_Zheng.png)

The Causal Relationship between FinTech, Financial Inclusion, and Income Inequality in African Economies

Abstract

:1. Introduction

2. Literature Review

2.1. FinTech and Income Inequality

2.2. FinTech and Financial Inclusion

2.3. Financial Inclusion and Income Inequality

3. Data and Methodology

3.1. Research Data

3.2. Research Model Specification

3.3. Research Method of Data Analysis

4. Results and Discussion

4.1. Summary Statistics

4.2. Pooled OLS Regression Analysis

4.3. Structural Equation Model (SEM) Analysis

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Abdullah, Abdul, Hristos Doucouliagos, and Elizabeth Manning. 2015. Does Education Reduce Income Inequality? Me-ta-Regression Analysis. Journals of Economic Services 29: 301–16. [Google Scholar] [CrossRef]

- Aker, Jenny C., and Isaac M. Mbiti. 2010. Mobile Phones and Economic Development in Africa. Journal of Economic Perspectives 24: 207–32. [Google Scholar] [CrossRef]

- Appaya, Sharmista. 2021. World Bank blog. Retrieved from World Bank. Available online: https://blogs.worldbank.org/psd/fintech-and-financial-inclusion (accessed on 6 August 2023).

- Appiah-Otoo, Isaac, and Na Song. 2021. The Impact of Fintech on Poverty Reduction: Evidence from China. Sustainability 13: 5225. [Google Scholar] [CrossRef]

- Asongu, Simplice. 2015. The impact of mobile phone penetration on African inequality. International Journal of Social Economics 42: 706–16. [Google Scholar] [CrossRef]

- Asongu, Simplice, and Jacinta Nwachukwu. 2018. Comparative human development thresholds for absolute and relative pro-poor mobile banking in developing countries. Information Technology & People 31: 63–83. [Google Scholar] [CrossRef]

- Asongu, Simplice, and Nicholas M. Odhiambo. 2019. Mobile banking usage, quality of growth, inequality, and poverty in developing countries. Information Development 35: 303–18. [Google Scholar] [CrossRef]

- Atadouanla Segning, Beauclair, Constant Fouopi Djiogap, Serge Mandiefe Piabuo, and Elie Ngasseu Noupie. 2023. Financial Inclusion and Income Inequality in Sub-Saharan Africa: Taking Socio-Cultural Particularities into Account. Journal of the Knowledge Economy, 1–24. [Google Scholar] [CrossRef]

- Bauer, Johannes M. 2018. The Internet and Income Inequality: A Socio-Economic Challenge in a Hyperconnected Society. Telecommunications Policy 42: 333–43. [Google Scholar] [CrossRef]

- Bazarbash, Majid, and Kimberly Beaton. 2020. Filling the Gap: Digital Credit and Financial Inclusion. IMF Working Paper No. 2020/150. Washington, DC: International Monetary Fund. [Google Scholar]

- Beck, Thorsten, and Ross Levine. 2004. Stock markets, banks, and growth: Panel evidence. Journal of Banking & Finance 28: 423–42. [Google Scholar] [CrossRef]

- Breusch, Trevor S., and Adrian R. Pagan. 1980. The Lagrange Multiplier Test and its Applications to Model Specification in Econometrics. The Review of Economic Studies 47: 239–53. [Google Scholar] [CrossRef]

- Canh, Nguyen Phuc, Christophe Schinckus, Su Dinh Thanh, and Felicia Chong Hui Ling. 2020. Effects of the internet, mobile, and land phones on income inequality and The Kuznets curve: Cross-country analysis. Telecommunications Policy 44: 102041. [Google Scholar] [CrossRef]

- Chinoda, Tough, and Tafirei Mashamba. 2021. Fintech, financial inclusion, and income inequality nexus in Africa. Cogent Economics & Finance 9: 1986926. [Google Scholar] [CrossRef]

- Demir, Ayse, Vanesa Pesqué-Cela, Yener Altunbas, and Victor Murinde. 2020. Fintech, financial inclusion, and income inequality: A quantile regression approach. The European Journal of Finance 28: 86–107. [Google Scholar] [CrossRef]

- Doerrenberg, Philipp, and Andreas Peichl. 2014. The impact of redistributive policies on inequality in OECD countries. Applied Economics 46: 2066–86. [Google Scholar] [CrossRef]

- Gabor, Daniela, and Sally Brooks. 2017. The digital revolution in financial inclusion: International development in the fintech era. New Political Economy 22: 423–36. [Google Scholar] [CrossRef]

- Glomm, Gerhard, and B. Ravikumar. 2003. Public education and income inequality. European Journal of Political Economy 19: 289–300. [Google Scholar] [CrossRef]

- Hatch, Megan, and Elizabeth Rigby. 2015. Laboratories of (In)equality? Redistributive Policy and Income Inequality in the American States. The Policy Studies Journal 43: 163–87. [Google Scholar] [CrossRef]

- Hausman, Jerry. 1978. Specification Tests in Econometrics. Econometrica 46: 1251–71. [Google Scholar] [CrossRef]

- Hodula, Martin. 2023. Fintech credit, big tech credit and income inequality. Finance Research Letters 51: 103387. [Google Scholar] [CrossRef]

- Hsing, Yu. 2005. Economic growth and income inequality: The case of the US. International Journal of Social Economics 32: 639–47. [Google Scholar] [CrossRef]

- Hunjra, Ahmed Imran, Muhammad Azam, Maria Giuseppina Bruna, and Dilvin Taskin. 2022. Role of financial development for sustainable economic development in low middle income countries. Finance Research Letters 47: 102793. [Google Scholar] [CrossRef]

- Jin, Yi. 2009. A Note on Inflation, Economic Growth, And Income Inequality. Macroeconomic Dynamics 13: 138–47. [Google Scholar] [CrossRef]

- Keller, Katarina R. I. 2010. How Can Education Policy Improve Income Distribution? An Empirical Analysis of Education Stages and Measures on Income Inequality. Journals of Developing Areas 43: 51–77. [Google Scholar] [CrossRef]

- Lan, Chu Khanh, and Chu Viet Hung. 2018. Effect of Financial Inclusion on Income Inequality: Evidence from Cross-Country Analysis. Available online: https://ssrn.com/abstract=3308044 (accessed on 30 July 2023).

- Law, Chee-Hong, and Siew-Voon Soon. 2020. The Impact of Inflation on Income Inequality: The Role of Institutional Quality. Applied Economics Letters 27: 1735–38. [Google Scholar] [CrossRef]

- Lee, Dong Jin, and Jong Chil Son. 2016. Economic Growth and Income Inequality: Evidence from Dynamic Panel Investigation. Global Economic Review 45: 331–58. [Google Scholar] [CrossRef]

- Lee, Jong-Wha, and José De Gregorio. 2002. Education and Income Inequality: New Evidence from Cross-Country Data. Review of Income and Wealth 48: 395–416. [Google Scholar] [CrossRef]

- Lin, Faqin, and Dahai Fu. 2016. Trade. Institution Quality and Income Inequality. World Development 77: 129–42. [Google Scholar] [CrossRef]

- Lucas, Henry, and Richard Sylla. 2003. The Global Impact of the Internet: Widening the Economic Gap Between Wealthy and Poor Nations? Prometheus 21: 1–22. [Google Scholar] [CrossRef]

- Madukala, J. I., and M. T. Silva. 2022. Financial Inclusion, Poverty, and Income Inequality in Sri Lanka. Sri Lankan Journal of Business Economics 2: 22–38. [Google Scholar] [CrossRef]

- Menyelim, Chima, Abiola Babajide, Alexander Omankhanlen, and Benjamin Ehikioya. 2021. Financial Inclusion, Income Inequality and Sustainable Economic Growth in Sub-Saharan African Countries. Sustainability 13: 1780. [Google Scholar] [CrossRef]

- Meschi, Elena, and Marco Vivarelli. 2009. Trade and income inequality in developing countries. World Development 37: 287–302. [Google Scholar] [CrossRef]

- Ofori, Isaac K., Emmanuel Y. Gbolonyo, Toyo Amègnonna M. Dossou, and Richard K. Nkrumah. 2022. Remittances and Income Inequality in Africa: Financial development thresholds for economic policy. Research in Globalization 4: 100084. [Google Scholar] [CrossRef]

- Omar, Md Abdullah, and Kazuo Inaba. 2020. Does financial inclusion reduce poverty and income inequality in developing countries? A panel data analysis. Economic Structures 9: 37. [Google Scholar] [CrossRef]

- Pazarbasioglu, Ceyla, and Alfonso Garcia Mora. 2020. Expanding Digital Financial Services Can Help Developing Economies Cope with Crisis Now and Boost Growth Later. Available online: https://blogs.worldbank.org/voices/expanding-digital-financial-services-can-help-developing-economies-cope-crisis-now-and-boost-growth-later (accessed on 10 August 2023).

- Polacko, Matthew. 2021. Causes and Consequences of Income Inequality—An Overview. Statistics, Politics and Policy 12: 341–57. [Google Scholar] [CrossRef]

- Polloni-Silva, Eduardo, Naijela da Costa, Herick Fernando Moralles, and Mario Sacomano Neto. 2021. Does Financial Inclusion Diminish Poverty and Inequality? A Panel Data Analysis for Latin American Countries. Social Indicators Research 158: 889–925. [Google Scholar] [CrossRef] [PubMed]

- Prasad, Eswar. 2021. New Financial Technologies, Sustainable Development, and the International Monetary System. ADBI Working Paper 1277. Tokyo: Asian Development Bank Institute (ADBI). [Google Scholar]

- Raychaudhuri, Ajitava, and Prabir De. 2016. Trade, Infrastructure, and Income Inequality in Selected Asian Countries Empirical analysis. In International Trade and International Finance. New Delhi: Springer, pp. 257–78. [Google Scholar] [CrossRef]

- Rodrguez-Pose, Andrés, and Vassilis Tselios. 2009. Education and Income Inequality in the Regions of the European union. Journal of Regional Science 49: 411–37. [Google Scholar] [CrossRef]

- Rougoor, Ward, and Charles Van Marrewijk. 2015. Demography, Growth, and Global Income Inequality. World Development 74: 220–32. [Google Scholar] [CrossRef]

- Rubin, Amir, and Dan Segal. 2015. The Effects of Economic Growth on Income Inequality in the US. Journal of Macroeconomics 45: 258–73. [Google Scholar] [CrossRef]

- Rudra, Pradhan, Arvin Mak, and Norman Neville. 2015. The dynamics of information and communications technologies infrastructure, economic growth, and financial development evidence from Asian countries. Technology in Society 42: 135–49. [Google Scholar] [CrossRef]

- Saraswati, Birgitta Dian, Ghozali Maski, David Kalug, and Rachmad Kresna Sakti. 2020. Does Financial Technology Affect Income Inequality in Indonesia? In 3rd International Research Conference on Economics and Business. Malang: Universitas Negeri Malang (UM), pp. 151–61. [Google Scholar] [CrossRef]

- Sassi, Seifallah, and Mohamed Goaied. 2013. Financial development, ICT diffusion, and economic growth: Lessons from the MENA region. Telecommunication Policy 37: 252–61. [Google Scholar] [CrossRef]

- Shamim, Farkhanda. 2007. The ICT environment, financial sector, and economic growth: Across a country analysis. Journal of Economic Studies 34: 352–67. [Google Scholar] [CrossRef]

- Silva, Julie A. 2007. Trade and Income Inequality in a Less Developed Country: The case of Mozambique. Economic Geography 83: 111–36. [Google Scholar] [CrossRef]

- Silva, Julie A., and Robin M. Leichenko. 2004. Regional Income Inequality and International Trade. Economic Geography 80: 261–86. [Google Scholar] [CrossRef]

- Soro, Kolotioloman, and Melain Modeste Senou. 2023. Digital financial inclusion and income inequality in WAEMU: What causality for what heterogeneity? Cogent Economics & Finance 11: 2. [Google Scholar] [CrossRef]

- Stiglitz, Joseph E. 2016. How to Restore Equitable and Sustainable Economic Growth in the United States. American Economic Review 106: 43–47. [Google Scholar] [CrossRef]

- Sylwester, Kevin. 2000. Can education expenditures reduce income inequality? Economics of Education Review 21: 43–52. [Google Scholar] [CrossRef]

- Tita, Anthanasius Fomum, and Meshach Jesse Aziakpono. 2017. The relationship between financial inclusion and income inequality in sub-Saharan Africa: Evidence from disaggregated data. African Review of Economics and Finance 9: 30–65. [Google Scholar]

- World Bank. 2021. The Global Findex Database 2021. Available online: https://www.worldbank.org/en/publication/globalfindex/interactive-executive-summary-visualization (accessed on 10 September 2023).

- World Bank. 2022. Available online: https://www.worldbank.org/en/topic/financialinclusion/overview (accessed on 27 August 2023).

- Yermack, David. 2018. FinTech in Sub-Saharan Africa: What Has Worked Well, and What Has Not. Working paper 25007. Cambridge: National Bureau of Economic Research. [Google Scholar] [CrossRef]

- Zhang, Shu, Feng Li, and Jing Jian Xiao. 2020. Internet Penetration and Consumption Inequality in China. International Journal of Consumer Studies 44: 407–22. [Google Scholar] [CrossRef]

- Zhang, Xun, Jiajia Zhang, Guanghua Wan, and Zhi Luo. 2020. Fintech, Growth, and Inequality: Evidence from China’s Household Survey Data. The Singapore Economic Review 65: 75–93. [Google Scholar] [CrossRef]

- Zheng, Zhijie. 2020. Inflation and Income Inequality in a Schumpeterian economy with Menu Costs. Economics Letters 186: 108524. [Google Scholar] [CrossRef]

{kind=link}

| Name of Variable | Source of Data | Definition and Measurement |

|---|---|---|

| ||

| Gini coefficient—Disposable | The Standardized World Income Inequality Database (SWIID) | Net Inequality |

| Palma ratio | The Standardized World Income Inequality Database (SWIID) | Net Inequality |

| ||

| FinTech | Global Findex | Send and receive digital payment (% age 15+) |

| ||

| Financial inclusion | Global Findex | (Account, saving, borrowing) |

| ||

| ICT infrastructure | Telecommunication Union (ITU) World Telecommunication/ICT Indicators Database | Internet broadband penetration and cell phone subscriber per 100 persons |

| Consumer price index | World development indicator (World Bank Data) | Inflation rate |

| Trade | World development indicator (World Bank Data) | Trade % Of GDP |

| Education | World development indicator (World Bank Data) | Secondary school enrolment rate |

| Population | World development indicator (World Bank Data) | Population growth annual rate |

| Economic growth | World development indicator (World Bank Data) | Real GDP per capita growth |

| Variable | Observation | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|---|

| GINI | 87 | 51.15 | 9.65 | 32.00 | 68.00 |

| Palma | 87 | 4.52 | 3.13 | 1.00 | 18.00 |

| Fintech | 87 | 0.38 | 0.22 | 0.04 | 0.90 |

| Account | 87 | 0.45 | 0.22 | 0.07 | 0.94 |

| Saving | 87 | 0.51 | 0.13 | 0.17 | 0.76 |

| Borrowing | 87 | 0.50 | 0.13 | 0.26 | 0.86 |

| Mobile | 87 | 1.99 | 0.11 | 1.74 | 2.21 |

| Internet | 87 | 1.42 | 0.34 | 0.73 | 1.92 |

| RGDPG | 87 | 1.49 | 2.93 | −8.12 | 7.51 |

| Trade | 87 | 1.78 | 0.16 | 1.35 | 2.12 |

| Inflation | 87 | 8.40 | 19.91 | −1.09 | 154.76 |

| Govt exp | 87 | 14.50 | 5.14 | 2.36 | 27.73 |

| Education | 87 | 1.93 | 0.06 | 1.74 | 2.00 |

| Population | 87 | 2.39 | 1.64 | −2.42 | 11.79 |

| 1 | 2 | |

|---|---|---|

| Variables | GINI | PALMA |

| FinTech | 67.66 | 14.21 |

| (0.002) *** | (0.096) * | |

| Account | −56.55 | −13.56 |

| (0.006) *** | (0.095) * | |

| Saving | 34.99 | 9.164 |

| (0.001) *** | (0.021) ** | |

| Borrowing | −17.66 | −3.07 |

| (0.065) * | (0.417) | |

| Mobile phone | 0.00288 | 0.00842 |

| (0.939) | (0.576) | |

| Internet | −0.175 | −0.0408 |

| (0.001) *** | (0.052) * | |

| RGDPG | 0.292 | −0.0475 |

| (0.369) | (0.713) | |

| Trade | 0.0426 | −0.00816 |

| (0.326) | (0.636) | |

| Inflation | 0.0463 | 0.0196 |

| (0.323) | (0.295) | |

| Govt exp | 0.550 | 0.255 |

| (0.008) *** | (0.002) *** | |

| Education | 0.263 | 0.0419 |

| (0.001) *** | (0.017) ** | |

| Population | 0.622 | 0.0573 |

| (0.288) | (0.805) | |

| Constant | 11.81 | −4.363 |

| (0.254) | (0.291) | |

| Observations | 87 | 87 |

| R-squared | 0.544 | 0.311 |

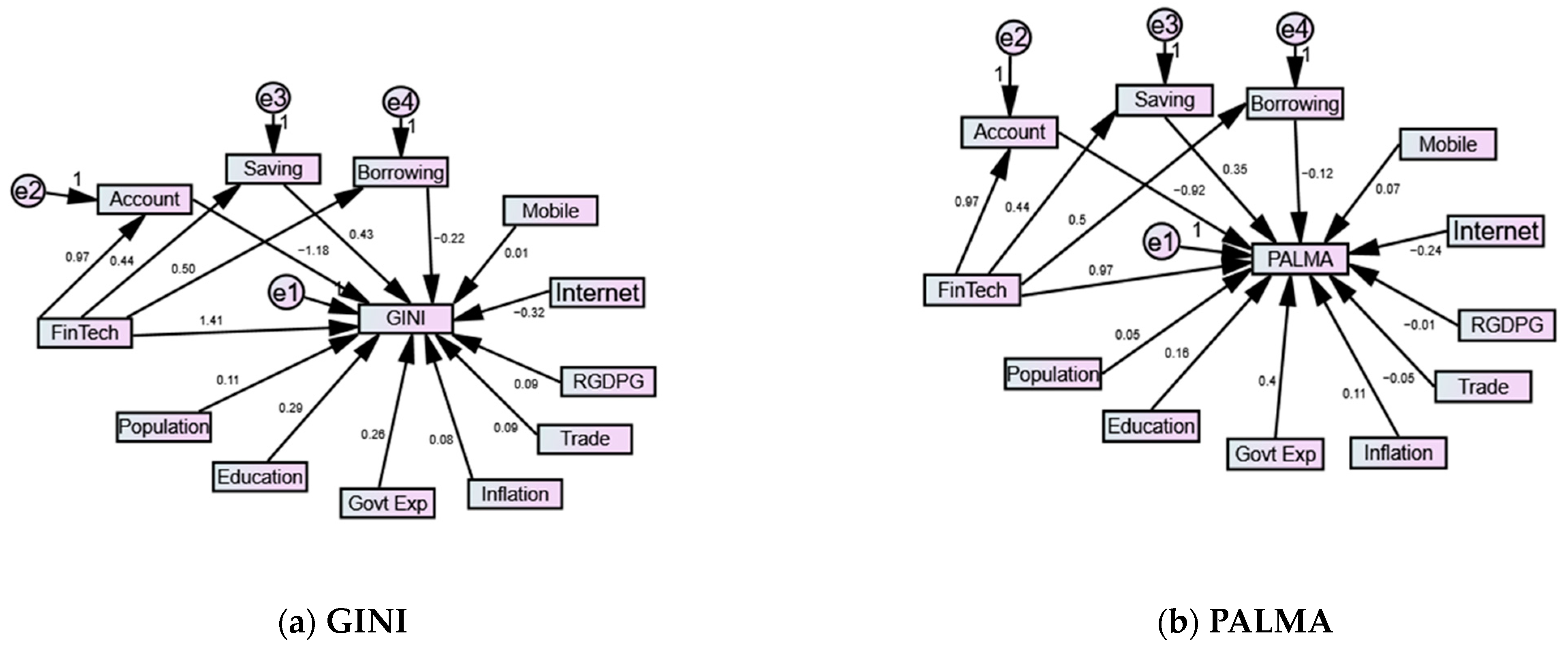

| GINI | PALMA Ratio | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Estimate | p-Value | Estimate | p-Value | ||||||

| Account | <--- | FinTech | 0.974 | *** | Account | <--- | FinTech | 0.974 | *** |

| Saving | <--- | FinTech | 0.44 | *** | Saving | <--- | FinTech | 0.44 | *** |

| Borrowing | <--- | FinTech | 0.496 | *** | Borrowing | <--- | FinTech | 0.496 | *** |

| GINI | <--- | FinTech | 1.407 | *** | PALMA | <--- | FinTech | 0.967 | ** |

| GINI | <--- | Account | −1.176 | *** | PALMA | <--- | Account | −0.924 | ** |

| GINI | <--- | Saving | 0.429 | *** | PALMA | <--- | Saving | 0.354 | *** |

| GINI | <--- | Borrowing | −0.223 | ** | PALMA | <--- | Borrowing | −0.12 | 0.194 |

| GINI | <--- | Trade | 0.087 | 0.163 | PALMA | <--- | Govt Exp | 0.396 | *** |

| GINI | <--- | Inflation | 0.077 | 0.213 | PALMA | <--- | Inflation | 0.113 | 0.159 |

| GINI | <--- | Govt Exp | 0.259 | *** | PALMA | <--- | Trade | −0.049 | 0.543 |

| GINI | <--- | Population | 0.115 | * | PALMA | <--- | RGDPG | −0.014 | 0.862 |

| GINI | <--- | Education | 0.29 | *** | PALMA | <--- | Internet | −0.238 | ** |

| GINI | <--- | RGDPG | 0.093 | 0.134 | PALMA | <--- | Mobile | 0.068 | 0.397 |

| GINI | <--- | Internet | −0.323 | *** | PALMA | <--- | Population | 0.047 | 0.553 |

| GINI | <--- | Mobile | 0.015 | 0.813 | PALMA | <--- | Education | 0.161 | ** |

| Variables | Total effect FinTech | Indirect effect FinTech | Variable | Total effect FinTech | Indirect effect FinTech | ||||

| Account | 0.974 | 0 | Account | 0.974 | 0 | ||||

| Saving | 0.44 | 0 | Saving | 0.44 | 0 | ||||

| Borrowing | 0.496 | 0 | Borrowing | 0.496 | 0 | ||||

| GINI | 0.34 | −1.067 | PALMA | 0.164 | −0.804 | ||||

| Model fit indices—GINI | Model fit indices—Palma | ||||||||

| NFI 0.901, RFI 0.946, IFI 0.934, TLI 0.912 CFI 0.957, REMSA 0.002, SRMR 0.005 | NFI 0.897, RFI 0.901, IFI 0.9721, TLI 0.943 CFI 0.905, REMSA 0.002, SRMR 0.004 | ||||||||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Girma, A.G.; Huseynov, F. The Causal Relationship between FinTech, Financial Inclusion, and Income Inequality in African Economies. J. Risk Financial Manag. 2024, 17, 2. https://doi.org/10.3390/jrfm17010002

Girma AG, Huseynov F. The Causal Relationship between FinTech, Financial Inclusion, and Income Inequality in African Economies. Journal of Risk and Financial Management. 2024; 17(1):2. https://doi.org/10.3390/jrfm17010002

Chicago/Turabian StyleGirma, Abebe Gule, and Fariz Huseynov. 2024. "The Causal Relationship between FinTech, Financial Inclusion, and Income Inequality in African Economies" Journal of Risk and Financial Management 17, no. 1: 2. https://doi.org/10.3390/jrfm17010002

APA StyleGirma, A. G., & Huseynov, F. (2024). The Causal Relationship between FinTech, Financial Inclusion, and Income Inequality in African Economies. Journal of Risk and Financial Management, 17(1), 2. https://doi.org/10.3390/jrfm17010002