Russia–Ukraine Conflict, Commodities and Stock Market: A Quantile VAR Analysis

Abstract

1. Introduction

- Is there a relationship between the Eurostoxx 50 index and real market variables, such as the wheat futures price and the TTF gas futures price?

- If such a relationship exists, in which direction and with which characteristics does it manifest?

- If such a relationship exists, did it arise after the conflict broke out, or was it already present before?

2. Literature Review

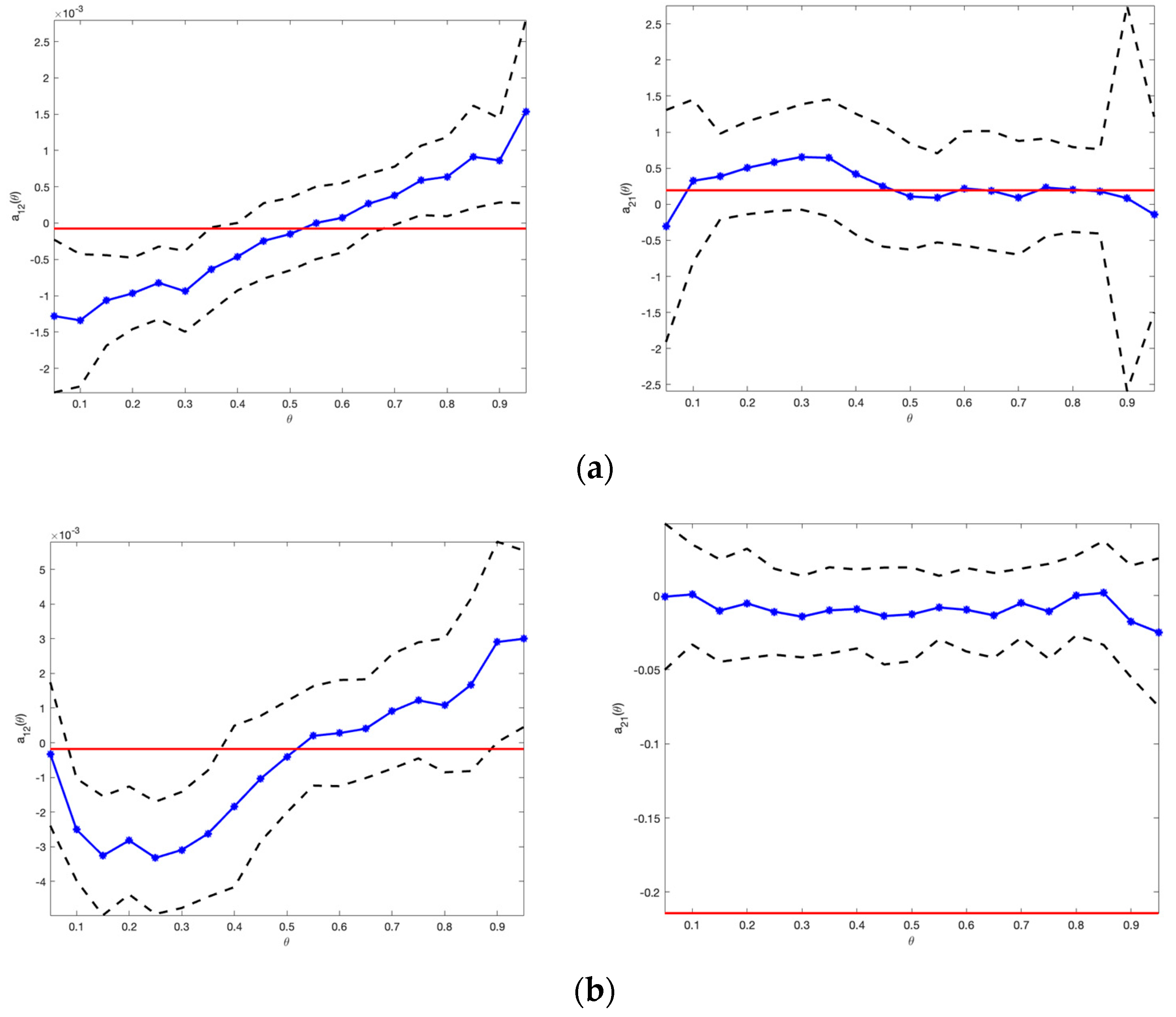

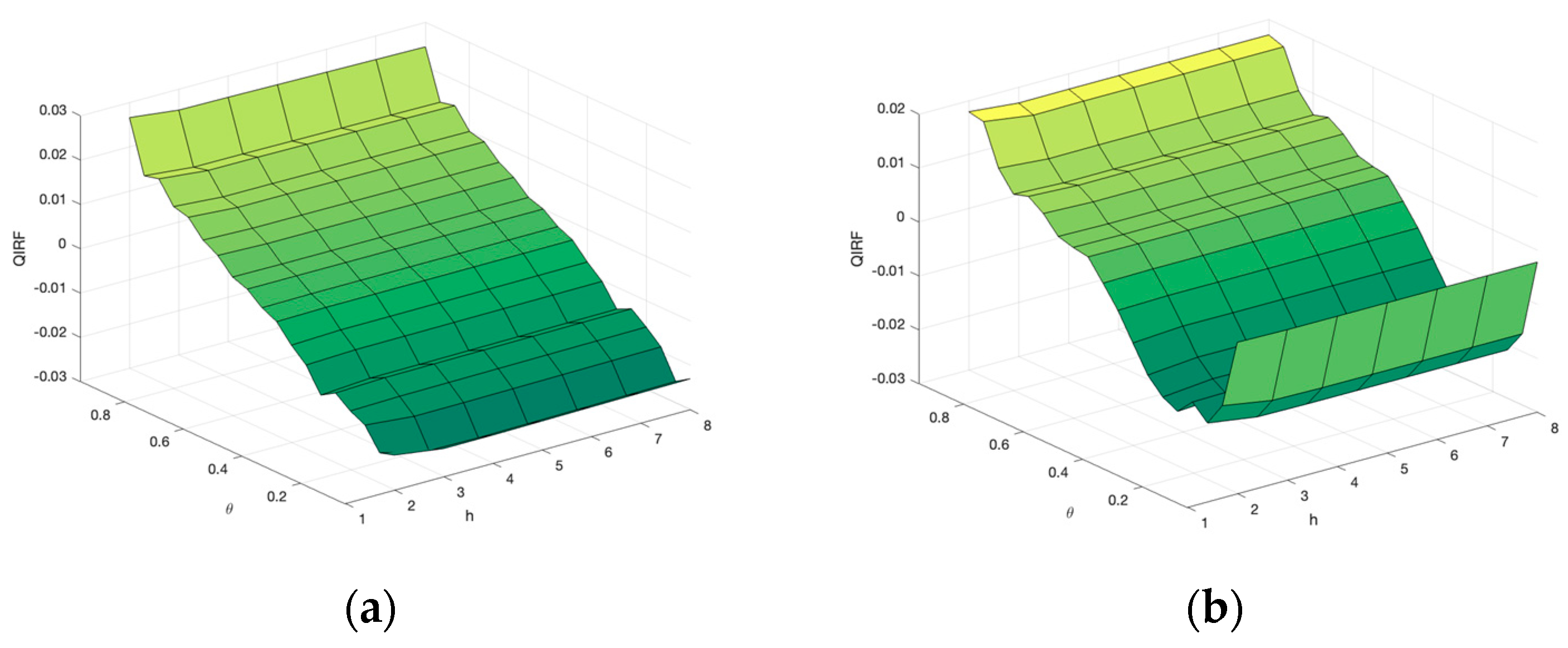

3. Materials and Methods

4. Results

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Adekoya, Oluwasegun B., Johnson A. Oliyide, OlaOluwa S. Yaya, and Mamdouh Abdulaziz Saleh Al-Faryan. 2022. Does oil connect differently with prominent assets during war? Analysis of intra-day data during the Russia-Ukraine saga. Resources Policy 77: 102728. [Google Scholar] [CrossRef]

- Adekoya, Oluwasegun B., Mahdi Ghaemi Asl, Johnson A. Oliyide, and Parviz Izadi. 2023. Multifractality and cross-correlation between the crude oil and the European and non-European stock markets during the Russia-Ukraine war. Resources Policy 80: 103134. [Google Scholar] [CrossRef]

- Adrian, Tobias, and Makus Brunnermeier. 2016. CoVar. American Economic Review 106: 1705–41. [Google Scholar] [CrossRef]

- Alam, Md. Kausar, Mosab I. Tabash, Mabruk Billah, Sanjeev Kumar, and Suhaib Anagreh. 2022. The impacts of the Russia-Ukraine invasion on global markets and commodities: A dynamic connectedness among G7 and BRIC markets. Journal of Risk and Financial Management 15: 352. [Google Scholar] [CrossRef]

- Algieri, Bernardina, and Arturo Leccadito. 2017. Assessing contagion risk from energy and non-energy commodity markets. Energy Economics 62: 312–22. [Google Scholar] [CrossRef]

- An, Henry, Feng Qui, and James Rude. 2021. Volatility spillovers between food and fuel markets: Do administrative regulations affect the transmission? Economic Modelling 102: 105552. [Google Scholar] [CrossRef]

- Bagchi, Bhaskar, and Biswajit Paul. 2023. Effects of crude oil prices shocks on stock markets and currency exchange rates in the context of Russia-Ukraine conflict: Evidence from G7 countries. Journal of Risk and Financial Management 16: 64. [Google Scholar] [CrossRef]

- Chavleishvili, Sulkhan, and Simone Manganelli. 2019. Forecasting and Stress Testing with Quantile Vector Autoregression. Working Paper Series No. 2330; Frankfurt: European Central Bank. [Google Scholar]

- Clancey-Shang, Danjue, and Chengbo Fu. 2023. The Russia-Ukraine conflict and foreign stocks on the US market. Journal of Risk Finance 24: 6–23. [Google Scholar] [CrossRef]

- De Cesari, Amedeo, Alberto Manelli, Roberta Pace, and Maria Leone. 2018. The sustainability of the interaction between financial and commodity markets. Rivista di Studi sulla Sostenibilità 2: 133–53. [Google Scholar] [CrossRef]

- Fang, Yi, and Zhiquan Shao. 2022. The Russia-Ukraine conflict and volatility risk of commodity markets. Finance Research Letters 50: 103264. [Google Scholar] [CrossRef]

- Garderbroek, Cornelis, and Manuel A. Hernandez. 2013. Do energy prices stimulate food price volatility? Examing volatility transmission between US oil, ethanol and corn markets. Energy Economics 40: 119–29. [Google Scholar] [CrossRef]

- Glauben, Thomas, Soren Prehn, Tebbe Dannemann, Bernhard Brummer, and Jens-Peter Loy. 2014. Options Trading in Agricultural Futures Markets: A Reasonable Instrument of Risk Hedging, or a Driver of Agricultural Price Volatility? IAMO Policy Brief No. 919-2016-72756. Halle: Institute of Agricultural Development in Transition Economies (IAMO). [Google Scholar]

- Gong, Xu, Kequin Guan, Liquing Chen, Tangyong Liu, and Chengbo Fu. 2021. What drives oil prices?—A Markov switching VAR approach. Resources Policy 74: 102316. [Google Scholar] [CrossRef]

- Guilleminot, Benoit, Jean-Jacques Ohana, and Steve Ohana. 2014. The interaction of speculators and index investors in agricultural derivatives markets. Agricultural Economics 45: 767–92. [Google Scholar] [CrossRef]

- Hallin, Marc, and Miroslav Siman. 2017. Multiple-output quantile regression. In Handbook of Quantile Regression. Boca Raton: CRC Press LLC. [Google Scholar]

- Hardle, Wolfgang Karl, Weining Wang, and Lining Yu. 2016. TENET: Tail-Event driven NETwork risk. Journal of Econometrics 192: 499–513. [Google Scholar] [CrossRef]

- Huchet, Nicolas, and Papa G. Fam. 2016. The role of speculation in international futures markets on commodity prices. Research in International Business and Finance 37: 49–65. [Google Scholar] [CrossRef]

- Jebabli, Ikram, and David Roubaud. 2018. Time-varying efficiency in food and energy markets: Evidence and implications. Economic Modelling 70: 97–114. [Google Scholar] [CrossRef]

- Jebabli, Ikram, Mohamed Arouri, and Frederic Teulon. 2014. On the effects of world stock market and oil price shocks on food prices: An empirical investigation based on TVP-VER models with stochastic volatility. Energy Economics 45: 66–98. [Google Scholar] [CrossRef]

- Khalfaoui, Rabeh, Eduard Baumohl, Suleman Sarwar, and Tomas Vyrost. 2021. Connectedness between energy and nonenergy commodity markets: Evidence from quantile coherency networks. Resources Policy 74: 102318. [Google Scholar] [CrossRef]

- Koenker, Roger. 2005. Quantile Regression. Cambridge: Cambridge University Press. [Google Scholar]

- Koenker, Roger, and Gilbert J. Bassett. 1978. Regression quantiles. Econometrica 46: 33–50. [Google Scholar] [CrossRef]

- Koenker, Roger, and Zhijie Xiao. 2006. Quantile autoregression. Journal of the American Statistical Association 101: 980–1006. [Google Scholar] [CrossRef]

- Kumari, Vineeta, Gaurav Kumar, and Dharen Kumar Pandey. 2023. Are the European Union stock markets vulnerable to the Russia-Ukraine war? Journal of Behavioral and Experimental Finance 37: 100793. [Google Scholar] [CrossRef]

- Martins, Antonio Miguel, Pedro Correia, and Ricardo Gouveia. 2023. Russia-Ukraine conflict: The effects on European banks’ stock market returns. Journal of multinational Financial Management 67: 100786. [Google Scholar] [CrossRef]

- Masters, Michael W. 2008. Testimony before the Committee on Homeland Security and Governmental Affairs United States Senate. Available online: https://www.hsgac.senate.gov/wp-content/uploads/imo/media/doc/052008Masters.pdf (accessed on 1 January 2024).

- Mensi, Walid, Makram Beljid, Adel Boubaker, and Shunsuke Managi. 2013. Correlations and volatility spillovers across commodity and stock markets: Linking energies, food, and gold. Economic Modelling 32: 15–22. [Google Scholar] [CrossRef]

- Nerlinger, Martin, and Sebastian Utz. 2022. The impact of Russia-ukraine conflict on energy firms: A capital market perspective. Finance Research Letters 50: 103243. [Google Scholar] [CrossRef]

- Obi, Pat, Freshia Waweru, and Moses Nyangu. 2023. An event study on the reaction of equity and commodity markets to the onset of the Russia-Ukraine conflict. Journal of Risk and Financial Management 16: 256. [Google Scholar] [CrossRef]

- Sanders, Dwight R., and Scott H. Irwin. 2011. New evidence on the impact of index funds in U.S. grain futures markets. Canadian journal of Agricultural Economics 59: 519–32. [Google Scholar] [CrossRef]

- Serra, Teresa. 2011. Volatility spillovers between food and energy markets: A semiparametric approach. Energy Economics 33: 1155–64. [Google Scholar] [CrossRef]

- Tang, Ke, and Wei Xiong. 2012. Index investment and the financialization of commodities. Financial Analysts Journal 68: 54–74. [Google Scholar] [CrossRef]

- Tosun, Onur K., and Arman Eshraghi. 2022. Corporate decisions in times of war: Evidence from the Russia-Ukraine conflict. Finance Research Letters 48: 102920. [Google Scholar] [CrossRef]

- Umar, Zaghum, Ahmed Bossman, Sun-Yong Choi, and Tamara Teplova. 2022. Does geopolitical risk matter for global asset returns? Evidence from quantile-on-quantile regression. Finance Research Letters 48: 102991. [Google Scholar] [CrossRef]

- UNCTAD. 2022. The Impact on the Trade and Development in the War in Ukraine. Available online: unctad.org/system/files/official-document/osginf2022d1_en.pdf (accessed on 1 January 2024).

- Wang, Xiaoyang. 2022. Efficient market are more connected: An entropy-based analysis of the energy, industrial metal and financial markets. Energy Economics 111: 106067. [Google Scholar] [CrossRef]

- Wang, Yihan, Elie Bouri, Zeeshan Fareed, and Yuhui Dai. 2022. Geopolitical risk and the systemic risk in the commodity markets under the war in Ukraine. Finance Research Letters 49: 103066. [Google Scholar] [CrossRef]

- Wei, Wen H. 2009. On regression model selection for the data with correlated errors. Annals of the Institute of Statistical Mathematics 61: 291–308. [Google Scholar] [CrossRef]

- White, Halbert, Tae-Hwan Kim, and Simone Manganelli. 2015. VAR for VAR: Measuring tail dependence using multivariate regression quantile. Journal of Econometrics 187: 169–88. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Eurostoxx 50—Wheat and TTF | ||||

| taus | ||||

| 0.01 | 0.05 | 0.95 | 0.99 | |

| Wheat | 0.30846 *** | 0.23613 *** | 0.29235 *** | 0.28593 *** |

| (0.4130) | (0.2190) | (0.00814) | (0.00633) | |

| TTF | 0.06966 *** | 0.05829 *** | 0.06545 *** | 0.06071 *** |

| (0.01188) | (0.00823) | (0.00821) | (0.00146) | |

| Wheat and TTF—Eurostoxx 50 | ||||

| taus | ||||

| 0.01 | 0.05 | 0.95 | 0.99 | |

| Wheat | −0.12725 (0.21221) | 1.66857 *** (0.56462) | 1.60796 *** (0.09548) | 1.87666 *** (0.11383) |

| TTF | 4.51014 *** (0.030943) | 5.63083 *** (0.41008) | 1.97677 (1.35020) | 2.34817 *** (1.21809) |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Manelli, A.; Pace, R.; Leone, M. Russia–Ukraine Conflict, Commodities and Stock Market: A Quantile VAR Analysis. J. Risk Financial Manag. 2024, 17, 29. https://doi.org/10.3390/jrfm17010029

Manelli A, Pace R, Leone M. Russia–Ukraine Conflict, Commodities and Stock Market: A Quantile VAR Analysis. Journal of Risk and Financial Management. 2024; 17(1):29. https://doi.org/10.3390/jrfm17010029

Chicago/Turabian StyleManelli, Alberto, Roberta Pace, and Maria Leone. 2024. "Russia–Ukraine Conflict, Commodities and Stock Market: A Quantile VAR Analysis" Journal of Risk and Financial Management 17, no. 1: 29. https://doi.org/10.3390/jrfm17010029

APA StyleManelli, A., Pace, R., & Leone, M. (2024). Russia–Ukraine Conflict, Commodities and Stock Market: A Quantile VAR Analysis. Journal of Risk and Financial Management, 17(1), 29. https://doi.org/10.3390/jrfm17010029