Investor Intention in Equity Crowdfunding. Does Trust Matter?

Abstract

1. Introduction

2. Conceptual Framework and Hypothesis

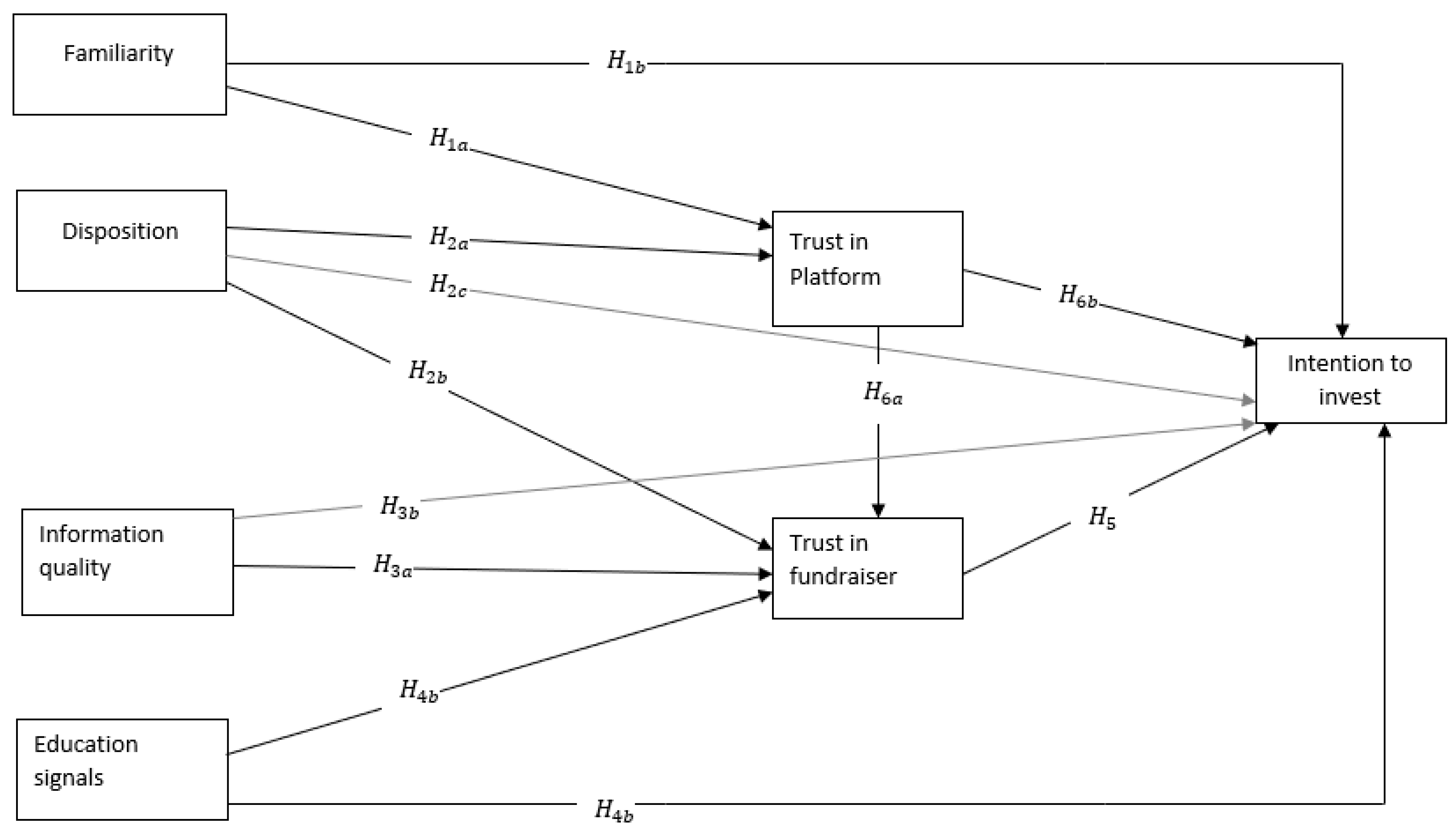

2.1. Conceptual Framework

2.2. Hypothesis

2.2.1. Familiarity

2.2.2. Disposition to Trust

2.2.3. Project Quality

2.2.4. Education Signal

2.2.5. Fundraisers Trust

2.2.6. Platform Trust

3. Methodology

3.1. Context of the Research

3.2. Sample

3.3. Measurement

4. Results

4.1. Model Measurement

4.1.1. Common Method Bias (CMB)

4.1.2. KMO and Bartlett’s Test

4.1.3. Reliability, Validity Analysis and Model Fit

4.1.4. Confirmatory Factor Analysis (CFA)

4.1.5. Discriminant Validity

4.2. Structural Equation Model

5. Discussion and Implications

6. Conclusions, Limitations and Future Study

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Abosag, Ibrahim, and Peter Naudé. 2014. Development of Special Forms of B2B Relationships: Examining the Role of Interpersonal Liking in Developing Guanxi and Et-Moone Relationships. Industrial Marketing Management 43: 887–96. [Google Scholar] [CrossRef]

- Ahlers, Gerrit K. C., Douglas Cumming, Christina Günther, and Denis Schweizer. 2015. Signaling in Equity Crowdfunding. Entrepreneurship Theory and Practice 39: 955–80. [Google Scholar] [CrossRef]

- Alegre, Inés, and Melina Moleskis. 2016. Crowdfunding: A Review and Research Agenda. Available online: https://ssrn.com/abstract=2900921 (accessed on 7 October 2016).

- Backes-Gellner, Uschi, and Arndt Werner. 2007. Entrepreneurial Signaling via Education: A Success Factor in Innovative Start-Ups. Small Business Economics 29: 173–90. [Google Scholar] [CrossRef]

- Bansal, Gaurav, Fatemeh Mariam Zahedi, and David Gefen. 2016. Do Context and Personality Matter? Trust and Privacy Concerns in Disclosing Private Information Online. Information & Management 53: 1–21. [Google Scholar]

- Barbi, Massimiliano, and Sara Mattioli. 2019. Human Capital, Investor Trust, and Equity Crowdfunding. Research in International Business and Finance 49: 1–12. [Google Scholar] [CrossRef]

- Bélanger, France, and Lemuria Carter. 2008. Trust and Risk in E-Government Adoption. The Journal of Strategic Information Systems 17: 165–76. [Google Scholar] [CrossRef]

- Bell, Emma, and Alan Bryman. 2007. The Ethics of Management Research: An Exploratory Content Analysis. British Journal of Management 18: 63–77. [Google Scholar] [CrossRef]

- Belleflamme, Paul, Thomas Lambert, and Armin Schwienbacher. 2014. Crowdfunding: Tapping the Right Crowd. Journal of Business Venturing 29: 585–609. [Google Scholar] [CrossRef]

- Bi, Sheng, Zhiying Liu, and Khalid Usman. 2017. The Influence of Online Information on Investing Decisions of Reward-Based Crowdfunding. Journal of Business Research 71: 10–18. [Google Scholar] [CrossRef]

- Bottazzi, Laura, Marco Da Rin, and Thomas Hellmann. 2016. The Importance of Trust for Investment: Evidence from Venture Capital. The Review of Financial Studies 29: 2283–318. [Google Scholar] [CrossRef]

- Bouncken, Ricarda B., Malvine Komorek, and Sascha Kraus. 2015. Crowdfunding: The Current State of Research. International Business & Economics Research Journal (IBER) 14: 407–16. [Google Scholar]

- Brown, Houghton G., Marshall Scott Poole, and Thomas L. Rodgers. 2004. Interpersonal Traits, Complementarity, and Trust in Virtual Collaboration. Journal of Management Information Systems 20: 115–38. [Google Scholar] [CrossRef]

- Cabrera, Elizabeth F., and Angel Cabrera. 2005. Fostering Knowledge Sharing through People Management Practices. The International Journal of Human Resource Management 16: 720–35. [Google Scholar] [CrossRef]

- Chen, Dongyu, Fujun Lai, and Zhangxi Lin. 2014. A Trust Model for Online Peer-to-Peer Lending: A Lender’s Perspective. Information Technology and Management 15: 239–54. [Google Scholar] [CrossRef]

- Chen, Yuangao, Ruyi Dai, Jianrong Yao, and Yixiao Li. 2019. Donate Time or Money? The Determinants of Donation Intention in Online Crowdfunding. Sustainability 11: 4269. [Google Scholar] [CrossRef]

- Connelly, Brian L., T. Russell Crook, James G. Combs, David J. Ketchen, Jr., and Herman Aguinis. 2018. Competence-and Integrity-Based Trust in Interorganizational Relationships: Which Matters More? Journal of Management 44: 919–45. [Google Scholar] [CrossRef]

- Cooper, Arnold C., F. Javier Gimeno-Gascon, and Carolyn Y. Woo. 1994. Initial Human and Financial Capital as Predictors of New Venture Performance. Journal of Business Venturing 9: 371–95. [Google Scholar] [CrossRef]

- Crowdfunding—Saudi Arabia|Statista Market Forecast. n.d. Statista. Available online: https://www.statista.com/outlook/335/110/crowdfunding/saudi-arabia (accessed on 21 September 2020).

- Cumming, Douglas J., Lars Hornuf, Moein Karami, and Denis Schweizer. 2020. Disentangling Crowdfunding from Fraudfunding. Max Planck Institute for Innovation & Competition Research Paper No. 16-09. Available online: https://ssrn.com/abstract=2828919 (accessed on 4 January 2020).

- Diamantopoulos, Adamantios, and Judy A. Siguaw. 2006. Formative versus Reflective Indicators in Organizational Measure Development: A Comparison and Empirical Illustration. British Journal of Management 17: 263–82. [Google Scholar] [CrossRef]

- Dodds, William B., Kent B. Monroe, and Dhruv Grewal. 1991. Effects of Price, Brand, and Store Information on Buyers’ Product Evaluations. Journal of Marketing Research 28: 307–19. [Google Scholar]

- Erikson, Erik H. 1968. Identity: Youth and Crisis. New York: WW Norton & Company. [Google Scholar]

- Fukuyama, Francis. 1995. Trust: The Social Virtues and the Creation of Prosperity. New York: Free Press, vol. 99. [Google Scholar]

- Gazzaz, Heba. 2019. Crowdfunding in Saudi Arabia: A Case Study of the Manafa Platform. International Journal of Economics and Finance 11: 1–72. [Google Scholar] [CrossRef]

- Gefen, David. 2000. E-Commerce: The Role of Familiarity and Trust. Omega 28: 725–37. [Google Scholar] [CrossRef]

- Gefen, David, Elena Karahanna, and Detmar W. Straub. 2003. Trust and TAM in Online Shopping: An Integrated Model. MIS Quarterly 27: 51–90. [Google Scholar] [CrossRef]

- Grabner-Kräuter, Sonja, and Ewald A. Kaluscha. 2003. Empirical Research in On-Line Trust: A Review and Critical Assessment. International Journal of Human-Computer Studies 58: 783–812. [Google Scholar] [CrossRef]

- Grossman, Michael. 2006. Education and Nonmarket Outcomes. In Handbook of the Economics of Education. Amsterdam: Elsevier, vol. 1, pp. 577–633. [Google Scholar]

- Hair, Joseph F., Rolph E. Anderson, Barry J. Babin, and Wiiliam C. Black. 2010. Multivariate Data Analysis: A Global Perspective. Upper Saddle River: Pearson, vol. 7. [Google Scholar]

- Harman, Harry H. 1976. Modern Factor Analysis. Chicago: University of Chicago Press. [Google Scholar]

- Hazleton, Vincent, and William Kennan. 2000. Social Capital: Reconceptualizing the Bottom Line. Corporate Communications: An International Journal 5: 81–87. [Google Scholar] [CrossRef]

- He, Wu, Guandong Xu, Haichao Zheng, Jui-Long Hung, Zihao Qi, and Bo Xu. 2016. The Role of Trust Management in Reward-Based Crowdfunding. Online Information Review 40: 97–118. [Google Scholar]

- Hollas, Judd. 2013. Is Crowdfunding Now a Threat to Traditional Finance? Corporate Finance Review 18: 27. [Google Scholar]

- Hsu, David H. 2007. Experienced Entrepreneurial Founders, Organizational Capital, and Venture Capital Funding. Research Policy 36: 722–41. [Google Scholar] [CrossRef]

- Jarvenpaa, Sirkka L., Kathleen Knoll, and Dorothy E. Leidner. 1998. Is Anybody out There? Antecedents of Trust in Global Virtual Teams. Journal of Management Information Systems 14: 29–64. [Google Scholar] [CrossRef]

- Jöreskog, Karl G. 1993. Testing Structural Equation Models. Sage Focus Editions 154: 294–94. [Google Scholar]

- Kang, Minghui, Yiwen Gao, Tao Wang, and Haichao Zheng. 2016. Understanding the Determinants of Funders’ Investment Intentions on Crowdfunding Platforms. Industrial Management & Data Systems 116: 1800–19. [Google Scholar] [CrossRef]

- Kenning, Peter. 2008. The Influence of General Trust and Specific Trust on Buying Behaviour. International Journal of Retail & Distribution Management 36: 461–76. [Google Scholar] [CrossRef]

- Kim, Dan J., Donald L. Ferrin, and H. Raghav Rao. 2008. A Trust-Based Consumer Decision-Making Model in Electronic Commerce: The Role of Trust, Perceived Risk, and Their Antecedents. Decision Support Systems 44: 544–64. [Google Scholar] [CrossRef]

- Kline, Paul. 2014. An Easy Guide to Factor Analysis. Abingdon-on-Thames: Routledge. [Google Scholar]

- Komiak, Sherrie Y. X., and Izak Benbasat. 2006. The Effects of Personalization and Familiarity on Trust and Adoption of Recommendation Agents. MIS Quarterly 30: 941–60. [Google Scholar] [CrossRef]

- Kshetri, Nir. 2018. Informal Institutions and Internet-Based Equity Crowdfunding. Journal of International Management 24: 33–51. [Google Scholar] [CrossRef]

- Lee, Jung, Jae-Nam Lee, and Bernard CY Tan. 2010. Emotional Trust and Cognitive Distrust: From A Cognitive-Affective Personality System Theory Perspective. Paper presented at the PACIS 2010, Taipei, Taiwan, July 9–12; p. 114. [Google Scholar]

- Lewis, J. David, and Andrew Weigert. 1985. Trust as a Social Reality. Social Forces 63: 967–85. [Google Scholar] [CrossRef]

- Lin, Mingfeng, Nagpurnanand R. Prabhala, and Siva Viswanathan. 2013. Judging Borrowers by the Company They Keep: Friendship Networks and Information Asymmetry in Online Peer-to-Peer Lending. Management Science 59: 17–35. [Google Scholar] [CrossRef]

- Liu, De, Daniel Brass, Yong Lu, and Dongyu Chen. 2015. Friendships in Online Peer-to-Peer Lending: Pipes, Prisms, and Relational Herding. Mis Quarterly 39: 729–42. [Google Scholar] [CrossRef]

- Liu, Lili, Ayoung Suh, and Christian Wagner. 2018. Empathy or perceived credibility? An empirical studyon individual donation behavior in charitable crowdfunding. Internet Research 28: 623–65. [Google Scholar] [CrossRef]

- Luhmann, Niklas. 2018. Trust and Power. Hoboken: John Wiley & Sons. [Google Scholar]

- Massolution, C. L. 2015. Crowdfunding Industry Report. Available online: http://Reports.Crowdsourcing.Org/Index.Php (accessed on 20 January 2020).

- McKnight, D. Harrison, and Norman L. Chervany. 2001. What Trust Means in E-Commerce Customer Relationships: An Interdisciplinary Conceptual Typology. International Journal of Electronic Commerce 6: 35–59. [Google Scholar] [CrossRef]

- McKnight, D. Harrison, Vivek Choudhury, and Charles Kacmar. 2002. Developing and Validating Trust Measures for E-Commerce: An Integrative Typology. Information Systems Research 13: 334–59. [Google Scholar] [CrossRef]

- McKnight, D. Harrison, Larry L. Cummings, and Norman L. Chervany. 1998. Initial Trust Formation in New Organizational Relationships. Academy of Management Review 23: 473–90. [Google Scholar] [CrossRef]

- Meyerson, Debra, Karl E. Weick, and Roderick M. Kramer. 1996. Swift Trust and Temporary Groups. Trust in Organizations: Frontiers of Theory and Research 166: 195. [Google Scholar]

- Mochkabadi, Kazem, and Christine K. Volkmann. 2020. Equity Crowdfunding: A Systematic Review of the Literature. Small Business Economics 54: 75–118. [Google Scholar] [CrossRef]

- Moritz, Alexandra, and Joern H. Block. 2016. Crowdfunding: A Literature Review and Research Directions. In Crowdfunding in Europe. Berlin/Heidelberg: Springer, pp. 25–53. [Google Scholar]

- Moritz, Alexandra, Joern Block, and Eva Lutz. 2015. Investor Communication in Equity-Based Crowdfunding: A Qualitative-Empirical Study. Qualitative Research in Financial Markets 7: 309–42. [Google Scholar] [CrossRef]

- Moysidou, Krystallia, and J. Piet Hausberg. 2019. In Crowdfunding We Trust: A Trust-Building Model in Lending Crowdfunding. Journal of Small Business Management 58: 511–43. [Google Scholar] [CrossRef]

- Nahapiet, Janine, and Sumantra Ghoshal. 1998. Social Capital, Intellectual Capital, and the Organizational Advantage. Academy of Management Review 23: 242–66. [Google Scholar] [CrossRef]

- Parks, Malcolm R., and Kory Floyd. 1996. Making Friends in Cyberspace. Journal of Computer-Mediated Communication 1: JCMC144. [Google Scholar]

- Paschen, Jeannette. 2017. Choose Wisely: Crowdfunding through the Stages of the Startup Life Cycle. Business Horizons 60: 179–88. [Google Scholar] [CrossRef]

- Pavlou, Paul A. 2003. Consumer Acceptance of Electronic Commerce: Integrating Trust and Risk with the Technology Acceptance Model. International Journal of Electronic Commerce 7: 101–34. [Google Scholar]

- Pavlou, Paul A., and David Gefen. 2004. Building Effective Online Marketplaces with Institution-Based Trust. Information Systems Research 15: 37–59. [Google Scholar] [CrossRef]

- Podsakoff, Philip M., Scott B. MacKenzie, Jeong-Yeon Lee, and Nathan P. Podsakoff. 2003. Common Method Biases in Behavioral Research: A Critical Review of the Literature and Recommended Remedies. Journal of Applied Psychology 88: 879. [Google Scholar] [CrossRef] [PubMed]

- Resources—Fintech Saudi. n.d. Available online: https://fintechsaudi.com/resources/ (accessed on 21 September 2020).

- Robert, Lionel P., Alan R. Denis, and Yu-Ting Caisy Hung. 2009. Individual Swift Trust and Knowledge-Based Trust in Face-to-Face and Virtual Team Members. Journal of Management Information Systems 26: 241–79. [Google Scholar] [CrossRef]

- Rotter, Julian B. 1967. A New Scale for the Measurement of Interpersonal Trust 1. Journal of Personality 35: 651–65. [Google Scholar] [CrossRef] [PubMed]

- Rotter, Julian B. 1980. Interpersonal Trust, Trustworthiness, and Gullibility. American Psychologist 35: 1. [Google Scholar] [CrossRef]

- Spence, Michael. 1978. Job Market Signaling. In Uncertainty in Economics. Amsterdam: Elsevier, pp. 281–306. [Google Scholar]

- Spicer, John. 2005. Making Sense of Multivariate Data Analysis: An Intuitive Approach. Thousand Oaks, London and New Delhi: Sage. [Google Scholar]

- Stewart, Katherine J. 2003. Trust Transfer on the World Wide Web. Organization Science 14: 5–17. [Google Scholar] [CrossRef]

- Strohmaier, David, Jianqiu Zeng, and Muhammad Hafeez. 2019. Trust, Distrust, and Crowdfunding: A Study on Perceptions of Institutional Mechanisms. Telematics and Informatics 43: 101252. [Google Scholar] [CrossRef]

- Sun, Heshan. 2010. Sellers’ Trust and Continued Use of Online Marketplaces. Journal of the Association for Information Systems 11: 2. [Google Scholar] [CrossRef]

- Teo, Thompson S. H., and Jing Liu. 2007. Consumer Trust in E-Commerce in the United States, Singapore and China. Omega 35: 22–38. [Google Scholar] [CrossRef]

- Tomczak, Alan, and Alexander Brem. 2013. A Conceptualized Investment Model of Crowdfunding. Venture Capital 15: 335–59. [Google Scholar] [CrossRef]

- Ullah, Saif, and Yulin Zhou. 2020. Gender, Anonymity and Team: What Determines Crowdfunding Success on Kickstarter. Journal of Risk and Financial Management 13: 80. [Google Scholar] [CrossRef]

- Uslaner, Eric M. 2008. Where You Stand Depends upon Where Your Grandparents Sat: The Inheritability of Generalized Trust. Public Opinion Quarterly 72: 725–40. [Google Scholar] [CrossRef]

- Van der Have, Robert P., and Luis Rubalcaba. 2016. Social Innovation Research: An Emerging Area of Innovation Studies? Research Policy 45: 1923–35. [Google Scholar] [CrossRef]

- Walthoff-Borm, Xavier, Armin Schwienbacher, and Tom Vanacker. 2018. Equity Crowdfunding: First Resort or Last Resort? Journal of Business Venturing 33: 513–33. [Google Scholar] [CrossRef]

- Wang, Nan, Xiao-Liang Shen, and Yongqiang Sun. 2013. Transition of Electronic Word-of-Mouth Services from Web to Mobile Context: A Trust Transfer Perspective. Decision Support Systems 54: 1394–403. [Google Scholar] [CrossRef]

- Wang, Wei-Tsong, Yi-Shun Wang, and En-Ru Liu. 2016. The Stickiness Intention of Group-Buying Websites: The Integration of the Commitment–Trust Theory and e-Commerce Success Model. Information & Management 53: 625–42. [Google Scholar]

- Wiersema, Margarethe F., and Karen A. Bantel. 1992. Top Management Team Demography and Corporate Strategic Change. Academy of Management Journal 35: 91–121. [Google Scholar]

- Xu, Jingjun, Izak Benbasat, and Ronald T. Cenfetelli. 2013. Integrating Service Quality with System and Information Quality: An Empirical Test in the e-Service Context. MIS Quarterly 37: 777–94. [Google Scholar] [CrossRef]

- Zheng, Haichao, Dahui Li, Jing Wu, and Yun Xu. 2014. The Role of Multidimensional Social Capital in Crowdfunding: A Comparative Study in China and US. Information & Management 51: 488–96. [Google Scholar]

| 1 | Reward-based, seed, or pre-ordering crowdfunding is when the crowd fund’s entrepreneurs or artists give products or services in return for funding, such as membership in a fan rewards club or a ticket for an event (Moritz and Block 2016). Nevertheless, social capital has a significant impact on the success of reward-based crowdfunding campaigns. |

| 2 | The peer-to-peer or lending crowdfunding platform works like a bank by giving loans to borrowers, but at interest rates lower than banks. The platform links lenders or investors with borrowers. Some platforms link the lenders directly to individual borrowers, while other platforms connect the individual to small businesses indirectly by collecting the funds from individuals on the businesses’ behalf (Massolution 2015). |

| 3 | Donation crowdfunding is the donation of funds to non-profit projects. The funders of donation crowdfunding donate through the platform for no tangible return (Moritz and Block 2016). |

{kind=link}

{kind=link}

| Variable | Frequency | Percent [%] |

|---|---|---|

| Age | ||

| 18 to 24 | 3 | 1.4% |

| 25 to 34 | 84 | 38.9% |

| 35 to 44 | 104 | 48.1% |

| 45 to 54 | 19 | 8.8% |

| 55 and older | 6 | 2.8% |

| Gender | ||

| Male | 171 | 79.2% |

| Female | 45 | 20.8% |

| Occupation | ||

| Student | 40 | 18.5% |

| Employed | 148 | 68.5% |

| Retired | 15 | 6.9% |

| Unemployment | 10 | 4.6% |

| Other | 3 | 1.4% |

| Education | ||

| High school or equivalent | 26 | 12% |

| Bachelor’s degree | 102 | 47.2% |

| Master’s degree | 83 | 38.4% |

| Doctoral degree | 5 | 2.3% |

| Marital status | ||

| Married | 134 | 62% |

| Single | 75 | 34.7% |

| Widowed | 0 | 0% |

| Divorced | 7 | 3.2% |

| Code | Item | Source |

|---|---|---|

| FAM1 | I am generally familiar with crowdfunding. | |

| FAM2 | I am familiar with conducting online investments in crowdfunding projects. | (Gefen 2000) |

| FAM3 | The process of supporting crowdfunding projects is known to me. | |

| DIS1 | In general, I trust other people. | |

| DIS2 | I tend to count on other people. | (Gefen 2000) |

| DIS3 | In general, I trust other people unless they give me a reason not to trust them. | |

| PROJQ1 | I am satisfied with the information on this project page. | |

| PROJQ2 | Overall, I would give the content quality of the project a high mark. | (Kim et al. 2008; Xu et al. 2013) |

| PROJQ3 | Overall, I would give a high rating in terms of the content quality for the crowdfunding project. | |

| EDU1 | A fundraiser’s education is important to me. | Now developed |

| EDU2 | A fundraiser’s heavy investment in education gives me a signal that the project will succeed in equity crowdfunding. | |

| EDU3 | A fundraiser who has spent heavily on higher education is important to me. | |

| PTRUST1 | I believe that the platform is trustworthy. | |

| PTRUST2 | I believe (the platform) keeps its promises. | (McKnight et al. 2002) |

| PTRUST3 | (The platform) can be trusted at all times. | |

| FTRUST1 | I am convinced that the project creator(s) will fulfil his/her/their obligations. | |

| FTRUST2 | I would call the project creator(s) honest. | (McKnight et al. 2002) |

| FTRUST3 | I believe that the project creator(s) has the competence and efficiency to successfully achieve the goals and keep all promises made to me. | |

| IN1 | The probability that I would fund the crowdfunding project is high. | |

| IN2 | My willingness to invest in the crowdfunding project is high. | (Dodds et al. 1991) |

| IN3 | I intend to contribute financially to crowdfunding campaigns. |

| Items | Factor Loading | Composite Reliability | AVE | α |

|---|---|---|---|---|

| Familiarity | 0.893 | 0.736 | 0.888 | |

| FAM1 | 0.870 | |||

| FAM2 | 0.929 | |||

| FAM3 | 0.767 | |||

| Disposition to trust | 0.822 | 0.608 | 0.822 | |

| DIS1 | 0.789 | |||

| DIS2 | 0.854 | |||

| DIS3 | 0.688 | |||

| Education | 0.767 | 0.525 | 0.765 | |

| EDU1 | 0.765 | |||

| EDU2 | 0.759 | |||

| EDU3 | 0.643 | |||

| Project quality | 0.823 | 0.607 | 0.820 | |

| PROJQ1 | 0.751 | |||

| PROJQ2 | 0.796 | |||

| PROJQ3 | 0.790 | |||

| Platform trust | 0.764 | 0.522 | 0.757 | |

| PTRUST2 | 0.666 | |||

| PTRUST3 | 0.828 | |||

| PTRUST4 | 0.660 | |||

| Fundraise trust | 0.772 | 0.540 | 0.713 | |

| FTRUST1 | 0.906 | |||

| FTRUST2 | 0.552 | |||

| FTRUST3 | 0.703 | |||

| Intention | 0.747 | 0.497 | 0.746 | |

| IN1 | 00.769 | |||

| IN2 | 0.657 | |||

| IN3 | 0.685 |

| Variable | [1] | [2] | [3] | [4] | [5] | [6] | [7] |

|---|---|---|---|---|---|---|---|

| Project quality [1] | 0.779 | ||||||

| Platform trust [2] | 0.501 | 0.722 | |||||

| Familiarity [3] | 0.252 | 0.363 | 0.858 | ||||

| Fundraiser trust [4] | 0.374 | 0.438 | 0.087 | 0.735 | |||

| Disposition to trust [5] | 0.015 | 0.089 | 0.006 | 0.045 | 0.780 | ||

| Intention [6] | 0.469 | 0.462 | 0.302 | 0.358 | −0.059 | 0.705 | |

| Education [7] | 0.251 | 0.078 | −0.042 | 0.122 | −0.052 | 0.066 | 0.725 |

| Hypothesis | Estimate | t-Value | p | Outcome | ||

|---|---|---|---|---|---|---|

| Disposition to trust | ⟶ | Platform trust | 0.084 | 1.626 | 0.104 | Not Supported |

| Disposition to trust | ⟶ | Intention | −0.107 | −2.173 | 0.030 | Supported |

| Disposition to trust | ⟶ | Fundraiser trust | 0.009 | 0.177 | 0.859 | Not Supported |

| Familiarity | ⟶ | Platform trust | 0.292 | 6.694 | <0.001 | Supported |

| Familiarity | ⟶ | Intention | 0.111 | 2.351 | 0.019 | Supported |

| Project quality | ⟶ | Fundraiser trust | 0.162 | 2.885 | 0.004 | Supported |

| Project quality | ⟶ | Intention | 0.325 | 5.734 | <0.001 | Supported |

| Education | ⟶ | Fundraiser trust | 0.067 | 0.866 | 0.386 | Not Supported |

| Education | ⟶ | Intention | −0.079 | −1.072 | 0.284 | Not Supported |

| Platform trust | ⟶ | Fundraiser trust | 0.411 | 6.595 | <0.001 | Supported |

| Platform trust | ⟶ | Intention | 0.286 | 4.113 | <0.001 | Supported |

| Fundraiser trust | ⟶ | Intention | 0.167 | 2.583 | 0.010 | Supported |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Alharbey, M.; Van Hemmen, S. Investor Intention in Equity Crowdfunding. Does Trust Matter? J. Risk Financial Manag. 2021, 14, 53. https://doi.org/10.3390/jrfm14020053

Alharbey M, Van Hemmen S. Investor Intention in Equity Crowdfunding. Does Trust Matter? Journal of Risk and Financial Management. 2021; 14(2):53. https://doi.org/10.3390/jrfm14020053

Chicago/Turabian StyleAlharbey, Mohammed, and Stefan Van Hemmen. 2021. "Investor Intention in Equity Crowdfunding. Does Trust Matter?" Journal of Risk and Financial Management 14, no. 2: 53. https://doi.org/10.3390/jrfm14020053

APA StyleAlharbey, M., & Van Hemmen, S. (2021). Investor Intention in Equity Crowdfunding. Does Trust Matter? Journal of Risk and Financial Management, 14(2), 53. https://doi.org/10.3390/jrfm14020053