Recovering Historical Inflation Data from Postage Stamps Prices

Abstract

1. Introduction and Motivation

2. The Data

3. Two Econometric Models

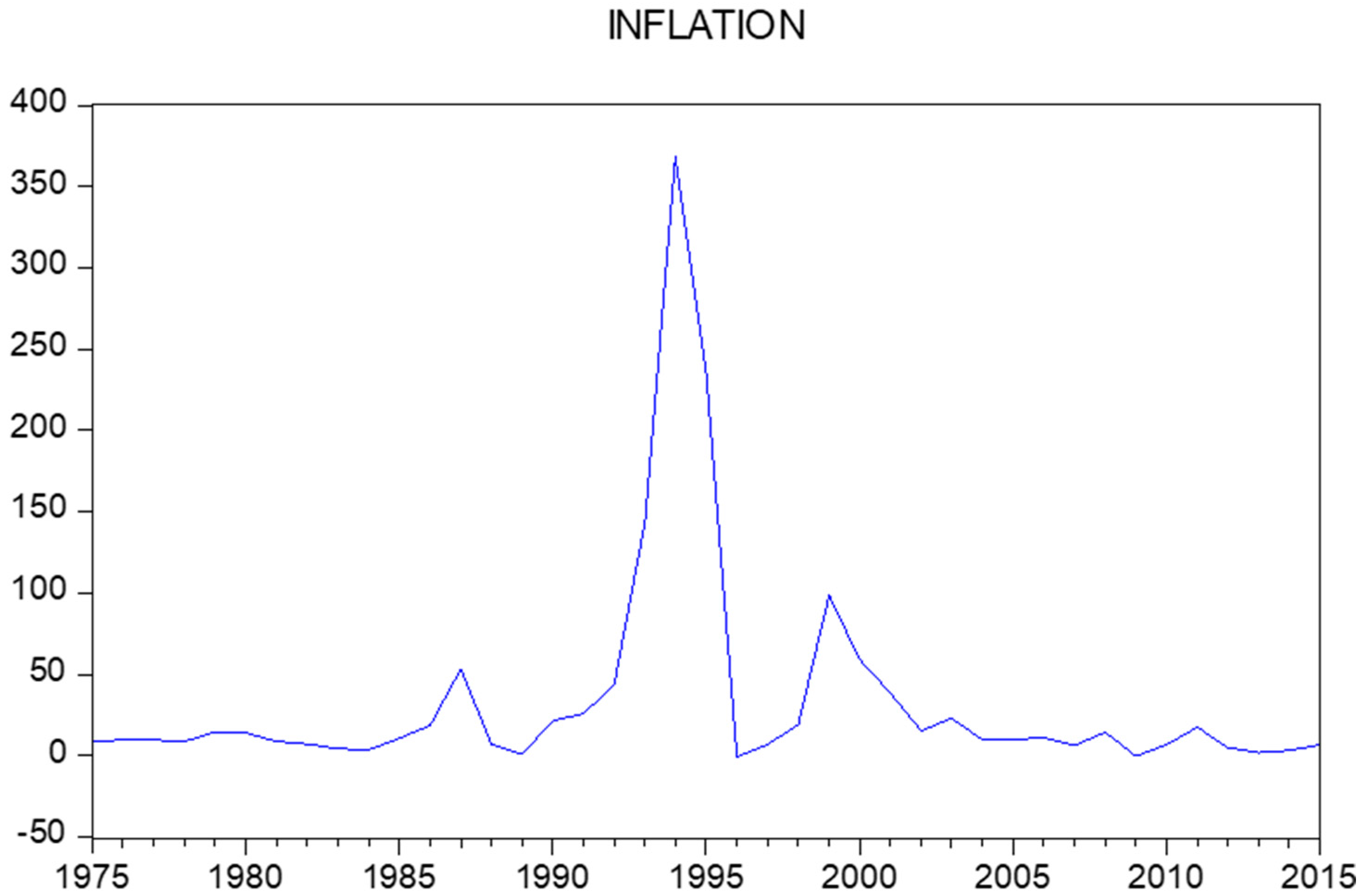

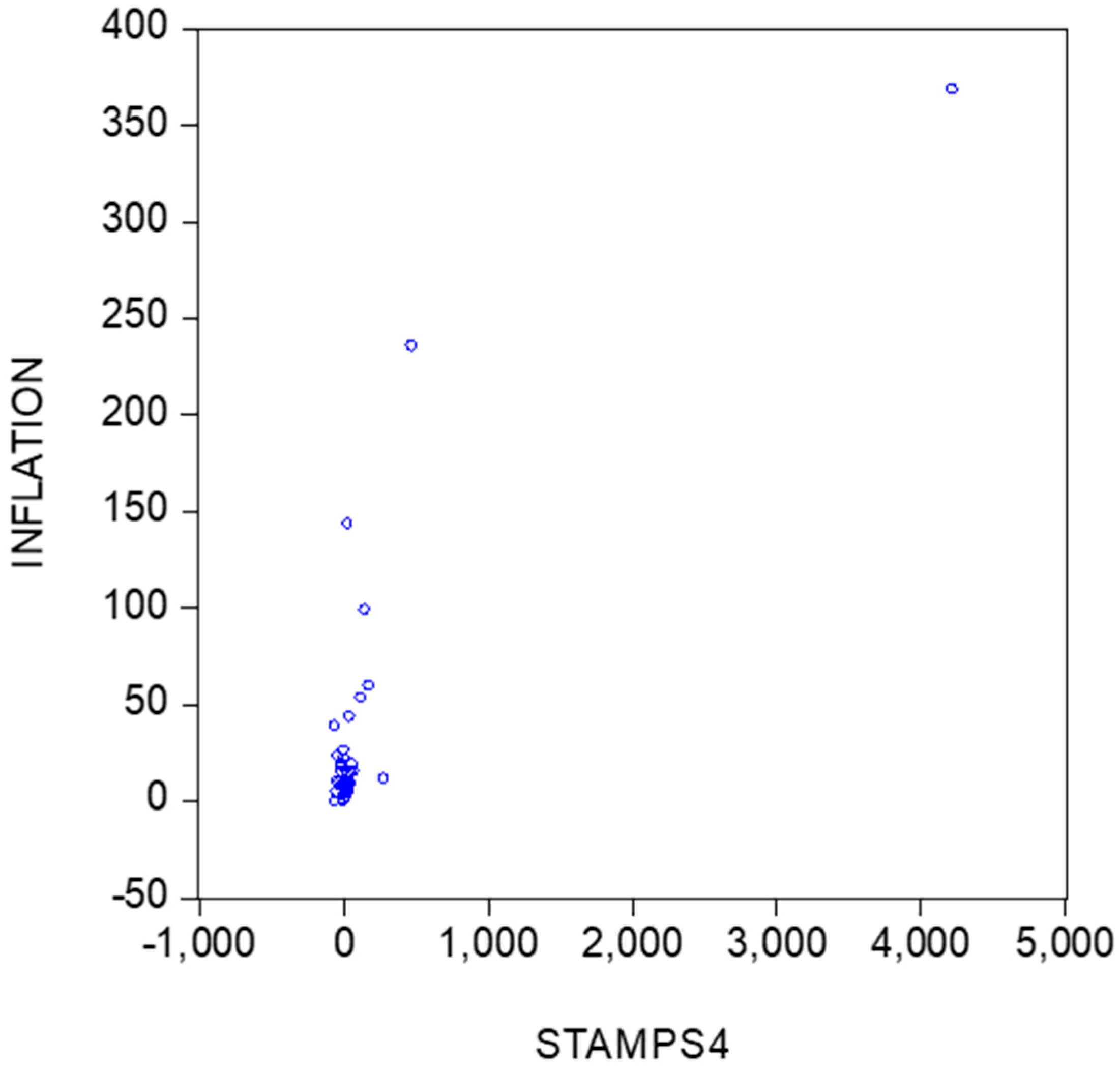

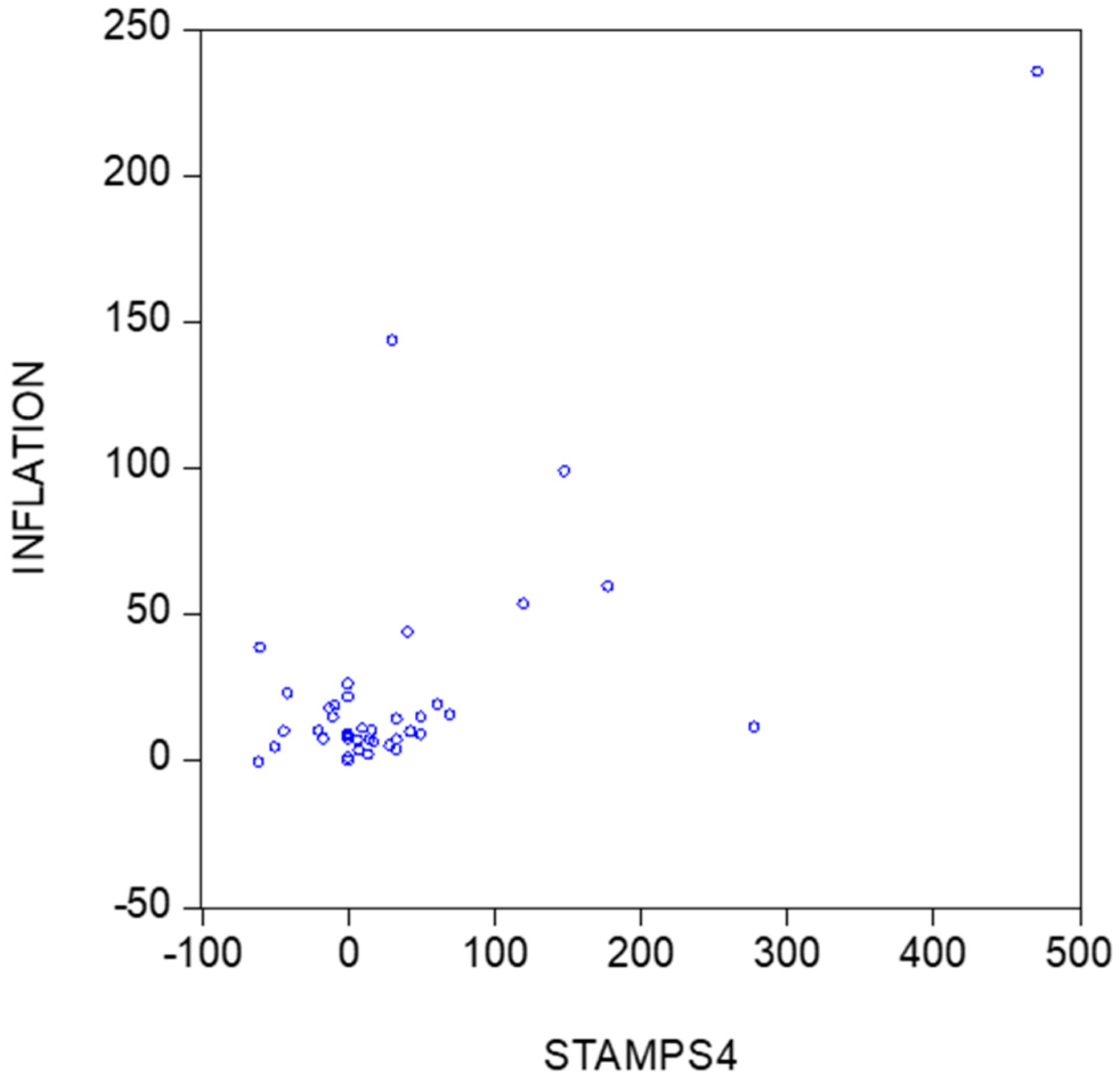

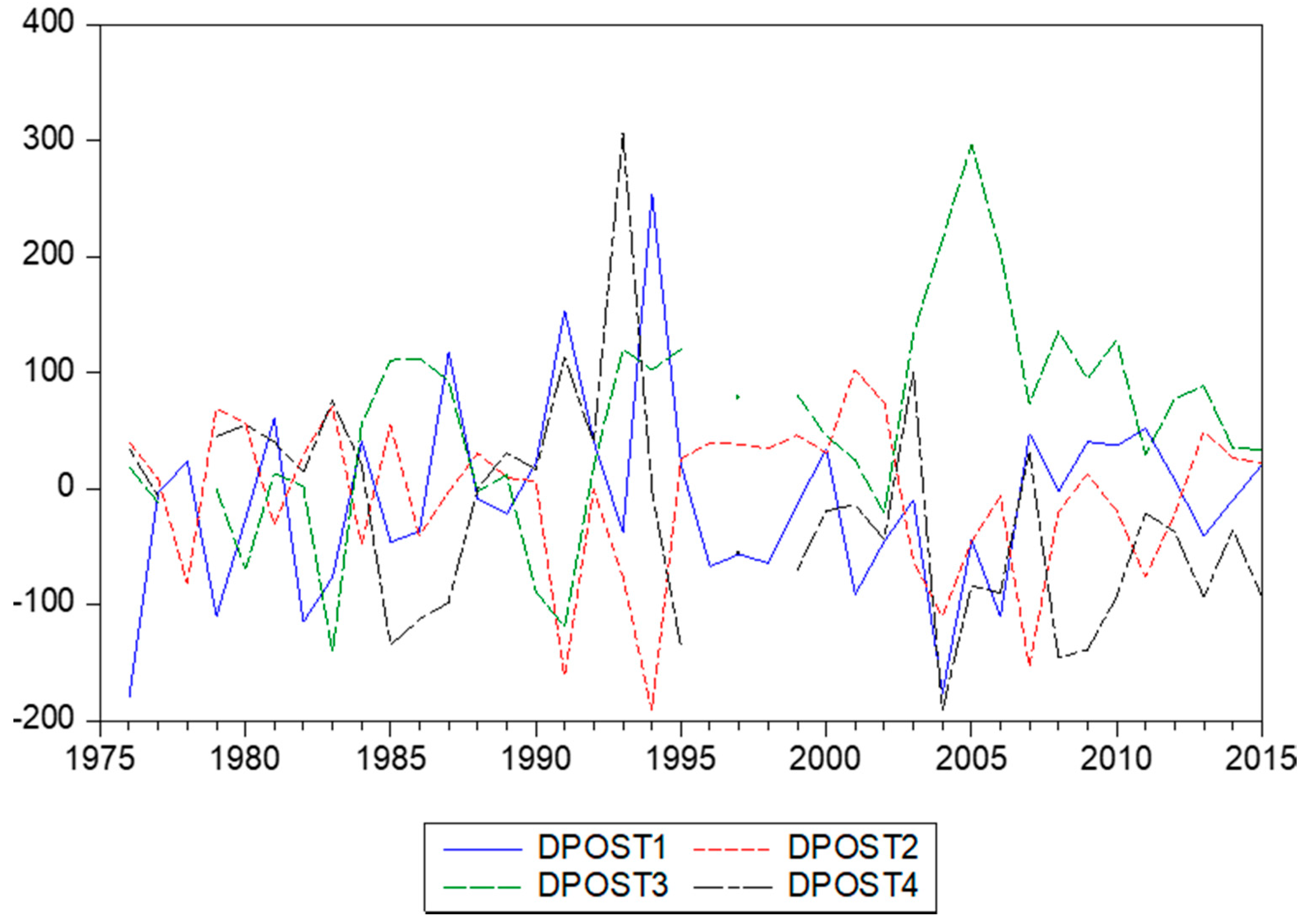

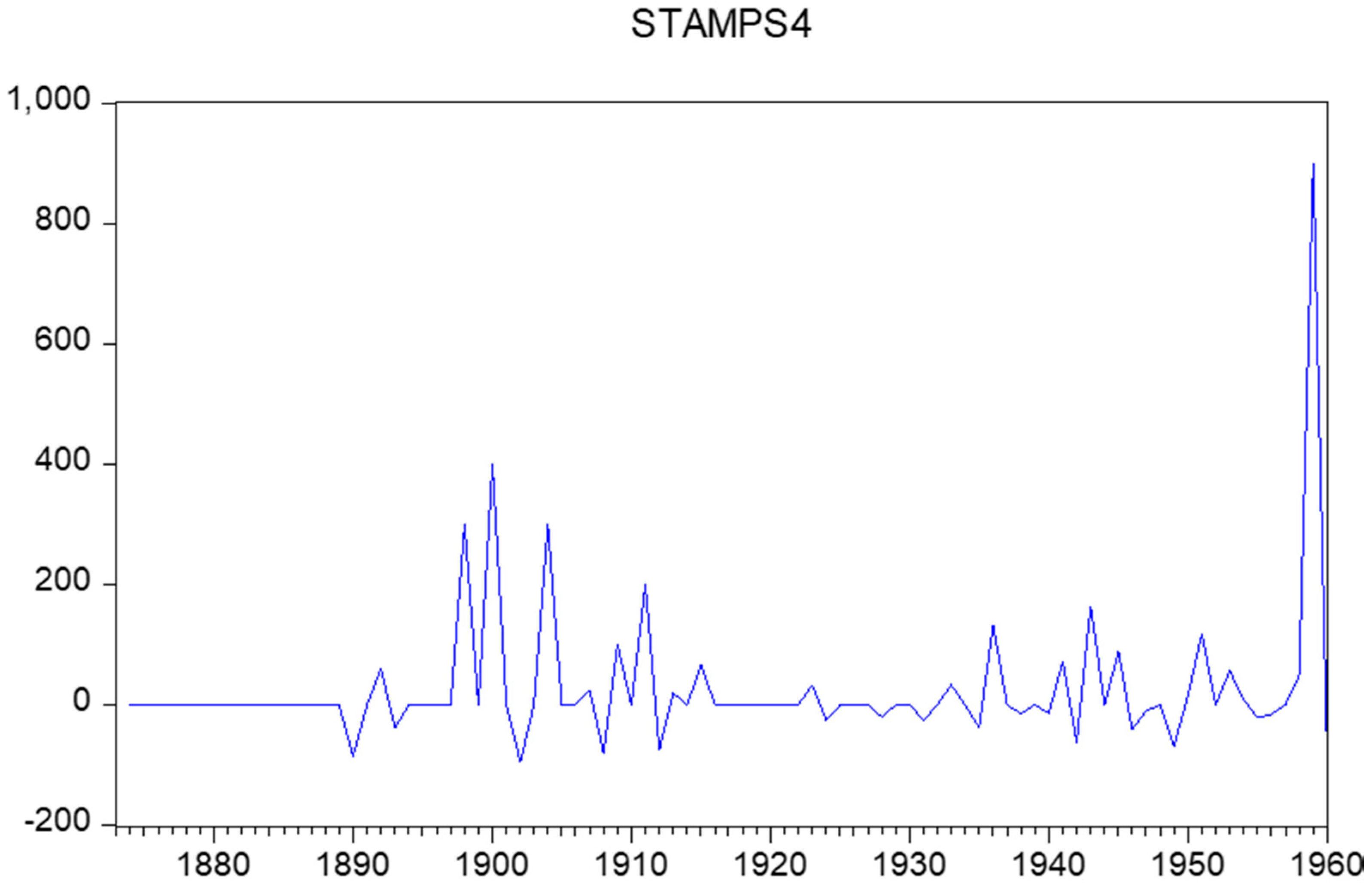

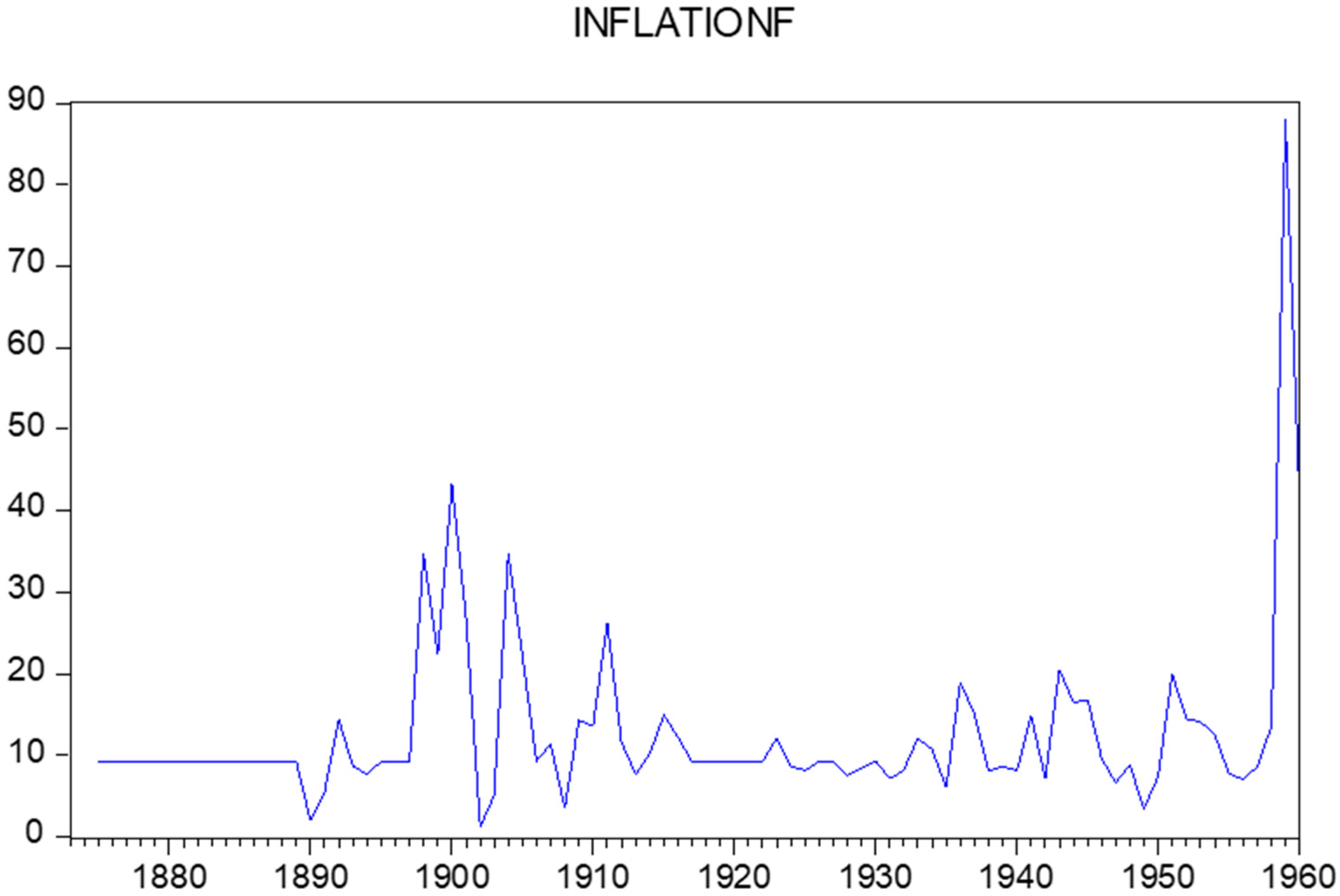

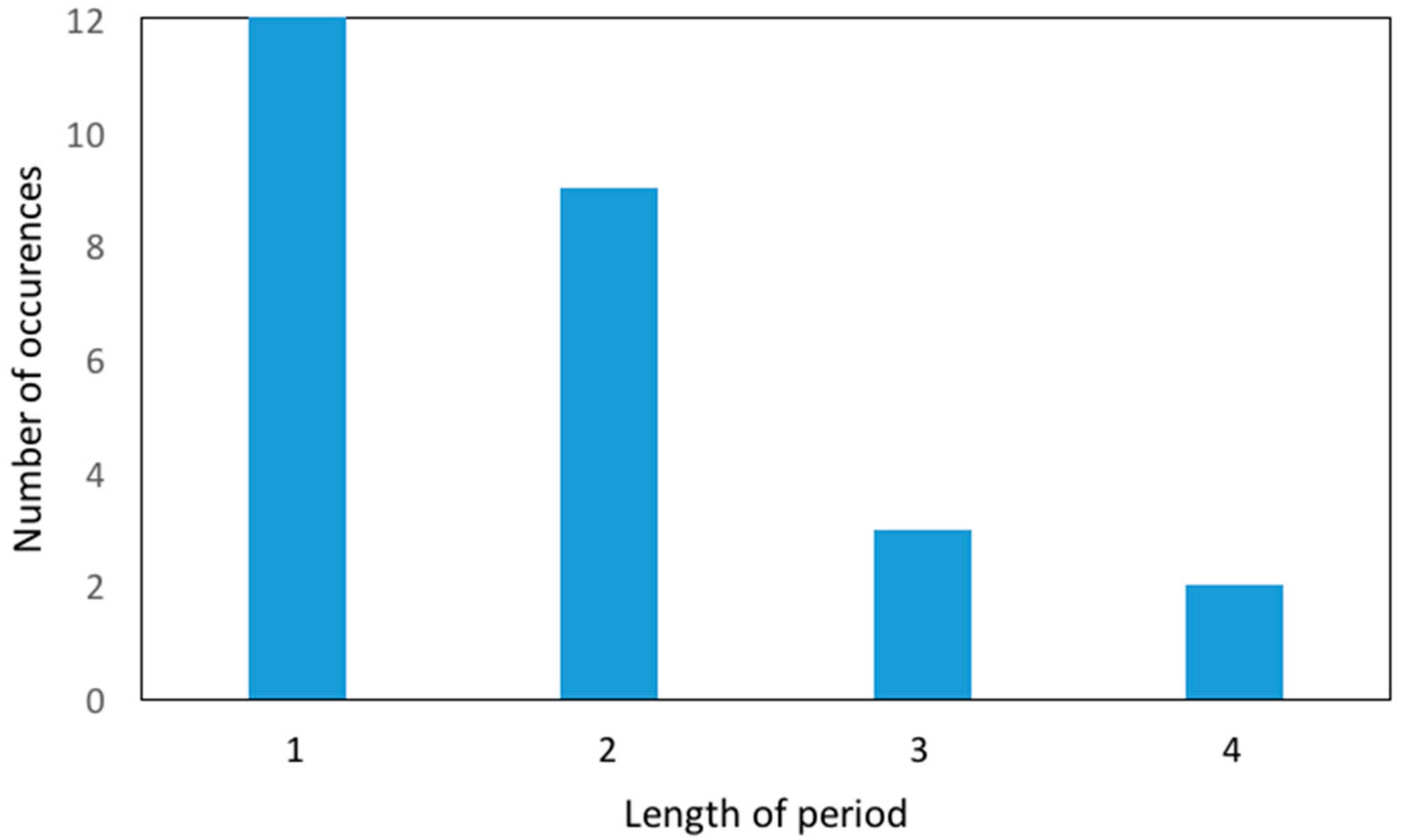

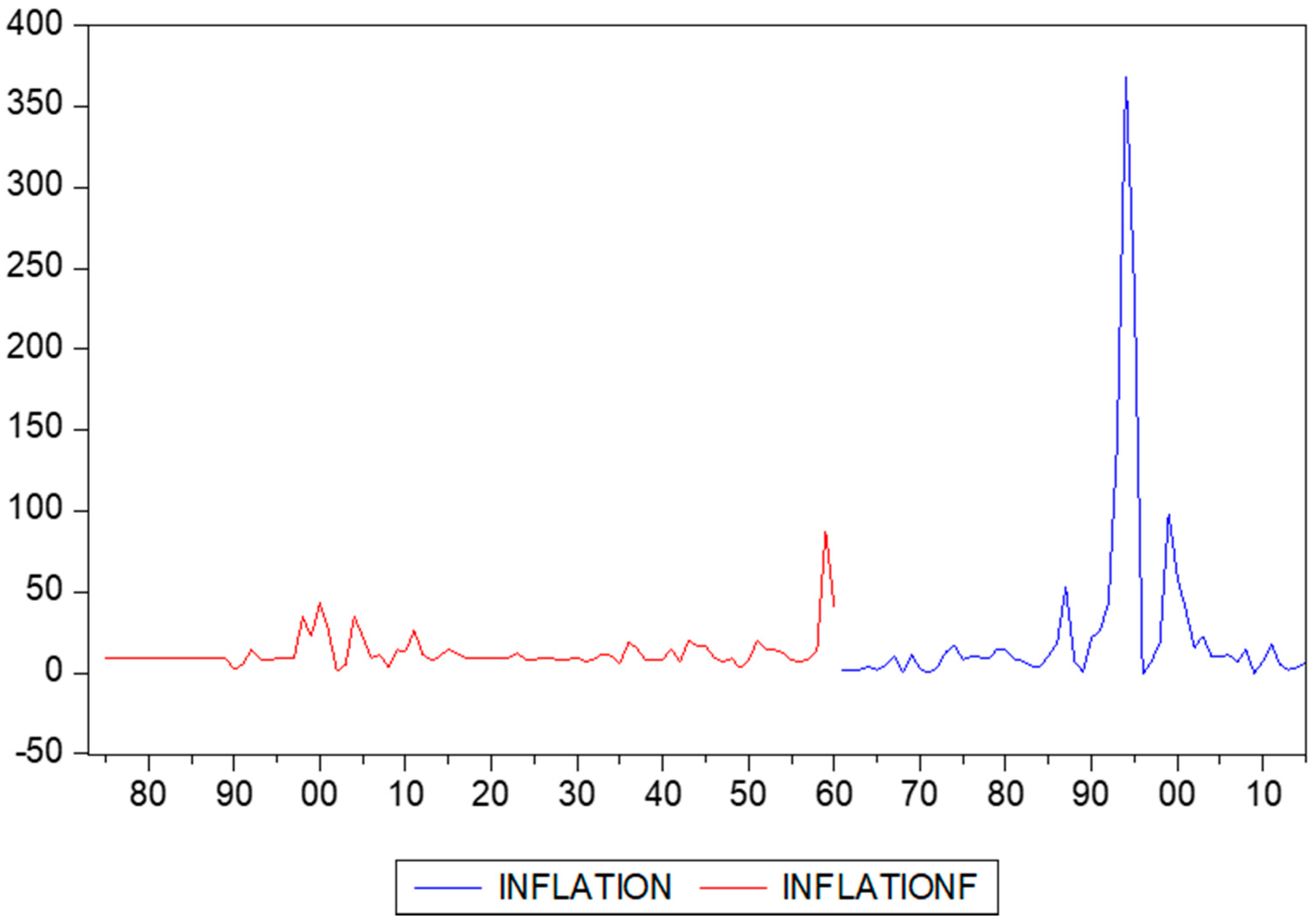

4. Recovery of Historical Inflation Rates

5. Conclusions

Author Contributions

Conflicts of Interest

References

- Allen, Robert C., Jean-Pascal Bassino, Debin Ma, Christine Moll-Murata, and Jan Luiten van Zanden. 2011. Wages, prices, and living standards in China, 1738–1925: In comparison with Europe, Japan, and India. Economic History Review 64: 8–38. [Google Scholar] [CrossRef]

- Andreou, Elena, Eric Ghysels, and Andros Kourtellos. 2010. Regression models with mixed sampling frequencies. Journal of Econometrics 158: 246–61. [Google Scholar] [CrossRef]

- Bolt, Jutta, and Jan Luiten van Zanden. 2014. The Maddison Project: Collaborative research on historical national accounts. Economic History Review 67: 627–51. [Google Scholar] [CrossRef]

- Cendejas Bueno, Jose Luis, and Cecilia Font de Villanueva. 2015. Convergence of inflation with a common cycle: Estimating and modelling Spanish historical inflation from the 16th to the 18th centuries. Empirical Economics 48: 1643–65. [Google Scholar] [CrossRef]

- Chang, Chia-Lin, and Michael McAleer. 2017. The correct regularity condition and interpretation of asymmetry in EGARCH. Economics Letters 161: 52–55. [Google Scholar] [CrossRef]

- Clements, Michael P., and Anna B. Galvao. 2008. Macroeconomic forecasting with mixed-frequency data. Journal of Business and Economic Statistics 26: 546–54. [Google Scholar] [CrossRef]

- Deaton, Angus, and Alan Heston. 2010. Understanding PPPs and PPP-based national accounts. American Economic Journal: Macroeconomics 2: 1–35. [Google Scholar] [CrossRef]

- Frankema, Ewout H. P., and Marlous van Waijenburg. 2012. Structural impediments to African growth? New evidence from real wages in British Africa, 1880–1965. Journal of Economic History 72: 895–926. [Google Scholar] [CrossRef]

- Franses, Philip Hans, and Rianne Legerstee. 2014. Statistical institutes and economic prosperity. Quality and Quantity 48: 507–20. [Google Scholar] [CrossRef]

- Ghysels, Eric, Pedro Santa-Clara, and Rossen Valkanov. 2004. The MIDAS Touch: Mixed Data Sampling Regression Models. CIRANO Working Paper 2004s-20. Montreal, QC, Canada: CIRANO. [Google Scholar]

- Ghysels, Eric, Arthur Sinko, and Rossen Valkanov. 2007. Midas regressions: Further results and new directions. Econometric Reviews 26: 53–90. [Google Scholar] [CrossRef]

- Hoefte, Rosemarijn. 2013. Suriname in the Long Twentieth Century: Domination, Contestation, Globalization. Berlin: Springer. [Google Scholar]

- Jerven, Morten. 2009. The relativity of poverty and income: How reliable are African economic statistics? African Affairs 109: 77–96. [Google Scholar] [CrossRef]

- McAleer, Michael, and Christiaan Hafner. 2014. A one line derivation of EGARCH. Econometrics 2: 92–97. [Google Scholar] [CrossRef]

- Van Velzen, Thoden, and Wim Hoogbergen. 2013. Een Zwarte Vrijstaat in Suriname (Deel 2): De Okaanse Samenleving in de Negentiende en Twintigste Eeuw. Leiden: Brill. [Google Scholar]

| 1 | See Franses and Legerstee (2014) for a table with dates for 106 countries when statistical bureaus were founded. |

| 2 | Important references to MIDAS regression are Andreou et al. (2010), Clements and Galvao (2008), Ghysels et al. (2004), and Ghysels et al. (2007). |

| 3 | |

| 4 | |

| 5 | See Chang and McAleer (2017) and McAleer and Hafner (2014) for two recent studies on this very useful model. |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| 1961 | 1.7 | 1971 | 0.2 | 1981 | 8.8 |

| 1962 | 2.1 | 1972 | 3.2 | 1982 | 7.3 |

| 1963 | 2.1 | 1973 | 12.9 | 1983 | 4.4 |

| 1964 | 4.2 | 1974 | 16.9 | 1984 | 3.7 |

| 1965 | 1.9 | 1975 | 8.4 | 1985 | 10.9 |

| 1966 | 4.7 | 1976 | 10.1 | 1986 | 18.7 |

| 1967 | 10.7 | 1977 | 9.7 | 1987 | 53.4 |

| 1968 | 0.2 | 1978 | 8.8 | 1988 | 7.3 |

| 1969 | 11.3 | 1979 | 14.8 | 1989 | 0.8 |

| 1970 | 2.6 | 1980 | 14.1 | 1990 | 21.7 |

| 1991 | 26 | 2001 | 38.6 | 2011 | 17.7 |

| 1992 | 43.7 | 2002 | 15.5 | 2012 | 5 |

| 1993 | 143.5 | 2003 | 23 | 2013 | 2 |

| 1994 | 368.5 | 2004 | 10 | 2014 | 3.3 |

| 1995 | 235.6 | 2005 | 9.9 | 2015 | 6.9 |

| 1996 | −0.7 | 2006 | 11.3 | ||

| 1997 | 7.1 | 2007 | 6.4 | ||

| 1998 | 19 | 2008 | 14.7 | ||

| 1999 | 98.8 | 2009 | −0.2 | ||

| 2000 | 59.4 | 2010 | 6.9 |

| 1961 | 33.33 | 1971 | 8.7 | 1981 | 50 |

| 1962 | −30 | 1972 | 20 | 1982 | −16.67 |

| 1963 | 0 | 1973 | 0 | 1983 | −50 |

| 1964 | 3.57 | 1974 | 0 | 1984 | 33.33 |

| 1965 | 3.45 | 1975 | 0 | 1985 | 10 |

| 1966 | 33.33 | 1976 | 16.67 | 1986 | −9.09 |

| 1967 | 25 | 1977 | 42.86 | 1987 | 120 |

| 1968 | 0 | 1978 | 0 | 1988 | 0 |

| 1969 | 0 | 1979 | −10 | 1989 | 0 |

| 1970 | −8 | 1980 | 33.33 | 1990 | 0 |

| 1991 | 0 | 2001 | −60 | 2011 | −12.5 |

| 1992 | 40.91 | 2002 | 70 | 2012 | 28.57 |

| 1993 | 30.65 | 2003 | −41.18 | 2013 | 13.89 |

| 1994 | 4220.99 | 2004 | −20 | 2014 | 7.32 |

| 1995 | 471.43 | 2005 | −43.75 | 2015 | 6.82 |

| 1996 | −61 | 2006 | 277.78 | ||

| 1997 | 15.38 | 2007 | 17.65 | ||

| 1998 | 61.11 | 2008 | 50 | ||

| 1999 | 148.28 | 2009 | 0 | ||

| 2000 | 177.78 | 2010 | 33.33 |

| Sample | Sample | Sample | |

|---|---|---|---|

| Variable | 1975–2015 | 1975–2015 (without 1993, 1999) | 1961–2015 (without 1993, 1999) |

| Intercept | 15.683 (5.398) | 11.032 (2.796) | 9.288 (2.171) |

| 0.026 (0.162) | |||

| 0.083 (0.005) | 0.085 (0.001) | 0.085 (0.001) | |

| 0.040 (0.013) | 0.043 (0.001) | 0.044 (0.001) | |

| R2 | 0.858 | 0.967 | 0.964 |

| p value tests | |||

| Normality | 0.000 | 0.131 | 0.000 |

| Autocorrelation | 0.010 | 0.037 | 0.008 |

| Variable | Version 1 | Variable | Version 2 | ||

|---|---|---|---|---|---|

| Intercept | 1.828 | (3.240) | Intercept | 0.315 | (2.811) |

| 0.554 | (0.037) | 0.893 | (0.134) | ||

| 0.240 | (0.066) | 0.190 | (0.065) | ||

| 0.209 | (0.060) | 0.051 | (0.099) | ||

| 0.190 | (0.085) | −0.023 | (0.078) | ||

| 0.402 | (0.068) | 0.232 | (0.061) | ||

| 0.430 | (0.073) | 0.049 | (0.050) | ||

| 0.319 | (0.100) | 0.084 | (0.050) | ||

| −0.264 | (0.098) | ||||

| R2 | 0.932 | 0.944 | |||

| p value tests | |||||

| Normality | 0.184 | 0.645 | |||

| Autocorrelation | 0.149 | 0.740 | |||

| RMSPE, in sample | 19.305 | 18.363 | |||

| Years | Potential Causes |

|---|---|

| 1900s | Gold rush (Lawa railway construction) |

| 1930s | Economic decline, social upheaval in the form of riots |

| 1940s | WW II |

| 1957 | Establishment of the Central Bank of Suriname, Brokopondo-agreement with Alcoa and Eisenhower Recession |

| Parameters | Sample | |||

|---|---|---|---|---|

| 1961–2015 | 1873–2015 | |||

| μ | 1.457 | (0.200) | 1.595 | (0.219) |

| ρ | 0.327 | (0.089) | 0.314 | (0.096) |

| ω | −0.939 | (0.249) | −0.311 | (0.103) |

| 1.073 | (0.308) | 0.311 | (0.113) | |

| 0.711 | (0.182) | 0.208 | (0.095) | |

| 0.659 | (0.146) | 0.855 | (0.048) | |

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Franses, P.H.; Janssens, E. Recovering Historical Inflation Data from Postage Stamps Prices. J. Risk Financial Manag. 2017, 10, 21. https://doi.org/10.3390/jrfm10040021

Franses PH, Janssens E. Recovering Historical Inflation Data from Postage Stamps Prices. Journal of Risk and Financial Management. 2017; 10(4):21. https://doi.org/10.3390/jrfm10040021

Chicago/Turabian StyleFranses, Philip Hans, and Eva Janssens. 2017. "Recovering Historical Inflation Data from Postage Stamps Prices" Journal of Risk and Financial Management 10, no. 4: 21. https://doi.org/10.3390/jrfm10040021

APA StyleFranses, P. H., & Janssens, E. (2017). Recovering Historical Inflation Data from Postage Stamps Prices. Journal of Risk and Financial Management, 10(4), 21. https://doi.org/10.3390/jrfm10040021