1. Introduction

Poverty has long been a major issue of concern among developing and underdeveloped countries. Poverty is defined as a situation in which individuals are unable to meet the bare subsistence such as food, clothing, and shelter, along with the lack of employment, skills, assets and self-esteem, with restricted access to social and economic infrastructure that would ensure maintaining a minimum standard of living (

Okpara 2010). There are several plausible explanations of the prevalence of poverty such as inequality of resource ownership which leads to unequal distribution of income, thus causing poverty or differences in the quality of human resources, which also leads to poverty that may result from differing access to social capital (

Setiawan 2016). Poverty has been the greatest challenge of all time. Therefore, in order to alleviate it, governments across the globe have come up with the idea of financing the poor through banks (

Adeyemi 2008). However, the poor tend to have circumscribed access to banks’ services because of the lack of physical collateral and the cumbersome process of transactions which significantly discourage those with less education to approach banks (

Imai and Azam 2012). This means that to make this idea work, the provision of financial services must be universal, covering all people as shown in the empirical evidence which suggests that an inclusive financial system significantly improves growth, alleviates poverty and provides wider economic opportunities (

Raman 2012).

Several studies have been conducted on the relationship between financial development and growth (

Chistopoulos and Tsionas 2004). The question of whether financial development significantly contributes to poverty reduction persists (

Honohan 2004). A strong correlation was found between economic growth and poverty alleviation in developing countries (

Knowles 2005). The ability of the economy to produce jobs can significantly affect the relationship between economic growth and poverty. Moreover, the sound fiscal policies and social protection can prove beneficial to poverty reduction (

Paci et al. 2004). Mallick’s study (

Mallick 2008) suggested that the availability of credit for businesses must be the key component of monetary policy to combat poverty as a credit provision, especially for agriculture which reduces poverty significantly. However, the high cost unit of small loans is also an impediment for poor households to access bank credits because initial set-up cost is being required by financial intermediations offers, of which poor households cannot afford (

Greenwood and Jovanovic 1990). Poor households are not able to risk their savings and fall further below in income distribution, which is why international aid is greatly involved in micro-financing institutions, which is inherently problematic (

Jeanneney and Kpodar 2011).

Despite literature revealing the positive impacts of financial development on alleviating poverty, income inequality has been on the rise in most countries since the early 1980s (

Seven and Coskun 2016). One of the plausible claims is that there is no universal way to measure or evaluate whether provision of credit is meeting its social goals or not. As a result, banks only focus on easily measured financial outcomes which do not depict the true picture of poverty alleviation (

Copestake et al. 2005). This is because if banks measure the success rate of loans repayment, they then ignore the fact related to how those loans are benefitting poor people socially.

In particular, when the poor are still hungry, there are rare chances that they will use micro-finance for investing in business, which implies that provision of credit by banks is causing more harm than good due to the fact that accumulated debt would lead already poor individuals into further destitution and an unending cycle of debt. Secondly, financial development can only be effective in the alleviation of poverty when banks reach out to the poorest of the poor. For instance, a study conducted on the Vietnam Bank for Social Policies (VBSP) to investigate whether the institution is actually reaching out to the poor or not, shows that only 12% of poor households participated in the program while up to 67% of the participants belonged to non-poor households (

Cuong 2008). Thirdly, provision of micro-credit may lead to polarization between the poor and may even be detrimental for the poorest of the poor in view of the fact that many institutions require individuals to guarantee the return of the full loan amount. This means that as the size of the loan grows, it becomes harder to repay it (

Copestake 2002).

Moreover, despite the extensive bank networks and systems of today, poverty still persists. More than 500 million continue to live in urban slums with close to one billion people in persistent hunger in all regions of the Muslim world (

Ahmed 2004, p. 150). Banks did only a little to bridge the global socio-economic and technological gap; their micro-financing of privileged segments is set for profit-making at the expense of the poor and languishing (

Abu Zahrah 1971, pp. 156–67). Developed countries are doing a shady job of development in developing countries; and, when countries in the third world are largely funded by non-governmental organizations, world banks and international monetary funds that make most of them incur unfathomable amounts of debt, causing more damage to already prevailing conditions of poverty in those countries (

Ahmed 2004, p. 150).

The Islamic tradition is replete with moral, ethical, and legal teaching on wealth generation, development, and distribution. The Qur’an calls for equitable distribution of wealth and resources. Poverty should be eradicated as showcased in the numerous injunctions of voluntary sharing of resources with the poor and needy. This highlights Muslim responsibility on poverty alleviation, support, and integration of the underprivileged into economic and financial empowerment (

Young 2010, pp. 201–23). Justice, compassion, and solidarity towards the poor eases the socio-economic empowerment of the poor and needy. This requires the state, community, and people to commit together to alleviating poverty and helping those without food or healthcare (

Dawwabah 2005, pp. 48–75). The Qur’an (59:7) acknowledges economic disparities among rich and poor and sets the vision, measures, and incentives of its alleviation. The Qur’an, for instance, encourages Muslims to strive towards spiritual and economic empowerment while promoting acquisition and development of wealth. Dependence on others is seen as a form of self-caused demise (

Renneboog et al. 2008, pp. 1723–42). The idea is that one should commit to hard work, diligence, and transparency for wealth search with only a few limitations on how to look for it.

According to the Qur’an, resources should be explored (

Buttle 2007, pp. 1076–88), used and disposed of consistently with justice. In their effort to counter unequal distribution of wealth, both the state and society need to share the responsibility of protecting and providing for the poor through moderate consumption of resources, as well as to assure provision for the under-privileged. The shared responsibility of the state and the community is to ensure effective distribution of wealth. The duty of economic development that is incumbent on the state demands distribution of wealth in accordance with the stipulations of Shari’ah (

Siddiqi 2004, p. 81). The state should initiate programs that support and empower the poor by way of the provision of sustainable employment opportunities. This requires balancing out the rights of the poor to treasury allocation without neglecting the remaining population; others are owed a spiritual and ethical duty of care (

Hassan and Shahid 2010, pp. 309–28). Morally speaking, there is a close relationship between the individual and community in the Muslim society (

Grodach 2011, pp. 300–9). Still, a similar relationship exists between economic and spiritual empowerment and development.

Speaking of the context of economic transactions, God created resources in abundance (

Dunya 2002, pp. 57–82). The Qur’an holds high regard for those who sacrifice their wealth for the poor by way of charity (

sadaqat) or

awqāf (

Zaman 1999, pp. 1–8). It is mandatory to give zakat and recommended charities (

sadaqat) to those in need or less privileged (

Abdel Mohsin 2009, pp. 17–27). Those go in conjunction with cooperating with one another. One needs to be righteous and uphold the principles of fairness while keeping away from fraud and unlawful betting. Individual obligations towards others are reinforced when there is freedom to act in total disregard of self-interest of material wealth and personal well-being (

Zaman 1999, pp. 1–8). In the quest to disregard self-interest, Islamic law appreciates when those are used in the provision to the economic and spiritual advantage of less privileged people.

Spirituality cuts across both, striving to sustain the self in the best way possible and ensuring that poor neighbors are supported to attain self-sustenance. This is essential for socio-economic development since the individuals providing help to neighbors do not look forward to reward or appreciation for what they do (

Klugman 2009, pp. 13–46). Philanthropy echoes a sense of responsibility and makes one consume that which is adequate without wasting resources, especially when others are hungry. The resources God created should not be exhausted excessively at the expense of others who lack them (

Kahf 1998, pp. 2–4). When hard work, labor indulgence and investments are combined with the principle of altruism, then the poor will not be exploited by those with illicit and malicious intentions of domination or economic exploitation (

Kahf 2008, pp. 2–4). On the contrary, the poor will be increasingly exposed to opportunities of development, whether spiritual or socio-economic, and will have fairer chances of growth, empowerment, development, and integration.

Let us, before proceeding further, turn to the fundamental concept of awqāf. Awqāf is an Islamic religious endowment fundamentally set to freeze the proprietorship of assets, as is the case of a voluntary and irrevocable dedication of one’s wealth or a portion of it—in cash or kind (such as a house or a garden), and its disbursement for Shari’ah-compliant projects such as mosques or religious schools. Awqāf helps eradicate poverty while ensuring sustainable support of the poor (

Mishra 2006, pp. 1538–45). The sustainable nature of awqāf finds support in the Qur’an, tradition of the Prophet Muhammad, and Islamic law. Prophet Muhammad is reported to have said that deeds of individuals cease to continue upon death except for those dedicated as charity (

sadaqa), beneficial knowledge or pious children. Awqāf is also characterized with principles like inalienability of the rights of the poor, permanent endurance, and potential to generate income. However, there is a need to gear awqāf towards making income generation and re-generation. More light should be shed on this issue, which can be fulfilled in many different ways (Haji

Mohammad 2015, pp. 37–73).

It follows that responsible resource management proves the care of Muslims not only about their present generation, but also of their posterity (

Dreher 2006, pp. 769–88). Prophet Muhammad established what is known as

habs (endowment) which is economically self-reliant, charitable, and sustainable. Unlike other Islamic institutions such as charity (sadaqa) and religious donations or compensations (

kaffarah), awqāf remains perpetually charitable (

Obaidullah 2007, p. 3) because it is not subject to revocation or transfer. Awqāf can also generate its own income and fund charitable activities of the poor and underprivileged. Awqāf institutions can be presented in different ways, including cash and real estate (

Barizah Abu Bakar et al. 2005).

Earlier literature on the financial dimensions of awqāf institutions has focused largely on the way the religious nature of awqāf resulted in successful financial development of awqāf properties and related initiated investments are initiated (

Siddiqi 2004, p. 81). In the 19th Century and after, many political conflicts in the Muslim nations caused serious deterrence for awqāf. Cash awqāf was not very predominant and the real estate awqāf took all the limelight (

Barizah Abu Bakar et al. 2005). Issues of profit-making properties remain generally lacking. Only a few have delved into issues of funding of awqāf institutions, portraying it as a lending and benevolent institution. Most characterize awqāf as an institution set to counter the influence of the conventional financial institutions but which had inadequate assets to enable it to overcome the challenges that it was due to face (

Amin et al. 2003, pp. 59–82). There exist, however, several avenues to address such an information deficit, including, for example, the development of original awqāf practice of socio-economic empowerment by way of improving maximum wealth creation (

Mohammad 2011a, p. 381). This would ensure that awqāf funds, or other funds collected by the bank, are used for obtaining additional property and funds, which would be used again for favorable micro-financing programs for less privileged people who cannot afford the bank charges on financial lending.

Despite the growing literature on the awqāf, finance and the economy, and on how the awqāf impacts socio-economic development, the discussion of the establishment of a awqāf bank that would effectively manage awqāf capital while microfinancing the poor segment and contributing to the overall development of society still needs more focus and attention. This is crucial as it places the awqāf discourse on a much more practical platform, touching not only upon the different aspects and experiences of financing, banking, and development, but also upon the very criteria of a Shari’ah- compliant awqāf bank today.

This research discusses the rationale, vision, and relevance of a Shari’ah-compliant awqāf bank, in addition to relevant issues including the legality of a cash awqāf (awqāf naqdi). This study first provides some basic definitions of the awqāf and social banks. It also addresses questions of bank management and structures such as Shari’ah compliance, service rendering, investment and awqāf distribution, as well as how to provide interest-free and affordable loans to the poor and lower income demographics and empowerment of beneficiaries in need, poverty eradication, removing socio-economic inequalities while honoring the conditions and stipulations of endowers (waqifs) and contributing to overall national development and economic growth.

The current research is important not only to the theoretical field of awqāf studies, but also to new fields and issues of awqāf, banking and finance, digitization, greening, and, more importantly, to the core impact of awqāf on bettering human lives and the world. Much of the discussion around the Shari’ah awqāf bank touches on areas of fiqh innovation, creativity, and ijtihad. However, it would remain critical to advancing our understanding of the ways and means of helping the poor, needy and underprivileged, and also of the sustainable strategies that would secure and develop the awqāf capita while changing the lives of people and their environments for the better.

2. Awqāf Institutions and Social Banks

Institution of awqāf can be described as charity profit-making organizations with great potential power of community empowerment and nation building. They may appear as privately-owned financial institutions, social banking institutions, income-generating institutions, and institutions interested in charity activities and the redistribution of wealth (

Ahmed 2004, p. 150). Moreover, they have various objectives and respective challenges such as being under-financed or being short-lived because of the unfavorable conditions of poverty without financial aid from other organizations (

Arnawut 2005, pp. 3–20). Social banks, on the other hand, represent non-profit organizations dedicated to socio-economic welfare. Islamic social banks seek to alleviate poverty while contributing to the community’s economic development and upbringing of micro-finance institutions against poverty (

Ammar 2006, pp. 11–19).

In the context of the Muslim world, increased attention is given to poverty alleviation. There are also ongoing evaluations of the contributions and effects of awqāf on the sustainability of socio-economic development. However, the challenge of how to systematically eradicate poverty persists. This, however, requires investment in all possible anti-poverty financial measures, and more importantly, perhaps in establishment of the awqāf bank, with characteristics that are acceptable to the culture and religious affiliations of the community alongside checking the ways according to which awqāf would achieve its goals effectively (

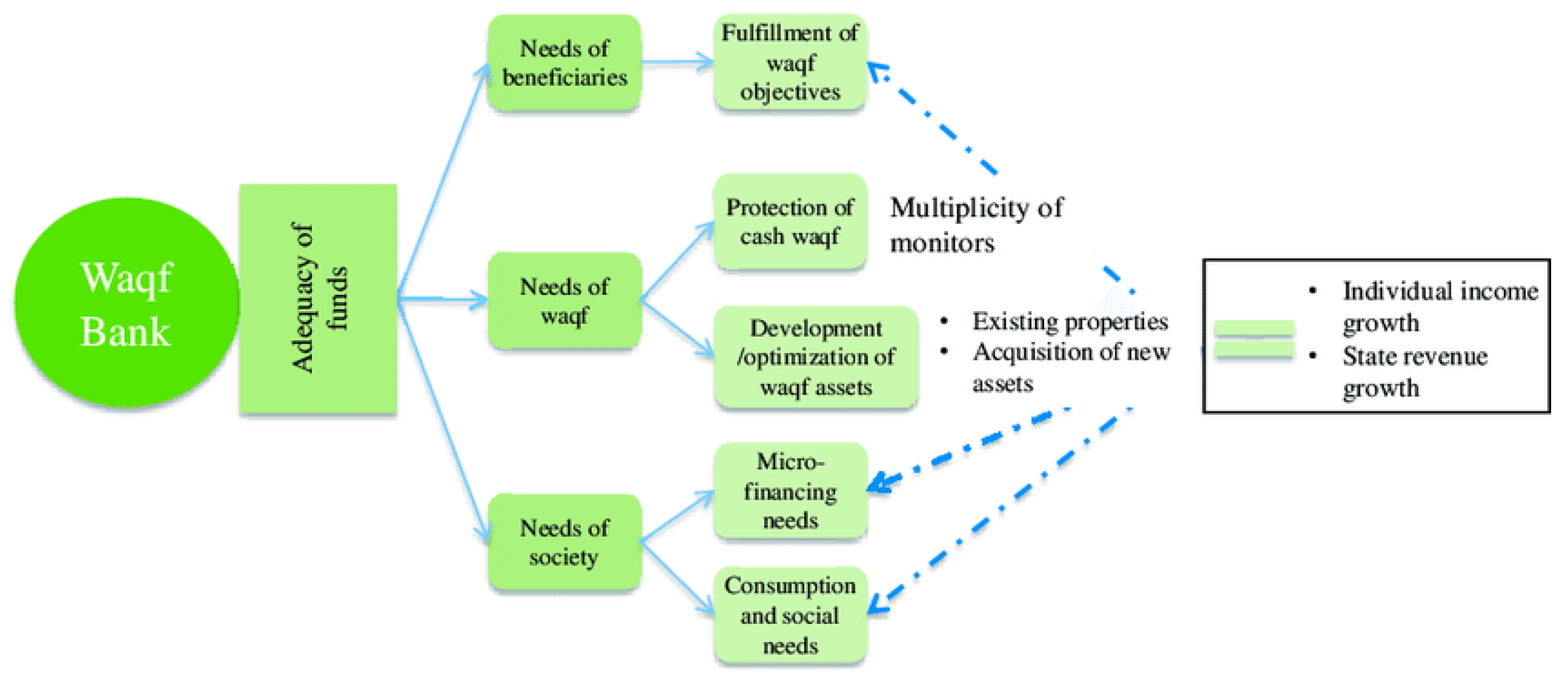

Cizakca 2004, pp. 40–59). Unlike conventional banks and indigenous awqāf financial institutions, however, awqāf institutions provide an alternative financial structure as shown

Figure 1 and amalgamates and also consolidates the properties of both institutions and sets them in one single package (

Vakulabharanam 2005, pp. 971–97). This is to be held in the best interests of all parties in the Muslim community; whether un-bankable or more privileged, which as

Mohammad (

2015, pp. 37–73). Noted, renders it in the best interest of the poor.

According to the current financial model, income generating operations largely target wealthy and privileged segments and do not embrace micro-financing models in countries like Yemen, Bangladesh, and England inter alia (

Ammar 2006, pp. 11–19). The model of finance applied in those countries tends to be more conventional and the few current awqāf social financial institutions major on profit making initiatives to finance their charitable activities. In countries like Bangladesh for instance, only a part of the bank deals with awqāf (

Young 2010, pp. 201–23). Still, that part does not use the gained funds to supply awqāf-based charitable activities; on the opposite, it provides the bank with financial funding, which fails to extend any financial help to the poor; and as profit-making institution, it is only concerned with profit maximization, however, in the name of a social awqāf institution, as is the case of the Islamic Social Bank in Bangladesh or the Vakif Bank in Turkey (

Zarqa 1994, pp. 55–62).

With regards to the Islamic social banks making profits out of earnings of the services offered by the bank, which are set to finance social welfare activities and especially micro-financing, indigenous awqāf financing institutions are based on pure charity or organizations with no prospect of making profits. They are also conducted according to awqāf fundamental principles, rules, and values and would resemble other financial institutions in need of funding, however, remain different from conventional banks. Their lending would be advantageous to individuals, parties, or institutions, Muslims, and others alike. They would also be different in many aspects of social banking systems (

Abu Zahrah 1971, pp. 156–67).

In spite of the several inherent yet fundamental distinctions, there exists, in England, for example, banks that masquerade as awqāf institutions, with their own forms of operation through which they would obtain and use funds to provide interest-based loans for the poor and underprivileged that would otherwise lack collaterals and securities to make them eligible for loans. Their particular feature however, is that the parties providing funds must not be parties interested in achieving charitable objectives, but, on the contrary, parties which are after a conventional means to an end (

Zarqa 1994, pp. 55–62). The probable notion is that the bank is generally any other conventional bank. The bank, in turn, uses their earnings from those financial relationships to finance their charitable activities; that is, provision of unsecured loans to the poor and unprivileged in the Muslim communities, as is the case with the Charity Bank of England and the England’s Industrial Common Ownership Finance Ltd (ICOF). Their focus is on social banking and activities pertaining to the poor in a bid to bridge the large gap among rich and poor in the Muslim community. Those very activities have been influenced by the awqāf incessant and persistent bid to alleviate poverty in most Muslim countries.

However, in view of the inherent inter-connection of awqāf with the Muslim belief, spirituality, morality, and law, one would assume that awqāf operations would only be appealing in religious and faith-based contexts. Having said that, one should note that there exists still a gross disparity in the execution of awqāf initiatives related in most to the fact that the effectiveness of awqāf operations is largely connected with the development index and socio-economic levels, as it would be much easier, for instance, to implement awqāf resolutions, applications or solutions in countries like the United Arab Emirates and Kuwait, and extremely difficult in others like India, Pakistan or Iraq. In countries like Somalia, for instance, economic disparity is predominant, especially with the ongoing political conflicts and instability, making it impossible to implement the initiatives of awqāf financial institutions (

Mohammad 2011b, pp. 250–54).

3. Cash Awqāf in Islamic Law

Awqāf banks are the next step up from cash-based Awqāf, the latter being a natural consideration once the cash system is acknowledged by a Muslim community (

Arnawut 2005, pp. 3–20). Awqāf bank are subject to Islamic law, which covers various issues such as capital generation, management and even ownership. However, awqāf represent a controversial issue among Muslim scholars despite potentially being one of the best modes of sustainable profit generation. This reluctance is largely because the idea of a cash-based awqāf is not explicitly addressed cash awqāf in the primary sources of Islamic law (

Renneboog et al. 2008, pp. 1723–42). Some jurists have considered it permissible through legal analogy as is the case with many other legal issues. Some have accepted it, by considering cash for cash awqāf as a movable property in that early Qur’anic notions were largely more concerned with property than a medium of trade (

Roodman and Morduch 2014, pp. 583–604).

More generally, there is no one school of jurisprudence whose jurists agreed unanimously on the prohibition of cash awqāf. The schools with the strongest legal support for cash awqāf are the Maliki and the Hanafis schools. The Hanbalite school adopted a similar stance as shown in the ruling made by its leading jurists Ibn Taymiyyah. The Shafi’i school is perhaps the least favorite in the issue of cash awqāf (

Dunya 2002). Abu Su’ud wrote a treatise on cash awqāf in which he supported the opinion of permissibility based on the principle of juristic preference (

istihsan), transactions of people, and customs. He issued seventy-nine fatwas in favor of cash awqāf investment through Islamic equity-based partnership contract (

mudharabah) (

Abu al-Suud 1997, p. 13). Nevertheless, most Muslim scholars opt for the permissibility of cash awqāf, viewing it as a means of trade and comparable asset (

Mandaville 1979). Their argument is based on the recognition of both the Qur’an and hadith of moveable property. Few jurists however, recognized cash awqāf to procure a loan. Others recognize it in the light of their consideration of awqāf. However, some views in the Shafi’i school of law rejects cash awqāf based on their own legal methodology and juristic interpretations. The validity of the cash awqāf, however, is still accepted, especially when it sustains and derives its own profits and is operated to procure loans and establish investments. For Mandaville, many other schools began to recognize the validity of cash Awqāf, including the Hanafis and the Malikis who hold different justifications for recognizing cash awqāf, such as its ability to influence the establishment of investments (1979).

Contemporary jurists rule in favor of the admissibility and acceptance of cash awqāf for its purposes in investments. They maintain permissibility of cash awqāf in investments of bonds and banks. Some go further to recognize not only currencies, but also liquid assets pertaining to cash awqāf. In 2004, the Islamic Fiqh Academy of the Organization of the Islamic Conference (OIC) authorized the perpetual and temporary cash awqāf in the resolution No 140 (15/6) on investment in awqāf and its yields and rents. The Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) authorized the cash awqāf, stocks, funds and sukuk awqāf in Sharia Standard No 60 (amended), items No. 2/4/13, 2/4/14 and 2/4/15 (

AAOIFI 2019).

According to contemporary Muslim jurists, cash awqāf has numerous advantages including the creation of more opportunities for socio-economic empowerment. It has a very high potential of constantly sustained income generation and regeneration (

Arnawut 2005, pp. 3–20). Cash awqāf has many elements that qualify it to play a significant role in the fulfillment of both the charitable and development mission of awqāf in the most satisfactory fashion. Attention and efforts should then be given to this type of awqāf for its formulation and development as it represents a crucial entry in the rejuvenation of awqāf in our modern times (

Ahmed 2004). Cash awqāf is far more important since it is more productive compared to land, buildings, books, cattle and so on, as it is testified by the existing research studies and have been found profitable in the practices of modern Islamic financial system (

Ab Aziz et al. 2013).

Cash awqāf also appears to be flexible; facilitative for donations and realizes liquidity in most of the time (

Mahadi 2015, p. 70). The investments initiated through cash awqāf can be diversified and used in many opportunities, demonstrating that it stands out as the most effective method for joint awqāf creation. Furthermore, the fact that the core assets are of a liquid nature also makes it beneficial in all sorts of economic transactions, including income generating activities for the awqāf which would otherwise not be feasible (

Barizah Abu Bakar et al. 2005). A simple example is the facilitation of operational capital which can most efficiently be implemented by having liquid assets.

Cash awqāf has been proposed as one of the most effective modes to eradicate poverty in the Muslim community (

Grodach 2011, pp. 300–9). However, this is subject to many limitations, including the deficiency of awqāf fund management. In addition, some of the generated funds might be abused by awqāf managers (

nuzzar) for fraudulent uses, and hence facilitate the destruction of cash awqāf institution. In many scenarios and as a practical example, the funds gained and those earned through awqāf are not usually accounted for, and so therefore most parties usually use those for personal benefits instead of charity purposes (

Zaman 1999, pp. 1–8). The remedy for awqāf abuse problems lies in the creation of awqāf bank, which would provide various services for income generation, and which again are used to procure services to the poor and needy. One needs to keep in mind, however, that the true essence of the creation of awqāf is to facilitate the management of awqāf funds and create chances for investments in various avenues (

Buttle 2007, pp. 1076–88).

Pertiwi et al. (

2019) discussed three types of awqāf management: traditional, semi-professional and professional awqāf management. This latter relates to the current discussion of cash bank awqāf. The traditional awqāf management is characterized by the placement of awqāf as worship or rituals, set in awqāf property in the form of physical development, such as mosques, boarding schools or burial grounds. Semi-professional awqāf management is characterized by the development of awqāf assets. The professional awqāf management, however, is characterized by productive empowerment of awqāf and professionalism in management and includes management aspects, human resources for awqāf supervisors (nazir), business partnership patterns, and forms of movable awqāf (

Pertiwi et al. 2019, pp. 769–70).

5. Conclusions

As stated earlier, the awqāf bank would drive the economy towards improved socio-economic standards, thus effectively lifting the lower bar of income per capita as well as unpopulated crowds from poverty. Such results are expected to happen according to the perspective of awqāf funds investment and development which provide affordable financing to lower income demographics, helping them break the cycle of poverty. However, Awqāf bank interested beneficiaries may be concerned with the mismanagement, misuse, and misconduct of the awqāf managers and administrators, as well as their uncertainty of their profitable investment to grow the bank’s income. The bank should solicit funds from the public, Islamic corporations, governments, Islamic banks, awqāf capital, awqāf reserves, zakat ministries and public charities. Awqāf bank maintains its raison d’être of perpetuity for the poor and needy through provision of free interest yet affordable financing and full banking services. Awqāf bank should be an independent statutory body, financially based on equity participation such as mudaraba or musharaka. Awqāf capital and awqāf reserves should be invested in the protection of its capital and generation of more income. The bank should be Shari’ah-compliant, with its funds’ investments based on participants’ equity. Its use of capital of charitable funds should be zakat and charities (sadaqat).

This study highlights the legitimate need for Shari’ah-compliant awqāf banks, which in addition to providing basic services for its beneficiaries and for society at large, would also manage investments and awqāf funds in such a way that would make impactful contributions to overall national development and economic growth. This research would be of high relevance to experts, practitioners, financial managers, regulators, and policy makers in the fields of awqāf, banking and finance. Future lines of research should embrace both theoretical and empirical studies, and would address several issues related to the concept methodology and indexes of Sharia compliance, the role of the maqasid in the management of awqāf financing and banking, awqāf funds’ investments in contemporary societies, in addition to evaluation studies of models of awqāf banks.

However, it is worth remembering that in spite of the anticipated advantages of a Shari’ah-compliant awqāf bank in poverty eradication, improving human welfare and development in general, it essentially belongs to a much broader perspective of awqāf, social welfare and civilizational development. The awqāf, as a voluntary and irrevocable dedication of Muslim wealth to God, continues for a long period, toward the development of many critical sectors of society, including the most needed areas and welfare of most aspects of community life and people. The awqāf also provides essential services such as food, education, health, accommodation, and general infrastructure. This only implies that the proposed awqāf bank is not expected to function alone nor in a vacuum of social change, but rather only complements the community’s ethical and religious commitment to brotherhood, solidarity, cooperation, and equality.

{kind=link}