Modelling Sector-Level Asset Prices

Abstract

1. Introduction

2. Methodology

2.1. Models and Econometric Approach

2.2. Sample and Data5

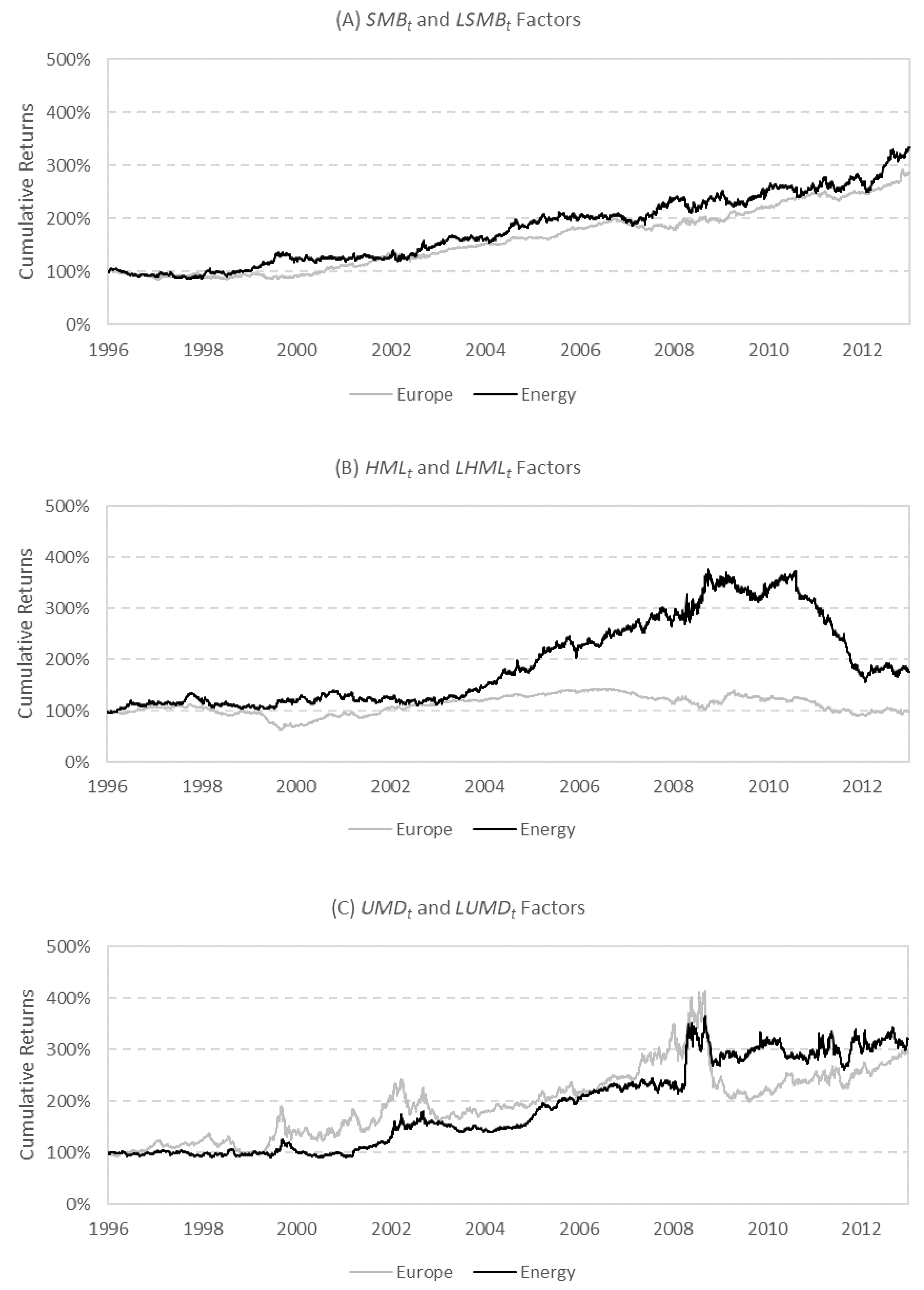

2.3. The Local Stock Market Risk Factors: Size, Value and Momentum

2.4. The 12 Energy Utility Portfolios

2.5. Time-Varying Risk Factor Sensitivities

2.6. Better Isolate Firm-Specific Returns

3. Results

3.1. Descriptive Statistics

3.2. Local Stock Market Risk Factors Better Explain Sector-Level Returns

3.3. Portfolios within the Energy Sector Have Heterogeneous Risk Exposure

3.4. Time-Varying Risk Factor Sensitivities: Annual Regressions

3.5. Time-Varying Risk Factor Sensitivities: Inductive Structural Breakpoint Tests

3.6. Better Isolate Firm-Specific Returns: Inductive Structural Breakpoint Tests

3.7. Robustness

4. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A. Data Variables and Description

| Symbol | Data Variable | Description |

| The 12 value-weighted portfolios include the energy sector | Twelve portfolios of energy stocks grouped based on characteristics: portfolios of energy utilities grouped on firm characteristics, including the energy sector as a whole; small and big utilities; high-BE/ME (value), mid-BE/ME (neutral) and low-BE/ME (growth) utilities; upper, medium and down momentum utilities; and electricity, natural gas and multi-utilities. | |

| A portfolio of high-BE/ME utilities | High BE/ME stocks are value stocks. The market capitalisation of value stocks is equal to or below the book value of equity. The top 30% of BE/ME values in our sample is used as the breakpoint. | |

| A portfolio of mid-BE/ME utilities | Mid BE/ME are neither value nor growth stocks. The market capitalisation of value stocks is almost equal to the book value of equity. This group represents the middle 40% BE/ME values in our sample. | |

| A portfolio of low-BE/ME utilities | Low BE/ME stocks are growth stocks. Growth stocks’ market capitalisation is well above their book value of equity. The bottom 30% of BE/ME values in our sample is used as the breakpoint. | |

| A portfolio of up momentum utilities | Upper-momentum stocks are stocks with the top 30% of average excess returns calculated over the formation period from day t − 251 to day t − 21 and exclude the sort month. This is commonly known as a portfolio of winners. | |

| A portfolio of neutral momentum utilities | Neutral-momentum stocks are stocks with the middle 40% average excess returns calculated over the formation period from day t − 251 to day t − 21 and exclude the sort month. | |

| A portfolio of down momentum utilities | Down-momentum stocks are stocks with the bottom 30% of average excess returns calculated over the formation period from day t − 251 to day t − 21 and exclude the sort month. This is commonly known as a portfolio of losers. | |

| A portfolio of electricity utilities | A portfolio of stocks where electric utilities operations are defined as the primary revenue source. | |

| A portfolio of natural gas utilities | A portfolio of stocks where natural gas operations are defined as the primary revenue source. | |

| A portfolio of multi utilities | A portfolio of stocks where multi-utility, or combined utility services, are defined as the primary revenue source. | |

| A portfolio of small utilities | A portfolio of stocks where market capitalisation was below the median sample market capitalisation | |

| A portfolio of big utilities | A portfolio of stocks where market capitalisation was above the median sample market capitalisation. | |

| A market factor | The STOXX® 600 Europe Index is used as a proxy for broad market returns. | |

| A global size factor | The global SMB factor is calculated as the daily difference between the arithmetic average return of the three small portfolios (S/L, S/M and S/H) minus the arithmetic average return of the three big portfolios (B/L, B/M and B/H). The global risk factors are calculated with a universe of 600 European companies across various sectors. | |

| A global value factor | The global HML factor is calculated as the daily difference between the arithmetic average of the two high-BE/ME portfolios (S/H and B/H) minus the arithmetic average of the two low-BE/ME portfolios (S/L and B/L). The global risk factors are calculated using 600 European companies across various sectors. | |

| A global momentum factor | The global UMD factor is calculated as the daily difference between the returns of the upper momentum and down momentum portfolios. The global risk factors are calculated using 600 European companies across various sectors. | |

| A local size factor | The local SMB factor is calculated as the daily difference between the arithmetic average return of the three small portfolios (S/L, S/M and S/H) minus the arithmetic average return of the three big portfolios (B/L, B/M and B/H). The global risk factors are calculated using 600 European companies across various sectors. | |

| A local value factor | The local HML factor is calculated as the daily difference between the arithmetic average of the two high-BE/ME portfolios (S/H and B/H) minus the arithmetic average of the two low-BE/ME portfolios (S/L and B/L). The global risk factors are calculated using our sample of 91 European energy utilities. | |

| A local momentum factor | The local UMD factor is calculated as the daily difference between the returns of the up-momentum and down-momentum portfolios. The global risk factors are calculated using our sample of 91 European energy utilities. | |

| Term premium | Term premium is calculated as the difference between the daily yields on the three- and one-month UK Treasury bills. | |

| Return on oil prices | London Brent Crude Oil Index proxies for oil price, sourced from the Intercontinental Exchange (ICE). | |

| Return on coal prices | Coal price is measured using a European-specific steam (thermal) coal index for power and heat generation, sourced from the Hamburg Institute of International Economics (HWWI). | |

| Return on gas prices | Natural gas price is measured using the one-month forward index, also sourced from the ICE. | |

| Return on carbon prices | Carbon allowance prices, measured as the price (in euros) per EUA, are sourced from the ICE European Climate Exchange (ECX). |

References

- Alford, Andrew W., Jennifer J. Jones, and Mark E. Zmijewski. 1994. Extensions and violations of the statutory SEC form 10-K filing requirements. Journal of Accounting and Economics 17: 229–54. [Google Scholar] [CrossRef]

- Bai, Jushan, and Pierre Perron. 1998. Estimating and Testing Linear Models with Multiple Structural Changes. Econometrica 66: 47–78. [Google Scholar] [CrossRef]

- Bai, Jushan, and Pierre Perron. 2003. Computation and Analysis of Multiple Structural Change Models. Journal of Applied Econometrics 18: 1–22. [Google Scholar] [CrossRef]

- Batten, Jonathan A., Harald Kinateder, Peter G. Szilagyi, and Niklas F. Wagner. 2017. Can stock market investors hedge energy risk? Evidence from Asia. Energy Economics 66: 559–70. [Google Scholar] [CrossRef]

- Bellman, Richard, and Robert Roth. 1969. Curve Fitting by Segmented Straight Lines. Journal of the American Statistical Association 64: 1079–84. [Google Scholar] [CrossRef]

- Boni, Leslie, and Kent L. Womack. 2006. Analysts, Industries, and Price Momentum. Journal of Financial and Quantitative Analysis 41: 85–109. [Google Scholar] [CrossRef]

- Carhart, Mark M. 1997. On Persistence in Mutual Fund Performance. The Journal of Finance 52: 57–82. [Google Scholar] [CrossRef]

- Chan, Kevin C., Nai-fu Chen, and David A. Hsieh. 1985. An Exploratory Investigation of the Firm Size Effect. Journal of Financial Economics 14: 451–71. [Google Scholar] [CrossRef]

- Chan, Louis K. C., Yasushi Hamao, and Josef Lakonishok. 1991. Fundamentals and Stock Returns in Japan. The Journal of Finance 46: 1739–64. [Google Scholar] [CrossRef]

- Conover, C. Mitchell, Robert E. Miller, and Andrew Szakmary. 2008. The timeliness of accounting disclosures in international security markets. International Review of Financial Analysis 17: 849–69. [Google Scholar] [CrossRef]

- Dickey, David A., and Wayne A. Fuller. 1979. Distribution of the Estimators for Autoregressive Time Series with a Unit Root. Journal of the American Statistical Association 74: 427–31. [Google Scholar] [CrossRef]

- El-Sharif, Idris, Dick Brown, Bruce Burton, Bill Nixon, and Alex Russell. 2005. Evidence on the Nature and Extent of the Relationship between Oil Prices and Equity Values in the UK. Energy Economics 27: 819–30. [Google Scholar] [CrossRef]

- Faff, Robert W., and Timothy J. Brailsford. 1999. Oil Price Risk and the Australian Stock Market. Journal of Energy Finance & Development 4: 69–87. [Google Scholar] [CrossRef]

- Fama, Eugene F., and Kenneth R. French. 1992. The Cross-section of Expected Stock Returns. The Journal of Finance 47: 427–65. [Google Scholar] [CrossRef]

- Fama, Eugene F., and Kenneth R. French. 1993. Common Risk Factors in the Returns on Stocks and Bonds. Journal of Financial Economics 33: 3–56. [Google Scholar] [CrossRef]

- Fama, Eugene F., and Kenneth R. French. 1995. Size and Book-to-market Factors in Earnings and Returns. The Journal of Finance 50: 131–55. [Google Scholar] [CrossRef]

- Fama, Eugene F., and Kenneth R. French. 1997. Industry Costs of Equity. Journal of Financial Economics 43: 153–93. [Google Scholar] [CrossRef]

- Fama, Eugene F., and Kenneth R. French. 1998. Value versus Growth: The International Evidence. The Journal of Finance 53: 1975–99. [Google Scholar] [CrossRef]

- Fama, Eugene F., and Kenneth R. French. 2006. The Value Premium and the CAPM. The Journal of Finance 61: 2163–85. [Google Scholar] [CrossRef]

- Fama, Eugene F., and Kenneth R. French. 2012. Size, Value, and Momentum in International Stock Returns. Journal of Financial Economics 105: 457–72. [Google Scholar] [CrossRef]

- Fama, Eugene F., and Kenneth R. French. 2015. A five-factor asset pricing model. Journal of Financial Economics 116: 1–22. [Google Scholar] [CrossRef]

- Fisher, Walter D. 1958. On Grouping for Maximum Homogeneity. Journal of the American Statistical Association 53: 789–98. [Google Scholar] [CrossRef]

- French, Kenneth R. 2015. Data Library. Available online: http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html (accessed on 20 December 2015).

- Guthery, Scott B. 1974. Partition Regression. Journal of the American Statistical Association 69: 945–47. [Google Scholar] [CrossRef]

- Hansen, Bruce E. 2001. The New Econometrics of Structural Change: Dating Breaks in U.S. Labor Productivity. The Journal of Economic Perspectives 15: 117–28. [Google Scholar] [CrossRef]

- Jamasb, Tooraj, and Michael Pollitt. 2005. Electricity Market Reform in the European Union: Review of Progress toward Liberalization & Integration. The Energy Journal 26: 11–41. [Google Scholar] [CrossRef]

- Koch, Nicolas, and Alexander Bassen. 2013. Valuing the Carbon Exposure of European Utilities. The Role of Fuel Mix, Permit Allocation and Replacement Investments. Energy Economics 36: 431–43. [Google Scholar] [CrossRef]

- Kumar, Alok. 2009. Hard-to-Value Stocks, Behavioral Biases, and Informed Trading. Journal of Financial and Quantitative Analysis 44: 1375–401. [Google Scholar] [CrossRef]

- Mollick, André Varella, and Tibebe Abebe Assefa. 2013. US stock returns and oil prices: The tale from daily data and the 2008–2009 financial crisis. Energy Economics 36: 1–18. [Google Scholar] [CrossRef]

- Moskowitz, Tobias J., and Mark Grinblatt. 1999. Do Industries Explain Momentum? The Journal of Finance 54: 1249–90. [Google Scholar] [CrossRef]

- Newey, Whitney K., and Kenneth D. West. 1987. A Simple, Positive Semi-Definite, Heteroskedasticity and Autocorrelation Consistent Covariance Matrix. Econometrica 55: 703–8. [Google Scholar] [CrossRef]

- Oberndorfer, Ulrich. 2009. Energy Prices, Volatility, and the Stock Market: Evidence from the Eurozone. Energy Policy 37: 5787–95. [Google Scholar] [CrossRef]

- Quandt, Richard E. 1960. Tests of the Hypothesis That a Linear Regression System Obeys Two Separate Regimes. Journal of the American Statistical Association 55: 324–30. [Google Scholar] [CrossRef]

- Rosenberg, Barr, Kenneth Reid, and Ronald Lanstein. 1985. Persuasive Evidence of Market Inefficiency. The Journal of Portfolio Management 11: 9–16. [Google Scholar] [CrossRef]

- Sadorsky, Perry. 2001. Risk Factors in Stock Returns of Canadian Oil and Gas Companies. Energy Economics 23: 17–28. [Google Scholar] [CrossRef]

- Sarwar, Golam, Cesario Mateus, and Natasa Todorovic. 2018. US sector rotation with five-factor Fama–French alphas. Journal of Asset Management 19: 116–32. [Google Scholar] [CrossRef]

- Silvapulle, Param, Russell Smyth, Xibin Zhang, and Jean-Pierre Fenech. 2017. Nonparametric panel data model for crude oil and stock market prices in net oil importing countries. Energy Economics 67: 255–67. [Google Scholar] [CrossRef]

- Smyth, Russell, and Paresh Kumar Narayan. 2018. What do we know about oil prices and stock returns? International Review of Financial Analysis 57: 148–56. [Google Scholar] [CrossRef]

- The Economist. 2013. How to Lose Half a Trillion Euros. The Economist, October 15. [Google Scholar]

- Tulloch, Daniel J., Ivan Diaz-Rainey, and Inguruwatt M. Premachandra. 2017a. The Impact of Liberalization and Environmental Policy on the Financial Returns of European Energy Utilities. The Energy Journal 38: 77–106. [Google Scholar] [CrossRef]

- Tulloch, Daniel J., Ivan Diaz-Rainey, and Inguruwatt M. Premachandra. 2017b. The Impact of Regulatory Change on EU Energy Utility Returns: The Three Liberalization Packages. Applied Economics 50: 957–72. [Google Scholar] [CrossRef]

| 1 | This paper is part of a wider research project which includes Tulloch et al. (2017a) and Tulloch et al. (2017b). Tulloch et al. (2017a) is a direct precursor to this paper, as it implements the global AFFM to make comparisons across sectors and relies on deductive structural breaks. Tulloch et al. (2017b) use an event-study approach to explore the effect of various policy reforms on the returns of the energy sector as a whole. The focus in this paper is a more nuanced understanding of sector-level returns, using subcategories of energy utilities, local risk factors, and time-varying risk factor sensitivities, and isolating the firm-specific component of return. This paper is distinct yet complementary to Tulloch et al. (2017a) and Tulloch et al. (2017b). |

| 2 | For brevity, we denote all excess returns over the one-month UK treasury bill in bold; simple returns are nonbold. |

| 3 | Term premium represents borrowing costs and is calculated as the spread between the yields of a three- and one-month treasury bill. Term premium represents the risk-free short-term discount rate and an indicator of the present state of the economy, which tends to be lower during economic downturn and higher in times of growth (Sadorsky 2001). |

| 4 | The European Union Emissions Trading Scheme was established in 2005, meaning the annual conditional regressions can only examine the impact of carbon prices in the latter years. |

| 5 | The underlying dataset used in this paper is similar to that used in [author identifying citation] with some additions: namely, the use of multiple sector-level portfolios. |

| 6 | Note, Tulloch et al. (2017b) use weekly stock market data. The results are substantively the same. |

| 7 | This is a key requirement of Fama and French (1993), where the premia of size and value are argued to be buried within the market factor. Thus, we must isolate our size and value factors from the sample of companies, which proxy for the market factor. |

| 8 | Groups include the European Distribution System Operators’ Association (EDSO), ENTSO-E, Gas Infrastructure Europe (GIE), Gas Transmission Europe (GTE), Gas Storage Europe (GSE), Gas LNG Europe (GLE), ENTSO-G, and Eurogas. |

| 9 | To ensure the accounting variables predate the returns they are used to explain, the accounting data for fiscal year t − 1 are matched with the returns for July of year t to June of t + 1 (Fama and French 1992). This six-month lag is based on research by Alford et al. (1994) and Conover et al. (2008) regarding the lag between the fiscal year-end and the publication of annual reports. |

| 10 | Due to the significant data omissions for 2014, 2013 was the most comprehensive end date possible, and, therefore, also determined the end date of the analysis. |

| 11 | Matching SICs of year to returns of year t only made minor differences to the cumulative returns of the natural gas and multi-utility portfolios. The overall trend of the three portfolios did not change. |

| 12 | Note, three alternative lag structures were also tested but made no difference to estimates: (1) no lag specification, (2) Schwarz information criterion and (3) Hannan-Quinn Information Criterion. |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| N | 4435 | 4435 | 4435 | 4435 | 4435 | 4435 | 4435 | 4435 | 4435 | 4435 | 4435 | 4435 |

| Mean | −0.0051% | 0.0102% | −0.0027% | −0.0131% | 0.0291% | 0.0095% | −0.0022% | 0.0136% | 0.0127% | 0.0006% | 0.0155% | −0.0062% |

| t-Mean | (−0.30) | (0.53) | (−0.15) | (−0.80) | (2.85) *** | (0.56) | (−0.16) | (0.81) | (0.58) | (0.03) | (1.12) | (−0.36) |

| Std. Dev. Daily | 1.11% | 1.29% | 1.23% | 1.09% | 0.67% | 1.14% | 0.90% | 1.10% | 1.49% | 1.20% | 0.89% | 1.15% |

| Mean Annualised | −1.32% | 2.69% | −0.70% | −3.35% | 7.86% | 2.50% | −0.57% | 3.60% | 3.36% | 0.16% | 4.11% | −1.60% |

| Min | −8.10% | −9.53% | −8.29% | −8.34% | −5.48% | −8.46% | −7.98% | −9.49% | −10.48% | −9.80% | −10.53% | −8.45% |

| Max | 13.60% | 8.04% | 14.38% | 13.22% | 6.85% | 14.70% | 5.83% | 13.00% | 12.96% | 16.13% | 7.71% | 14.09% |

| Skew | 0.09 | −0.43 | 0.15 | 0.11 | 0.53 | 0.24 | −0.58 | 0.03 | 0.20 | 0.20 | −0.86 | 0.12 |

| Kurt | 14.80 | 8.85 | 12.93 | 15.03 | 14.70 | 15.49 | 14.63 | 16.51 | 10.18 | 15.68 | 14.36 | 15.06 |

| Mean Market Cap. | 7869.25 | 3383.21 | 12,722.44 | 11,599.21 | 7318.08 | 11,553.89 | 9208.67 | 6381.02 | 14,954.77 | 13,489.90 | 1201.88 | 17,696.09 |

| Mean Book Value | 5134.55 | 3831.36 | 7482.48 | 3661.81 | 3730.04 | 6315.23 | 5253.09 | 6469.90 | 2747.28 | 2693.20 | 1046.02 | 9266.01 |

| BE/ME Ratio | 0.65 | 1.13 | 0.59 | 0.32 | 0.51 | 0.55 | 0.57 | 1.01 | 0.18 | 0.20 | 0.87 | 0.52 |

| Median companies | 45.5 | 13 | 18 | 13.5 | 13 | 18 | 13 | 24 | 7 | 14 | 22.5 | 22.5 |

| N | 4435 | 4435 | 4435 | 4435 | 4435 | 4435 | 4435 | 4435 | 4435 | 4435 | 4435 | 2135 |

| Mean | 0.0036% | 0.0252% | 0.0017% | 0.0312% | 0.0309% | 0.0184% | 0.0313% | 0.0262% | 0.0383% | 0.0158% | 0.0424% | −0.4233% |

| t-Mean | (0.19) | (3.06) *** | (0.18) | (1.81) * | (2.50) ** | (1.18) | (2.04) ** | (7.90) **** | (1.32) | (0.78) | (0.74) | (−2.64) *** |

| Std. Dev. Daily | 1.26% | 0.55% | 0.62% | 1.15% | 0.85% | 1.06% | 1.01% | 0.16% | 1.78% | 1.36% | 3.73% | 7.42% |

| Mean Annualised | 0.94% | 6.78% | 0.43% | 8.45% | 8.35% | 4.91% | 8.48% | 7.05% | 10.47% | 4.19% | 11.65% | −66.81% |

| Min | −7.94% | −3.47% | −7.29% | −7.27% | −6.46% | −9.42% | −5.68% | −0.71% | −11.35% | −16.08% | −28.13% | −138.63% |

| Max | 9.40% | 4.68% | 4.29% | 7.55% | 4.94% | 8.00% | 7.49% | 0.36% | 12.56% | 19.78% | 47.77% | 109.86% |

| Skew | −0.17 | −0.29 | −0.07 | −0.48 | −0.13 | −0.15 | 0.43 | −1.06 | −0.27 | 0.80 | 2.58 | −3.14 |

| Kurt | 7.96 | 7.21 | 11.19 | 7.72 | 5.71 | 9.07 | 10.19 | 4.74 | 6.17 | 38.75 | 28.85 | 121.76 |

| Mean Market Cap. | ||||||||||||

| Mean Book Value | ||||||||||||

| BE/ME Ratio |

| Portfolio | Model | Sig. | Mean VIF | Heterosked. | Autocorr. | |||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Energy Sector | 1 | −0.0001 | 0.7218 | **** | 0.6696 | 1852.86 | **** | 1.00 | 84.95 | **** | 33.98 | **** | ||||||||||||||

| 2 | −0.0001 | 0.7227 | **** | −0.0017 | 0.0109 | −0.0371 | **** | 0.0020 | 0.6717 | 486.99 | **** | 1.00 | 73.23 | **** | 31.46 | **** | ||||||||||

| 3 | 0.0001 | 0.6298 | **** | −0.2964 | **** | −0.0975 | **** | −0.0673 | *** | 0.7256 | 1105.38 | **** | 1.12 | 88.34 | **** | 34.17 | **** | |||||||||

| 4 | 0.0001 | 0.6306 | **** | −0.2975 | **** | −0.0973 | **** | −0.0661 | **** | −0.0430 | 0.0103 | −0.0370 | **** | 0.0028 | 0.7277 | 579.51 | **** | 1.06 | 79.29 | **** | 30.14 | **** | ||||

| Energy Sector | 5 | −0.0001 | 0.6896 | **** | −0.1369 | **** | 0.2368 | **** | 0.0512 | **** | −0.0117 | 0.0113 | −0.0323 | *** | 0.0019 | 0.6879 | 347.80 | **** | 1.14 | 70.28 | **** | 23.27 | **** | |||

| Big utilities | 4 | 0.0001 | 0.6400 | **** | −0.3442 | **** | −0.1107 | **** | −0.0679 | *** | −0.0430 | 0.0098 | −0.0383 | **** | 0.0028 | 0.7357 | 594.18 | **** | 1.06 | 84.80 | **** | 28.86 | **** | |||

| Small utilities | 4 | 0.0000 | 0.4940 | **** | 0.4271 | **** | 0.1015 | **** | −0.0388 | ** | −0.0329 | 0.0122 | * | −0.0266 | *** | 0.0023 | 0.4468 | 194.94 | **** | 1.06 | 32.18 | **** | 28.15 | **** | ||

| High-BE/ME (value) | 4 | 0.0001 | 0.4535 | **** | −0.3287 | **** | 0.6503 | **** | −0.0442 | * | −0.0256 | 0.0203 | ** | −0.0311 | ** | 0.0053 | * | 0.6081 | 269.88 | **** | 1.06 | 113.44 | **** | 8.56 | *** | |

| Mid-BE/ME (neutral) | 4 | 0.0001 | 0.6887 | **** | −0.3020 | **** | −0.0804 | **** | −0.0648 | *** | −0.0825 | 0.0021 | −0.0437 | **** | 0.0026 | 0.6859 | 514.33 | **** | 1.06 | 79.78 | **** | 9.40 | *** | |||

| Low-BE/ME (growth) | 4 | 0.0000 | 0.5255 | **** | −0.2934 | **** | −0.2866 | **** | −0.0765 | **** | −0.0012 | 0.0188 | *** | −0.0197 | * | 0.0034 | 0.6398 | 308.26 | **** | 1.06 | 46.43 | **** | 11.35 | **** | ||

| Up momentum | 4 | 0.0002 | *** | 0.2919 | **** | −0.1204 | **** | −0.0338 | **** | 0.4308 | **** | −0.0144 | 0.0142 | **** | −0.0068 | 0.0030 | * | 0.5920 | 233.31 | **** | 1.06 | 78.27 | **** | 14.02 | **** | |

| Neutral momentum | 4 | 0.0002 | * | 0.5973 | **** | −0.3069 | **** | −0.0927 | **** | −0.0137 | −0.0273 | 0.0043 | −0.0448 | **** | 0.0061 | ** | 0.6129 | 301.30 | **** | 1.06 | 77.32 | **** | 17.75 | **** | ||

| Down momentum | 4 | 0.0002 | *** | 0.2919 | **** | −0.1204 | **** | −0.0338 | **** | −0.5692 | **** | −0.0144 | 0.0142 | **** | −0.0068 | 0.0030 | * | 0.7736 | 615.33 | **** | 1.06 | 38.89 | **** | 14.02 | **** | |

| Electricity | 4 | 0.0002 | ** | 0.5798 | **** | −0.1963 | **** | −0.0982 | **** | −0.0715 | *** | −0.0714 | 0.0140 | * | −0.0239 | * | 0.0087 | *** | 0.5805 | 268.04 | **** | 1.06 | 63.61 | **** | 15.36 | **** |

| Natural gas | 4 | 0.0002 | 0.7431 | **** | −0.3186 | **** | −0.1406 | **** | 0.0398 | * | 0.0415 | 0.0318 | *** | −0.0203 | 0.0074 | * | 0.5134 | 281.39 | **** | 1.06 | 69.10 | **** | 3.13 | * | ||

| Multi-utilities | 4 | 0.0002 | 0.5857 | **** | −0.3102 | **** | −0.1381 | **** | −0.0917 | **** | −0.0678 | −0.0044 | −0.0453 | *** | −0.0005 | 0.5775 | 291.09 | **** | 1.06 | 57.67 | **** | 20.04 | **** | |||

- Model 1, CAPM:

- Model 2, augmented-CAPM:

- Model 3, local four-factor model:

- Model 4, local AFFM: (Equation (2))

- Model 5, global AFFM (Equation (1))

| Year | Sig. | ||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1996 A | 0.0000 | 0.5148 | **** | −0.4256 | **** | 0.0776 | * | 0.0748 | 0.5126 | ** | −0.0175 | −0.0392 | −0.0081 | 73.58% | 46.60 | **** | |||||||

| 1997 | 0.0001 | 0.5709 | **** | −0.3323 | **** | 0.0470 | 0.1591 | **** | −0.0679 | 0.0119 | −0.0179 | 0.0076 | 80.27% | 133.24 | **** | ||||||||

| 1998 | 0.0003 | 0.4935 | **** | −0.3486 | **** | 0.0035 | −0.0399 | 0.0576 | 0.0117 | −0.0803 | **** | 0.0003 | 77.83% | 115.07 | **** | ||||||||

| 1999 | −0.0003 | 0.3297 | **** | −0.6388 | **** | 0.0335 | −0.0129 | 0.0299 | −0.0073 | 0.0314 | *** | −0.0015 | 80.79% | 137.68 | **** | ||||||||

| 2000 | 0.0006 | 0.2291 | **** | −0.4463 | **** | −0.0072 | −0.0070 | −0.4484 | 0.0018 | 0.0262 | −0.0015 | 45.83% | 28.39 | **** | |||||||||

| 2001 | 0.0003 | 0.3927 | **** | −0.3747 | **** | −0.0758 | −0.0280 | 0.1708 | 0.0238 | −0.0193 | 0.0055 | 67.36% | 68.08 | **** | |||||||||

| 2002 | 0.0000 | 0.5029 | **** | −0.3191 | **** | 0.0404 | −0.0556 | * | −0.0981 | −0.0297 | 0.0065 | 0.0030 | 84.76% | 181.73 | **** | ||||||||

| 2003 | 0.0004 | * | 0.4696 | **** | −0.3819 | **** | −0.1531 | **** | −0.0923 | ** | 0.2921 | −0.0055 | −0.0718 | ** | −0.0022 | 85.15% | 187.37 | **** | |||||

| 2004 | 0.0008 | **** | 0.5517 | **** | −0.2240 | **** | −0.0610 | * | 0.0703 | 0.0355 | 0.0046 | −0.0245 | 0.0038 | 66.06% | 64.51 | **** | |||||||

| 2005 | 0.0004 | 0.8385 | **** | −0.1151 | *** | −0.0993 | *** | 0.0785 | 0.1272 | −0.0097 | −0.0186 | −0.0005 | 61.90% | 53.59 | **** | ||||||||

| 2006 | 0.0005 | ** | 0.7548 | **** | −0.1295 | **** | −0.0902 | ** | 0.0559 | 0.0948 | 0.0551 | **** | −0.0046 | 0.0021 | 0.0093 | ** | 71.08% | 71.72 | **** | ||||

| 2007 | 0.0006 | * | 0.6208 | **** | −0.2301 | **** | −0.0627 | * | 0.0646 | −0.4056 | 0.0605 | ** | −0.0071 | −0.0042 | 0.0006 | * | 67.23% | 60.27 | **** | ||||

| 2008 | 0.0001 | 0.6559 | **** | −0.4474 | **** | −0.3765 | **** | 0.0034 | 0.1124 | 0.0214 | −0.0517 | ** | 0.0238 | * | −0.0032 | 85.03% | 165.69 | **** | |||||

| 2009 | 0.0002 | 0.5695 | **** | −0.4310 | **** | −0.2592 | **** | −0.0999 | ** | −0.3600 | 0.0186 | 0.0306 | * | −0.0051 | 0.0011 | 78.67% | 107.53 | **** | |||||

| 2010 | −0.0080 | 0.7551 | **** | −0.2447 | **** | −0.1819 | **** | −0.1251 | **** | 4.3887 | 0.0410 | ** | −0.0460 | ** | 0.0064 | −0.0084 | 85.34% | 169.15 | **** | ||||

| 2011 | 0.0000 | 0.8207 | **** | −0.3054 | **** | 0.0723 | −0.0682 | * | −0.1636 | 0.0237 | −0.0093 | 0.0073 | 0.0064 | 84.06% | 152.74 | **** | |||||||

| 2012 | 0.0000 | 0.7282 | **** | −0.1719 | **** | 0.1762 | **** | −0.1989 | **** | −0.1061 | −0.0176 | −0.0192 | −0.0164 | 0.0114 | 74.35% | 84.75 | **** | ||||||

| 2013 A | −0.0020 | 0.7334 | **** | −0.2738 | **** | 0.1586 | *** | −0.1887 | *** | 1.0720 | −0.0368 | −0.0055 | −0.0285 | 0.0043 | 72.04% | 37.65 | **** | ||||||

| Mean: | −0.0003 | 0.5851 | −0.3244 | −0.0421 | −0.0228 | 0.2913 | 0.0083 | −0.0178 | −0.0005 | 0.0027 | 74.52% |

| Break Test | F-Statistic | Scaled F-Statistic | Critical Value ** | Sequential | Repartition |

|---|---|---|---|---|---|

| 0 vs. 1 * | 23.49 | 187.89 | 22.92 | 01/11/2004 | 01/09/1998 |

| 1 vs. 2 * | 15.22 | 121.76 | 25.15 | 01/09/1998 | 30/03/2000 |

| 2 vs. 3 * | 10.73 | 85.83 | 26.38 | 07/07/2010 | 10/09/2001 |

| 3 vs. 4 * | 15.72 | 125.73 | 27.09 | 18/06/2008 | 01/09/2004 |

| 4 vs. 5 * | 8.44 | 67.54 | 27.77 | 18/05/2001 | 25/07/2007 |

| 5 vs. 6 * | 5.03 | 40.21 | 28.15 | 30/03/2000 | 18/06/2008 |

| 6 vs. 7 * | 4.97 | 39.80 | 28.61 | 28/04/2009 | 28/04/2009 |

| 7 vs. 8 * | 4.34 | 34.69 | 28.90 | 25/07/2007 | 01/02/2011 |

| 8 vs. 9 | 2.82 | 22.59 | 29.19 | Nil | Nil |

| Partition | Start | End | Obs | Sig. | |||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 01/07/1996 | 31/08/1998 | 0.0001 | 0.6084 | **** | −0.2877 | **** | 0.0262 | 0.1097 | **** | 0.1037 | −0.0038 | −0.0339 | ** | 0.0035 | 566 | 0.8042 | 228.59 | **** | ||||

| 2 | 01/09/1998 | 29/03/2000 | 0.0001 | 0.3011 | **** | −0.6225 | **** | 0.0905 | ** | −0.0423 | 0.0194 | −0.0109 | 0.0070 | 0.0058 | 412 | ||||||||

| 3 | 30/03/2000 | 07/09/2001 | 0.0003 | 0.2759 | **** | −0.3497 | **** | −0.0849 | ** | 0.0727 | * | 0.0493 | 0.0159 | 0.0078 | −0.0076 | 377 | |||||||

| 4 | 10/09/2001 | 31/08/2004 | 0.0001 | 0.4956 | **** | −0.3391 | **** | −0.0416 | * | −0.0784 | **** | 0.3948 | *** | −0.0109 | −0.0301 | ** | 0.0019 | 777 | |||||

| 5 | 01/09/2004 | 24/07/2007 | 0.0004 | *** | 0.7495 | **** | −0.1390 | **** | −0.0705 | **** | 0.0655 | ** | 0.0506 | 0.0218 | ** | −0.0088 | 0.0028 | 755 | |||||

| 6 | 25/07/2007 | 17/06/2008 | 0.0007 | 0.6502 | **** | −0.3026 | *** | −0.0187 | 0.0828 | * | 0.3420 | 0.1284 | *** | −0.0215 | −0.0004 | 235 | |||||||

| 7 | 18/06/2008 | 27/04/2009 | −0.0010 | 0.5448 | **** | −0.4062 | **** | −0.5345 | **** | −0.0088 | 0.5015 | 0.0004 | −0.0331 | * | 0.0093 | 224 | |||||||

| 8 | 28/04/2009 | 31/01/2011 | −0.0010 | 0.6914 | **** | −0.2985 | **** | −0.1402 | **** | −0.1297 | **** | 0.4890 | 0.0094 | −0.0288 | ** | −0.0088 | 460 | ||||||

| 9 | 01/02/2011 | 28/06/2013 | −0.0001 | 0.7964 | **** | −0.2577 | **** | 0.1394 | **** | −0.1270 | **** | −0.1037 | −0.0063 | −0.0061 | 0.0048 | 629 |

| Method | Partition | Start | End | Sig. | Sig. | |||

|---|---|---|---|---|---|---|---|---|

| (1) Unconditional regression | 1 | 01/07/1996 | 29/10/2003 | 0.0000 | 0.61% | 13.69 | **** | |

| 2 | 30/10/2003 | 09/06/2008 | 0.0006 | **** | ||||

| 3 | 10/06/2008 | 28/06/2013 | −0.0006 | *** | ||||

| (2) Conditional annual regressions | 1 | 01/07/1996 | 28/06/2013 | 0.0000 | 00.00% | - | - | |

| (3) Sequential breakpoints | 1 | 01/07/1996 | 28/06/2013 | 0.0000 | 00.00% | - | - |

| Partition | Start | End | Obs | Sig. | ||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 01/07/1996 | 31/08/1998 | 0.0000 | −0.0223 | 0.0097 | 0.1233 | **** | 0.1756 | **** | 0.1037 | −0.0140 | 0.0032 | 0.0008 | 566 | 27.95% | 22.50 | **** | |||||||

| 2 | 01/09/1998 | 29/03/2000 | 0.0000 | −0.3297 | **** | −0.3251 | **** | 0.1877 | **** | 0.0237 | 0.0194 | −0.0211 | * | 0.0441 | ** | 0.0031 | 412 | |||||||

| 3 | 30/03/2000 | 07/09/2001 | 0.0002 | −0.3549 | **** | −0.0523 | 0.0123 | 0.1387 | **** | 0.0493 | 0.0057 | 0.0449 | * | −0.0104 | 377 | |||||||||

| 4 | 10/09/2001 | 31/08/2004 | 0.0000 | −0.1351 | **** | −0.0417 | 0.0555 | ** | −0.0125 | 0.3948 | *** | −0.0211 | ** | 0.0070 | −0.0008 | 777 | ||||||||

| 5 | 01/09/2004 | 24/07/2007 | 0.0003 | ** | 0.1188 | **** | 0.1584 | **** | 0.0267 | 0.1315 | **** | 0.0506 | 0.0116 | 0.0283 | *** | 0.0000 | 755 | |||||||

| 6 | 25/07/2007 | 17/06/2008 | 0.0006 | 0.0195 | −0.0052 | 0.0784 | 0.1487 | *** | 0.3420 | 0.1182 | *** | 0.0155 | −0.0031 | 235 | ||||||||||

| 7 | 18/06/2008 | 27/04/2009 | −0.0011 | −0.0859 | ** | −0.1089 | −0.4373 | **** | 0.0571 | 0.5015 | −0.0098 | 0.0040 | 0.0066 | 224 | ||||||||||

| 8 | 28/04/2009 | 31/01/2011 | −0.0011 | 0.0607 | ** | −0.0012 | −0.0431 | −0.0638 | ** | 0.4890 | −0.0008 | 0.0083 | −0.0115 | ** | 460 | |||||||||

| 9 | 01/02/2011 | 28/06/2013 | −0.0002 | 0.1657 | **** | 0.0396 | 0.2366 | **** | −0.0611 | ** | −0.1037 | −0.0165 | 0.0310 | ** | 0.0021 | 629 | ||||||||

| Estimated AFFM coefficients extracted from Table 2. | ||||||||||||||||||||||||

| 0.0001 | 0.6306 | **** | −0.2975 | **** | −0.0973 | **** | −0.0661 | **** | −0.0430 | 0.0103 | −0.0370 | **** | 0.0028 | |||||||||||

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tulloch, D.J.; Diaz-Rainey, I.; Premachandra, I.M. Modelling Sector-Level Asset Prices. J. Risk Financial Manag. 2020, 13, 120. https://doi.org/10.3390/jrfm13060120

Tulloch DJ, Diaz-Rainey I, Premachandra IM. Modelling Sector-Level Asset Prices. Journal of Risk and Financial Management. 2020; 13(6):120. https://doi.org/10.3390/jrfm13060120

Chicago/Turabian StyleTulloch, Daniel J., Ivan Diaz-Rainey, and I. M. Premachandra. 2020. "Modelling Sector-Level Asset Prices" Journal of Risk and Financial Management 13, no. 6: 120. https://doi.org/10.3390/jrfm13060120

APA StyleTulloch, D. J., Diaz-Rainey, I., & Premachandra, I. M. (2020). Modelling Sector-Level Asset Prices. Journal of Risk and Financial Management, 13(6), 120. https://doi.org/10.3390/jrfm13060120