Integrated Intellectual Investment Portfolio as an Efficient Instrument to Manage Personal Financial Investment

Abstract

:1. Introduction

- Disclosure of the logic and compatibility of the selected actions;

- Presentation of harmonized analytical solutions;

- Presentation of practical examples of the obtained solution.

2. Literature Review

3. Methodology

- Development and use of a stop-loss order system for operational risk management;

- Ranking of shares according to their suitability for the portfolio to achieve the intended objectives;

- Selection of the most suitable shares or a small group of them for each specific investment step.

3.1. Development and Use of a Stop-Loss Order System for Operational Risk Management

- How an effectively designed system of coordinated stop-loss orders can successfully change the performance of the portfolio, understanding and informing about the incurred costs;

- How deeply the emerging patterns in the market are revealed, even if the market is subject to limited interventions;

- How a moving array of historical data inform about remaining and emerging regularities.

3.2. Ranking of Equities According to Their Suitability for Portfolio Purposes

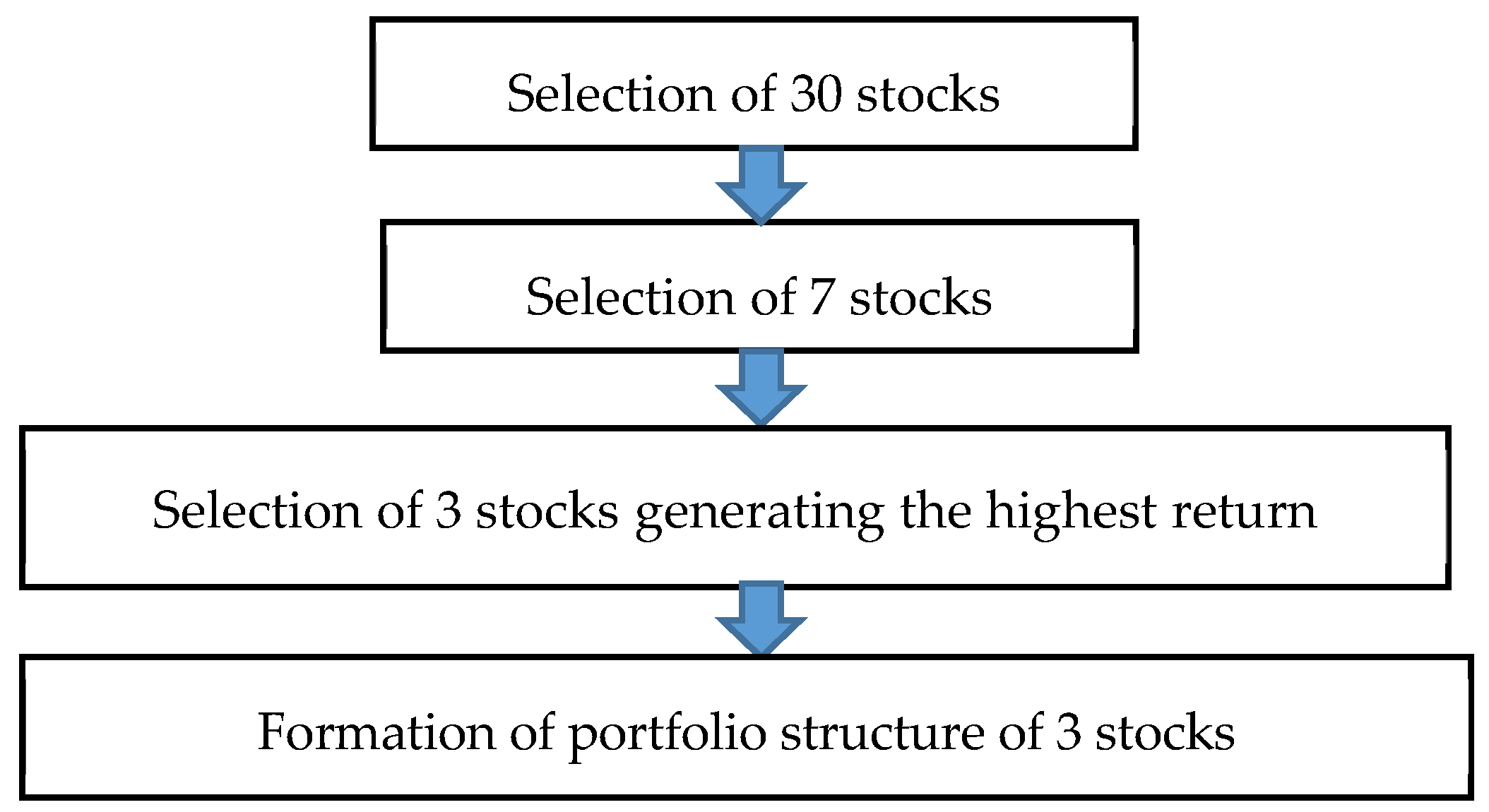

3.3. Selection of the Most Suitable Shares for Each Investment Step

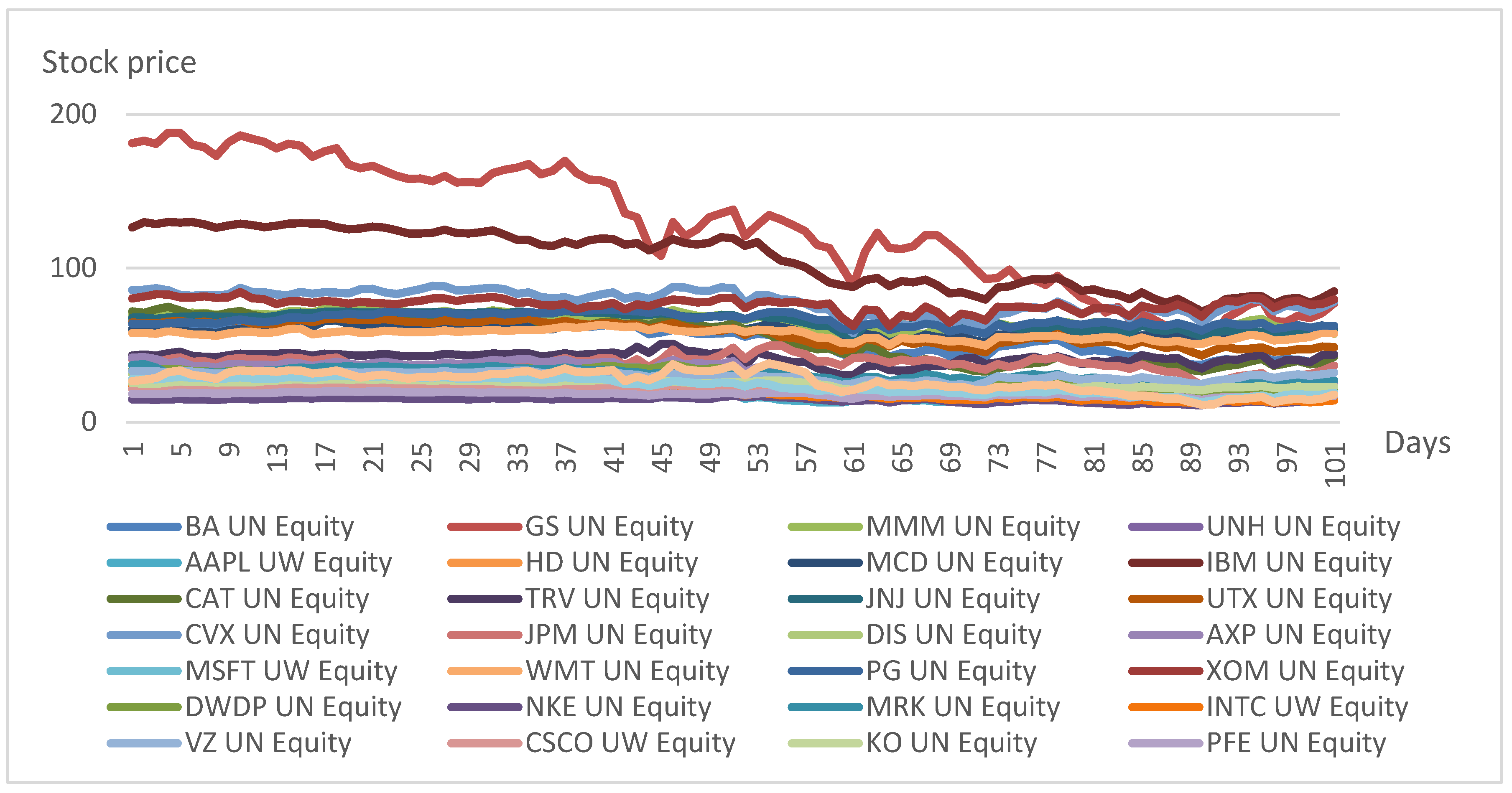

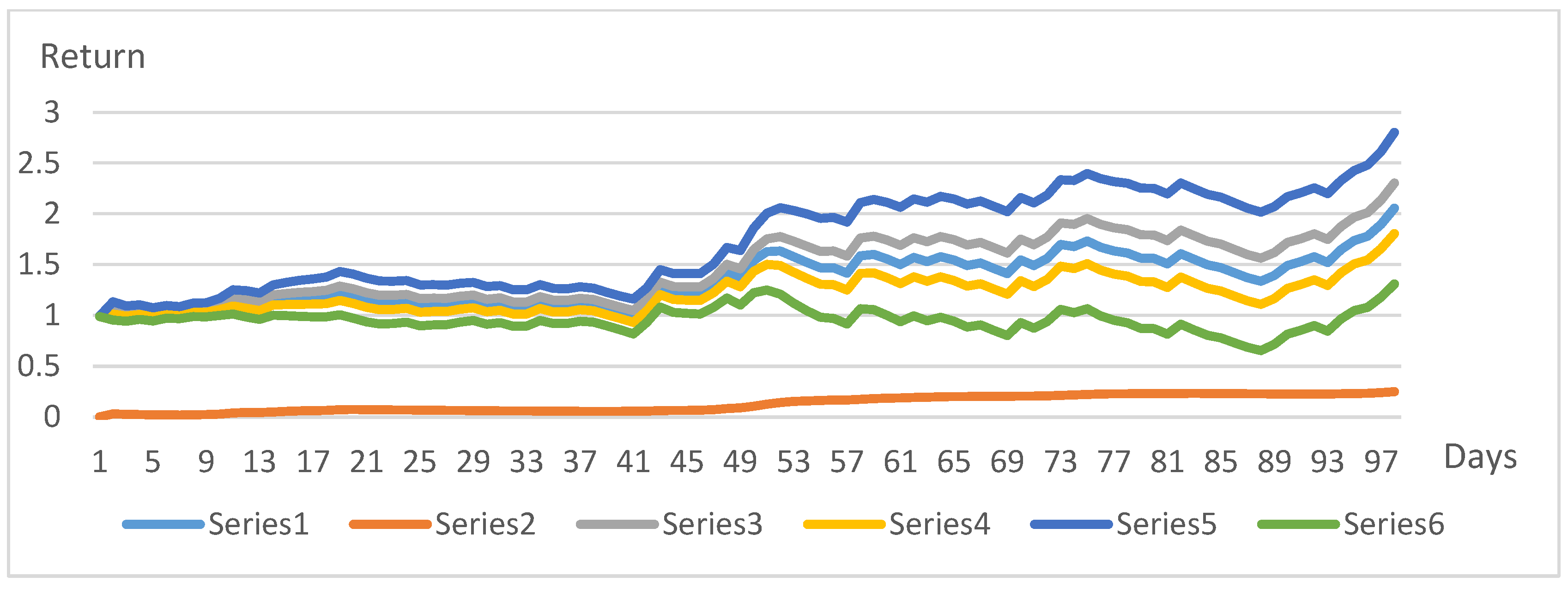

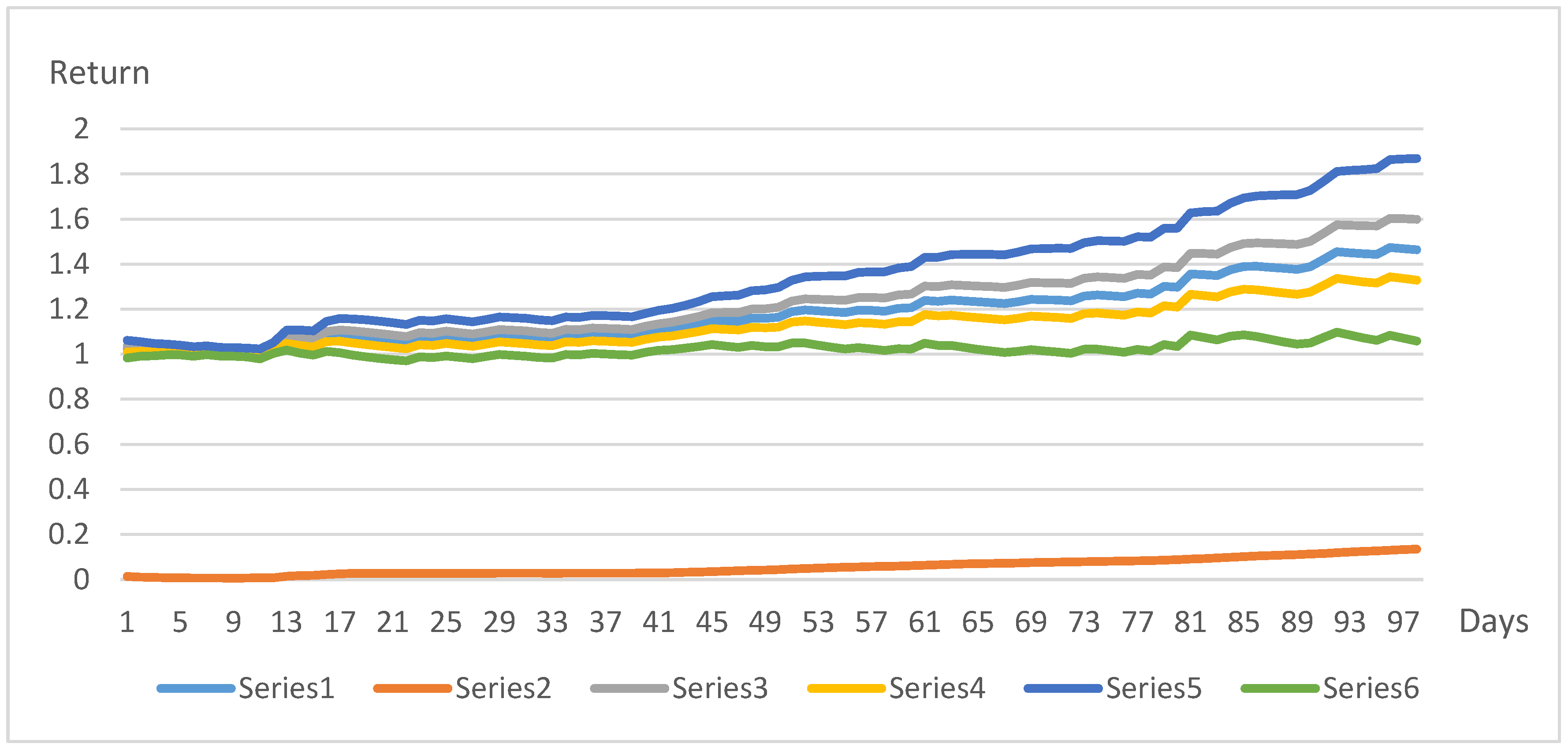

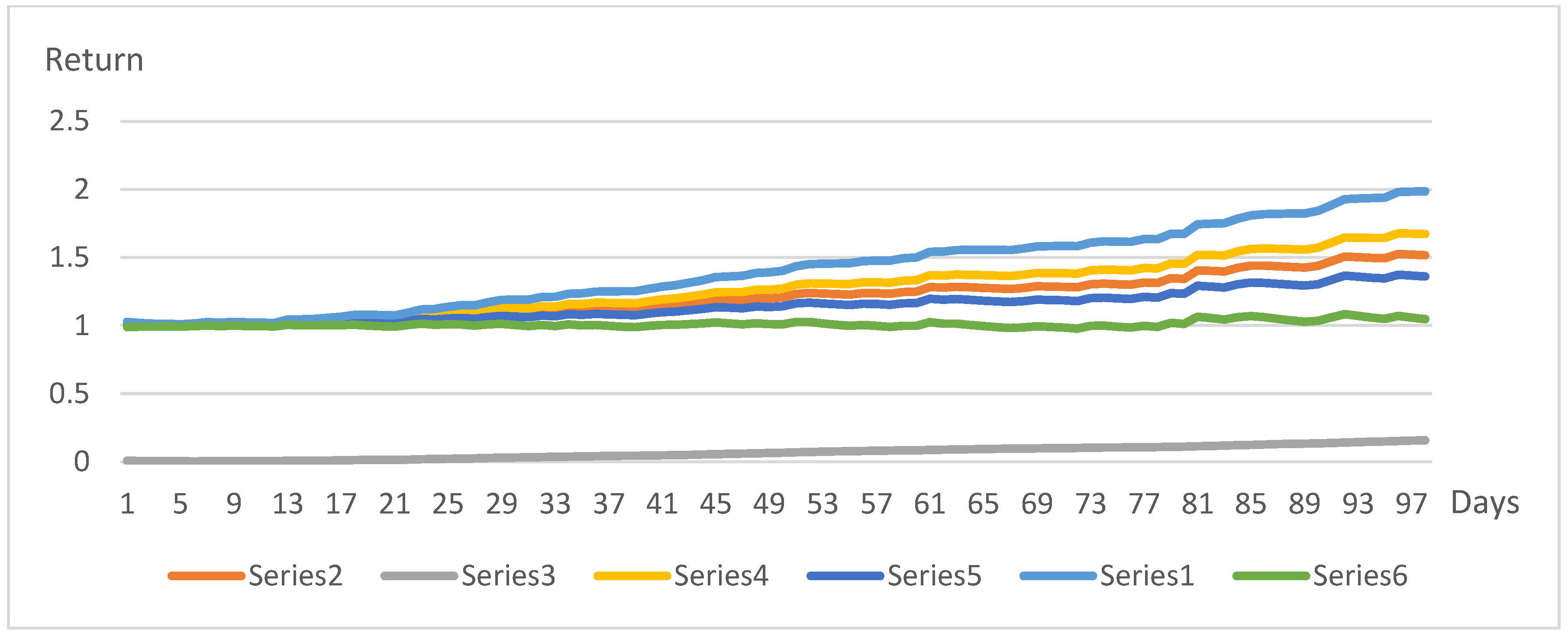

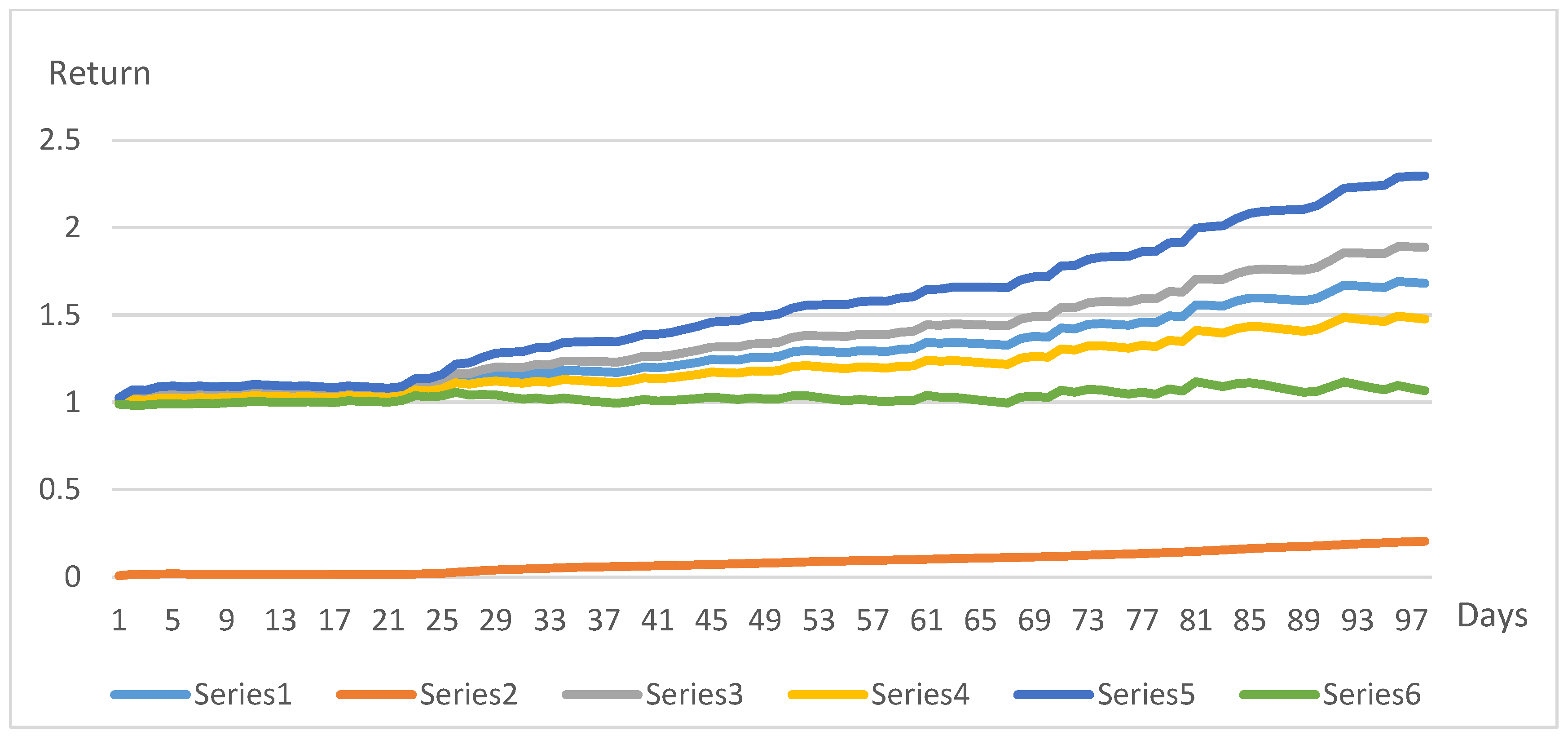

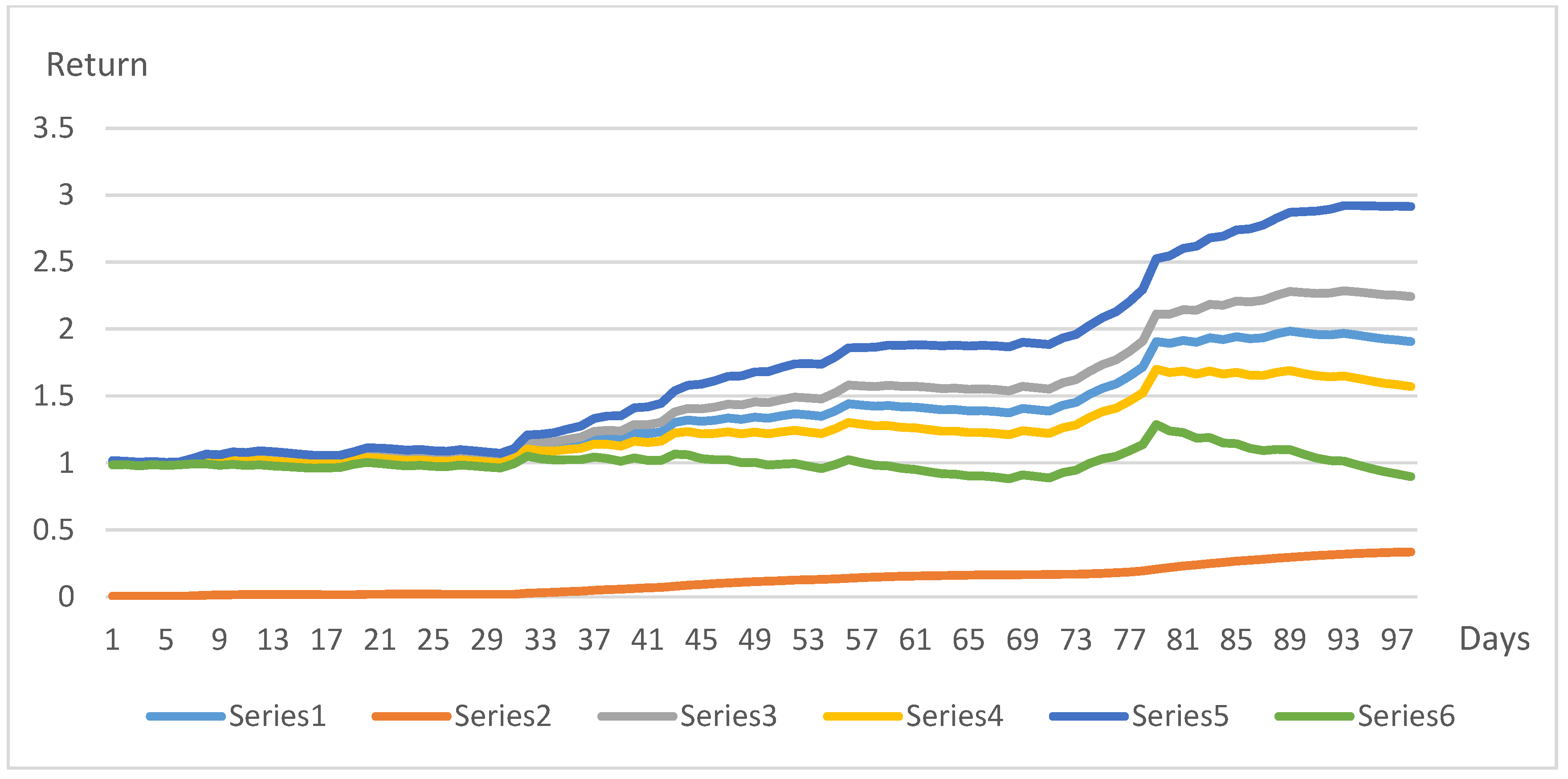

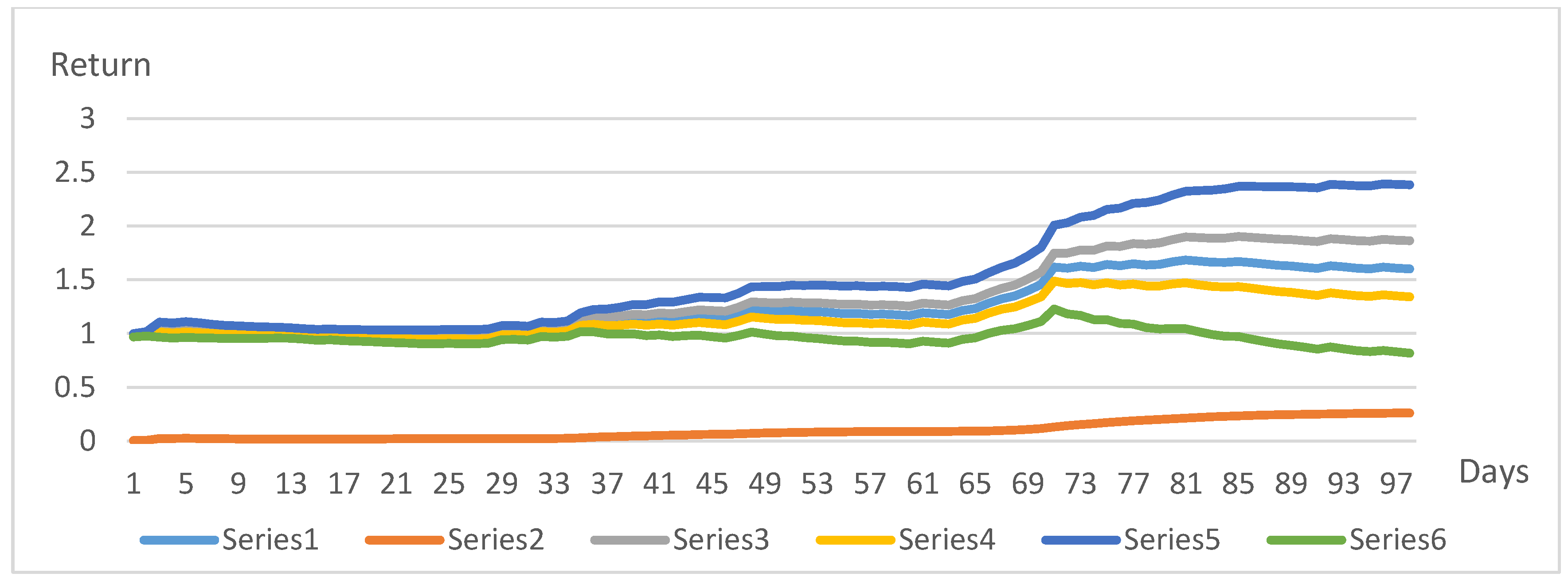

4. Results

4.1. The Search for the Highest Return during the Financial Crisis

4.2. Preconditions for the Practical Experiment

4.3. Presentation of Performed Experimental Solutions

5. Conclusions and Discussion

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Allen, David Edmund, and Elisa Luciano. 2019. Risk Analysis and Portfolio Modelling. Journal of Risk and Financial Management 12: 154. [Google Scholar] [CrossRef] [Green Version]

- Balloch, Adnan, Anamaria Nicolae, and Dennis Philip. 2015. Stock market literacy, trust, and participation. Review of Finance 19: 1925–63. [Google Scholar] [CrossRef]

- Basilio, Marcio Pereira, Jessica Galdino de Freitas, Milton George Fonseca Kmpffe, and Ricardo Bordeaux Rego. 2018. Investment portfolio formation via multicriteria decision aid: A Brazilian stock market study. Journal of Modelling in Management 13: 394–417. [Google Scholar] [CrossRef]

- Bhattacharyya, Rupak, Samarjit Kar, and Dwijesh Dutta Majumder. 2011. Fuzzy mean-variance-skewness portfolio selection models by interval analysis. Computers & Mathematics with Applications 61: 126–37. [Google Scholar] [CrossRef] [Green Version]

- Blanchett, David, and Philip Straehl. 2017. Portfolio implications of job-specific human capital risk. Journal of Asset Management 18: 1–15. [Google Scholar] [CrossRef]

- Boussaidi, Ramzi. 2017. The winner-loser effect in the Tunisian stock market: A multidimensional risk-based explanation. Borsa Istanbul Review 17: 178–89. [Google Scholar] [CrossRef]

- Bradfield, David, and Brian Munro. 2017. The number of stocks required for effective portfolio diversification: The South African case. South African Journal of Accounting Research 31: 44–59. [Google Scholar] [CrossRef]

- Cardak, Buly A., and Roger Wilkins. 2009. The determinants of household risky asset holding: Australian evidence on background risk and other factors. Journal of Banking and Finance 33: 830–60. [Google Scholar] [CrossRef] [Green Version]

- Dai, Bochuan, Ben R. Marshall, Nhut H. Nguyen, and Nuttawat Visaltanachoti. 2020. Risk reduction using trailing stop-loss rules. International Review of Finance 21: 1334–52. [Google Scholar] [CrossRef]

- De la Torre-Torres, Oscar V., Rvaristo Galeana-Figueroa, and José Álvarez-García. 2021. A Markov-Switching VSTOXX Trading Algorithm for Enhancing EUR Stock Portfolio Performance. Mathematics 9: 1030. [Google Scholar] [CrossRef]

- Frijns, Bart, Esther Koellen, and Thorsten Lehnert. 2008. On the determinants of portfolio choice. Journal of Economic Behavior & Organization 66: 373–86. [Google Scholar] [CrossRef]

- Fu, Yi, Shuai Cao, and Tao Pang. 2020. A Sustainable Quantitative Stock Selection Strategy Based on Dynamic Factor Adjustment. Sustainability 12: 3978. [Google Scholar] [CrossRef]

- Gambrah, Priscilla Serwaa Nkyira, and Traian Adrian Pirvu. 2014. Risk measures and portfolio optimization. Journal of Risk and Financial Management 7: 113–29. [Google Scholar] [CrossRef] [Green Version]

- Gao, Wei, Ruzhen Yan, and Xu Wu. 2016. Research Progress of Algorithmic Trading at Home and Abroad. Proceedings of the First International Conference on Economic and Business Management (FEBM 2016) 16: 40–45. [Google Scholar]

- Ha, Youngmin, and Hai Zhang. 2020. Algorithmic trading for online portfolio selection under limited market liquidity. European Journal of Operational Research 286: 1033–51. [Google Scholar] [CrossRef]

- Han, Yufeng, Guofu Zhou, and Yingzi Zhu. 2016. Taming momentum crashes: A simple stop-loss strategy. SSRN Working Paper. September 24. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2407199 (accessed on 5 November 2021).

- Jain, Jinesh, Nidhi Walia, Sanjay Gupta, Kriti Aggarwal, and Simarjeet Singh. 2021. A fuzzy analytical hierarchy process framework for stock selection in the Indian stock market. Journal of Public Affairs, e2710. [Google Scholar] [CrossRef]

- Jothimani, Dhanya, Ravi Shankar, and Surendra S. Yadav. 2017. A PCA-DEA framework for stock selection in Indian stock market. Journal of Modelling in Management 12: 386–403. [Google Scholar] [CrossRef]

- Khan, Mohammad Tariqul Islam, Siow-Hooi Tan, Lee-Lee Chong, and Gerald Guan Gan Goh. 2021. Investment environment, stock market perception and stock investments after stock market crash. International Journal of Emerging Markets. Ahead of print. [Google Scholar] [CrossRef]

- Li, Bo, and Ranran Zhang. 2021. A new mean-variance-entropy model for uncertain portfolio optimization with liquidity and diversification. Chaos, Solitons & Fractals 146: 110842. [Google Scholar] [CrossRef]

- Li, Jianjun, Qize Li, and Xu Wei. 2020. Financial literacy, household portfolio choice and investment return. Pacific-Basin Finance Journal 62: 101370. [Google Scholar] [CrossRef]

- Lu, Xiaomeng, Jiaojiao Guo, and Hailing Zhou. 2021. Digital financial inclusion development, investment diversification, and household extreme portfolio risk. Accounting and Finance 61: 6225–61. [Google Scholar] [CrossRef]

- Markowitz, Harry. 1952. Portfolio selection. The Journal of Finance 7: 77–91. [Google Scholar]

- Naqvi, Bushra, Nawazish Mirza, Waqar Azeem Naqvi, and S. K. A. Rizvi. 2017. Portfolio optimisation with higher moments of risk at the Pakistan Stock Exchange. Economic Research Ekonomska Istrazivanja 30: 1594–610. [Google Scholar] [CrossRef] [Green Version]

- Oyenubi, Adeola. 2019. Diversification Measures and the Optimal Number of Stocks in a Portfolio: An Information Theoretic Explanation. Computational Economics 54: 1443–71. [Google Scholar] [CrossRef] [Green Version]

- Pan, Heping, and Manxiao Long. 2021. Intelligent Portfolio Theory and Application in Stock Investment with Multi-Factor Models and Trend Following Trading Strategies. Procedia Computer Science 187: 414–19. [Google Scholar] [CrossRef]

- Rutkauskas, Aleksandras Vytautas, and Viktorija Stasytytė. 2020. Stochastic informative expert system for investment. Journal of Business Economics and Management 21: 136–56. [Google Scholar] [CrossRef] [Green Version]

- Scherer, Bernd. 2017. Algorithmic portfolio choice: Lessons from panel survey data. Financial Markets and Portfolio Management 31: 49–67. [Google Scholar] [CrossRef]

- Shen, Kao-Yi, and Gwo-Hshiung Tzeng. 2015. Combined soft computing model for value stock selection based on fundamental analysis. Applied Soft Computing 37: 142–55. [Google Scholar] [CrossRef]

- Sun, Yutong, and Hanqing Zhao. 2015. Stock Selection Model Based on Advanced AdaBoost Algorithm. Paper presented at 7th International Conference on Modelling,Identification and Control (ICMIC), Sousse, Tunisia, December 18–20; pp. 290–96. [Google Scholar]

- Temel Nalin, Halime. 2013. Determinants of household saving and portfolio choice behaviour in Turkey. Acta Oeconomia 63: 309–31. [Google Scholar] [CrossRef]

- Thakurata, Indrajit. 2021. Optimal portfolio choice with stock market entry costs and human capital investments: A developing country model. International Review of Economics & Finance 73: 175–95. [Google Scholar] [CrossRef]

- Toit, Tim. 2015. Truths about Stop-Losses That Nobody Wants to Believe. Hamburg: Serendipity Ventures UG, Available online: https://www.quant-investing.com/blogs/general/2015/02/16/truths-about-stop-losses-that-nobody-wants-to-believe (accessed on 10 November 2021).

- Wang, Feng, Keren Dong, and Xiaotie Deng. 2009a. Algorithmic trading system: Design and applications. Frontiers of Computer Science in China 3: 235–46. [Google Scholar] [CrossRef]

- Wang, Jia, Gulser Meric, Zugang Liu, and Ilhan Meric. 2009b. Stock market crashes, firm characteristics, and stock returns. Journal of Banking and Finance 33: 1563–74. [Google Scholar] [CrossRef]

- Yang, Chunpeng, and Zhanpei Zhang. 2021. Realization utility with stop-loss strategy. Quarterly Review of Economics and Finance 81: 261–75. [Google Scholar] [CrossRef]

- Yao, Rui, and Shan Lei. 2018. Source of Information and Projected Household Investment Portfolio Performance. Family & Consumer Sciences Research Journal 46: 219–37. [Google Scholar] [CrossRef] [Green Version]

- Yu, Jaeyong, Gunyoung Lee, and Jang Ho Kim. 2021. Towards Personal Financial Sustainability Based on Human Capital Analysis in Korea. Sustainability 13: 2700. [Google Scholar] [CrossRef]

- Zaimovic, Azra, Adna Omanovic, and Almira Arnaut-Berilo. 2021. How Many Stocks Are Sufficient for Equity Portfolio Diversification? A Review of the Literature. Journal of Risk and Financial Management 14: 551. [Google Scholar] [CrossRef]

- Zhang, Weiwei. 2017. Household risk aversion and portfolio choices. Mathematics and Financial Economics 11: 369–81. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Days | US | Germany | UK | ||||||

|---|---|---|---|---|---|---|---|---|---|

| TSLA | PFE | WBA | TKA | MRK | IFX | RR | RSW | TSCO | |

| 1 | 0 | 0 | 1 | 0 | 1 | 0 | 0 | 1 | 0 |

| 2 | 0 | 0 | 1 | 0 | 1 | 0 | 0 | 1 | 0 |

| 3 | 1 | 0 | 0 | 0 | 1 | 0 | 1 | 0 | 0 |

| 4 | 1 | 0 | 0 | 0 | 1 | 0 | 1 | 0 | 0 |

| 5 | 1 | 0 | 0 | 0 | 1 | 0 | 1 | 0 | 0 |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 96 | 1 | 0 | 0 | 0 | 1 | 0 | 1 | 0 | 0 |

| 97 | 1 | 0 | 0 | 0 | 1 | 0 | 1 | 0 | 0 |

| 98 | 1 | 0 | 0 | 0 | 1 | 0 | 1 | 0 | 0 |

| 99 | 1 | 0 | 0 | 0 | 1 | 0 | 1 | 0 | 0 |

| 100 | 1 | 0 | 0 | 0 | 1 | 0 | 1 | 0 | 0 |

| Steps | NIO, Inc | Boeing, Co | Pfizer, Inc |

|---|---|---|---|

| 1 | 1 | 0 | 0 |

| 2 | 1 | 0 | 0 |

| 3 | 0 | 1 | 0 |

| 4 | 0 | 1 | 0 |

| 5 | 0 | 1 | 0 |

| ... | ... | ... | ... |

| 196 | 1 | 0 | 0 |

| 197 | 1 | 0 | 0 |

| 198 | 1 | 0 | 0 |

| 199 | 1 | 0 | 0 |

| 200 | 1 | 0 | 0 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Rutkauskas, A.V.; Stasytytė, V. Integrated Intellectual Investment Portfolio as an Efficient Instrument to Manage Personal Financial Investment. J. Risk Financial Manag. 2022, 15, 30. https://doi.org/10.3390/jrfm15010030

Rutkauskas AV, Stasytytė V. Integrated Intellectual Investment Portfolio as an Efficient Instrument to Manage Personal Financial Investment. Journal of Risk and Financial Management. 2022; 15(1):30. https://doi.org/10.3390/jrfm15010030

Chicago/Turabian StyleRutkauskas, Aleksandras Vytautas, and Viktorija Stasytytė. 2022. "Integrated Intellectual Investment Portfolio as an Efficient Instrument to Manage Personal Financial Investment" Journal of Risk and Financial Management 15, no. 1: 30. https://doi.org/10.3390/jrfm15010030

APA StyleRutkauskas, A. V., & Stasytytė, V. (2022). Integrated Intellectual Investment Portfolio as an Efficient Instrument to Manage Personal Financial Investment. Journal of Risk and Financial Management, 15(1), 30. https://doi.org/10.3390/jrfm15010030