Some simple parametric regression results are discussed before the non-parametric results are reported. As we will see, the non-parametric results provide more nuanced details on the results reported in the paper, but are not substantively different from the results arising from the probit regressions. In both cases, the decomposition exercise will find that most of the changes in arrears over time can be attributed to changes in the repayment behaviour of borrowers, rather than changes in either loan applications or loan acceptances.

5.1. Parametric Results

The results from a Probit regression of the effect of a set of household characteristics

for household

i on arrears

are reported for each wave in

Table 3, with similar results across waves. Younger households are more likely to be in arrears than older households (the differences between age-groups is significant in all waves except 2007). Except in the first wave, lower income households are significantly more likely to be in arrears than higher income households. There are also differences in the effect of the other household variables on arrears, but couple, gender, and college education are only significant in one of the waves, and being white is never significant in these regressions.

The supplementary material in the

Appendix A reports the results of a Probit regression for wave of the data for the the effect of household characteristics on application behaviour

A, acceptance behaviour

C and repayment among borrowers

R. In each case, the results are broadly in line with expectations. Younger households, and higher income households, are more likely to apply for credit, and more likely to receive credit. Lower income households are less likely to repay should they receive a loan. Most of the other household characteristics do not have a consistent and clear affect on applications, acceptances, or repayment among borrowers.

The results of these individual regressions, in themselves, are of only minor interest. More interesting is to understand how these regression results are changing over time, and how this affects the pattern of arrears in the population over time: understanding this issue is a key aim of this paper.

Table 4 reports how overall arrears are changing over time, and the decomposition exercise based on Equation (

3) above. The top row of

Table 4 reports the predicted level of arrears that arise from the regression results (the weighted average of each households probability of non-payment

D for each of the waves). It shows that the regression analysis predicts that 6.6 percent of households are in arrears in 1995; this falls to 6 percent in 2001; rises to 8.2 percent in 2004; falls in 2007 (the eve of the financial crisis); and rises again to a peak in 2010. Unsurprisingly, this pattern mirrors the actual arrears in the population reported earlier.

The second column constructs an estimate of the predicted level of arrears in the population using the probit regression coefficients of the current wave

, but the characteristics of the households in the next wave

.

4 Using the 1995 Probit estimates, but the 2001 household characteristics, the predicted level of arrears is 6.27 percent. The 1995 characteristics (the cell above), had predicted a level of arrears of 6.59 percent. This suggests that slightly over half of the difference between predicted arrears in 1995 and predicted arrears in 2001 can be explained by changes in the characteristics of the households between these two waves of the data. What happens when we repeat this analysis for the change in predicted arrears between 2001 and 2004. The table shows that predicted arrears rose 6.04 to 8.22 percent. However, replacing the 2001 household characteristics with the 2004 characteristics only increased arrears to 6.08, a negligible increase. Predicted arrears fall to 6.17 percent in 2007, but the change in characteristics only reduce it to 7.94; again, a very small effect. In the last wave, the regression model predicts arrears at 8.85 percent, but the change in characteristics between 2007 and 2010 only increases arrears to 6.46 percent. The overall story seems to be that changes in household characteristics are only a small part of the explanation of the change in the level of arrears between the different waves of the data.

The bottom three rows of

Table 4 show the effect on arrears of first changing the application behaviour of households

A, then changing the acceptance of lenders

C and finally changing the repayment behaviour of borrowers

R. The first column and row three construct the predicted level of arrears using the 1995 household characteristics, the 2001 regression for applications

A, and the 1995 regression for acceptance

C and repayment

R. This means, compared to the top column, the only change is that we are using the estimated application behaviour from 2001 in place of the 1995 application behaviour. This change in application behaviour means that predicted arrears rise from 6.59 percent to 7.00 percent. Arrears fell between these two waves, but the change in application behaviour, by itself, increased arrears. The fourth row shows the effect of using the 2001 regression equation for applications

A and acceptances

C, which increases arrears to 7.74 percent (again the effect is in the opposite direction to the overall fall in arrears between 1995 and 2001). The last row shows the effect of using the 2001 model for arrears

A, acceptances

C and repayment among borrowers

R, but using the 1995 household characteristics. Predicted arrears fall to 6.41 percent, suggesting a substantial proportion of the change in the overall arrears between 1995 and 2001 can be explained by the change in repayment behaviour of borrowers. The change in arrears between the bottom row of column 1 and the top row of column 2 shows the effect of changing characteristics: arrears fall to 6.04 percent. This suggests there is an important effect from changing characteristics, but this effect is smaller than the change in repayment behaviour.

This type of analysis can be repeated for the changes between the other waves included in the analysis. Between 2001 and 2004, the change in applications slightly increased arrears, and the change in acceptances slightly reduced arrears. However, these effects are small: the largest effect is from the change in repayment behaviour which increases arrears from 6.04 percent to 8.44 percent. Between 2004 and 2007, applications and arrears very slightly increase arrears; but the change in repayment behaviour among borrowers dramatically reduces arrears from 8.51 percent to 6.21 percent. Finally, between 2007 and 2010, the change in application behaviour and acceptance behaviour slightly reduced arrears, from 6.17 percent to 5.98 percent. The change in acceptance behaviour between these two waves then raises arrears to 8.64 percent.

The overall story that clearly arises from the decomposition exercise reported in

Table 4 is that the change in default between different waves of the data is that application and acceptance behaviour seem to play little role in explaining the change in arrears (and the sign of their effect on arrears is of the ‘wrong’ sign). There is a moderate effect from changes in characteristics between 1995 and 2001, and again between 2007 and 2010, but the effect is rather small, and cannot explain much of the change in default behaviour. Overwhelmingly, the change in arrears between waves is the result of the substantial swings in the default behaviour of borrowing households.

The change in arrears can differ substantially with household characteristics, and this is investigated in

Table 5, although the effect of only some household characteristics are reported.

5 It shows that between 1995 and 2001, the oldest age group included in the table had a significant increase in their level of arrears (the changes reported in the table are starred when they are significant at the 5 percent level). However, the other changes between 1995 and 2001 are never statistically significant. Between 2001 and 2004, households between 35 and 44 increase their level of arrears by over 5 percent, and there is a significant increase in arrears for couples and for poorly educated households. Arrears fell between 2004 and 2007 for younger households, and for poorly educated households. The increase in arrears between 2007 and 2010 was significant for middle-aged households and for almost all income groups (although the increase was larger for lower income households). A more thorough investigation of the differences between demographic groups will be undertaken, with some fully non-parametric regressions.

5.2. Non-Parametric Estimates of Arrears

The non-parametric regression results for each of the individual waves are reported in detail in the supporting material in

Appendix B, and are only summarised here since the main focus of the paper is the decomposition exercise. Each regression includes age and income, and some households characteristics as explanatory variables, with separate regressions estimated for each wave of the SCF. The main section of the paper will plot the results using figures; they are discussed further in the appendix. The figures do not plot confidence intervals, since it would make the figures too cluttered to be easily read. The analysis here will also concentrate on the age and income variables although other household characteristics are included in the kernel regressions. The non-parametric results will confirm that most of the changes in arrears over time can be attributed to changes in the repayment behaviour of borrowers rather than changes in either loan applications or loan acceptances.

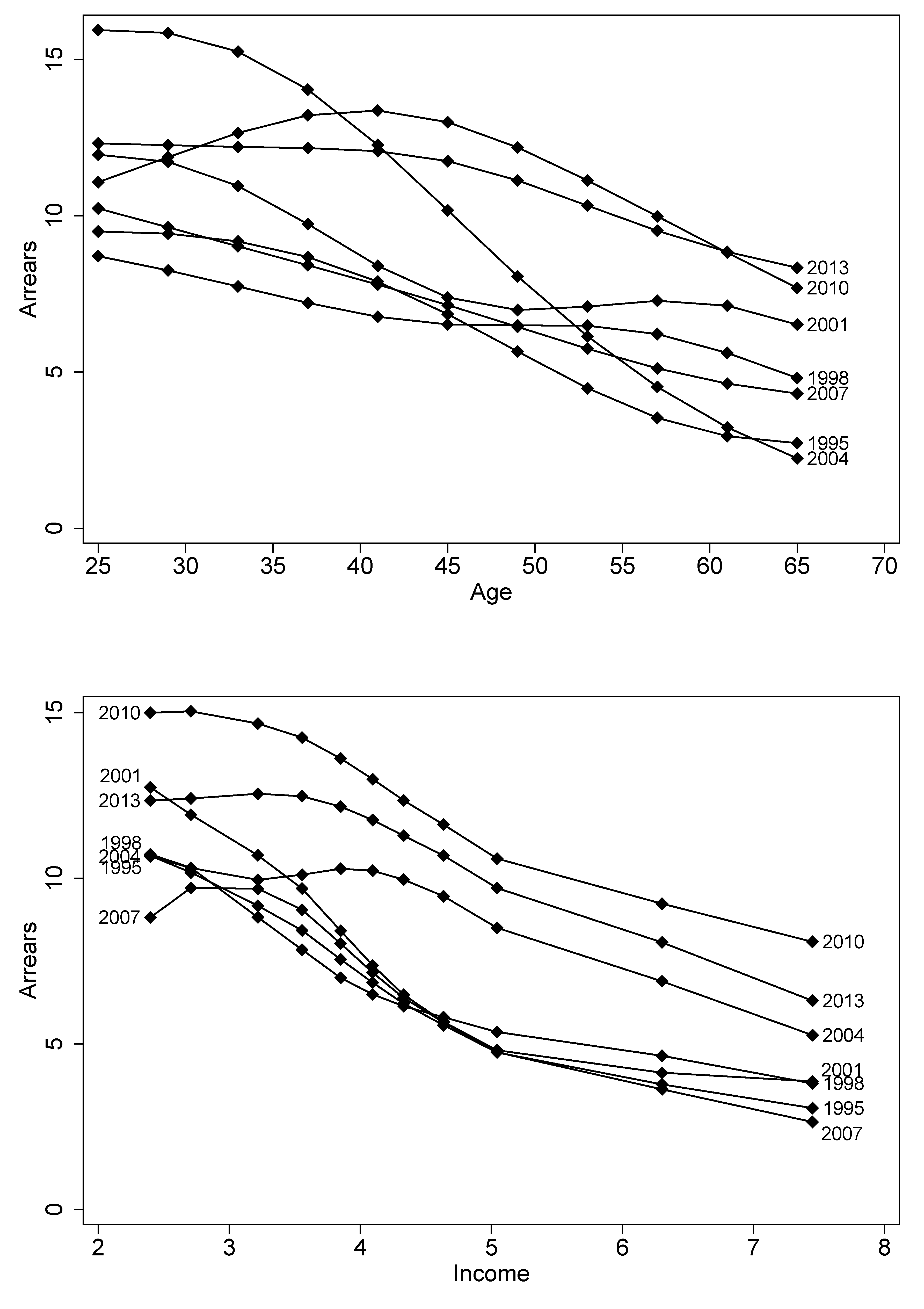

Figure 2 plots the regression results for the level of arrears among

all households for each wave of the data from 1995 to 2013 (

Appendix B contains more details). The top panel shows how the age profile of arrears has changed for each wave of the survey (holding the other variables at their median value). Arrears are two-to-three times higher at younger ages than at older ages; and the difference between age groups is statistically significant in every wave. Middle-aged households have intermediate rates of arrears.

More interestingly for this paper, arrears for each age-group change from year to year. By 2001 (the year of the dot-com crisis), the arrears rate is significantly higher than in 1995 for households aged 53 and above: at age 65, the rate of arrears increased from 2.72% of households to 6.52% of households. In 2004, the youngest households under 45 are significantly more likely to report arrears compared to 1998 or 1995. However, older households are not now more likely to enter arrears than in these earlier years (repayment rates are significantly higher among households age 57 and over in 2004 than in 2001).

6 Recall that households were surveyed in 2007 before the sub-prime crisis had started, but after the Bankruptcy Reform Act of 2005 had tried to make bankruptcy more difficult for those with above median levels of income.

7 The rates of arrears among younger households recovered in 2007 (their arrears was significantly lower than in 2004), but arrears for older households are not significantly different to earlier years. The contrast between the 2010 and 2007 wave reflects the effect of the subprime crisis. The figure shows arrears increased significantly at all age-groups over the age of 35, and these rates of arrears remained high in 2013. The preliminary conclusion from this analysis is that arrears increased among middle-aged and older households both in the dot-com recession and in the subprime crisis, and that arrears among younger households had been especially high just prior to the Bankruptcy Reform Act of 2005.

The effect of income on arrears at age 45 is reported in the bottom panel of

Figure 2. The figure plots arrears for each decile of the income distribution (and at the 5th and 95th centile). In 1995, over 10% of households at the 5th centile of income (the bottom of the income range) are in arrears, but only 3% of households at the 95th centile are in arrears. The results in 1998 and 2001 show similar differences by income (these differences are statistically significant). In 2004, there has been a sharp, statistically significant increase in arrears, especially among middle-income and higher income households. The fact that the increase in arrears was among these income groups explains the focus that the Bankruptcy Reform Act of 2005 placed on making it more difficult for richer households to escape their debts. Indeed, in 2007, there was a statistically significant fall in rates of arrears among middle and higher income households: rates of arrears had returned to those observed in earlier years, suggesting that the Act had succeeded in its objectives. Arrears increased following the onset of the subprime crisis in 2010: low, middle, and high income households all increased arrears by around 6%. In 2013, there was a small but statistically insignificant recovery in rates of arrears at all income groups.

A key advantage of using a non-parametric estimator is that the estimation can allow for the effect of income to be different for younger households compared to older households. These results are discussed in more detail in the supporting evidence. For households at age 30, over 13% of households at the 10th centile of income are in arrears in 1995, while only around 4.4% of households in the 90th centile are in arrears. In contrast, for 60-year-old households, 5.2% households at the 10th centile of income are in arrears, while being only 1.6% of the 90th centile rate of arrears. These differences are statistically significant. These arrears changed over time. By 2001, there was a sharp deterioration in repayment rates for lower income households, with poor older households more likely to be in arrears than poor younger households: at the 10th income decile, the rate of arrears is around 15.1% for 60-year-olds, but only 11.9% at age 30. In 2004, with the recovery of the economy after the dot-com recession, the rate of arrears of low-income older households recovered to pre-recession levels, and, surprisingly, differences across income levels for these older households are no longer statistically significant. In contrast, younger household arrears increased at all income levels (these differences are statistically significant for middle-income households). Rates of arrears for the youngest households fell in 2007: from 14.7% to 10.4% for households at the 10th income centile; from 15.7% to 9.6% for middle-income households; and from 9.6% to 5.2% at the 90th centile. Older households, however, have not significantly changed their level of arrears. Overall, young and middle-aged households of middling income increased their rate of arrears in 2004, and that the Bankruptcy Reform Act of 2005 was successful in reversing this increase in arrears in 2007. Following the sub-prime crisis, for younger households, arrears increased for all income groups: low-income households increased arrears from 10.3% to 15.2% (although this is not statistically significant); while high income household arrears increased from 5.2% to 9.8%. Arrears also increased for older households: lower income households increased arrears from 5.6% to 11.9%, while higher income households increased arrears from 2.3% to 5.1%. These results are similar to what we found for middle-aged households.

5.3. Application and Acceptance Behaviour

A key aim of the paper is to understand the extent to which the changing pattern of arrears can be attributed to either changes in the application behaviour of households or the lending behaviour of banks.

Section 5.4 below will describe this decomposition, but before proceeding, it is necessary to briefly describe some estimates of the probability of a household applying for a loan and the probability of an applicant household receiving a loan (these results are described in more detail in the additional supporting material in

Appendix C at the end of the paper).

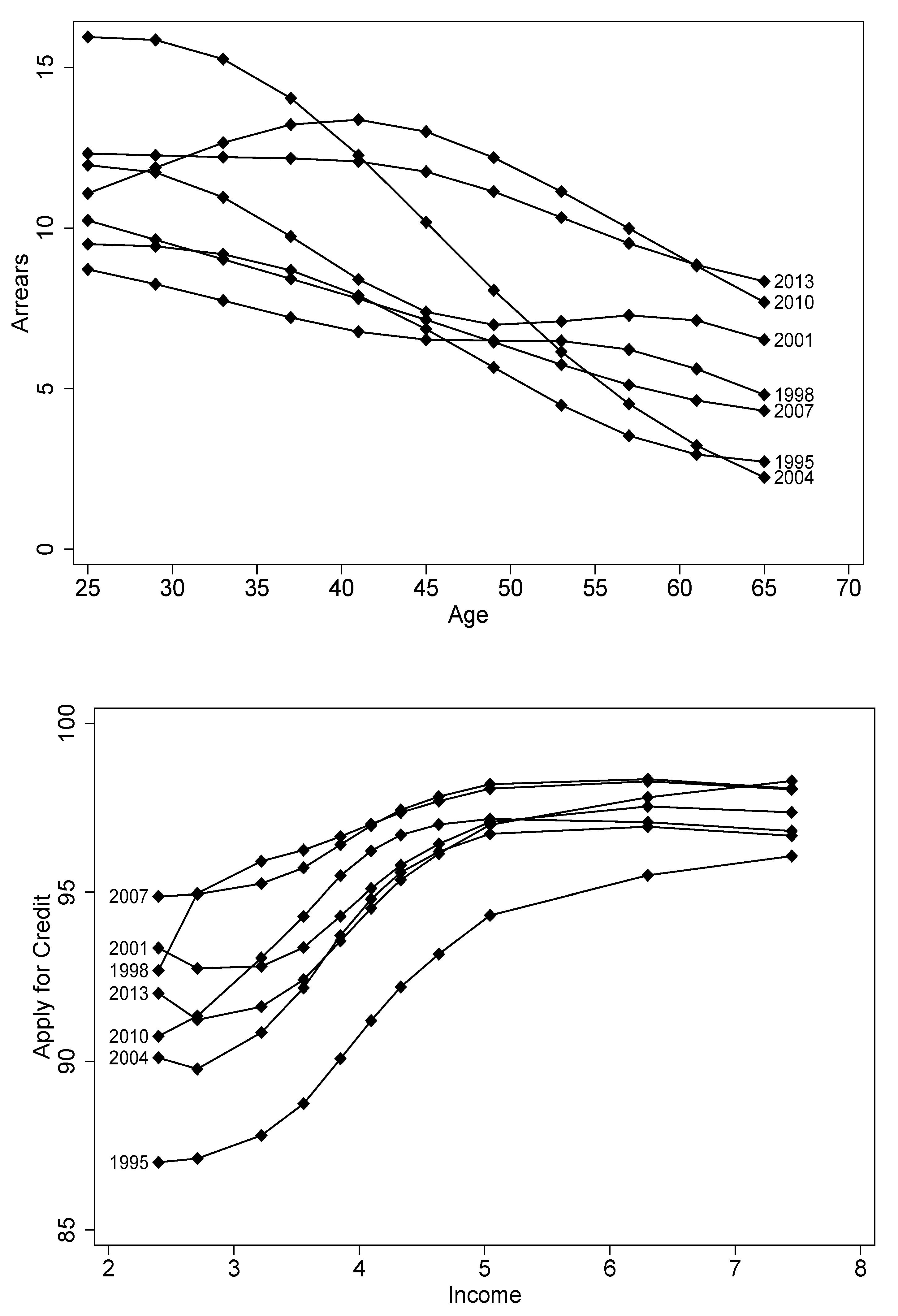

Figure 3 shows how application behaviour has been changing between waves: the top panel shows application behaviour at different ages, while the bottom panel shows different income groups in each wave; in each case, all other variables are held at their median. The top panel shows that, while in each year, the difference across age groups is not large, nevertheless, credit applications have been changing over time. Significantly more households desired credit in 1998 than in 1995 at all age levels (there was a 3 percent increase at younger ages, and a 4 percent increase at older ages). Similarly, in 2007, the demand for credit was significantly higher than in 2004. The demand for credit then fell significantly in 2010 for the oldest households, and had fallen back to 2004 levels for all households by 2013.

The bottom panel of

Figure 3 shows that in each year, low income households are significantly less likely to apply for credit than high income households. Moreover, the proportion of households wanting credit in each income group has been changing over time. More households wanted credit in 1998 and 2001 compared to 1995, and this increase was larger for lower income households. There was a small, but statistically insignificant decline in the desire for credit in 2004, before the desire for credit recovered in 2007: this increase was concentrated in lower income households. Finally, there has been a decline in households reporting that they would like a loan between 2007 and 2013.

Figure 4 describes the rate at which credit applications are accepted by the lender and given the loan. The top panel of the figure shows that in the early years of the sample; younger households are significantly more likely to get the credit they want than older households. Although credit acceptance increased for all households in 1998 and 2001, this increase was larger for these older households. In 2004, credit to older households continued to increase, while there was a sharp decline in credit to the youngest households. This decline reversed in 2007. In 2010 and 2013, households of all ages saw a decline in credit acceptance, but the falls are largest (and only statistically significant) for the youngest households.

The bottom panel of

Figure 4 shows that, in all years, low income households are significantly less likely to get credit they want than high-income households. At the top of the income distribution, there is no statistical difference in credit acceptance over the years, as changes in credit acceptance over time are concentrated in middle- and low-income households. For example, middle-income households are 2.8 percent more likely to get credit in 2001 than in 1995, while households at the 10th income centile are 5.4 percent more likely to get credit in 2001 (although the higher variance of the low-income estimates mean this difference in not statistically significant). Credit acceptance declined in 2004 for all households below the 50th centile, with the declines much larger for the lowest income households, and failed to much recover in 2007. The results in 2010 and 2013 are similar to those in 2004.

5.4. Decomposing the Arrears Behaviour

The raw data suggest that arrears increased among older households in the 2001 and 2010 recessions, but that younger households increased their level of arrears in 2004 and after the crisis in 2008. However, we would like to say something more about the the observed changes in arrears behaviour.

Table 6 shows the results of the decomposition exercise described by Equation (

3) in

Section 4. It reports the change in default for 1995–2001, 2001–2004, 2004–2007 and 2007–2010 in bold, with the results starred when the regression results reported earlier had shown the changes to be statistically significant at the 5 percent level. For age and income, these results correspond to those reported in

Figure 2. Looking at the table, the first result in bold at the top of the left-hand column shows that for 25-year-old households, arrears increased by 2.63 percent; but this is not statistically significant (it is not starred). The next three columns denote how much of the change in default can be attributed to changes in applications (A), to credit acceptance among applicants (C), and to repayment among borrowers (R) using Equation (

1) above. The effect of changes in application behaviour (holding acceptances and arrears among borrowers fixed at their 1995 level) is to increase arrears by 0.26 percent; the effect of credit-acceptance increases arrears by 0.40 percent and repayment among borrowers increases arrears by 1.98 percent between 1995 and 2001. Overall, putting all these effects together results in a increase in arrears behaviour, which, however, is not statistically significant. We can repeat this process for each group and each pair of years in the table to review the cause of the observed changes in arrears behaviour, in order to better understand what has happened during the period of study.

Between 1995 and 2001, the change in arrears was found to be significant for households whose head is age 53 and over (the change in arrears, shown in the bolded column, is marked with an asterisk). At 53, the arrears increased by 2.71 percent. The decomposition exercise shows that the change in application behaviour (shown in column A), increased arrears by 0.17 percent; the change in acceptance behaviour (column C) increased arrears by 0.18 percent; and the change in the repayment behaviour of borrowers (column R) increased arrears by 2.35 percent. This result suggests that over 85 percent of the change in arrears among 53-year-old households is driven by changes in borrower behaviour rather than changes in the composition of the borrower population. A similar conclusion arises for households aged 57, where changes in repayment among borrowers account for 3.45 percent of the 3.75 percent change in arrears; and the results are also similar among 61-year-old households and 65-year-old households where most of the change in arrears again seems to be the consequence of a change in the repayment behaviour of borrowers.

Table 6 shows that between 2001 and 2004, 29-year-old households increased arrears by 3.76 percent, and that this change was earlier found to be statistically significant at the 5 percent level. The decomposition exercise shows that changes in application behaviour reduced arrears by 0.12 percent and that changes in acceptance by lenders reduced arrears by 0.77 percent. The main cause of the increase in arrears for 29-year-old households was that there was an increase in arrears among borrowers (the decomposition exercise shows this would have increased arrears by 4.66 percent). The results for households aged between 33 and 45 had earlier all shown significant increases in arrears (they all starred in the table). In all cases, the decomposition exercise shows that this increase in arrears was despite a reduction in applications (the effect of applications

A is negative in each case) and a reduction in lending to these households (column

C shows the effect of acceptance is also negative). The increase in arrears among these households is driven by a change in the repayment behaviour of borrowers, shown in column

R. While younger households increased arrears, there was a significant reduction in arrears among older households over 60. The decomposition exercise shows that, while the change in applications has the right sign, the effect on arrears is tiny. Changes in acceptance behaviour have the wrong sign: it increases arrears by 0.40 percent among 61-year-old households, and by 0.50 percent among 65-year-old households. The exercise shows that the reduction in arrears for households over 60 is overwhelmingly because of changes in the behaviour of households who receive a loan, as shown in column

R. Low education households also had a significant increase in arrears between 2001 and 2004, and the decomposition attributes this increase to a change in borrower behaviour, rather than to a change in either applications or acceptances.

Between 2004 and 2007, 45-year-old households and younger significantly decreased arrears while for older households there is a statistically insignificant increase in arrears. Again, these changes are almost entirely due to changes in non-payment among borrowers (column R), since there were negligible effects on arrears from changes in the demand for loans (column A) or in credit acceptance (column C). Couples and non-college-educated households also significantly reduced their arrears (column D), and the decomposition exercise shows that the change can be overwhelmingly attributed to changes in arrears among borrowers (column R).

In 2010, there was an increase in arrears among all households except those under 30, with the largest increase among middle-aged households. As before, the increase can be attributed to changes in arrears behaviour among borrowers (the changes in wanting a loan, or being denied credit, by themselves, contribute to a very small reduction in arrears as the sign of the effect is negative in column A and column C). Younger households have a smaller increase in arrears, which would have been much larger if there had not been an increase in credit refusals, shown in column C. However, if demand and credit acceptance had not changed, the increase in arrears would still have been smaller than for middle-aged or older households (see column R). This suggests that the reduction in credit may not have been aimed at those age-groups, which increased arrears the most. Couples and non-college households also had a large increase in arrears between 2007 and 2010 (over 5 percent in each case). In both cases, applications and acceptances had the effect of slightly reducing arrears, but there was a very large change in borrower behaviour, which caused an overall increase in arrears for these groups.

The results so far suggest that behaviour differs for young and old households (other variables held at their median). The second half of the table looks at the income distribution at age 30, age 45 and age 60. It shows that the change in the rate of arrears for young and middle aged households between 1995 and 2001 is never significant. However, for old households, the changes are large, positive, and significant for all households at or below the 70th income centile (these results are starred in the table), and the increase is larger for lower income households. This increase is mostly attributable to changes in the behaviour of borrowers (column R), with much smaller changes attributable to changes in application behaviour (column A) or lending behaviour (column C). For example, at age 60, applications increase arrears by 0.44 percent for households at the 10th income centile, while more generous lending increases their arrears by 0.69 percent. However, the reduction in repayment among borrowers increases their arrears by 8.80 percent, which is a much larger effect.

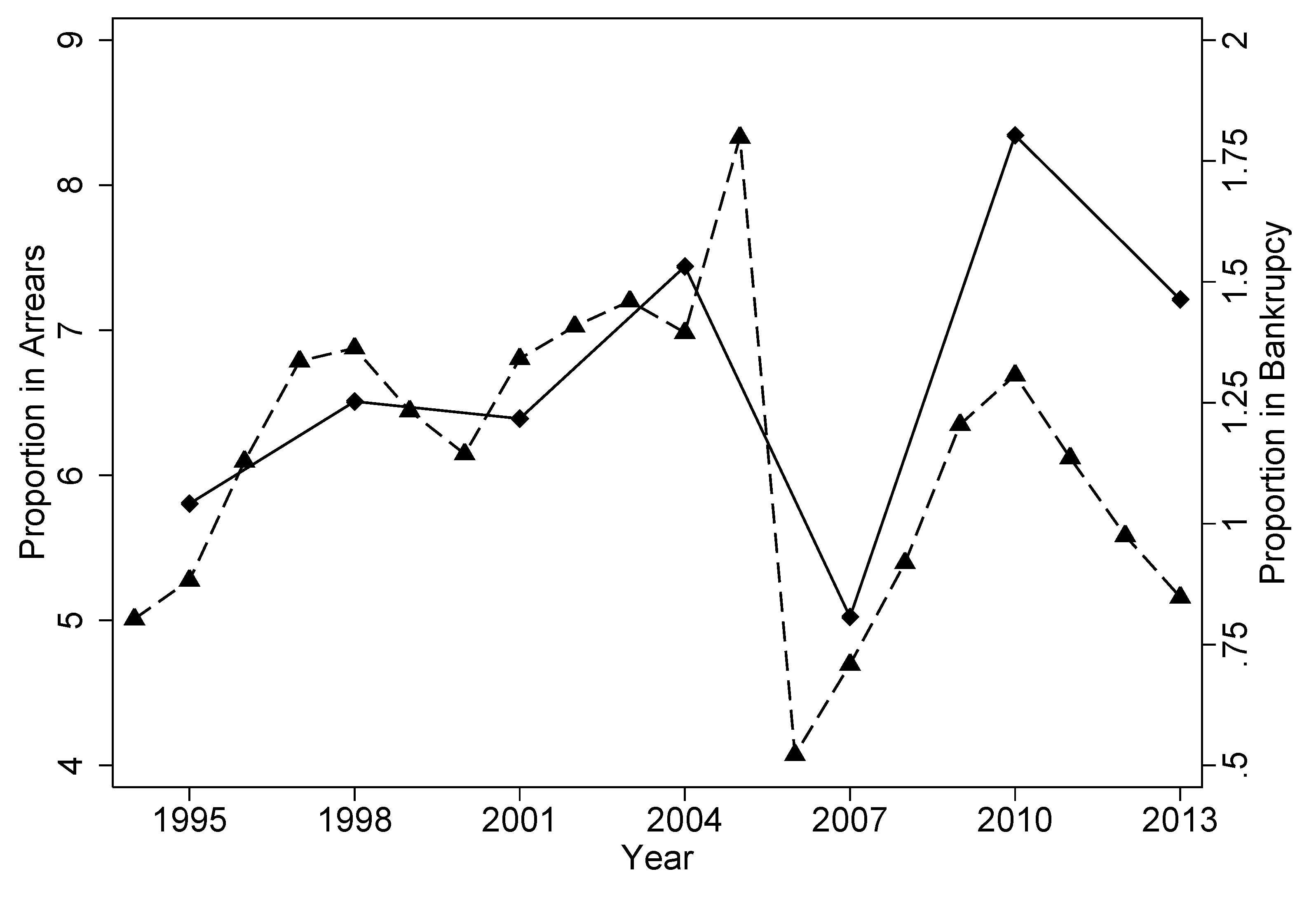

What about the changes between 2001 and 2004, during which the economy recovered from the dotcom crisis? This period is just prior to the bankruptcy reforms enacted in 2005; recall that

Figure 1 shows a sharp spike in bankruptcy filings in 2005. The results shown in

Table 6 show that for 60-year-old households, there was a significant reduction in arrears for households below the 60th income centile. The decomposition exercise shows that this reduction in arrears among older households is almost entirely attributable to a reduction in arrears among borrowers (column

R): changes in applications had a very small effect, while column

C shows that there was a reduction in lending to the lowest income households (which reduced arrears by 2.26 percent for households at the 5th centile), but that lending actually became more generous for households at or above the 20th income centile. It seems that, for older households, the decrease in arrears fully reversed the earlier increase between 1995 and 2001, and moreover, these changes are mostly attributable to changes in the repayment behaviour of borrowers. However, for middle-aged households, there was a statistically significant increase in arrears for households between the 50th and 90th income centiles, while for the youngest households, arrears increased for households between the 50th and 70th income centiles. For these middle-aged and younger households, column

A shows a very small reduction in applications, while column

C shows a small reduction in lending, hence neither can explain the increase in arrears. Rather, column

R shows that the increase in arrears is explained by the worsening repayment behaviour of households receiving a loan.

After the enactment of the bankruptcy reforms in 2005,

Figure 1 shows a sharp reduction in bankruptcy filings in 2006 and 2007. However, our results show that the change in arrears between 2004 and 2007 is never significant for older households (and the point estimates of the change are small). The reduction in arrears was instead concentrated on younger households between the 30th and 90th income centiles, and on middle-aged households between the 50th and 90th income centiles. Perhaps surprisingly, these are mostly the households which had increased arrears between 2001 and 2004. For younger households between 2004 and 2007, the decomposition exercise shows that the reduction in arrears is not due to changes in either application or lending behaviour (column

A shows that applications are increasing arrears, while column

C shows that lenders became more generous in giving loans to younger households). For middle-aged households, an increase in applications again had the effect of slightly increasing arrears, while there was a negligible reduction in arrears resulting from changes in lender behaviour. Column

R shows that the overall change in arrears between 2004 and 2007 can be attributed to changes in the repayment behaviour of borrowers. Given that an aim of the bankruptcy reform of 2005 was to encourage higher income households to repay their debts, it seems that the reforms succeeded in their aim among middle-aged and younger households. Moreover, the reforms had remarkably little effect on lender behaviour.

The rate of arrears shown in

Figure 1 sharply increased in 2010. This increase has often been attributed to lower income households receiving credit hitherto refused, and consequently defaulting on their debts (hence the sub-prime crisis). The regression results reported earlier also show that between 2007 and 2010, there was a significant increase in arrears across all income groups for middle-aged and older households, and for households above the 70th income centile among younger households (this is shown by starring the change in arrears in

Table 6). The size of the change among 60-year-old households was larger for lower income households than higher income households; but there were rather smaller differences across income groups among 45-year-old households. The decomposition exercise shows that applications and acceptances (columns

A and

C) had a negligible effect on arrears (and the sign in both cases is negative). For all income levels, the change in arrears is fully attributable to changes in arrears among borrowers, shown in column

R.

Table 6 shows that the change in arrears between 2007 and 2010 for young lower-income households is not significant. The decomposition exercise shows that if only the behaviour of borrowers changed, then the overall increase in arrears of these households would have been larger than it was (but still smaller than for higher income 30-year-olds), but that a reduction in the granting of credit roughly halved the change in the rate of arrears for households between the 20th and 40th centile. The increase in arrears does not fully support the story about sub-prime lending driving arrears, for two reasons. First, except among the oldest households, the increase in arrears is not larger among lower income households; in fact, for younger households, it is the wealthier households who have increased their rate of arrears. Second, the decomposition exercise suggests that the increase in arrears can not really be attributed to either increases in applications or acceptances.

The results reported in this section suggest, rather surprisingly, that most of the changes in arrears over time are due to dramatic fluctuations in the repayment behaviour of borrowers rather than to changes in the composition of the borrower population. Studying all three major events (the two recessions and the bankruptcy reform) together has enabled us to see that this feature is common to all three events: the change in the repayment of borrowers explains the increase in arrears of poorer older households between 1995 and 2001 and their reduction in arrears between 2001 and 2004; it explains the increase in arrears of middle-income younger and middle-aged households between 2001 and 2004, and their reduction in arrears in 2007; and it largely explains the increase in arrears for all households (except young low-income households) between 2007 and 2010.

{kind=link}

{kind=link}

{kind=link}

{kind=link}