1. Introduction

Since the global financial crisis in 2008, two monetary phenomena have garnered unprecedented attention by academics, policymakers, the media and the general public alike. The first is the realization that our financial systems are, on the whole, brittle and prone to repetitive crises that can occur without prior warning. The other is the diversification of the practice of complementary currencies, be it in the form of local initiatives like the Brixton Pound, timebanks, business-to-business currencies and, of course, Bitcoin and its many emulators called “crypto-currencies”.

From a vantage point in this practice of currency innovation, this paper looks back at the legal definitions of conventional money and questions their adequacy for enabling long-term stability through monetary diversification.

This question is based on an argument of ecological economics, which sees both phenomena, diversity and systemic stability, as connected; as in natural ecosystems, so in finance: Theoretic ecology defines sustainability to be a trade-off function between efficiency and resilience (

Ulanowicz et al. 2009). Hence, efficiency in extremis makes systems prone to failure from external shocks. Resilience, on the other hand, is a composite function from diversity and interconnectivity where the excessive focus on diversity over efficiency leads to stagnation. Systems theory extends those findings to all flow-network-systems, including our economic and financial systems, with their ostensible imperative for efficiency gains (

Goerner et al. 2009). Consequently, monetary diversity is here seen as a way to increase the resilience of our financial system to prevent recurring crises and shift the balance towards sustainability (

Lietaer et al. 2010).

Furthermore, increased agility, choice and diversity in economic valuation and transacting offered by monetary innovation allows for the use of new information technologies without sacrificing ever more components of the human and natural world to the logic of monetization. As novel currencies can be based not only on new technologies but on completely different value systems, they can extend financial inclusion to communities and individuals, in all their societal embeddedness, without creating more liabilities to the hegemonic powers of our current economic system. (

Lietaer and Belgin 2011).

Hence, diversity in financial systems needs to be sought not only at the level of banks and similar financial service providers, as beneficial as a multitude of different business models may already be at that level (see

Prieg and Greenham 2012). The fundamental level for diversity in finance here argued for is that of currencies used to measure and orientate our economic activities in general. This paper argues that the numerous national and supranational currencies, which make up that level today, constitute only a nominal form of diversity. They are all too similar in their issuance-mechanisms and furthermore linked through international forex markets, which value them with reference to only a small number of internationally dominating currencies like the US dollar, the euro, yen and British Pound (

Bahaj and Reis 2020).

This limited diversity is boosted to some degree by novel forms of transmission technologies and operators, often referred to as the payments- and FinTech-industries, which facilitate the aggregation and redistribution of those same currencies. Going beyond the praise and attention that these sectors currently receive for their innovation and proliferation, it is here deemed important to redirect our attention towards the diversity of currencies themselves in order to ensure the long term sustainability of our monetary systems. This kind of diversity is predominantly offered by the practice of “complementary currencies”, a term here used to refer to all systems of transferable units that facilitate collaboration within designated geographic, virtual or sectoral communities and co-exist with what is here called “conventional currencies” (e.g., the euro, the US dollar, the yen, and the like).

In retrospect, it is surprising that the state and nature of our global monetary system with its recurrent financial crises was only called into question at large in the aftermath of its last global crash in 2008. General suspicions towards the design and dynamics of modern money and finance have been iconically echoed even by Queen Elizabeth II asking at the Bank of England: “I guess in monetary terms it is difficult foreseeing. But people had got a bit… lax?” (

Melendez 2012). At the same time, headlines about the astronomical rise of the Bitcoin price catapulted the idea that money could, and possibly should, be created in completely different ways, into main-stream (media-)attention and awareness (see, e.g.,

European Central Bank 2012). The practice of crypto-currencies has since fanned out enormously but still only constitutes a fraction of the potential for monetary diversity here ascribed to complementary currencies. While crypto-currencies are now being considered for the diversification of individual portfolios (compare

Papadamou et al. 2020), their diversity in terms of currency design is comparably limited. The above argument that 180 national currencies only constitute a “formal” diversity also applies to most crypto-currencies. Particularly the most popular ones are as similar to each other as they are alien to conventional finance (for example, in regards to their strongly correlated market price, see

Vaz de Melo Mendes and Fluminense Carneiro 2020).

Few realize that complementary currencies (in the following abbreviated as CCs) have always existed in parallel to the incumbent conventional currencies. Bitcoin was by no means the first. Previously, however, CCs were seen to be too marginal to be recognized by academics and commentators of the economic disciplines. Under the radar, CCs have become a more or less unified field of advocacy and research since the 1990s, when the emergence of widely accessible information technologies accelerated their proliferation. In parallel, key authors and activists found a niche in the consolidating field of transdisciplinary “alternative economics” and introduced the practice and tentative theory of CCs to ever-expanding audiences (exemplary, in alphabetical order, are Edgar Cahn, Thomas Greco, Margrit Kennedy, Bernard Lietaer and Michael Linton). In the academic arena, this was accompanied by a specialist peer-reviewed journal (the IJCCR) launched in 1997, and finally, an international research association (the RAMICS), founded in 2015.

However, in practice, the diversification of complementary currencies and other forms of financial and monetary innovations are still stifled in two ways. First, by the often unquestioned prevalence of incumbent forms of money and the market saturation of established financial service providers, which together make it hard for any challengers to gain widespread traction. The second factor, which is the focus of this paper, are the regulatory hurdles, which are often prohibitively costly in terms of money and/or time for innovators to overcome. Because for certain monetary innovations, the acquisition of adequate licenses, or even just achieving official recognition of their legality, often hinges on the question of whether they are considered “money” in or by the law, and what rights and obligations would follow from that judgment (compare

CCIA 2015b). It is with regard to those practical difficulties of currency innovation that this paper will examine the definitions of “money” and “currency” in current law for their adequacy in accommodating called for innovation and diversification or not.

2. “Money” and “Currency” in Financial Legislation

Legal professionals do not claim the final word on establishing “what money is” and refer to economists for having a broader and practically more relevant vision of money (compare

Proctor 2012, p. 10). Yet, when economists are probed to define money beyond descriptions of its use and functionality, they are quick to admit, even at the Bank of England, that “there is no universal agreement on what money actually is” (

McLeay et al. 2014a)—and they refer back to the legal disciplines for concise answers (e.g., in

Bholat et al. 2015).

For the feasibility of complementary currencies initiatives, this situation remains untenable. Previous research with multi-sector currency issuers in Europe has revealed how legal uncertainties and misconceptions on the part of the prudential regulators limit their establishment and success (

CCIA 2015a, p. 126ff.;

CCIA 2015d). This is particularly true for small not-for-profit organizations for whom the risk of any legal challenges is prohibitively expensive, even if the charges would ultimately turn out to be unfounded. In this way, legal gray areas constitute an undue advantage to incumbents and stifle innovation.

Consequently, the hypothesis of the research here presented is that difficulties in categorizing and then regulating monetary innovation are due to the basic definitions of money and currency in the law. As surprising as such suspicions towards the letter of the law may seem to lay observers, they have been broadly pointed at even in regards to conventional money. 20th-century economist von Hayek already jibed “that there is one clearly defined thing called “money” […], a fiction introduced to satisfy the work of the lawyer or judge, was never true” (

von Hayek 1990, p. 57). More recently, legal scholar Proctor observed in his seminal textbook on “the legal aspects of money” that the monetary theory found in US legislation today “has an air of unreality about it” (

Proctor 2012, p. 40). Moreover, speaking more specifically to the stance of this paper, the Tapscott technology exegetes found current legislation “woefully inadequate” when it attempts to regulate state-of-the-art currency innovation with “rules written around the time of the Civil War.” (

Tapscott and Tapscott 2017, p. 24).

However, a critical word-by-word analysis of legal definitions across a broad-spectrum of financial statutes not geared at solving only a specific legal case but concerned with the fundamental question of the nature of money and complementary currencies lacked from the literature. While legal professions may be limited in what they can see and say due to disciplinary expectations and the terminological framework they inherited, the transdisciplinary approach of this paper lends a fresh rigor and relevance to the seemingly drained research question of “what is the legal definition of money”. To make sure that the analysis of legal texts, presented in the next section, clearly distinguishes between the obscurity of language and the obscurity of meaning, the help of legal professionals was sought during a doctoral research placement at a law firm in California in the first quarter of 2017.

The conclusions drawn from the US are here deemed to point towards a widespread and general issue while recognizing that legal texts differ from country to country, particularly when comparing common-law (like the US and the UK) and civic-law systems (like in continental Europe). Because, in today’s highly digitized and globalized financial system, any substantial differences in legal definitions of “money” are likely to harbor opportunities of regulatory arbitrage that would force all constituencies to align in fundamental aspects of their regulatory practices (

Riles 2014). What is more, there is a range of international organizations like the Bank for International Settlements (BIS), the International Monetary Fund (IMF), and the World Bank which negotiate and monitor the global financial system. These two factors would be expected to have flagged up and equalized any major differences between monetary definitions and practices across dominant constituencies (compare

Cihak et al. 2012;

Claessens and Kodres 2014, p. 8;

Blanc 2017, p. 244).

With this view,

Section 4 will present findings and examples from the UK and the EU to support the general validity of the findings from the United States. Finally, recognizing the difficulty of reforming any legal structure (

Weeks and Smith 2018, p.10), particularly in subject areas that are as opaque and dominated by strong incumbent lobbies as money, finance and banking currently are (

Amann 2011;

Schroeder 2017),

Section 5 will make a case for a definition of “money” and “currency” that can unite theory and practice and be incorporated into financial policy and laws with only “minimally invasive” changes.

With regard to an assumed readership outside the legal disciplines, laws and statutes are here referenced in a way that makes it easy to find and verify their source.

3. Critical Examination of US Legal Definitions

A standard textbook, consulted by law students trying to comprehend the financial law of the US, uses the two terms “money” and “currency” in a way that suggests them being legally synonymous. The authors posit that “money”, in a narrow statutory sense, equals “cash”—and all other payment instruments are only “money substitutes” (

Gillette et al. 2007, p. 1). In support of this equation, they draw on the often-cited definition of “money” in the US Uniform Commercial Code (UCC), which reads: “a medium of exchange authorized or adopted by a domestic or foreign government” (U.C.C. § 1–201(24), see

Uniform Commercial Code 2017). “Cash” is here equal to the term “currency” in as much as it is defined in another central statute of the US, the Code of Federal Regulation (CFR). There, “currency” is: “The coin and paper money of the United States or of any other country that is designated as legal tender and that circulates and is customarily used and accepted as a medium of exchange” (CFR § 1010.100 (m), see

Code of Federal Regulations 2017).

Taken together, the two definitions lead to the textbook equation of “money” and “currency”. This, of course, contradicts both the everyday experience as well as the economists’ take on the matter. Both would agree that most “money” in circulation today comes not in the form of cash, but as electronic balances issued by commercial banks (

McLeay et al. 2014b;

Yang 2007, p. 201;

Huber 2016,

2017). However, those bank balances are explicitly excluded from the legal definition of currency here cited. It seems tempting to dismiss the relevance of this finding as a quirk attributed to legalistic language so often joked about being unintelligible and disjunct from common parlance. Moreover, obviously, it cannot have severe consequences in the real world; because otherwise, our economies would be left with hardly any “money” at all. As much as this complacency towards the letter of the law may seem justified while everything is running smoothly, it is here argued that such inconsistencies between theory and practice will become untenable in times of change, whether induced by crises or pre-emptive design.

To first understand the provenance of these surprising legal definitions, one needs to look back into the history of money and banking in the United States. In this paper, only a whistle-stop tour of the most relevant milestones of this history can be offered, with some exemplary findings and rulings from past and current legislation (for an in-depth analysis, see Chp. 7 in

Bindewald 2018).

3.1. Historic Monetary Statutes

The federal statute that launched the first step towards today’s banking system was the National Bank Act from 1863/64. Before this time, all bank charters were granted by individual states, not the federal government. The original text of this act also describes the new federal agency to control these new banks that were licensed to operate across all states, the Office of the Comptroller of the Currency (OCC) (Section 1,

U.S. Congress 1864, p. 99). The OCC thus created still exists today. The same act specifies the purpose of banks as “to carry on the business of banking by discounting and negotiating promissory notes, drafts, bills of exchange, and other evidence of debt; by receiving deposits; by buying and selling exchange, coin, and bullion; by loaning money on personal security; by obtaining, issuing, and circulating notes” (Section 8,

U.S. Congress 1864, p. 101). These notes here referred to were to be “a National Currency, secured by a Pledge of United State Bonds” (

U.S. Congress 1864, p. 99).

As commonplace as a “national currency” might seem today, at a time when the United States was consolidating their territories geographically across the whole continent, the notes issued by the new national banks, valid homogeneously across the whole nation, was a novelty. To appreciate their advantage, it is important to remember that “eight to nine thousand different-looking pieces of paper, each with the name of a [different] bank on it and a number of dollars” (

Sylla 2010) circulated in the US at that time. Even if the U.S. Constitution from 1788 had determined that all these colorful pieces of paper had to be backed 1:1 by their nominal worth in gold or silver (

Solomon 1996, p. 81), the verification of their trustworthiness was often difficult in a vast country without any of the information technology that we are so used to today.

Without explicit definitions given in the laws of the day, the meaning of the term “money” and “currency” in the National Bank Act can only be inferred by its usage in the text. The word “money” appears 48 times in the 64 sections of the act. Nearly half of those (22) come in the compound term “lawful money,” referring to the so-called “greenback” notes issued by congress in 1861–62, during the civil war (see

Solomon 1996, p. 62). The other 26 mentions of the word “money” appear in various generic contexts including, but not limited to, the new notes now to be issued, for example, in the sense that the national banks are “hereby authorized to issue and circulate [them] the same as money” (Section 23,

U.S. Congress 1864, p. 106).

The word “currency” appears with a very similar frequency—50 times altogether. The vast majority of those mentions (44) are in the name given to the above-mentioned regulatory agencies, the OCC. The other six examples also describe the new notes to be issued by the national banks. Hence, in functional proximity to coins, then and now only issued by governments, the term “currency” is here only employed for notes that are licensed and circulate at the national level. In this way, the usage of the two terms, “money” and “currency,” in 19th-century laws are indeed in close logical proximity to each other, and their implied synonymy would not have contradicted the practicalities of monetary means at the time. Following this line of reasoning, with “money” and “currency” both ascribed only to what the government issues or licenses, the next major legal milestone to observe is the Federal Reserve Act of 1913.

Half a century after the National Bank Act, the Federal Reserve Act (

U.S. Congress 1913) then established a further centralized banking structure for the now geographically and politically consolidated United States. This included the exclusive issuance of dollar notes not by the previously discussed national banks, but by the newly established Federal Reserve Banks (the FEDs). These notes were basically the same dollar notes that are still used today, if with upgraded visual designs and security features. In the 1913 FED act, the term “money” appears sixteen times, nine of these again in the composite term “lawful money”. The other instances refer to “money” held in reserve at the FEDs or the treasury, but it remains unspecified if this consisted only of “lawful money” or include other notes or assets as well. Three times, in the context of these reserves, the plural “moneys” is used (

U.S. Congress 1913, pp. 4, 17, 18). This could support the notion that reference to “money” here meant more than just “lawful money”, or it could simply refer to “lawful money” having accumulated from different sources, in the way that the term “monies” is defined in dictionaries today, as in funds composed of several individual “amounts of money” (

Cambridge University Press n.d.).

The FED Act uses the term “currency” 37 times, but again, 33 of those are in the title of the OCC. The word “currency” is only mentioned once in regard to the notes to be issued by the FEDs (

U.S. Congress 1913, p. 1), and the remaining three mentions are in the context of the notes issued by national banks chartered by the National Bank Act (

U.S. Congress 1913, pp. 13, 26, 29). With this, the legal term “currency” continues to refer only to the notes put into circulation by the government, or banks directly mandated by it, while the meaning of the term “money” retains its ambiguity. However, probing language from the vantage point of another century demands to first apply the benefit of the doubt: what appears to be an ambiguity in light of today’s practices of money and finance may not have been inconsistent at the time. This consideration raises the question at which point the narrow meaning of “money” in the law (being equal to that of “currency”) would have uncoupled from financial practice? A follow-up question would then be why this went unheeded when later laws were written? To answer those, it seems necessary to not only consult financial law itself but to expand the field of vision to encompass other societal and technological developments.

3.2. Development of Information Technology and Banking

Around the time of the radical changes to banking and notes-issuance described above, other sectors also experienced enormous innovations, which would soon become relevant for finance and banking as well. Before the telegraph found widespread use for news and personal messages, the now legendary Pony Express Service had hauled small volumes of messages and important papers, including commercial ones, across the American continent within ten days. The transport and logistics company Wells Fargo was involved in the last six months of the service’s existence until it was made abruptly redundant simply by the installation of one continuous cable running across the breadth of the United States in 1861 (

Engstrand 2013, p. 27). This had effectively reduced the transmission time of messages from ten days to a few seconds. With this, the age of information technologies had begun. This also led to a step-change in the way payments and banking were conducted: In 1918, the FED banks started to use Morse code to execute long-distance electronic payments (

Federal Reserve 2014, p. 7). All payments to that date relied on a physical medium of exchange, be it coins, precious metal, banknotes or letters with codified instructions, to be transmitted “hand-to-hand”. A trace of this pedigree, from ponies to instant payments, can still be observed in the company histories and even the names of some of the largest banks in the US. Wells Fargo and American Express both started off as transport companies but, following the evolution of money, they abandoned their trade entirely and moved into banking (

Bindewald 2018, pp. 175–78). The electromagnetic representations of monetary media eventually affected not only the practicalities and industry of money transmission but eventually also the nature of money itself.

With the expansion of the field of communication technologies and computing, electronic representations of “money” increased gradually in usefulness and prevalence until their number grew almost exponentially in the 1970s (

Positive Money n.d.). Today, nearly all payments and nearly all the issuance of conventional money is done electronically, by procedures and entities not foreseen by the statutes discussed above. However, despite these fundamental changes to the common medium of exchange in the 20th-century, modern laws continue to define currency as it appeared more than two hundred years ago: only as “coin and paper money” (CFR § 1010.100 (m), see

Code of Federal Regulations 2017).

To examine the adequacy and consequences of those antiquated notions still present in modern financial regulation, we will now fast forward to the latest major change to affect the way financial transactions are being conducted today, namely to the phenomenon called “virtual currency”.

3.3. Contemporary Innovation and Statutes

With the astounding increase of Bitcoin’s market value and prominent cases of criminal activities involving its use, not only regulatory and legislative agencies but also the courts were soon presented with the question of categorizing this new phenomenon in regards to its status as money. Because if Bitcoin and the like would not be considered “money,” how would they fall under financial supervision and regulation? A landmark court case was the US Securities and Exchange Commission (SEC) suing the founder of a Bitcoin-related website for fraud against the people who used his website to purchase and hold Bitcoins with the expectation of a financial return (

Greene 2013). Unsurprisingly, the defendant argued that Bitcoin has nothing to do with money, and consequently, the SEC and the courts had no case in this. On the face of it, his website operated in the classic form of a Ponzi scheme through which newly paid-in funds provide the capital to pay returns to previous investors. This, of course, only works as long as new people buy into it. Thus, there was clearly an element of fraud in the defendant’s activities, and the courts affirmed their position and convicted him. In the argumentation, however, judge Mazzant took the extra step of likening Bitcoin to “money” and “currency”, saying: “Bitcoin is an electronic form of currency unbacked by any real asset and without species, such as a coin or precious metal. [...] It is clear that Bitcoin can be used as money. It can be used to purchase goods or services [...].” (

Mazzant 2013, p. 3). Through the use of the comparative “as money”, this still holds a certain openness as to the definition of both terms, money and currency, or their equivalence. However, Mazzant went on to conclude most definitely: “Therefore, Bitcoin is a currency or form of money and investors wishing to invest in [the defendant’s online platform] provided an investment of money”.

His functional or phenomenological argumentation that something “can be used as money” is an approach to defining money that provides a much greater openness than the definitions we have thus far found in the law. The word “currency” would then describe “a form of money”, which holds the two words in a clear relationship to each other, but not as synonymous. Judge Mazzant is not alone in this use of language, which is much closer to practice, yet obviously divergent from what the law suggests. Since 2013 several US agencies, from law enforcement to financial regulators and tax collectors, have reiterated such a description of Bitcoin as a sort of “currency”, and by extension “a form of money”, if with the addition of the descriptor “virtual” (compare

Internal Revenue Service 2014). Had they adhered to the letter of the law, by which “currency” is defined as notes and coins, no unit that exists only virtually or electronically could qualify to match this description, and the term “virtual currency” or “electronic currency” would simply amount to an oxymoron. In the case of Bitcoin, the second legal criterion for what a “currency” is, namely, being issued by state authority, would make the usage of the term additionally paradoxical. In 2013, apparently conscious of this problem, the United States Treasury’s Financial Crime Enforcement Network (FINCEN) defined “virtual currency” in their first comprehensive guidance note on Bitcoin businesses in reference to the above mentioned definition of “currency” in the CFR:

“In contrast to real currency, “virtual” currency is a medium of exchange that operates like a currency in some environments, but does not have all the attributes of real currency. In particular, virtual currency does not have legal tender status in any jurisdiction. This guidance addresses “convertible” virtual currency. This type of virtual currency either has an equivalent value in real currency, or acts as a substitute for real currency.”

By contrasting “virtual currency” with the term “real currency”, the simple term “currency” by itself loses all definitory solidity. Another verbatim illustration of this thread-bareness of seemingly simple terms is the “money transmitter legislation,” which is often evoked in regards to Bitcoin and other unconventional currencies because a FINCEN ruling of 2014 required all companies running, for example, a Bitcoin exchange platform, to obtain such a “money transmitter” license (

FINCEN 2014). However, when looking at the legislation defining what being a “money transmitter” means, it is curious to observe that a law by that title does not speak of “money” at all. It rather defines services that require a money transmitter license as those involved in “the transmission of currency, funds, or other value that substitutes for currency [...] by any means” (31 CFR § 1010.100 (ff)(5)(i)(A), see

Code of Federal Regulations 2017). However, straightforward as this may appear, the legal definition of “currency” cited above (notes and coins) is here ignored. Because the transport of cash, which would be the most tangible and historically predominant form of “money transmission”, is here explicitly excluded in a subclause of the same statute: “The term “money transmitter” shall not include a person that only [...] physically transports currency, other monetary instruments, other commercial paper, or other value that substitutes for currency” (31 CFR § 1010.100 (ff)(5)(ii)(D), see

Code of Federal Regulations 2017). What is left then of forms of money to be covered by this statute must be electronic ones, which is also made explicit in their definition of the term “transmission” which “includes, but is not limited to [...], an electronic funds transfer network” (31 CFR § 1010.100 (ff)(5)(i)(A), see

Code of Federal Regulations 2017).

On the other hand, the term “other value that can substitute for currency” in the above definition retains an option for including the transfer of absolutely anything valuable to fall under the “money transmission” regulation. This demonstrates the tacit understanding in modern law that the word “money” cannot simply equate to conventional currencies, neither in their cash nor electronic instantiations. Yet, if one were to explicitly follow the legal definitions of money and currency, the content of the “money transmitter act” would turn its title into a complete misnomer. By any standard of legal rigor, it would better be called “something-valuable-other-than-cash transmitter legislation”—otherwise one would implicitly accept, that the legal term “money” is ultimately void of any definitive meaning.

3.4. Legal Irrelevance of “Legal Tender”

The last landmark ruling to be examined here is the Internal Revenue Service (IRS) guidance on Bitcoin from 2014. To a large extent they followed the wording of

FINCEN (

2013) quoted above, but with a caveat about Bitcoin not being considered “legal tender”: it only “operates like “real” currency—i.e., the coin and paper money of the United States or of any other country that is designated as legal tender, [...], but does not have legal tender status in any jurisdiction” (

Internal Revenue Service 2014). This indicates that the concept of “legal tender” remains as a potential category by which to distinguish “money” from “not money”. However, by now it is probably not surprising to find that this term, like the others discussed above, is more ambiguous in the law than its use in common language would have us believe. To many people, across different countries and languages, a form of money or currency described as “legal tender” would be the official means of payment of a country, particularly when it comes to the final discharge of tax obligations. Some currency notes like the US dollar bills explicitly state that they are “legal tender for all debts, public and private”. By inference, any other form of money/currency is deemed to be of lesser status or ultimately even illegal. However, when put to the test in practice, one finds that businesses in most countries are allowed to refuse payments in cash, particularly when it comes to large sums.

The Department of the Treasury published a FAQ on this very question, deflating any strong commonplace assumption: the term only “means that all United States money as identified above are [sic] a valid and legal offer of payment for debts when tendered to a creditor. There is, however, no Federal statute mandating that a private business, a person or an organization must accept currency or coins as payment for goods and/or services.” (

Department of the Treasury 2011). Hence the “legality” of legal tender only concerns it being offered, while every person or business is free to accept that offer. The only case to which “legal tender” would thus not apply is a form of currency or payment that has been explicitly prohibited from being offered. Obvious examples of this would be counterfeit notes and coins resembling the US dollar. Illegality could also pertain to complementary currencies like Bitcoin or gold-coins. The former has been made illegal to trade or use in countries like Thailand (

Bajpai n.d.), the latter became illegal even in the United States when President Roosevelt signed Executive Order 6102 in 1933. This forbade Americans to own and trade in gold other than what was contained in their dental fillings (

Roosevelt 1933). This order remained in place until 1977.

In the absence of such explicit exclusions of what can be offered in contracts, the legal tender attribute is again no reliable distinction to elucidate what “money” may ultimately mean in the law.

4. International Comparison and Consequences

The critical reading of the US legislation has revealed how legal positions falsely assume that only economists have a wider understanding of the term “money”, while at the same time, economists falsely assume that the legal professions can offer a clear definition. If the narrow positions of “money equals currency” and “currency equals notes and coins” were to be followed, this would not only have radical ramifications for complementary currencies—namely that none of them would be either money or a currency—but also for the status of electronic bank balances: they would not be money in the legal sense either.

While this definitory narrowness might have been desirable in the 19th-century, at a time when political and structural centralization was key to the establishment of a large market-democracy, it now needs to be regarded critically. Monetary and economic policies that have led the world to the brink of ecosystem collapse and social unrest can hardly be expected to offer many alternative scenarios. However, innovation and diversification on all system levels need to be supported by adequate legislation.

To demonstrate how the legal equation of “money”, “currency” and “cash” is not only a source of friction for the critical theorist, and to support the introductory proposition that findings from the US would have some bearing on the situation elsewhere, it is illustrative to notice a court case brought to the highest courts of the European Union. It is about the seemingly simple matter of paying government fees in cash. A German journalist had tried to do just that at a public broadcaster in Frankfurt. When the corporation insisted on electronic payments, he persisted and took the case first to the German Federal Administrative Court, which deferred it to the EU Court of Justice (

Dietrich and Häring v. Hessischer Rundfunk; see

InfoCuria 2019). This court case is relevant here not because of the status of cash in modern economies, nor the plaintiff’s ambition to safeguard its existence in the face of strong lobbies calling for a “war on cash” (

Mason 2016). The fact that this case has gone through to the highest courts simply adds practical evidence for the prior argument that legal definitions of what constitutes “money” or “currency” are not as solid as one would expect, even in regards to the conventional currency.

With regard to Bitcoin, the European monetary system and its definitions seem similarly confused. In 2018 the European Central Bank published a statement saying that Bitcoin is not a currency and it falls outside their regulatory mandate (

European Central Bank 2018). Virtually at the same time, the German Ministry of Finance declared, just as explicitly, that the use of Bitcoins and other “so-called crypto-currencies will be treated as equal to conventional means of payment” (

Bundesministerium der Finanzen 2018, my translation). It seems to be only a matter of time until such inconsistencies become untenable and will be dealt with in courts.

In the UK, the terminology around Bitcoin and other novel currencies has even been called “categorical anarchy” (

Vergne and Swain 2017). Legal definitions of “money” have there been found lacking in rigor and clarity, just as was here demonstrated for the US (

Harrington 2017). After examining the statutes of the United Kingdom in a manner similar to the one here employed, linguist and barrister Dr. Kate Harrington affirms that, even if conventional money today comes mostly in electronic or virtual forms, “the language of the tangible will still creep in” and “cash” and “money” have become confounded terms in the law (

Harrington 2017, p. 286). Money, she concludes, “must, for legal purposes, have a very specific meaning as the definition in its particular legal situations must necessarily often determine complex disputes as well as regulate the smooth working of commercial and domestic lives” (

Harrington 2017, p. 288). However, to the contrary, “money in law is difficult to define: it can encompass almost every common meaning or it may equate to none” (

Harrington 2017, p. 303).

This confusion also has effects on the definition of what banks are and do. Their defining activity has covertly evolved from “deposit-taking” to the creation of the electronic units (

Jakab and Kumhof 2015), for which the name “deposit” is a mere atavism. Enter novel currencies and things become even more confusing. In 2016 the federal OCC proposed a new type of bank-charter for financial technology providers in the US including, but not limited to, Bitcoin-exchanges, which neither take nor create conventional “deposits” (

OCC 2016). For this, the OCC was sued not by the affected FinTech challengers but by the financial regulator of the State of New York, claiming that this was an attempt to undermine state law by bending the federal definition of what a bank is and does (

Finextra 2017a). This case has been dismissed in court because the OCC had not actually created the proposed charters yet (

Finextra 2017b). However, the difficulty of classifying monetary innovations within traditional organizational categories remains and the imperative to update them continues to grow.

In other cases, proceedings do not pass so gently. In 2013 Will Ruddick and his team of currency innovators in Kenya found themselves imprisoned just ahead of the launch of a complementary paper currency. It was designed to provide small traders in an informal settlement near Mombasa with a self-issued media of exchange to bridge the lack of liquidity in the local micro-economy. It took several months for the prosecution to finally attest that no laws had been broken, and the issuance of something akin to money was not necessarily forgery (

Ruddick et al. 2015). Despite the positive outcome in Kenya, fears of potential repercussions for the issuers of complementary currencies had been fed by the US Federal Bureau of Investigation (FBI) accusing Bernard Nothaus, the issuer of silver coins called Liberty Dollars, of “a unique form of domestic terrorism” (

FBI 2011). Against this backdrop, many currency operators either shy away from launching their initiatives in the face of legal uncertainties (compare

CCIA 2015b, p.13) or choose to avoid the language of money and currency in public communications altogether (

Hart 2001, p. 281 and the author’s personal communications with activists in Germany, UK and US) despite their espoused objective of “reinventing money” (

Martignoni 2017).

Legal incoherence also harbors a form of favoritism towards commercial interests and large corporations. In contrast to the prohibitive effect of costly legal challenges for small nonprofit companies, the gray areas created by contradictory language in the law are an opportunity for companies affluent enough to afford legal consultants and lobbyists. There are two noteworthy cases that relate to a piece of European legislation prompted by a pre-blockchain innovation in payments. In the late 1990s, a new type of payment card was developed and commercially deployed, in which balances were stored directly on the chip of the card and could thus be spent at offline terminals without further verification. Since this form of “currency” fell in between and outside of the material form of cash and the so-called “scriptural” form of bank balances, European legislators spent significant time and paper on creating a custom licensing scheme for the operators of these cards: the Electronic Money Directive (EMD, see

European Commission 2009). Of course, only with respect to the underlying notion of “money equals cash” would the units stored “like cash” on a chip-card seem like a novel form deserving of the name “electronic money”, a designation never applied to conventional electronic bank balances. However, this novel technology always remained marginal in the payments market (

Bankenverband 2009) and the EMD had little traction. Enter a young American provider of online payments, called PayPal, in search of a license to expand their European business. Conveniently, the fallow EMD was expanded beyond its original scope and wording to accommodate them (

Godschalk 2007) until they grew out of their custom built gray area and acquired a banking license from their new headquarters in Luxembourg (

Brown 2007).

In an opposite movement, Facebook’s Libra currency was introduced in 2019 to much buzzword-fanfare. Positioning itself as standing outside traditional payment providers and harnessing the hype around “crypto-currencies” gave the scheme operator a marketing advantage with media-outlets and potential users. It also prompted high-level politicians to speak up against the private issuance of currencies while they had never taking issue with the issuance of bank balances by commercial banks. For Facebook, any news about their claimed innovation was good news. For industry experts, however, able to see behind the crypto-smokescreen, the operation of Libra seemed to promise nothing but a payment system akin to PayPal apart from the rebaptized name of the transacted units. (

PaySys 2019). Now, if Libra would be allowed to come to market under an e-money license, it would provide politicians the opportunity of claiming sovereignty over the beast while again allowing an entity of colossal proportions to be regulated more leniently than a local credit union.

The legal gray areas, created by the monetary definitions here revealed, can only be negotiated opportunistically by large commercial entities with aggressive legal teams. Radical, diverse and particularly non-commercial initiatives are severely disadvantaged. Leveling the playing field for small benign issuers of currency is not only important for the systemic sustainability of the monetary system through diversification of currencies but also an imperative of consumer choice and protection in such a central aspect of our market economies. Both seem impossible, while legal terminology—instead of offering clarity—adds yet another layer of obfuscation to today’s financial regulations.

5. Coherent Terminology and Legal Reform

Updating laws and regulations to meet contemporary practices and requirements is difficult in practice (

Weeks and Smith 2018, p.10), however convincing or pressing the need and evidence may be. The results than often add further bloat to the already convoluted and voluminous corpus of legal texts. The 2010 Dodd–Frank act added 848 pages to existing financial regulations in the US (

The Economist 2012), while the total of EU regulations passed at the same time came to 34,019 pages (

Schick et al. 2016). With this in mind, the terminology here proposed is not only measured against its fit with the whole spectrum of monetary practices and its commensurability with rigorous monetary ontologies (see

Bindewald 2018, Chp. 3), but also for the “minimally invasive” changes required to introduce coherence and clarity to all existing laws currently speaking of money and currency.

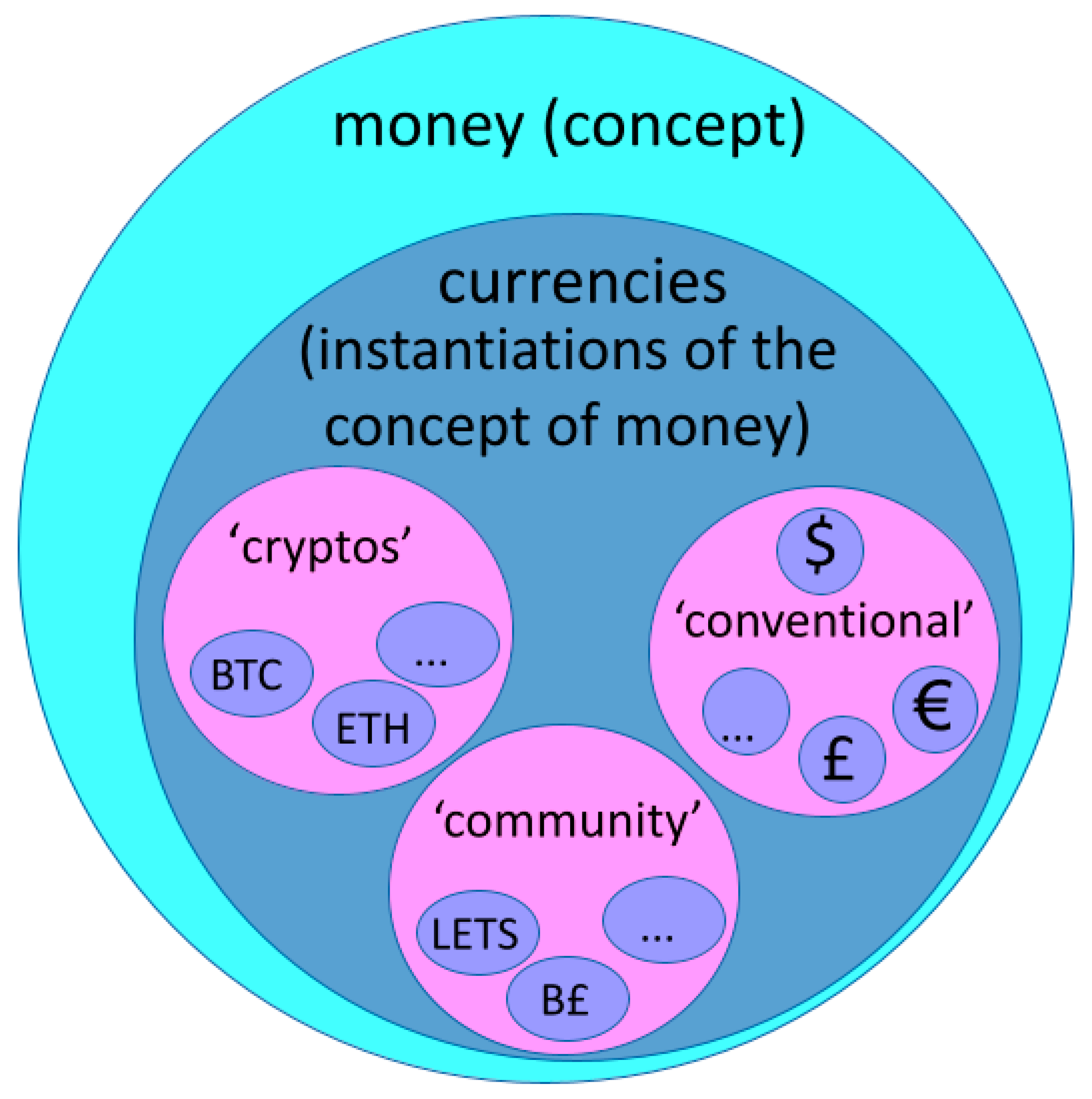

The underlying conceptual “hack” (in a sense ascribed to the word by

Scott 2013) would be to limit the meaning of the term “money” to that of a mere idea and leave all phenomena of instantiation of the concept of “money” to be described as “currencies”. The two words would thus be distinct, in the same way, we, for example, are accustomed to differentiating between the concept of “identity” and the derivative phenomenon called “passports”, or “energy” versus “electricity”, or how we do not use the words “car” and “transport” synonymously, however dominant cars as a form of transportation may be today. Granting the difference between ideal concepts and their worldly instantiations due awareness in the monetary domain is here seen as a precondition to solving the historic-terminological muddle outlined in the previous sections and merits reserving both their own specific term. Repurposing the terms “money” and “currency” with this new terminology seems not too much of a stretch since the following definitions are already implicitly included in common parlance, just not exclusively. The definitions here proposed are:

| “money” | = the abstract concept of transferable units that facilitate collaboration |

| “currency” | = the actual instantiations of the concept “money”: |

| | | unit-systems that are intentionally or implicitly designed for a |

| | | specific group of agents to transact for a specific purpose, in specific |

| | | ways and contexts. |

For the assignment of the term currency/currencies to any instantiation of the concept of money, it does here not matter in which particular way a currency system is designed and implemented or how transactions are executed: Be it by handing-over physical representations of those units made from whatever material, or by the reassignment of electromagnetic representations, in distributed or centralized databases.

Depicting the two terms as sets (see

Figure 1) still allows for terms like “crypto-currencies”, “community currencies”, “loyalty points,” or “time banks” to be coherently positioned in relation to each other and alongside conventional national currencies. They would simply become subsets or subcategories within or under the wider term currency. Only the term “complementary currencies” thus becomes somewhat redundant because without the theoretic and linguistic hegemony of conventional “money,” all currencies would equally complement all other currencies. However, in current practice and parlance, the term “complementary currencies” would adhere to the whole space/set of “currencies” apart from the subspace here labeled “conventional”.

To incorporate this terminology into current law would not require the amendment of current passages with more text. The simple if radical way here proposed would be to omit all references to the word “money” from all law texts, at least where it is not meant in the broad sense defined above. Instead, it would be replaced with the exact name or description of the currency/currencies that a given law is concerned with. Consequently, most appearances of the word “currency” in today’s legal texts would also be replaced with the words “notes and coins”, “cash”, or more concise descriptions like “euro-banknotes”, “US dollar coins”, etc. In the US this would mean that laws only refer to the US dollar, in the eurozone to the euro, in the UK to pound sterling and not, broad brush, to “money”.

This would have two direct effects on diversity and reform. First, any (complementary) currency system that has no direct interface with the national currency system falls clearly outside the scope of the laws that are then explicitly only concerned with, for example, the US dollar. It would thus not matter anymore if the issuers, users or any observer regard, categorize, describe, or even advertise currencies like the Sardex, the WIR, timebanks or LETS as “money” or something completely different. The ambiguity of that term would cease to be an impediment for the clarity of the law and, by extension, to the innovation, implementation and regulation of nonconventional currencies.

The second immediate benefit would be the elimination of the current legal contradictions, as revealed in the two previous sections, in regard to the question of whether notes, coins and central bank reserves are equivalent to electronic balances issued and held by commercial banks. That all of those practically counts as “money”, for all discourses, but the law, has been widely noted not only by economists but also by legal scholars (compare

von Hayek 1990, p. 91;

Proctor 2012, p. 40;

Huber 2016, p. 22). If the law were to refer to the US dollar instead of “money”, all payment instruments, physical or electronic, denominated in the US dollar would be included without a doubt.

6. Conclusions

The critical reading of US legislation presented in this paper has shown that the definitions of the terms “money” and “currency” are not only antiquated but inconsistent in their use even in modern statutes. The transdisciplinary approach here taken found answers to the question of “what is the legal definition of money” that revealed a level of contradictions in the statutes of the United States that cannot be explained or excused with the preconception that legal language is always difficult to understand. Complex language is only merited where it leads to more coherence, not less. Otherwise, it is simply jargon. Specifically, the term “currency” cannot, as it was found in the statutes examined here, be consistently defined as cash issued by national governments, while it is simultaneously used to talk about the opposite: units transacted electronically and issued by private institutions, whether banks or FinTech-challengers. The term money was found to be even more ambiguous: being at times used synonymously with currency and at other times encompassing anything of value that can be transacted. This equates to a haphazard appropriation of a term which is easily regarded as too general and idealistic to allow the law or state any exclusive right over it.

A general call for more concise legal definitions in monetary matters has been found elsewhere in the literature (e.g.,

Proctor 2012;

Huber 2016;

Harrington 2017). The following conclusions and policy recommendations build on that literature, but would benefit from future studies by legal scholars retracing the analyses of this paper across the individual statutes of the US. Similarly, the assumption here made about findings from a single constituency to be indicative of a general issue across all major economies (see

Section 2 and

Section 4) would merit in-depth multilingual research comparing definitions found in the Anglo-Saxon common-law system with those of so-called civil-law systems, for example in French and German legislation.

Financial regulations and legislation are important to protect individuals, companies and the economy as a whole from fraud, exploitation and undue volatility. Conventional currencies like the US dollar are important elements of their respective economies. As such, they merit preferential treatment by the law, for example, when it comes to the regulation of who may provide financial services denominated in these currencies and under what conditions. However, maintaining its protective function without becoming rigid, unresponsive, and a hindrance to innovation and democratic participation seems only possible if the law becomes more inclusive in recognizing the dominant electronic forms/practices of “money as we know it”.

Many banknotes today already bear a copyright symbol to declare and enforce the exclusive right of their respective central banks to their (re-)production. However, such intellectual property must not be attached to the term “money”, not even by inference based on inapt use of the word in legal texts. To be clear, this is not to support the libertarian notion that all currencies should be unregulated (compare

von Hayek 1990). Any issuer of a currency will create certain rules in the conception or design process of their units (see

Bindewald 2018, Chp. 5 and

CCIA 2015a) while complying with many societal and legal rules that apply to any activity in public, like, for example, taxation, consumer and data protection, etc. (

CCIA 2015c). However, no rules created for the protection of one currency system, even the biggest one, should infringe on the next currency, even if marginal in scale and scope. This argument directly opposes the narrow reading of so-called chartalist theories, according to which only a state can issue “money” (e.g.,

Ingham 1996, p. 523; compare

Proctor 2012, p. 40), while agreeing with those authors in their observation of the special status of state issued “currencies”.

When it comes to policy implications of the situation here described, it has been widely recognized that innovation demands adaptation. In the words of Gillette et al.: “The subject [of money] comes complete with a long and intricate history; an esoteric language [...]; and a dependence on technological developments that require constant accommodations in legal doctrine” (

Gillette et al. 2007, p. 1). However, the findings of this paper show that these “accommodations” do not happen consistently. Where laws and regulations have taken heed of innovation, they failed to do so coherently and thus created a situation that even the US government’s own watchdog calls “complex and fragmented” (

Government Accountability Office 2016), a judgment that this paper now allows to be extended even to the most basic terminology used in legal texts. Without radical revisions, as proposed in the previous section, new legislation will only ever be patchwork and will, as regularly warned against, lag behind innovation (

Cumming et al. 2019, p. 10) and become ever more disjunct from reality. A situation that, given the current state of global crises, is a risk to more than the financial system itself.

The view of monetary reform advocates, that if “legislators continue to slumber, it might very well happen, that [...] hardly revertible global facts are being created, which will finish off any financial sovereignty” (

Huber 2017, my translation), has here been extended to include monetary innovation and diversity. Policymakers must candidly consider basic definitions in the law and question their fit for a financial system that supports sustainability. Monetary diversity needs to be regarded as an important systemic feature that is worth protecting for more than nationalistic benefits which were argued for in opposition to the introduction of the euro (see

Blake 2020, p. 16). Following in the wake of technological advances and accommodating the ensuing profit-driven hypes will no longer be sufficient for lawmakers concerned with the common good. For those US statutes here analyzed, legal opinion had it that the findings of this paper were clear enough to introduce bills for their reform, if only a political sponsor was found to introduce the case to the respective courts and legislative branches.

To support the above policy implications, it is also important that research, practice and advocacy pay more minute attention to the way they use the terms money and currency. Of course, some manners of speaking may be more conducive to communicate certain points to certain audiences. However, to support the monetary, financial and economic reforms demanded by the seemingly permanent state of global crises we are now confronted with, the language at the basis of our common understanding needs to be simultaneously clear and inclusive. Currency innovation, practically and discursively, offers an opportunity to consider questions otherwise forgotten: What is the role we want money to play in our societies, and to what end? Moreover, which are the currencies that would fulfill this role most effectively?

The way in which money and currencies are talked about, inside and outside of legal contexts, needs to be seen as more than semantics. Language and discourse are how money and currencies are imbued with reality and social relevance. As “discursive institutions” (

Bindewald 2018), they become what we say they are—in a manner of speaking. Moreover, the stories told by the use and description of individual currencies coalesce into the ever-evolving story that is money. Consequently, the recognition that money or currency are not givens, particularly not given in or by the law alone, demands a heightened sense of alertness and zeal for coherence from scholars, advocates and practitioners alike.

{kind=link}