Exploring the Impact and Path of Environmental Protection Tax on Different Air Pollutant Emissions

Abstract

:1. Introduction

2. Literature Review and Hypothesis

2.1. Environmental Protection Tax and Pollutants Emission

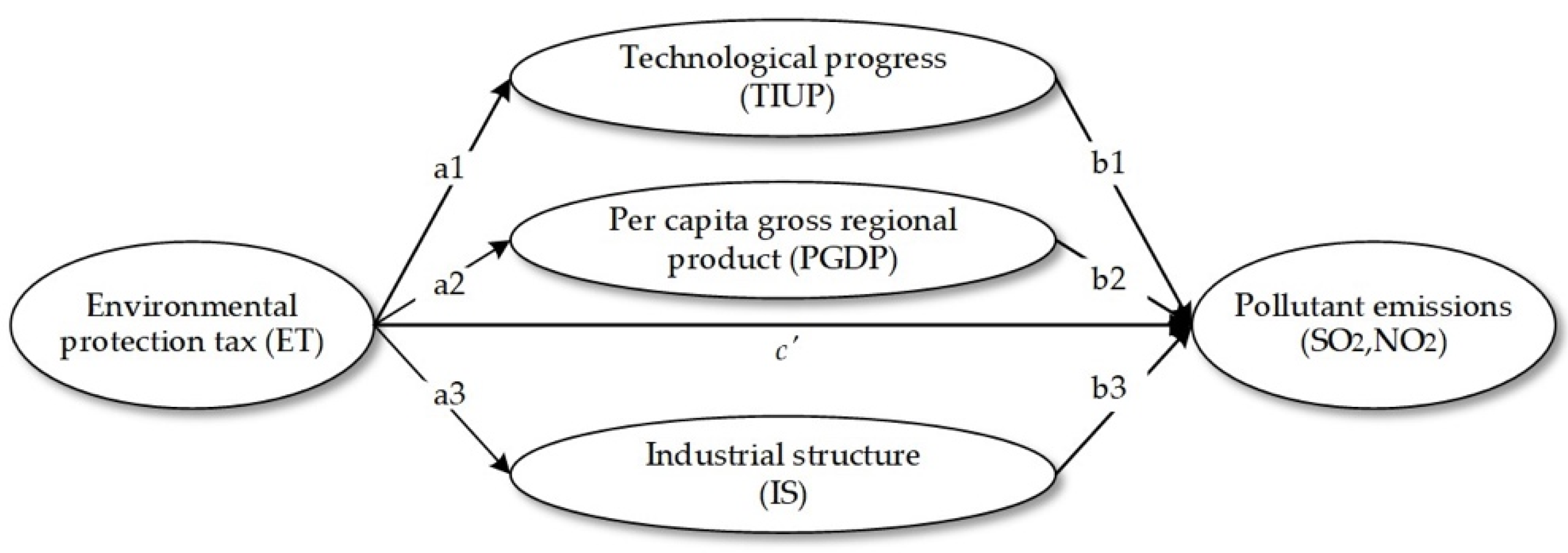

2.2. Analysis of the Path of Environmental Protection Tax to Different Pollutants Emissions

2.3. Hypotheses

3. Methods and Data

3.1. Models

3.1.1. Panel Threshold Regression Model

3.1.2. Mediating Effect Model

3.2. Variables

3.2.1. Dependent Variable

3.2.2. Independent Variable

3.2.3. Mediating Variable

3.2.4. Control Variable

3.3. Data

4. Results and Discussion

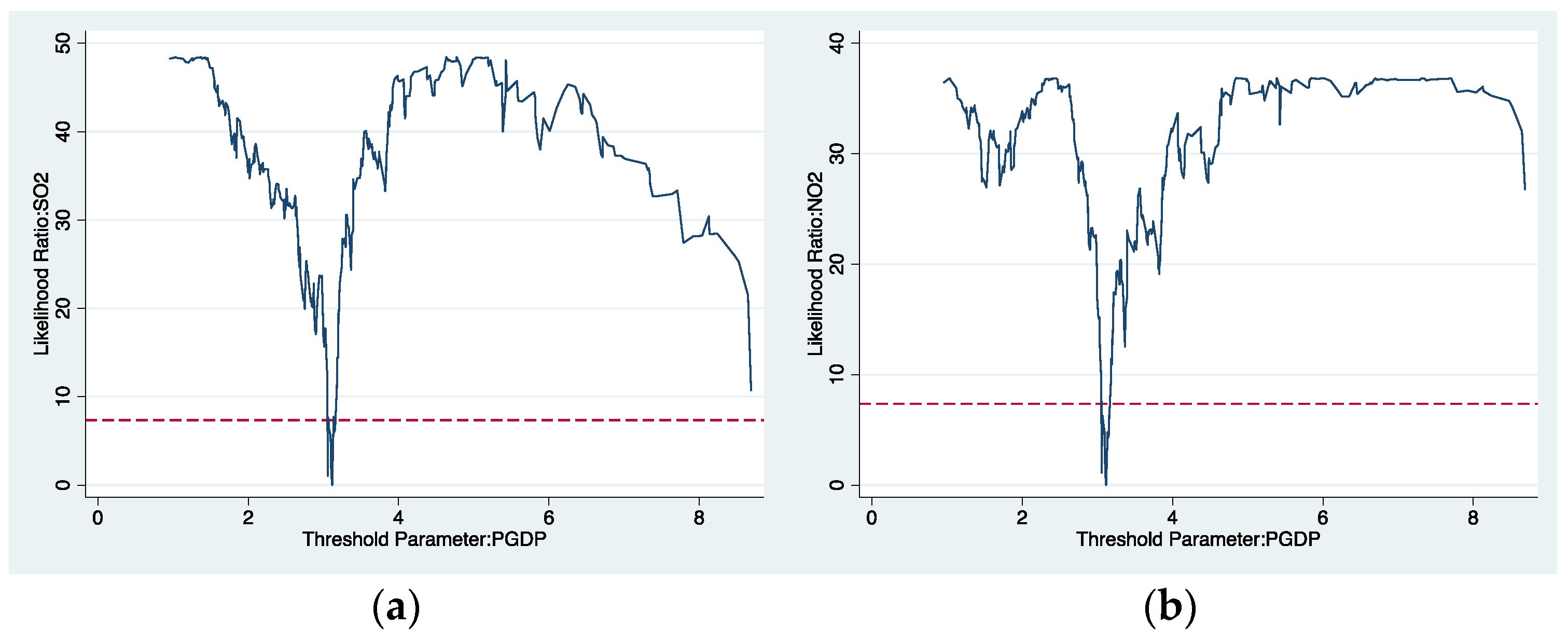

4.1. Threshold Effect of Environment Protection Tax on Pollutants Emission

4.1.1. Threshold Effect of Environmental Protection Tax on SO2 and NO2

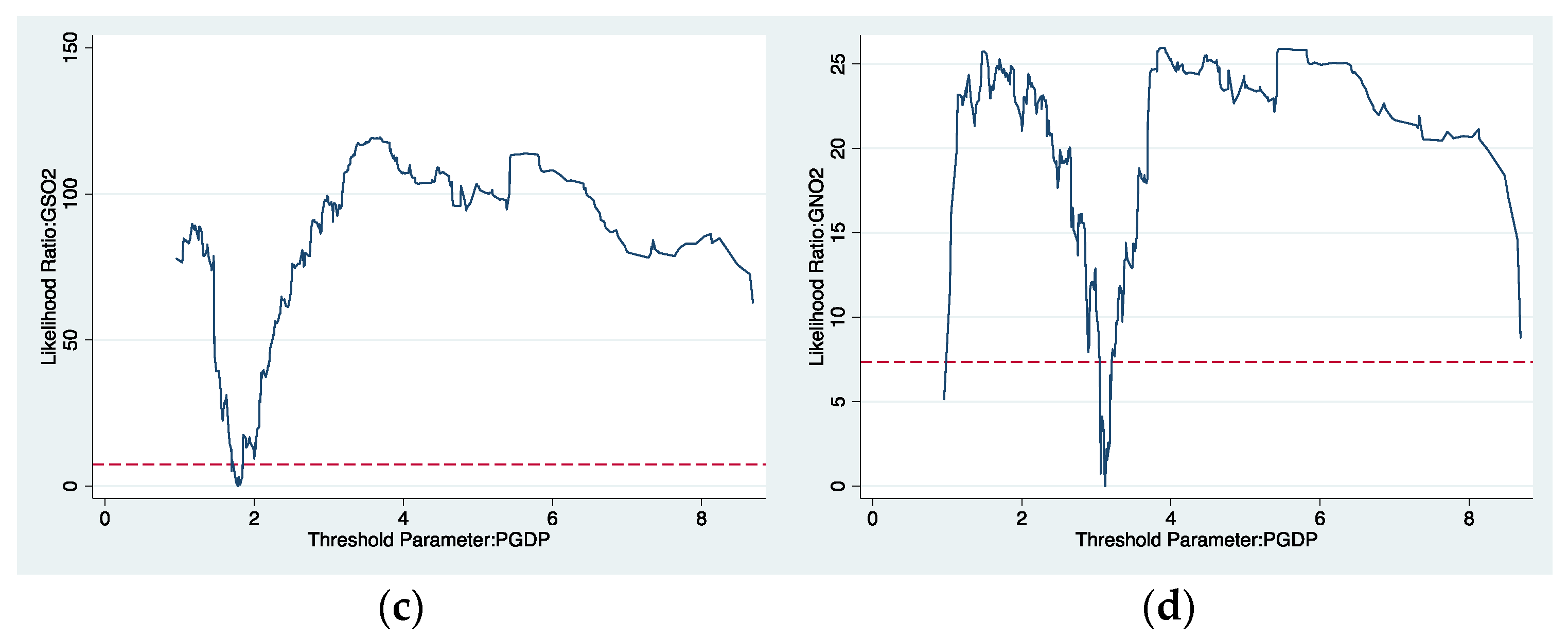

4.1.2. Threshold Effect of Environmental Protection Tax on GSO2 and GNO2

4.2. Mediating Effect of Environmental Protection Tax on Pollutants Emission

4.2.1. Mediating Effect of Environmental Protection Tax on SO2 and NO2

4.2.2. Mediating Effect of Environmental Protection Tax on GSO2 and GNO2

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Itaya, J.-I. Can Environmental Taxation Stimulate Growth? The role of indeterminacy in endogenous growth models with environmental externalities. J. Econ. Dyn. Control 2008, 32, 1156–1180. [Google Scholar] [CrossRef]

- Abdullah, S.; Morley, B. Environmental taxes and economic growth: Evidence from panel causality tests. Energ. Econ. 2014, 42, 27–33. [Google Scholar] [CrossRef] [Green Version]

- Feng, Y.Q.; Yu, X.Y.; Chiu, Y.H.; Lin, T.Y. Energy efficiency and health efficiency of old and new EU member states. Front. Public Health 2020, 8, 168. [Google Scholar] [CrossRef]

- Zhou, Z.B.; Zhang, W.G.; Pan, X.X.; Hu, J.F.; Pu, G.L. Environmental tax reform and the "double dividend" hypothesis in a small open economy. Int. J. Env. Res. Pub. Health 2020, 17, 217. [Google Scholar] [CrossRef] [Green Version]

- Sun, Y.Y.; Zhi, Y.; Zhao, Y.W. Indirect effects of carbon taxes on water conservation: A water footprint analysis for China. J. Environ. Manag. 2021, 279, 111747. [Google Scholar] [CrossRef]

- Hu, X.; Liu, Y.; Yang, L.; Shi, Q.; Zhang, W.; Zhong, C. SO2 emission reduction decomposition of environmental tax based on different consumption tax refunds. J. Clean. Prod. 2018, 186, 997–1010. [Google Scholar] [CrossRef]

- Hu, H.; Dong, W.; Zhou, Q. A comparative study on the environmental and economic effects of a resource tax and carbon tax in China: Analysis based on the computable general equilibrium model. Energy Policy 2021, 156, 112460. [Google Scholar] [CrossRef]

- Baron, R.M.; Kenny, D.A. The moderator mediator variable distinction in social psychological-research-conceptual, strategic, and statistical considerations. J. Pers. Soc. Psychol. 1986, 51, 1173–1182. [Google Scholar] [CrossRef] [PubMed]

- Preacher, K.J.; Hayes, A.F. SPSS and SAS procedures for estimating indirect effects in simple mediation models. Behav. Res. Methods Instrum. Comput. 2004, 36, 717–731. [Google Scholar] [CrossRef] [Green Version]

- Zhao, X.; Lynch, J.G., Jr.; Chen, Q. Reconsidering Baron and Kenny: Myths and truths about mediation analysis. J. Consum. Res 2010, 37, 197–206. [Google Scholar] [CrossRef]

- Wang, Y.; Yu, L. Can the current environmental tax rate promote green technology innovation? Evidence from China’s resource-based industries. J. Clean. Prod. 2021, 278, 123443. [Google Scholar] [CrossRef]

- Lei, Z.J.; Huang, L.Y.; Cai, Y. Can environmental tax bring strong porter effect? Evidence from Chinese Listed Companies. Environ. Sci. Pollut. Res. 2022, 29, 171199. [Google Scholar] [CrossRef] [PubMed]

- Lu, J. Can environmental protection tax aggravate illegal pollution discharge of heavy polluting enterprises? Environ. Sci. Pollut. Res. 2022, 29, 180023. [Google Scholar] [CrossRef] [PubMed]

- Han, F.; Li, J. Assessing impacts and determinants of China’s environmental protection tax on improving air quality at provincial level based on bayesian statistics. J. Environ. Manag. 2020, 271, 111017. [Google Scholar] [CrossRef]

- Li, G.; Zhang, R.S.; Masui, T. CGE modeling with disaggregated pollution treatment sectors for assessing China’s environmental tax policies. Sci. Total Environ. 2021, 761, 143264. [Google Scholar] [CrossRef]

- Zhao, L.; Yang, C.; Su, B.; Zeng, S. Research on a single policy or policy mix in carbon emissions reduction. J. Clean. Prod. 2020, 267, 122030. [Google Scholar] [CrossRef]

- Xu, J.; Wei, W.X. Would carbon tax be an effective policy tool to reduce carbon emission in China? Policies simulation analysis based on a CGE model. Appl. Econ. 2022, 54, 115–134. [Google Scholar] [CrossRef]

- Shahzad, U. Environmental taxes, energy consumption, and environmental quality: Theoretical survey with policy implications. Environ. Sci. Pollut. Res. 2020, 27, 24848–24862. [Google Scholar] [CrossRef]

- Fredriksson, P.G. How pollution taxes may increase pollution and reduce net revenues. Public Choice 2001, 107, 65–85. [Google Scholar] [CrossRef]

- Tobin, I.; Cho, W. Performance tools and their impact on pollution reduction: An assessment of environmental taxation and R&D. Int. Rev. Public Adm. 2010, 15, 53–65. [Google Scholar]

- Fan, X.; Li, X.; Yin, J. Impact of environmental tax on green development: A nonlinear dynamical system analysis. PLoS ONE 2019, 14, e0221264. [Google Scholar] [CrossRef] [PubMed]

- Karmaker, S.C.; Hosan, S.; Chapman, A.J.; Saha, B.B. The role of environmental taxes on technological innovation. Energy 2021, 232, 121052. [Google Scholar] [CrossRef]

- Safi, A.; Chen, Y.; Wahab, S.; Zheng, L.; Rjoub, H. Does environmental taxes achieve the carbon neutrality target of G7 economies? Evaluating the importance of environmental R&D. J. Environ. Manag. 2021, 293, 112908. [Google Scholar]

- Wang, J.; Wang, K.; Shi, X.; Wei, Y.-M. Spatial heterogeneity and driving forces of environmental productivity growth in China: Would it help to switch pollutant discharge fees to environmental taxes? J. Clean. Prod. 2019, 223, 36–44. [Google Scholar] [CrossRef]

- Castiglione, C.; Infante, D.; Minervini, M.T.; Smirnova, J. Environmental taxation in Europe: What does it depend on? Cogent Econo. Financ. 2014, 2, 967362. [Google Scholar] [CrossRef]

- Miceikiene, A. Assessment of the effect of environmental taxes on environmental protection. Ekon. Časopis 2018, 3, 286–308. [Google Scholar]

- He, P.; Ning, J.; Yu, Z.; Xiong, H.; Shen, H.; Jin, H. Can environmental tax policy really help to reduce pollutant emissions? An empirical study of a panel ARDL model based on OECD countries and China. Sustainability 2019, 11, 4384. [Google Scholar] [CrossRef] [Green Version]

- Hu, X.; Sun, Y.; Liu, J.; Meng, J.; Wang, X.; Yang, H.; Tao, S. The impact of environmental protection tax on sectoral and spatial distribution of air pollution emissions in China. Environ. Res. Lett. 2019, 14, 054013. [Google Scholar] [CrossRef]

- Esen, Ö.; Yıldırım, D.Ç.; Yıldırım, S. Pollute less or tax more? Asymmetries in the EU environmental taxes—Ecological balance nexus. Environ. Impact Assess. 2021, 91, 106662. [Google Scholar] [CrossRef]

- Brock, W.; Taylor, M.S. Economic growth and the environment: A review of theory and empirics. Handb. Econ. Growth 2005, 1, 1749–1821. [Google Scholar]

- Gerlagh, R.; Kuik, O. Spill or leak? Carbon leakage with international technology spillovers: A CGE analysis. Energ. Econ. 2014, 45, 381–388. [Google Scholar] [CrossRef]

- Huang, L.; Liu, S.; Han, Y.; Peng, K. The nature of state-owned enterprises and collection of pollutant discharge fees: A study based on Chinese industrial enterprises. J. Clean. Prod. 2020, 271, 122420. [Google Scholar] [CrossRef]

- Fernández, Y.F.; López, M.F.; Blanco, B.O. Innovation for sustainability: The impact of R&D spending on CO2 emissions. J. Clean. Prod. 2018, 172, 3459–3467. [Google Scholar]

- Niu, T.; Yao, X.; Shao, S.; Li, D.; Wang, W. Environmental tax shocks and carbon emissions: An estimated DSGE model. Struct. Change Econ. Dyn. 2018, 47, 9–17. [Google Scholar] [CrossRef]

- Taylor, A.B.; MacKinnon, D.P.; Tein, J.Y. Tests of the three-path mediated effect. Organ. Res. Methods 2008, 11, 241–269. [Google Scholar] [CrossRef]

- Mackinnon, D.P.; Warsi, G.; Dwyer, J.H. A simulation study of mediated effect measures. Multivar. Behav. Res. 1995, 30, 41–62. [Google Scholar] [CrossRef] [Green Version]

- MacKinnon, D.P.; Lockwood, C.M.; Hoffman, J.M.; West, S.G.; Sheets, V. A comparison of methods to test mediation and other intervening variable effects. Psychol. Methods 2002, 7, 83–104. [Google Scholar] [CrossRef]

- Iacobucci, D. Mediation analysis and categorical variables: The final frontier. J. Consum. Psychol. 2012, 22, 582–594. [Google Scholar] [CrossRef]

- Morley, B. Empirical evidence on the effectiveness of environmental taxes. Appl. Econo. Lett. 2012, 19, 1817–1820. [Google Scholar] [CrossRef] [Green Version]

- Huang, J.; Li, X.; Wang, Y.; Lei, H. The effect of energy patents on China’s carbon emissions: Evidence from the STIRPAT model. Technol. Forecast. Soc. 2021, 173, 121110. [Google Scholar] [CrossRef]

- Grossman, G.M.; Krueger, A.B. Economic growth and the environment. Q. J. Econ. 1995, 110, 353–377. [Google Scholar] [CrossRef] [Green Version]

- Holtz-Eakin, D.; Selden, T.M. Stoking the fires? CO2 emissions and economic growth. J. Pub. Econ. 1995, 57, 85–101. [Google Scholar] [CrossRef] [Green Version]

- Cole, M.A.; Rayner, A.J.; Bates, J.M. The environmental kuznets curve: An empirical analysis. Environ. Dev. Econ. 1997, 2, 401–416. [Google Scholar] [CrossRef]

- Dehnavi, J.; Haghnejad, A. Energy consumption, economic growth, and pollution in selected OPEC countries: Testing the environmental kuzents curve hypothesis. J. Acad. Res. Econ. 2012, 4, 149–166. [Google Scholar]

- Yang, T.; Zhu, Y.; Li, Y.; Zhou, B. Achieving win-win policy outcomes for water resource management and economic development: The experience of Chinese cities. Sustain. Prod. Consump. 2021, 27, 873–888. [Google Scholar] [CrossRef]

- Park, E.J.; Sung, H.C.; Seo, J.Y.; Kang, K.Y.; Sung, M.S. Analyses of residents satisfaction with the differences in green space infrastructure for three cities, Gwacheon, Uiwang, and Hanam. J. Korean Soc. Environ. Restor. Technol. 2007, 10, 60–70. [Google Scholar]

- Liu, C.; Li, L. Place-based techno-industrial policy and innovation: Government responses to the information revolution in China. China Econ. Rev. 2021, 66, 101600. [Google Scholar] [CrossRef]

- Hsu, C.-C.; Zhang, Y.; Ch, P.; Aqdas, R.; Chupradit, S.; Nawaz, A. A step towards sustainable environment in China: The role of eco-innovation renewable energy and environmental taxes. J. Environ. Manag. 2021, 299, 113609. [Google Scholar] [CrossRef]

- Yao, X.; Kou, D.; Shao, S.; Li, X.; Wang, W.; Zhang, C. Can urbanization process and carbon emission abatement be harmonious? New evidence from China. Environ. Impact Assess. 2018, 71, 70–83. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Variable | Meaning | Index or Source | |

|---|---|---|---|

| Dependent variable | SO2 | Sulfur dioxide emissions scale | Volume of sulfur dioxide emissions |

| NO2 | Nitrogen oxide emissions scale | Volume of nitrogen dioxide emissions | |

| GSO2 | Sulfur dioxide emissions intensity | Emissions per unit GDP | |

| GNO2 | Nitrogen oxides emissions intensity | Emissions per unit GDP | |

| Independent variable | BET | Environmental protection tax | China Statistical Yearbook on Environment |

| Mediating variable | TIUP | Technological progress | Total of invention and utility patents |

| PGDP | Per capita GDP | Per capita GDP | |

| IS | Industrial structure | Ratio of added value of tertiary industry to secondary industry | |

| Control variable | PCP | Per capita park green area | Per capita park green area |

| FSS | Fiscal self-sufficiency rate | Ratio of budgeted expenditure/budgeted income |

| Variable | Unit | Mean | Std. Dev. | Min | Max | Obs |

|---|---|---|---|---|---|---|

| ESO2 | Hundred thousand tons | 48.880 | 37.676 | 0.088 | 162.864 | 390 |

| ENO2 | Hundred thousand tons | 39.406 | 30.033 | 0.801 | 127.360 | 390 |

| GSO2 | Ton/hundred million yuan | 50.305 | 52.745 | 0.036 | 369.923 | 390 |

| GNO2 | Ton/hundred million yuan | 35.964 | 34.208 | 0.33 | 291.191 | 390 |

| BET | % | 17.160 | 6.096 | 4.237 | 43.905 | 390 |

| TIUP | Ten thousand piece | 2.869 | 4.476 | 0.011 | 34.248 | 390 |

| PGDP | Ten thousand yuan/person | 3.617 | 1.902 | 0.692 | 11.261 | 390 |

| ISR | / | 8.094 | 9.706 | 1.289 | 59.186 | 390 |

| ISU | % | 108.244 | 62.194 | 49.959 | 516.924 | 390 |

| PCP | SQM/person | 11.957 | 2.966 | 5.89 | 21.049 | 390 |

| FSS | % | 44.703 | 17.633 | 12.113 | 92.291 | 390 |

| Threshold Type | (1) | (2) | (3) | (4) | |

|---|---|---|---|---|---|

| SO2 | NO2 | GSO2 | GNO2 | ||

| Estimator of PGDP threshold | Single threshold | 3.116 | 3.116 | 1.782 | 3.116 |

| Double threshold | 3.116 | 3.056 | 1.759 | 3.116 | |

| 8.689 | 4.476 | 3.056 | 0.958 | ||

| Triple threshold | 2.019 | 6.349 | 0.958 | 8.688 | |

| F test of UR threshold effect | Single threshold | 49.07 *** | 37.33 ** | 120.97 * | 26.31 * |

| Double threshold | 21.88 | 9.91 | 42.85 * | 28.93 * | |

| Triple threshold | 9.52 | 9.78 | 42.98 | 8.01 | |

| p value | Single threshold | (0.010) | (0.050) | (0.000) | (0.087) |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| SO2 | SO2 | NO2 | NO2 | GSO2 | GSO2 | GNO2 | GNO2 | |

| BET (PGDP ≤ δ) | −1.082 ** | −0.840 ** | −0.559 * | −0.614 ** | −1.863 *** | −1.568 ** | −2.450 *** | −1.982 *** |

| (0.007) | (0.041) | (0.051) | (0.043) | (0.001) | (0.002) | (0.000) | (0.000) | |

| BET (PGDP > δ) | −2.125 *** | −1.832 *** | −1.204 *** | −1.259 *** | −4.603 *** | −3.248 *** | −3.241 *** | −2.741 *** |

| (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | |

| TIUP | −4.012 *** | −3.813 *** | −3.291 *** | −3.251 *** | 1.151 ** | 1.494 ** | −0.445 | −0.465 |

| (0.000) | (0.000) | (0.000) | (0.000) | (0.048) | (0.004) | (0.346) | (0.321) | |

| PGDP | 3.581 ** | 4.971 ** | 7.872 *** | 7.382 *** | −12.684 *** | −4.505 * | −0.877 | 2.822 |

| (0.043) | (0.013) | (0.000) | (0.000) | (0.000) | (0.060) | (0.648) | (0.209) | |

| ISU | −0.281 *** | −0.234 *** | −0.255 *** | −0.249 *** | −0.255 *** | −0.156 ** | −0.227 *** | −0.202 *** |

| (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | (0.001) | (0.000) | (0.000) | |

| PCP | −2.608 *** | 0.097 | −9.036 *** | −2.938 *** | ||||

| (0.000) | (0.850) | (0.000) | (0.000) | |||||

| FSS | 0.776 *** | 0.146 | 0.529 ** | 0.118 | ||||

| (0.001) | (0.372) | (0.046) | (0.621) | |||||

| cons | 104.657 *** | 86.004 *** | 62.662 *** | 57.030 *** | 193.789 *** | 215.678 *** | 113.341 *** | 118.915 *** |

| (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | |

| N | 390.000 | 390.000 | 390.000 | 390.000 | 390.000 | 390.000 | 390.000 | 390.000 |

| R2 | 0.536 | 0.565 | 0.454 | 0.452 | 0.629 | 0.711 | 0.382 | 0.405 |

| F | 96.478 | 77.355 | 71.404 | 50.955 | 138.744 | 141.782 | 54.946 | 42.922 |

| SO2 | NO2 | |||||||

|---|---|---|---|---|---|---|---|---|

| c | ab | ab/c | c | ab | ab/c | |||

| BET | −3.188 ** | −1.403 ** | ||||||

| (0.001) | (0.018) | |||||||

| TIUP | −0.389 *** | −2.799 *** | 0.122 | −0.238 *** | −1.165 *** | 0.170 | ||

| (0.000) | (0.000) | (0.007) | (0.002) | |||||

| PGDP | −1.892 *** | −1.296 ** | 0.593 | −0.152 *** | −1.251 ** | 0.108 | ||

| (0.000) | (0.028) | (0.004) | (0.000) | |||||

| ISU | −1.130 *** | −2.057 *** | 0.354 | −0.911 *** | −0.493 | 0.649 | ||

| (0.000) | (0.000) | (0.000) | (0.280) | |||||

| GSO2 | GNO2 | |||||||

|---|---|---|---|---|---|---|---|---|

| c | ab | ab/c | c | ab | ab/c | |||

| BET | −7.858 *** | −4.328 *** | ||||||

| (0.000) | (0.000) | |||||||

| TIUP | −0.245 ** | −7.613 *** | 0.031 | −0.155 ** | −4.173 *** | 0.036 | ||

| (0.011) | (0.000) | (0.011) | (0.000) | |||||

| PGDP | −2.434 *** | −5.424 *** | 0.310 | −1.112 *** | −3.216 *** | 0.257 | ||

| (0.000) | (0.000) | (0.000) | (0.000) | |||||

| ISU | −1.172 *** | −6.687 *** | 0.149 | −0.752 *** | −3.576 *** | 0.174 | ||

| (0.000) | (0.000) | (0.000) | (0.000) | |||||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Liu, W.; Liu, T. Exploring the Impact and Path of Environmental Protection Tax on Different Air Pollutant Emissions. Int. J. Environ. Res. Public Health 2022, 19, 4767. https://doi.org/10.3390/ijerph19084767

Liu W, Liu T. Exploring the Impact and Path of Environmental Protection Tax on Different Air Pollutant Emissions. International Journal of Environmental Research and Public Health. 2022; 19(8):4767. https://doi.org/10.3390/ijerph19084767

Chicago/Turabian StyleLiu, Weijiang, and Tingting Liu. 2022. "Exploring the Impact and Path of Environmental Protection Tax on Different Air Pollutant Emissions" International Journal of Environmental Research and Public Health 19, no. 8: 4767. https://doi.org/10.3390/ijerph19084767

APA StyleLiu, W., & Liu, T. (2022). Exploring the Impact and Path of Environmental Protection Tax on Different Air Pollutant Emissions. International Journal of Environmental Research and Public Health, 19(8), 4767. https://doi.org/10.3390/ijerph19084767