Blockchain-Based ICOs: Pure Hype or the Dawn of a New Era of Startup Financing?

Abstract

1. Introduction

2. Literature and Hypotheses

2.1. Startup Financing

2.2. Hypotheses

2.3. Blockchain Technology

2.4. Blockchain-Based Startup Financing

3. Data and Methodology

3.1. Data Sources

3.2. Operationalization of the Variables

4. Results

4.1. Descriptive Statistics

4.2. Multivariate Results

5. Discussion

5.1. Implications for Theory

5.2. Implications for Practice

5.3. Limitations

6. Conclusions

Supplementary Materials

Author Contributions

Funding

Conflicts of Interest

References

- Adhami, Saman, Giancarlo Giudici, and Stefano Martinazzi. 2018. Why do businesses go crypto? An empirical analysis of Initial Coin Offerings. Journal of Economics and Business. in press. [Google Scholar] [CrossRef]

- Agrawal, Ajay, Christian Catalini, and Avi Goldfarb. 2014. Some simple economics of crowdfunding. Innovation Policy and the Economy 14: 63–97. [Google Scholar] [CrossRef]

- Ahlers, Gerrit K. C., Douglas Cumming, Christina Günther, and Denis Schweizer. 2015. Signaling in equity crowdfunding. Entrepreneurship Theory and Practice 39: 955–80. [Google Scholar] [CrossRef]

- Ahlstrom, David, and Garry D. Bruton. 2006. Venture capital in emerging economies: Networks and institutional change. Entrepreneurship Theory and Practice 30: 299–320. [Google Scholar] [CrossRef]

- Alexy, Oliver T., Joern H. Block, Philipp Sandner, and Anne L. J. Ter Wal. 2012. Social capital of venture capitalists and start-up funding. Small Business Economics 39: 835–51. [Google Scholar] [CrossRef]

- Amit, Raphael, and Christoph Zott. 2001. Value creation in e-business. Strategic Management Journal 22: 493–520. [Google Scholar] [CrossRef]

- Amsden, Ryan, and Denis Schweizer. 2018. Are Blockchain Crowdsales the New ‘Gold Rush’? Success Determinants of Initial Coin Offerings. Available online: https://ssrn.com/abstract=3163849 (accessed on 1 August 2018).

- Ante, Lennart. 2018. Cryptocurrency and crime. In The Money Laundering Market: Regulating the Criminal Economy. Edited by Killian J. McCarthy. London: Agenda Publishing. [Google Scholar]

- Barrow, Colin, Paul Barrow, and Robert Brown. 2001. The Business Plan Workbook, 4th ed. London: Kogan Page. [Google Scholar]

- Baum, Joel A. C., and Brian S. Silverman. 2004. Picking winners or building them? Alliance, intellectual, and human capital as selection criteria in venture financing and performance of biotechnology startups. Journal of Business Venturing 19: 411–36. [Google Scholar] [CrossRef]

- Becker, Gary S. 1993. Nobel lecture: The economic way of looking at behavior. Journal of Political Economy 101: 385–409. [Google Scholar] [CrossRef]

- Belleflamme, Paul, Thomas Lambert, and Armin Schwienbacher. 2014. Crowdfunding: Tapping the right crowd. Journal of Business Venturing 29: 585–609. [Google Scholar] [CrossRef]

- Björkdahl, Joakim. 2009. Technology cross fertilization and the business model: The case of integrating ICTs in mechanical engineering products. Research Policy 38: 1468–77. [Google Scholar] [CrossRef]

- Burtch, Gordon, Anindya Ghose, and Sunil Wattal. 2013. Cultural differences and geography as determinants of online pro-social lending. Business Research Paper, November 21. [Google Scholar]

- Busenitz, Lowell W., James O. Fiet, and Douglas D. Moesel. 2005. Signaling in venture capitalists—New venture team funding decisions: Does it indicate long-term venture outcomes? Entrepreneurship Theory and Practice 29: 1–12. [Google Scholar] [CrossRef]

- Buterin, Vitalik. 2014. Ethereum: A Next-Generation Smart Contract and Decentralized Application Platform. Available online: https://github.com/ethereum/wiki/wiki/White-Paper (accessed on 20 September 2018).

- Calia, Rogerio C., Fabio M. Guerrini, and Gilnei L. Moura. 2007. Innovation networks: From technological development to business model reconfiguration. Technovation 27: 426–32. [Google Scholar] [CrossRef]

- Casadesus-Masanell, Ramon, and Joan Enric Ricart. 2010. From strategy to business models and to tactics. Long Range Planning 43: 195–215. [Google Scholar] [CrossRef]

- Chen, Xiao-Ping, Xin Yao, and Suresh Kotha. 2009. Entrepreneur passion and preparedness in business plan presentations: A persuasion analysis of venture capitalists’ funding decisions. Academy of Management Journal 52: 199–214. [Google Scholar] [CrossRef]

- Chesbrough, Henry. 2010. Business model innovation: opportunities and barriers. Long Range Planning 43: 354–63. [Google Scholar] [CrossRef]

- Chesbrough, Henry, and Richard S. Rosenbloom. 2002. The role of the business model in capturing value from innovation: Evidence from Xerox Corporation’s technology spin-off companies. Industrial and Corporate Change 11: 529–55. [Google Scholar] [CrossRef]

- Cholakova, Magdalena, and Bart Clarysse. 2015. Does the possibility to make equity investments in crowdfunding projects crowd out reward-based investments? Entrepreneurship Theory and Practice 39: 145–72. [Google Scholar] [CrossRef]

- Clayton, Jay. 2017. Statement on Cryptocurrencies and Initial Coin Offerings. Available online: https://www.sec.gov/news/public-statement/statement-clayton-2017-12-11 (accessed on 1 August 2018).

- Coleman, Susan, and Alicia Robb. 2014. Access to Capital by High-Growth Women-Owned Businesses; Washington, DC: National Women’s Business Council, pp. 1–32.

- Colombo, Massimo G., Chiara Franzoni, and Cristina Rossi-Lamastra. 2015. Internal social capital and the attraction of early contributions in crowdfunding. Entrepreneurship Theory and Practice 39: 75–100. [Google Scholar] [CrossRef]

- Conley, John P. 2017. Blockchain and the Economics of Crypto-Tokens and Initial Coin Offerings (No. 17-00008). Nashville: Vanderbilt University Department of Economics. [Google Scholar]

- Cosh, Andy, Douglas Cumming, and Alan Hughes. 2009. Outside Entrepreneurial Capital. Economic Journal 119: 1494–533. [Google Scholar] [CrossRef]

- Cumming, Douglas J., Lars Hornuf, Moein Karami, and Denis Schweizer. 2016. Disentangling Crowdfunding from Fraudfunding. Max Planck Institute for Innovation and Competition Research Paper No. 16-09. Available online: https://www.researchgate.net/profile/Denis_Schweizer/publication/317997302_Disentangling_Crowdfunding_from_Fraudfunding/links/59f8ea17a6fdcc075ec99ba9/Disentangling-Crowdfunding-from-Fraudfunding.pdf (accessed on 8 August 2018).

- De Filippi, Primavera, and Samer Hassan. 2018. Blockchain technology as a regulatory technology: From code is law to law is code. arXiv, arXiv:1801.02507. [Google Scholar]

- Deakins, David, and Mark S. Freel. 2003. Entrepreneurship and Small Firms. London: McGraw Hill Higher Education. [Google Scholar]

- Du, Qianzhou, Weiguo Fan, Zhilei Qiao, Gang Wang, Xuan Zhang, and Mi Zhou. 2015. Money talks: A predictive model on crowdfunding success using project description. Paper presented at Americas Conference on Information Systems (AMCIS), Puerto Rico, Territory, August 13–15. [Google Scholar]

- Dubosson-Torbay, Magali, Alexander Osterwalder, and Yves Pigneur. 2002. E-business model design, classification, and measurements. Thunderbird International Business Review 44: 5–23. [Google Scholar] [CrossRef]

- Fisch, Christian. 2019. Initial coin offerings (ICOs) to finance new ventures. Journal of Business Venturing 34: 1–22. [Google Scholar] [CrossRef]

- Florin, Juan, Michael Lubatkin, and William Schulze. 2003. A social capital model of high-growth ventures. Academy of Management Journal 46: 374–84. [Google Scholar]

- Frehen, Rik G. P., William N. Goetzmann, and K. Geert Rouwenhorst. 2013. New evidence on the first financial bubble. Journal of Financial Economics 108: 585–607. [Google Scholar] [CrossRef]

- Gimmon, Eli, and Jonathan Levie. 2010. Founder’s human capital, external investment, and the survival of new high-technology ventures. Research Policy 39: 1214–26. [Google Scholar] [CrossRef]

- Griffin, Zachary J. 2012. Crowdfunding: Fleecing the American masses. Case Western Reserve Journal of Law, Technology and the Internet 4: 375. [Google Scholar] [CrossRef]

- Hall, John, and Charles W. Hofer. 1993. Venture capitalists’ decision criteria in new venture evaluation. Journal of Business Venturing 8: 25–42. [Google Scholar] [CrossRef]

- Harrison, Richard, and Colin Mason. 1996. Developments in the promotion of informal venture capital in the UK. International Journal of Entrepreneurial Behaviour and Research 2: 6–33. [Google Scholar] [CrossRef]

- Hellmann, Thomas, and Manju Puri. 2002. Venture capital and the professionalization of start-up firms: Empirical evidence. Journal of Finance 57: 169–97. [Google Scholar] [CrossRef]

- Hofstede, Geert. 1984. Cultural dimensions in management and planning. Asia Pacific Journal of Management 1: 81–99. [Google Scholar] [CrossRef]

- Hornuf, Lars, and Armin Schwienbacher. 2017. Market mechanisms and funding dynamics in equity crowdfunding. Journal of Corporate Finance 50: 556–74. [Google Scholar] [CrossRef]

- Hsu, David H. 2007. Experienced entrepreneurial founders, organizational capital, and venture capital funding. Research Policy 36: 722–41. [Google Scholar] [CrossRef]

- Iansiti, Marco, and Karim R. Lakhani. 2017. The truth about blockchain. Harvard Business Review 95: 118–27. [Google Scholar]

- Jentzsch, Christoph. 2016. Decentralized Autonomous Organization to Automate Governance. Available online: https://download.slock.it/public/DAO/WhitePaper.pdf (accessed on 8 August 2018).

- Jin, Fujie, Andy Wu, and Lorin Hitt. 2017. Social Is the New Financial: How Startup Social Media Activity Influences Funding Outcomes. Academy of Management Proceedings 1: 13329. [Google Scholar] [CrossRef]

- Joshi, Archana Prashanth, Meng Han, and Yan Wang. 2018. A survey on security and privacy issues of blockchain technology. Mathematical Foundations of Computing 1: 121–47. [Google Scholar] [CrossRef]

- Kim, Jin-Hyuk, and Liad Wagman. 2016. Early-stage entrepreneurial financing: A signaling perspective. Journal of Banking and Finance 67: 12–22. [Google Scholar] [CrossRef]

- Lechner, Christian, Michael Dowling, and Isabell Welpe. 2006. Firm networks and firm development: The role of the relational mix. Journal of Business Venturing 21: 514–40. [Google Scholar] [CrossRef]

- Lee, Ji Hyung, and Peter C. B. Phillips. 2016. Asset pricing with financial bubble risk. Journal of Empirical Finance 38: 590–622. [Google Scholar] [CrossRef]

- Lee, Choonwoo, Kyungmook Lee, and Johannes M. Pennings. 2001. Internal capabilities, external networks, and performance: A study on technology-based ventures. Strategic Management Journal 22: 615–40. [Google Scholar] [CrossRef]

- Linn, Laure A., and Martha B. Koo. 2016. Blockchain for health data and its potential use in health it and health care related research. In ONC/NIST Use of Blockchain for Healthcare and Research Workshop; Gaithersburg: ONC/NIST. [Google Scholar]

- Macht, Stephanie A., and John Robinson. 2009. Do business angels benefit their investee companies? International Journal of Entrepreneurial Behavior and Research 15: 187–208. [Google Scholar] [CrossRef]

- Malmendier, Ulrike, and Devin Shanthikumar. 2007. Are small investors naive about incentives? Journal of Financial Economics 85: 457–89. [Google Scholar] [CrossRef]

- Manning, Willard G., and John Mullahy. 2001. Estimating log models: to transform or not to transform? Journal of Health Economics 20: 461–94. [Google Scholar] [CrossRef]

- McGrath, Rita Gunther. 2010. Business models: A discovery driven approach. Long Range Planning 43: 247–61. [Google Scholar] [CrossRef]

- Mollick, Ethan R. 2013. Swept Away by the Crowd? Crowdfunding, Venture Capital, and the Selection of Entrepreneurs. Available online: https://ssrn.com/abstract=2239204 (accessed on 1 August 2018).

- Muzyka, Dan, Sue Birley, and Benoit Leleux. 1996. Trade-offs in the investment decisons of European venture capitalists. Journal of Business Venturing 11: 273–87. [Google Scholar] [CrossRef]

- Nakamoto, Satoshi. 2008. Bitcoin: A Peer-to-Peer Electronic Cash System. Available online: https://bitcoin.org/bitcoin.pdf (accessed on 12 June 2018).

- Nevin, Sean, Rob Gleasure, Philip O’Reilly, Joseph Feller, Shanping Li, and Jerry Cristoforo. 2017. Social Identity and Social Media Activities in Equity Crowdfunding. Paper presented at 13th International Symposium on Open Collaboration, Galway, Ireland, August 23–25; p. 11. [Google Scholar]

- Osgood, Ryan. 2016. The Future of Democracy: Blockchain Voting. In COMP116: Information Security, Tufts University Department of Computer Science. Available online: http://www.cs.tufts.edu/comp/116/archive/fall2016/rosgood.pdf (accessed on 5 August 2018).

- Pástor, Ľuboš, and Pietro Veronesi. 2006. Was there a Nasdaq bubble in the late 1990s? Journal of Financial Economics 81: 61–100. [Google Scholar] [CrossRef]

- Pastor, Lubos, and Pietro Veronesi. 2009. Learning in financial markets. Annual Review of Financial Economics 1: 361–81. [Google Scholar] [CrossRef]

- Powell, Anne, John Galvin, and Gabriele Piccoli. 2006. Antecedents to team member commitment from near and far: A comparison between collocated and virtual teams. Information Technology and People 19: 299–322. [Google Scholar] [CrossRef]

- Puthal, Deepak, Nisha Malik, Saraju P. Mohanty, Elias Kougianos, and Gautam Das. 2018. Everything You Wanted to Know About the Blockchain: Its Promise, Components, Processes, and Problems. IEEE Consumer Electronics Magazine 7: 6–14. [Google Scholar] [CrossRef]

- Robb, Alicia M., and David T. Robinson. 2014. The capital structure decisions of new firms. Review of Financial Studies 27: 153–79. [Google Scholar] [CrossRef]

- Sandner, Philipp G., and Joern Block. 2011. The market value of R and D, patents, and trademarks. Research Policy 40: 969–85. [Google Scholar] [CrossRef]

- Schwienbacher, Armin, and Benjamin Larralde. 2010. Crowdfunding of small entrepreneurial ventures. In Handbook of Entrepreneurial Finance. Oxford: Oxford University Press. [Google Scholar]

- Scott, Brett. 2016. How Can Cryptocurrency and Blockchain Technology Play a Role in Building Social and Solidarity Finance? No. 2016-1. UNRISD Working Paper. Available online: https://www.econstor.eu/bitstream/10419/148750/1/861287290.pdf (accessed on 22 August 2018).

- SEC. 2017a. U.S. Securities and Exchange Commission. Investor Bulletin: Initial Coin Offerings. Available online: https://www.sec.gov/oiea/investor-alerts-and-bulletins/ib_coinofferings (accessed on 17 August 2018).

- SEC. 2017b. U.S. Securities and Exchange Commission. Securities and Exchange Commission, Securities Exchange Act of 1934, Release No. 81207/25 July 2017, Report of Investigation Pursuant to Section 21(a) of the Securities Exchange Act of 1934: The DAO. Available online: www.sec.gov/litigation/investreport/34-81207.pdf (accessed on 17 August 2018).

- SEC. 2017c. U.S. Securities and Exchange Commission. Securities Act of 1933 Release no. 10445/11 December 2017. Administrative Proceeding File no. 3-18304. Order Instituting Cease-Anddesist Proceedings Pursuant to Section 8a of the Securities Act of 1933, Making Findings, and Imposing a Cease-and-Desist ordeR. Available online: www.sec.gov/litigation/admin/2017/33-10445.pdf (accessed on 17 August 2018).

- Shafer, Scott M., H. Jeff Smith, and Jane C. Linder. 2005. The power of business models. Business Horizons 48: 199–207. [Google Scholar] [CrossRef]

- Shepherd, Dean A., and Evan J. Douglas. 1999. Attracting Equity Investors: Positioning, Preparing and Presenting the Business Plan. Thousand Oaks: Sage. [Google Scholar]

- Solomon, Michael, Rebekah Russell-Bennett, and Josephine Previte. 2012. Consumer Behaviour. Melbourne: Pearson Higher Education AU. [Google Scholar]

- Spence, Michael. 1973. Job market signaling. Quarterly Journal of Economics 87: 355–74. [Google Scholar] [CrossRef]

- Sprenger, Timm O., Philipp G. Sandner, Andranik Tumasjan, and Isabell M. Welpe. 2014. News or noise? Using Twitter to identify and understand company-specific news flow. Journal of Business Finance and Accounting 41: 791–830. [Google Scholar] [CrossRef]

- Stuart, Toby E., Ha Hoang, and Ralph C. Hybels. 1999. Interorganizational endorsements and the performance of entrepreneurial ventures. Administrative Science Quarterly 44: 315–49. [Google Scholar] [CrossRef]

- Tankhiwale, Shekhar. 2009. Exploring the interrelationship between Telco business model innovation and the change in business process architecture. Journal of Telecommunications Management 2: 126–37. [Google Scholar]

- Thaler, Richard H., and Eric J. Johnson. 1990. Gambling with the house money and trying to break even: The effects of prior outcomes on risky choice. Management Science 36: 643–60. [Google Scholar] [CrossRef]

- Timmers, Paul. 1998. Business models for electronic markets. Electronic Markets 8: 3–8. [Google Scholar] [CrossRef]

- Vismara, Silvio. 2016. Information cascades among investors in equity crowdfunding. Entrepreneurship Theory and Practice. [Google Scholar] [CrossRef]

- Wheale, Peter Robert, and Laura Heredia Amin. 2003. “Bursting the dot. com” bubble’: A case study in investor behaviour. Technology Analysis and Strategic Management 15: 117–36. [Google Scholar] [CrossRef]

- Witt, Peter. 2004. Entrepreneurs’ networks and the success of start-ups. Entrepreneurship and Regional Development 16: 391–412. [Google Scholar] [CrossRef]

- Wood, Gavin. 2014. Ethereum: A secure decentralised generalised transaction ledger. Ethereum Project Yellow Paper 151: 1–32. [Google Scholar]

- Yang, Song, and Ron Berger. 2017. Relation between start-ups’ online social media presence and fundraising. Journal of Science and Technology Policy Management 8: 161–80. [Google Scholar] [CrossRef]

- Yermack, David. 2013. Is Bitcoin a Real Currency? An Economic Appraisal. No. w19747. Cambridge: National Bureau of Economic Research. [Google Scholar]

- Zacharakis, Andrew, and Dean A. Shepherd. 2005. A non-additive decision-aid for venture capitalists’ investment decisions. European Journal of Operational Research 162: 673–89. [Google Scholar] [CrossRef]

- Zelizer, Viviana A. Rotman. 1994. The Social Meaning of Money. New York: Basic Books. [Google Scholar]

- Zott, Christoph, Raphael Amit, and Lorenzo Massa. 2011. The business model: Recent developments and future research. Journal of Management 37: 1019–42. [Google Scholar] [CrossRef]

| 1 | Legally, the term ‘investor’ may not be universally applicable, as ICO contributions, strictly speaking, often constitute donations. |

| 2 | |

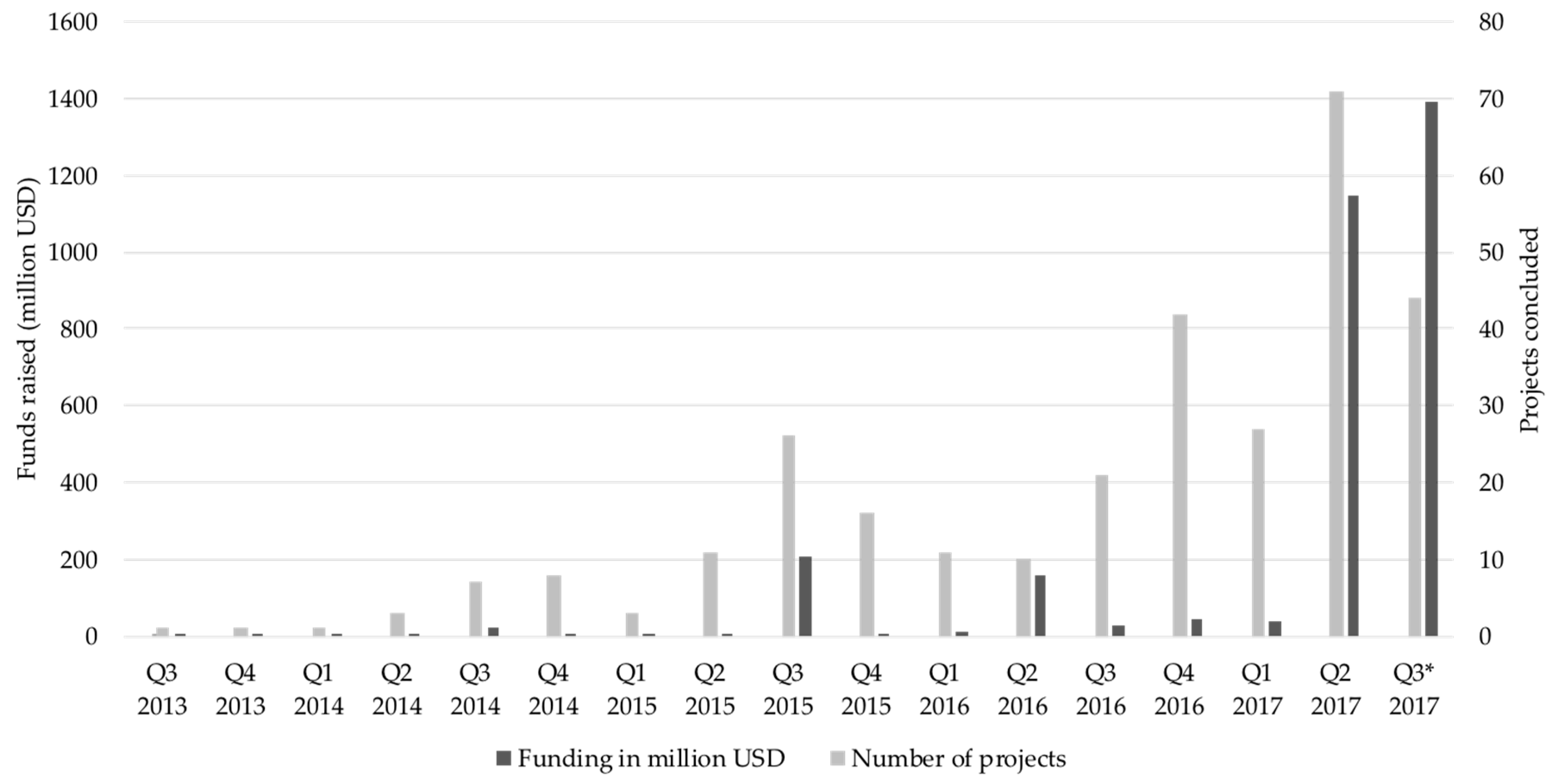

| 3 | The example of the project, Digix Global, illustrates the effects of cryptocurrency price fluctuations. The project raised 462,719 Ether in March 2016, worth around $5.5 million at the time. Thanks to the cryptocurrency price increase, the projects’ funds were worth around $132 million only two years later (https://etherscan.io/address/0xf0160428a 8552ac9bb7e050d90eeade4ddd52843). |

| 4 | Instead, the number of posts until the end of the ICO phase should have been used to determine the social media scores. Yet, this data is virtually impossible to retrieve automatically for past years. |

{kind=link}

{kind=link}

| Variables | Obs. | Mean | Std. Dev. | Median | Min. | Max. |

|---|---|---|---|---|---|---|

| Funds raised | 278 | 6,515,099 | 23,241,612 | 436,316 | 25 | 227,817,556 |

| Log(Funds raised) | 278 | 5.471 | 1.315 | 5.64 | 1.4 | 8.36 |

| Team size | 278 | 3.910 | 6.141 | 0 | 0 | 46 |

| Team network | 278 | 97.477 | 147.021 | 0 | 0 | 500 |

| Advisors | 278 | 1.162 | 2.804 | 0 | 0 | 17 |

| Business model: infrastructure | 278 | 0.662 | 0.779 | 0 | 0 | 2 |

| Business model: financial | 278 | 0.644 | 0.69 | 1 | 0 | 2 |

| Business model: utility | 278 | 0.651 | 0.72 | 1 | 0 | 2 |

| ICO duration | 276 | 26.070 | 62.817 | 15 | 0 | 906 |

| Log(ICO duration) 1 | 276 | 0.996 | 0.647 | 1.48 | 0 | 2.957 |

| Whitepaper: score | 278 | 13.230 | 17.601 | 2.5 | 0 | 131 |

| Whitepaper: exists | 277 | 0.520 | 0.501 | 1 | 0 | 1 |

| Twitter score | 278 | 4.750 | 9.714 | 2.025 | 0 | 115.21 |

| Facebook score | 278 | 3.332 | 13.755 | 0 | 0 | 143.213 |

| Reddit Score | 278 | 1.211 | 8.062 | 0.002 | 0 | 98.033 |

| Bitcointalk Score | 278 | 117.681 | 266.287 | 25.85 | 0 | 2379.9 |

| Financial | 278 | 0.414 | 0.493 | 0 | 0 | 1 |

| Blocknet | 278 | 0.133 | 0.340 | 0 | 0 | 1 |

| Media | 278 | 0.112 | 0.315 | 0 | 0 | 1 |

| Gambling | 278 | 0.054 | 0.226 | 0 | 0 | 1 |

| Gaming | 278 | 0.054 | 0.226 | 0 | 0 | 1 |

| Cloud Computing | 278 | 0.216 | 0.146 | 0 | 0 | 1 |

| Team dispersion | 278 | 1.040 | 1.628 | 0 | 0 | 9 |

| Variables | Model 1 | Model 2 | Model 3 | Model 4 |

|---|---|---|---|---|

| Team size | 0.019 * | 0.016 | 0.018 * | 0.032 *** |

| (0.075) | (0.123) | (0.089) | (0.009) | |

| Team network | 0.009 ** | 0.001 *** | 0.001 * | 0.001 ** |

| (0.047) | (0.008) | (0.045) | (0.014) | |

| Advisors | 0.061 *** | 0.061 *** | 0.063 *** | 0.055 ** |

| (0.007) | (0.008) | (0.006) | (0.016) | |

| Business model: Infrastructure | 0.043 | −0.034 | 0.048 | 0.093 |

| (0.614) | (0.696) | (0.573) | (0.288) | |

| Business model: Financial | 0.358 *** | 0.395 *** | 0.364 *** | 0.391 *** |

| (0.000) | (0.000) | (0.000) | (0.000) | |

| Business model: Utility | 0.265 *** | 0.178 * | 0.252 *** | 0.266 *** |

| (0.005) | (0.065) | (0.008) | (0.005) | |

| Whitepaper: Score | 0.005 | 0.004 | 0.005 | 0.004 |

| (0.291) | (0.321) | (0.279) | (0.367) | |

| Whitepaper: Exists | 0.806 *** | 0.811 *** | 0.783 *** | 0.829 *** |

| (0.000) | (0.000) | (0.000) | (0.000) | |

| Twitter score | 0.008 | 0.005 | 0.008 | 0.011 |

| (0.169) | (0.410) | (0.200) | (0.148) | |

| Bitcointalk score | - | - | - | −0.000 |

| (0.446) | ||||

| Facebook score | - | - | - | 0.001 |

| (0.776) | ||||

| Reddit score | - | - | - | −0.001 |

| (0.850) | ||||

| ICO duration | 0.001 * | 0.001 | - | - |

| (0.083) | (0.208) | |||

| Log(ICO duration) | - | - | 0.093 | - |

| (0.274) | ||||

| Team dispersion | - | - | - | −0.105 ** |

| (0.039) | ||||

| Blocknet | - | 0.046 | - | - |

| (0.801) | ||||

| Financial | - | −0.462 *** | - | - |

| (0.000) | ||||

| Media | - | −0.275 | - | - |

| (0.149) | ||||

| Gambling | - | −0.097 | - | - |

| (0.696) | ||||

| Gaming | - | 0.041 | - | - |

| (0.869) | ||||

| Cloud computing | - | 0.455 | - | - |

| (0.227) | ||||

| F | 39.48 | 26.8 | 39.01 | 30.79 |

| Adj. R2 | 0.5857 | 0.6021 | 0.5831 | 0.5854 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ante, L.; Sandner, P.; Fiedler, I. Blockchain-Based ICOs: Pure Hype or the Dawn of a New Era of Startup Financing? J. Risk Financial Manag. 2018, 11, 80. https://doi.org/10.3390/jrfm11040080

Ante L, Sandner P, Fiedler I. Blockchain-Based ICOs: Pure Hype or the Dawn of a New Era of Startup Financing? Journal of Risk and Financial Management. 2018; 11(4):80. https://doi.org/10.3390/jrfm11040080

Chicago/Turabian StyleAnte, Lennart, Philipp Sandner, and Ingo Fiedler. 2018. "Blockchain-Based ICOs: Pure Hype or the Dawn of a New Era of Startup Financing?" Journal of Risk and Financial Management 11, no. 4: 80. https://doi.org/10.3390/jrfm11040080

APA StyleAnte, L., Sandner, P., & Fiedler, I. (2018). Blockchain-Based ICOs: Pure Hype or the Dawn of a New Era of Startup Financing? Journal of Risk and Financial Management, 11(4), 80. https://doi.org/10.3390/jrfm11040080