The Economic Viability of PV Power Plant Based on a Neural Network Model of Electricity Prices Forecast: A Case of a Developing Market

Abstract

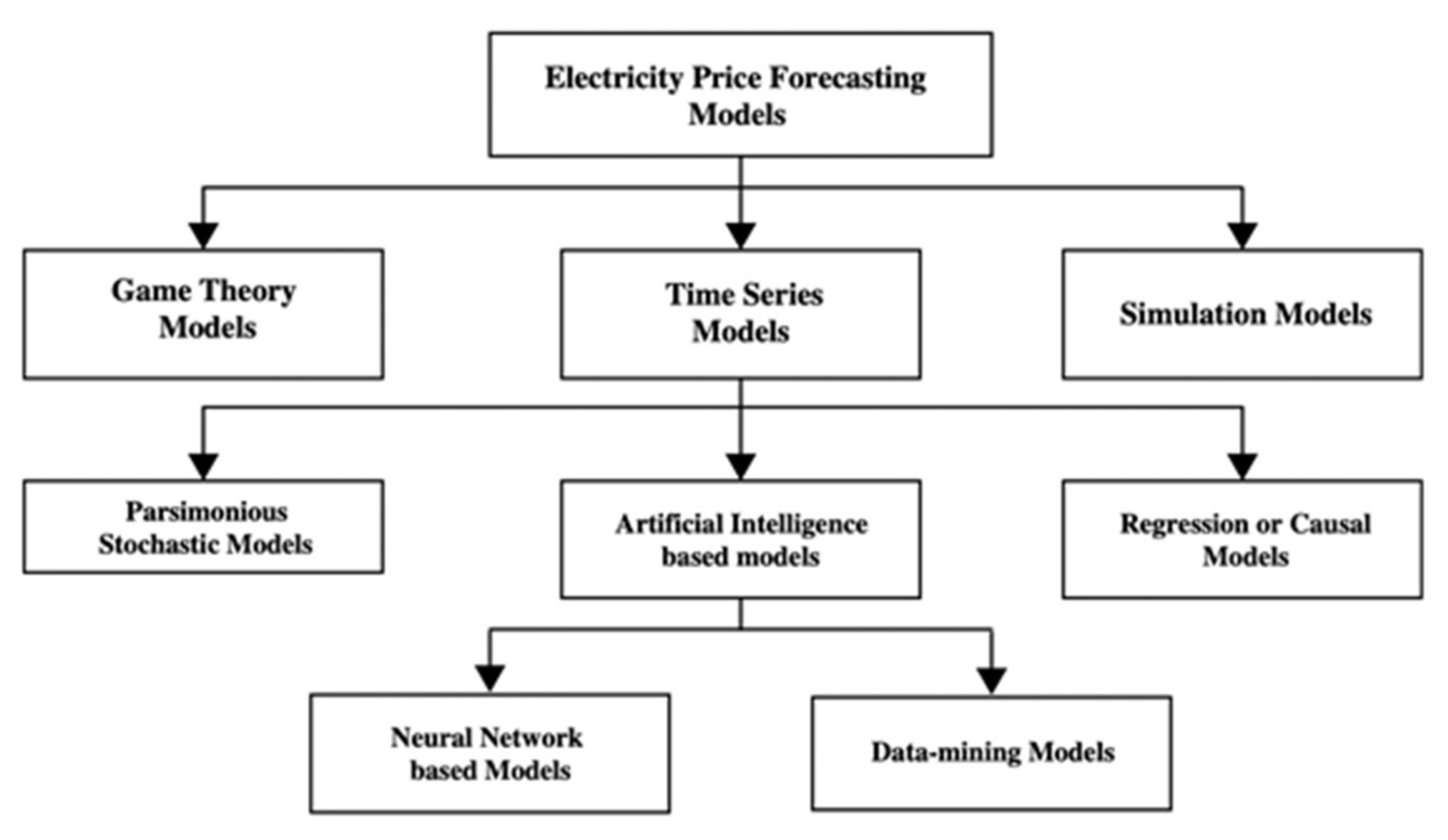

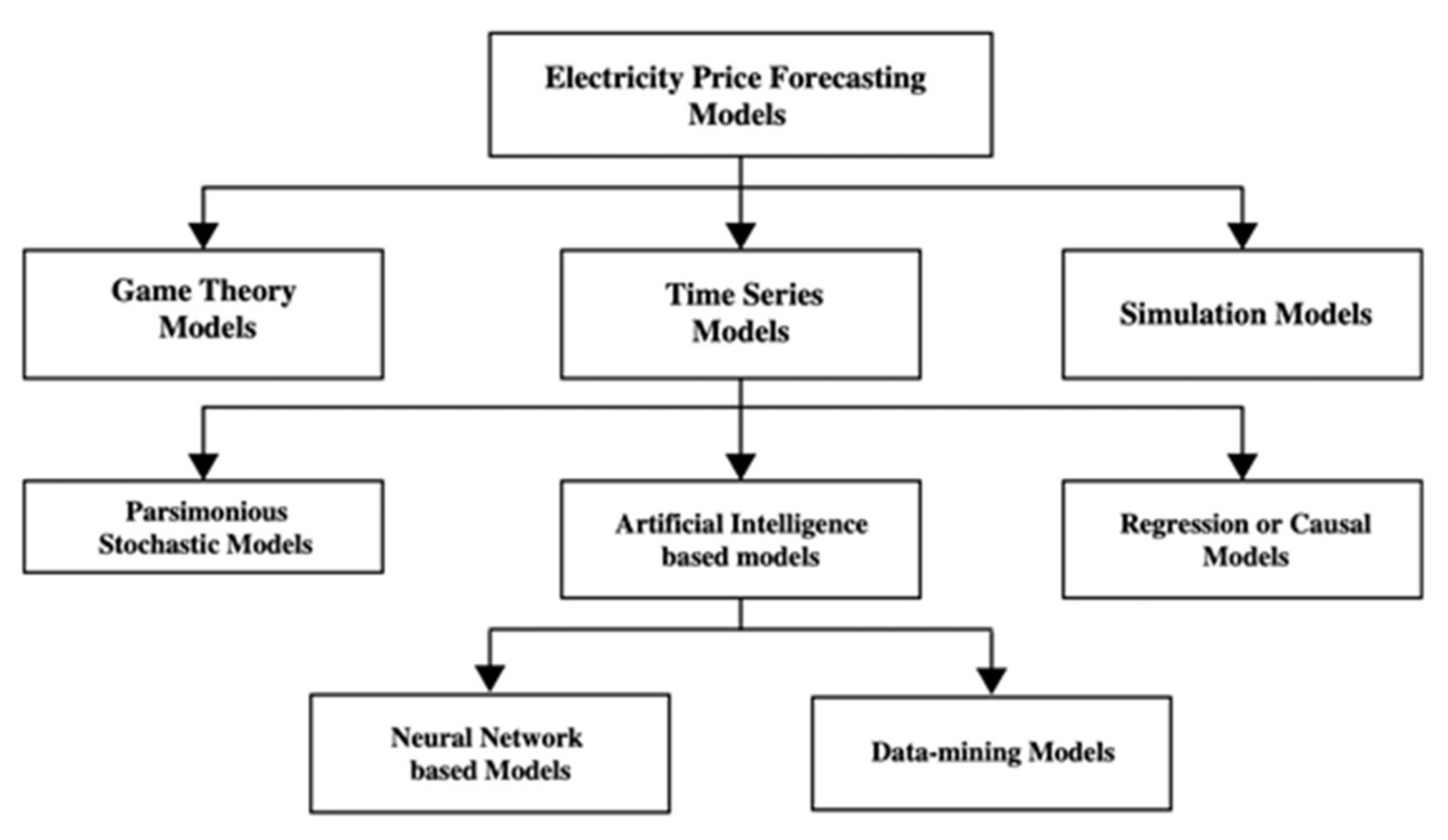

:1. Introduction

2. Methods

- -

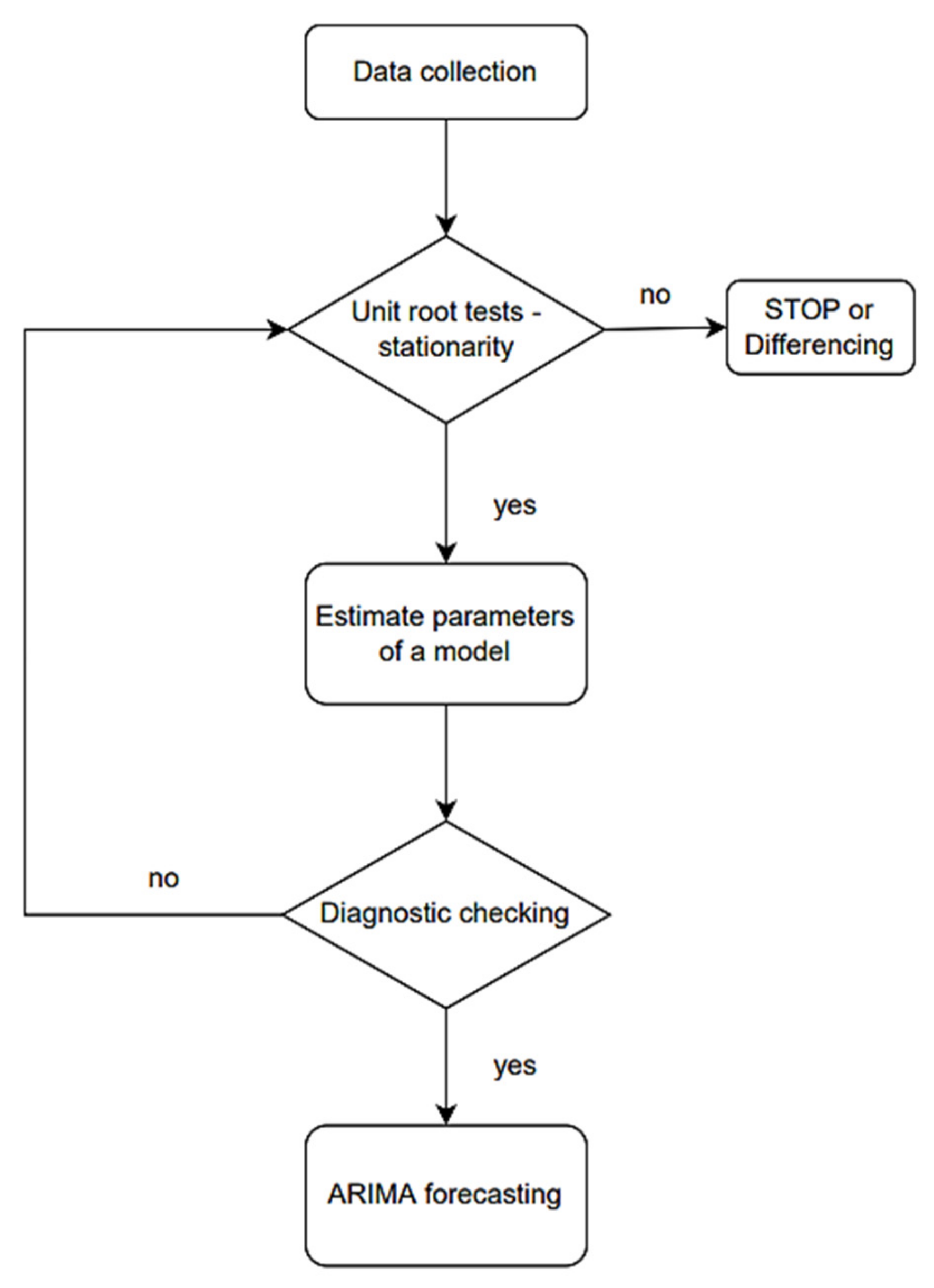

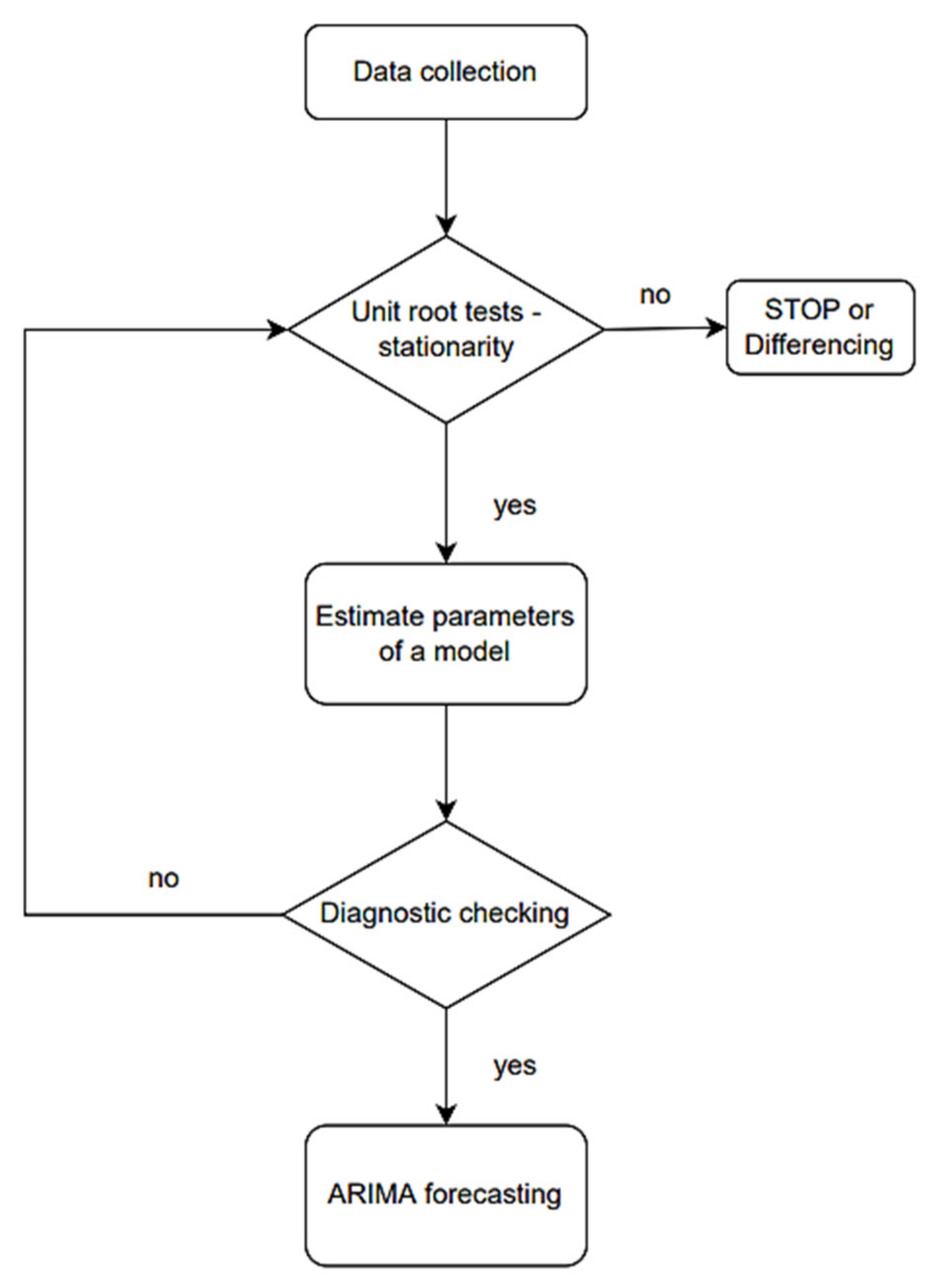

- Examining the stationarity of the observed series as a condition for model specifications. If the series is stationary, the procedure continues the step 3, if not–with step 2.

- -

- Testing the stationarity of the first difference of the observed series.

- -

- Determining the appropriate ARIMA model based on the ACF and PACF values.

- -

- Evaluating the ARIMA model.

- -

- Examining the statistical significance of the model parameters. If they are not significant, the p and q order has to be reduced.

- -

- Calculating the ACF and PACF residual model (if model is well-estimated, it should be close to zero).

- -

- Deciding on the best model, according to information criteria and adjusted coefficients of determination. If the model is appropriate, an ARIMA forecast could be obtained. If not, the previous step should be repeated.

3. Case Study

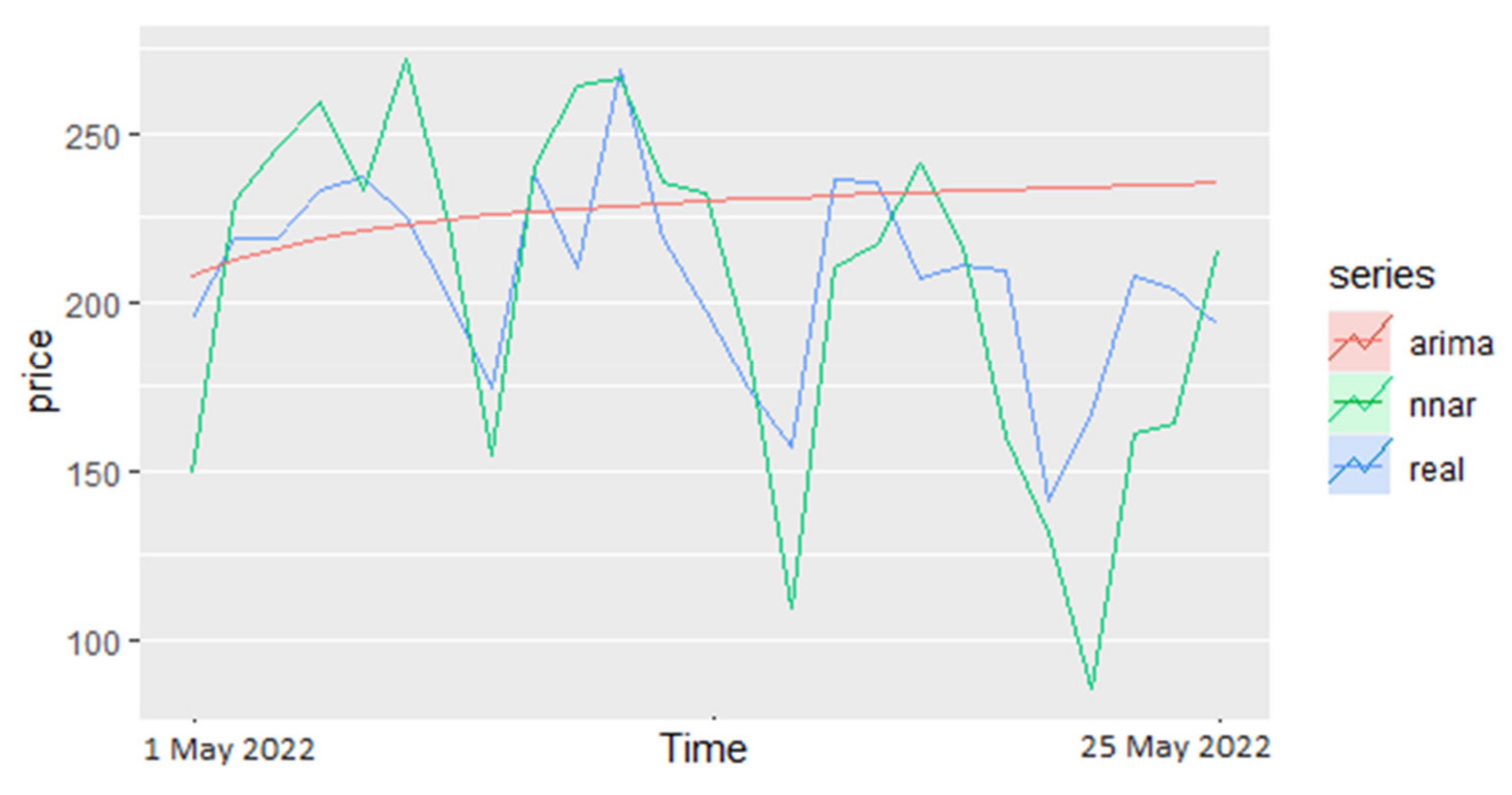

4. Results

5. Discussion and Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Manoj Kumar, N.; Sudhakar, K.; Samykano, M. Techno-Economic Analysis of 1 MWp Grid Connected Solar PV Plant in Malaysia. Int. J. Ambient Energy 2019, 40, 434–443. [Google Scholar] [CrossRef]

- Althuwaini, Y.E.Y.Y.E.; Philbin, S.P. Techno-Economic Analysis of Solar Power Plants in Kuwait: Modelling the Performance of PV and CSP Systems. Int. J. Renew. Energy Res. 2021, 11, 2009–2024. [Google Scholar] [CrossRef]

- Saleh, A.; Faridun, M.; Tajuddin, N.; Eddine, T.; Zidane, K.; Su, C.; Jawad, A.; Alrubaie, K.; Alwazzan, M.J. Techno-Economic and Environmental Evaluation of PV/Diesel/Battery Hybrid Energy System Using Improved Dispatch Strategy. Energy Rep. 2022, 8, 6794–6814. [Google Scholar] [CrossRef]

- IEA. Electricity Market Report; IEA: Paris, France, 2022. [Google Scholar]

- Agga, A.; Abbou, A.; Labbadi, M.; El Houm, Y. Short-Term Self Consumption PV Plant Power Production Forecasts Based on Hybrid CNN-LSTM, ConvLSTM Models. Renew. Energy 2021, 177, 101–112. [Google Scholar] [CrossRef]

- Gürtürk, M. Economic Feasibility of Solar Power Plants Based on PV Module with Levelized Cost Analysis. Energy 2019, 171, 866–878. [Google Scholar] [CrossRef]

- Solouki, A.; Jaffer, S.A.; Chaouki, J. Process Development and Techno-Economic Analysis of Microwave-Assisted Demetallization and Desulfurization of Crude Petroleum Oil. Energy Rep. 2022, 8, 4373–4385. [Google Scholar] [CrossRef]

- Le, P.T.; Nguyen, V.D.; Le, P.L. Techno-Economic Analysis of Solar Power Plant Project in Binh Thuan, Vietnam. In Proceedings of the 2018 4th International Conference on Green Technology and Sustainable Development (GTSD), Ho Chi Minh City, Vietnam, 23–24 November 2018; pp. 82–85. [Google Scholar] [CrossRef]

- Elnajjar, H.M.; Shehata, A.S.; Elbatran, A.H.A.; Shehadeh, M.F. Experimental and Techno-Economic Feasibility Analysis of Renewable Energy Technologies for Jabel Ali Port in UAE. Energy Rep. 2021, 7, 116–136. [Google Scholar] [CrossRef]

- Cui, T.; Wang, C.; Nie, P.Y. Economic Analysis of Marsh Gas Development in Countryside of China: A Case Study of Gongcheng County in Guangxi Province. Energy Rep. 2019, 5, 462–466. [Google Scholar] [CrossRef]

- Tcvetkov, P.; Cherepovitsyn, A.; Makhovikov, A. Economic Assessment of Heat and Power Generation from Small-Scale Liquefied Natural Gas in Russia. Energy Rep. 2020, 6, 391–402. [Google Scholar] [CrossRef]

- Zou, X.; Qiu, R.; Yuan, M.; Liao, Q.; Yan, Y.; Liang, Y.; Zhang, H. Sustainable Offshore Oil and Gas Fields Development: Techno-Economic Feasibility Analysis of Wind–Hydrogen–Natural Gas Nexus. Energy Rep. 2021, 7, 4470–4482. [Google Scholar] [CrossRef]

- Contreras, J.; Espínola, R.; Nogales, F.J.; Conejo, A.J. ARIMA Models to Predict Next-Day Electricity Prices. IEEE Trans. Power Syst. 2003, 18, 1014–1020. [Google Scholar] [CrossRef]

- Wu, L.; Shahidehpour, M. A Hybrid Model for Day-Ahead Price Forecasting. IEEE Trans. Power Syst. 2010, 25, 1519–1530. [Google Scholar] [CrossRef]

- Colantoni, A.; Villarini, M.; Monarca, D.; Carlini, M.; Mosconi, E.M.; Bocci, E.; Rajabi Hamedani, S. Economic Analysis and Risk Assessment of Biomass Gasification CHP Systems of Different Sizes through Monte Carlo Simulation. Energy Rep. 2021, 7, 1954–1961. [Google Scholar] [CrossRef]

- Anbazhagan, S.; Kumarappan, N. Day-Ahead Deregulated Electricity Market Price Forecasting Using Neural Network Input Featured by DCT. Energy Convers. Manag. 2014, 78, 711–719. [Google Scholar] [CrossRef]

- Zhou, X.; Yang, J.; Wang, F.; Xiao, B. Economic Analysis of Power Generation from Floating Solar Chimney Power Plant. Renew. Sustain. Energy Rev. 2009, 13, 736–749. [Google Scholar] [CrossRef]

- Gao, G.; Lo, K.; Fan, F.; Gao, G.; Lo, K.; Fan, F. Comparison of ARIMA and ANN Models Used in Electricity Price Forecasting for Power Market. Energy Power Eng. 2017, 9, 120–126. [Google Scholar] [CrossRef]

- Shafie-Khah, M.; Moghaddam, M.P.; Sheikh-El-Eslami, M.K. Price Forecasting of Day-Ahead Electricity Markets Using a Hybrid Forecast Method. Energy Convers. Manag. 2011, 52, 2165–2169. [Google Scholar] [CrossRef]

- Box, G.E.P.; Jenkins, G.M.; Reinsel, G.C.; Ljung, G.M. Time Series Analysis: Forecasting and Control, 5th ed.; Wiley: Hoboken, NJ, USA, 2015; ISBN 978-1-118-67502-1. [Google Scholar]

- Lo, K.L.; Wu, Y.K. Risk Assessment Due to Local Demand Forecast Uncertainty in the Competitive Supply Industry. IEE Proc. Gener. Transm. Distrib. 2003, 150, 573–582. [Google Scholar] [CrossRef]

- Chen, Z.; Zhang, D.; Jiang, H.; Wang, L.; Chen, Y.; Xiao, Y.; Liu, J.; Zhang, Y.; Li, M. Load Forecasting Based on LSTM Neural Network and Applicable to Loads of “Replacement of Coal with Electricity”. J. Electr. Eng. Technol. 2021, 16, 2333–2342. [Google Scholar] [CrossRef]

- Reza, A.; Debnath, T. An Approach to Make Comparison of ARIMA and NNAR Models For Forecasting Price of Commodities. 2020. Available online: https://www.researchgate.net/publication/342563043_An_Approach_to_Make_Comparison_of_ARIMA_and_NNAR_Models_For_Forecasting_Price_of_Commodities (accessed on 1 June 2022).

- Alfares, H.K.; Nazeeruddin, M. Electric Load Forecasting: Literature Survey and Classi®cation of Methods. Int. J. Syst. Sci. 2002, 33, 23–34. [Google Scholar] [CrossRef]

- Aggarwal, S.K.; Saini, L.M.; Kumar, A. Electricity Price Forecasting in Deregulated Markets: A Review and Evaluation. Int. J. Electr. Power Energy Syst. 2009, 31, 13–22. [Google Scholar] [CrossRef]

- Lago, J.; Marcjasz, G.; De Schutter, B.; Weron, R. Forecasting Day-Ahead Electricity Prices: A Review of State-of-the-Art Algorithms, Best Practices and an Open-Access Benchmark. Appl. Energy 2021, 293, 116983. [Google Scholar] [CrossRef]

- Jakaša, T.; Andročec, I.; Sprčić, P. Electricity Price Forecasting ARIMA Model Approach. In Proceedings of the 2011 8th International Conference on the European Energy Market (EEM), Zagreb, Croatia, 25–27 May 2011; pp. 222–225. [Google Scholar] [CrossRef]

- Box, G.E.P.G.M.J. Time Series Analysis, Control and Forecasting; Holden Day: San Francisco, CA, USA, 1976. [Google Scholar]

- Karadžić, V.; Pejovic, B. Inflation Forecasting in the Western Balkans and EU: A Comparison of Holt-Winters, ARIMA and NNAR Models. Amfiteatru Econ. 2021, 23, 517. [Google Scholar] [CrossRef]

- Nespoli, A.; Ogliari, E.; Pretto, S.; Gavazzeni, M.; Vigani, S.; Paccanelli, F. Electrical Load Forecast by Means of LSTM: The Impact of Data Quality. Forecast 2021, 3, 91–101. [Google Scholar] [CrossRef]

- Hochreiter, S.; Schmidhuber, J. Long Short-Term Memory. Neural Comput. 1997, 9, 1735–1780. [Google Scholar] [CrossRef]

- Sala, S.; Amendola, A.; Leva, S.; Mussetta, M.; Niccolai, A.; Ogliari, E. Comparison of Data-Driven Techniques for Nowcasting Applied to an Industrial-Scale Photovoltaic Plant. Energies 2019, 12, 4520. [Google Scholar] [CrossRef]

- Hyndman, R.J.; Athanasopoulos, G. Forecasting: Principles and Practice. Princ. Optim. Des. 2018, 504, 46–48. [Google Scholar]

- Da Silva, F.L.C.; da Costa, K.; Rodrigues, P.C.; Salas, R.; López-Gonzales, J.L. Statistical and Artificial Neural Networks Models for Electricity Consumption Forecasting in the Brazilian Industrial Sector. Energies 2022, 15, 588. [Google Scholar] [CrossRef]

- Han, J.; Moraga, C. The Influence of the Sigmoid Function Parameters on the Speed of Backpropagation Learning. Lect. Notes Comput. Sci. 1995, 930, 195–201. [Google Scholar] [CrossRef]

- Dubey, R.; Joshi, D.; Bansal, R.C. Optimization of Solar Photovoltaic Plant and Economic Analysis. Electr. Power Compon. Syst. 2016, 44, 2025–2035. [Google Scholar] [CrossRef]

- Zala, J.N.; Jain, P. Design and Optimization of a Biogas-Solar-Wind Hybrid System for Decentralized Energy Generation for Rural India. Int. Res. J. Eng. Technol. 2017, 37, 1–8. [Google Scholar]

- Al-Khori, K.; Bicer, Y.; Koç, M. Comparative Techno-Economic Assessment of Integrated PV-SOFC and PV-Battery Hybrid System for Natural Gas Processing Plants. Energy 2021, 222, 119923. [Google Scholar] [CrossRef]

- Sistem-MNE. Main Project Design-PV Kuči; Sistem-MNE: Podgorica, Montenegro, 2022. [Google Scholar]

- HUPX. Historic data. Available online: https://hupx.hu/en/market-data/dam/historical-data (accessed on 25 May 2022).

- Cedis Doo. Metodologija za odredjivanje cijena. Available online: http://cedis.me/regulativa/ (accessed on 25 May 2022).

- CGES. Metodologija za odredjivanje cijena prenosnih kapaciteta. Available online: https://www.cges.me/regulativa/interna-akta-cges-a (accessed on 25 May 2022).

- SEE CAO. Dnevni rezulatati aukcija. Available online: https://www.seecao.com/daily-results (accessed on 25 May 2022).

- Pexapark. PPA transaction database. Available online: https://pexapark.com/ppa-checklist/ (accessed on 25 May 2022).

- Damodaran, A. Useful Data Sets. Available online: https://pages.stern.nyu.edu/~adamodar/New_Home_Page/datacurrent.html (accessed on 20 June 2022).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| CAPEX Analysis | |

|---|---|

| Category | Amount |

| Land plot acquisition | EUR 250,000 |

| Grid connection fee | EUR 190,000 |

| Main project design | EUR 50,000 |

| Groundworks | EUR 210,000 |

| Concrete works | EUR 170,000 |

| Metal substructure with installation | EUR 375,000 |

| Solar modules and inverters with installation | EUR 1,650,000 |

| Substation with construction works | EUR 350,000 |

| Electric and other cables | EUR 280,000 |

| Supervision works | EUR 60,000 |

| Other construction works | EUR 180,000 |

| Overheads (10%) | EUR 376,500 |

| Total | EUR 4,141,500 |

| Total per kW | EUR 828.30 |

| Series | Values |

|---|---|

| Observations | 485 |

| Mean | 139.9281 |

| Median | 113.2758 |

| Maximum | 544.7283 |

| Minimum | 14.89583 |

| Std. Dev. | 85.20709 |

| Skewness | 0.951737 |

| Kurtosis | 3.950774 |

| Jarque–Bera | 91.48687 |

| Probability | 0 |

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

|---|---|---|---|---|

| C | 0.381232 | 0.173292 | 2.199938 | 0.0283 |

| AR (1) | 0.771313 | 0.036749 | 20.98848 | 0.0000 |

| MA (1) | −0.972690 | 0.013996 | −69.49627 | 0.0000 |

| Model |

|---|

| NNETAR Series: p1 NNAR (22,1,12) [365] Call: nnetar (y = p1, lambda = “0”) Average of 20 networks, each of which is a 23-12-1 network with 301 weights options were–linear output units |

| estimated as 0.0002105 |

| Model | ||

|---|---|---|

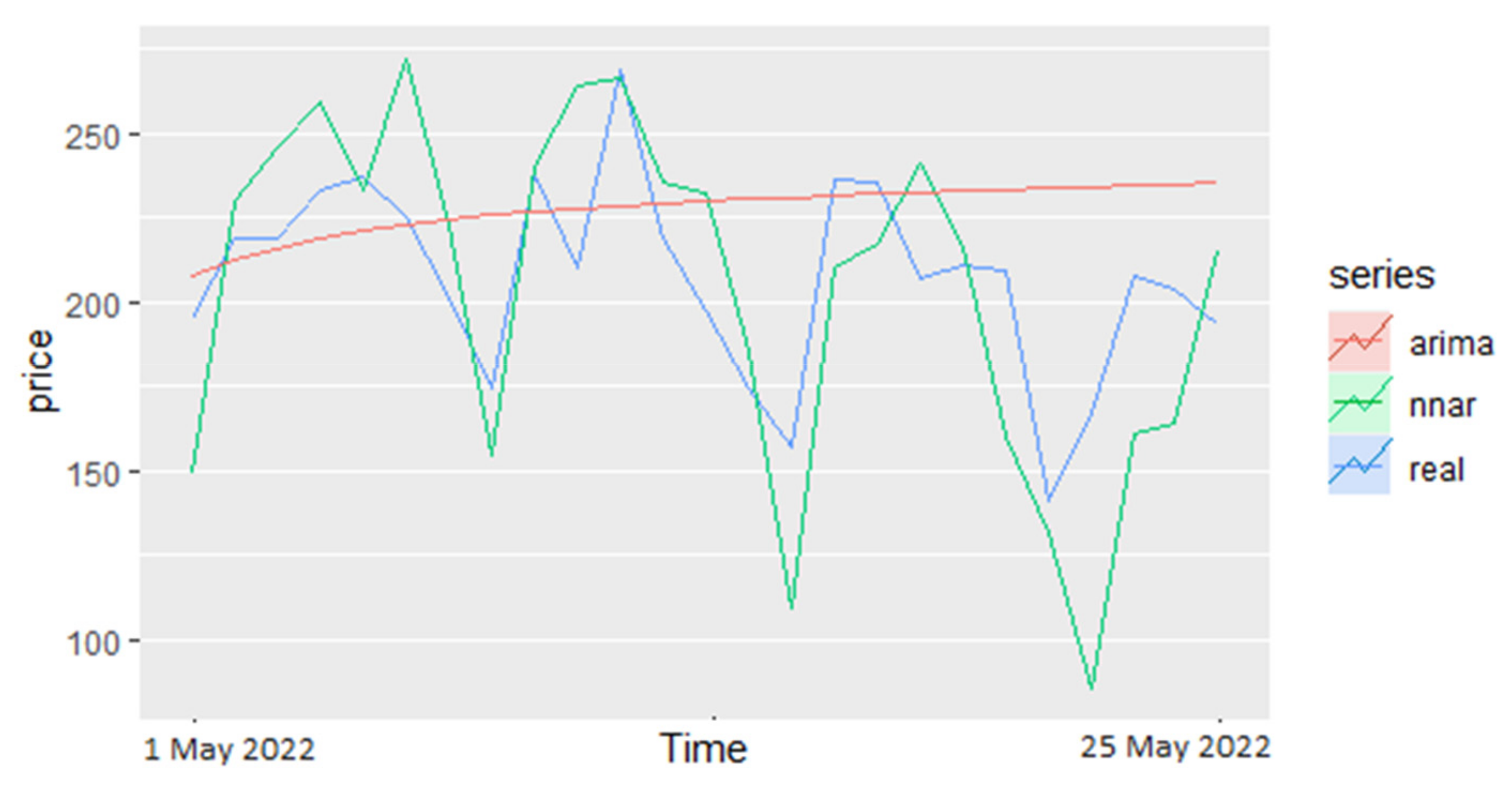

| Criteria | ARIMA | NNAR |

| ME | −20.26215 | 3.16550823 |

| RMSE | 36.89402 | 34.2124869 |

| MAE | 28.46972 | 28.2489473 |

| MPE | −12.20065 | 2.380968496 |

| MAPE | 15.54559 | 14.3177964 |

| Theil’s U | 1.0893 | 1.006192 |

| Model |

| NNAR (27,1,14) [365] Call: nnetar (y = p, lambda = “0”) Average of 20 networks, each of which is a 28-114-1 network with 421 weights options were–linear output units |

| estimated as 0.0001958 |

| Electricity Price Calculation | |

|---|---|

| Category | Amount |

| Average electricity price on HUPX | EUR 155.40 |

| Grid operator fee | EUR −13.00 |

| Balancing cost (% of the price on the market) | EUR −17.09 |

| Trader’s fee (% of the price on the market) | EUR −4.66 |

| Electricity price | EUR 120.64 |

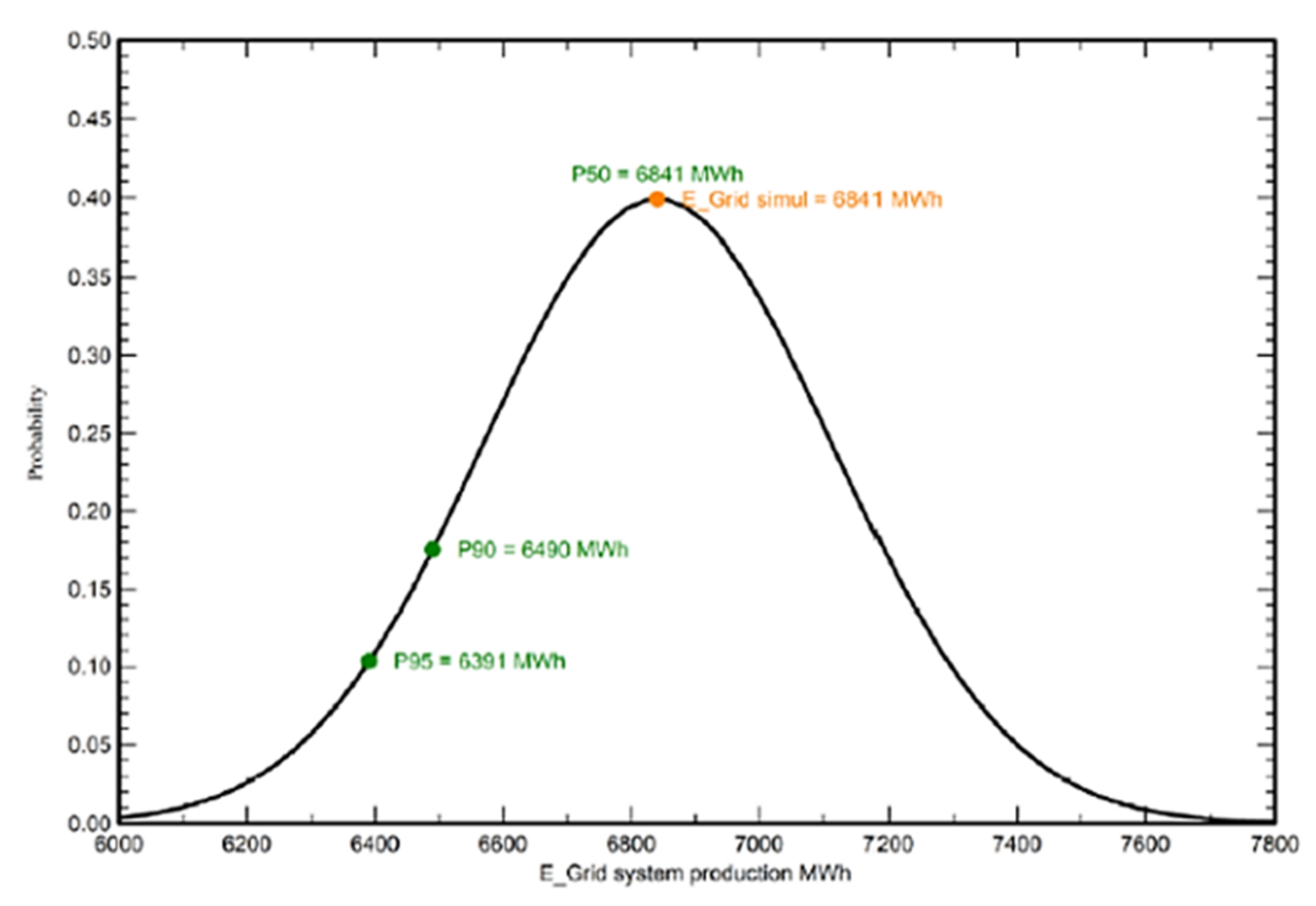

| Expected annual production (/MWh) | 6841 |

| Annual income | EUR 825,325.60 |

| Parameter | Unit | Value |

|---|---|---|

| NPV | € | 2,780,054.33 |

| LCOE | €/MWh | 58.89 |

| IRR | % | 12.93 |

| PBP | Years | 7.1 |

| Variables | Electricity Price −20% | Electricity Price +20% | Fixed PPA | Balancing Cost +30% | Balancing Cost −10% | Annual Production −10% | Annual Production +5% | WACC for Europe Instead of Emerging Markets |

|---|---|---|---|---|---|---|---|---|

| NPV | −24.28% | 24.28% | −36.92% | −4.66% | 1.56% | −25.81% | 12.91% | 3.85% |

| LCOE | −1.72% | 1.71% | −2.60% | −0.33% | 0.11% | 9.09% | −3.89% | −1.19% |

| IRR | −17.00% | 19.90% | −24.79% | −3.48% | 1.19% | −13.94% | 6.95% | 0.00% |

| PBP | 26.76% | −27.46% | 40.85% | 5.63% | −1.41% | 14.08% | −2.82% | −1.41% |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mišnić, N.; Pejović, B.; Jovović, J.; Rogić, S.; Đurišić, V. The Economic Viability of PV Power Plant Based on a Neural Network Model of Electricity Prices Forecast: A Case of a Developing Market. Energies 2022, 15, 6219. https://doi.org/10.3390/en15176219

Mišnić N, Pejović B, Jovović J, Rogić S, Đurišić V. The Economic Viability of PV Power Plant Based on a Neural Network Model of Electricity Prices Forecast: A Case of a Developing Market. Energies. 2022; 15(17):6219. https://doi.org/10.3390/en15176219

Chicago/Turabian StyleMišnić, Nikola, Bojan Pejović, Jelena Jovović, Sunčica Rogić, and Vladimir Đurišić. 2022. "The Economic Viability of PV Power Plant Based on a Neural Network Model of Electricity Prices Forecast: A Case of a Developing Market" Energies 15, no. 17: 6219. https://doi.org/10.3390/en15176219

APA StyleMišnić, N., Pejović, B., Jovović, J., Rogić, S., & Đurišić, V. (2022). The Economic Viability of PV Power Plant Based on a Neural Network Model of Electricity Prices Forecast: A Case of a Developing Market. Energies, 15(17), 6219. https://doi.org/10.3390/en15176219