2019)

4.1. Common Method Bias (CMB) Test

To ascertain the potential existence of CMB in the data, the data were thoroughly investigated for collinearity, to ensure its absence. The term ‘common method bias’ (CMB) describes a potential source of bias in research data that results from the commonality of the data collection method rather than from the constructs to be measured. Harman’s one-factor test (

Podsakoff et al. 2003) was used to conduct the common method bias (CMB) test. The findings indicated that only 48.55% of the variance in the research data was accounted for, and it was less than the critical threshold of 50%. A full collinearity test was also performed to evaluate CMB thoroughly. The findings revealed that the VIF values for all variables were below 3.3, as suggested by

Kock (

2015). In other words, the dataset showed no signs of CMB.

4.2. Assessment of Measurement Model

The foundational aspect of structural equation modeling relies on the measurement model. It ensures the validity and reliability of instruments in effectively capturing the constructs (

Hair et al. 2021). The composite reliability and Cronbach’s alpha scores were assessed to ensure the internal consistency and reliability of each construct. In general, satisfactory reliability is attained when the value of Cronbach’s alpha coefficient and composite reliability exceeds the threshold of 0.70 (

Henseler et al. 2016). As per

Table 2, values of Cronbach’s alpha coefficients and composite reliability ranged from 0.816 to 0.913, and it confirmed the internal consistency and reliability of the constructs.

A construct’s AVE value needs to be higher than 0.50 in order to exhibit convergent validity (

Hair et al. 2021). A strong convergent validity is evident from

Table 2 as all variables in the research model reported AVE values greater than 0.50. To assess discriminant validity, the Fornell–Larcker Criterion was used in the research (

Fornell and Larcker 1981).

Table 3 demonstrates that the square route of AVE values consistently surpasses the correlations between any two constructs under study. This finding established the discriminant validity of this study by the guidelines provided by

Hair et al. (

2021). Furthermore, we evaluated multicollinearity using variance inflation factors (VIFs). The VIF values varied from 1.551 to 2.656 in our study, which were less than the suggested threshold value of 3 (

Hair et al. 2021). Consequently, we do not find any significant multicollinearity issues in our dataset.

4.3. Assessment of the Structural Model

We proceeded to evaluate the hypotheses of the research after establishing the validity of the measurement model.

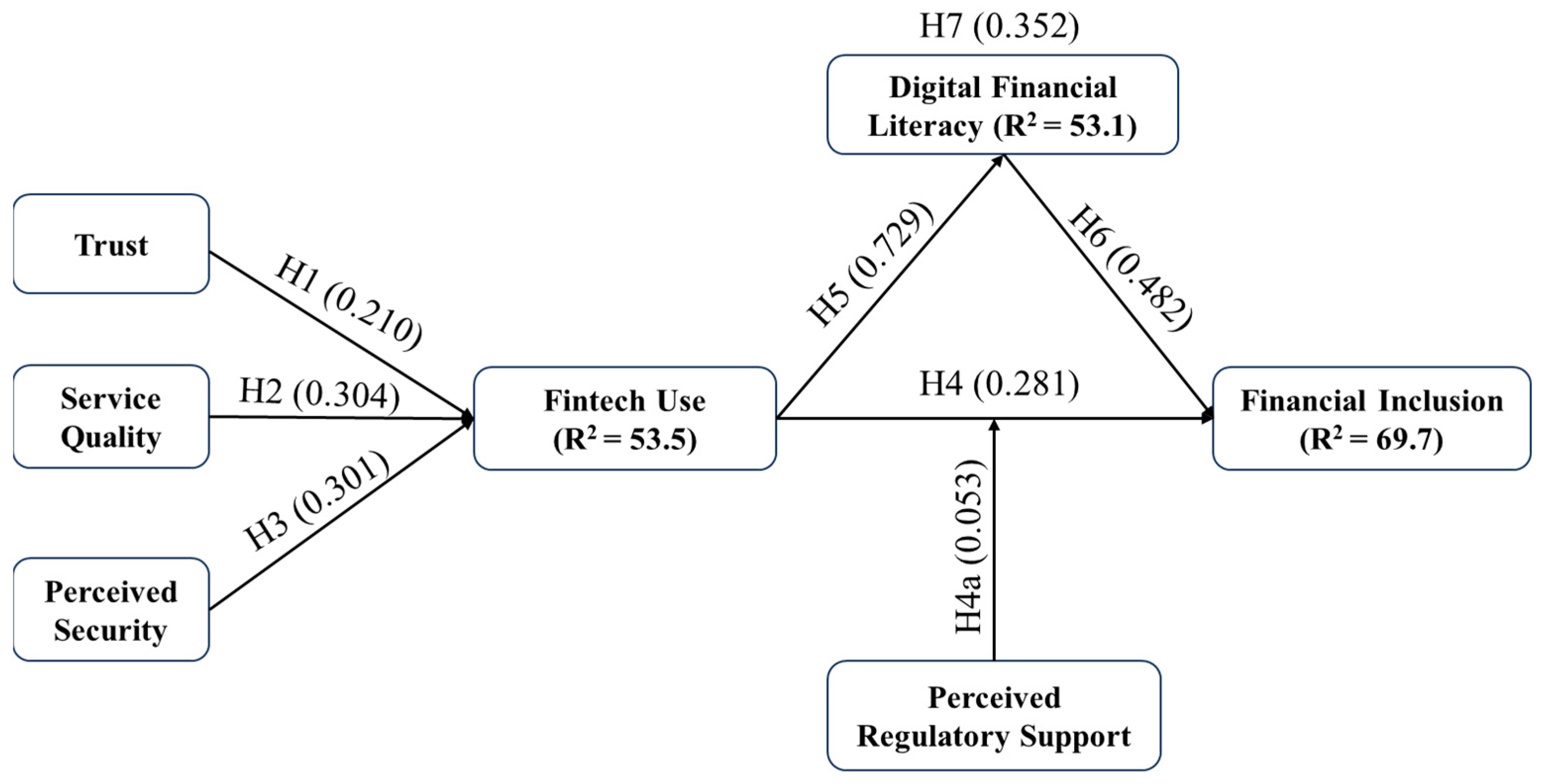

Table 4 presents the results of the hypotheses test, which revealed significant positive effects of trust (β = 0.210;

p < 0.001), service quality (β = 0.304;

p < 0.001), and perceived security (β = 0.301;

p < 0.001) on FinTech use; therefore, H1, H2, and H3 were accepted. Similarly, the results indicated that FinTech use (β = 0.281;

p < 0.001) exerted a positive and significant impact on financial inclusion. Hence, H4 was supported. Regarding the relationship between FinTech use and digital financial literacy, the results indicated that FinTech use had significant positive impact on digital financial literacy (β = 0.729;

p < 0.001), which validated H5. The findings also demonstrated the significant effect of digital financial literacy on Financial Inclusion (β = 0.482;

p < 0.01), thereby supporting H6. The findings indicated a substantial mediation effect of digital financial literacy (β = 0.352;

p < 0.001) in the FinTech use and financial inclusion relationship; therefore, H7 was supported.

The results also demonstrated that the FinTech use and financial inclusion relationship has the moderation effect of perceived regulatory support (β = 0.053;

p < 0.01), supporting H4a.

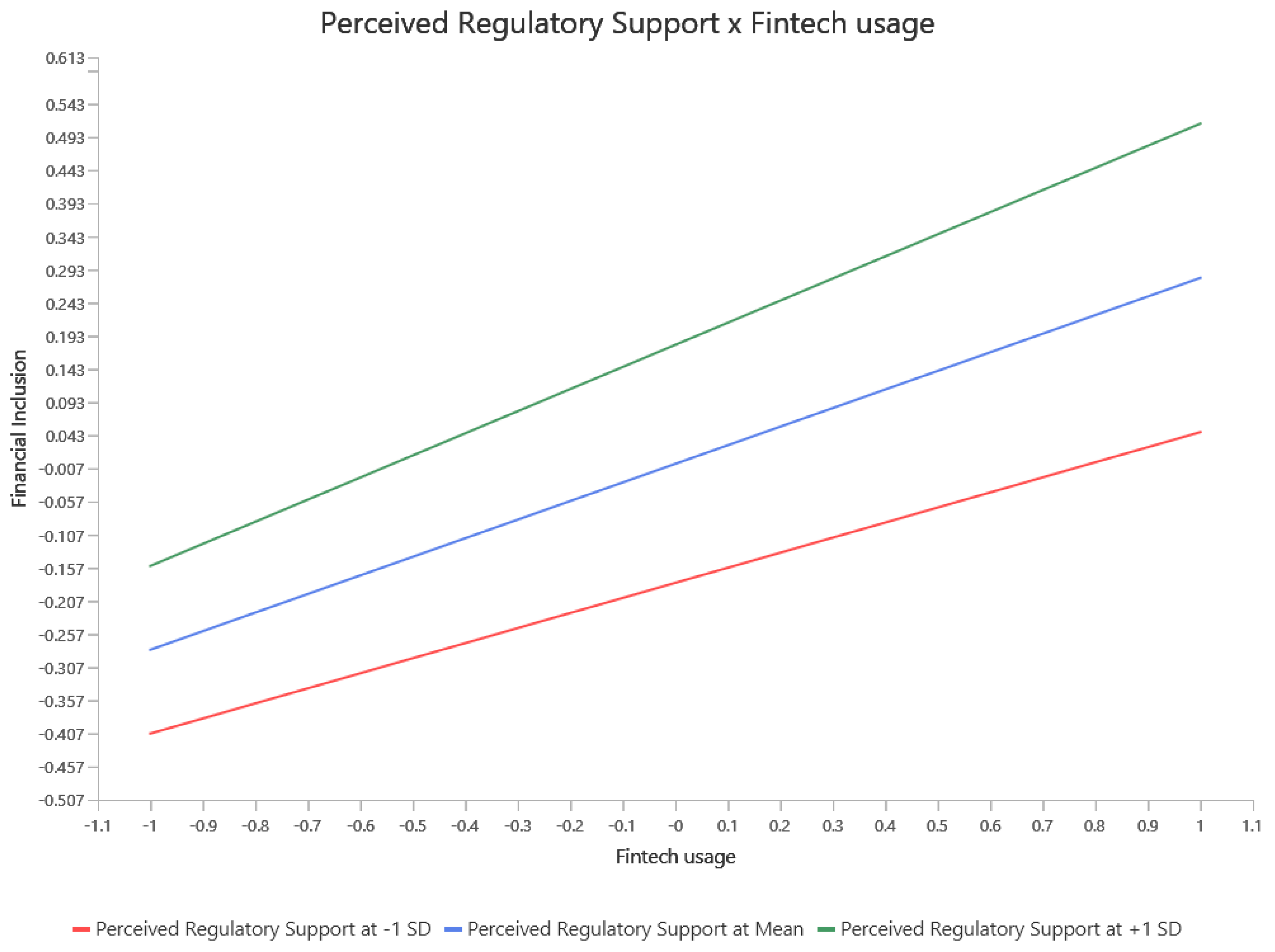

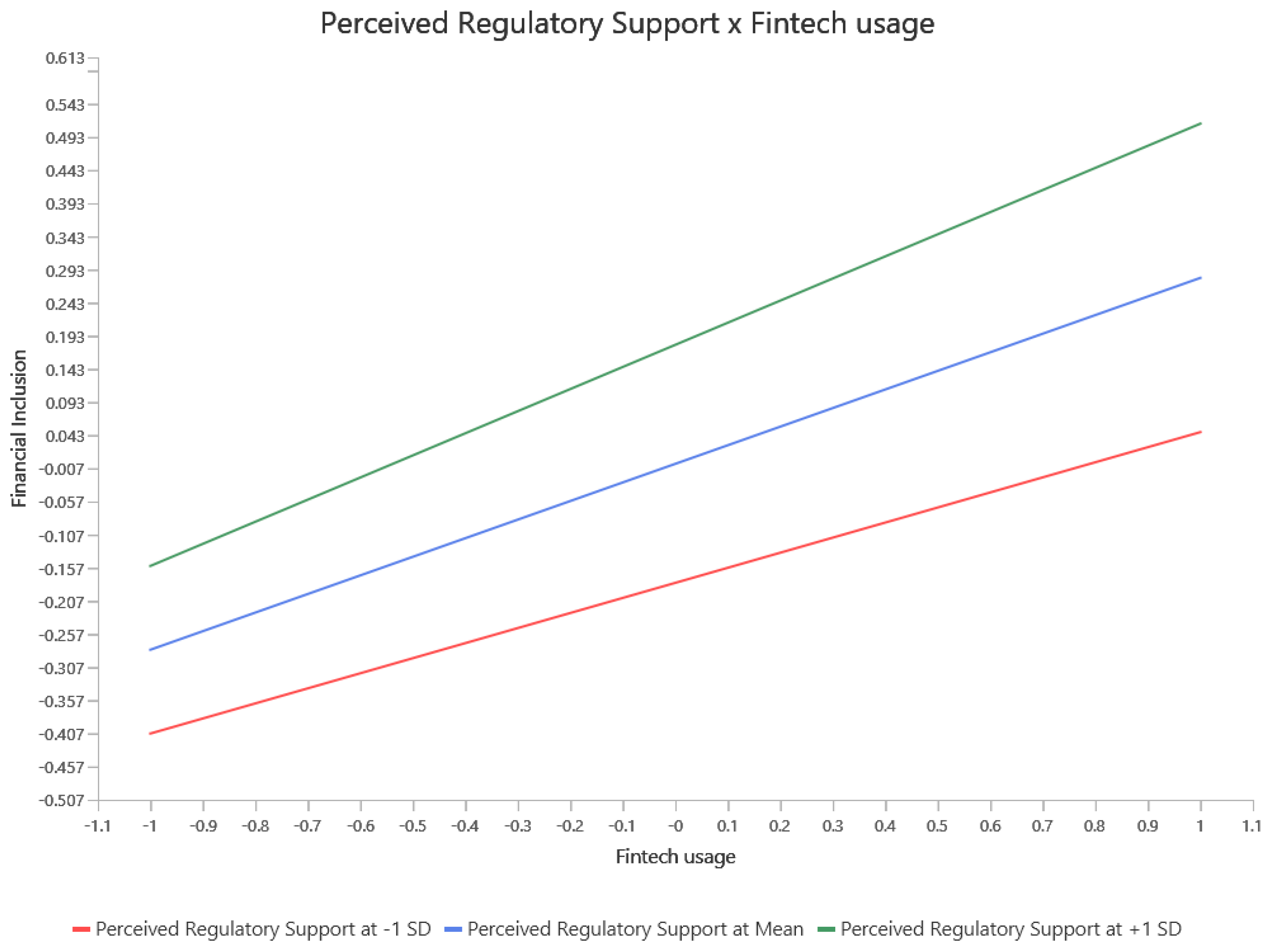

Figure 2 shows that the correlation between FinTech usage and financial inclusion is stronger when there is a high perceived level of regulatory support, as compared to moderate or lower levels of perceived regulatory support. Moreover, when Fintech usage escalates from low to high, the relationship between FinTech usage and financial inclusion becomes stronger, especially when there is high perceived regulatory support in contrast to moderate or low perceived regulatory support. The variation in the slope of the curve provides additional evidence for supporting the moderation hypothesis (H4a).

According to the R-squared values, the model could explain 53.5% of the variability in FinTech use, 53.1% in digital financial literacy, and 69.7% in financial inclusion. These findings suggest a satisfactory level of fit for the model. Additionally, the Stone–Geisser test criterion (Q

2) values for the dependent variables were calculated to verify the predictive relevance of the research model. The analysis revealed that the values of FinTech use (Q2 = 0.527), digital financial literacy (Q

2 = 0.499), and financial inclusion (Q

2 = 0.527) were greater than zero (Q

2 > 0), which confirmed the predictive accuracy of our model (

Hair et al. 2021).

The empirical model is presented in

Figure 3.

5. Discussion

Recognizing the importance of digital financial literacy and perceived regulatory support in FinTech-enabled financial inclusion, this study empirically tested the mediating and moderating effects of these variables in the association between FinTech use and financial inclusion. The motivation for this research emanated from a gap in the existing literature, which has not explored the mediating role of digital financial literacy and the moderating influence of perceived regulatory support.

First, the results demonstrated that trust significantly and positively influenced the use of FinTech services (Hypothesis 1), concurring with prior research (

Alrawad et al. 2023;

Amnas et al. 2023;

Savitha et al. 2022;

Wang et al. 2019;

Zarifis and Cheng 2022). This confirmation established the essential function that trust plays in promoting the utilization of FinTech platforms. The likelihood of users accepting and utilizing FinTech platforms increases when they feel that the service provider is committed to protecting their financial information. Second, the results also revealed that the usage of FinTech services is significantly and favorably impacted by service quality (Hypothesis 2), in line with other studies (

Ahmed et al. 2021;

George and Sunny 2023;

Gautam and Sah 2023;

Sultana et al. 2023). In other words, the quality of the FinTech products like user-friendly designs, extensive features, speed, customization options, quick customer support, and clear communication can attract users to FinTech platforms and promote continuous usage of these services. Third, the positive association of perceived security with FinTech use (Hypothesis 3) found support in this study, which is consistent with other studies from the literature (

Bajunaied et al. 2023;

Lim et al. 2019;

Meng et al. 2019;

Nasir et al. 2023) that shows when people feel secure about their sensitive information, they are more inclined to use FinTech platforms. In other words, the perception of security helps ease worries about privacy, boosts confidence, and lowers the risks tied to online transactions.

The fourth key finding in this research is the positive and substantial influence of FinTech use on financial inclusion (Hypothesis 4), which is consistent with previous studies (

Arner et al. 2020;

Asif et al. 2023;

Shaikh et al. 2023;

Yang and Zhang 2022). It means getting into FinTech can increase access to financial services through digital channels. Fifth, this study found that the utilization of FinTech services also enhanced digital financial literacy (Hypothesis 5). This means FinTech is facilitating learning about finances with educational resources, hands-on learning experiences, and real-time monitoring. Sixth, this study found that digital financial literacy has significant influence on financial inclusion (Hypothesis 6) consistent with other research (

He et al. 2024;

Kumar et al. 2023;

Ravikumar et al. 2022). That indicates consumers with greater levels of digital financial literacy can make informed financial decisions, reduce the risk involved with FinTech services, and actively engage in the formal financial system. Seventh, this study shows that the FinTech use and financial inclusion relationship is mediated by digital financial literacy (Hypothesis 7). So, when people use FinTech, they are likely to improve their digital financial literacy with the support of educational resources provided by FinTech platforms, which, in turn, helps out with improved financial inclusion.

The eighth finding is support for the moderating influence of perceived regulatory support in the relationship between FinTech and financial inclusion (Hypothesis 4a). When users feel like there is good regulatory backup, it creates a positive impact on the association between FinTech and financial inclusion. Having strong support from the regulators makes users more confident and willing to stick with FinTech services. The perceived regulatory support can make a difference in how FinTech impacts financial inclusion by acting as an important factor for the development of confidence in users of FinTech.

6. Theoretical Implications

This study’s theoretical implications are important because this research sheds further light on the complicated interaction between FinTech, digital financial literacy, regulatory support, and financial inclusion. One of the noteworthy contributions this study made was to bring in digital financial literacy as a mediator in the FinTech and financial inclusion relationship. In the context of FinTech, theoretical frameworks for financial inclusion need to be updated to consider the growing importance of digital financial literacy, as it is a necessary intermediate step toward financial inclusion. This study also confirmed that perceived security, trust, and service quality are key factors that influence people’s decision to use FinTech. This study introduced perceived regulatory support as a moderator, showing that rules and regulations can amp up FinTech’s impact on financial inclusion. So, the existing theories about financial systems might need an update to consider the relevance of perceived regulatory support in FinTech. The research opens opportunities for future scholars to look deeper into these theoretical dimensions and refine existing frameworks to better capture the complexities of the FinTech-driven financial inclusion landscape.

7. Practical Implications

This research holds various implications for financial institutions, policymakers, and FinTech service providers. First, FinTech companies need to make sure users trust them. That means being super clear in communication, implementing increased security, and having top-notch customer support will help to create customers’ trust. Second, investment for making their services better in terms of user interface, speed, and reliability is a smart move to improve service quality, which is essential for retaining users. Now, security is a big deal. Regularly updating users on security information and educating them about how their data is being protected can help ease the worries of the users. It is all about building confidence. Third, policymakers and educational institutions should team up to take steps to improve the digital financial literacy of the people. FinTech companies can facilitate improving literacy by offering tutorials and educational content on their platforms in innovative and interesting ways. Third, policymakers also may focus on making clear rules and frameworks and being transparent about regulatory frameworks, which can boost confidence and make people more likely to depend on FinTech for their financial needs. Special initiatives to boost digital financial literacy, especially in underserved groups, could be a game-changer. Lastly, FinTech companies, policymakers, and regulators need to keep their eyes on the evolving FinTech platforms. Regular checks on user experiences, security measures, and how well digital literacy programs are working will maintain the favorable impact on financial inclusion by FinTech going strong.

8. Limitations and Future Scope of this Study

Though this study offers insightful information, it is not free from limitations. This study employed a convenience sampling method because there was no predefined list of FinTech customers. It is a practical approach, but it could introduce bias since it might not represent all FinTech users out there. Also, this study focused on FinTech users in India, so the findings might not fit for other places, because the different geographical locations have different economic situations, rules, and FinTech landscapes. Furthermore, the effect of the personality characteristics of respondents on FinTech use and financial inclusion was not investigated in this study. It is more likely that age, experience, and attitude toward the use of technology may have profound influence on FinTech use and financial inclusion.

To increase our knowledge in this area, future research could go beyond quantitative research and focus on qualitative studies. First, the interaction with people through interviews or focus groups could give us a deeper knowledge of how users see and deal with FinTech. Second, it might also be interesting to compare how FinTech services change across different groups based on age, income, and education levels. That could uncover some interesting findings regarding how FinTech affects financial inclusion. Third, future studies can also focus on specific FinTech services like mobile payments, peer-to-peer lending, or robo-advisors. Each one might have a different impact on financial inclusion, so it is worth checking out. Fourth, large samples may be used to increase the generalizability of the findings from this study.

9. Conclusions

This study offers insightful information on the complex association between the use of FinTech and financial inclusion. The research found that trust, service quality, and perceived security are key factors that make people stick with FinTech services. As per the findings, FinTech promotes financial inclusion by increasing accessibility to financial services and lowering transaction costs. According to this study, knowing how to handle digital finances is super important for making the most out of FinTech services. In other words, in this age of crazy tech advancements, being digitally literate is a must for making smart money moves and being part of the formal financial system.

The research also brings up an interesting point about how people’s perception of regulatory support affects the connection between FinTech use and financial inclusion. If people feel like there is good regulatory support, it amplifies the favorable effects on financial inclusion by FinTech use. So, having a supportive regulatory environment is crucial for building trust and allowing more people to jump on the FinTech landscape. This study not only fills gaps in the existing research by looking into digital financial literacy and regulatory support but also gives us a clear picture of how FinTech use and financial inclusion are connected. The model and concepts introduced by this research would contribute substantially to the growing body of literature in the realms of FinTech use and financial inclusion.

Author Contributions

Conceptualization, M.B.A. and M.S.; methodology, M.S. and S.P.; software, M.B.A. and S.P.; validation, M.S. and S.P.; formal analysis, M.B.A. and S.P.; investigation, M.B.A. and M.S.; resources, M.B.A. and M.S.; data curation, M.S. and S.P.; writing—original draft preparation, M.B.A. and S.P.; writing—review and editing, M.S. and S.P.; visualization, M.S. supervision, M.S.; project administration, M.S. and S.P. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Data Availability Statement

We make the data available on request.

Conflicts of Interest

The authors declare no conflicts of interest.

Appendix A. Survey Instrument (with Sources of Constructs)

| Constructs | Items | Questions | Sources |

| Trust (TR) | TR1 | I trust that FinTech platforms will securely handle and protect my financial information. | Singh and Srivastava (2018) and Kumar et al. (2018) |

| TR2 | I have confidence in the reliability and stability of FinTech services for my financial transactions. |

| TR3 | I trust that FinTech platforms will promptly address any issues or concerns I may have. |

| TR4 | I trust that FinTech platforms adhere to ethical standards and guidelines in their business practices. |

| Service quality (SQ) | SQ1 | FinTech services consistently meet my expectations in terms of reliability and performance. | Zhou (2013) |

| SQ2 | I am satisfied with the speed and efficiency of problem resolution when I encounter issues with FinTech services. |

| SQ3 | The user interface of FinTech apps is intuitive and easy to navigate. |

| SQ4 | FinTech platforms provide clear and transparent information about fees, charges, and terms of use. |

| Perceived security (PS) | PS1 | I believe that my personal and financial information is secure when using FinTech platforms. | George and Sunny (2023) |

| PS2 | I am confident that FinTech platforms promptly address and resolve any security vulnerabilities. |

| PS3 | I have confidence in the effectiveness of the authentication methods employed by FinTech services to prevent unauthorized access. |

| PS4 | I believe that FinTech companies implement sufficient measures to safeguard against fraud and cyber threats. |

| FinTech use (FU) | FU1 | I frequently employ FinTech for making payments and transferring funds. | Venkatesh et al. (2012) |

| FU2 | I leverage FinTech investment platforms to oversee my investment portfolio. |

| FU3 | I turn to FinTech services when I require financial assistance. |

| FU4 | I actively engage with FinTech insurance services to purchase and oversee insurance policies. |

Financial I

inclusion | FI1 | FinTech services have expanded my access to financial products and services. | Bongomin and Ntayi (2020) |

| FI2 | FinTech services have increased my ability to save and invest my money. |

| FI3 | FinTech adoption has made it easier for me to send and receive money. |

| FI4 | FinTech services have improved my ability to access credit and loans. |

| Digital financial literacy | DFL1 | I am knowledgeable about the various features and functionalities of fintech apps. | Ravikumar et al. (2022) |

| DFL2 | I am aware of the potential risks and security measures associated with using digital payment systems. |

| DFL3 | I know how to troubleshoot common issues related to digital financial transactions. |

| DFL4 | I am familiar with the terms and concepts related to digital financial services. |

| Perceived regulatory support | PRS1 | My decision to utilize FinTech services is positively impacted by governmental initiatives and policies. | Chandra et al. (2010) |

| PRS2 | Government promotions highlighting the advantages of FinTech services make me more predisposed to using them. |

| PRS3 | The backing of the government instills a greater sense of security and confidence in my utilization of FinTech services. |

| PRS4 | Government support plays a role in enhancing the accessibility and affordability of FinTech services. |

References

- Ahmed, Rizwan Raheem, Dalia Streimikiene, Zahid Ali Channar, Riaz Hussain Soomro, and Justas Streimikis. 2021. E-banking Customer Satisfaction and Loyalty: Evidence from Serial Mediation through Modified E-S-QUAL Model and Second-Order PLS-SEM. Engineering Economics 32: 407–21. [Google Scholar] [CrossRef]

- AlBenJasim, Salah, Tooska Dargahi, Haifa Takruri, and Rabab Al-Zaidi. 2023. FinTech Cybersecurity Challenges and Regulations: Bahrain Case Study. Journal of Computer Information Systems, 1–17. [Google Scholar] [CrossRef]

- Aleemi, Abdur Rahman, Fatima Javaid, and Syed Sajid Hafeez. 2023. Finclusion: The nexus of Fintech and financial inclusion against banks’ market power. Heliyon 9: e22551. [Google Scholar] [CrossRef] [PubMed]

- Alrawad, Mahmaod, Abdalwali Lutfi, Mohammed Amin Almaiah, and Ibrahim A. Elshaer. 2023. Examining the influence of trust and perceived risk on customers intention to use NFC mobile payment system. Journal of Open Innovation: Technology, Market, and Complexity 9: 100070. [Google Scholar] [CrossRef]

- Al-Slehat, Zaher Abdel Fattah. 2023. Fintech and financial inclusion: The mediating role of digital marketing. Business: Theory and Practice 24: 183–93. [Google Scholar] [CrossRef]

- Amnas, Muhammed Basid, Murugesan Selvam, Mariappan Raja, Sakthivel Santhoshkumar, and Satyanarayana Parayitam. 2023. Understanding the Determinants of FinTech Adoption: Integrating UTAUT2 with Trust Theoretic Model. Journal of Risk and Financial Management 16: 505. [Google Scholar] [CrossRef]

- Arner, Douglas W., Ross P. Buckley, Dirk A. Zetzsche, and Robin Veidt. 2020. Sustainability, FinTech and Financial Inclusion. European Business Organization Law Review 21: 7–35. [Google Scholar] [CrossRef]

- Asif, Mohammad, Mohd Naved Khan, Sadhana Tiwari, Showkat K. Wani, and Firoz Alam. 2023. The Impact of Fintech and Digital Financial Services on Financial Inclusion in India. Journal of Risk and Financial Management 16: 122. [Google Scholar] [CrossRef]

- Bajunaied, Kholoud, Nazimah Hussin, and Suzilawat Kamarudin. 2023. Behavioral intention to adopt FinTech services: An extension of unified theory of acceptance and use of technology. Journal of Open Innovation: Technology, Market, and Complexity 9: 100010. [Google Scholar] [CrossRef]

- Björkegren, Daniel, and Darrell Grissen. 2018. The Potential of Digital Credit to Bank the Poor. AEA Papers and Proceedings 108: 68–71. [Google Scholar] [CrossRef]

- Bongomin, George Okello Candiya, and John C. Munene. 2021. Analyzing the Relationship between Mobile Money Adoption and Usage and Financial Inclusion of MSMEs in Developing Countries: Mediating Role of Cultural Norms in Uganda. Journal of African Business 22: 1–20. [Google Scholar] [CrossRef]

- Bongomin, George Okello Candiya, and Joseph Mpeera Ntayi. 2020. Mobile money adoption and usage and financial inclusion: Mediating effect of digital consumer protection. Digital Policy, Regulation and Governance 22: 157–76. [Google Scholar] [CrossRef]

- Brown, Eric, and Dóra Piroska. 2022. Governing Fintech and Fintech as Governance: The Regulatory Sandbox, Riskwashing, and Disruptive Social Classification. New Political Economy 27: 19–32. [Google Scholar] [CrossRef]

- Bu, Ya, Hui Li, and Xiaoqing Wu. 2022. Effective regulations of FinTech innovations: The case of China. Economics of Innovation and New Technology 31: 751–69. [Google Scholar] [CrossRef]

- Carè, Rosella, Iustina Alina Boitan, and Razia Fatima. 2023. How do FinTech companies contribute to the achievement of SDGs? Insights from case studies. Research in International Business and Finance 66: 102072. [Google Scholar] [CrossRef]

- Chandra, Shalini, Shirish C. Srivastava, and Yin-Leng Theng. 2010. Evaluating the Role of Trust in Consumer Adoption of Mobile Payment Systems: An Empirical Analysis. Communications of the Association for Information Systems 27: 562–88. [Google Scholar] [CrossRef]

- Choung, Youngjoo, Swarn Chatterjee, and Tae-Young Pak. 2023. Digital financial literacy and financial well-being. Finance Research Letters 58: 104438. [Google Scholar] [CrossRef]

- De Blanes Sebastián, María García, Arta Antonovica, and José Ramón Sarmiento Guede. 2023. What are the leading factors for using Spanish peer-to-peer mobile payment platform Bizum? The applied analysis of the UTAUT2 model. Technological Forecasting and Social Change 187: 122235. [Google Scholar] [CrossRef]

- Demirgüç-Kunt, Asli, Leora Klapper, Dorothe Singer, and Saniya Ansar. 2022. The Global Findex Database 2021: Financial Inclusion, Digital Payments, and Resilience in the Age of COVID-19. Washington, DC: World Bank Publications. [Google Scholar]

- Ediagbonya, Victor, and Comfort Tioluwani. 2023. The role of fintech in driving financial inclusion in developing and emerging markets: Issues, challenges and prospects. Technological Sustainability 2: 100–19. [Google Scholar] [CrossRef]

- Faul, Franz, Edgar Erdfelder, Albert-Georg Lang, and Axel Buchner. 2007. G*Power 3: A flexible statistical power analysis program for the social, behavioral, and biomedical sciences. Behavior Research Methods 39: 175–91. [Google Scholar] [CrossRef] [PubMed]

- Feyen, Erik, Harish Natarajan, and Matthew Saal. 2023. Fintech and the Future of Finance: Market and Policy Implications. Washington, DC: World Bank Publications. [Google Scholar] [CrossRef]

- Fornell, Claes, and David F. Larcker. 1981. Structural Equation Models with Unobservable Variables and Measurement Error: Algebra and Statistics. Journal of Marketing Research 18: 382–88. [Google Scholar] [CrossRef]

- Gansser, Oliver, and Christina Reich. 2021. A new acceptance model for artificial intelligence with extensions to UTAUT2: An empirical study in three segments of application. Technology in Society 65: 101535. [Google Scholar] [CrossRef]

- Gautam, Dhruba Kumar, and Gunja Kumari Sah. 2023. Online Banking Service Practices and Its Impact on E-Customer Satisfaction and E-Customer Loyalty in Developing Country of South Asia-Nepal. SAGE Open 13: 1–14. [Google Scholar] [CrossRef]

- Gautam, Rahul Singh, Shailesh Rastogi, Aashi Rawal, Venkata Mrudula Bhimavarapu, Jagjeevan Kanoujiya, and Samaksh Rastogi. 2022. Financial Technology and Its Impact on Digital Literacy in India: Using Poverty as a Moderating Variable. Journal of Risk and Financial Management 15: 311. [Google Scholar] [CrossRef]

- George, Ajimon, and Prajod Sunny. 2021. Developing a Research Model for Mobile Wallet Adoption and Usage. IIM Kozhikode Society & Management Review 10: 82–98. [Google Scholar] [CrossRef]

- George, Ajimon, and Prajod Sunny. 2023. Why do people continue using mobile wallets? An empirical analysis amid COVID-19 pandemic. Journal of Financial Services Marketing 28: 807–21. [Google Scholar] [CrossRef]

- Ghosh, Manimay. 2018. Measuring electronic service quality in India using E-S-QUAL. International Journal of Quality & Reliability Management 35: 430–45. [Google Scholar] [CrossRef]

- Hair, Joseph F., Claudia Binz Astrachan, Ovidiu I. Moisescu, Lăcrămioara Radomir, Marko Sarstedt, Santha Vaithilingam, and Christian M. Ringle. 2021. Executing and interpreting applications of PLS-SEM: Updates for family business researchers. Journal of Family Business Strategy 12: 100392. [Google Scholar] [CrossRef]

- Hair, Joseph F., Jeffrey J. Risher, Marko Sarstedt, and Christian M. Ringle. 2019. When to use and how to report the results of PLS-SEM. European Business Review 31: 2–24. [Google Scholar] [CrossRef]

- Hasan, Morshadul, Thi Le, and Ariful Hoque. 2021a. How does financial literacy impact on inclusive finance? Financial Innovation 7: 40. [Google Scholar] [CrossRef]

- Hasan, Rashedul, Muhammad Ashfaq, and Lingli Shao. 2021b. Evaluating Drivers of Fintech Adoption in the Netherlands. Global Business Review. [Google Scholar] [CrossRef]

- He, Huihua, Wenwei Luo, Ying Gong, Ilene R. Berson, and Michael J. Berson. 2024. Digital Financial Literacy of Young Chinese Children in Shanghai: A Mixed Method Study. Early Education and Development 35: 57–76. [Google Scholar] [CrossRef]

- Henseler, Jörg, Geoffrey Hubona, and Pauline Ash Ray. 2016. Using PLS path modeling in new technology research: Updated guidelines. Industrial Management & Data Systems 116: 2–20. [Google Scholar] [CrossRef]

- Jangir, Kshitiz, Vikas Sharma, Sanjay Taneja, and Ramona Rupeika-Apoga. 2022. The Moderating Effect of Perceived Risk on Users’ Continuance Intention for FinTech Services. Journal of Risk and Financial Management 16: 21. [Google Scholar] [CrossRef]

- Jun, Jaehyeon, Insu Cho, and Heejun Park. 2018. Factors influencing continued use of mobile easy payment service: An empirical investigation. Total Quality Management and Business Excellence 29: 1043–57. [Google Scholar] [CrossRef]

- Kakinuma, Yosuke. 2022. Financial literacy and quality of life: A moderated mediation approach of fintech adoption and leisure. International Journal of Social Economics 49: 1713–26. [Google Scholar] [CrossRef]

- Khan, Habib Hussain, Shoaib Khan, and Abdul Ghafoor. 2023. Fintech adoption, the regulatory environment and bank stability: An empirical investigation from GCC economies. Borsa Istanbul Review 23: 1263–81. [Google Scholar] [CrossRef]

- Kilani, Abd Al-Haleem Zaid, Dana Kakeesh, Ghazi A. Al-Weshah, and Mutaz M. Al-Debei. 2023. Consumer post-adoption of e-wallet: An extended UTAUT2 perspective with trust. Journal of Open Innovation: Technology, Market, and Complexity 9: 100113. [Google Scholar] [CrossRef]

- Kim, Hee-Woong, Hock-Chuan Chan, and Sumeet Gupta. 2007. Value-based adoption of mobile internet: An empirical investigation. Decision Support Systems 43: 111–26. [Google Scholar] [CrossRef]

- Kock, Ned. 2015. Common Method Bias in PLS-SEM. International Journal of E-Collaboration 11: 1–10. [Google Scholar] [CrossRef]

- Kumar, Anup, Amit Adlakaha, and Kampan Mukherjee. 2018. The effect of perceived security and grievance redressal on continuance intention to use M-wallets in a developing country. International Journal of Bank Marketing 36: 1170–89. [Google Scholar] [CrossRef]

- Kumar, Parul, Rekha Pillai, Neha Kumar, and Mosab I. Tabash. 2023. The interplay of skills, digital financial literacy, capability, and autonomy in financial decision making and well-being. Borsa Istanbul Review 23: 169–83. [Google Scholar] [CrossRef]

- Lai, Karen P. Y., and Paul Langley. 2023. Playful finance: Gamification and intermediation in FinTech economies. Geoforum, 103848. [Google Scholar] [CrossRef]

- Lee, Chungah, Haejung Yun, and Chunghun Lee. 2015. Factors affecting continuous intention to use mobile wallet: Based on value-based adoption model. The Journal of Society for e-Business Studies 20: 117–35. [Google Scholar] [CrossRef]

- Lim, Se Hun, Dan J. Kim, Yeon Hur, and Kunsu Park. 2019. An Empirical Study of the Impacts of Perceived Security and Knowledge on Continuous Intention to Use Mobile Fintech Payment Services. International Journal of Human–Computer Interaction 35: 886–98. [Google Scholar] [CrossRef]

- Lyons, Angela C., and Josephine Kass-Hanna. 2021. A methodological overview to defining and measuring “digital” financial literacy. Financial Planning Review 4: e1113. [Google Scholar] [CrossRef]

- Madan, Khushbu, and Rajan Yadav. 2016. Behavioural intention to adopt mobile wallet: A developing country perspective. Journal of Indian Business Research 8: 227–44. [Google Scholar] [CrossRef]

- Malladi, Chandra Mohan, Rupesh K. Soni, and Sanjay Srinivasan. 2021. Digital financial inclusion: Next frontiers—challenges and opportunities. CSI Transactions on ICT 9: 127–34. [Google Scholar] [CrossRef]

- Meng, Weizhi, Liqiu Zhu, Wenjuan Li, Jinguang Han, and Yan Li. 2019. Enhancing the security of FinTech applications with map-based graphical password authentication. Future Generation Computer Systems 101: 1018–27. [Google Scholar] [CrossRef]

- Morgan, Peter J., Bihong Huang, and Long Q. Trinh. 2020. The need to Promote Digital Financial Literacy in the Digital Age. Tokyo: T-20 Japan. Available online: https://t20japan.org/policy-brief-need-promote-digital-financial-literacy/ (accessed on 4 March 2024).

- Mujinga, Mathias. 2020. Online Banking Service Quality: A South African E-S-QUAL Analysis. Lecture Notes in Computer Science 12066: 228–38. [Google Scholar] [CrossRef]

- Nasir, Abdul, Naeem Jan, Dragan Pamucar, and Sami Ullah Khan. 2023. Analysis of cybercrimes and security in FinTech industries using the novel concepts of interval-valued complex q-rung orthopair fuzzy relations. Expert Systems with Applications 224: 119976. [Google Scholar] [CrossRef]

- Ng, Artie W., and Benny K. B. Kwok. 2017. Emergence of Fintech and cybersecurity in a global financial centre. Journal of Financial Regulation and Compliance 25: 422–34. [Google Scholar] [CrossRef]

- Nugraha, Deni Pandu, Budi Setiawan, Robert Jeyakumar Nathan, and Maria Fekete-Farkas. 2022. Fintech Adoption Drivers for Innovation for SMEs in Indonesia. Journal of Open Innovation: Technology, Market, and Complexity 8: 208. [Google Scholar] [CrossRef]

- Ong, Mohd Hanafi Azman, Muhammad Yassar Yusri, and Nur Ibrahim. 2023. Use and behavioural intention using digital payment systems among rural residents: Extending the UTAUT-2 model. Technology in Society 74: 102305. [Google Scholar] [CrossRef]

- Otieno, Geoffrey, and Ruth Kiraka. 2023. Beyond the innovator’s Dilemma: The process and effect of fintech regulatory environment. Cogent Business & Management 10: 2226422. [Google Scholar] [CrossRef]

- Panos, Georgios A., and John O. S. Wilson. 2020. Financial literacy and responsible finance in the FinTech era: Capabilities and challenges. The European Journal of Finance 26: 297–301. [Google Scholar] [CrossRef]

- Patnaik, Amitabh, Pallavi Kudal, Sunny Dawar, Varada Inamdar, and Prince Dawar. 2023. Exploring User Acceptance of Digital Payments in India: An Empirical Study Using an Extended Technology Acceptance Model in the Fintech Landscape. International Journal of Sustainable Development and Planning 18: 2587–97. [Google Scholar] [CrossRef]

- Paul, Madhumita. 2022. India Still among Countries with Poor access to Banking: Report, More than Half of Population without Access to Banking Lives in 7 Developing Countries: World Bank, Down to Earth. Available online: https://www.downtoearth.org.in/news/economy/india-still-among-countries-with-poor-access-to-banking-report-83542 (accessed on 4 March 2024).

- Podsakoff, Philip M., Scott B. MacKenzie, Jeong-Yeon Lee, and Nathan P. Podsakoff. 2003. Common method biases in behavioral research: A critical review of the literature and recommended remedies. Journal of Applied Psychology 88: 879–903. [Google Scholar] [CrossRef]

- Prasad, Hanuman, Devendra Meghwal, and Vijay Dayama. 2018. Digital Financial Literacy: A Study of Households of Udaipur. Journal of Business and Management 5: 23–32. [Google Scholar] [CrossRef]

- Prete, Anna Lo. 2022. Digital and financial literacy as determinants of digital payments and personal finance. Economics Letters 213: 110378. [Google Scholar] [CrossRef]

- Putri, Gustita Arnawati, Ari Kuncara Widagdo, and Doddy Setiawan. 2023. Analysis of financial technology acceptance of peer-to-peer lending (P2P lending) using extended technology acceptance model (TAM). Journal of Open Innovation: Technology, Market, and Complexity 9: 100027. [Google Scholar] [CrossRef]

- Ravikumar, T., B. Suresha, N. Prakash, Kiran Vazirani, and T. A. Krishna. 2022. Digital financial literacy among adults in India: Measurement and validation. Cogent Economics & Finance 10: 2132631. [Google Scholar] [CrossRef]

- Roh, Taewoo, Young Soo Yang, Shufeng Xiao, and Byung Il Park. 2022. What makes consumers trust and adopt fintech? An empirical investigation in China. Electronic Commerce Research. [Google Scholar] [CrossRef]

- Sampat, Brinda, Emmanuel Mogaji, and Nguyen Phong Nguyen. 2023. The dark side of FinTech in financial services: A qualitative enquiry into FinTech developers’ perspective. International Journal of Bank Marketing 42: 38–65. [Google Scholar] [CrossRef]

- Savitha, Basri, Iqbal Thonse Hawaldar, and Naveen Kumar K. 2022. Continuance intentions to use FinTech peer-to-peer payments apps in India. Heliyon 8: e11654. [Google Scholar] [CrossRef] [PubMed]

- Şenol, Doğaç, and Ceylan Onay. 2023. Impact of gamification on mitigating behavioral biases of investors. Journal of Behavioral and Experimental Finance 37: 100772. [Google Scholar] [CrossRef]

- Senyo, Prince Kwame, and Ellis L. C. Osabutey. 2020. Unearthing antecedents to financial inclusion through FinTech innovations. Technovation 98: 102155. [Google Scholar] [CrossRef]

- Setiawan, Maman, Nury Effendi, Teguh Santoso, Vera Intanie Dewi, and Militcyano Samuel Sapulette. 2022. Digital financial literacy, current behavior of saving and spending and its future foresight. Economics of Innovation and New Technology 31: 320–38. [Google Scholar] [CrossRef]

- Shahzad, Arfan, Nurhana Zahrullail, Ahsan Akbar, Hana Mohelska, and Arsalan Hussain. 2022. COVID-19’s Impact on Fintech Adoption: Behavioral Intention to Use the Financial Portal. Journal of Risk and Financial Management 15: 428. [Google Scholar] [CrossRef]

- Shaikh, Aijaz A., Richard Glavee-Geo, Heikki Karjaluoto, and Robert Ebo Hinson. 2023. Mobile money as a driver of digital financial inclusion. Technological Forecasting and Social Change 186: 122158. [Google Scholar] [CrossRef]

- Shen, Yan, C. James Hueng, and Wenxiu Hu. 2020. Using digital technology to improve financial inclusion in China. Applied Economics Letters 27: 30–34. [Google Scholar] [CrossRef]

- Shen, Yan, Wenxiu Hu, and C. James Hueng. 2018. The Effects of Financial Literacy, Digital Financial Product Usage and Internet Usage on Financial Inclusion in China. MATEC Web of Conferences 228: 05012. [Google Scholar] [CrossRef]

- Singh, Sindhu, and R. K. Srivastava. 2018. Predicting the intention to use mobile banking in India. International Journal of Bank Marketing 36: 357–78. [Google Scholar] [CrossRef]

- Sultana, Nahida, Rubaiyat Shaimom Chowdhury, and Afruza Haque. 2023. Gravitating towards Fintech: A study on Undergraduates using extended UTAUT model. Heliyon 9: e20731. [Google Scholar] [CrossRef] [PubMed]

- Uthaileang, Wasan, and Supaporn Kiattisin. 2023. Developing the capability of digital financial literacy in developing countries: A Case of online loan for small entrepreneurs. Heliyon 9: e21961. [Google Scholar] [CrossRef] [PubMed]

- Venkatesh, Viswanath, James Y. L. Thong, and Xin Xu. 2012. Consumer Acceptance and Use of Information Technology: Extending the Unified Theory of Acceptance and Use of Technology. MIS Quarterly 36: 157. [Google Scholar] [CrossRef]

- Venkatesh, Viswanath, Michael G. Morris, Gordon B. Davis, and Fred D. Davis. 2003. User Acceptance of Information Technology: Towards a Unified View. MIS Quarterly 27: 425–78. [Google Scholar] [CrossRef]

- Vyas, Vishal, and Priyanka Jain. 2021. Role of digital economy and technology adoption for financial inclusion in India. Indian Growth and Development Review 14: 302–24. [Google Scholar] [CrossRef]

- Wang, Jen-Sheng. 2023. Reconfigure and evaluate consumer satisfaction for Open API in advancing FinTech. Journal of King Saud University-Computer and Information Sciences 35: 101738. [Google Scholar] [CrossRef]

- Wang, Zhenning, Zhengzhi (Gordon) Guan, Fangfang Hou, Boying Li, and Wangyue Zhou. 2019. What determines customers’ continuance intention of FinTech? Evidence from YuEbao. Industrial Management & Data Systems 119: 1625–37. [Google Scholar] [CrossRef]

- Xia, Huosong, Duqun Lu, Boqiang Lin, Jeretta Horn Nord, and Justin Zuopeng Zhang. 2023. Trust in Fintech: Risk, Governance, and Continuance Intention. Journal of Computer Information Systems 63: 648–62. [Google Scholar] [CrossRef]

- Xie, Jianli, Liying Ye, Wei Huang, and Min Ye. 2021. Understanding FinTech Platform Adoption: Impacts of Perceived Value and Perceived Risk. Journal of Theoretical and Applied Electronic Commerce Research 16: 1893–911. [Google Scholar] [CrossRef]

- Yang, Tong, and Xun Zhang. 2022. FinTech adoption and financial inclusion: Evidence from household consumption in China. Journal of Banking & Finance 145: 106668. [Google Scholar] [CrossRef]

- Yeyouomo, Aurelien Kamdem, Simplice A. Asongu, and Peter Agyemang-Mintah. 2023. Fintechs and the financial inclusion gender gap in Sub-Saharan African countries. Women’s Studies International Forum 97: 102695. [Google Scholar] [CrossRef]

- Yue, Pengpeng, Aslihan Gizem Korkmaz, Zhichao Yin, and Haigang Zhou. 2022. The rise of digital finance: Financial inclusion or debt trap? Finance Research Letters 47: 102604. [Google Scholar] [CrossRef]

- Zait, Adriana, and Patrice Elena Bertea. 2014. Financial literacy—Conceptual definition and proposed approach for a measurement instrument. Journal of Accounting and Management 4: 37–42. Available online: https://econpapers.repec.org/article/dugjaccma/y_3a2014_3ai_3a3_3ap_3a37-42.htm (accessed on 4 March 2024).

- Zarifis, Alex, and Xusen Cheng. 2022. A model of trust in Fintech and trust in Insurtech: How Artificial Intelligence and the context influence it. Journal of Behavioral and Experimental Finance 36: 100739. [Google Scholar] [CrossRef]

- Zhang, Wenxiang, Saeed Siyal, Samina Riaz, Riaz Ahmad, Mohd Faiz Hilmi, and Zhi Li. 2023. Data Security, Customer Trust and Intention for Adoption of Fintech Services: An Empirical Analysis from Commercial Bank Users in Pakistan. SAGE Open 13. [Google Scholar] [CrossRef]

- Zhou, Tao. 2013. An empirical examination of continuance intention of mobile payment services. Decision Support Systems 54: 1085–91. [Google Scholar] [CrossRef]

| Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

_Zheng.png)

{kind=link}

{kind=link}

{kind=link}