The Role of ERM and Corporate Governance in Managing COVID-19 Impacts: SMEs Perspective

Abstract

1. Introduction

2. Literature Review: Defining the Constructs

2.1. COVID-19 Perceptions Construct

2.2. ERM Sophistication Construct

2.3. Corporate Governance Construct

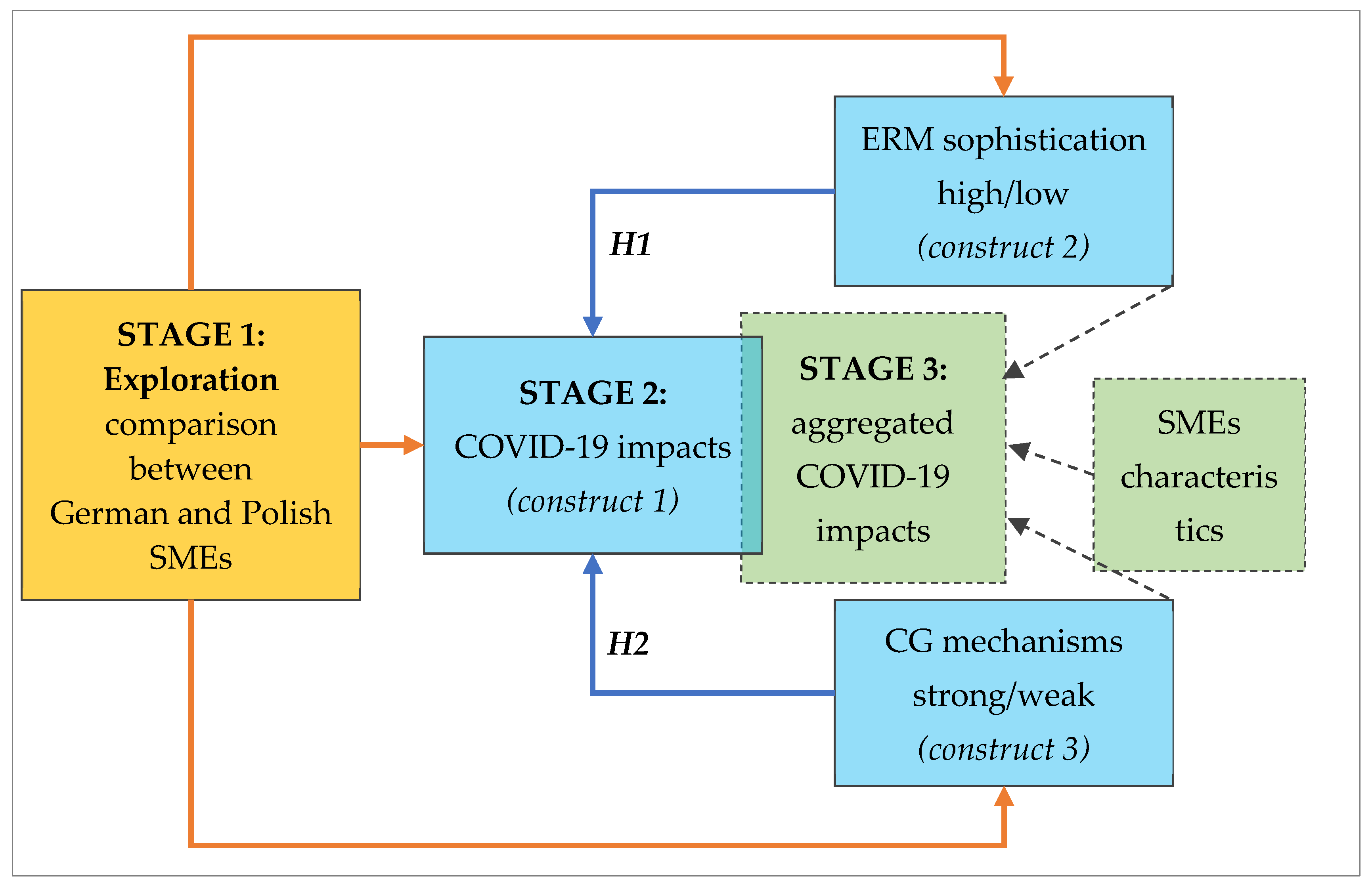

3. Research Design

3.1. Conceptual Map of Empirical Investigations

3.2. Survey Design

3.3. Sample Selection Scheme

4. Results

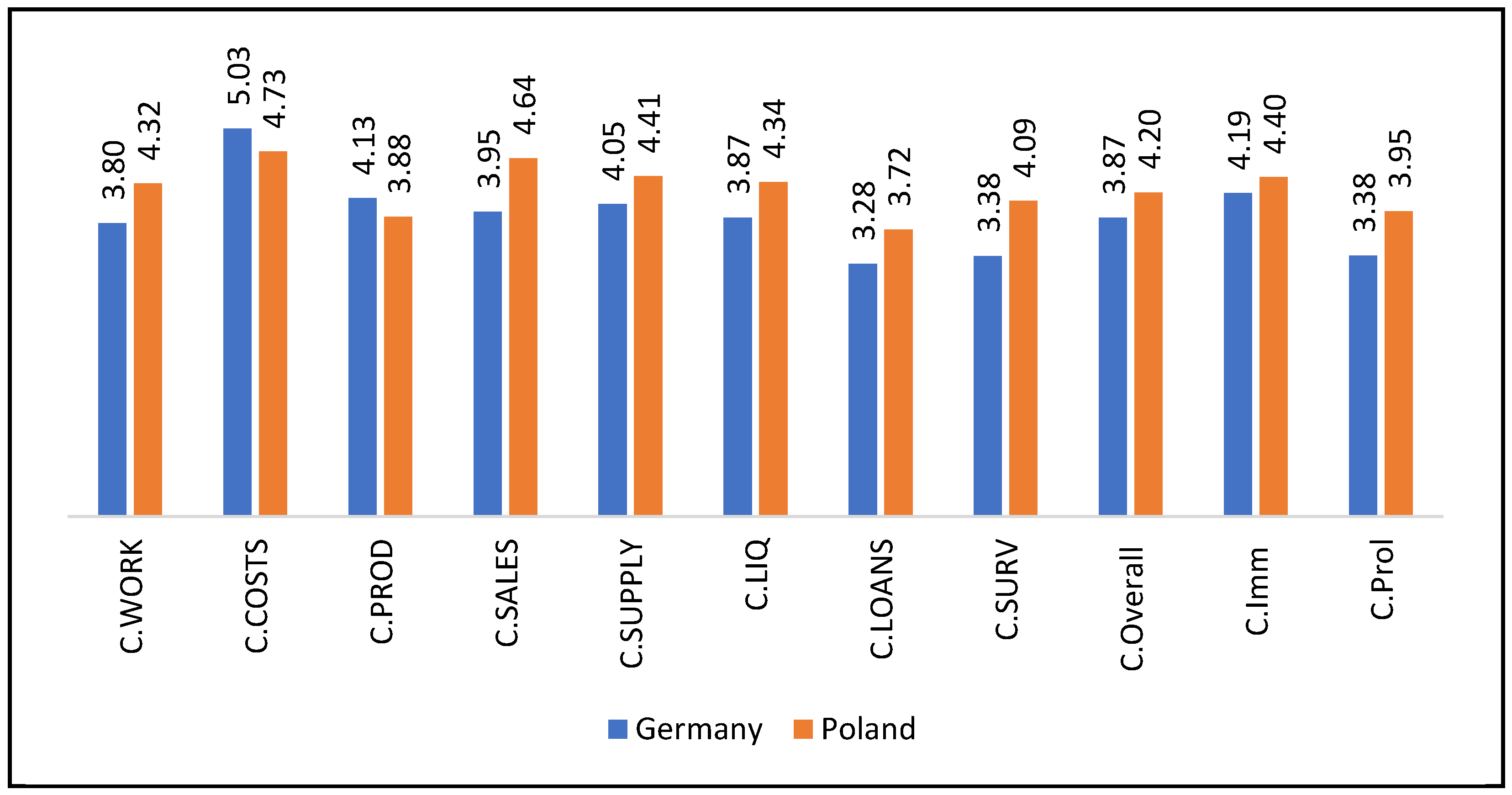

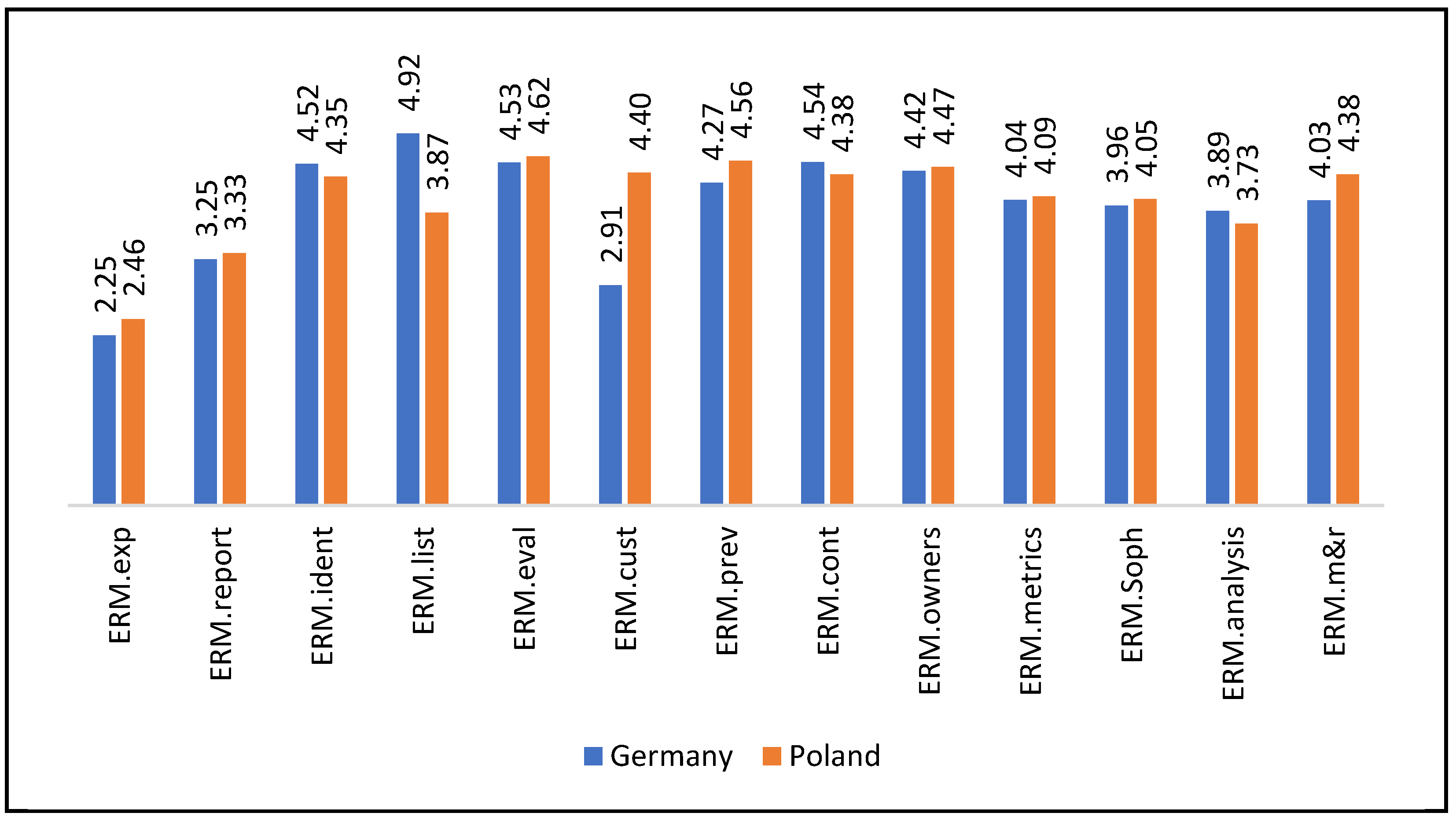

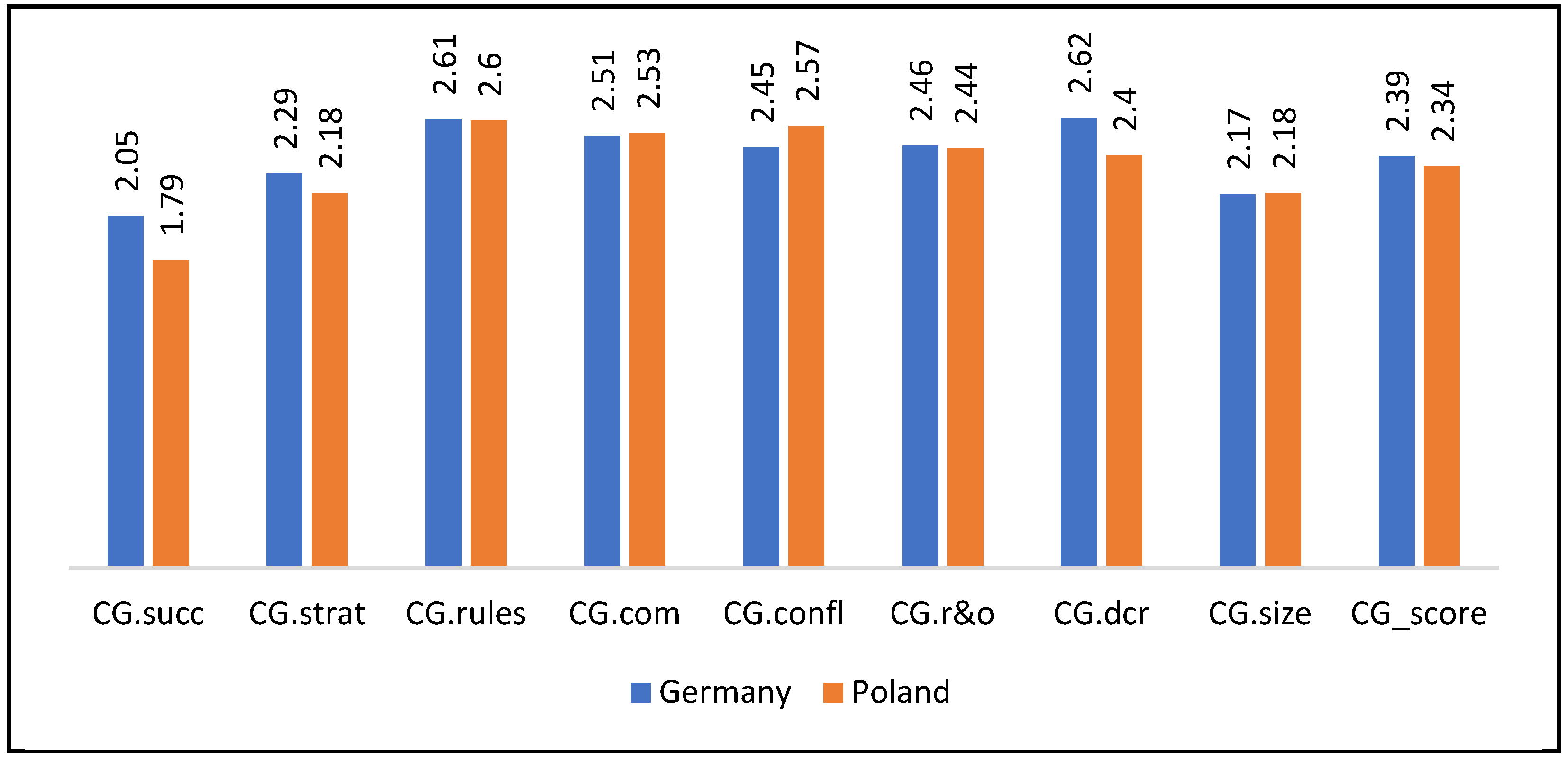

4.1. Exploration of Similarities and Differences between Germany and Poland: The Constructs

4.2. COVID-19 Impacts and ERM Sophistication (Hypothesis 1)

4.3. COVID-19 Impacts and Strength of CG Mechanisms (Hypothesis 2)

4.4. COVID-19 Impacts and SMEs Characteristics: Results of Quantile Regression

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A. Tests of Normality Distribution of Variables

| Germany | Poland | |||||||

| Kołmogorov-Smirnov | Shapiro-Wilk | Kołmogorov-Smirnov | Shapiro-Wilk | |||||

| Statistic | Sig. | Statistic | Sig. | Statistic | Sig. | Statistic | Sig. | |

| COVID-19 construct | ||||||||

| C.WORK | 0.198 | 0.000 | 0.198 | 0.000 | 0.803 | 0.000 | 0.803 | 0.000 |

| C.COSTS | 0.227 | 0.000 | 0.227 | 0.000 | 0.854 | 0.000 | 0.854 | 0.000 |

| C.PROD | 0.174 | 0.000 | 0.174 | 0.000 | 0.888 | 0.000 | 0.888 | 0.000 |

| C.SALES | 0.145 | 0.000 | 0.145 | 0.000 | 0.887 | 0.000 | 0.887 | 0.000 |

| C.SUPPLY | 0.155 | 0.000 | 0.155 | 0.000 | 0.920 | 0.000 | 0.920 | 0.000 |

| C.LIQ | 0.181 | 0.000 | 0.181 | 0.000 | 0.885 | 0.000 | 0.885 | 0.000 |

| C.LOANS | 0.199 | 0.000 | 0.199 | 0.000 | 0.866 | 0.000 | 0.866 | 0.000 |

| C.SURV | 0.161 | 0.000 | 0.161 | 0.000 | 0.904 | 0.000 | 0.904 | 0.000 |

| C.Overall | 0.073 | 0.028 | 0.073 | 0.028 | 0.986 | 0.081 | 0.986 | 0.081 |

| C.Imm | 0.060 | 0.200 | 0.060 | 0.200 | 0.991 | 0.401 | 0.991 | 0.401 |

| C.Prol | 0.087 | 0.003 | 0.087 | 0.003 | 0.970 | 0.001 | 0.970 | 0.001 |

| ERM sophistication construct | ||||||||

| ERM.exp | 0.256 | 0.000 | 0.256 | 0.000 | 0.787 | 0.000 | 0.787 | 0.000 |

| ERM.report | 0.204 | 0.000 | 0.204 | 0.000 | 0.864 | 0.000 | 0.864 | 0.000 |

| ERM.ident | 0.202 | 0.000 | 0.202 | 0.000 | 0.880 | 0.000 | 0.880 | 0.000 |

| ERM.list | 0.222 | 0.000 | 0.222 | 0.000 | 0.865 | 0.000 | 0.865 | 0.000 |

| ERM.eval | 0.180 | 0.000 | 0.180 | 0.000 | 0.906 | 0.000 | 0.906 | 0.000 |

| ERM.cust | 0.212 | 0.000 | 0.212 | 0.000 | 0.868 | 0.000 | 0.868 | 0.000 |

| ERM.prev | 0.152 | 0.000 | 0.152 | 0.000 | 0.924 | 0.000 | 0.924 | 0.000 |

| ERM.cont | 0.173 | 0.000 | 0.173 | 0.000 | 0.918 | 0.000 | 0.918 | 0.000 |

| ERM.owners | 0.222 | 0.000 | 0.222 | 0.000 | 0.873 | 0.000 | 0.873 | 0.000 |

| ERM.metrics | 0.149 | 0.000 | 0.149 | 0.000 | 0.917 | 0.000 | 0.917 | 0.000 |

| ERM.Soph | 0.079 | 0.011 | 0.079 | 0.011 | 0.970 | 0.001 | 0.970 | 0.001 |

| ERM.analysis | 0.096 | 0.001 | 0.096 | 0.001 | 0.960 | 0.000 | 0.960 | 0.000 |

| ERM.m&r | 0.077 | 0.016 | 0.077 | 0.016 | 0.973 | 0.002 | 0.973 | 0.002 |

| Strenght of CG mechanisms construct | ||||||||

| CG.succ | 0.206 | 0.000 | 0.206 | 0.000 | 0.806 | 0.000 | 0.806 | 0.000 |

| CG.strat | 0.346 | 0.000 | 0.346 | 0.000 | 0.717 | 0.000 | 0.717 | 0.000 |

| CG.rules | 0.406 | 0.000 | 0.406 | 0.000 | 0.656 | 0.000 | 0.656 | 0.000 |

| CG.com | 0.384 | 0.000 | 0.384 | 0.000 | 0.684 | 0.000 | 0.684 | 0.000 |

| CG.confl | 0.359 | 0.000 | 0.359 | 0.000 | 0.715 | 0.000 | 0.715 | 0.000 |

| CG.r&o | 0.349 | 0.000 | 0.349 | 0.000 | 0.725 | 0.000 | 0.725 | 0.000 |

| CG.dcr | 0.425 | 0.000 | 0.425 | 0.000 | 0.626 | 0.000 | 0.626 | 0.000 |

| CG.size | 0.266 | 0.000 | 0.266 | 0.000 | 0.787 | 0.000 | 0.787 | 0.000 |

| CG_score | 0.149 | 0.000 | 0.149 | 0.000 | 0.919 | 0.000 | 0.919 | 0.000 |

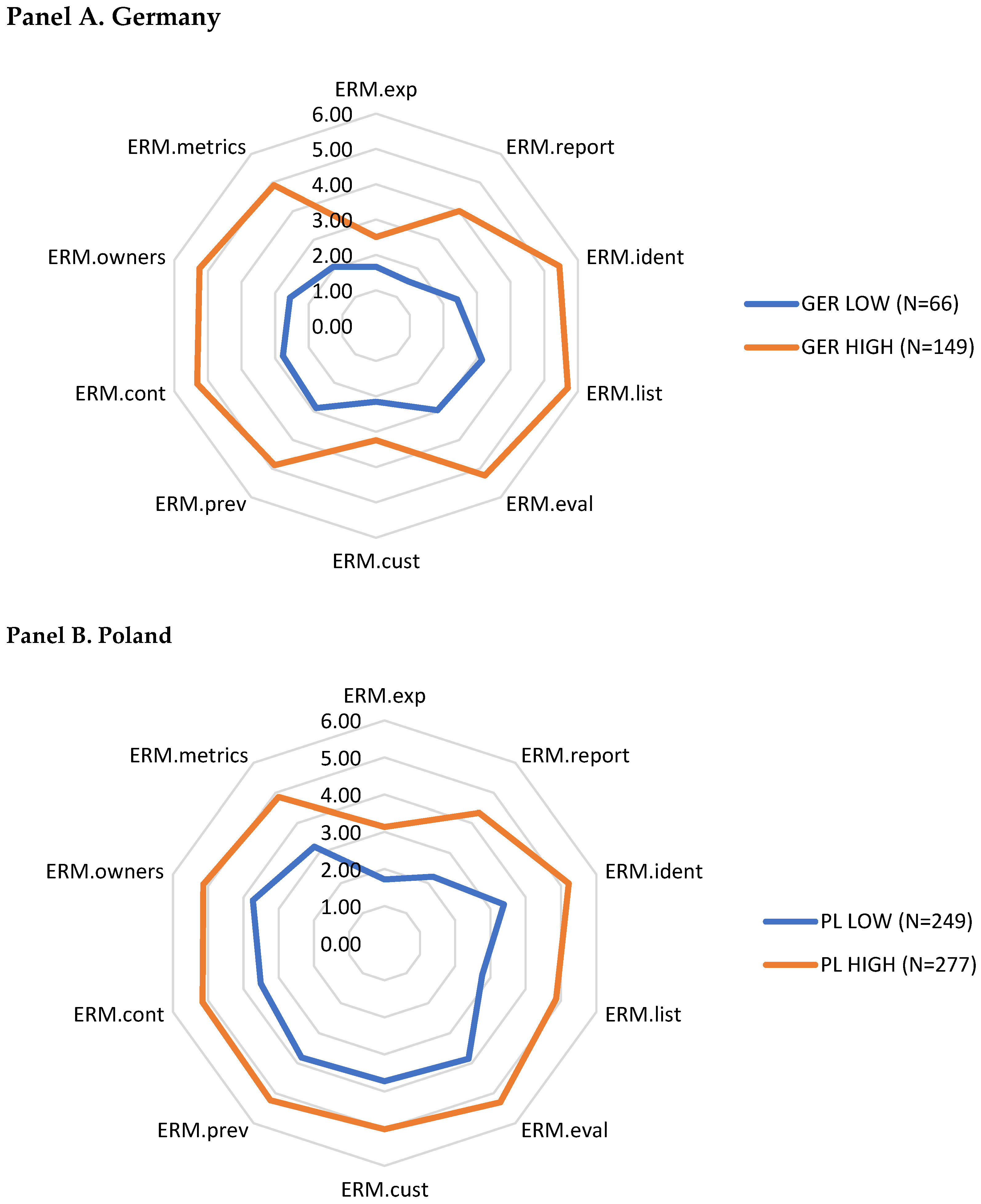

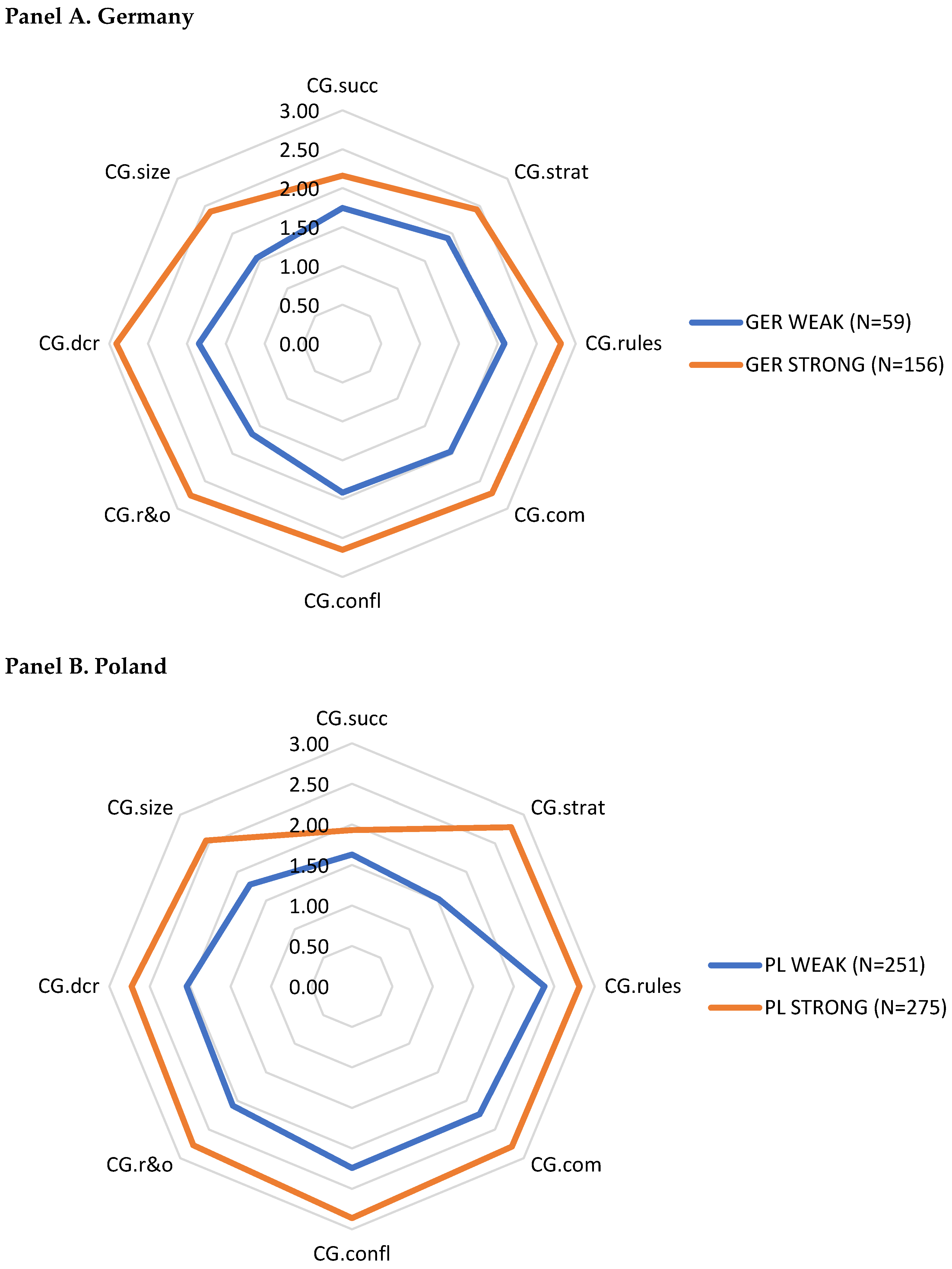

Appendix B. Results of K-Means Clustering

| Panel A. ERM sophistication construct | ||||||||

| Variable | Germany | Poland | ||||||

| Low (N = 66) | High (N = 149) | Low (N = 249) | High (N = 277) | |||||

| Mean | St.D. | Mean | St.D. | Mean | St.D. | Mean | St.D. | |

| ERM.exp | 1.67 | 1.19 | 2.50 | 1.65 | 1.72 | 0.87 | 3.13 | 1.57 |

| ERM.report | 1.55 | 0.88 | 4.01 | 1.92 | 2.22 | 1.09 | 4.34 | 1.37 |

| ERM.ident | 2.41 | 1.61 | 5.45 | 1.15 | 3.38 | 1.54 | 5.22 | 1.03 |

| ERM.list | 3.15 | 1.84 | 5.70 | 1.02 | 2.77 | 1.27 | 4.86 | 1.11 |

| ERM.eval | 2.95 | 1.54 | 5.23 | 1.42 | 3.85 | 1.54 | 5.30 | 1.01 |

| ERM.cust | 2.15 | 1.68 | 3.24 | 1.88 | 3.72 | 1.72 | 5.01 | 1.30 |

| ERM.prev | 2.88 | 1.74 | 4.88 | 1.59 | 3.81 | 1.45 | 5.23 | 1.00 |

| ERM.cont | 2.77 | 1.42 | 5.32 | 1.31 | 3.51 | 1.47 | 5.16 | 1.00 |

| ERM.owners | 2.56 | 1.61 | 5.25 | 1.57 | 3.73 | 1.47 | 5.14 | 1.09 |

| ERM.metrics | 2.06 | 1.19 | 4.91 | 1.47 | 3.22 | 1.26 | 4.86 | 1.05 |

| Panel B. Strength of corporate governance mechanisms | ||||||||

| Variable | Germany | Poland | ||||||

| Weak (N = 59) | Strong (N = 156) | Weak (N = 251) | Strong (N = 275) | |||||

| Mean | St.D. | Mean | St.D. | Mean | St.D. | Mean | St.D. | |

| CG.succ | 1.75 | 0.76 | 2.16 | 0.73 | 1.63 | 0.71 | 1.93 | 0.78 |

| CG.strat | 1.92 | 0.92 | 2.44 | 0.78 | 1.52 | 0.78 | 2.78 | 1.12 |

| CG.rules | 2.08 | 0.75 | 2.81 | 0.41 | 2.38 | 0.64 | 2.81 | 0.43 |

| CG.com | 1.97 | 0.72 | 2.72 | 0.48 | 2.23 | 0.64 | 2.80 | 0.45 |

| CG.confl | 1.92 | 0.70 | 2.65 | 0.57 | 2.24 | 0.66 | 2.86 | 0.38 |

| CG.r&o | 1.64 | 0.55 | 2.76 | 0.44 | 2.08 | 0.68 | 2.77 | 0.46 |

| CG.dcr | 1.85 | 0.61 | 2.91 | 0.29 | 2.04 | 0.67 | 2.72 | 0.52 |

| CG.size | 1.56 | 0.68 | 2.40 | 0.68 | 1.78 | 0.68 | 2.55 | 0.65 |

Appendix C. Correlation Matrix for Variables in Qualile Regression Models (Spearman Coefficients)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Parameter | C.Overall | C.Immed | C.Prolong | |

|---|---|---|---|---|

| ERM_score | Coef. | 0.055 | 0.126 ** | −0.035 |

| Sig. | 0.145 | 0.001 | 0.349 | |

| CG_score | Coef. | 0.022 | 0.087 * | −0.072 |

| Sig. | 0.563 | 0.018 | 0.056 | |

| Size | Coef. | −0.121 ** | −0.024 | −0.205 ** |

| Sig. | 0.001 | 0.519 | 0.000 | |

| Age | Coef. | −0.135 ** | −0.047 | −0.218 ** |

| Sig. | 0.000 | 0.197 | 0.000 | |

| LF (legal form) | Coef. | −0.185 ** | −0.099 ** | −0.265 ** |

| Sig. | 0.000 | 0.007 | 0.000 | |

| FB (family business) | Coef. | −0.024 | −0.048 | 0.035 |

| Sig. | 0.523 | 0.189 | 0.361 | |

| Sector | Coef. | 0.083 * | −0.010 | 0.159 ** |

| Sig. | 0.028 | 0.779 | 0.000 | |

| Country | Coef. | 0.120 ** | 0.067 | 0.181 ** |

| Sig. | 0.002 | 0.068 | 0.000 |

References

- Abid, Ammar, Ammar Ali Gull, Nazim Hussain, and Duc Khuong Nguyen. 2021. Risk governance and bank risk-taking behavior: Evidence from Asian banks. Journal of International Financial Markets, Institutions and Money 75: 101466. [Google Scholar] [CrossRef]

- Abor, Joshua, and Charles K. D. Adjasi. 2007. Corporate governance and the small and medium enterprises sector: Theory and implications. Corporate Governance 7: 111–22. [Google Scholar] [CrossRef]

- Al-ahdal, Waleed M., and Hafiza Aishah Hashim. 2021. Impact of audit committee characteristics and external audit quality on firm performance: Evidence from India. Corporate Governance: The International Journal of Business in Society 22: 424–45. [Google Scholar] [CrossRef]

- Almeida, Heitor, and Murillo Campello. 2002. Financial Constraints and Investment-Cash Flow Sensitivities: New Research Directions. Working Paper. New York: New York University. [Google Scholar] [CrossRef]

- Antony, Jiju, Maneesh Kumar, and Ashraf Labib. 2008. Gearing Six Sigma into UK manufacturing SMEs: Results from a pilot study. Journal of the Operational Research Society 59: 482–93. [Google Scholar] [CrossRef]

- Banham, Heather, and Yunke He. 2010. SME Governance: Converging Definitions And Expanding Expectations. International Business & Economics Research Journal 9: 77. [Google Scholar]

- Barbera, Francesco, and Tim Hasso. 2013. Do We Need to Use an Accountant? The Sales Growth and Survival Benefits to Family SMEs. Family Business Review 26: 271–92. [Google Scholar] [CrossRef]

- Beasley, Mark, Bruce Branson, and Don Pagach. 2015. An analysis of the maturity and and strategic impact of investments in ERM. Journal of Accounting and Public Policy 34: 219–43. [Google Scholar] [CrossRef]

- Beasley, Mark, Bruce Branson, Don Pagach, and Silvia Panfilo. 2021. Are required SEC proxy disclosures about the board’s role in risk oversight substantive? Journal of Accounting and Public Policy 40: 106816. [Google Scholar] [CrossRef]

- Boers, Börje, and Thomas Henschel. 2021. The role of entrepreneurial orientation in crisis management: Evidence from family firms in enterprising communities. Journal of Enterprising Communities: People and Places in the Global Economy 6: 756–80. [Google Scholar] [CrossRef]

- Bogodistov, Yevgen, and Veit Wohlgemuth. 2017. Enterprise risk management: A capability-based perspective. The Journal of Risk Finance 18: 234–51. [Google Scholar] [CrossRef]

- Bonadio, Barthélémy, Zhen Huo, Andrei A. Levchenko, and Nitya Pandalai-Nayar. 2020. Global Supply Chains in the Pandemic. NBER Working Papers 27224. Cambridge: National Bureau of Economic Research, Inc. [Google Scholar]

- Bongini, Paola, Malgorzata Iwanicz-Drozdowska, Oliviero Roggi, and Viktor Elliot. 2020. Global Report on Business Continuity Planning and Management (BCP/BCM). Survey Results. Available online: https://ssrn.com/abstract=3764401 (accessed on 1 November 2022).

- Bonss, Wolfgang. 2016. The notion of resilience: Trajectories and social science perspective. In New Perspectives on Resilience in Socio-Economic Spheres. Edited by Andrea Mauer. Wiesbaden: Springer, pp. 9–22. [Google Scholar] [CrossRef]

- Brigham, Eugene F., and Michael C. Ehrhardt. 2011. Financial Management Theory and Practice. London: South Western Cengage Learning Graphic World Inc. [Google Scholar]

- Bromiley, Philip, Michael McShane, Anil Nair, and Elzotbek Rustambekov. 2015. Enterprise risk management: Review, Critique and Research Directions. Long Range Planning 48: 265–76. [Google Scholar] [CrossRef]

- Brunninge, Olof, Mattias Nordqvist, and Johan Wiklund. 2007. Corporate Governance and Strategic Change in SMEs: The Effects of Ownership, Board Composition and Top Management Teams. Small Business Economics 29: 295–308. [Google Scholar] [CrossRef]

- Brustbauer, Johannes K., and Mike Peters. 2013. Risk perception of family and non-family firm managers. International Journal of Entrepreneurship and Small Business 20: 96–116. [Google Scholar] [CrossRef]

- Brustbauer, Johannes. 2016. Enterprise risk management in SMEs: Towards a structural model. International Small Business Journal 34: 70–85. [Google Scholar] [CrossRef]

- Bryce, Cormac, Patrick Ring, Simon Ashby, and Jamie K. Wardman. 2020. Resilience in the face of uncertainty: Early lessons from the COVID-19 pandemic. Journal of Risk Research 23: 880–87. [Google Scholar] [CrossRef]

- Burnard, Kevin, and Ran Bhamra. 2011. Organisational resilience: Development of a conceptual framework for organisational responses. International Journal of Production Research 49: 5581–99. [Google Scholar] [CrossRef]

- Caballero-Morales, Santiago-Omar. 2021. Innovation as recovery strategy for SMEs in emerging economies during the COVID-19 pandemic. Research in International Business and Finance 57: 101396. [Google Scholar] [CrossRef]

- Calabrò, Andrea, and Donata Mussolino. 2011. How do boards of directors contribute to family SME export intensity? The role of formal and informal governance mechanisms. Journal of Management & Governance 17: 363–403. [Google Scholar]

- Collin, Sven-Olof Yrjö, Jenny Ahlberg, Karin Berg, Pernilla Broberg, and Amelie Karlsson. 2017. The auditor as consigliere in family firm. Journal of Family Business Management 7: 2–20. [Google Scholar] [CrossRef]

- Coulson-Thomas, Colin. 2007. SME directors and boards: The contribution of directors and boards to the growth and development of Small and Medium-sized Enterprises (SMEs). International Journal of Business Governance and Ethics 3: 250–61. [Google Scholar] [CrossRef]

- Crossan, Kenny, and Thomas Henschel. 2012. An holistic model of corporate governance for SMEs. Journal of Management and Financial Sciences 5: 54–76. [Google Scholar]

- Crossan, Kenny, Elena Pershina, and Thomas Henschel. 2018. Corporate Governance in Small and Medium-sized Firms: A study of Scottish Enterprises. Interdisciplinary Journal of Economics and Business Law 7: 8–34. [Google Scholar]

- Crovini, Chiara, Gabriele Santoro, and Giovanni Ossola. 2021a. Rethinking risk management in entrepreneurial SMEs: Towards the integration with the decision-making process. Management Decision 59: 1085–113. [Google Scholar] [CrossRef]

- Crovini, Chiara, Giovanni Ossola, and Bernd Britzelmaier. 2021b. How to reconsider risk management in SMEs? An Advanced, Reasoned and Organised Literature Review. European Management Journal 39: 118–34. [Google Scholar] [CrossRef]

- de Araújo Lima, Priscila Ferreira, Maria Crema, and Chiara Verbano. 2020. Risk management in SMEs: A systematic review and future directions. European Management Journal 38: 78–94. [Google Scholar] [CrossRef]

- De Vito, Antonio, and Juan-Pedro Gómez. 2020. Estimating the COVID-19 cash crunch: Global evidence and policy. Journal of Accounting and Public Policy 39: 106741. [Google Scholar] [CrossRef]

- Durst, Susanne, and Thomas Henschel. 2014. Governance in small firms—A country comparison of current practices. International Journal of Entrepreneurship and Small Business 21: 16–32. [Google Scholar] [CrossRef]

- Durst, Susanne, and Thomas Henschel. 2021. COVID-19 as an accelerator for developing strong(er) businesses? Insights from Estonian small firms. Journal of the International Council for Small Business. [Google Scholar] [CrossRef]

- Eggers, Fabian. 2020. Masters of disasters? Challenges and opportunities for SMEs in times of crisis. Journal of Business Research 116: 199–208. [Google Scholar] [CrossRef]

- Eisenhardt, Kathleen M., and Jeffrey A. Martin. 2000. Dynamic capabilities: What are they? Strategic Management Journal 21: 1105–21. [Google Scholar] [CrossRef]

- Ellul, Andrew. 2015. The role of risk management in corporate governance. Annual Review of Financial Economics 7: 279–99. [Google Scholar] [CrossRef]

- European Commission. 2021a. SME Country Fact Sheet Poland. Available online: https://ec.europa.eu/growth/smes/sme-strategy/sme-performance-review_en#sba-fact-sheets (accessed on 1 November 2022).

- European Commission. 2021b. SME Country Fact Sheet Germany. Available online: https://ec.europa.eu/growth/smes/sme-strategy/sme-performance-review_en#sba-fact-sheets (accessed on 1 November 2022).

- Everitt, Brian S., Sabine Landau, Morven Leese, and Daniel Stahl. 2011. Cluster Analysis, 5th ed. Chichester: John Wiley and Sons. [Google Scholar]

- Farrell, Mark, and Ronan Gallagher. 2015. The Valuation Implications of Enterprise Risk Management Maturity. The Journal of Risk and Insurance 82: 625–57. [Google Scholar] [CrossRef]

- Farrell, Mark, and Ronan Gallagher. 2019. Moderating Influences on the ERM maturity-performance relationship. Research in International Business and Finance 47: 616–28. [Google Scholar] [CrossRef]

- Farre-Mensa, Joan, and Alexander Ljungqvist. 2016. Do Measures of Financial Constraints Measure Financial Constraints? The Review of Financial Studies 29: 271–308. [Google Scholar] [CrossRef]

- Florio, Cristina, and Giulia Leoni. 2017. Enterprise risk management and firm performance: The Italian case. The British Accounting Review 49: 56–74. [Google Scholar] [CrossRef]

- Florio, Cristina, Francesca Rossignoli, and Gaia Melloni. 2022. Drivers of ERM in SMEs: Which Corporate Governance Features Matter? In Risk Management Insights from Different Settings. Edited by Cristina Florio, Monika Wieczorek-Kosmala, Philip Linsley and Philip Shrives. Cham: Springer, pp. 141–67. [Google Scholar]

- Floyd, David, and John McManus. 2005. The role of SMEs in improving the competitive position of the European Union. European Business Review 17: 144–50. [Google Scholar] [CrossRef]

- Gibson, Brain. 2009. A Research Framework for Exploring Corporate Governance in SMEs. Paper presented at 54th ICSB World Conference, Seoul, Republic of Korea, June 21–24; pp. 1–12. [Google Scholar]

- Gourinchas, Pierre-Olivier, Şebnem Kalemli-Özcan, Veronika Penciakova, and Nick Sander. 2021. COVID-19 and SMEs: 2021 “Time Bomb”? National Bureau of Economic Research Working Paper No. 28418. Cambridge: National Bureau of Economic. [Google Scholar] [CrossRef]

- Heinze, Ilka, and Thomas Henschel. 2021. Risk(ing) sophistication: Towards a structural equation model for risk management in small and medium-sized enterprises. International Journal of Entrepreneurship and Small Business 44: 386–412. [Google Scholar] [CrossRef]

- Helfat, Constance E., Sydney Finkelstein, Will Mitchell, Margaret Peteraf, Harbir Singh, David Teece, and Sidney G. Winter. 2007. Dynamic Capabilities: Understanding Strategic Change in Organizations. Malden: Wiley-Blackwell. [Google Scholar]

- Henschel, Thomas, and Axel Daniel Lantzsch. 2022. The relationship between ERM and performance revisited: Empirical evidence from SMEs. In Risk and Risk Management in Diverse Settings. Edited by Cristina Florio, Monika Wieczorek-Kosmala, Philip Linsley and Philip Shrives. Cham: Springer, pp. 95–113. [Google Scholar] [CrossRef]

- Hiebl, Martin R. W., Christine Duller, and Herbert Neubauer. 2019. Enterprise risk management in family firms: Evidence from Austria and Germany. Journal of Risk Finance 20: 39–58. [Google Scholar] [CrossRef]

- Jensen, Michael C. 1986. Agency costs of free cash flow, corporate finance, and takeovers. The American Economic Review 76: 323–29. [Google Scholar]

- Juergensen, Jill, José Guimón, and Rajneesh Narula. 2020. European SMEs amidst the COVID-19 crisis: Assessing impact and policy responses. Journal of Industrial and Business Economics 47: 499–510. [Google Scholar] [CrossRef]

- Katchova, Ani. 2013. Available online: https://docs.google.com/file/d/0BwogTI8d6EEiYmVzN0kyQ19CU3M/edit?resourcekey=0-j7BdwyCNljyvfRBVl5mR4g (accessed on 1 November 2022).

- Kim, YoungJun, and Nicholas S. Vonortas. 2014. Managing risk in the formative years: Evidence from young enterprises in Europe. Technovation 34: 454–65. [Google Scholar] [CrossRef]

- Kirkpatrick, Grant. 2009. The corporate governance lessons from the financial crisis. OECD Journal: Financial Market Trends 2009: 61–87. Available online: http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.444.6047&rep=rep1&type=pdf (accessed on 1 November 2022). [CrossRef]

- Koenker, Roger, and Gilbert Bassett. 1978. Regression Quantiles. Econometrica 46: 33–50. [Google Scholar] [CrossRef]

- Linke, Arthur, and Cristina Florio. 2019. Enterprise Risk Management Measurement: Insights from an Interdisciplinary Literature Review. In Springer eBooks Business and Management. Multiple Perspectives in Risk and Risk Management, Proceedings of the ERRN 8th European Risk Conference 2018, Katowice, Poland, September 20–21. Edited by Philip Linsley, Philip Shrives and Monika Wieczorek-Kosmala. Berlin and Heidelberg: Springer, pp. 37–54. [Google Scholar] [CrossRef]

- Lorenz, Daniel F., and Cordula Dittmer. 2016. Resilience in Catastrophes, disasters and emergencies. Socio-scientific perspectives. In New Perspectives on Resilience in Socio-Economic Spheres. Edited by Andrea Maurer. Wiesbaden: Springer, pp. 25–59. [Google Scholar] [CrossRef]

- Mallak, Larry. 1998. Putting organizational resilience to work. Industrial Management 40: 8–13. [Google Scholar]

- Mayr, Stefan, and David Lixl. 2019. Restructuring in SMEs—A multiple case study analysis. Journal of Small Business Strategy 29: 85–98. [Google Scholar]

- McManus, Sonia, Erica Seville, John Vargo, and David Brunsdon. 2008. A facilitated process for improving organizational resilience. Natural Hazards Review 9: 81–90. [Google Scholar] [CrossRef]

- McShane, Michael. 2018. Enterprise risk management: History and a design science proposal. The Journal of Risk Finance 19: 137–53. [Google Scholar] [CrossRef]

- Meiseberg, Brinja, and Thomas Ehrmann. 2013. Tendency to Network of Small and Medium-sized Enterprises: Combining Organizational Economics and Resource-based Perspectives. Managerial and Decision Economics 34: 238–300. [Google Scholar] [CrossRef]

- Nguyen, Quang Khai, and Van Cuong Dang. 2022. Does the country’s institutional quality enhance the role of risk governance in preventing bank risk? Applied Economics Letters, 1–4. [Google Scholar] [CrossRef]

- OECD. 2020. OECD Principles of Corporate Governance 2020. Available online: http://www.oecd-ilibrary.org/industry-and-services/oecd-principles-of-corporate-governance-2020_9789264015999-en (accessed on 1 November 2022).

- Petersen, Bruce C., Steven Fazzari, and R. Gleen Hubbard. 1988. Financing constraints and corporate investment. National Bureau of Economic Research 1988: 141–206. [Google Scholar]

- Qiu, Joseph. 2020. Pandemic risk: Impact, modelling, and transfer. Risk Management and Insurance Review 23: 293–304. [Google Scholar] [CrossRef] [PubMed]

- Segaro, Ethiopia. 2010. Internationalization of family SMEs: The impact of ownership, governance, and top management team. Journal of Management & Governance 16: 147–69. [Google Scholar]

- Semrau, Thorsten, Tina Ambos, and Sascha Kraus. 2016. Entrepreneurial orientation and SME performance across societal cultures: An international study. Journal of Business Research 69: 1928–32. [Google Scholar] [CrossRef]

- Solange, Charas, and Sheri Perelli. 2013. Threats to board stability: Understanding SME director behavior. International Journal of Disclosure and Governance 10: 175–91. [Google Scholar]

- Spielmann, Nina. 2012. International Corporate Governance. Bern, Wien and Stuttgart: Haupt Verlag AG. [Google Scholar]

- Stein, Volker, and Arnd Wiedemann. 2016. Risk governance: Conceptualization, tasks, and research agenda. Journal of Business Economics 86: 813–36. [Google Scholar] [CrossRef]

- Stiglitz, Joseph E., and Andrew Weiss. 1981. Credit rationing in markets with imperfect information. The American Economic Review 71: 393–410. [Google Scholar]

- Tan, Consilz, and Su Zy Lee. 2021. Adoption of enterprise risk management (ERM) in small and medium-sized enterprises: Evidence from Malaysia. Journal of Accounting and Organizational Change 18: 100–31. [Google Scholar] [CrossRef]

- Whited, Toni M. 1992. Debt, liquidity constraints, and corporate investment: Evidence from panel data. The Journal of Finance 47: 1425–60. [Google Scholar] [CrossRef]

- WHO. 2021. Available online: https://covid19.who.int/region/euro/country/pl (accessed on 1 November 2022).

| Variables | Definition |

|---|---|

| Immediate COVID-19 effect/interruptions (survey-based) | |

| C.WORK | The COVID-19 pandemic resulted in limited accessibility of workers. |

| C.COSTS | The COVID-19 pandemic resulted in additional costs of the implementation of required safety measures. |

| C.PROD | The COVID-19 pandemic resulted in inability to continue production. |

| C.SALES | The COVID-19 pandemic resulted in inability to continue sales. |

| C.SUPPLY | The COVID-19 pandemic resulted in delayed delivery of production components/materials etc. or produced goods to the customers. |

| Prolonged COVID-19 effect/interruptions (survey based) | |

| C.LIQ | The COVID-19 pandemic resulted in worsening of financial liquidity. |

| C.LOANS | The COVID-19 pandemic resulted in limited accessibility of bank loans. |

| C.SURV | The overall impact of COVID-19 related interruptions threatened the survival of our company |

| Aggregated measures of COVID-19 interruptions: | |

| C.Overall | The score that reflects the consolidated COVID-19 impact, computed as the mean of the scores assigned by each of the respondents for particular impacts (8 variables) |

| C.Imm | The score that reflects the consolidated COVID-19 impact for the immediate pandemic effects (computed as the mean of the scores assigned to 5 variables: C.Work, C.Costs, C.Sales, C.Prod, C.Supply) |

| C.Prol | The score that reflects the consolidated COVID-19 impact for the prolonged effects (computed as the mean of the scores assigned to 3 variables: C.Liq, C.Loans, C.Surv) |

| Variables | Definition |

|---|---|

| Risk analysis (identification and evaluation) | |

| ERM.exp | Our company employs external experts to identify risks * |

| ERM.report | Our company writes reports on intensified risks * |

| ERM.ident | Our risk identification considers all aspects of our performance |

| ERM.list | We regularly review our list of identified risks |

| ERM.eval | We always evaluate risk impact from the perspective of our business objectives ** |

| Risk monitoring and response | |

| ERM.cust | Our company regularly surveys customers’ satisfaction ** |

| ERM.prev | To prevent errors, we always follow the predefined procedures/plans ** |

| ERM.cont | We have contingency plans for emergencies * |

| ERM.owners | Our company defined “risk owners”, that is key persons who are responsible for monitoring and handling particular exposures |

| ERM.metrics | We have implemented risk measures/metrics that are helpful in monitoring the first symptoms of risk |

| Aggregated measures of ERM sophistication | |

| ERM.Soph | mean of all ERM practices (10) |

| ERM.analysis | mean of risk analysis ERM practices (5) |

| ERM.m&r | mean of risk monitoring and response ERM practices (5) |

| Variables | Definition |

|---|---|

| CG strategic thinking | |

| CG.succ | Does the company have any plan of succession? (who will run the business in the case the owner is retired or ill?) 1—no, 2—yes, but informal, 3—yes, formal |

| CG.strat | Does a company have a formal business strategy plan? 1—no, 2—yes, with 1-year horizon; 3—yes, with a horizon up to 3 years, 4—yes, with a horizon exceeding 3 years perspective |

| CG internal organisational structure | |

| How important is each of the below-listed elements of the internal organizational structure? (all questions evaluated on 3-point Likert scale: 1 minor importance, 2 moderately important, 3 very important) | |

| CG.rules | clearly defined rules of decision making |

| CG.com | control of internal and external communication |

| CG.confl | handling of conflicts of interests |

| CG.r&o | defined rights and obligations of the management team |

| CG.dcr | qualifications and competences of the management team |

| CG.size | size and composition of the management team |

| Aggregated measure of strength of CG mechanisms | |

| CG.score | computed as the mean of the scores assigned for all CG characteristics |

| Variables | Definition |

|---|---|

| Size—the number of employees: | |

| micro | up to 9 persons |

| small | 10–49 persons |

| medium | 50–249 persons |

| Age—the number of years the company actively performs on the market: | |

| infant | up to 5 years |

| young | 6–10 years |

| intermediate | 11–20 years |

| mature | 21 years or more |

| The legal form of business performance | |

| SP | sole proprietor |

| P-personal | partnership—personal (owners bear whole responsibility for the business) |

| P-capital | partnership—capital (owners bear limited liability for the business) |

| Do you consider your business as a family firm? (the members of the family/the relatives are engaged in the business) | |

| Fam | YES—family firm |

| N-Fam | NO—non-family firm |

| Sector | |

| T | trade |

| P | production |

| S | services |

| Variables | Germany | Poland | |||

|---|---|---|---|---|---|

| N | % | N | % | ||

| In total | 215 | 100.00% | 526 | 100.00% | |

| Size | micro | 41 | 19.07% | 181 | 34.41% |

| small | 147 | 68.37% | 206 | 39.16% | |

| medium | 27 | 12.56% | 139 | 26.43% | |

| Age | infant | 15 | 6.98% | 86 | 16.35% |

| young | 32 | 14.88% | 137 | 26.05% | |

| intermediate | 53 | 24.65% | 185 | 35.17% | |

| mature | 115 | 53.49% | 118 | 22.43% | |

| Legal form | SP | 23 | 10.70% | 195 | 37.07% |

| P-personal | 67 | 31.16% | 77 | 14.64% | |

| P-capital | 125 | 58.14% | 254 | 48.29% | |

| Family business | Fam | 125 | 58.14% | 167 | 31.75% |

| N-Fam | 90 | 41.86% | 359 | 68.25% | |

| Sector | trade | 36 | 16.74% | 95 | 18.06% |

| production | 45 | 20.93% | 198 | 37.64% | |

| services | 134 | 62.33% | 233 | 44.30% | |

| In total | 215 | 100.00% | 526 | 100.00% | |

| Variable | U Mann-Whitney | W-Wilcoxon | Z | Sig. | Mean Ranks of U Mann-Whitney Test | |

|---|---|---|---|---|---|---|

| Germany | Poland | |||||

| C.WORK | 49,902.000 | 73,122.000 | −2.542 | 0.011 ** | 340.10 | 383.63 |

| C.COSTS | 49,439.500 | 188,040.500 | −2.736 | 0.006 *** | 404.05 | 357.49 |

| C.PROD | 52,625.500 | 191,226.500 | −1.498 | 0.134 | 389.23 | 363.55 |

| C.SALES | 46,348.000 | 69,568.000 | −3.905 | 0.000 *** | 323.57 | 390.39 |

| C.SUPPLY | 51,064.000 | 74,284.000 | −2.102 | 0.036 ** | 345.51 | 381.42 |

| C.LIQ | 49,202.500 | 72,422.500 | −2.810 | 0.005 *** | 336.85 | 384.96 |

| C.LOANS | 37,368.000 | 52,593.000 | −3.700 | 0.000 *** | 302.26 | 366.46 |

| C.SURV | 43,198.500 | 66,418.500 | −5.118 | 0.000 *** | 308.92 | 396.37 |

| C.Overall | 40,182.000 | 55,407.000 | −2.414 | 0.016 ** | 318.43 | 361.11 |

| C.Imm | 34,079.500 | 48,785.500 | −4.771 | 0.000 *** | 285.30 | 369.71 |

| C.Prol | 37,549.500 | 52,774.500 | −3.560 | 0.000 *** | 303.30 | 366.11 |

| Variable | U Mann-Whitney | W-Wilcoxon | Z | Sig. | Mean Ranks of U Mann-Whitney Test | |

|---|---|---|---|---|---|---|

| Germany | Poland | |||||

| ERM.exp | 48,922.000 | 72,142.000 | −3.003 | 0.003 *** | 335.54 | 385.49 |

| ERM.report | 53,497.500 | 76,717.500 | −1.170 | 0.242 | 356.83 | 376.79 |

| ERM.ident | 51,020.000 | 189,621.000 | −2.130 | 0.033 ** | 396.70 | 360.50 |

| ERM.list | 35,205.500 | 173,806.500 | −8.196 | 0.000 *** | 470.25 | 330.43 |

| ERM.eval | 56,134.500 | 194,735.500 | −0.159 | 0.874 | 372.91 | 370.22 |

| ERM.cust | 30,908.000 | 54,128.000 | −9.814 | 0.000 *** | 251.76 | 419.74 |

| ERM.prev | 52,583.000 | 75,803.000 | −1.530 | 0.126 | 352.57 | 378.53 |

| ERM.cont | 52,362.000 | 190,963.000 | −1.616 | 0.106 | 390.46 | 363.05 |

| ERM.owners | 53,897.500 | 192,498.500 | −1.022 | 0.307 | 383.31 | 365.97 |

| ERM.metrics | 56,057.000 | 194,658.000 | −0.188 | 0.851 | 373.27 | 370.07 |

| ERM.Soph | 55,838.000 | 79,058.000 | −0.267 | 0.789 | 367.71 | 372.34 |

| ERM.analysis | 50,308.000 | 188,909.000 | −2.362 | 0.018 ** | 400.01 | 359.14 |

| ERM.m&r | 48,775.500 | 71,995.500 | −2.943 | 0.003 *** | 334.86 | 385.77 |

| Variable | U Mann-Whitney | W-Wilcoxon | Z | Sig. | Mean Ranks of U Mann-Whitney Test | |

|---|---|---|---|---|---|---|

| Germany | Poland | |||||

| CG.succ | 46,167.000 | 184,768.000 | −4.195 | 0.000 *** | 419.27 | 351.27 |

| CG.strat | 52,049.000 | 190,650.000 | −1.776 | 0.076 * | 391.91 | 362.45 |

| CG.rules | 55,529.500 | 194,130.500 | −0.463 | 0.644 | 375.72 | 369.07 |

| CG.com | 56,320.500 | 79,540.500 | −0.098 | 0.922 | 369.96 | 371.43 |

| CG.confl | 51,654.000 | 74,874.000 | −2.148 | 0.032 ** | 348.25 | 380.30 |

| CG.r&o | 55,764.000 | 194,365.000 | −0.332 | 0.740 | 374.63 | 369.52 |

| CG.dcr | 46,517.500 | 185,118.500 | −4.291 | 0.000 *** | 417.64 | 351.94 |

| CG.size | 56,180.500 | 79,400.500 | −0.148 | 0.883 | 369.30 | 371.69 |

| CG_score | 50,236.500 | 188,837.500 | −2.395 | 0.017 ** | 400.34 | 359.01 |

| Variable | U Mann-Whitney | W Wilcoxon | Z | Sig. | Mean Ranks U Mann-Whitney Test | ||

|---|---|---|---|---|---|---|---|

| Low | High | Diff. | |||||

| Panel A. Germany | |||||||

| C.WORK | 4764.000 | 6975.000 | −0.376 | 0.707 | 105.68 | 109.03 | −3.345 |

| C.COSTS | 2954.000 | 5165.000 | −4.767 | 0.000 *** | 78.26 | 121.17 | −42.917 |

| C.PROD | 4120.500 | 6331.500 | −1.917 | 0.055 * | 95.93 | 113.35 | −17.414 |

| C.SALES | 4559.500 | 6770.500 | −0.861 | 0.389 | 102.58 | 110.40 | −7.816 |

| C.SUPPLY | 3875.500 | 6086.500 | −2.507 | 0.012 ** | 92.22 | 114.99 | −22.770 |

| C.LIQ | 4017.500 | 6228.500 | −2.165 | 0.030 ** | 94.37 | 114.04 | −19.666 |

| C.LOANS | 2661.500 | 3936.500 | −1.488 | 0.137 | 78.73 | 91.04 | −12.306 |

| C.SURV | 4219.000 | 6430.000 | −1.682 | 0.093 * | 97.42 | 112.68 | −15.260 |

| C.Overall | 2320.000 | 3595.000 | −2.595 | 0.009 *** | 71.90 | 93.79 | −21.890 |

| C.Imm | 3565.000 | 5776.000 | −3.218 | 0.001 *** | 87.52 | 117.07 | −29.559 |

| C.Prol | 2541.500 | 3816.500 | −1.862 | 0.063* | 76.33 | 92.00 | −15.674 |

| Panel B. Poland | |||||||

| C.WORK | 32,641.500 | 63,766.500 | −1.078 | 0.281 | 256.09 | 270.16 | −14.070 |

| C.COSTS | 34,370.500 | 65,495.500 | −0.068 | 0.946 | 263.03 | 263.92 | −0.885 |

| C.PROD | 27,392.000 | 58,517.000 | −4.127 | 0.000 *** | 235.01 | 289.11 | −54.104 |

| C.SALES | 33,521.500 | 64,646.500 | −0.563 | 0.573 | 259.62 | 266.98 | −7.359 |

| C.SUPPLY | 31,435.500 | 62,560.500 | −1.786 | 0.074 * | 251.25 | 274.51 | −23.267 |

| C.LIQ | 33,696.000 | 72,199.000 | −0.461 | 0.645 | 266.67 | 260.65 | 6.028 |

| C.LOANS | 32,338.500 | 63,463.500 | −1.268 | 0.205 | 254.87 | 271.25 | −16.381 |

| C.SURV | 34,265.000 | 72,768.000 | −0.130 | 0.897 | 264.39 | 262.70 | 1.689 |

| C.Overall | 31,956.500 | 63,081.500 | −1.454 | 0.146 | 253.34 | 272.63 | −19.294 |

| C.Imm | 30,853.500 | 61,978.500 | −2.090 | 0.037 ** | 248.91 | 276.62 | −27.706 |

| C.Prol | 34,334.000 | 65,459.000 | −0.088 | 0.930 | 262.89 | 264.05 | −1.163 |

| Variable | U Mann-Whitney | W Wilcoxon | Z | Sig. | Mean Ranks U Mann-Whitney Test | ||

|---|---|---|---|---|---|---|---|

| Weak | Strong | Diff. | |||||

| Panel A. Germany | |||||||

| C.WORK | 4571.000 | 6341.000 | −0.079 | 0.937 | 107.47 | 108.20 | −0.724 |

| C.COSTS | 4097.500 | 5867.500 | −1.266 | 0.205 | 99.45 | 111.23 | −11.785 |

| C.PROD | 4527.500 | 16,773.500 | −0.185 | 0.853 | 109.26 | 107.52 | 1.740 |

| C.SALES | 4377.000 | 16,623.000 | −0.560 | 0.575 | 111.81 | 106.56 | 5.256 |

| C.SUPPLY | 3714.000 | 5484.000 | −2.210 | 0.027 ** | 92.95 | 113.69 | −20.743 |

| C.LIQ | 4594.500 | 16,840.500 | −0.019 | 0.985 | 108.13 | 107.95 | 0.175 |

| C.LOANS | 2639.500 | 3720.500 | −1.060 | 0.289 | 80.88 | 89.88 | −8.998 |

| C.SURV | 4306.000 | 6076.000 | −0.737 | 0.461 | 102.98 | 109.90 | −6.914 |

| C.Overall | 2703.500 | 3784.500 | −0.821 | 0.412 | 82.27 | 89.38 | −7.107 |

| C.Imm | 4226.500 | 5996.500 | −0.924 | 0.356 | 101.64 | 110.41 | −8.771 |

| C.Prol | 2731.000 | 3812.000 | −0.729 | 0.466 | 82.87 | 89.16 | −6.294 |

| Panel B. Poland | |||||||

| C.WORK | 34,277.000 | 72,227.000 | −0.138 | 0.891 | 264.44 | 262.64 | 1.795 |

| C.COSTS | 29,580.000 | 61,206.000 | −2.888 | 0.004 *** | 243.85 | 281.44 | −37.588 |

| C.PROD | 28,861.500 | 60,487.500 | −3.286 | 0.001 *** | 240.99 | 284.05 | −43.063 |

| C.SALES | 32,362.000 | 63,988.000 | −1.255 | 0.210 | 254.93 | 271.32 | −16.388 |

| C.SUPPLY | 32,331.000 | 63,957.000 | −1.276 | 0.202 | 254.81 | 271.43 | −16.624 |

| C.LIQ | 34,135.500 | 72,085.500 | −0.220 | 0.826 | 265.00 | 262.13 | 2.873 |

| C.LOANS | 33,587.000 | 71,537.000 | −0.546 | 0.585 | 267.19 | 260.13 | 7.053 |

| C.SURV | 33,325.000 | 71,275.000 | −0.694 | 0.488 | 268.23 | 259.18 | 9.049 |

| C.Overall | 32,145.500 | 63,771.500 | −1.360 | 0.174 | 254.07 | 272.11 | −18.038 |

| C.Imm | 30,564.500 | 62,190.500 | −2.270 | 0.023 ** | 247.77 | 277.86 | −30.085 |

| C.Prol | 33,792.000 | 71,742.000 | −0.415 | 0.678 | 266.37 | 260.88 | 5.491 |

| Parameter | Model 1 Overall COVID-19 Impact (Dependent Variable: C.Overall) | Model 2 Immediate COVID-19 Impact (Dependent Variable: C.Immed) | Model 3 Prolonged COVID-19 Impact (Dependent Variable: C.Prolong) | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Coef. | Std.Err | t | Sig. | Coef. | Std.Err | t | Sig. | Coef. | Std.Err | t | Sig. | |

| Intercept | 28.457 | 5.1396 | 5.537 | 0.000 *** | 4.033 | 0.6662 | 6.053 | 0.000 *** | 8.550 | 2.2918 | 3.731 | 0.000 *** |

| ERM_score | 1.866 | 0.5079 | 3.674 | 0.000 *** | 0.130 | 0.0656 | 1.982 | 0.048 ** | 0.618 | 0.2265 | 2.730 | 0.007 *** |

| CG_score | 1.463 | 1.3091 | 1.117 | 0.264 | 0.390 | 0.1710 | 2.282 | 0.023 ** | 0.553 | 0.5838 | 0.947 | 0.344 |

| Size | −1.731 | 0.8638 | −2.004 | 0.045 ** | −0.094 | 0.1125 | −0.838 | 0.402 | −0.950 | 0.3852 | −2.466 | 0.014 ** |

| Age | −0.187 | 0.5475 | −0.341 | 0.733 | −0.020 | 0.0717 | −0.272 | 0.786 | −0.474 | 0.2441 | −1.940 | 0.053 * |

| LF (legal form) | −1.912 | 0.6918 | −2.764 | 0.006 *** | −0.234 | 0.0905 | −2.587 | 0.010 ** | −0.885 | 0.3085 | −2.867 | 0.004 *** |

| FB (family business) | −0.034 | 1.0912 | −0.031 | 0.975 | −0.088 | 0.1425 | −0.616 | 0.538 | 0.083 | 0.4866 | 0.170 | 0.865 |

| Sector | −0.146 | 0.6608 | −0.220 | 0.826 | −0.135 | 0.0867 | −1.556 | 0.120 | 0.887 | 0.2947 | 3.011 | 0.003 *** |

| Country | 1.601 | 1.2336 | 1.298 | 0.195 | 0.029 | 0.1563 | 0.187 | 0.852 | 1.418 | 0.5501 | 2.578 | 0.010 ** |

| Model quality | ||||||||||||

| Pseudo R Squared | 0.036 | 0.029 | 0.060 | |||||||||

| MAE (Mean Absolute Error) | 7.6841 | 1.0459 | 3.3559 | |||||||||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wieczorek-Kosmala, M.; Henschel, T. The Role of ERM and Corporate Governance in Managing COVID-19 Impacts: SMEs Perspective. J. Risk Financial Manag. 2022, 15, 587. https://doi.org/10.3390/jrfm15120587

Wieczorek-Kosmala M, Henschel T. The Role of ERM and Corporate Governance in Managing COVID-19 Impacts: SMEs Perspective. Journal of Risk and Financial Management. 2022; 15(12):587. https://doi.org/10.3390/jrfm15120587

Chicago/Turabian StyleWieczorek-Kosmala, Monika, and Thomas Henschel. 2022. "The Role of ERM and Corporate Governance in Managing COVID-19 Impacts: SMEs Perspective" Journal of Risk and Financial Management 15, no. 12: 587. https://doi.org/10.3390/jrfm15120587

APA StyleWieczorek-Kosmala, M., & Henschel, T. (2022). The Role of ERM and Corporate Governance in Managing COVID-19 Impacts: SMEs Perspective. Journal of Risk and Financial Management, 15(12), 587. https://doi.org/10.3390/jrfm15120587