Green Bond: A Systematic Literature Review for Future Research Agendas

Abstract

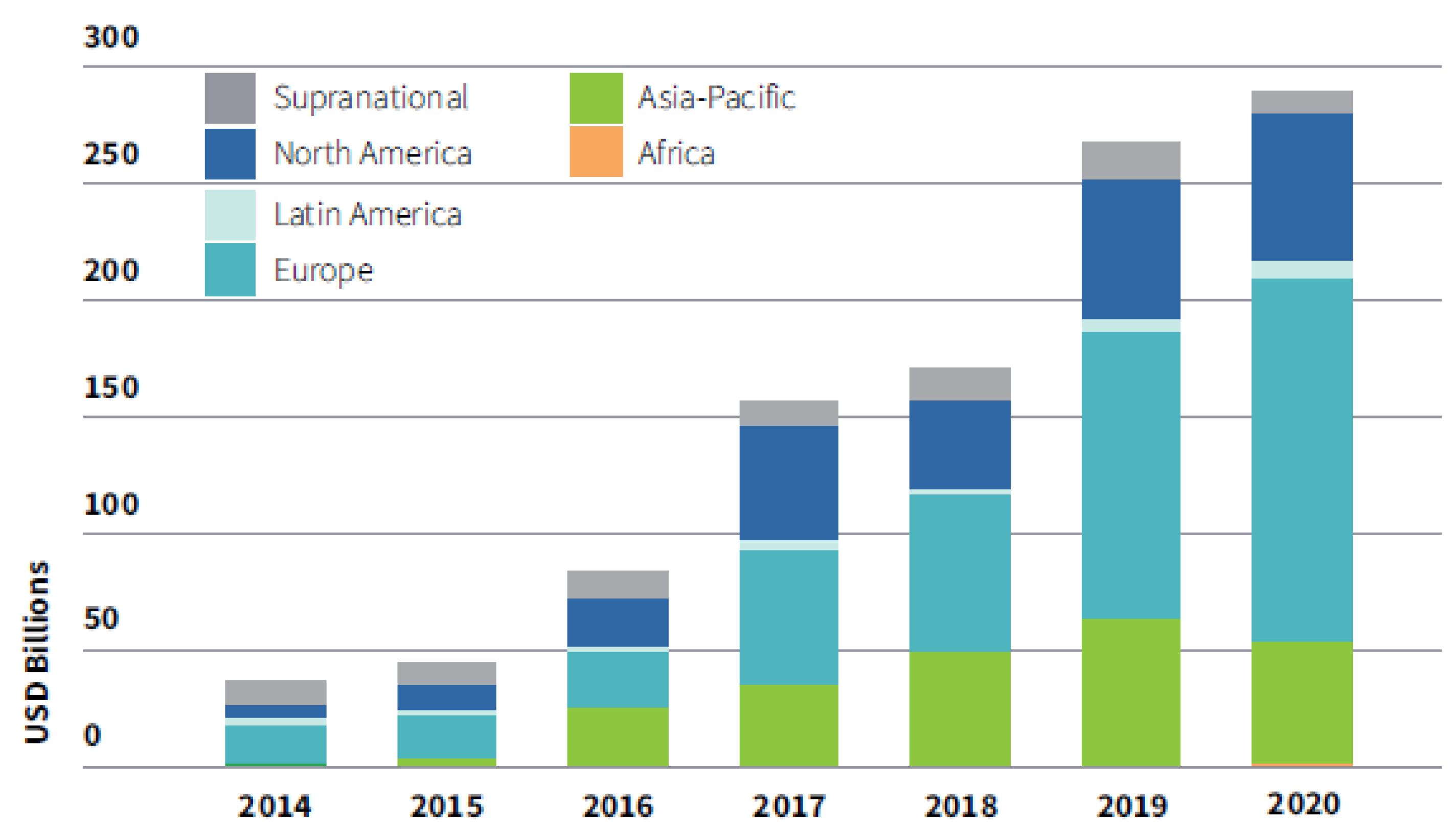

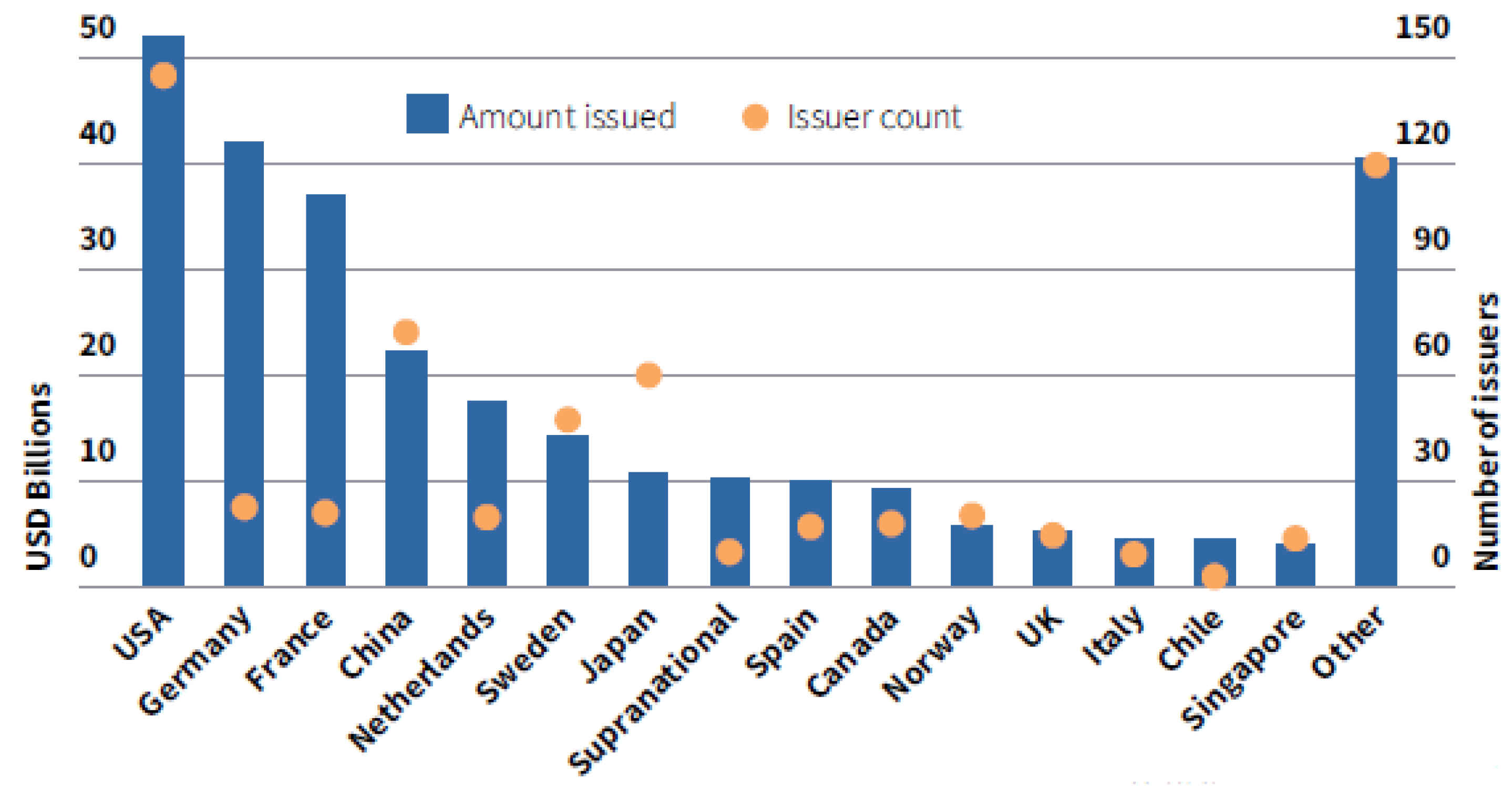

:1. Introduction

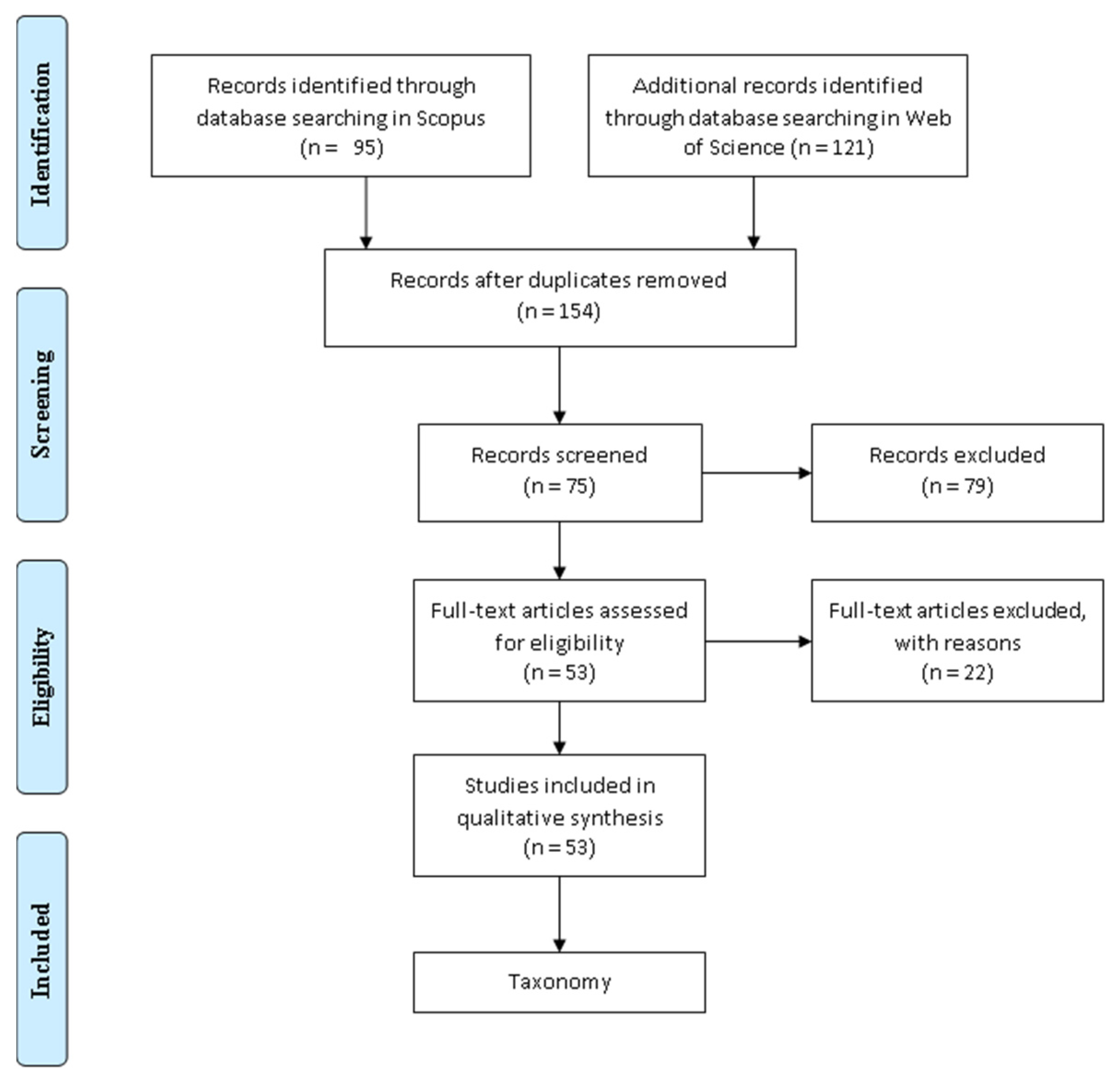

2. Materials and Methods

2.1. Research Questions, Databases, and Appropriate Research Terms

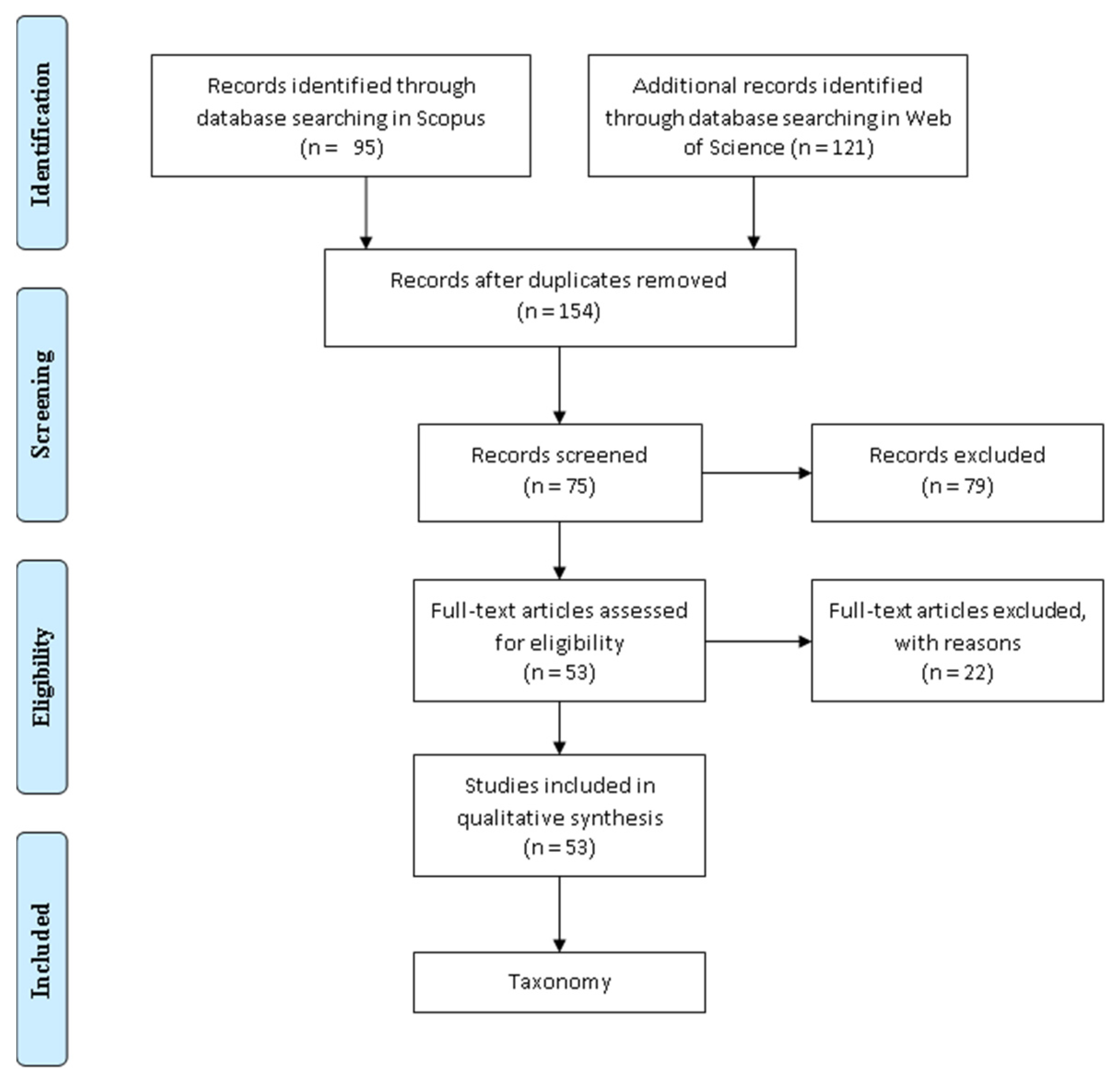

2.2. Sample Screening Criteria

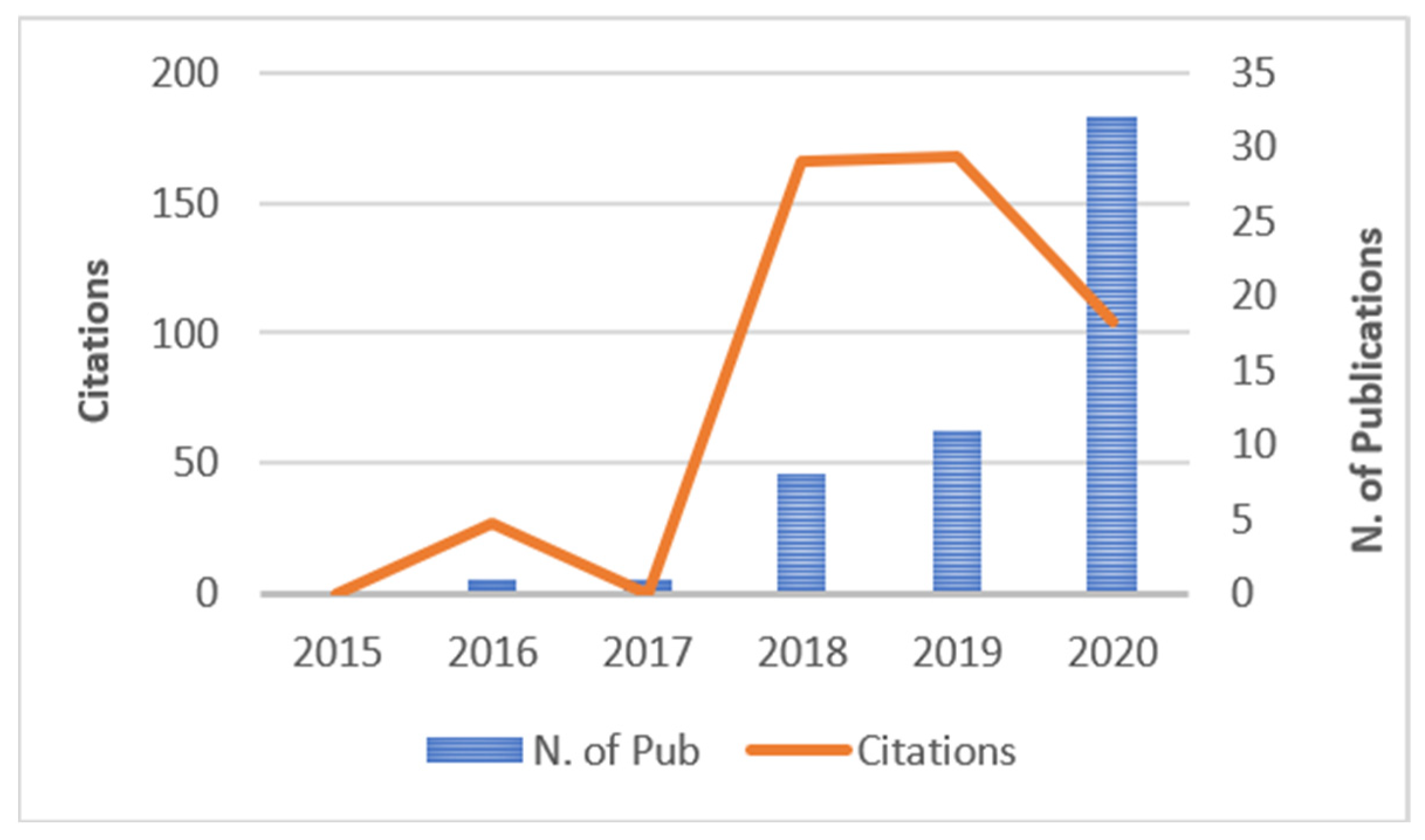

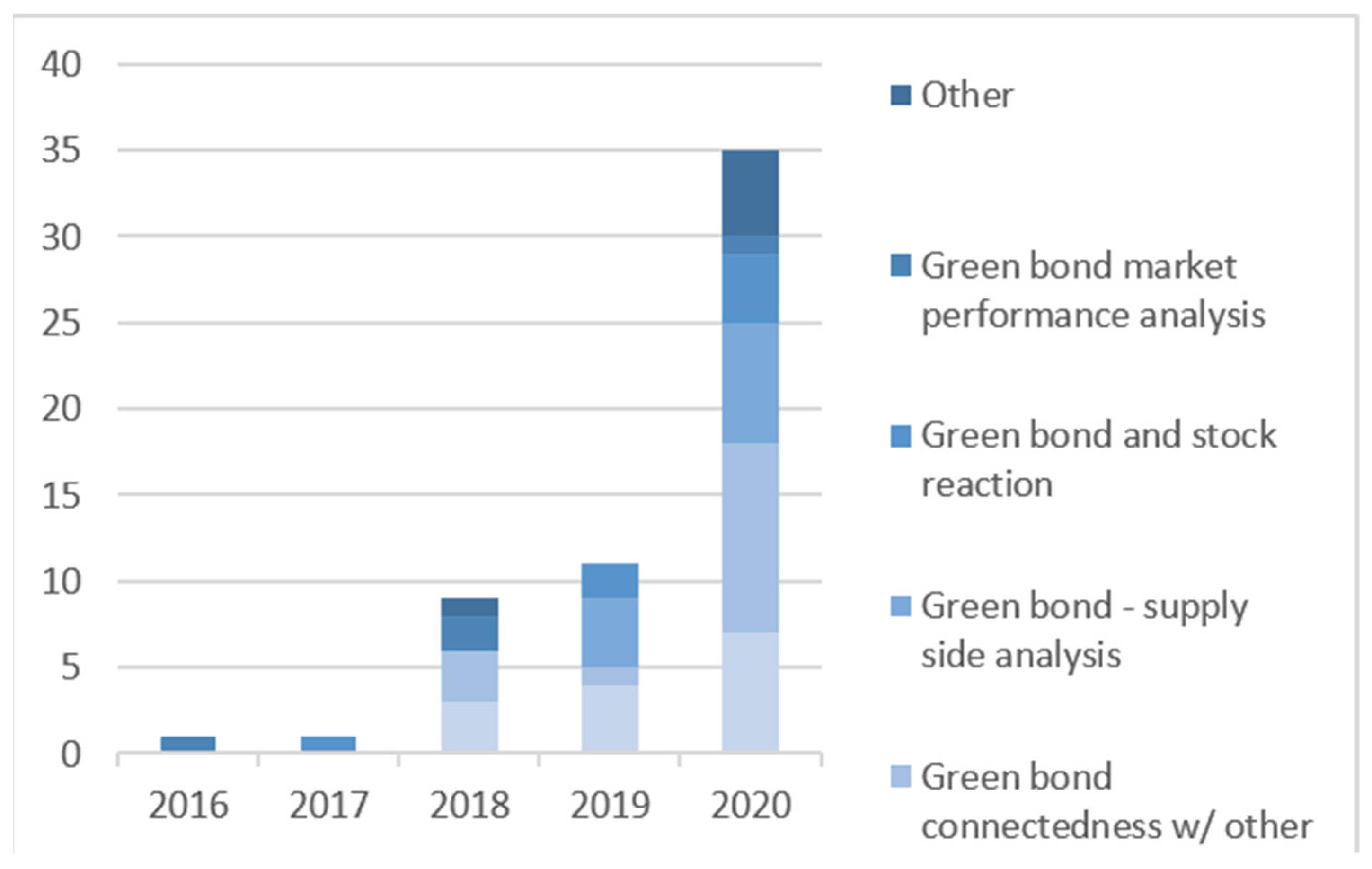

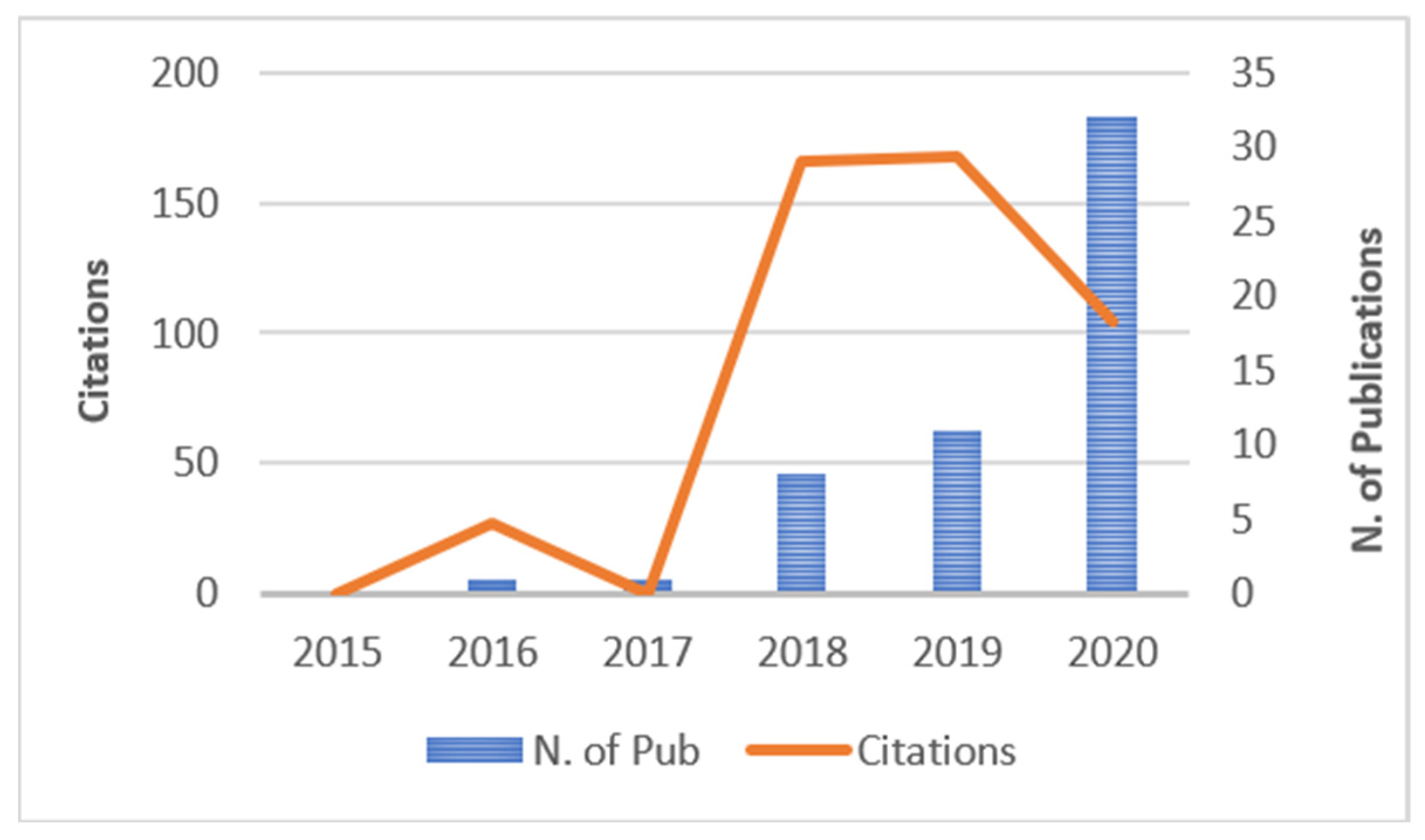

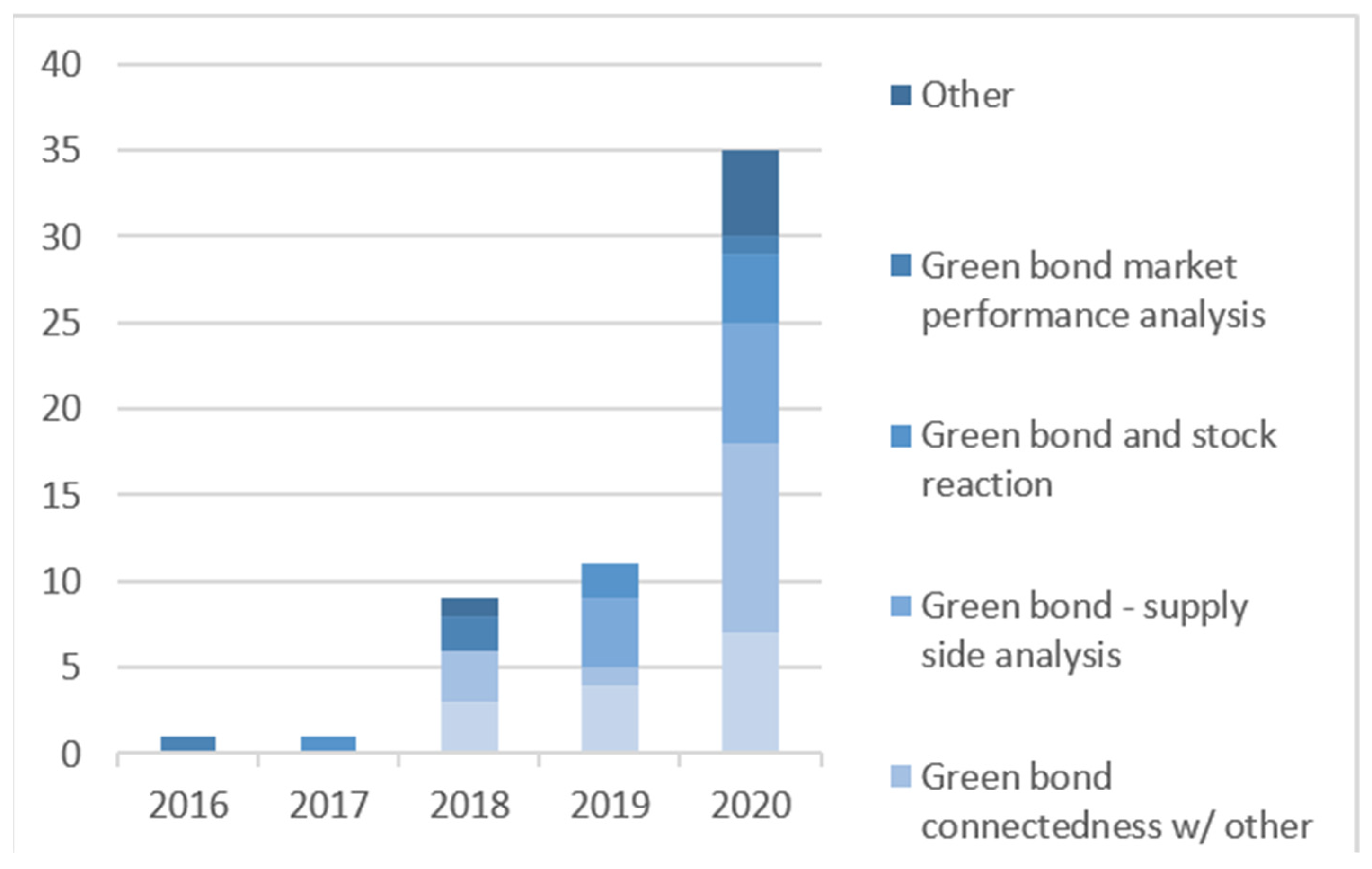

2.3. Sample Overview and Taxonomy

3. Results: Suggestions for Further Research

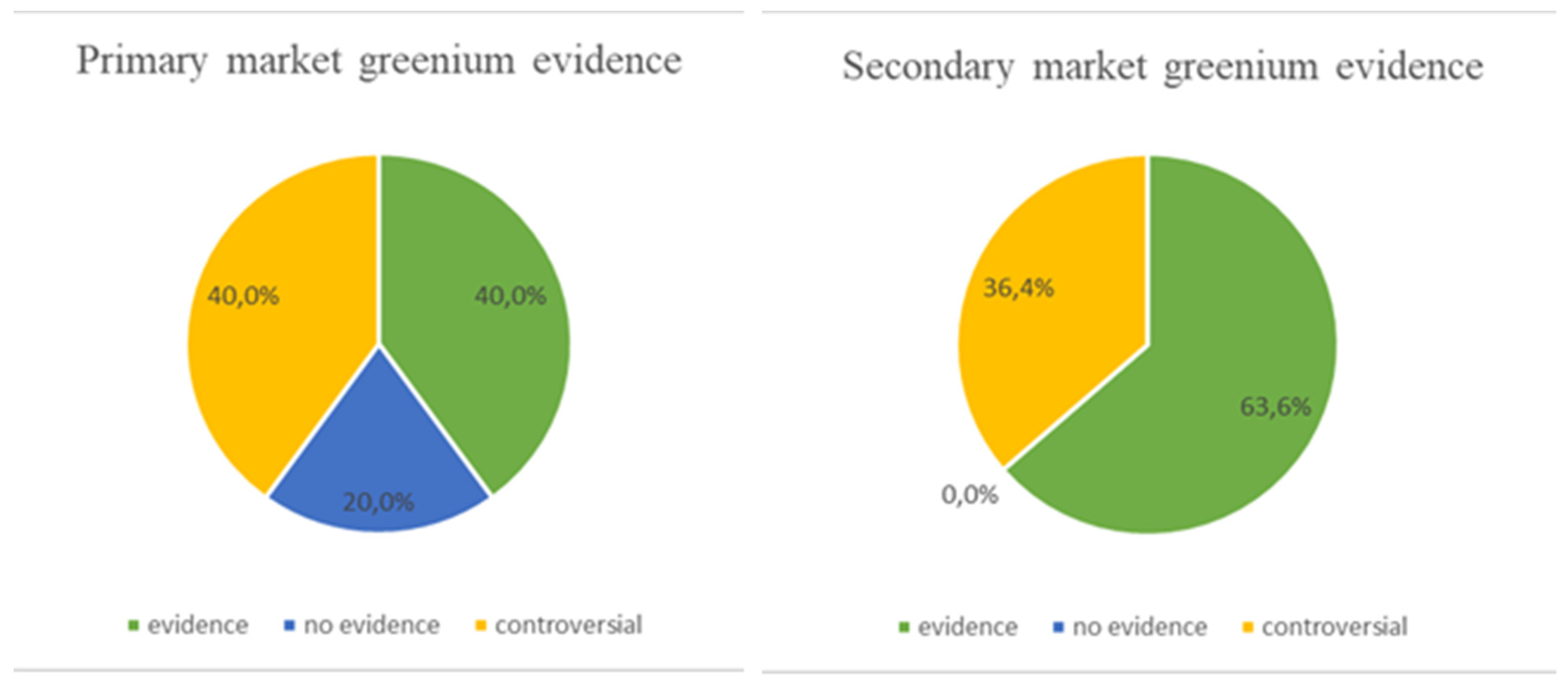

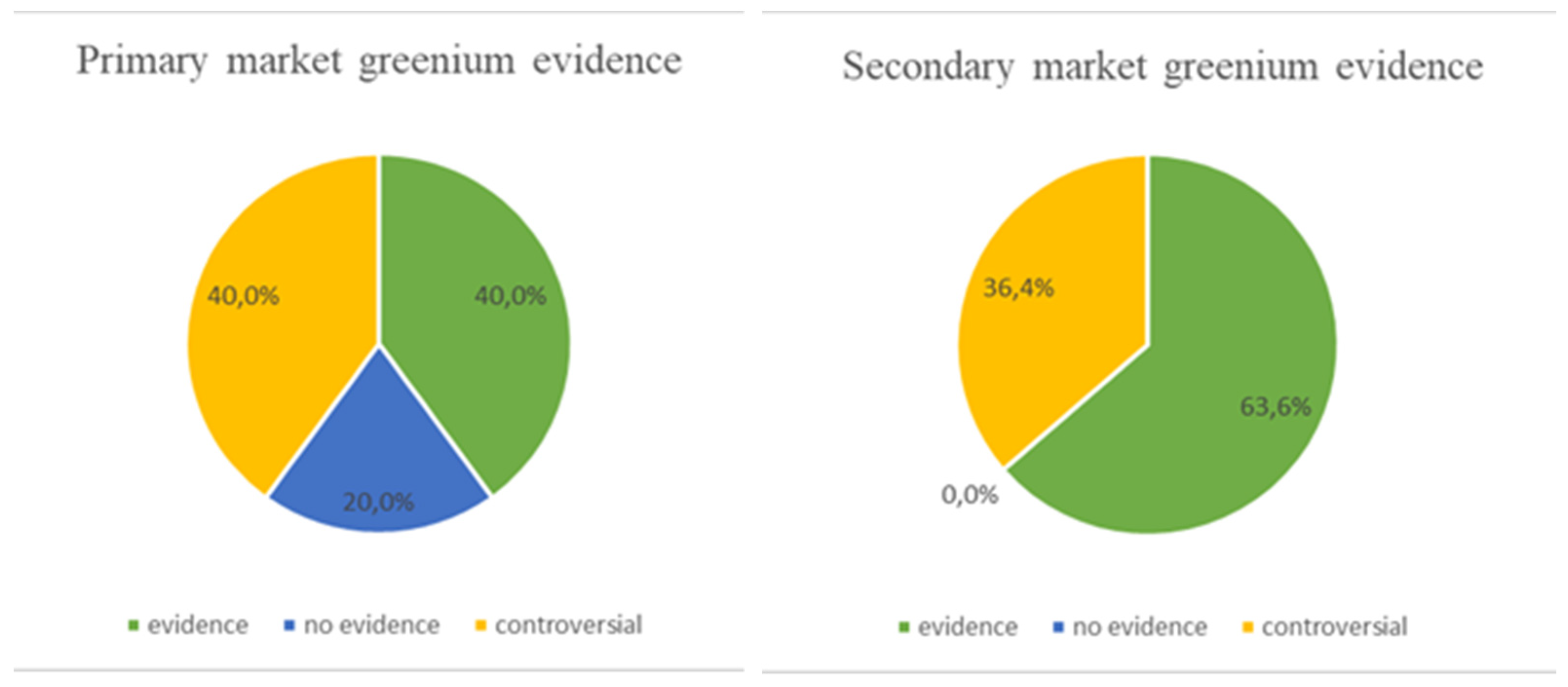

3.1. Greenium

3.2. Green Bond Connectedness with Other Financial Instruments

3.3. Green Bond and Stock Reaction

3.4. Green Bond—Supply-Side Analysis

3.5. Green Bond Market Performance Analysis

3.6. Other

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Author(s) | Year | Title | Journal | Taxonomy Group * |

|---|---|---|---|---|

| Alonso-Conde, A.B., Rojo-Suarez, J. | 2020 | On the Effect of Green Bonds on the Profitability and Credit Quality of Project Financing | Sustainability | 3 |

| Bachelet, M.J.; Becchetti, L.; Manfredonia, S. | 2019 | The Green Bonds Premium Puzzle: The Role of Issuer Characteristics and Third-Party Verification | Sustainability | 1 |

| Barua, S.; Chiesa, M. | 2019 | Sustainable financing practices through green bonds: What affects the funding size? | Business strategy and the environment | 3 |

| Baulkaran, V. | 2019 | Stock market reaction to green bond issuance | Journal of Asset Management | 4 |

| Broadstock, D.C.; Cheng, L.T.W. | 2019 | Time-varying relation between black and green bond price benchmarks: Macroeconomic determinants for the first decade | Finance Research Letters | 2 |

| Chang, K.; Feng, Y.L., Liu, W.: Lu, N.; Li, S.Z., | 2021 | The impacts of liquidity measures and credit rating on corporate bond yield spreads: Evidence from China’s green bond market | Applied Economics Letters | 3 |

| Chiesa, M.: Barua, S., | 2019 | The surge of impact borrowing: The magnitude and determinants of green bond supply and its heterogeneity across markets | Journal of Sustainable Finance and Investment | 3 |

| Daszynska-Zygadlo, K; Marszalek, J; Piontek, K | 2018 | Sustainable Finance Instruments’ Risk—Green Bond Market Analysis | Conference paper | 2 |

| Deng, Z.; Tang, D.Y.; Zhang, Y. | 2020 | Is “greenness” priced in the market? Evidence from green bond issuance in China | Journal of Alternative Investments | 3 |

| Dou, X.; Qi, S. | 2019 | The choice of green bond financing instruments | Cogent business and management | 3 |

| Draksaite, A; Kazlauskiene, V; Melnyk, L. | 2018 | The Perspective of the Green Bonds as Novel Debt Instruments in Sustainable Economy | Conference paper | 2 |

| Febi W.; Schäfer D.; Stephan A.; Sun C. | 2018 | The impact of liquidity risk on the yield spread of green bonds | Finance Research Letters | 1, 5 |

| Gianfrate, G.; Peri M. | 2019 | The green advantage: Exploring the convenience of issuing green bonds | Journal of Cleaner Production | 1 |

| Hachenberg, B.; Schiereck, D. | 2018 | Are green bonds priced differently from conventional bonds? | Journal of Asset Management | 1 |

| Halkos, G.; Managi, S.; Tsilika, K. | 2020 | Ranking Countries and Geographical Regions in the International Green Bond Transfer Network: A Computational Weighted Network Approach | Computational Economics | 6 |

| Hammoudeh, S.; Ajmi, A.N.; Mokni, K. | 2020 | Relationship between green bonds and financial and environmental variables: A novel time-varying causality | Energy Economics | 2 |

| Huynh, T.L.D. | 2020 | When ‘green’ challenges’ prime’: Empirical evidence from government bond markets | Journal of Sustainable Finance and Investment | 2 |

| Huynh, T.L.D.; Hille, E.; Nasir, M.A. | 2020 | Diversification in the age of the 4th industrial revolution: The role of artificial intelligence, green bonds, and cryptocurrencies | Technological Forecasting and Social Change | 2 |

| Hyun, S.; Park, D.; Tian, S. | 2020 | The price of going green: The role of greenness in green bond markets | Accounting and Finance | 1 |

| Hyun, S.; Park, D.; Tian, S. | 2021 | Pricing of Green Labeling: A Comparison of Labelled and Unlabelled Green Bonds | Finance Research Letters | 3 |

| Immel, M.; Hachenberg, B.; Kiesel, F.; Schiereck, D. | 2021 | Green bonds: Shades of green and brown | Journal of Asset Management | 1 |

| Jakubik, P.; Uguz, S. | 2021 | Impact of green bond policies on insurers: Evidence from the European equity market | Journal of Economics and Finance | 4 |

| Jin, J.; Han, L.; Wu, L; Zeng, H. | 2020 | The hedging effect of green bonds on carbon market risk | International Review of Financial Analysis | 2 |

| Kanamura, T. | 2020 | Are green bonds environmentally friendly and good performing assets? | Energy Economics | 1, 2 |

| Karpf, A; Mandel, A. | 2018 | The changing value of the ‘green’ label on the US municipal bond market | Nature climate change | 1 |

| Larcker, D.F.; Watts, E.M. | 2020 | Where is the Greenium? | Journal of Accounting and Economics | 1 |

| Lebelle, M.; Jarjir, SL.; Sassi, S. | 2020 | Corporate Green Bond Issuances: An International Evidence | Journal of risk and financial management | 4 |

| Li, Z.; Tang, Y.; Wu, J.; Zhang, J.; Lv, Q. | 2020 | The Interest Costs of Green Bonds: Credit Ratings, Corporate Social Responsibility, and Certification | Emerging Markets Finance and Trade | 3 |

| Liu, N.; Liu, C.; Da, B.; Zhang, T.; Guan, F. | 2021 | Dependence and risk spillovers between green bonds and clean energy markets | Journal of Cleaner Production | 2 |

| Mohd Roslen, S.N.; Yee, L.S.; Binti Ibrahim, S.A. | 2017 | Green Bond and shareholders’ wealth: A multi-country event study | Journal of globalization and small business | 4 |

| Monasterolo, I.; Raberto, M. | 2018 | The EIRIN Flow-of-funds Behavioral Model of Green Fiscal Policies and Green Sovereign Bonds | Ecological Economics | 6 |

| Nanayakkara, K.G.M.; Colombage, S. | 2020 | Does compliance with Green Bond Principles bring any benefit to make the ‘Green economy plan’ of the G20 a reality? | Accounting and Finance | 3 |

| Nanayakkara, M.; Colombage, S. | 2019 | Do investors in the Green Bond market pay a premium? Global evidence | Applied Economics | 1 |

| Nguyen, T.T.H.; Naeem, M.A.; Balli, F.; Balli, H.O.; Vo X.V. | 2021 | Time-frequency co-movement among green bonds, stocks, commodities, clean energy, and conventional bonds | Finance Research Letters | 2 |

| Park, D.; Park, J.; Ryu, D. | 2020 | Volatility Spillovers between Equity and Green Bond Markets | Sustainability | 2 |

| Partridge C.; Medda, F.R. | 2020 | The evolution of pricing performance of green municipal bonds | Journal of Sustainable Finance and Investment | 1 |

| Pham, L. | 2016 | Is it risky to go green? A volatility analysis of the green bond market | Journal of Sustainable Finance and Investment | 5 |

| Pham, L.; Huynh, T.L.D. | 2020 | How does investor attention influence the green bond market? | Finance Research Letters | 5 |

| Reboredo, J.C. | 2018 | Green bond and financial markets: Co-movement, diversification, and price spillover effects | Energy Economics | 2 |

| Reboredo, J.C.; Ugolini, A. | 2020 | Price connectedness between green bond and financial markets | Economic Modelling | 2 |

| Reboredo, J.C.; Ugolini, A.; Aiube, F.A.L. | 2020 | Network connectedness of green bonds and asset classes | Energy Economics | 2 |

| Russo, A.; Mariani, M.; Caragnano, A. | 2021 | Exploring the determinants of green bond issuance: Going beyond the long-lasting debate on performance consequences | Business strategy and the environment | 3 |

| Saeed, T.; Bouri, E.; Alsulami, H. | 2021 | Extreme return connectedness and its determinants between clean/green and dirty energy investments | Energy Economics | 2 |

| Shaydurova, A.; Panova, S.; Fedosova, R.; Zlotnikova, G. | 2018 | Investment attractiveness of “Green” financial instruments | Journal of Reviews on Global Economics | 5 |

| Tang, D.Y.; Zhang, Y. | 2020 | Do shareholders benefit from green bonds? | Journal of Corporate Finance | 1, 4 |

| Tolliver, C.; Keeley, A.R.; Managi, S. | 2020-1 | Drivers of green bond market growth: The importance of Nationally Determined Contributions to the Paris Agreement and implications for sustainability | Journal of Cleaner Production | 6 |

| Tolliver, C.; Keeley, A.R.; Managi, S. | 2020-2 | Policy targets behind green bonds for renewable energy: Do climate commitments matter? | Technological Forecasting and Social Change | 6 |

| Tu, C.A.; Rasoulinezhad, E.; Sarker, T. | 2020 | Investigating solutions for the development of a green bond market: Evidence from the analytic hierarchy process | Finance Research Letters | 6 |

| Tuhkanen, H.; Vulturius, G. | 2020 | Are green bonds funding the transition? Investigating the link between companies’ climate targets and green debt financing | Journal of Sustainable Finance and Investment | 6 |

| Wang J.; Chen X.; Li X.; Yu J.; Zhong R. | 2020 | The market reaction to green bond issuance: Evidence from China | Pacific-Basin Finance Journal | 1, 4 |

| Wang, Q.H.; Zhou, Y.N.; Luo, L.; Ji, J.P. | 2019 | Research on the Factors Affecting the Risk Premium of China’s Green Bond Issuance | Sustainability | 3 |

| Zerbib, O.D. | 2019 | The effect of pro-environmental preferences on bond prices: Evidence from green bonds | Journal of Banking and Finance | 1 |

| Zhou, X.G.; Cui, Y.D. | 2019 | Green Bonds, Corporate Performance, and Corporate Social Responsibility | Sustainability | 4 |

| 1 | CBI (Climate Bond Initiative) is an international not-for-profit organization aiming to mobilize larger capital flows to green climate-aligned projects. CBI operates by providing market intelligence, standards, and policy recommendations. |

| 2 | ICMA (International Capital Market Association) is a not-for-profit association composed of private and public financial actors, such as banks, asset managers, investment funds, central banks, law firms, etc. The main objective is to assist capital/security market participants, promote market good practices and standards, etc. From the starting coalition of four institutions (Bank of America Merrill Lynch, Citi, Credit Agricole and JP Morgan), ICMA now (as of the end of March 2020) counts on 600 Members in 62 countries. |

| 3 | According to ICMA, green bonds are any fixed income financial instruments where the proceeds will be exclusively used to finance (or re-finance) new (and/or existing) green projects where green projects are related to the followed field: Renewable energy, energy efficiency, pollution prevention, clean transportation, sustainable water management, etc. (ICMA 2018, Green Bond Principles). |

| 4 | The state of Massachusetts issued the first municipal green bond in July 2013. The first corporate green bond was issued by “Electricite de France” in November 2013. |

| 5 | In the same year, various green bond market indices were launched to sign the market progress contributing to the development of the market (Jones et al. 2020). |

| 6 | Scopus’s SCImago Journal Rank is a scientific influence index alternative to Impact Factor. The SJR measures weighted citations received by the journal. Citation weighting depends on the subject field and prestige (SJR) of the citing journal. |

References

- Alonso-Conde, Ana-Belén, and Javier Rojo-Suárez. 2020. On the effect of green bonds on the profitability and credit quality of project financing. Sustainability 12: 6695. [Google Scholar] [CrossRef]

- Ammann, Manuel, Martin Fehr, and Ralf Seiz. 2006. New Evidence on the Announcement Effect of Convertible and Exchangeable Bonds. Journal of Multinational Financial Management 16: 43–63. [Google Scholar] [CrossRef] [Green Version]

- Bachelet, Maria Jua, Leonardo Becchetti, and Stefano Manfredonia. 2019. The green bonds premium puzzle: The role of issuer characteristics and third-party verification. Sustainability 11: 1098. [Google Scholar] [CrossRef] [Green Version]

- Barua, Suborna, and Micol Chiesa. 2019. Sustainable financing practices through green bonds: What affects the funding size? Business Strategy and the Environment 28: 1131–47. [Google Scholar] [CrossRef]

- Baulkaran, Vishaal. 2019. Stock market reaction to green bond issuance. Journal of Asset Management 20: 331–40. [Google Scholar] [CrossRef]

- Broadstock, David C., and Louis T. W. Cheng. 2019. Time-varying relation between black and green bond price benchmarks: Macroeconomic determinants for the first decade. Finance Research Letters 29: 17–22. [Google Scholar] [CrossRef]

- Chang, Kai, Yan Ling Feng, Wang Liu, Ning Lu, and Sheng Ze Li. 2021. The impacts of liquidity measures and credit rating on corporate bond yield spreads: Evidence from China’s green bond market. Applied Economics Letters 28: 1446–57. [Google Scholar] [CrossRef]

- Chiesa, Micol, and Suborna Barua. 2019. The surge of impact borrowing: The magnitude and determinants of green bond supply and its heterogeneity across markets. Journal of Sustainable Finance & Investment 9: 138–61. [Google Scholar]

- Climate Bond Initiative (CBI). 2015. Year 2014 Green Bonds Final Report. London: Climate Bond Initiative. [Google Scholar]

- Dann, Larry Y., and Wayne H. Mikkelson. 1984. Convertible Debt Issuance, Capital Structure Change and Financing-Related Information: Some New Evidence. Journal of Financial Economics 13: 157–86. [Google Scholar] [CrossRef]

- Daszyńska-Żygadło, Karolina, Jakub Marszałek, and Krzysztof Piontek. 2018. Sustainable Finance Instruments’ Risk-Green Bond Market Analysis. European Financial Systems 2018: 78. [Google Scholar]

- Deng, Zhiyao, Dragon Yongjun Tang, and Yupu Zhang. 2020. Is “Greenness” Priced in the Market? Evidence from Green Bond Issuance in China. The Journal of Alternative Investments 23: 57–70. [Google Scholar] [CrossRef]

- Dou, Xiangsheng, and Shuxiu Qi. 2019. The choice of green bond financing instruments. Cogent Business & Management 6: 1652227. [Google Scholar]

- Draksaite, Aura, Vilma Kazlauskiene, and Leonid Melnyk. 2018. The Perspective of the Green Bonds as Novel Debt Instruments in Sustainable Economy. In Consumer Behavior, Organizational Strategy and Financial Economics. Cham: Springer, pp. 221–30. [Google Scholar]

- Ehlers, Torsten, and Frank Packer. 2017. Green bond finance and certification. Bank for International Settlements (BIS) Quarterly Review September. pp. 89–104. Available online: https://ssrn.com/abstract=3042378 (accessed on 1 December 2021).

- European Commission. 2018. Putting the Financial Sector at the Service of the Climate. Brussels: European Commission. [Google Scholar]

- Febi, Wulandari, Dorothea Schäfer, Andreas Stephan, and Chen Sun. 2018. The impact of liquidity risk on the yield spread of green bonds. Finance Research Letters 27: 53–59. [Google Scholar] [CrossRef]

- Fink, Arlene. 2019. Conducting Research Literature Reviews: From the Internet to Paper. London: Sage Publications. [Google Scholar]

- Forsbacka, Kristina, and Gregor Vulturius. 2019. A Legal Analysis of Terms and Conditions for Green Bonds. Europarättslig Tidskrift 3: 397–442. [Google Scholar]

- Gianfrate, Gianfranco, and Mattia Peri. 2019. The green advantage: Exploring the convenience of issuing green bonds. Journal of Cleaner Production 219: 127–35. [Google Scholar] [CrossRef]

- Hachenberg, Britta, and Dirk Schiereck. 2018. Are green bonds priced differently from conventional bonds? Journal of Asset Management 19: 371–83. [Google Scholar] [CrossRef]

- Halkos, George, Shunsuke Managi, and Kyriaki Tsilika. 2020. Ranking Countries and Geographical Regions in the International Green Bond Transfer Network: A Computational Weighted Network Approach. Computational Economics 58: 1301–46. [Google Scholar] [CrossRef]

- Hammoudeh, Shawkat, Ahdi Noomen Ajmi, and Khaled Mokni. 2020. Relationship between green bonds and financial and environmental variables: A novel time-varying causality. Energy Economics 92: 104941. [Google Scholar] [CrossRef]

- Haq, Inzamam Ul, Supat Chupradit, and Chunhui Huo. 2021. Do Green Bonds Act as a Hedge or a Safe Haven against Economic Policy Uncertainty? Evidence from the USA and China. International Journal of Financial Studies 9: 40. [Google Scholar] [CrossRef]

- Harrison, Caroline, and Bridget Boulle. 2017. Green Bond Pricing in the Primary Market: April–June 2017. London: Climate Bond Initiative. [Google Scholar]

- Harrison, Caroline, and Lea Muething. 2021. Sustainable Global State of the Market 2020. London: Climate Bonds Initiative. [Google Scholar]

- Hemmingson, Carl, and Robert Ydenius. 2017. The Convertible Bond Announcement Effect: An Event Study on the Nordic Markets. Master’s thesis, Lund University, Lund, Sweden. [Google Scholar]

- Huynh, Toan Luu Duc, Erik Hille, and Muhammad Ali Nasir. 2020. Diversification in the age of the 4th industrial revolution: The role of artificial intelligence, green bonds and cryptocurrencies. Technological Forecasting and Social Change 159: 120188. [Google Scholar] [CrossRef]

- Huynh, Toan Luu Duc. 2020. When ‘green’challenges ‘prime’: Empirical evidence from government bond markets. Journal of Sustainable Finance & Investment, 1–14. [Google Scholar] [CrossRef]

- Hyun, Suk, Donghyun Park, and Shu Tian. 2020. The price of going green: The role of greenness in green bond markets. Accounting & Finance 60: 73–95. [Google Scholar]

- Hyun, Suk, Donghyun Park, and Shu Tian. 2021. Pricing of Green Labeling: A Comparison of Labeled and Unlabeled Green Bonds. Finance Research Letters 41: 101816. [Google Scholar] [CrossRef]

- ICMA. 2018. Green bond Principles, Voluntary Process Guidelines for Issuing Green Bonds. Zurich: International Capital Market Association. [Google Scholar]

- Immel, Moritz, Britta Hachenberg, Florian Kiesel, and Dirk Schiereck. 2021. Green bonds: Shades of green and brown. Journal of Asset Management 22: 96–109. [Google Scholar] [CrossRef]

- Jakubik, Petr, and Sibel Uguz. 2021. Impact of green bond policies on insurers: Evidence from the European equity market. Journal of Economics and Finance 45: 381–93. [Google Scholar] [CrossRef]

- Jin, Jiayu, Liyan Han, Lei Wu, and Hongchao Zeng. 2020. The hedging effect of green bonds on carbon market risk. International Review of Financial Analysis 71: 101509. [Google Scholar] [CrossRef]

- Jones, Ryan, Tom Baker, Katherine Huet, Laurence Murphy, and Nick Lewis. 2020. Treating ecological deficit with debt: The practical and political concerns with green bonds. Geoforum 114: 49–58. [Google Scholar] [CrossRef]

- Kanamura, Takashi. 2020. Are green bonds environmentally friendly and good performing assets? Energy Economics 88: 104767. [Google Scholar] [CrossRef]

- Karpf, Andreas, and Antoine Mandel. 2018. The changing value of the ‘green’ label on the US municipal bond market. Nature Climate Change 8: 161–65. [Google Scholar] [CrossRef]

- Larcker, David F., and Edward M. Watts. 2020. Where’s the greenium? Journal of Accounting and Economics 69: 101312. [Google Scholar] [CrossRef]

- Lebelle, Martin, Souad Lajili Jarjir, and Syrine Sassi. 2020. Corporate green bond issuances: An international evidence. Journal of Risk and Financial Management 13: 25. [Google Scholar] [CrossRef] [Green Version]

- Li, Zhiyong, Ying Tang, Jingya Wu, Junfeng Zhang, and Qi Lv. 2020. The interest costs of green bonds: Credit ratings, corporate social responsibility, and certification. Emerging Markets Finance and Trade 56: 2679–92. [Google Scholar] [CrossRef]

- Liaw, K. Thomas. 2020. Survey of Green Bond Pricing and Investment Performance. Journal of Risk and Financial Management 13: 193. [Google Scholar] [CrossRef]

- Liu, Nana, Chuanzhe Liu, Bowen Da, Tong Zhang, and Fangyuan Guan. 2021. Dependence and risk spillovers between green bonds and clean energy markets. Journal of Cleaner Production 279: 123595. [Google Scholar] [CrossRef]

- MacAskill, Stefen, E. Roca, B. Liu, R. A. Stewart, and O. Sahin. 2021. Is there a green premium in the green bond market? Systematic literature review revealing premium determinants. Journal of Cleaner Production 280: 124491. [Google Scholar] [CrossRef]

- Moher, David, Alessandro Liberati, Jennifer Tetzlaff, and Douglas G. Altman. 2010. Preferred reporting items for systematic reviews and meta-analyses: The PRISMA statement. International Journal of Surgery 8: 336–41. [Google Scholar] [CrossRef] [Green Version]

- Monasterolo, Irene, and Marco Raberto. 2018. The EIRIN flow-of-funds behavioural model of green fiscal policies and green sovereign bonds. Ecological Economics 144: 228–43. [Google Scholar] [CrossRef]

- Monk, Alexander, and Richard Perkins. 2020. What explains the emergence and diffusion of green bonds? Energy Policy 145: 111641. [Google Scholar] [CrossRef]

- Naeem, Muhammad Abubakr, Elie Bouri, Mabel D. Costa, Nader Naifar, and Syed Jawad Hussain Shahzad. 2021. Energy markets and green bonds: A tail dependence analysis with time-varying optimal copulas and portfolio implications. Resources Policy 74: 102418. [Google Scholar] [CrossRef]

- Nanayakkara, Kariyawasam Galoluwage Madurika, and Sisira Colombage. 2021. Does compliance with Green Bond Principles bring any benefit to make G20′s ‘Green economy plan’ a reality? Accounting & Finance 61: 4257–85. [Google Scholar]

- Nanayakkara, Madurika, and Sisira Colombage. 2019. Do investors in green bond market pay a premium? Global evidence. Applied Economics 51: 4425–37. [Google Scholar] [CrossRef]

- Nguyen, Thi Thu Ha, Muhammad Abubakr Naeem, Faruk Balli, Hatice Ozer Balli, and Xuan Vinh Vo. 2021. Time-frequency co-movement among green bonds, stocks, commodities, clean energy, and conventional bonds. Finance Research Letters 40: 101739. [Google Scholar] [CrossRef]

- OECD. 2017. Investing in Climate, Investing in Growth. Paris: OECD Publishing. [Google Scholar]

- Park, Daehyeon, Jiyeon Park, and Doojin Ryu. 2020. Volatility spillovers between equity and green bond markets. Sustainability 12: 3722. [Google Scholar] [CrossRef]

- Partridge, Candace, and Francesca Romana Medda. 2020. The evolution of pricing performance of green municipal bonds. Journal of Sustainable Finance & Investment 10: 44–64. [Google Scholar]

- Pham, Linh, and Toan Luu Duc Huynh. 2020. How does investor attention influence the green bond market? Finance Research Letters 35: 101533. [Google Scholar] [CrossRef]

- Pham, Linh. 2016. Is it risky to go green? A volatility analysis of the green bond market. Journal of Sustainable Finance & Investment 6: 263–91. [Google Scholar]

- Preclaw, Ryan, and Anthony Bakshi. 2015. The Cost of Being Green. Barclays Credit Research. New York: Barclays. [Google Scholar]

- Reboredo, Juan C. 2018. Green bond and financial markets: Co-movement, diversification and price spillover effects. Energy Economics 74: 38–50. [Google Scholar] [CrossRef]

- Reboredo, Juan C., and Andrea Ugolini. 2020. Price connectedness between green bond and financial markets. Economic Modelling 88: 25–38. [Google Scholar] [CrossRef]

- Reboredo, Juan C., Andrea Ugolini, and Fernando Antonio Lucena Aiube. 2020. Network connectedness of green bonds and asset classes. Energy Economics 86: 104629. [Google Scholar] [CrossRef]

- Roslen, Siti Nurhidayah Mohd, Lee Sin Yee, and Salizatul Aizah Binti Ibrahim. 2017. Green Bond and shareholders’ wealth: A multi-country event study. International Journal of Globalisation and Small Business 9: 61–69. [Google Scholar] [CrossRef]

- Russo, Angeloantonio, Massimo Mariani, and Alessandra Caragnano. 2021. Exploring the determinants of green bond issuance: Going beyond the long-lasting debate on performance consequences. Business Strategy and the Environment 30: 38–59. [Google Scholar] [CrossRef]

- Saeed, Tareq, Elie Bouri, and Dang Khoa Tran. 2020. Hedging strategies of green assets against dirty energy assets. Energies 13: 3141. [Google Scholar] [CrossRef]

- Saeed, Tareq, Elie Bouri, and Hamed Alsulami. 2021. Extreme return connectedness and its determinants between clean/green and dirty energy investments. Energy Economics 96: 105017. [Google Scholar] [CrossRef]

- Shaydurova, Alina, Svetlana Panova, Raisa Fedosova, and Galina Zlotnikova. 2018. Investment Attractiveness of a “Green” Financial Instruments. Journal of Reviews on Global Economics 7: 710–15. [Google Scholar] [CrossRef] [Green Version]

- Stechemesser, Kristin, and Edeltraud Guenther. 2012. Carbon accounting: A systematic literature review. Journal of Cleaner Production 36: 17–38. [Google Scholar] [CrossRef]

- Syzdykov, Yerlan, and Jean Lacombe. 2020. Emerging Market Green Bonds Report 2019. Paris: Amundi Asset Management. [Google Scholar]

- Tang, Dragon Yongjun, and Yupu Zhang. 2020. Do shareholders benefit from green bonds? Journal of Corporate Finance 61: 101427. [Google Scholar] [CrossRef]

- Tolliver, Clarence, Alexander Ryota Keeley, and Shunsuke Managi. 2020a. Drivers of green bond market growth: The importance of Nationally Determined Contributions to the Paris Agreement and implications for sustainability. Journal of Cleaner Production 244: 118643. [Google Scholar] [CrossRef]

- Tolliver, Clarence, Alexander Ryota Keeley, and Shunsuke Managi. 2020b. Policy targets behind green bonds for renewable energy: Do climate commitments matter? Technological Forecasting and Social Change 157: 120051. [Google Scholar] [CrossRef]

- Tu, Chuc Anh, Ehsan Rasoulinezhad, and Tapan Sarker. 2020a. Investigating solutions for the development of a green bond market: Evidence from analytic hierarchy process. Finance Research Letters 34: 101457. [Google Scholar] [CrossRef]

- Tu, Chuc Anh, Tapan Sarker, and Ehsan Rasoulinezhad. 2020b. Factors Influencing the Green Bond Market Expansion: Evidence from a Multi-Dimensional Analysis. Journal of Risk and Financial Management 13: 126. [Google Scholar] [CrossRef]

- Tuhkanen, Heidi, and Gregor Vulturius. 2020. Are green bonds funding the transition? Investigating the link between companies’ climate targets and green debt financing. Journal of Sustainable Finance & Investment, 1–23. [Google Scholar] [CrossRef]

- Wang, Jiazhen, Xin Chen, Xiaoxia Li, Jing Yu, and Rui Zhong. 2020. The market reaction to green bond issuance: Evidence from China. Pacific-Basin Finance Journal 60: 101294. [Google Scholar] [CrossRef]

- Wang, Qinghua, Yaning Zhou, Li Luo, and Junping Ji. 2019. Research on the factors affecting the risk premium of China’s green bond issuance. Sustainability 11: 6394. [Google Scholar] [CrossRef] [Green Version]

- World Bank. 2019. 10 Years of Green Bonds: Creating the Blueprint for Sustainability Across Capital Markets. Washington, DC: World Bank. [Google Scholar]

- Zerbib, Olivier David. 2019. The effect of pro-environmental preferences on bond prices: Evidence from green bonds. Journal of Banking & Finance 98: 39–60. [Google Scholar]

- Zhou, Xiaoguang, and Yadi Cui. 2019. Green bonds, corporate performance, and corporate social responsibility. Sustainability 11: 6881. [Google Scholar] [CrossRef] [Green Version]

| Green Bond Type | Key Features |

|---|---|

| Use-of-Proceeds Bond |

|

| Use-of-Proceeds Revenue Bond |

|

| Project Bond |

|

| Securitized Bond |

|

| Agency (Acronyms) | Year (Version) | Initiative | External Review | Use of Proceeds Allocation |

|---|---|---|---|---|

| International Capital Market Association (ICMA) | 2014 (v 1) | Green Bond Principles | Voluntary | Do not provide a close taxonomy of eligible green areas |

| 2018 (v 2) | ||||

| Climate Bond Initiative (CBI) | 2015 (v 2.0) | Climate Bond Standard | Mandatory | Climate Bond Taxonomy |

| 2017 (v 2.1) | ||||

| 2019 (v 3.0) | ||||

| EU Commission | December 2019 | EU Green Bond Standard | Mandatory |

|

| People’s Bank of China (PBOC) | June 2020 | China Green Bond Endorsed Project Catalogue | Voluntary, recommended | Official list of eligible green areas (China Green Bond Endorsed Project Catalogue) |

| ASEAN Capital Market Forum (ACMF) | 2018 | ASEAN Green Bond Standards | Voluntary, recommended | Do not provide a close taxonomy of eligible green areas |

| Title | Authors | Topic | Methodology |

|---|---|---|---|

| Survey of Green Bond Pricing and Investment Performance | Liaw (2020) | Green bond premium | Not a standardized literature selection model |

| Is there a green premium in the green bond market? Systematic literature review revealing premium determinants | MacAskill et al. (2021) | Green bond premium | Systematic literature review |

| Group | Number of Articles |

|---|---|

| 1. Greenium | 14 |

| 2. Green bond connectedness with other financial instruments 1 | 15 |

| 3. Green bond—supply-side analysis | 11 |

| 4. Green bond and stock reaction 2 | 7 |

| 5. Green bond market performance analysis 3 | 4 |

| 6. Other | 6 |

| Author(s) (Year) | Characteristics of the Sample | Methodology | Main Results | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Time Span | Geographical Scope | Sample Size | Market Segment | Methods | Size-Effect Type | Greenium Evidence | Premium Dimension | Level of Statistical Significance | |

| Febi et al. (2018) | 2013–2016 | UK e Lux | 64 | Secondary market | Fixed effect panel regression model | Credit spread (difference between green bond yield and government bond yield) | Controversial | −69.2 bps in 2016 | 10% in 2016 no significance other years |

| Hachenberg and Schiereck (2018) | 2015–2016 | World | 63 | Secondary market | Matching method, yield curve, Wilcoxon test, Panel regression model | Spread between green bonds and similar conventional bonds | Controversial | −1.18 bps (entire sample) | no significance |

| Karpf and Mandel (2018) | 2010–2016 | US | 1880 | Secondary market | Yield curve, Mixed regression model, Oaxaca—Blinder decomposition | Yield to call (yield to maturity priced out the value of this option attached) | Yes | −7.8 bps (part of premium explained by green purpose) | n.a. |

| Bachelet et al. (2019) | 2013–2017 | World | 89 | Secondary market | Matching method, Regression model (OLS, FE) | Spread between green bond ask yield and matched conventional bond ask yields | Controversial | +5 bps (entire sample) −4 bps (subsample government/institution issuers) | 1% |

| Gianfrate and Peri (2019) | 2013–2017 | EU | 121 | Primary and secondary market | Propensity score matching | Secondary market yield bond spread | Yes | between −5 and −13 bps (on average depending on temporal windows of the study) | different significance levels |

| Nanayakkara and Colombage (2019) | 2016–2017 | World | 82 | Secondary market | Panel data regression with hybrid model | Daily option adjusted spread (OAS) | Yes | −63 bps | 1% |

| Zerbib (2019) | 2013–2017 | World | 110 | Secondary market | Matching method, Fixed effect panel regression | Daily ask yield between green bonds and synthetic conventional bonds | Yes | −2 bps (in the entire sample) | 1% |

| Hyun et al. (2020) | 2010–2017 | World | 60 | Secondary market | Matching method, OLS, and fixed effects generalized least squares (FEGLS) regression model | Liquidity-adjusted ask yield spread between green bonds and paired conventional bonds | Controversial | −6 bps (in case of third party verification) −15 bps (in case of CBI certification) | 1% |

| Kanamura (2020) | 2014–2018 | World | n.a. | Secondary market | Risk-Expected return model | Market indexes | Yes | n.a. | n.a. |

| Larcker and Watts (2020) | 2013—2018 | US | 640 | Primary market | Matching method, kernel density estimator, Nearest neighbors matching, Wilcoxon test | Initial offering credit spread | no | +0.5 bps (but in 85% of the cases yield spread is null) | 1% |

| Partridge and Medda (2020) | 2013–2018 | US | 453 | Primary market | Matching method, Yield curve, Panel regression model | Initial yields at issue | Controversial | −0.1 bps (in 2018) | no significance |

| Secondary market | Daily traded market yields | Yes | −4 bps (entire sample) | 1% | |||||

| Tang and Zhang (2020) | 2007–2017 | World | 1510 | Primary market | Matching method, Regression model, Diff-in-diff analysis | Yield spread at the issuance | Controversial | −6.94 bps (entire sample) no pricing difference when issuer’s characteristics are considered | 5% |

| Wang et al. (2020) | 2016–2019 | China | 159 | Primary market | Matching method, univariate and multivariate analysis | Credit spread (spread between the “at-issue green bond yield” and the yield on a treasury security of comparable maturity) | Yes | −34 bps | 1% |

| Immel et al. (2021) | 2007–2019 | World | 466 | Secondary market | OLS regression | Secondary market yield bond spread | Yes | between −8 and −14 bps | 1% |

| Author(s) (Year) | Time Span | Geographical Scope | Methodology |

|---|---|---|---|

| Daszyńska-Żygadło et al. (2018) | 2014–2018 | World | Multivariate Garch framework |

| Draksaite et al. (2018) | 2007–2016 | EU | Covariation and regression based analysis |

| Reboredo (2018) | 10/2014–08/2017 | World | Time-invariant and time-varying copula approaches |

| Broadstock and Cheng (2019) | 28/11/2008–31/7/2018 | US | Dynamic conditional correlations (DCC), dynamic model averaging (DMA) |

| Reboredo and Ugolini (2020) | 10/2014–06/2019 | World | Structural VAR (Vector Autoregressive) model parameters |

| Hammoudeh et al. (2020) | 6/2014–2/2020 | World | Time-varying Granger causality test |

| Huynh et al. (2020) | 12/2017–01/2020 | World | Tail dependence as copulas, volatility interconnectedness via the Generalized Forecast Error Variance Decomposition |

| Huynh (2020) | 12/2008–11/2019 | World | Copulas modelling approach |

| Jin et al. (2020) | 12/2008–12/2018 | World | Dynamic hedge ratio models: DCC-APGARCH, DCC-T-GARCH, and DCC-GJRGARCH models |

| Kanamura (2020) | 11/2014–12/2018 | World | Structural price model, Dynamic conditional correlation (DCC) model |

| Liu et al. (2021) | 07/2011–2/2020 | World | Time-invariant and time-varying copula approaches with CoVaR |

| Nguyen et al. (2021) | 12/2008–12/2019 | World | Rolling window wavelet correlation approach |

| Park et al. (2020) | 01/2010–01/2020 | World | BEKK model, dynamic conditional correlation-generalized autoregressive conditional heteroskedasticity (DCC-GARCH) model |

| Reboredo et al. (2020) | 10/2014–12/2018 | US, EU | Wavelet analysis, Structural VAR (Vector Autoregressive) model parameters |

| Saeed et al. (2021) | 01/2012–11/2019 | US | Quantile based VAR model |

| Author(s) (Year) | Time Span | Geographical Scope | Sample Size | Type of Green Bond (and Issuer) Analyzed | Methodology |

|---|---|---|---|---|---|

| Mohd Roslen et al. (2017) | 2010–07/2015 | World | 156 GB issuances and 118 GB issuance announcements | Listed issuer (financial institutions and non-financial issuers with extraordinary finance operations were excluded) | Event study analysis of average abnormal return (AAR) and cumulative abnormal return (CAR) |

| Baulkaran (2019) | n.d. | World | 54 GB issuers | Listed corporate GB issuer, with height market capitalization | Event study method; regression analysis |

| Zhou and Cui (2019) | 2016–2019 | China | 144 GB issuances, 70 Chinese listed issuers | All types of listed issuers (financial and non-financial, private and public); only long-term issuances are considered | Event study approach, propensity score matching (PSM), difference-in-differences (DID) |

| Jakubik and Uguz (2021) | 2012–2019 | EU | 15 issuers | Listed EU Insurance company with GB policy | OLS regression |

| Lebelle et al. (2020) | 2009–2018 | World | 475 GB issuances, 145 GB issuers | Private, listed GB issuers (financial and non-financial); securitized GB excluded | Event study method CAPM, Fama-French three-factor model, Carhart four-factor model |

| Tang and Zhang (2020) | 2007–2017 | World | 1510 GB issuances, 132 GB issuers | Private, listed GB issuers | Event study analysis and cumulative abnormal return (CAR) |

| Wang et al. (2020) | 01/2016–06/2019 | China | 159 GB issuances, 56 GB issuers | Listed, private (non-financial), rated and Chinese GB issuers | Matching method, Zerbib method—event study method |

| Author(s) (Year) | Time Span | Geographical Scope | Sample Size | Green Bond (and Issuer) Type | Methodology |

|---|---|---|---|---|---|

| Barua and Chiesa (2019) | 2010–2017 | World | 771 GB | All types | Cross-sectional OLS regression |

| Chiesa and Barua (2019) | 2010–2017 | World | 771 GB | All types | Cross-sectional OLS regression, Blinder–Oaxaca Decomposition |

| Dou and Qi (2019) | 2016–2018 | China | 308 GB | Corporate issuers, medium and long-term maturity green bonds | Logit model and maximum likelihood estimation method |

| Wang et al. (2019) | 1/2016–12/2018 | China | 305 GB | ABS and project green bonds excluded | Multivariate statistical regression analysis on cross-sectional data |

| Alonso-Conde and Rojo-Suárez (2020) | n.a. | n.a. | n.a. | n.a. | Business case (Sagunto regasification plant) |

| Deng et al. (2020) | 2016–2018 | China | 163 GB | All types | OLS regression |

| Hyun et al. (2021) | 01/2014–12/2017 | World | 3578 GB | All types | Propensity score matching (PSM) OLS regression |

| Li et al. (2020) | 01/2016–09/2018 | China | 114 GB | Listed green bonds | OLS regression |

| Nanayakkara and Colombage (2021) | 2007–2016 | G-20 countries | 399 GB | Supranational issuers excluded | Cross-sectional regression |

| Chang et al. (2021) | 01/2018–12/2019 | China | 112 GB | Corporate issuers | Panel data regression and generalized method of moments (GMM) |

| Russo et al. (2021) | 2013–2016 | World | 306 GB | Corporate issuers | GLS regression |

| Author(s) (Year) | Time Span | Geographical Scope | Methodology |

|---|---|---|---|

| Pham (2016) | 30/4/2010–29/4/2015 | World | Multivariate GARCH |

| Febi et al. (2018) | 2013–2016 | UK and Lussemburgo | Two-factor model; LOT liquidity measure; OLS panel regression |

| Shaydurova et al. (2018) | 12/2015–5/2018 | World | Standard analysis of the performance of the indices; VAR model |

| Pham and Huynh (2020) | 10/2014–11/2019 | World | Univariate analysis; GARCH models; Covariance stationary VAR model |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Cortellini, G.; Panetta, I.C. Green Bond: A Systematic Literature Review for Future Research Agendas. J. Risk Financial Manag. 2021, 14, 589. https://doi.org/10.3390/jrfm14120589

Cortellini G, Panetta IC. Green Bond: A Systematic Literature Review for Future Research Agendas. Journal of Risk and Financial Management. 2021; 14(12):589. https://doi.org/10.3390/jrfm14120589

Chicago/Turabian StyleCortellini, Giuseppe, and Ida Claudia Panetta. 2021. "Green Bond: A Systematic Literature Review for Future Research Agendas" Journal of Risk and Financial Management 14, no. 12: 589. https://doi.org/10.3390/jrfm14120589

APA StyleCortellini, G., & Panetta, I. C. (2021). Green Bond: A Systematic Literature Review for Future Research Agendas. Journal of Risk and Financial Management, 14(12), 589. https://doi.org/10.3390/jrfm14120589